Asia-Pacific Industrial Gases Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

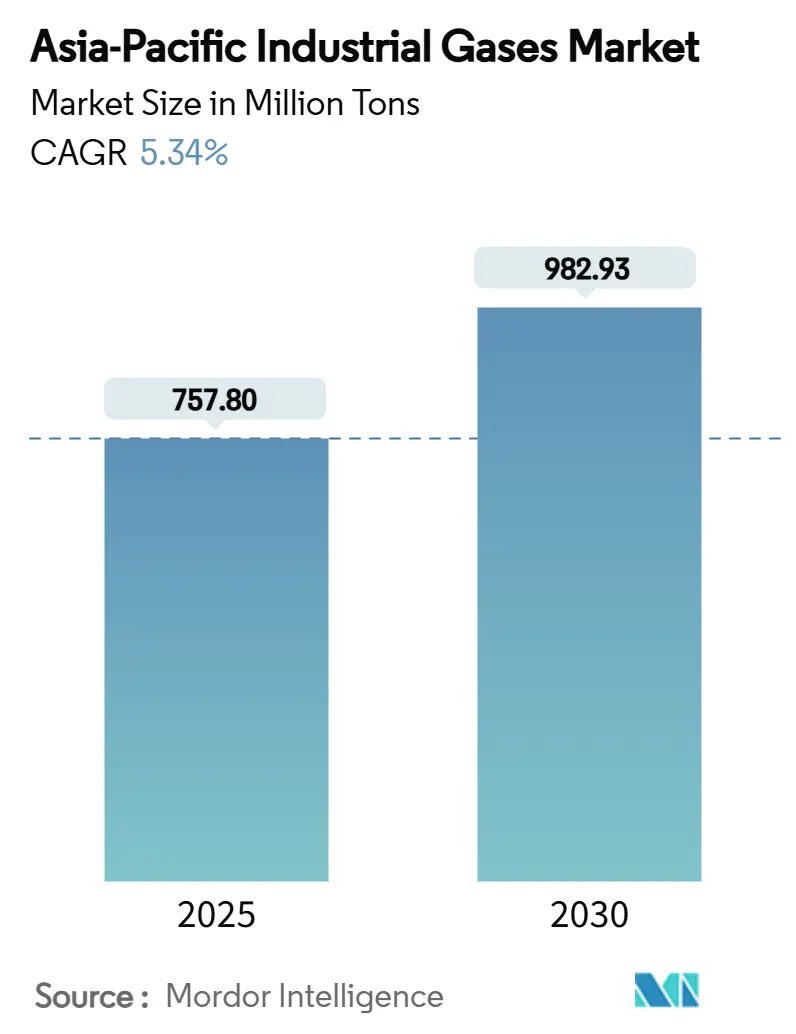

| Market Volume (2025) | 757.80 Million tons |

| Market Volume (2030) | 982.93 Million tons |

| Growth Rate (2025 - 2030) | 5.34% CAGR |

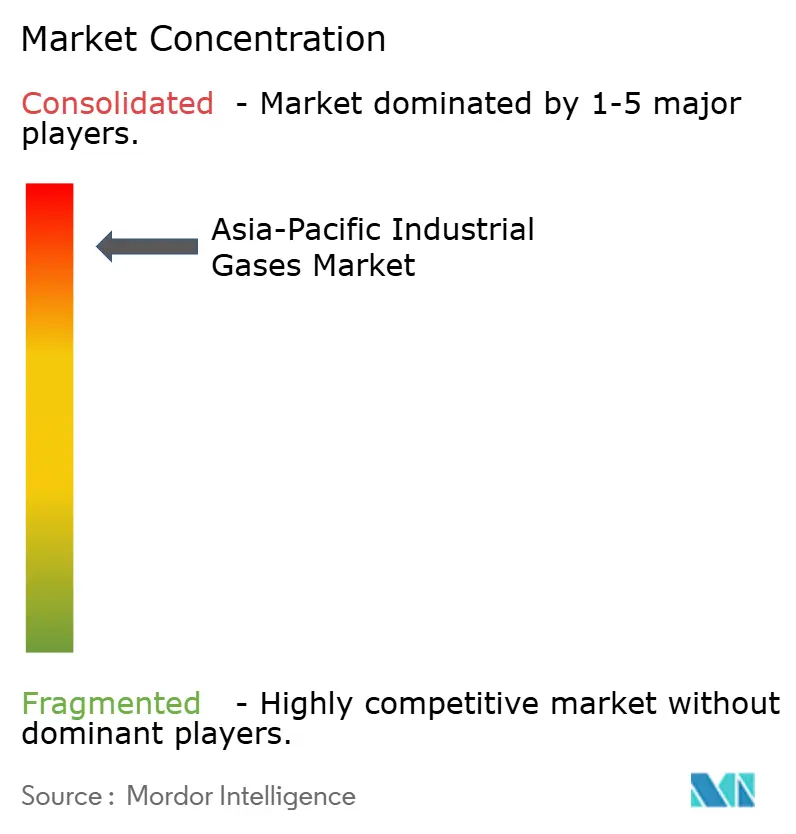

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Industrial Gases Market Analysis by Mordor Intelligence

The Asia-Pacific Industrial Gases Market size is estimated at 757.80 Million tons in 2025, and is expected to reach 982.93 Million tons by 2030, at a CAGR of 5.34% during the forecast period (2025-2030). This solid growth reflects persistent capacity additions in semiconductor fabrication, the scaling-up of green hydrogen projects, and resilient consumption from chemical processing, energy generation, and food preservation. Oxygen retains volume leadership thanks to steelmaking and medical demand, while nitrogen enjoys the fastest uptick because electronics assemblers and cold-chain operators require inert and cryogenic atmospheres. China continues to anchor regional volumes, yet India’s rapid industrialization, supportive natural-gas policies, and high-growth manufacturing sectors are reshaping demand patterns. Parallel government decarbonization programs and corporate net-zero targets spur investment in low-carbon hydrogen, large air-separation units, and carbon-capture solutions, amplifying long-term opportunities for suppliers across the Asia-Pacific industrial gases market.

Key Report Takeaways

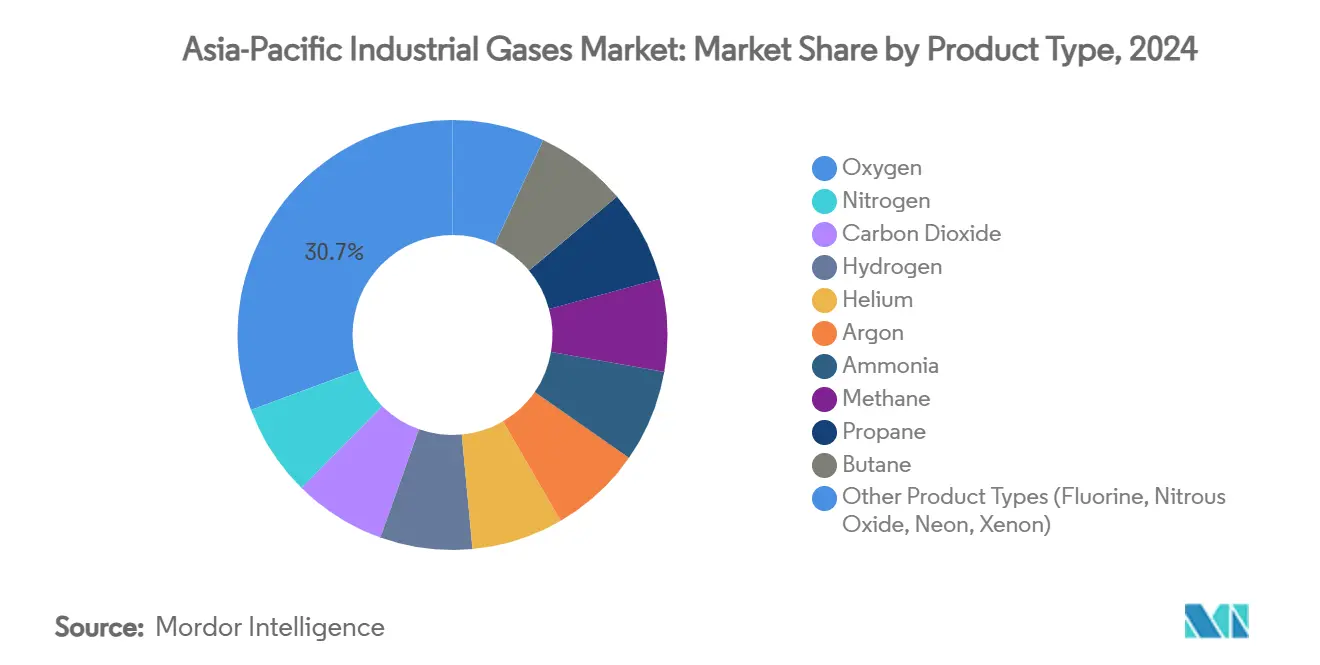

- By product type, oxygen held 30.67% of the Asia-Pacific industrial gases market share in 2024; nitrogen is on track to expand at a 5.71% CAGR through 2030.

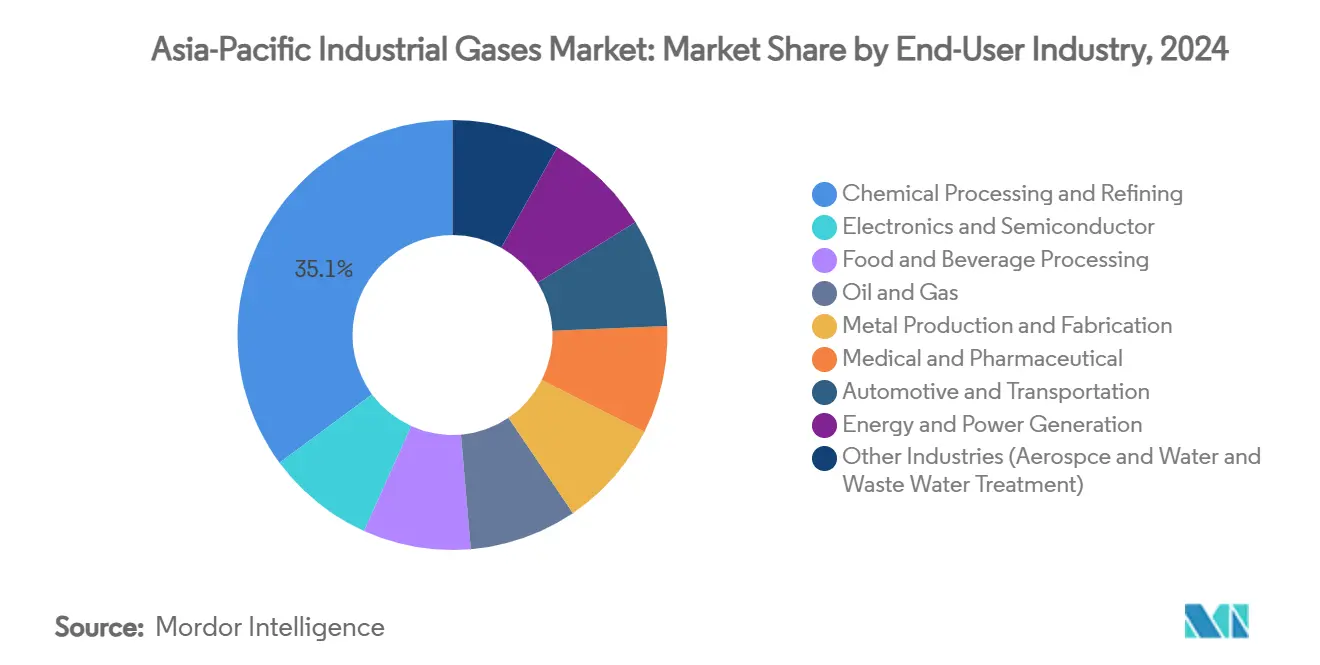

- By end-user industry, chemical processing and refining accounted for 35.14% of the Asia-Pacific industrial gases market size in 2024, whereas energy and power generation is forecast to post a 6.85% CAGR up to 2030.

- By geography, China dominated with 45.56% of the Asia-Pacific industrial gases market share in 2024, while India is set to register a 7.78% CAGR to 2030.

Asia-Pacific Industrial Gases Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for frozen & stored food | +0.80% | Global, with concentration in China, India, Japan | Medium term (2-4 years) |

| Growing need for alternate energy sources (green H₂, LNG) | +1.20% | APAC core, Australia leading hydrogen exports | Long term (≥ 4 years) |

| Semiconductor & electronics manufacturing boom | +1.50% | Taiwan, South Korea, China, Singapore | Short term (≤ 2 years) |

| Govt-led industrial decarbonization clusters | +0.90% | China, Japan, South Korea, Australia | Long term (≥ 4 years) |

| Expansion of small-scale LNG & coal-gasification projects | +0.70% | Southeast Asia, India, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Frozen & Stored Food

Accelerated urbanization and rising disposable incomes heighten the appeal of convenience meals across emerging Asian markets, putting pressure on processors to expand cold-chain capacity. Liquid-nitrogen quick-freezing technology, such as Air Products’ Freshline IQF+ tunnel, maintains product texture by curbing ice-crystal growth and delivers lower environmental impact than high-GWP refrigerants. The International Institute of Refrigeration confirms nitrogen’s chemical inertness allows direct contact with food without taste alteration[1]“Cryogenic Nitrogen in the Food and Beverage Industry,” International Institute of Refrigeration, iifiir.org . Although operating costs remain above those of mechanical refrigeration, premium frozen products and plant-based alternatives justify adoption, sustaining additional nitrogen volumes for the Asia-Pacific industrial gases market. Growing e-commerce grocery channels further reinforce demand for temperature-controlled logistics networks that heavily rely on cryogenic gases.

Growing Need for Alternate Energy Sources (Green H₂, LNG)

Australia’s USD 10 billion Green Springs venture headlines a pipeline of electrolysis initiatives targeting 10 GW of solar-powered hydrogen by 2030. The latest IEA Global Hydrogen Review shows announced electrolyser capacity of 20 GW worldwide, with China out in front[2]“Global Hydrogen Review 2024,” International Energy Agency, iea.org . ASEAN forecasts indicate delivered hydrogen costs could decline to USD 2.7–4.3 per kg by 2050, unlocking incremental gas transport, compression, and liquefaction volumes. In parallel, Asia consumes 45% of the incremental global LNG demand recorded in 2024, with India aiming for a 15% gas share in its energy mix by 2030. The combined hydrogen-and-LNG build-out injects durable growth momentum into the Asia-Pacific industrial gases market.

Semiconductor & Electronics Manufacturing Boom

Asia’s leadership in chip fabrication drives surging uptake of ultra-high-purity helium, nitrogen, argon, and tailored etch gases. Spot helium prices jumped more than 40% between 2020 and 2022 on the back of tightened supply, squeezing margins for Samsung and other Korean foundries. Linde LienHwa’s long-term supply contract for Taiwan’s new advanced-node campus underscores how gas vendors lock in multi-year volumes through on-site plants. Air Liquide’s Naoshima Island ASU will add 1,400 tons per day of oxygen and specialty neon to support domestic lithography demand. Rapid AI-chip capacity expansion multiplies throughput requirements for process gases, firmly anchoring electronics as a structural growth pillar for the Asia-Pacific industrial gases market.

Expansion of Small-Scale LNG & Coal-Gasification Projects

Indonesia’s Tangguh UCC project, now sanctioned at USD 7 billion, will deploy carbon-capture and utilization to monetize 3 trillion cubic feet of additional gas reserves, illustrating the pivot toward lower-emission LNG supply. New regasification terminals slated for the Philippines and Vietnam extend demand nodes for industrial-grade nitrogen and LNG vaporization gases. China continues to back coal-gasification in integrated refining complexes that swing between fuels and petrochemical feedstocks, keeping oxygen demand buoyant. Nonetheless, rapidly falling solar-PV costs challenge the longer-term LNG outlook, implying suppliers must balance near-term build-outs with potential renewable displacement risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental regulations & safety issues | -0.60% | Global, stricter enforcement in developed APAC markets | Medium term (2-4 years) |

| High energy cost of gas separation & liquefaction | -0.90% | Australia, Japan, South Korea facing highest energy costs | Short term (≤ 2 years) |

| Helium global supply-chain volatility | -0.40% | Global, acute impact on South Korea, Taiwan semiconductor hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Regulations & Safety Issues

Australia’s stricter Ozone Protection amendments and Singapore’s new persistent-chemical rules oblige producers to upgrade leak detection, licensing, and training protocols, driving up compliance costs. The Asian Development Bank notes that Asia still emits over 50% of global greenhouse gases, catalyzing tougher carbon accounting and reporting mandates. Alignment with global disclosure frameworks such as the International Sustainability Standards Board demands granular energy and emissions data, placing smaller operators at risk of non-compliance. While these requirements lift production expenses, they simultaneously stimulate demand for low-carbon hydrogen, carbon-capture solutions, and high-efficiency air-separation equipment—opportunities the Asia-Pacific industrial gases market can capture.

High Energy Cost of Gas Separation & Liquefaction

Wholesale electricity prices in Australia have tripled since 2022, and spot gas quotes have quadrupled, triggering cost anxiety for energy-intensive air-separation facilities. Orica and other heavy users have warned that sustained cost inflation could force production curtailments, undercutting domestic oxygen and nitrogen supply. Nippon Sanso Holdings cites electricity tariffs as a primary factor suppressing operating margins in 2024. Although next-generation fast-start ASUs and novel oxy-fuel cycles promise higher efficiency, capital requirements may delay wide deployment, flattening near-term profitability in the Asia-Pacific industrial gases market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oxygen Dominance Amid Nitrogen’s Rapid Ascent

Oxygen captured 30.67% of the Asia-Pacific industrial gases market share in 2024, buoyed by steel output, medical usage, and oxidation reactions in petrochemicals. Linde logged a record 59 small on-site wins in 2024, most of them for oxygen and nitrogen supply to electronics and green steel plants. Nitrogen, the fastest-growing product, is forecast to rise at a 5.71% CAGR through 2030 as chipmakers, battery lines, and cold-chain operators expand capacity across India, Vietnam, and Malaysia.

Carbon dioxide maintains steady intake for beverage carbonation and enhanced oil recovery, while hydrogen accelerates through policy-backed electrolyser rollouts and refinery decarbonization. Argon serves welding and sputtering in metalworks and flat-panel displays. Specialty gases—neon, xenon, fluorine—command premium pricing and tighter purity specifications, prompting local production initiatives in Japan to cushion supply risk. Collectively, product diversification protects the Asia-Pacific industrial gases market from single-segment volatility and supports balanced growth.

By End-user Industry: Chemical Processing Leadership Challenged by Energy Sector Surge

Chemical processing and refining retained 35.14% of the Asia-Pacific industrial gases market size in 2024 as integrated complexes across China, Singapore, and South Korea consumed vast oxygen and hydrogen volumes for oxidation, hydrocracking, and desulfurization. Yet cracker margins tightened in Southeast Asia, nudging operators toward yield-maximization and CO₂-reduction strategies that still rely heavily on on-purpose hydrogen.

Energy and power generation will deliver the fastest growth at a 6.85% CAGR to 2030, propelled by LNG regasification, combined-cycle additions, and carbon-capture retrofits. Electronics ranks third; its double-digit uplift in ultra-pure helium, nitrogen, and specialty mixtures keeps it a strategic focus for suppliers keen on margin defense. Food and beverage, metals, medical, automotive, and water treatment continue to furnish diversified downstream pull, ensuring the Asia-Pacific industrial gases market remains resilient even when individual sectors soften.

Geography Analysis

China contributed 45.56% of the Asia-Pacific industrial gases market in 2024, underpinned by record 14.8 million barrels per day refining throughput and a push to raise gas-storage working capacity to up to 60 billion m³ by 2025. Air Liquide enlarged its footprint with a EUR 60 million ASU for Wanhua Chemical in Yantai, confirming ongoing heavy-industry appetite. Despite cyclical softness in construction, policy support for renewables, hydrogen, and carbon capture preserves long-term gas demand.

India, expanding at a 7.78% CAGR, targets a natural-gas share of 15% in its energy mix by 2030, with demand forecast to triple by 2050—80% of which will be industrial[3]“Industry to drive tripling of natural gas consumption in India by 2050,” U.S. Energy Information Administration, eia.gov . Linde’s de-captivation of two ASUs at Tata Steel in Odisha and Sojitz’s USD 400 million biomethane joint venture exemplify rising opportunities across steel, fertilizer, and sustainable fuels.

Japan and South Korea showcase advanced hydrogen ecosystems and value-added semiconductor clusters. Air Liquide’s Naoshima Island ASU supports copper refining and neon production, while ongoing helium shortages force fab operators to renegotiate multisource contracts. Indonesia, Vietnam, the Philippines, and Thailand leverage energy diversification, metals processing, and electronics assembly to widen the downstream customer base, ensuring healthy volumes for the Asia-Pacific industrial gases market.

Competitive Landscape

Global majors dominate a consolidated field in which capital intensity, on-site supply contracts, and technology depth erect high barriers to entry. Following its USD 33 billion Praxair merger, Linde booked a USD 10 billion project backlog and delivered an APAC operating margin above 30% in 2024. Air Liquide reported record margin improvement in 2024, channeling capital toward large-scale oxygen and hydrogen investments that meet stringent decarbonization targets.

Air Products streamlined its portfolio via a USD 1.81 billion LNG equipment sale to Honeywell to unlock headroom for world-scale hydrogen-ammonia ventures. Regional specialist Nippon Sanso Holdings continues to consolidate Southeast Asian distributors and invests in advanced ASUs geared toward electronics purity specs, leveraging deep client ties to shield share against global entrants.

Competition increasingly revolves around low-carbon solutions: liquid-hydrogen transport, high-efficiency cryogenic pumps, and digitally optimized ASUs. Providers that bundle engineering, purification, and process-integration services command premium pricing and longer contract tenures, reinforcing structural advantages in the Asia-Pacific industrial gases market.

Asia-Pacific Industrial Gases Industry Leaders

Air Liquide

Air Products and Chemicals Inc.

Linde plc

Nippon Sanso Holdings Corporation

Yingde Gas Shanghai

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Linde announced that it achieved a record number of new small on-site projects for nitrogen and oxygen supply for the fifth consecutive year. In 2024, the company signed 59 long-term agreements to build, own, and operate 64 plants at customer locations.

- February 2025: Air Liquide has started building a large-scale Air Separation Unit on Naoshima Island, Japan, to produce up to 1,400 tons of oxygen daily, along with nitrogen, argon, and neon for semiconductor manufacturing. Operations will begin in 2027, supported by financial grants from Japan's Ministry of Economy, Trade and Industry.

Asia-Pacific Industrial Gases Market Report Scope

Industrial gases are gases produced in relatively large quantities by gas manufacturing companies for use in various industrial manufacturing processes. These gases are sold to other enterprises and industries, including oil and gas, petrochemicals, chemicals, power, mining, steelmaking, metals, environmental protection, medicine, pharmaceuticals, biotechnology, food, water, fertilizers, nuclear power, and electronics.

The Asia-Pacific industrial gases market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into nitrogen, oxygen, carbon dioxide, hydrogen, helium, argon, ammonia, methane, propane, butane, and other types (fluorine and nitrous oxide). By end-user industry, the market is segmented into chemical processing and refining, electronics, food and beverage, oil and gas, metal manufacturing and fabrication, medical and pharmaceutical, automotive and transportation, energy and power, and other end-user industries (water treatment and environmental protection). The report also covers the market size and forecasts for the Asia-Pacific industrial gases market in five countries across the Asia-Pacific region.

For each segment, the market sizing and forecasts are provided on the basis of volume (tons).

| Nitrogen |

| Oxygen |

| Carbon Dioxide |

| Hydrogen |

| Helium |

| Argon |

| Ammonia |

| Methane |

| Propane |

| Butane |

| Other Product Types (Fluorine, Nitrous Oxide, Neon, Xenon) |

| Chemical Processing and Refining |

| Electronics and Semiconductor |

| Food and Beverage Processing |

| Oil and Gas |

| Metal Production and Fabrication |

| Medical and Pharmaceutical |

| Automotive and Transportation |

| Energy and Power Generation |

| Other Industries (Aerospce and Water and Waste Water Treatment) |

| China |

| India |

| Japan |

| South Korea |

| Indonesia |

| Thailand |

| Malaysia |

| Vietnam |

| Rest of Asia-Pacific |

| By Product Type | Nitrogen |

| Oxygen | |

| Carbon Dioxide | |

| Hydrogen | |

| Helium | |

| Argon | |

| Ammonia | |

| Methane | |

| Propane | |

| Butane | |

| Other Product Types (Fluorine, Nitrous Oxide, Neon, Xenon) | |

| By End-user Industry | Chemical Processing and Refining |

| Electronics and Semiconductor | |

| Food and Beverage Processing | |

| Oil and Gas | |

| Metal Production and Fabrication | |

| Medical and Pharmaceutical | |

| Automotive and Transportation | |

| Energy and Power Generation | |

| Other Industries (Aerospce and Water and Waste Water Treatment) | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size of the Asia-Pacific industrial gases market?

The market handles 757.80 million tons in 2025 and is projected to reach 982.93 million tons by 2030.

Which product leads regional demand?

Oxygen leads with 30.67% share in 2024, primarily serving steel, medical, and refining applications.

Why is nitrogen growing fastest?

Electronics manufacturing expansion and cold-chain upgrades push nitrogen volumes, supporting a forecast 5.71% CAGR through 2030.

Which end-user industry will expand most rapidly?

Energy and power generation shows the quickest rise at a 6.85% CAGR owing to LNG regasification and hydrogen projects.

How do government decarbonization policies affect suppliers?

Policies that mandate hydrogen, carbon capture, and strategic gas storage create concentrated demand hubs, underpinning long-term investments in large air-separation and liquefaction assets.

Page last updated on: