Hydrogen Gas Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

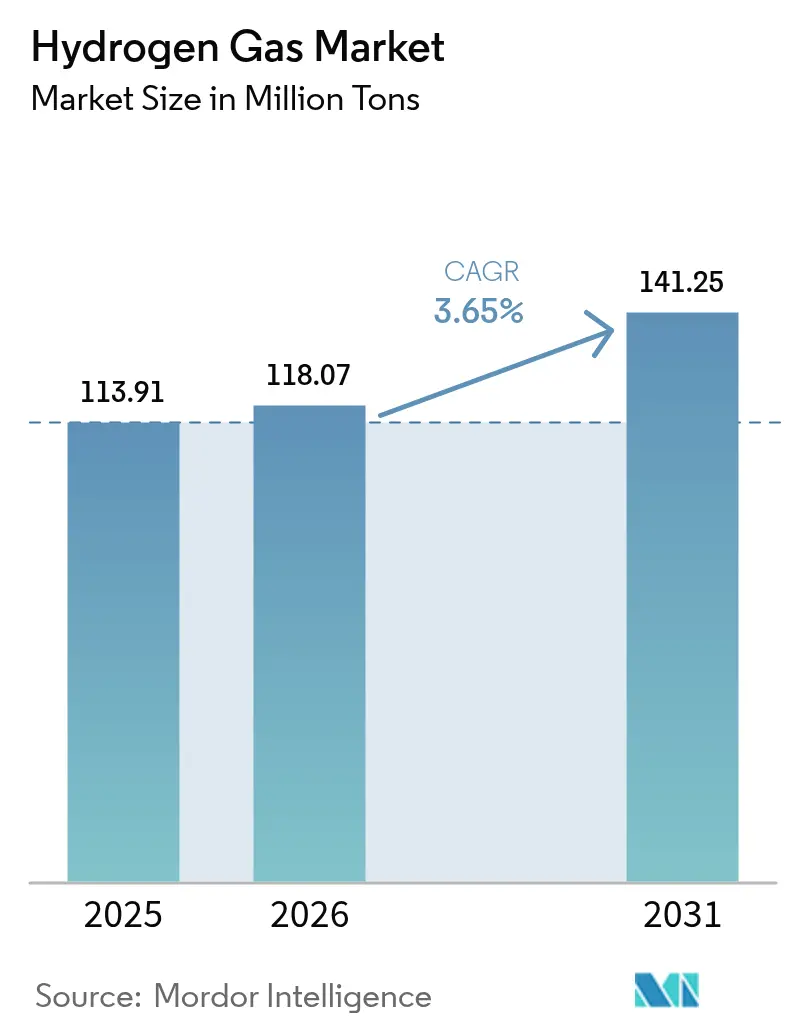

| Market Volume (2026) | 118.07 Million tons |

| Market Volume (2031) | 141.25 Million tons |

| Growth Rate (2026 - 2031) | 3.65% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrogen Gas Market Analysis by Mordor Intelligence

The Hydrogen Gas Market size was valued at 113.91 Million tons in 2025 and is estimated to grow from 118.07 Million tons in 2026 to reach 141.25 Million tons by 2031, at a CAGR of 3.65% during the forecast period (2026-2031). Tightening sulfur limits, mounting green-hydrogen incentives, and early commercial deployment of fuel-cell vehicles are reshaping the competitive landscape even though grey hydrogen still dominates installed capacity. Pipeline networks that serve refineries and fertilizer complexes anchor current volumes, but falling electrolyzer costs are unlocking distributed production near steel mills and mobility hubs. Asia-Pacific keeps the largest regional share, yet the Middle East and Africa post the highest growth as export-oriented megaprojects integrate low-cost solar with desalination. Meanwhile, fuel-cell trucks and buses move beyond pilots, supported by public-refueling corridors and OEM production commitments, which lift long-run demand visibility despite storage and transport bottlenecks.

Key Report Takeaways

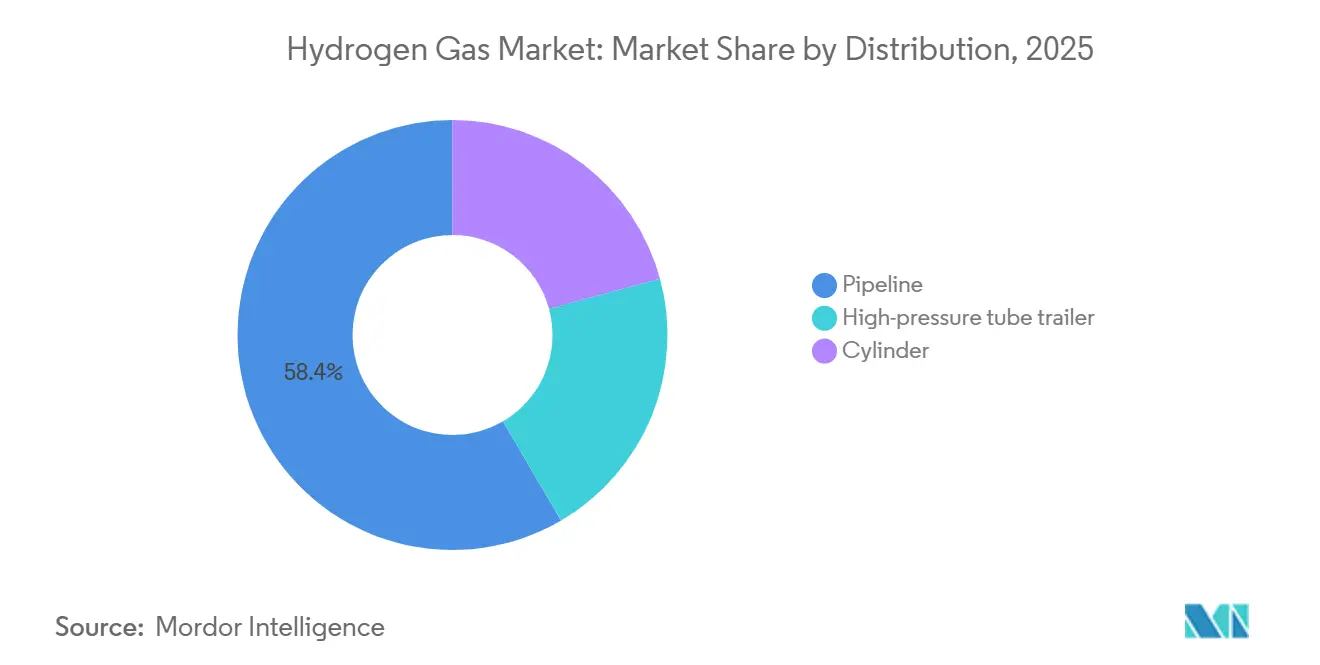

- By distribution, pipeline held 58.42% of the Hydrogen Gas market share in 2025 and is expected to expand at a 4.12% CAGR during the forecast period of 2026-2031.

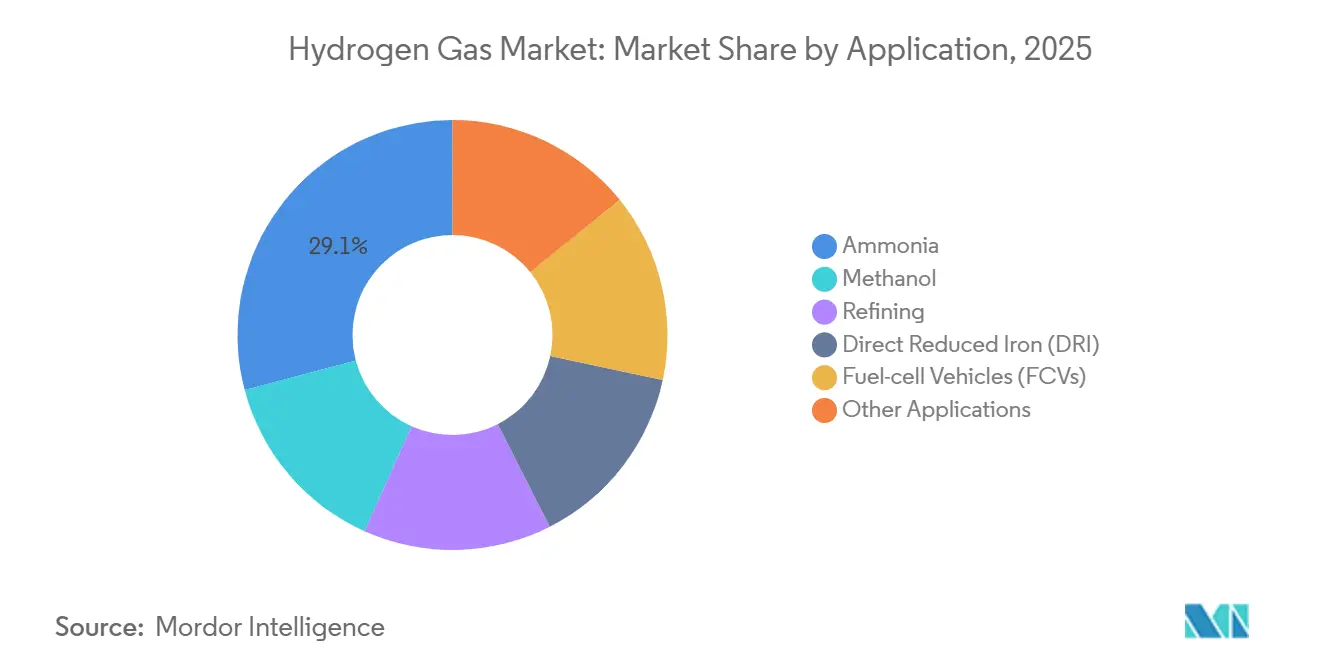

- By application, ammonia accounted for 29.11% of the Hydrogen Gas market size in 2025, whereas fuel-cell vehicles are advancing at the fastest 4.42% CAGR during the forecast period 2026-2031.

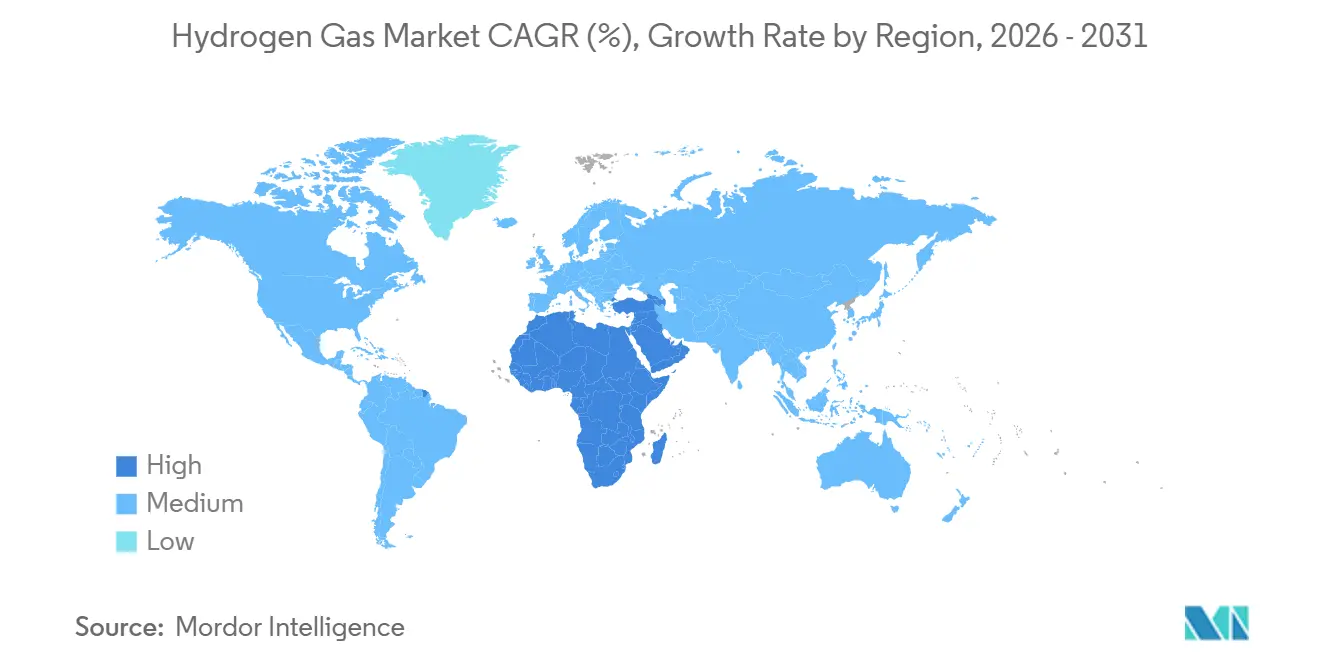

- By geography, the Asia-Pacific region commanded a 34.23% share of the Hydrogen Gas market size in 2025; the Middle East and Africa are recording the highest 4.12% CAGR during the forecast period 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrogen Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Refinery Desulfurization Regulations | +0.80% | Global, concentrated in North America, Europe, Asia-Pacific coastal refineries | Medium term (2–4 years) |

| Government Incentives for Green H₂ | +1.20% | North America (IRA), Europe (Hydrogen Bank), East Asia (national subsidies) | Long term (≥4 years) |

| Rising Fuel-Cell Vehicle Roll-out | +0.60% | Asia-Pacific (China, Japan, South Korea), California, Germany | Long term (≥4 years) |

| Hydrogen-Gas-Grid Blending Mandates | +0.50% | Europe (Germany, UK, Netherlands), select U.S. states | Medium term (2–4 years) |

| Surplus-Renewables-Driven Power-to-Gas Economics | +0.50% | Global, with early gains in Germany, California, South Australia, Chile | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Refinery Desulfurization Regulations

International Maritime Organization fuel rules and US Tier 3 gasoline standards increase hydrotreater hydrogen demand by 5–8% for each incremental sulfur cut[1]International Maritime Organization, “2020 Global Sulphur Cap,” imo.org. Gulf Coast, Rotterdam, and Singapore refineries therefore expand on-site steam-methane reformers tied into dedicated pipelines, locking in multi-year merchant contracts. Emerging-market refineries still purchasing tube-trailer gas pay USD 0.50-0.80 more per kg on a delivered basis. ISO 14001 reporting now requires disclosure of hydrogen carbon intensity, which is steering spot purchases toward lower-emission supply. Compliance deadlines through 2026 sustain baseline demand even as electrolyzer retrofits near parity in carbon-priced regions.

Government Incentives for Green H₂

Section 45V of the US Inflation Reduction Act offers up to USD 3 per kg for hydrogen below 0.45 kg CO₂-eq, stimulating co-located renewable-power electrolyzers[2]U.S. Department of the Treasury, “Section 45V Credit Guidance,” treasury.gov. Europe’s Hydrogen Bank awarded EUR 720 million of contracts-for-difference in 2024 to narrow the cost gap with grey hydrogen, but auctioned volumes remain a fraction of the 10 Mt annual import target for 2030. Japan, China, and South Korea extend purchase subsidies and feed-in tariffs that underpin multi-megawatt stack orders, driving Chinese alkaline electrolyzer prices under USD 200 per kW according to manufacturer disclosures. These layered incentives bring the hydrogen gas market closer to cost competitiveness in mobility, steel, and fertilizer.

Rising Fuel-Cell Vehicle Roll-out

Hyundai delivered more than 1,800 Xcient fuel-cell trucks to European carriers during 2024-2025, accumulating over 8 million km with 95% uptime on Alpine routes. Toyota expanded Mirai output to 12,000 units a year and co-funded 50 US stations dispensing 700-bar gas in under five minutes. China added 428 stations in 2025, bringing the national total to 1,104 and underpinning municipal procurement quotas for buses and sanitation fleets. Station capex, roughly USD 2–3 million for 40-vehicle-per-day capacity, remains the key bottleneck, but anchor fleets improve utilization economics. With Europe targeting 1,200 stations by 2030, the hydrogen gas market gains a credible mobility demand platform.

Hydrogen-Gas-Grid Blending Mandates

Germany authorized 20% hydrogen blends in select transmission loops from 2024, avoiding new pipeline capex but forcing burner retrofits in industrial boilers. The UK’s Redcar Hydrogen Village will convert 2,000 homes to 100% hydrogen by late 2025, testing appliance swap-outs and cast-iron main relining. Dutch community opposition halted a similar pilot, illustrating social-license risks even when technical codes such as ASME B31.12 are met. Distribution-node injection via tube trailers often suits dispersed demand clusters better than long-haul trunk lines. Successful pilots could unlock sizable distributed volumes inside the hydrogen gas market by the decade’s end.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expensive Storage and Transport Logistics | -0.90% | Global, acute in regions lacking pipeline infrastructure (South America, Sub-Saharan Africa) | Short term (≤2 years) |

| Community Opposition to New H₂ Pipelines | -0.40% | North America (Gulf Coast), Europe (Netherlands, Germany), localized in suburban corridors | Medium term (2–4 years) |

| Water-Scarcity Constraints in Arid Regions | -0.30% | Middle East and North Africa, with mitigation through desalination in Saudi Arabia, UAE, Oman | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Expensive Storage and Transport Logistics

Compressed storage at 350 bar packs one-tenth the energy density of diesel, so tube-trailer fleets incur delivery premiums above USD 2 per kg on routes exceeding 300 km. Liquefaction consumes 25–35% of hydrogen’s lower heating value and needs cryogenic tanks costing about USD 1,000 per kg daily throughput. Liquid-organic carriers cut boil-off losses yet suffer 40% round-trip efficiency losses and costly dehydrogenation catalysts. New hydrogen-grade pipelines run USD 3–5 million per km before right-of-way, limiting deployments in South America and Sub-Saharan Africa, where greenfield projects must bundle production and distribution capex. These costs weigh on near-term economics for the hydrogen gas industry.

Community Opposition to New H₂ Pipelines

A 1,200-km Gulf Coast-to-Midwest hydrogen corridor faced landowner objections that forced a 180-km reroute and USD 340 million in mitigation spend. The Netherlands’ HyNetwork backbone encountered municipal demands for third-party risk audits, delaying final investment decisions by 18 months. Germany’s retrofit of natural-gas lines proceeds faster due to existing easements, yet environmental groups challenge permits on groundwater-leak grounds. Absent federal hydrogen-specific integrity rules, US developers navigate a patchwork of state codes, which pushes insurance premiums 15-25% above natural-gas analogues. Social-license delays temper the hydrogen gas market’s infrastructure rollout pace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Distribution: Pipeline Dominance Anchored by Refinery Proximity

Pipeline networks supplied 58.42% of the hydrogen gas market size in 2025 and are projected to expand at a 4.12% CAGR during the forecast period (2026-2031) as refineries and ammonia plants demand uninterrupted flows. Tube trailers remain essential for 50–500 kg-per-day industrial users lacking spur lines, while cylinder packs shrink in laboratories and telecom backup systems that transition to cartridge formats. Emerging export pipelines reinforce future growth: Saudi Arabia’s 1,500-km NEOM line to Aqaba will feed green-ammonia export, and Europe plans to repurpose 11,600 km of gas transmission lines, trimming build costs 60% versus new construction. The Middle East and Africa lead pipeline additions, supporting gigawatt electrolyzers that target delivered costs of USD 1.50-2.00 per kg by 2030.

Tube-trailer economics improve where demand is fragmented; a 300-bar rig carrying 1,000 kg can serve six customers within 200 km, lowering deadhead mileage 20–30% using advanced route optimization. Cylinder packs still appeal to seasonal float-glass and specialty-welding shops, yet five-year hydrostatic tests under ISO 11114 inflate lifetime costs. In the hydrogen gas market, distribution portfolios therefore balance high-volume pipelines with flexible road logistics until regional demand clusters justify new steel.

By Application: Ammonia’s Feedstock Lock-In Versus Mobility’s Growth Potential

Ammonia synthesis absorbed 29.11% of the 2025 volume, holding the top hydrogen gas market share because Haber-Bosch reactors require continuous 150-300 bar hydrogen feeds. Refiners followed closely as hydrocrackers strip sulfur to meet IMO 2020 and Euro 6 fuel rules, yet longer-term gasoline demand erosion caps incremental growth. Methanol plants pivot toward green methanol for marine fuel; orders for 24 methanol-ready container ships signal new downstream demand. Direct-reduced-iron pilots, such as HYBRIT’s 1.2 Mt output in 2025, illustrate steel decarbonization potential once electrolyzer costs drop.

Fuel-cell vehicles are expected to log the highest CAGR at 4.42% during the forecast period (2026-2031), though only 1.5 Mt of hydrogen in 2025, as station roll-outs unlock heavy-duty trucking niches where batteries struggle with duty-cycle and refuel time. Nikola shipped 247 hydrogen trucks in 2024-2025, and Daimler Truck’s GenH2 prototype executed a 1,000-km run on one 80 kg fill. Ancillary uses, glass annealing, silicon etching, and edible-oil processing expand with industrial GDP, offering steady demand. Green-ammonia export complexes in Saudi Arabia and Australia will each require 600,000-800,000 t-per-year hydrogen by 2028, volumes that surpass North American mobility demand today. Application diversification thus safeguards the hydrogen gas market against single-sector volatility.

Geography Analysis

Asia-Pacific held 34.23% of the 2025 hydrogen gas market, propelled by China’s 1,104 refueling stations, Japan’s ammonia-import plans, and South Korea’s 6.2 Mt 2040 consumption target. China’s provincial grants for 10 MW-plus electrolyzers slashed alkaline stack costs below USD 200 per kW, half the European average, positioning Chinese suppliers for export. India’s National Hydrogen Mission commits INR 197 billion (USD 2.4 billion) to produce 5 Mt by 2030, focusing on Gujarat and Odisha corridors with sub-INR 2 kWh solar tariffs. ASEAN pilots in Thailand, Singapore, and Malaysia test grid blending and coal-plant ammonia co-firing while awaiting carbon-pricing clarity.

The Middle East and Africa are expected to record the fastest 4.12% CAGR during the forecast period (2026-2031). Projects in Saudi Arabia, UAE, Oman, and Egypt couple 30-40% capacity-factor solar with desalination, reaching projected costs of USD 1.50-2.00 per kg by 2030. The NEOM venture will ship 650 t-per-day hydrogen as ammonia from late 2026, while South Africa’s Boegoebaai targets 400,000 t green-ammonia from 2028 despite desalination add-ons of USD 0.30-0.50 per kg.

In North America, the US Department of Energy funded seven regional hubs, each producing 50,000-100,000 t annually for refining, fertilizer, and transport. Canada pursues blue hydrogen with carbon capture in Alberta and green hydrogen via hydropower in Quebec, eyeing EU exports once carbon-border levies finalize. Europe repurposes legacy gas grids; Germany allows 20% blends in select segments, the UK plans a 100% hydrogen village, and France backs a 200 MW Dunkirk electrolyzer supplying ArcelorMittal’s DRI pilot. South American ambitions concentrate in Chile’s high-wind Magallanes and Brazil’s Pecém port, although grid-tie delays push several final decisions into 2026. Collectively, diversified regional pipelines, hub programs, and export projects underpin the hydrogen gas market’s global expansion.

Competitive Landscape

The Hydrogen Gas market is moderately consolidated. Chinese stack makers such as LONGi and Sungrow leverage scaled photovoltaic manufacturing to sell alkaline electrolyzers at USD 180-220 per kW, creating price pressure on Western PEM suppliers, though lower efficiency and durability constrain immediate utility-scale adoption. Competitive intensity in the hydrogen gas market stems from cost-down races in electrolyzers, lock-in effects of pipeline franchises, and premium-segment differentiation around lifecycle emissions tracking.

Hydrogen Gas Industry Leaders

Air Liquide

Linde plc

Air Products and Chemicals, Inc.

Messer SE & Co. KGaA

TAIYO NIPPON SANSO CORPORATION

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Waaree Clean Energy Solutions, an Indian renewable energy firm, announced plans to construct, own, and manage a 2.5MW electrolyser plant in Uttar Pradesh. This facility aims to generate 4.1 million Nm³ of green hydrogen and 2 million Nm³ of green oxygen for a regional supplier.

- August 2025: Torrent Group inaugurated India's second green hydrogen plant in Gorakhpur, Uttar Pradesh, India. The plant aims to produce 72 tonnes of green hydrogen annually, which will be blended into natural gas pipelines at concentrations reaching up to 2%.

Global Hydrogen Gas Market Report Scope

Hydrogen gas is a clean, burning, and efficient fuel used in refining processes and producing many chemicals like ammonia and methanol. Hydrogen gas is created through steam methane reforming, coal gasification, and water electrolysis.

The Hydrogen Gas market is segmented by distribution, application, and geography. By distribution, the market is segmented into pipelines, high-pressure tube trailers, and cylinders. By application, the market is segmented into ammonia, methanol, refining, direct reduced iron (DRI), fuel cell vehicles (FCV), and other applications. The report also covers the market size and forecasts for the Hydrogen Gas market in 16 countries across major regions. For each segment, the market sizing and forecasts are provided based on volume (tons).

| Pipeline |

| High-pressure tube trailer |

| Cylinder |

| Ammonia |

| Methanol |

| Refining |

| Direct Reduced Iron (DRI) |

| Fuel-cell Vehicles (FCVs) |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Distribution | Pipeline | |

| High-pressure tube trailer | ||

| Cylinder | ||

| By Application | Ammonia | |

| Methanol | ||

| Refining | ||

| Direct Reduced Iron (DRI) | ||

| Fuel-cell Vehicles (FCVs) | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for hydrogen reach by 2031?

The hydrogen gas market size is projected to hit 141.25 million tons by 2031, expanding at a 3.65% CAGR from 2026.

Which application uses the most hydrogen today?

Ammonia synthesis leads, absorbing 29.11% of 2025 volume thanks to continuous-flow Haber-Bosch plants.

What region will grow fastest over the next five years?

The Middle East and Africa post the highest 4.12% CAGR through 2031 as export-oriented green-hydrogen megaprojects come online.

Why do pipelines dominate hydrogen distribution?

Refinery and fertilizer complexes cluster near SMR production and value uninterrupted pipeline supply, giving pipelines a 58.42% 2025 share.

What is the main cost restraint on hydrogen adoption?

Storage and transport add up to USD 2 per kg for road delivery and consume 25–35% of energy in liquefaction, slowing near-term economics.

Page last updated on: