Market Overview

| Study Period | 2020 - 2031 |

|---|---|

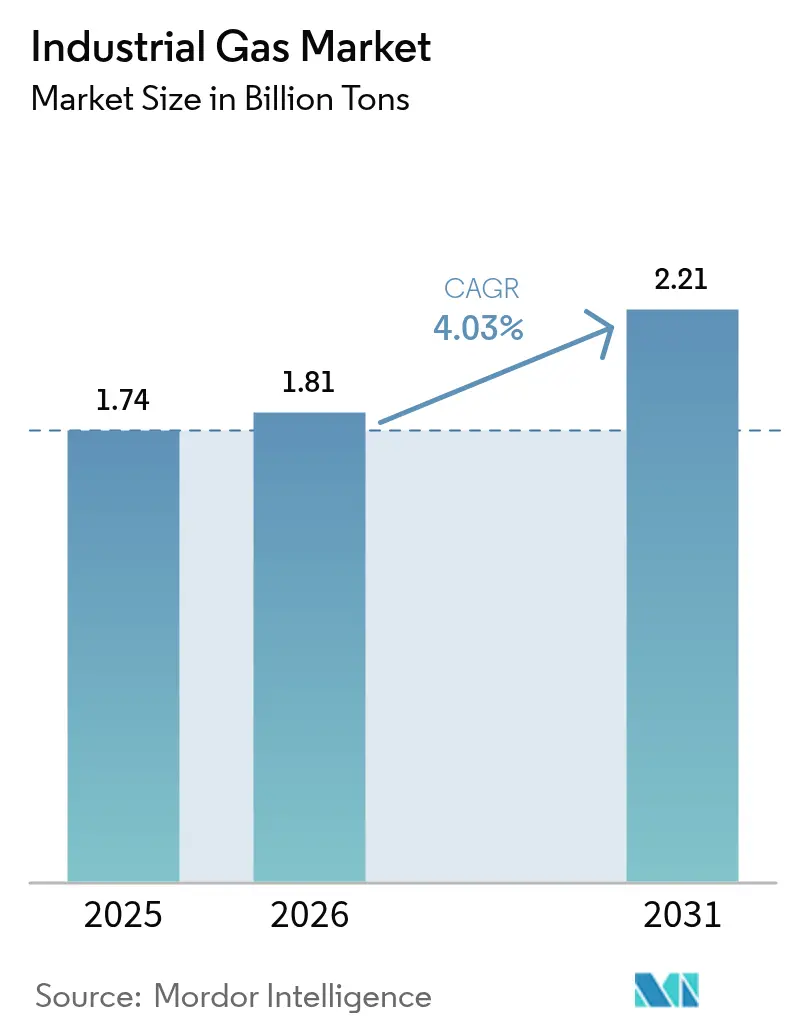

| Market Volume (2026) | 1.81 Billion tons |

| Market Volume (2031) | 2.21 Billion tons |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

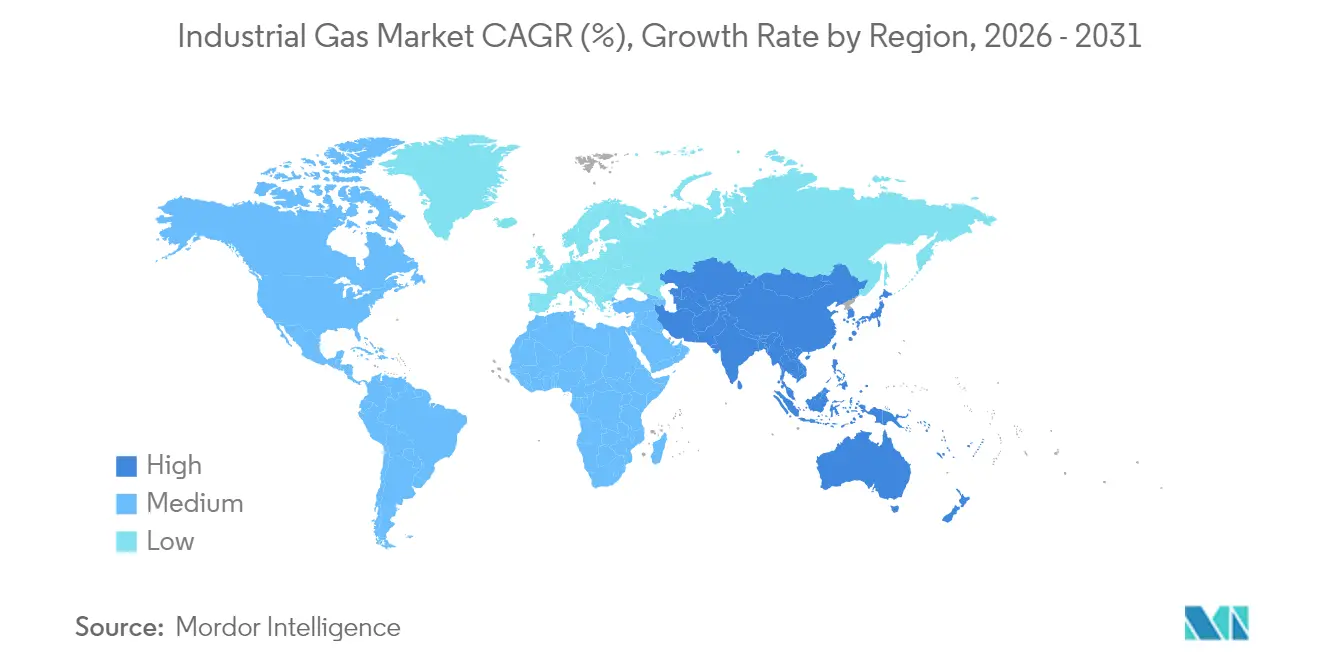

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Gas Market Analysis by Mordor Intelligence

The Industrial Gas Market size is expected to grow from 1.74 billion tons in 2025 to 1.81 billion tons in 2026 and is forecast to reach 2.21 billion tons by 2031 at 4.03% CAGR over 2026-2031. Healthy demand from steel, semiconductor, and chemical producers underpins this growth, while product innovation around green-hydrogen, high-purity oxygen, and food-grade carbon dioxide keeps value creation ahead of volume expansion. Producers are reinforcing on-site supply models to reduce logistics exposure, and large energy users are signing multi-decade supply contracts that lock in power costs. Regionalization of semiconductor fabrication is shifting high-purity nitrogen and argon flows toward the United States and Europe, even as Asia retains overall volume leadership. At the same time, helium recovery projects, carbon capture ventures, and small-footprint air-separation units are attracting fresh capital from both incumbents and infrastructure investors.

Key Report Takeaways

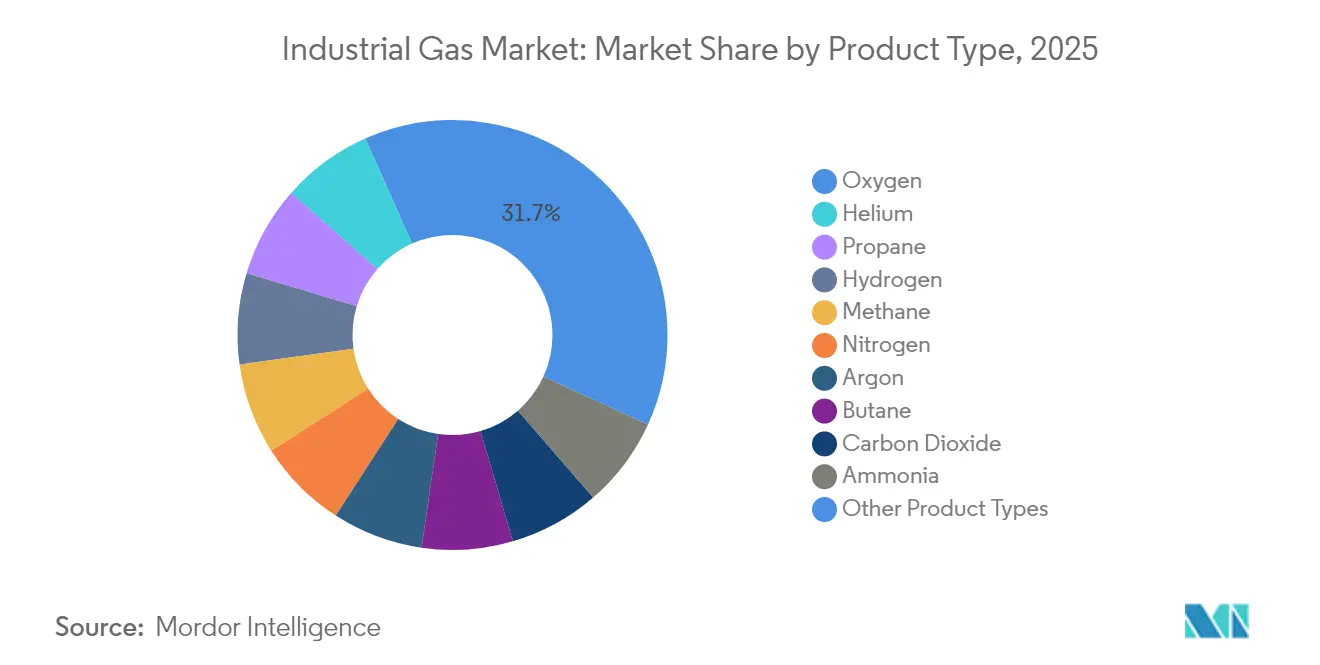

- By product type, oxygen led with 31.65% revenue share in 2025, while nitrogen is on track for a 4.38% CAGR through 2031.

- By mode of supply, the packaged/cylinder segment commanded a 36.78% share in 2025; on-site (tonnage) generation is projected to expand at a 4.29% CAGR through 2031.

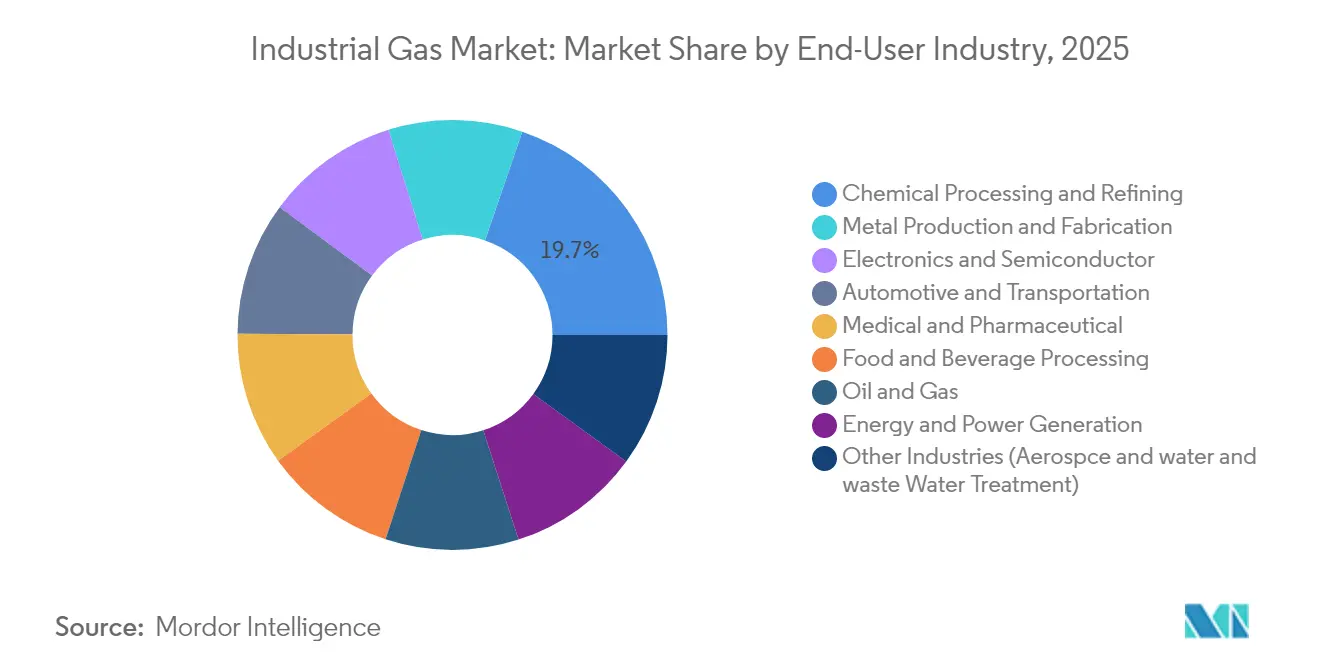

- By end-user industry, chemical processing and refining accounted for 19.74% of the industrial gases market share in 2025, while food and beverage processing are advancing at a 5.05% CAGR to 2031.

- By geography, Asia-Pacific held a 42.55% stake in 2025 and is set to grow at a 4.96% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Industrialization in Emerging Economies | +0.90% | Asia, Middle East | Medium term (2-4 years) |

| Green-Hydrogen Push Driving On-Site Electrolysis Contracts in EU & Australia | +1.10% | European Union, Australia, Gulf | Long term (≥ 4 years) |

| Oxygen Uptake from Low-Carbon DRI Steel Plants in US & MENA | +0.70% | United States, MENA | Medium term (2-4 years) |

| CO₂ Capture & Re-Use Projects in EU Breweries & Soda Plants | +0.40% | European Union | Short term (≤ 2 years) |

| Helium Supply-Security Platforms Expanding in North America | +0.30% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Industrialization in Emerging Economies

Robust manufacturing expansion across Asia, especially in China and India, is lifting base-load demand for volume gases such as oxygen and nitrogen. Western India alone houses a large concentration of steel mills, petrochemical clusters, and fertilizer complexes that collectively anchor localized air-separation capacity. Regional authorities are pressing ahead with Make-in-India incentives, encouraging investment in electronics assembly, solar-cell production, and electric-vehicle supply chains that use high-purity nitrogen and argon. Parallel infrastructure projects—from metro rail to greenfield refineries—are extending distributed demand pockets that favor packaged and microbulk deliveries. The U.S. Energy Information Administration projects Asian natural-gas consumption will triple by 2050, with 80% channelled into industry, a proxy for the scale of process-gas requirements[1]U.S. Energy Information Administration, “International Energy Outlook 2023,” eia.gov .

Green-Hydrogen Push Driving On-Site Electrolysis Contracts

Decarbonization targets are accelerating the adoption of low-carbon hydrogen, prompting chemical, steel, and heavy-transport operators to lock in long-term supply agreements. In partnership with ACWA Power and NEOM, Air Products is developing a USD 8.5 billion renewable-powered electrolysis plant in Saudi Arabia that will supply 650,000 t/y of green ammonia feedstock. Similar contracts across the European Union, Australia, and the United States are under construction, collectively exceeding 1.1 million t/y of planned output. These projects boost demand for associated gases such as nitrogen (for inerting) and oxygen (as a by-product), and they reinforce on-site generation as the preferred delivery model, reducing trucking emissions and power losses.

Oxygen Uptake from Low-Carbon DRI Steel Plants

Steelmakers are shifting from blast furnaces to natural-gas-based Direct Reduced Iron processes that use oxygen-enhanced combustion to cut CO₂ intensity. Linde signed 59 long-term agreements in 2024 to build and operate 64 small on-site nitrogen and oxygen plants, many dedicated to metal producers adopting DRI routes. The company’s ECOVAR modular ASU offers quick installation and energy-efficient vacuum pressure swing adsorption back-ups, lowering the total cost of ownership for mills. The International Energy Agency estimates that each million tons of DRI capacity can displace 1.4 million tons of CO₂ versus conventional blast-furnace steel, reinforcing policy support for oxygen-rich processes.

CO₂ Capture & Re-Use Projects in EU Breweries & Soda Plants

European breweries are installing closed-loop systems that capture CO₂ from fermentation, re-compress it, and reuse it for beverage carbonation. These skid-mounted units, supplied by Air Liquide and Linde, stabilize supply during merchant-CO₂ shortages and cut Scope 1 emissions. A leading German brewer reported a 45% drop in purchased CO₂ volumes after switching to in-house capture, freeing up merchant capacity for food-processing and healthcare end-markets. Similar projects are underway at soda bottling plants in Italy and Denmark, illustrating how food-grade gases can gain circularity while meeting stringent EU purity regulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment and Operational Costs | -0.80% | Global | Long term (≥ 4 years) |

| Stringent Safety and Environmental Regulations | -0.50% | Global | Medium term (2-4 years) |

| Volatility in Raw Material and Energy Prices | -0.40% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Helium Supply-Security Platforms Expanding in North America

Tight global helium balances continue to disrupt MRI equipment uptime, semiconductor fabrication, and aerospace inerting. The Cliffside Helium System in Texas, a strategic storage complex, remains under receivership yet sustains a minimum allocation for critical users. Quantum Technology Corp. started Western Canada’s first new helium refinery in four decades, adding small but important regional redundancy. Nonetheless, helium prices rose sharply in late 2024, pressuring procurement budgets and encouraging end-users to invest in recovery, purification, and recycling skids. This volatility underpins cautious CAPEX planning for greenfield fabs and acts as a near-term drag on overall consumption growth.

High Capital Investment and Operational Costs

Air-separation plants and hydrogen steam-methane reformers are power-intensive and cost between USD 200–350 million for a single large-scale unit producing up to 5,000 t/d of oxygen, consuming as much electricity as 72,000 homes[2]Cryogenic Society of America, “Air Separation Unit Economics,” cryogenicsociety.org . Deregulated power markets expose operators to spot price spikes that can erode margins or force pass-through surcharges onto customers. As a result, only a handful of global majors possess the balance sheet strength and technical expertise to design, construct, and maintain these units, reinforcing high entry barriers. Smaller players often prefer distribution partnerships or merchant-bulk sourcing rather than owning production assets, constraining market fragmentation in the long run.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oxygen Strengthens Lead in Steel, Healthcare, and Chemicals

Oxygen retained a commanding 31.65% share of the industrial gases market size in 2025 and continues to outpace overall volume growth as steelmakers migrate to DRI furnaces and hospitals expand high-flow ventilator capacity. During 2024, Linde and Air Liquide commissioned more than 20 vacuum pressure swing adsorption units dedicated to medical oxygen, reflecting post-pandemic baseline demand. In parallel, research at Nagoya University demonstrated an adsorptive-dissolution membrane capable of separating oxygen from argon at lower energy intensity, pointing toward future cost savings in ultra-high-purity applications.

Nitrogen is driven by semiconductor inerting, laser-cutting, and modified-atmosphere packaging for premium food lines. The segment benefits from a balanced mix of delivery modes: packaged cylinders for metal-fabrication shops, merchant liquid for electronics clean rooms, and on-site generators at cold-storage hubs. Carbon dioxide volume slipped in 2024 because of feedstock disruptions at ethanol plants; however, in-house capture at breweries cushioned beverage producers against outright shortages.

By Mode of Supply: Packaged/Cylinder Retains Leadership, On-Site Surges

The packaged/cylinder channel held 36.78% of the industrial gases market share in 2025 as small-batch users across welding, laboratories, and healthcare sought flexible, immediate supply. Airgas manages roughly 40,000 bulk deliveries each month in the United States using telemetry-enabled ordering that trims empty miles and ensures safety compliance. While cylinders prevail for intermittent consumption, the MicroBulk segment—including Chart Industries’ Orca delivery trailers—offers a step-up solution for users with 20–150,000 SCF monthly needs, reducing cylinder handling risks.

On-site generation recorded the most pronounced project momentum in 2024, evidenced by Linde’s 59-unit award slate, many under 300 t/d capacity. Semiconductor fabs prefer on-site nitrogen purification to safeguard ultra-high-purity specifications, and steel mini-mills opt for modular ASUs to match incremental output. Merchant bulk liquid, while ceding share to on-site setups, remains indispensable for mid-scale clients such as regional hospitals and chemical parks where redundancy and code compliance dictate remote production. Segmented logistics planning that blends on-site backbones with backup trailers is becoming the norm, raising switching costs for customers and securing long-term offtake for producers.

By End-User Industry: Chemical Processing Dominates, Electronics Outpaces

Chemical processing and refining consumed 19.74% of the industrial gases market size in 2025, anchored by hydrogen for hydro-treating, nitrogen for purge safety, and oxygen for ethylene oxide synthesis. U.S. refiners sourced 68% of their hydrogen from external suppliers in 2024, up from 53% a decade earlier, indicating a secular outsourcing trend that enlarges merchant gas pools. Volatility in crude-sulfur content and stricter fuel sulfur caps keep hydro-processing throughput high, locking in consistent hydrogen uplift.

Electronics and semiconductor fabrication exhibited the steepest demand curve, thanks to reshor-ing incentives and record wafer-fab announcements in the United States, Germany, and Japan. Ultra-clean nitrogen, argon, and hydrogen fluoride are essential for photoresist stripping and chamber cleaning, with purity thresholds measured in parts-per-trillion. Industrial gases industry players offer on-site gas cabinets, redundancy storage, and advanced leak detection to support fabs where downtime can cost USD 2 million per hour. Food and beverage end-markets stayed resilient, leveraging cryogenic freezing with liquid nitrogen and CO₂ to preserve texture and taste. Healthcare demand grew steadily as hospitals upgraded oxygen manifolds and specialty gas pharmacopoeias, further diversifying the customer mix.

Geography Analysis

Asia accounted for a dominant 42.55% share of the industrial gases market size in 2025, driven by strong petrochemical, ferrous metallurgy, and electronics clusters. China’s integrated steel capacity and India’s robust infrastructure spending jointly supported more than 600 t/d of new ASU capacity additions last year. Regional governments are promoting carbon capture pilots and green-hydrogen export corridors, aligning industrial gas flows with net-zero roadmaps. The competitive terrain features joint ventures between global majors and domestic firms that localize production while retaining world-scale engineering standards.

North America, characterized by mature pipelines supplying Gulf Coast refineries and adaptable merchant-liquid networks serving the Midwest and Northeast, demonstrates significant volume in the market. Purchases of hydrogen by U.S. refiners rose 29% between 2012 and 2022, illustrating a gradual shift from captive reformers to outsourced supply. Ongoing inflation-reduction incentives for clean-energy projects are catalyzing low-carbon ammonia, sustainable aviation fuel, and CO₂ sequestration ventures, each requiring dedicated industrial gas inputs. Canada is emerging as a niche helium hub, adding redundancy to a market long dominated by the U.S. Bureau of Land Management’s storage system.

Europe remains a value-added epicenter, focusing on green-hydrogen corridors and food-grade carbon capture. Air Liquide, Linde, and others are synchronizing renewable power purchase agreements with proton-exchange membrane electrolyzers to support maritime shipping and long-haul trucking decarbonization. Stricter F-gas regulation and methane thresholds are nudging refrigeration OEMs toward natural refrigerants, further diversifying gas portfolios in the region.

Competitive Landscape

The industrial gases market is highly consolidated. Linde reported USD 33 billion of sales and carried a record USD 10.4 billion project backlog, underscoring its capacity to self-fund multi-year decarbonization contracts. Air Liquide reaffirmed targets to cut carbon intensity by 30% by 2025 and achieve carbon neutrality by 2050, signaling a shift toward green-hydrogen, biomethane, and high-efficiency ASUs. Air Products doubled down on multi-gigawatt electrolysis projects in Saudi Arabia and Texas, betting that first-mover scale will unlock favorable long-run power tariffs.

Mid-tier players are carving regional niches by pairing localized cylinder distribution with merchant-bulk imports. These companies often adopt asset-light, build-own-operate models that conserve capital yet offer contractual stickiness. Technology partnerships are deepening across the value chain. Air Liquide’s turbo-Brayton technology for LNG boil-off management secured nearly 70 units of order intake by February 2025, validating cryogenic innovation in maritime transport. Proprietary membrane, adsorption, and liquefaction patents create high switching costs for customers and sustain return on invested capital for leading producers.

Industrial Gas Industry Leaders

Linde plc

Air Liquide

Air Products and Chemicals Inc.

Nippon Sanso Holdings Corporation

Messer SE & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Linde announced its achievement of its fifth consecutive year of record-breaking success in securing new small on-site projects for nitrogen and oxygen supply. In 2024, the company signed 59 long-term agreements to build, own, and operate 64 plants at customer locations.

- January 2025: Air Liquide has expanded its supply of low-carbon medical gases to hospitals across Europe and Brazil. This strategic move is expected to strengthen the company's position in the industrial gases market by addressing the growing demand for sustainable and environmentally friendly solutions.

Global Industrial Gas Market Report Scope

Industrial gases mainly comprise carbon dioxide, carbon monoxide, hydrogen, argon, nitrogen, oxygen, helium, and krypton-xenon. The atmospheric gases like oxygen, nitrogen, and argon are captured by reducing the air temperature until the components are liquified and separated. The industrial gas market is segmented by product type, end-user industry, and geography. The market is segmented by product type into nitrogen, oxygen, carbon dioxide, hydrogen, helium, argon, ammonia, methane, propane, butane, and other types. The end-user industry segments the market into chemical processing and refining, electronics, food and beverage, oil and gas, metal manufacturing and fabrication, medical and pharmaceutical, automotive and transportation, energy and power, and other end-user industries. The report also covers the market size and forecasts for the industrial gas market in 17 countries across major regions. Each segment's market sizing and forecasts are based on volume (tons).

By Product Type

| Nitrogen |

| Oxygen |

| Carbon Dioxide |

| Hydrogen |

| Helium |

| Argon |

| Ammonia |

| Methane |

| Propane |

| Butane |

| Other Product Types |

By Mode of Supply

| Packaged/Cylinder |

| Merchant Bulk Liquid |

| On-Site (Tonnage) Generation |

By End-user Industry

| Chemical Processing and Refining |

| Electronics and Semiconductor |

| Food and Beverage Processing |

| Oil and Gas |

| Metal Production and Fabrication |

| Medical and Pharmaceutical |

| Automotive and Transportation |

| Energy and Power Generation |

| Other Industries (Aerospce and water and waste Water Treatment) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Nordics | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Nitrogen | |

| Oxygen | ||

| Carbon Dioxide | ||

| Hydrogen | ||

| Helium | ||

| Argon | ||

| Ammonia | ||

| Methane | ||

| Propane | ||

| Butane | ||

| Other Product Types | ||

| By Mode of Supply | Packaged/Cylinder | |

| Merchant Bulk Liquid | ||

| On-Site (Tonnage) Generation | ||

| By End-user Industry | Chemical Processing and Refining | |

| Electronics and Semiconductor | ||

| Food and Beverage Processing | ||

| Oil and Gas | ||

| Metal Production and Fabrication | ||

| Medical and Pharmaceutical | ||

| Automotive and Transportation | ||

| Energy and Power Generation | ||

| Other Industries (Aerospce and water and waste Water Treatment) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current industrial gases market size and projected growth?

The market stands at 1.81 billion tons in 2026 and is expected to reach 2.21 billion tons by 2031, growing at a 4.03 % CAGR.

Which product leads the industrial gases industry?

Oxygen leads with a 31.65% market share because of its extensive use in steelmaking, healthcare, and chemical processing.

Why is on-site generation gaining traction?

On-site plants lower logistics costs, enhance supply security, and align with decarbonisation objectives for energy-intensive users.

How are green-hydrogen projects impacting the market?

They are creating demand for electrolyser-based hydrogen and associated oxygen streams, prompting suppliers to develop integrated low-carbon solutions.

Which region holds the largest industrial gases market share?

Asia leads with a 42.55% share, supported by rapid industrialisation, infrastructure development, and expanding manufacturing capacity.

Page last updated on: