Market Overview

| Study Period | 2020 - 2031 |

|---|---|

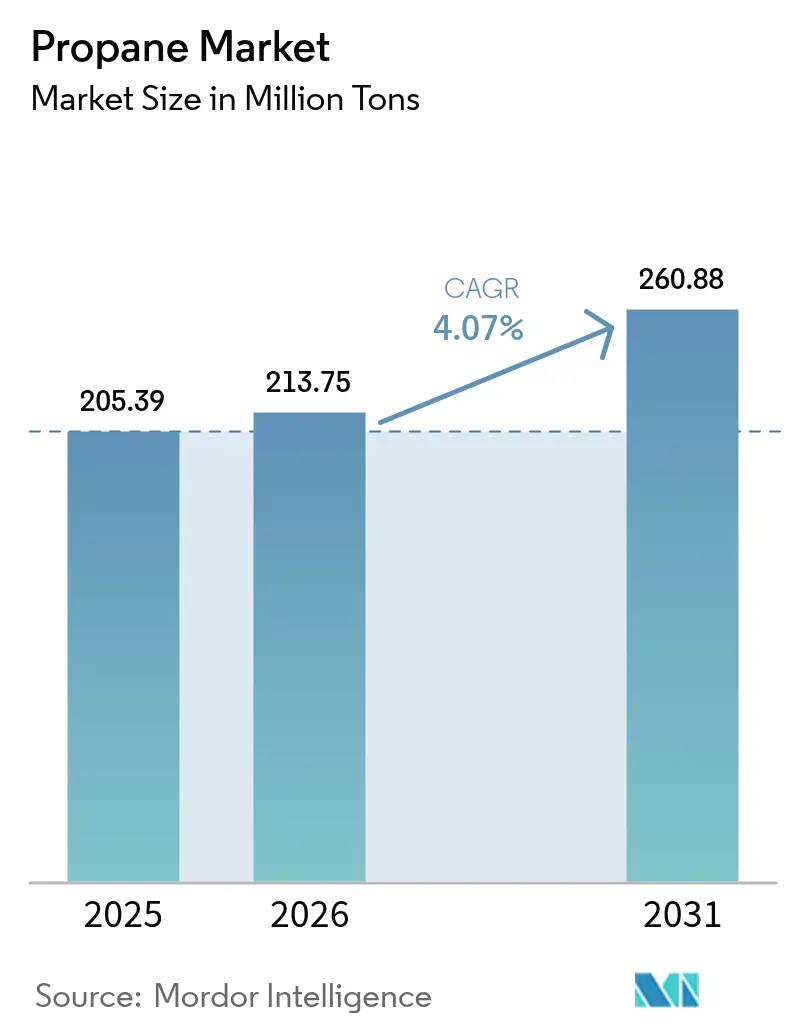

| Market Volume (2026) | 213.75 Million tons |

| Market Volume (2031) | 260.88 Million tons |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Propane Market Analysis by Mordor Intelligence

The Propane Market size is expected to grow from 205.39 Million tons in 2025 to 213.75 Million tons in 2026 and is forecast to reach 260.88 Million tons by 2031 at 4.07% CAGR over 2026-2031. Demand is benefiting from propane’s comparatively low carbon intensity, its cost advantage over electricity in many rural and suburban locations, and its growing role as a petrochemical feedstock. Cylinder distribution, expanding last-mile networks, and safety upgrades are broadening access across emerging economies, while bio-propane investment is accelerating as producers target sharp life-cycle emission cuts. Autogas programs, tax credits for low-emission fuels, and school-bus fleet conversions are enlarging transportation demand, whereas resilient agricultural consumption continues to underpin seasonal offtake. On the supply side, robust natural-gas liquids production in North America and new propane dehydrogenation (PDH) capacity in Asia are anchoring liquidity, even as spot NGL price swings challenge independent marketers.

Key Report Takeaways

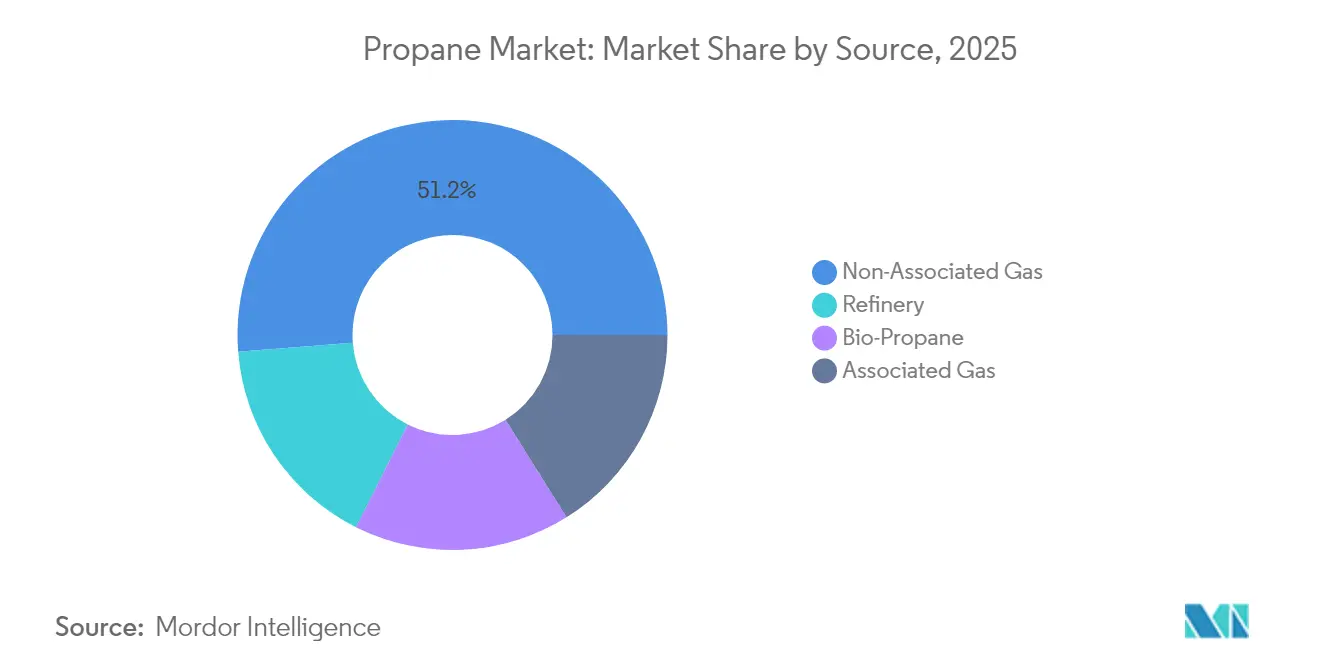

- By source, non-associated gas held 51.25% of the propane market share in 2025, while bio-propane is forecast to expand at a 8.75% CAGR through 2031.

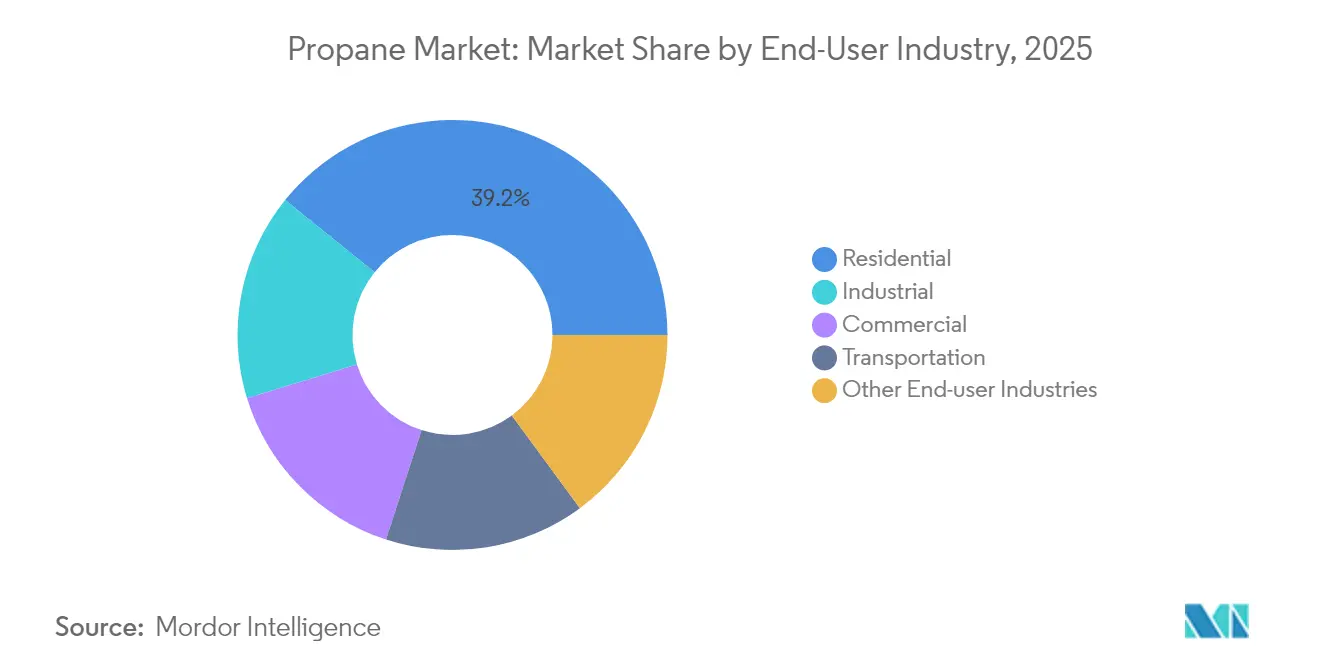

- By end-user, residential applications led with accounted for 39.20% revenue of propane market share in 2025; while industrial demand is projected to grow at a 5.08% CAGR to 2031.

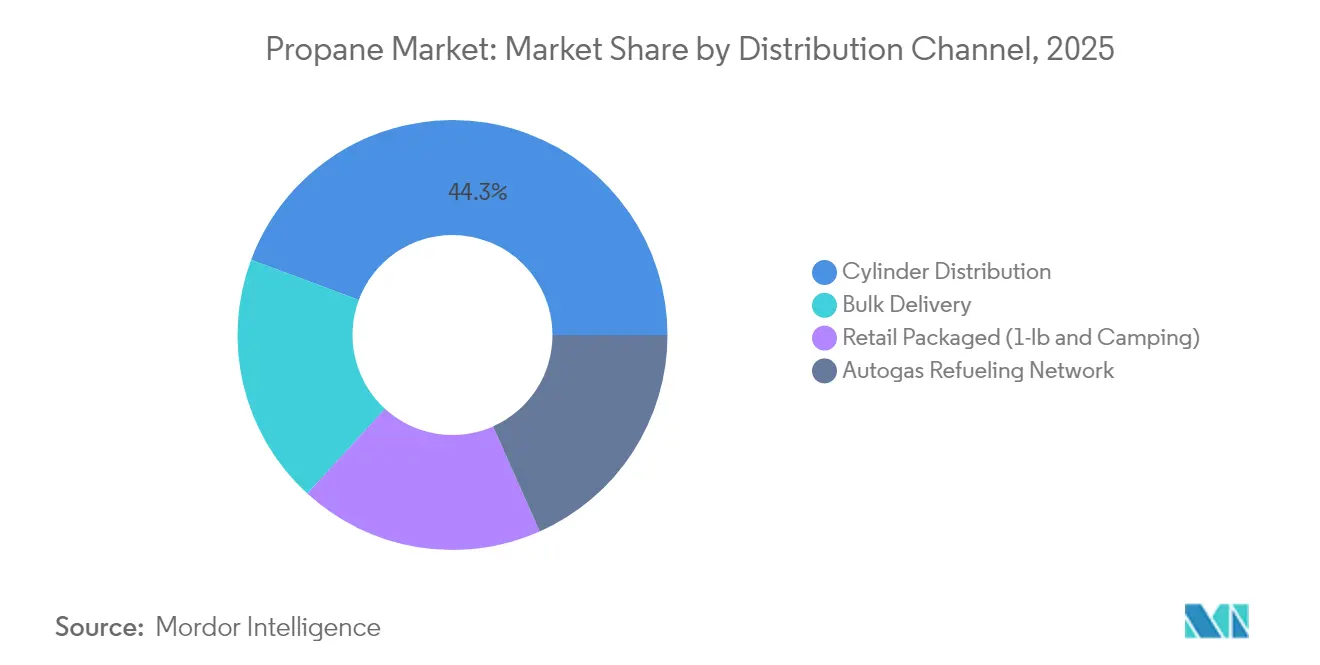

- By distribution channel, cylinder distribution commanded 44.30% of the propane market size in 2025 and is advancing at a 6.2% CAGR.

- By geography, Asia Pacific captured 40.75% of the propane market share in 2025 and is set to record the highest regional CAGR of 5.98% toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Propane Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Demand from the Residential Sectors | +1.20% | North America, Europe | Medium term (2-4 years) |

| Demand in the Petrochemical Industry | +1.50% | China, South Korea | Short term (≤2 years) |

| Government-Mandated Bio-Propane Blending Targets in the Europe Transport Sector (Europe) | +0.80% | Europe, North America | Medium term (2-4 years) |

| Rising Demand in Agriculture | +0.60% | Midwest US | Short term (≤2 years) |

| Increase in Demand from the Transportation Sector | +0.70% | Global, with concentration in North America and Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Residential demand resilience despite electrification push

Lower-carbon heating mandates did not erode core residential consumption, which accounted for 40% of global offtake in 2024. Natural-gas or propane-heated homes in the United States saved an average of USD 1,132 a year relative to all-electric dwellings, reinforcing propane’s cost proposition[1]American Gas Association, “2025 Winter Outlook,” aga.org . Rural dependence is pronounced, with more than 24 million US households relying on propane, especially across the Midwest. Although Massachusetts ended most equipment rebates in 2024, incentives for high-efficiency units remained for low-income residents, signalling policy pragmatism. Retail prices softened nationwide—averaging USD 2.475 per gallon in May 2024—helping maintain demand. These dynamics are expected to uphold moderate growth in mature markets even as heat-pump adoption rises.

Industrial applications driving higher growth rates

Industrial uptake is outpacing overall growth in the propane industry, advancing at a 5.25% CAGR as petrochemical producers add dedicated PDH plants to convert propane into propylene. New Asian projects accelerated propylene output in 2024, narrowing spreads yet widening propane throughput. Sustainability targets are prompting operators to trial carbon-capture solutions and renewable-propane blending to curb Scope 1 emissions without compromising process efficiency. The combination of feedstock reliability and de-risked decarbonization paths positions industry demand as a durable growth pillar across the forecast horizon.

Bio-propane: transformative growth amid decarbonization

Bio-propane, chemically identical to its fossil counterpart yet offering 70-80% lower life-cycle emissions, ranks as the fastest-growing source in the propane industry at a 9.20% CAGR. European industry projections show renewable LPG meeting continental demand entirely by 2050, equating to 8-12 million tons of annual renewable propane requirements. US output is on track to triple by 2025 as SAF producers generate renewable propane co-products. Pinnacle Propane’s Texas program already retails blends up to 100% renewable content, cutting greenhouse-gas emissions by as much as 80%. Funding from the US Department of Energy for high-impact R&D is set to enlarge the commercial pipeline, bolstering supply security[2]US Department of Energy, “High-Impact RD&D Funding Opportunity,” energy.gov .

Transportation sector: autogas expansion despite EV competition

Medium-duty fleet operators and school districts are pivoting to propane Autogas in the propane industry, which delivers a 52% greenhouse-gas reduction versus grid-charged electric equivalents on a well-to-wheel basis. A new federal tax credit for low-emission transportation fuels effective January 2025 is expected to accelerate adoption. The NPGA has formed a Renewable Fuels Committee to lobby for supportive legislation, highlighting the industry’s strategic focus on transportation diversification[3]National Propane Gas Association, “Policy Priorities 2025,” npga.org . Faster refuelling, extended range, and low station-build costs underpin the competitive case, especially for route-based assets that cannot accommodate long charge dwell times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Harmful Effects of Propane at Higher Concentrations | -0.30% | Global | Long term (≥ 4 years) |

| Spot NGL Price Volatility Compressing Margins for Independent Marketers (Global) | -0.80% | North America | Short term (≤2 years) |

| Storage and Safety Risks | -0.40% | Densely populated regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Spot NGL price volatility

Propane prices remain sensitive to crude-oil swings and inventory cycles , compressing marketing margins for independent distributors. The Conway Index illustrates Midwest price dips during bumper shale output, followed by sharp spikes in high-demand winters, complicating hedging strategies. Volatility discourages capital investment in storage infrastructure among smaller firms and can slow autogas station roll-outs, marginally tempering near-term expansion in the propane industry.

Storage and safety risks

Although propane has an established safety record, industrial incidents highlight the hazard of leaks in congested urban settings Regulators in Europe and Asia are tightening tank-inspection and valve-integrity standards, raising compliance costs for distributors. Public-sector tender specifications now increasingly require remote telemetry and emergency-shutoff systems, adding capital intensity to fleet renewal. While technology mitigates most operational risk, perception challenges can slow permitting for new bulk sites in high-density areas in the propane industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Non-Associated Gas Holds the Lead While Bio-Propane Accelerates

Non-associated gas yielded 51.25% of global supply in 2025, anchored by prolific shale development and midstream build-outs. The United States alone produced 3.0 million barrels per day of NGLs—including propane—in 2025, up 10% on the previous year. Incremental cryogenic processing in the Permian Basin and Appalachian region secured feedstock continuity, ensuring a stable base for the propane market. Refinery and associated-gas streams provided complementary volumes but grew more slowly, constrained by refinery utilization ceilings and flaring-reduction initiatives.

Bio-propane’s 8.75% CAGR underscores its pivotal role in the energy-transition narrative. Capacity expansions at dedicated hydrotreated-vegetable-oil (HVO) units and co-processing lines are set to lift global renewable-propane output from 19,000 barrels per day in 2023 to 51,000 barrels per day by 2025. Developing economies in Southeast Asia and Latin America are also piloting waste-oil pathways, broadening geographic supply diversity. As renewable certification schemes mature, traders expect price premiums to compress, fostering mainstream uptake across residential blends and industrial furnaces.

By End-User Industry: Residential Remains Core While Industrial Momentum Builds

The residential segment retained 39.20% of 2025 volumes in the propane industry, benefiting from propane’s versatility for space heating, cooking, and water-heating tasks in off-grid locales. Heating-oil conversions and expanding rural electrification only partly erode this base, since propane appliances generally exhibit lower upfront and lifecycle costs than full electric retrofits for older housing stock. Government efficiency standards are encouraging the replacement of legacy vent-free heaters with high-efficiency condensing furnaces, anchoring replacement demand.

Industrial demand, forecast to rise at 5.08% annually, draws strength from the strong polypropylene outlook in automotive and consumer-goods applications. Asian petrochemical giants are commissioning multiple single-train complexes, leveraging propane-based PDH routes to mitigate feedstock risks associated with naphtha. Emerging low-carbon incentives, such as the EU Innovation Fund, may further stimulate industrial users to shift toward propane blended with renewable fractions to balance emission inventories.

By Distribution Channel: Cylinder Distribution Leads Both Share and Growth

Cylinder distribution represented 44.30% of global offtake in 2025 and is projected to log a 6.2% CAGR through 2031 in the propane market, reflecting convenience and portability in household, commercial, and leisure settings. Smart metering solutions that transmit fill-level data are reducing run-outs and route-planning costs, improving service reliability for millions of small-volume customers. Governments in India and Indonesia continue rolling out subsidized cylinder programs to replace biomass cooking, fuelling volume additions.

Bulk delivery retains a firm foothold among industrial plants, grain dryers, and large hospitality venues in the propane market, where tank telemetry and digitized truck dispatching are squeezing logistics costs. The global autogas network, exceeding 80,000 stations in 2025, increasingly embeds propane distribution operators within multimodal energy-retail ecosystems, diversifying their revenue. Retail packaged mini-cylinders for outdoor recreation hold stable demand profiles, supported by e-commerce supply chains that simplify product replenishment for end users.

Geography Analysis

Asia Pacific anchored 40.75% of propane market volumes in 2025 and is forecast to expand at a 5.98% CAGR to 2031, buoyed by industrialization, population growth, and supportive LPG adoption schemes. Chinese consumption climbed to 73.9 million tons in 2022 and continues to climb as PDH capacity ramps to satisfy polypropylene demand in automotive interiors and consumer packaging. India’s Pradhan Mantri Ujjwala Yojana keeps rural cylinder penetration rising, aiding household fuel switching. Canadian exporter AltaGas plans to double Ridley Island propane export throughput by 2026, underscoring the supply-chain link between North America and Asian buyers.

North America retains a substantial production and export surplus. US shipments reached 1.8 million barrels per day in 2024, marking the 17th consecutive annual increase. Ample shale gas liquids and expanding Gulf Coast dock capacity ensure reliable feedstock for global customers. Domestic demand growth is steadier, with residential heating plateauing but autogas and renewable-propane blending providing incremental lift.

Europe confronts mature demand in traditional heating uses but posts vigorous momentum in renewable-propane blending. The Renewable Energy Directive III and fit-for-55 packages incentivize suppliers to decarbonize bulk portfolios and aviation-fuel coproduct streams. Infrastructure repurposing to handle blended molecules positions the region for a gradual supply-mix transition through 2030.

The Middle East and Africa leverage abundant associated-gas streams to feed growing domestic petrochemical ambitions in the propane market, while South America’s market progresses steadily on the back of Brazil’s cylinder program expansions and Argentina’s agricultural drying needs.

Competitive Landscape

Major integrated energy companies—including Saudi Arabian Oil Co., ExxonMobil, Shell, Chevron, and BP—dominate upstream production and long-term offtake contracts in the propane industry. Portfolio resilience is enhanced by vertical integration into shipping, storage, and trading arms that manage pricing risk and capture arbitrage flows. These firms are allocating growing capital to renewable-propane and circular-economy projects; BP alone invested over USD 500 million in bio-LPG and renewable natural gas ventures by early 2025.

Strategic partnerships have multiplied over the past two years, illustrating that even large players seek collaborative models to secure feedstock or expand market presence. Suburban Propane Partners’ USD 53 million acquisition of regional marketers in New Mexico and Arizona in February 2025 enlarged its service footprint across the US Southwest. Independent distributors, while nimble, face margin compression from NGL volatility, prompting a wave of technology adoption to boost route efficiency and customer stickiness.

Digital capability is now a key battleground in the propane market. The Propane Education & Research Council logged 165,000 hours of online workforce training in 2024, evidencing sector-wide upskilling to operate smart tanks, data-driven dispatch, and safety platforms. AI-enabled customer portals are enhancing reorder accuracy and predictive maintenance, sharpening competitive differentiation among top-tier marketers.

Propane Industry Leaders

Saudi Arabian Oil Co.

Exxon Mobil Corporation

Shell PLC

Chevron Corporation

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Suburban Propane Partners announced the USD 53 million acquisition of retail propane assets in New Mexico and Arizona. The move enlarges its footprint in a region benefiting from population growth and commercial construction activity.

- May 2024: AltaGas confirmed an expansion of propane export capacity at its British Columbia terminal, aiming to satisfy rising Asian demand. The project’s modular design will enable phased construction and may shorten time-to-market compared with conventional builds.

Global Propane Market Report Scope

Propane is a flammable hydrocarbon gas liquefied through pressurization and is commonly used as fuel for heating, cooking, hot water, and vehicles. The propane market is segmented by end-user industry and geography. By end-user industry, the market is segmented into residential, commercial, transportation, industrial, and other end-user industries. The report also covers the size and forecasts for the market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (kiloton).

By Source

| Refinery |

| Associated Gas |

| Non-Associated Gas |

| Bio-Propane |

By End-user Industry

| Residential |

| Commercial |

| Industrial |

| Transportation |

| Other End-user Industries |

By Distribution Channel

| Bulk Delivery |

| Cylinder Distribution |

| Autogas Refueling Network |

| Retail Packaged (1-lb and Camping) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Source | Refinery | |

| Associated Gas | ||

| Non-Associated Gas | ||

| Bio-Propane | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial | ||

| Transportation | ||

| Other End-user Industries | ||

| By Distribution Channel | Bulk Delivery | |

| Cylinder Distribution | ||

| Autogas Refueling Network | ||

| Retail Packaged (1-lb and Camping) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global propane market?

The propane market is valued at 213.75 million tons in 2026 and is forecast to climb to 260.88 million tons by 2031.

Which region leads the propane market, and how fast is it growing?

Asia Pacific held a 40.75% share in 2025 and is projected to expand at a 5.98% CAGR through 2031.

Why is bio-propane gaining attention?

Bio-propane delivers 70-80% lower life-cycle emissions than fossil propane, and its output is expected to triple in the United States by 2025.

What role does propane play in transportation decarbonization?

Propane autogas cuts greenhouse-gas emissions by 52% compared to grid-charged electric vehicles for certain fleet duty cycles and benefits from new US tax credits starting in 2025.

Which distribution channel in the propane market is growing the fastest?

Cylinder distribution leads both share and growth, holding 44.30% of 2025 volumes and posting a 6.2% CAGR outlook thanks to expanding last-mile delivery networks.

Page last updated on: