High Pressure Seals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

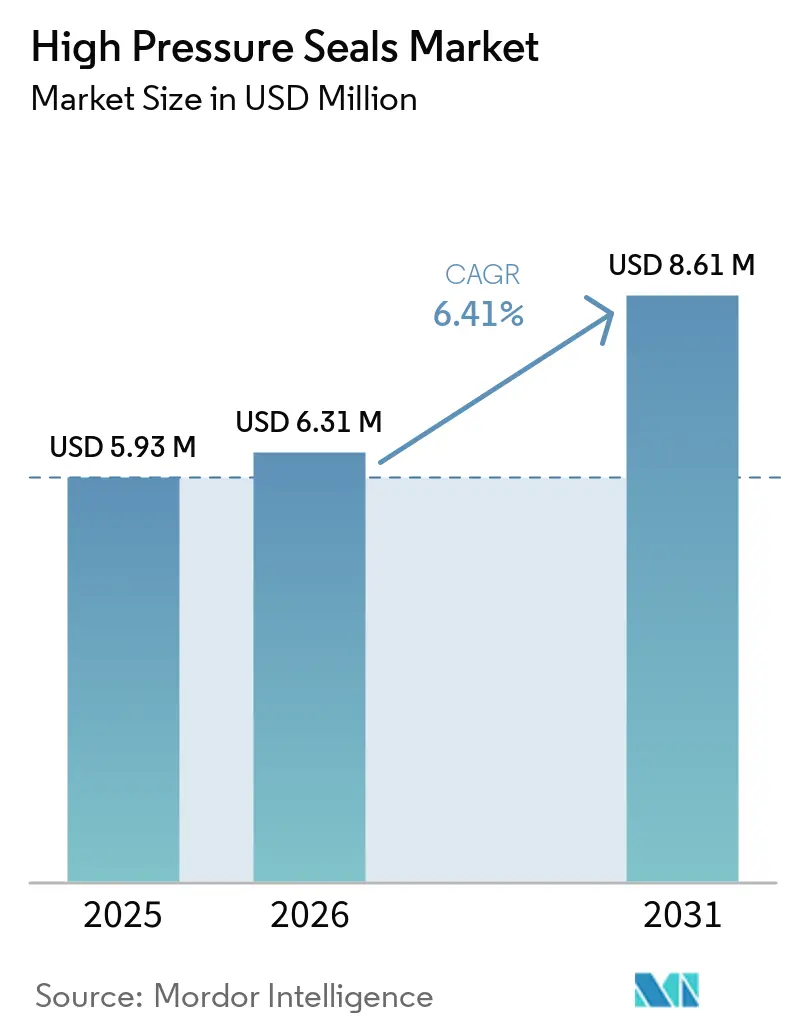

| Market Size (2026) | USD 6.31 Million |

| Market Size (2031) | USD 8.61 Million |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Pressure Seals Market Analysis by Mordor Intelligence

The High Pressure Seals Market size is expected to grow from USD 5.93 million in 2025 to USD 6.31 million in 2026 and is forecast to reach USD 8.61 million by 2031 at 6.41% CAGR over 2026-2031. Hydrogen refueling stations, geothermal well completions, and ultra-high-pressure water-jet systems are driving changes in sealing specifications, leading to increased demand. Investments in 700-bar and 950-bar hydrogen compression cascades, along with metal-centric seal architectures for Enhanced Geothermal Systems (EGS), are raising material requirements beyond traditional elastomers. Manufacturers are utilizing polyether ether ketone (PEEK), carbon-fiber-reinforced polytetrafluoroethylene (PTFE), and spring-energized metal designs capable of withstanding rapid gas decompression and temperatures exceeding 250°C. Additionally, capacity expansions in mega-petrochemical complexes, particularly in the Asia-Pacific region, are focusing procurement on higher-value, American Petroleum Institute (API)-qualified seals.

Key Report Takeaways

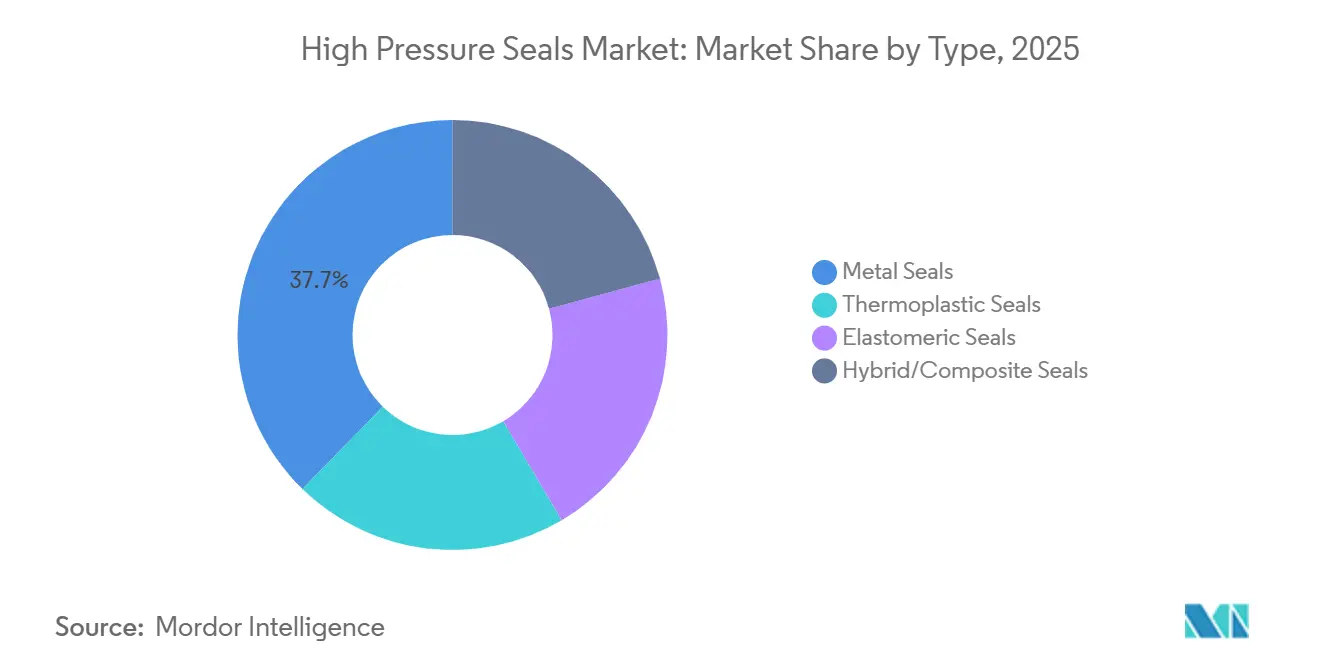

- By type, metal seals led with 37.71% of the high pressure seals market share in 2025, and hybrid/composite seals are advancing at 6.82% through 2031.

- By material, fluoro-elastomers (FKM/FPM) led with 33.31% of the high pressure seals market share in 2025, and other material types are advancing at 6.91% through 2031.

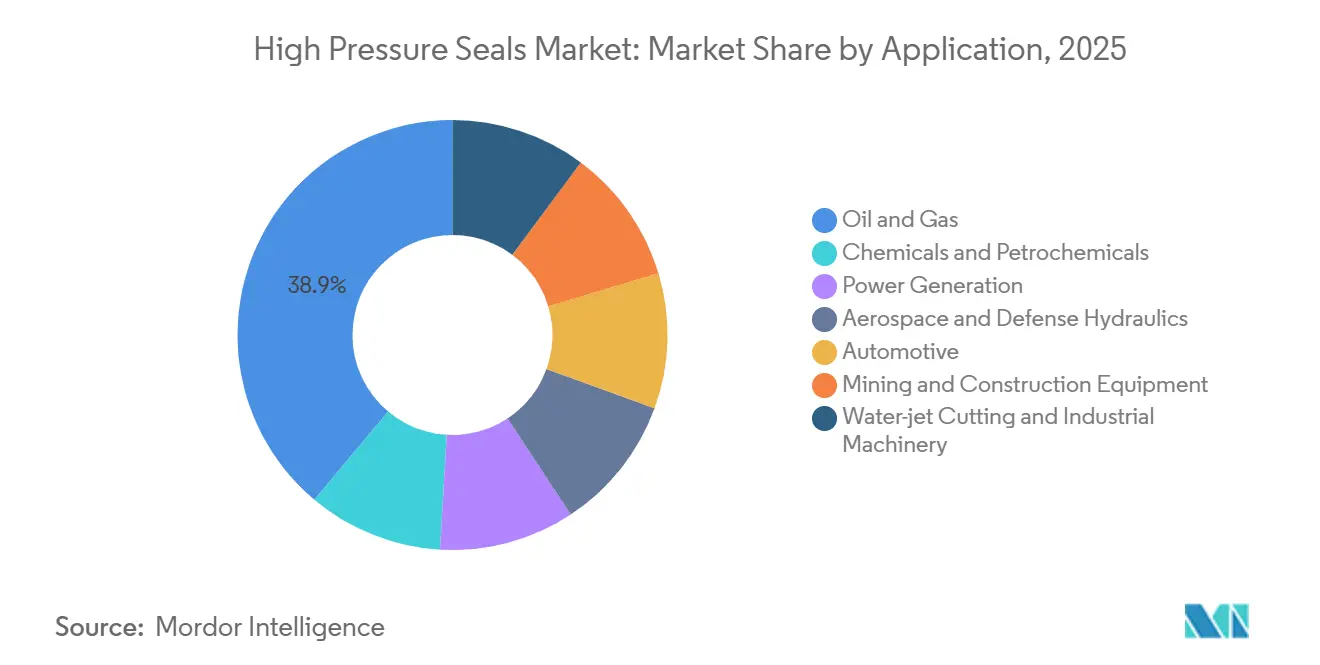

- By application, Oil and Gas led with 38.89% of the high pressure seals market share in 2025, and power generation is advancing at 7.22% through 2031.

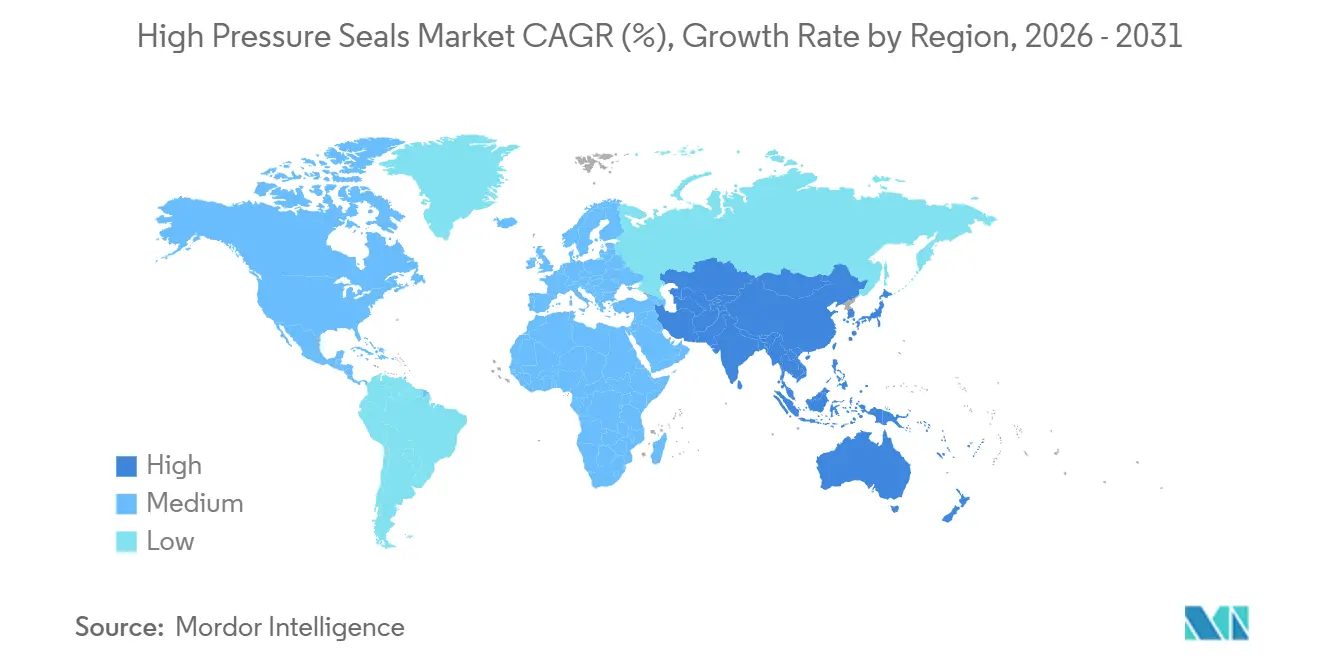

- By geography, Asia-Pacific captured 42.22% of 2025 revenue and is advancing at a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Pressure Seals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capacity additions in chemical and petrochemical mega-complexes | +1.2% | Global, with concentration in Middle East, China, and US Gulf Coast | Medium term (2-4 years) |

| Hydrogen pipeline and refueling infrastructure build-out | +1.5% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Rising adoption of ultra-high-pressure water-jet cutting in Electric Vehicle and electronics | +0.9% | APAC core (China, Japan, South Korea), spill-over to North America and Europe | Short term (≤ 2 years) |

| Geothermal EGS well completions | +0.7% | United States (Utah, Nevada), Iceland, Indonesia, Kenya | Long term (≥ 4 years) |

| Micro-fluidic and lab-on-chip miniaturized HP systems | +0.4% | North America, Europe, select APAC research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capacity Additions in Chemical and Petrochemical Mega-Complexes

Integrated refinery-petrochemical sites are commissioning single-train ethylene crackers with capacities exceeding 1.5 million tons per year (tpy). These crackers are designed to seal in corrosive, high-pressure hydrocarbon and steam services. Sealmatic India secured a USD 1.8 million contract, delivering 247 API 682 mechanical seals to the Mongol Refinery. These seals, equipped with dual pressurization chambers and silicon-carbide faces, are engineered to reduce fugitive emissions. Additionally, supplier qualifications under NACE MR0175 and ISO 21049 increase switching costs, supporting premium pricing for compliant vendors.

Hydrogen Pipeline and Refueling Infrastructure Build-Out

Germany has approved a 9,040 km hydrogen core network, while North America is actively deploying stations. This development is driving orders for 700-bar dispensers and 950-bar storage seals. Compounds like Greene Tweed’s Fusion 938 fluoro-elastomer and Arlon 3000XT polyetheretherketone (PEEK) are rated for rapid gas decompression at duty cycles of –40°C to +85°C. This capability helps mitigate the risk of seal failures during rapid fills.[1]Flow Control Network, “Hydrogen Refueling Station Equipment and Components,” flowcontrolnetwork.com

Rising Adoption of Ultra-High-Pressure Water-Jet Cutting in EV and Electronics

Battery-cover plants and printed circuit board (PCB) production lines are integrating pumps operating between 60,000 pounds per square inch (PSI) to 90,000 PSI. These pumps require polytetrafluoroethylene (PTFE) primary seals, complemented by ultra-high-molecular-weight polyethylene (UHMW-PE) rings, to prevent extrusion over numerous cycles. KMT’s Streamline PRO, capable of delivering 90,000 PSI, utilizes ceramic plungers sealed for 95% uptime in mass production[2]KMT Waterjet, “Waterjet Products – Pumps,” kmtwaterjet.com. As the industry transitions from job-shop to high-volume manufacturing, there is an increase in the demand for premium seal kits.

Geothermal EGS Well Completions

Fervo Energy’s Cape Station is targeting injections at 950 bar and 291°C. To achieve this, they have opted for spring-energized metal C-rings and graphite composites, avoiding elastomers. Meanwhile, Utah FORGE’s field program has validated multi-stage fracturing below 220°C, emphasizing the demand for American Society of Mechanical Engineers (ASME) Section III-qualified seals.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance degradation greater than 250°C under cyclic thermal shock | -0.8% | Global, particularly in geothermal, nuclear, and advanced aerospace applications | Short term (≤ 2 years) |

| Proliferation of low-cost regional manufacturers | -1.1% | APAC core (China, India, Southeast Asia), spill-over to the Middle East and Africa | Medium term (2-4 years) |

| Design standardization curbing custom HP seal demand | -0.6% | Global, with the strongest effect in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Performance Degradation Greater Than 250°C Under Cyclic Thermal Shock

Elastomers experience accelerated compression set when subjected to thermal cycling above 250°C. While nitrile starts to degrade at 207°C, only polytetrafluoroethylene (PTFE) and graphite composites can endure exposures of up to 500°C without any mass loss. As a result, enhanced geothermal systems (EGS) and supercritical carbon dioxide (CO₂) turbines utilize metallic or ceramic-filled polyether ether ketone (PEEK) seals, increasing capital expenditures and influencing volume growth in high-temperature applications.

Proliferation of Low-Cost Regional Manufacturers

Lepu Seal, operating a 40,000 square meter automated facility in China, dispatches over 5,000 American Petroleum Institute (API) 682 Category 3 dry-gas seals each month, pricing them 30% lower than their Western counterparts. This pricing strategy impacts margins for commodity O-rings. In 2024, Indian manufacturers expanded their capacity by 65%, intensifying price competition in the Asia-Pacific region. Additionally, original equipment manufacturers (OEMs) mandating dual sourcing are contributing to this competitive trend.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Metal Dominance Meets Composite Innovation

Metal Seals accounted for 37.71% of 2025 revenue, driven by demand from subsea oil completions and aerospace hydraulics requiring robust, explosive-decompression-resistant designs. Hybrid/Composite products are projected to grow at the fastest 6.82% compound annual growth rate (CAGR), combining polyether ether ketone (PEEK) backup rings with fluoroelastomer (FKM) primaries to prevent extrusion in 5,000 pounds per square inch (PSI) mining hydraulics.

Designers are incorporating metal bellows, carbon fiber, and fluoroelastomers to achieve a balance between flexibility and thermal stability. Aerospace actuators on the Bell Future Long-Range Assault Aircraft (FLRAA) military tiltrotor utilize such hybrids to maintain leak rates below 1 cubic centimeter per minute (cm³/min) at 3,000 PSI across a temperature range of –54°C to +135°C.

By Material: Fluoro-Elastomers Lead, PEEK Accelerates

Fluoroelastomers held a 33.31% share of 2025 revenue, supported by their chemical compatibility up to 204°C. Fusion 938 demonstrated durability through 10,000 thermal cycles between –40°C and +85°C in 700-bar hydrogen dispensers. Other Materials, primarily PEEK and ultra-high-molecular-weight polyethylene (UHMW-PE), are expected to grow at a 6.91% CAGR through 2031, driven by the adoption of thermoplastic seals that replace backup rings and reduce part counts in 250°C pumps.

Perfluoroelastomers address temperature requirements between 260°C and 325°C, making them suitable for advanced aerospace ducts. Additionally, ISMAT’s Vertex H 17 hydrogenated nitrile butadiene rubber (HNBR) reduces hydrogen permeation to below 0.5 cm³·mm/m²·day·bar across a temperature range of –46°C to +160°C.

By Application: Oil & Gas Anchors, Power Generation Surges

Oil and Gas accounted for 38.89% of 2025 demand, supported by subsea compression and refinery upgrades. The High Pressure Seals market share for Oil and Gas is anticipated to decline slightly, while power generation is forecast to grow at the highest 7.22% CAGR through 2031. This growth is attributed to the demand for metal and hybrid seals rated above 200 bar in supercritical carbon dioxide (CO₂) turbines and advanced modular reactors. Additionally, applications such as water-jet cutting, industrial machinery, and electric vehicle (EV) thermal management are driving demand for pumps rated between 60,000 PSI and 90,000 PSI.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 42.22% of global revenue and is projected to grow at a compound annual growth rate (CAGR) of 7.11% through 2031. China's supply base, featuring Lepu Seal's facility producing 5,000 dry-gas seals monthly, caters to liquefied natural gas (LNG) terminals in 68 countries. In India, a EUR 270 billion (USD 312.28 billion) manufacturing expansion has driven seal demand by approximately 7% annually. To address this increase, Sealmatic's newly established 25,000 ft² Kaman plant has increased its monthly output by 65%, focusing on nuclear and defense contracts.

North America benefits from the Permian Basin's upstream activities and is developing a hydrogen core network, which compresses gas for 700 bar dispensers. Meanwhile, a pilot project at Utah Frontier Observatory for Research in Geothermal Energy (FORGE) in the United States is increasing the demand for metallic packer elements rated at 1,000 bar.

Europe's growth is influenced by its established bases but is supported by initiatives such as Germany's hydrogen backbone, geothermal loops in Iceland, and life-extension programs for reactors in France. Contributions from South America and the Middle East & Africa include Brazilian pre-salt projects and expansions in Saudi petrochemicals, both requiring American Petroleum Institute (API)-qualified seals capable of handling 15,000 pounds per square inch (PSI) duties.

Competitive Landscape

The high pressure seals market remains moderately fragmented. Parker Hannifin, Freudenberg Sealing Technologies, and John Crane, leveraging global service hubs and Original Equipment Manufacturer (OEM) qualifications, collectively account for just over one-third of the global revenue. Parker Hannifin's aerospace expertise has secured contracts for hydraulic fuses on F-16 fighters and sealing systems for the Bell Future Long-Range Assault Aircraft (FLRAA) program. Meanwhile, John Crane's Type 8628VL, equipped with metal bellows to reduce liquid carryover, is designed for 1,100 PSI ethane pipelines.

Greene Tweed, Kalsi Engineering, and DLSEALS differentiate themselves with proprietary compounds, such as Fusion 938 and perfluoroelastomer blends, effectively addressing the 260°C-325°C temperature range. Additionally, Chinese and Indian companies like Lepu Seal and Sealmatic, leveraging cost efficiencies, now meet standards such as API 682 Category 3 and ISO 9001, gradually increasing their presence in commodity categories.

Technological advancements are benefiting vendors who combine finite-element analysis with additive manufacturing, enabling rapid iterations of complex hybrid geometries. Moreover, service contracts ensuring uptime for hydrogen compressors and Enhanced Geothermal Systems (EGS) wells are emerging as significant profit opportunities, offsetting margin pressures in standard O-rings.

High Pressure Seals Industry Leaders

John Crane

Flowserve Corporation

Trelleborg Group

Freudenberg Sealing Technologies

PARKER HANNIFIN

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Baker Hughes has agreed to acquire Chart Industries for USD 13.6 billion. This acquisition aims to strengthen Baker Hughes' presence in liquefied natural gas (LNG), hydrogen, and carbon-capture systems. These systems rely on advanced high-pressure seals, which are critical for ensuring operational efficiency and safety in handling high-pressure environments.

- January 2025: Diploma PLC has completed acquisitions worth EUR 130 million (USD 150.35 million) to strengthen its portfolio in aerospace and nuclear sealing applications, particularly focusing on high-pressure seals. These acquisitions aim to enhance the company's capabilities in delivering advanced sealing solutions for demanding environments.

Global High Pressure Seals Market Report Scope

High pressure seals, made from materials such as ceramic, tungsten carbide, and polytetrafluoroethylene (PTFE), are essential in industries like oil and gas, hydraulic systems, and pumps. These seals prevent fluid or gas leaks in high-pressure environments and maintain system integrity by withstanding significant forces, often managing pressures that exceed standard thresholds.

The high pressure seals market is segmented by type, material, application, and geography. By type, the market is segmented into metal seals, thermoplastic seals, elastomeric seals, and hybrid/composite seals. By material, the market is segmented into hydrogenated nitrile butadiene rubber (HNBR), fluoro-elastomers (FKM/FPM), ethylene propylene diene monomer (EPDM), polytetrafluoroethylene (PTFE) and blends, and other material types (polyether ether ketone (PEEK), etc.). By application, the market is segmented into oil and gas, chemicals and petrochemicals, power generation, aerospace and defense hydraulics, automotive, mining and construction equipment, and water-jet cutting and industrial machinery. The report also covers the market size and forecasts for high pressure seals in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Metal Seals |

| Thermoplastic Seals |

| Elastomeric Seals |

| Hybrid/Composite Seals |

| Hydrogenated Nitrile Butadiene Rubber (HNBR) |

| Fluoro-elastomers (FKM/FPM) |

| Ethylene Propylene Diene Monomer (EPDM) |

| Polytetrafluoroethylene (PTFE) and blends |

| Other Material Types (Polyether ether ketone (PEEK), etc.) |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Power Generation |

| Aerospace and Defense Hydraulics |

| Automotive |

| Mining and Construction Equipment |

| Water-jet Cutting and Industrial Machinery |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Metal Seals | |

| Thermoplastic Seals | ||

| Elastomeric Seals | ||

| Hybrid/Composite Seals | ||

| By Material | Hydrogenated Nitrile Butadiene Rubber (HNBR) | |

| Fluoro-elastomers (FKM/FPM) | ||

| Ethylene Propylene Diene Monomer (EPDM) | ||

| Polytetrafluoroethylene (PTFE) and blends | ||

| Other Material Types (Polyether ether ketone (PEEK), etc.) | ||

| By Application | Oil and Gas | |

| Chemicals and Petrochemicals | ||

| Power Generation | ||

| Aerospace and Defense Hydraulics | ||

| Automotive | ||

| Mining and Construction Equipment | ||

| Water-jet Cutting and Industrial Machinery | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for the High Pressure Seals market between 2026 and 2031?

The High Pressure Seals Market size is expected to increase from USD 5.93 million in 2025 to USD 6.31 million in 2026 and reach USD 8.61 million by 2031, growing at a CAGR of 6.41% over 2026-2031.

Which segment grows fastest in material terms?

Hybrid/Composite seals, combining PEEK and elastomer elements, are set to grow at 6.82% CAGR through 2031.

Why is Asia-Pacific expanding quicker than other regions?

Vertically integrated supply chains in China and capacity additions in India’s manufacturing base drive a 7.11% CAGR for Asia-Pacific.

How do hydrogen refueling stations influence seal design?

700-bar dispensers and 950-bar storage banks require materials such as fluoro-elastomers and PEEK that resist rapid gas decompression and maintain integrity at -40°C to +85°C.

Page last updated on: