Specialty Gas Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

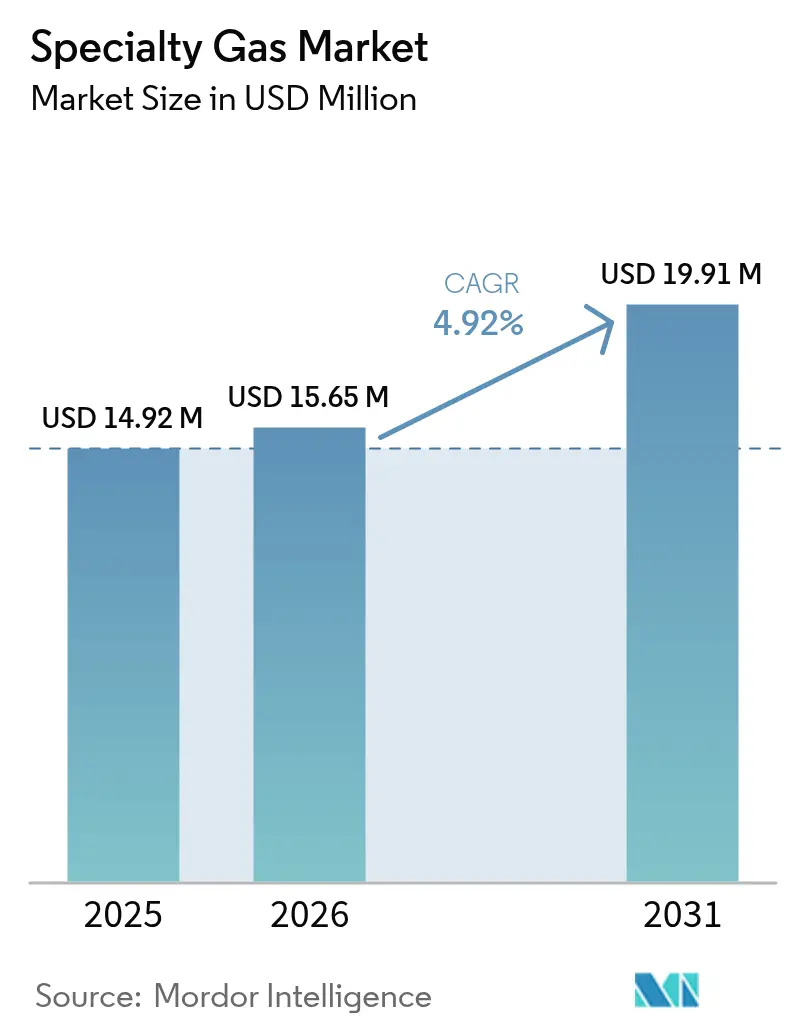

| Market Size (2026) | USD 15.65 Million |

| Market Size (2031) | USD 19.91 Million |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Specialty Gas Market Analysis by Mordor Intelligence

The Specialty Gas Market size in 2026 is estimated at USD 15.65 million, growing from 2025 value of USD 14.92 million with 2031 projections showing USD 19.91 million, growing at 4.92% CAGR over 2026-2031. Demand acceleration stems from soaring semiconductor fabrication, fast-growing medical-grade usage, and a surge of green hydrogen pilots that depend on calibration mixtures. Semiconductor process nodes below 5 nm require ultra-high-purity gas grades, prompting sustained investment in purification technology and on-site supply systems. Parallel momentum comes from petrochemical and solar power projects that adopt specialty gases for process optimization and emissions control. Environmental mandates are tightening production standards, yet producers are countering with low-carbon formulations and high-efficiency separation units, ensuring steady output while curbing greenhouse gases. Competitive dynamics remain moderately concentrated as global majors expand capacity, acquire regional distributors, and introduce digitally enabled traceability services to secure long-term contracts with chipmakers, refiners, and hospitals.

Key Report Takeaways

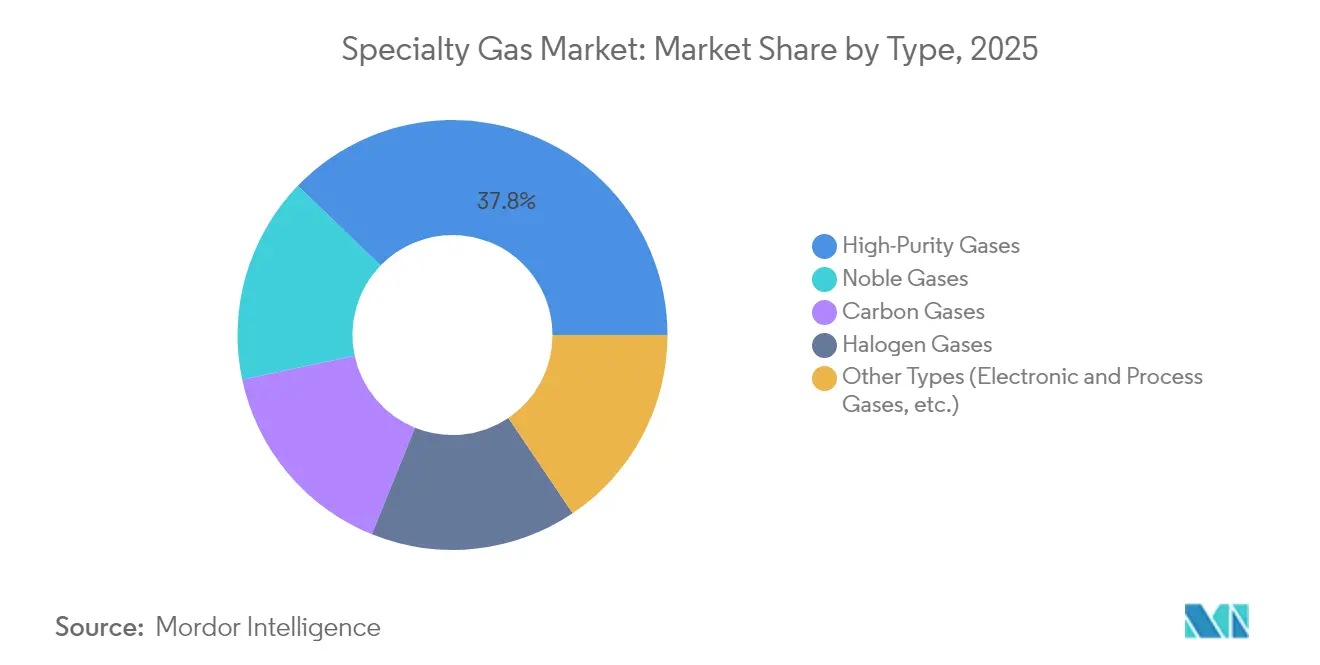

- By type, high-purity gases led with 37.79% revenue share in 2025; electronic and process gases are projected to expand at a 5.48% CAGR through 2031.

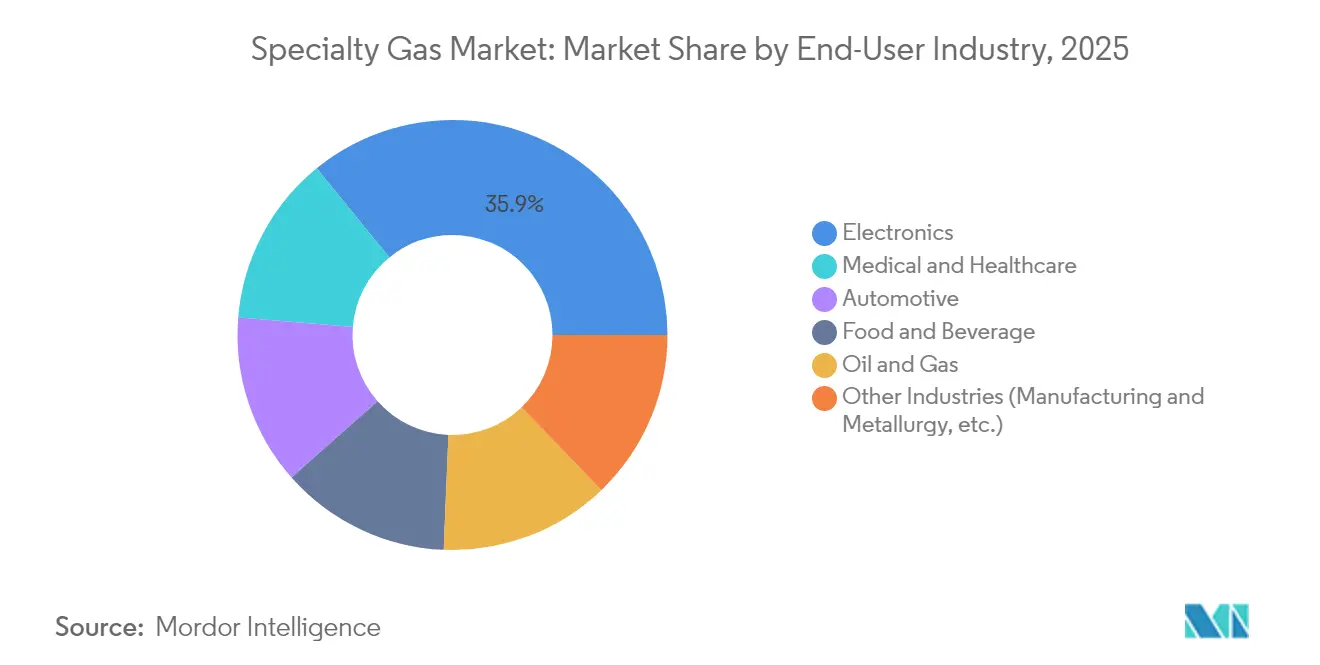

- By end-user industry, the electronics & semiconductor segment commanded 35.88% of the specialty gas market share in 2025, while healthcare is set to grow at a 6.22% CAGR to 2031.

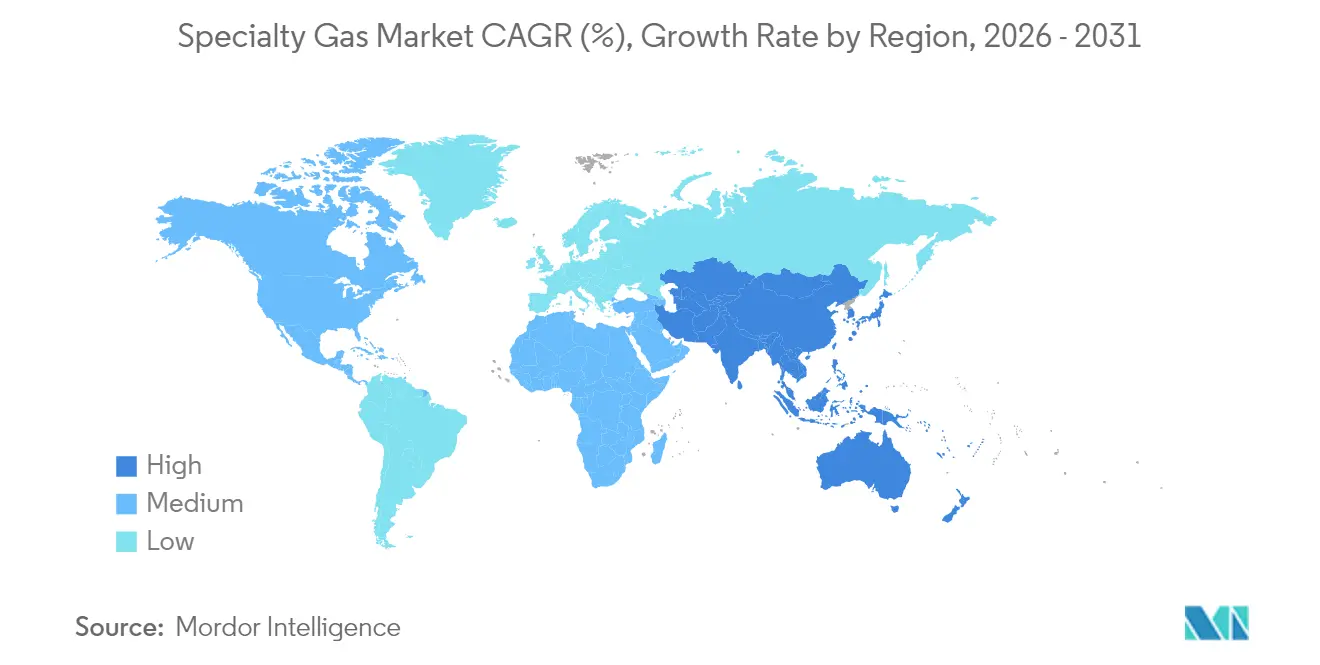

- By geography, Asia-Pacific captured 47.85% of the specialty gas market size in 2025 and is forecast to post the fastest regional CAGR of 6.55% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Specialty Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor-grade Wafer Fabrication Boom Creating Demand for Specialty Gas | +1.20% | Asia-Pacific, North America | Medium term (2-4 years) |

| Increasing Utilization for Specialty Gased from Petrochemcial Industry | +0.80% | Middle East, Asia-Pacific, North America | Medium term (2-4 years) |

| Rapid Expansion of Green Hydrogen Pilots Requiring Calibration Gases | +0.70% | Europe, North America | Long term (≥ 4 years) |

| Increasing Demand from the Healthcare Sector | +1.10% | Global, led by North America and Europe | Medium term (2-4 years) |

| Increasing Usage in the Solar Power Sector for Energy Absorption and Operational Efficiency | +0.90% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semiconductor-grade wafer fabrication boom creating demand for specialty gas

Unprecedented chip-fabrication investment is elevating consumption of ultra-high-purity nitrogen, argon, and fluorinated compounds. Plants now specify 6 N purity (99.9999%) for chemical vapor deposition, etching, and ion implantation, as shown by Linde’s SPECTRA plants that supply Samsung’s Pyeongtaek campus. The U.S. CHIPS and Science Act has catalyzed USD 450 billion in private spending across 90 projects, expected to triple national wafer output by 2032[1]Semiconductor Industry Association, “2024 State of the U.S. Semiconductor Industry,” semiconductors.org . Asia-Pacific fabs in Taiwan, South Korea, and mainland China are also scaling, fueling long-term contracts with global gas suppliers. These dynamics underpin a robust pipeline of purification skids, micro-bulk tanks, and electronic-grade fill plants. The specialty gas market therefore benefits from predictable volume off-take and premium pricing tied to purity guarantees.

Increasing utilization for specialty gases from petrochemical industry

Hydrogen, carbon monoxide, and bespoke hydrocarbon blends remain critical for hydrotreating, cracking, and catalyst regeneration within petrochemical complexes. Operators in the Middle East and Texas Gulf Coast are connecting to Air Products’ hydrogen pipelines that exceed 1,600 km in length. Real-time gas analytics enhance product yields while reducing flaring, driving procurement of calibration mixes and high-purity oxygen for oxidative processes. Refineries shifting toward low-sulfur fuels intensify consumption further. As a result, the specialty gas market sees stable base-load volumes and rising demand for turnkey supply schemes that bundle gas, equipment, and process control software.

Rapid expansion of green hydrogen pilots requiring calibration gases

Europe’s decarbonization roadmap doubles electrolyzer capacity to 10 GW by 2030, mandating rigorous quality checks for hydrogen purity and oxygen removal. Germany, the Netherlands, and Denmark are rolling out 1,800 km of hydrogen pipelines by 2028, each compressor station needing certified H₂, O₂, and N₂ standards. Australia’s Port Kembla project illustrates the trend with Asia-Pacific’s first heavy-transport hydrogen refueling hub, supplied by Coregas mixes. These pilots propel orders for specialty gas cylinders, mass-flow controllers, and portable analyzers, supporting the specialty gas market’s long-term CAGR.

Increasing demand from the healthcare sector

Hospitals and biotechnology labs rely on medical-grade oxygen, nitrogen, and carbon dioxide for respiratory care, cryopreservation, and drug formulation. The U.S. Defense Health Program allocates USD 40.27 billion in FY 2025 for healthcare services and modernization, encouraging upgrades to on-site gas plants and distribution networks[2]U.S. Department of Defense, “Defense Health Program Fiscal Year 2025 Budget,” comptroller.defense.gov . New therapeutic modalities—including cell and gene therapy—require stringent atmospheric controls, raising consumption of inert gases. Growth in elective surgeries post-pandemic is another booster, ensuring that healthcare remains the fastest-advancing end-use segment within the specialty gas market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environmental Regulations and Restrictions on Specialty Gas Production and Quality Control | -0.90% | Europe, North America | Medium term (2-4 years) |

| Supply Chain Concerns Impacting Utilization in Certain Geographies | -0.70% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| High Production and Purification Cost for Certain Gases | -0.60% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent environmental regulations and restrictions on specialty gas production and quality control

The AIM Act compels an 85% phase-down of HFC consumption by 2036, prompting reformulation of specialty refrigerant blends and investment in abatement systems[3]Environmental Protection Agency, “Fiscal Year 2025 Congressional Justification,” epa.gov . Methane emitters in the U.S. oil and gas sector face a Waste Emissions Charge of USD 900 per ton in 2024, rising to USD 1,500 by 2026[4]Federal Register, “Waste Emissions Charge for Petroleum and Natural Gas Systems,” federalregister.gov . European plants operate under the Industrial Emissions Directive and carbon pricing, which elevate compliance costs. Although these rules drive innovation in low-GWP gases, they can slow capacity additions and tighten short-term supply, putting minor downward pressure on the specialty gas market’s growth rate.

Supply chain vulnerabilities impacting utilization in certain geographies

Extreme concentration of electronic-grade gas production in East Asia exposes fabs elsewhere to shipping delays, geopolitical risks, and container shortages. The Asia Pacific Electronic Specialty Gas Conference stressed that Southeast Asian clusters must strengthen redundancy in filtration media and specialty cylinder supply. US importers continue to diversify suppliers to comply with any future trade restrictions, while European buyers pursue stockpile strategies. Until new regional distillation columns come online, intermittent shortages of neon, xenon, and helium may hamper downstream production and temper the specialty gas market’s growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: High-purity gases underpin semiconductor performance

High-purity gases accounted for a 37.79% revenue share in 2025 as fabs tightened impurity specifications to parts-per-trillion levels. UBE’s 30% capacity increase for high-purity nitric acid at its Ube facility underlines sustained semiconductor demand. Noble gases face sporadic supply disruptions following geopolitical tensions and maintenance outages at liquefaction plants, but targeted investments in recovery and liquefier upgrades are stabilizing availability. Electronic and process gases make up the fastest-growing sub-segment at 5.48% CAGR, benefiting from advanced etch chemistries needed in 3-D NAND and gate-all-around transistors.

Ultra-high-purity (UHP) hydrogen and fluorinated compounds support aggressively scaled EUV lithography lines that cannot tolerate metallic or moisture contamination beyond single-digit ppt thresholds. Meanwhile, demand for carbon-based specialty gases—including high-purity carbon monoxide for OLED precursor synthesis—remains strong across fine-chemical and display manufacturing. These diverse use cases reinforce the specialty gas market’s resilience to short-cycle swings in any one sector.

By End-User Industry: Electronics sector secures structural lead

The electronics & semiconductor domain captured 35.88% of 2025 revenue, driven by wafer-fab expansions in Asia and reshorings in the United States. The specialty gas market share for this segment is projected to hold steady while volumes grow, with penetration deepening as pattern densities shrink. Healthcare applications, advancing at a 6.22% CAGR, increasingly rely on nitrous oxide substitutes, hyperbaric oxygen protocols, and cylinder-less manifold systems for ICUs. Hospitals in Europe and North America are adopting track-and-trace smart valves that enhance patient safety and automate replenishment cycles.

Automotive electrification adds another layer of demand as battery cell plants order high-purity argon and nitrogen for dry-room environments, while EV test labs purchase calibration mixes for emission-free range verification. Petrochemical and oil & gas operators utilize laser-grade CO₂ and helium for leak-detection, contributing a stable base. Collectively, these industries ensure that the specialty gas market enjoys a diversified revenue portfolio insulated from isolated sector downturns.

Geography Analysis

Asia-Pacific generated 47.85% of global revenue in 2025 and is on course to grow at a 6.55% CAGR through 2031. Mainland China continues to commission memory and logic megafabs that consume bulk nitrogen and electronic-grade fluorinated gases. South Korea’s Pyeongtaek and Xi’an lines bolster demand for UHP argon. Taiwan’s cluster remains a heavy purchaser of neon sourced from diversified purification hubs to mitigate Ukrainian supply risk. Japanese OEMs invest in long-term helium contracts to shield domestic chip tool production, sustaining imports despite global shortages. ASEAN nations, led by Malaysia and Vietnam, have attracted advanced-packaging plants that require large volumes of forming-gas mixtures, drawing regional distributors closer to end-users. These combined investments secure Asia-Pacific’s long-running leadership in the specialty gas market.

North America benefits from USD 450 billion in private semiconductor investment sparked by the CHIPS Act, expanding wafer output and stimulating sales of precursor gases, high-purity ammonia, and chamber-clean blends. Shale gas production is set to hit 105 Bcf/d in 2025, improving feedstock economics for nitrogen and hydrogen. The region is also witnessing brisk installation of green-hydrogen electrolyzers and CO₂ capture units, each reliant on calibration standards that spur specialty gas procurement. Rising hospital refurbishment, coupled with the Defense Health Program budget, accelerates medical-grade demand. Consequently, the specialty gas market in the United States and Canada is on a firm, multi-year upswing.

Europe shows more measured growth due to stringent industrial-emission directives, yet its strong green-hydrogen ambitions and advanced research laboratories ensure steady consumption. Germany’s plan to double electrolyzer capacity underpins demand for H₂, O₂, and CO calibration gases, while France’s role as Europe’s largest LNG importer drives marine-fuel transition gases and bunker-grade nitrogen. Scandinavian fabs focusing on silicon carbide and gallium nitride devices order high-purity silane and dichlorosilane, expanding the specialty gas market’s niche segments. Eastern European pharmaceutical clusters add another layer of volume, purchasing sterile-grade CO₂ for lyophilization lines.

South America’s specialty gas market is smaller but rising, with Brazilian petrochemical complexes using hydrogen and nitrogen for polymer grade output, and Argentine refineries investing in sulfur-recovery upgrades that require specialty blends. In the Middle East & Africa, mega-refining and gas-to-chemicals projects in Saudi Arabia drive ordering of bulk hydrogen and SO₂ for trace-element removal, while South Africa’s healthcare sector expands bulk oxygen networks across provincial hospitals. These initiatives collectively widen the specialty gas market’s global footprint.

Competitive Landscape

Global majors command a majority share, resulting in highly consolidated concentration. Air Liquide achieved 2024 sales exceeding EUR 27 billion and improved its operating margin despite inflationary energy costs. Its investment pipeline now allocates 40% to energy-transition projects, such as low-carbon hydrogen and CCS, while maintaining aggressive spend on electronics gases for Asia-Pacific fabs. Linde secured 53 new small on-site agreements in 2023 worth USD 270 million, serving midsize manufacturers that prefer captive supply over bulk trucking. It is evaluating a partnership with Merck to integrate specialty gases with advanced semiconductor chemicals, indicating a potential vertically integrated offering.

Air Products continues to expand its global hydrogen backbone, adding looping segments in Texas and building new separation units in Jubail, Saudi Arabia. It is also supplying over 20 electrolyzer projects, bundling calibration-gas contracts that lock in downstream specialty gas revenue. Chart Industries posted USD 4.16 billion in 2024 sales, leveraging cryogenic expertise to fabricate hydrogen and CO₂ liquefaction modules. Nippon Sanso Holdings deploys modular specialty-gas plants near Japanese and Southeast Asian customers to ensure local security of supply.

Strategic moves feature capacity debottlenecking in helium recovery, adoption of IoT cylinder-tracking, and mergers that widen end-market access. For example, April 2025 saw Linde commit to larger nitrogen and argon supply lines for Samsung’s Pyeongtaek facility, reinforcing its electronics franchise. February 2025 discussions between Merck and Linde hint at co-developing high-k precursor gases. Overall, competition centers on technology leadership, renewable-energy alignment, and supply-chain reliability, all serving to differentiate offerings in the specialty gas market.

Specialty Gas Industry Leaders

Air Liquide

Air Products and Chemicals Inc.

Linde plc

Messer SE & Co. KGaA

TAIYO NIPPON SANSO CORPORATION

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Linde PLC has announced plans to expand its supply of specialty gases to Samsung's advanced semiconductor manufacturing facility in Pyeongtaek, South Korea. This development is expected to strengthen Linde's position in the specialty gas market, driving growth and supporting the increasing demand for high-purity gases in the semiconductor industry.

- February 2025: Merck and Linde are setting up specialty chemicals and gases facilities in India to strengthen the country's semiconductor manufacturing capabilities. These investments highlight the growing global interest in India's chip ecosystem, which is critical for ensuring supply chain reliability and driving industry growth.

Global Specialty Gas Market Report Scope

Specialty gases are gaseous substances of high purity and can be used in industrial processes as analytical lab gases and intermediates. These gases are essential to many sectors, including the healthcare, petrochemical, environmental, pharmaceutical, semiconductor, and chemical markets.

The specialty gas market is segmented by type, end-user industry, and geography. Based on type, the market is segmented into high-purity gases, noble gases, carbon gases, halogen gases, and other types. Based on the end-user industry, the market is segmented into automotive, electronics, healthcare, food and beverage, oil and gas, and other end-user industries. The report also covers the market size and forecasts for specialty gas in 15 countries across major regions.

For each segment, the market sizing and forecasts have been done based on revenue (USD million).

| High-Purity Gases |

| Noble Gases |

| Carbon Gases |

| Halogen Gases |

| Other Types (Electronic and Process Gases, etc.) |

| Electronics |

| Medical and Healthcare |

| Automotive |

| Food and Beverage |

| Oil and Gas |

| Other Industries (Manufacturing and Metallurgy, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East Africa |

| By Type | High-Purity Gases | |

| Noble Gases | ||

| Carbon Gases | ||

| Halogen Gases | ||

| Other Types (Electronic and Process Gases, etc.) | ||

| By End-User Industry | Electronics | |

| Medical and Healthcare | ||

| Automotive | ||

| Food and Beverage | ||

| Oil and Gas | ||

| Other Industries (Manufacturing and Metallurgy, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East Africa | ||

Key Questions Answered in the Report

What is the current size of the specialty gas market, and how fast is it growing?

The specialty gas market is valued at USD 15.65 billion in 2026 and is projected to reach USD 19.91 billion by 2031, growing at a 4.92% CAGR.

Which segment holds the largest specialty gas market share?

High-purity gases dominate with a 37.79% share in 2025 due to stringent semiconductor purity needs.

Why is Asia-Pacific the leading regional market for specialty gases?

Asia-Pacific hosts the bulk of global semiconductor fabrication and solar panel production, giving it 47.85% revenue share in 2025 and the fastest 6.55% regional CAGR through 2031.

How do environmental regulations influence specialty gas demand?

Rules such as the AIM Act’s HFC phase-down and methane emission fees push producers toward low-GWP formulations and control technologies, raising compliance costs but driving innovation in greener gases.

Which industries are driving future demand for specialty gases?

Semiconductors, healthcare, green hydrogen, petrochemicals, and solar power are the main engines, each requiring precise gas blends and high-purity grades for advanced processes.

Who are the leading players in the specialty gas market?

Air Liquide, Linde plc, Air Products and Chemicals Inc., Messer SE & Co. KGaA, and TAIYO NIPPON SANSO CORPORATION are the principal players.

Page last updated on: