Mechanical Seals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.97 Billion |

| Market Size (2031) | USD 9.97 Billion |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mechanical Seals Market Analysis by Mordor Intelligence

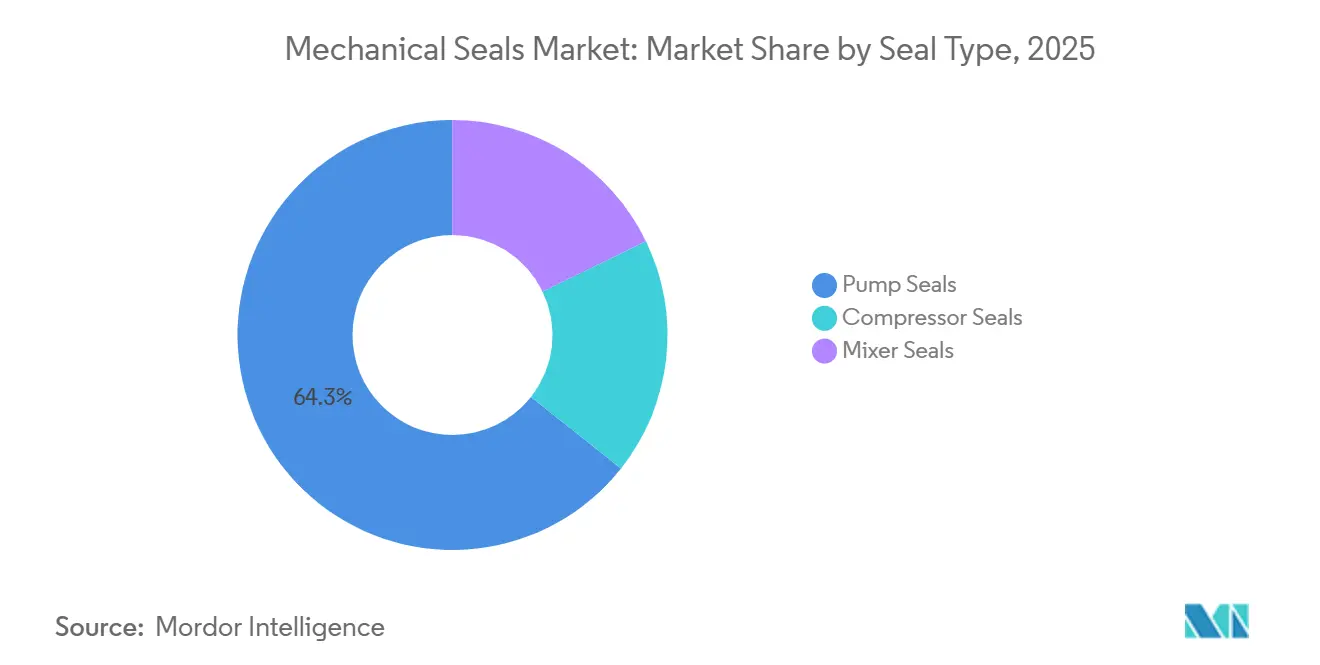

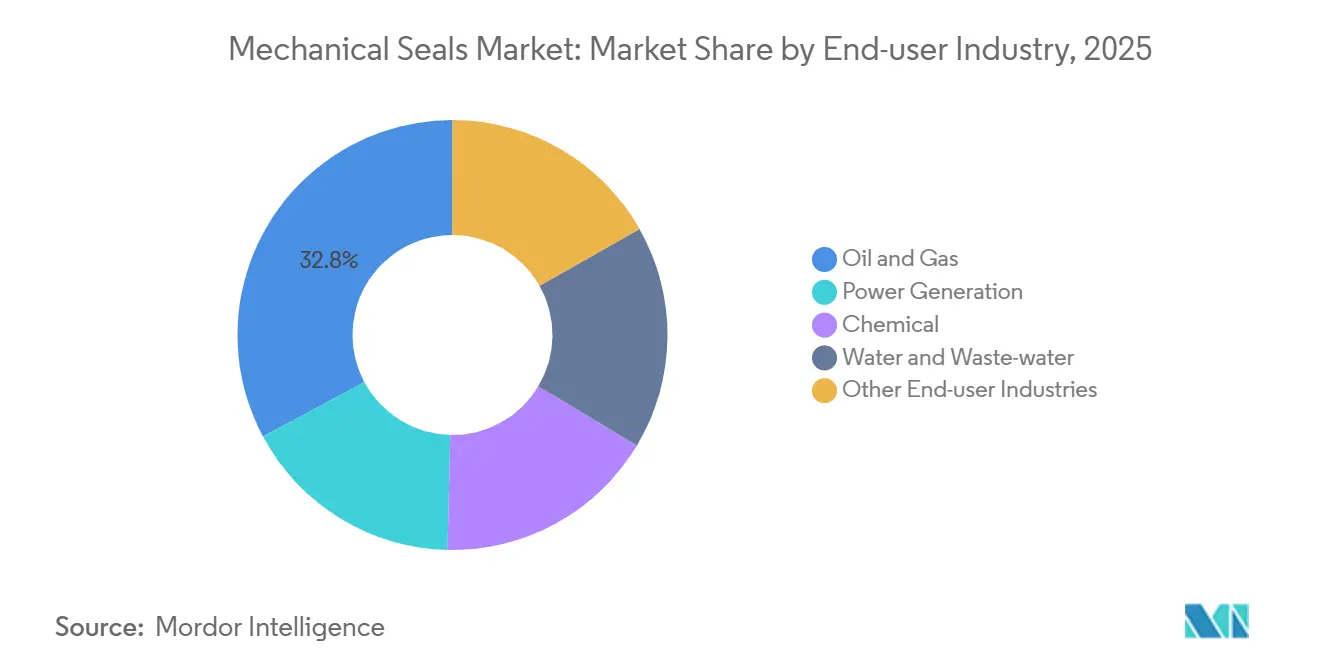

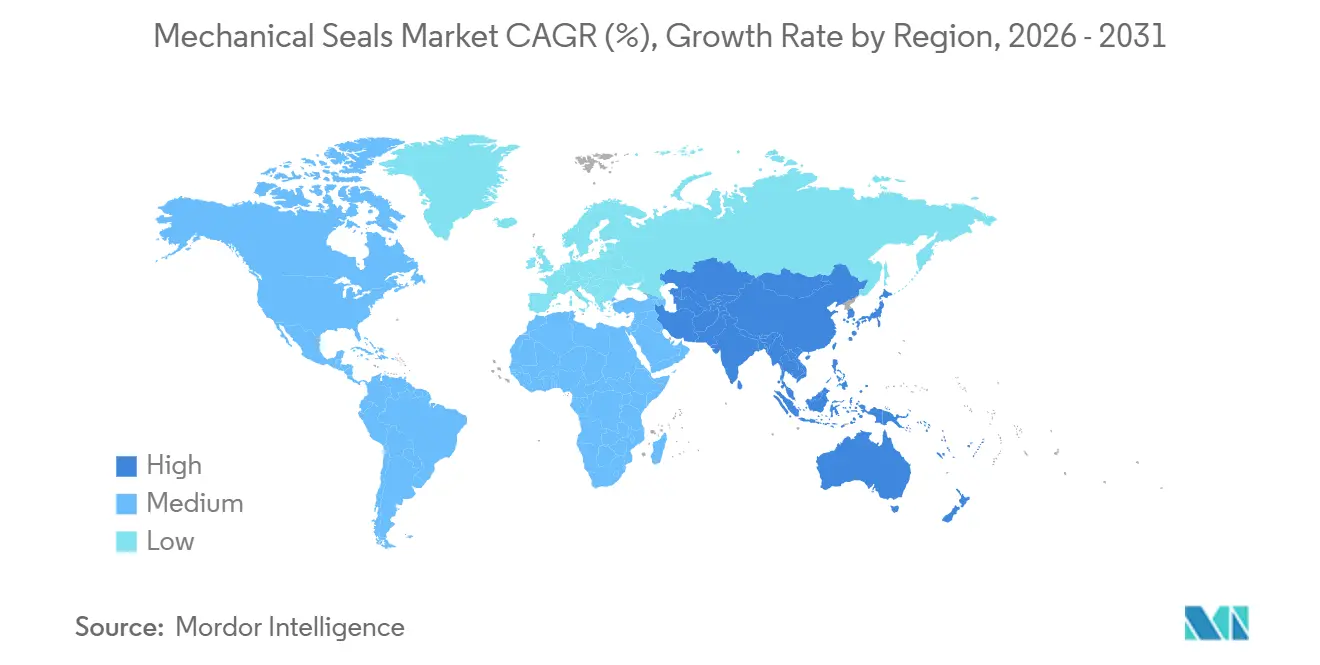

The Mechanical Seals Market size is expected to grow from USD 7.62 billion in 2025 to USD 7.97 billion in 2026 and is forecast to reach USD 9.97 billion by 2031 at a 4.58% CAGR over 2026-2031. Demand remains anchored in pumps and compressors, yet the mechanical seals market is splitting into high-volume commodity products that face price pressure from seal-less alternatives and premium engineered solutions that capture double-digit margins in hydrogen, super-critical carbon dioxide, and cryogenic services. Pump seals represented 64.35% of 2025 revenue, a share underwritten by the vast centrifugal pump installed base. Power-generation users form the fastest-growing customer group at a projected 4.88% CAGR because utilities are retrofitting turbines and commissioning hybrid plants that require advanced dry-gas seals. Asia-Pacific commanded 36.35% of the mechanical seals market share in 2025 and is set to grow at a 4.68% CAGR as China and India expand refining, petrochemical, and power assets.

Key Report Takeaways

- By seal type, pump seals commanded 64.35% of the mechanical seals market share in 2025, and are advancing at 4.56% through 2031.

- By design, cartridge seals held 43.61% of the mechanical seals market size in 2025, and Component/Pusher is advancing at 4.62% through 2031.

- By end-user, oil and gas accounted for 32.83% of the mechanical seals market size in 2025, while power generation is advancing at a 4.88% CAGR through 2031.

- By geography, Asia-Pacific generated 36.35% of the mechanical seals market revenue in 2025, expanding at a 4.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mechanical Seals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from oil and gas megaprojects | +1.2% | Middle East, Asia-Pacific (China, India), North America (US Gulf Coast LNG) | Medium term (2-4 years) |

| Surge in new power-generation capacity additions | +1.0% | Global, with concentration in Asia-Pacific (China, India) and Middle East | Medium term (2-4 years) |

| Tightening fugitive-emission regulations worldwide | +0.9% | North America, Europe; spillover to Asia-Pacific and Middle East by 2028-2030 | Long term (≥ 4 years) |

| Capacity expansion in chemical and petrochemical complexes | +0.8% | Middle East (Saudi Arabia, UAE), Asia-Pacific (China, India, South Korea) | Medium term (2-4 years) |

| Hydrogen and green-ammonia cryogenic infrastructure build-out | +0.6% | Europe, North America, Australia; early-stage in Middle East and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Oil and Gas Megaprojects

Saudi Arabia's push into downstream operations highlights a shift in seal requirements driven by crude-to-chemicals integration. Aramco's Amiral complex, set to commence operations in 2027, will demand premium seals for its mixed-feed crackers and high-pressure hydrocarbon pumps. Suppliers are now tasked with providing materials resilient to extreme temperatures and corrosive petrochemical streams. John Crane's Type 8628VL non-contacting spiral-groove seal boasts an extended mean time between repairs while significantly reducing flush demand. Such large-scale projects lean towards upfront investments in advanced technology, promising lifecycle savings, and putting pressure on vendors still dependent on traditional wet-seal lines.

Surge in New Power-Generation Capacity Additions

Worldwide installations of gas turbines, nuclear reactors, and hybrid renewables are on the rise. Yet, the primary demand for seals is concentrated in auxiliary feed-water pumps, cooling circuits, and steam turbines. A retrofit of AESSEAL’s STS steam turbine seal at a refinery in the UK resulted in significant steam savings annually per unit. This upgrade extended the turbine's lifespan, translating to impressive annual fleet savings. As grids increasingly incorporate intermittent renewables, combined-cycle turbines are set to cycle more frequently. This heightened activity accelerates seal wear, leading to a surge in aftermarket volumes. On the horizon, while modular nuclear concepts and closed-loop cooling might reduce the number of dynamic sealing points, tempering growth in the very long term, the immediate future looks robust.

Tightening Fugitive-Emission Regulations Worldwide

In December 2023, the U.S. EPA imposed methane leakage limits for wet-seal compressors and dry-seal ones[1]U.S. Environmental Protection Agency, “EPA’s Final Rule to Reduce Methane and Other Pollution from Oil and Natural Gas Operations,” epa.gov. To comply, operators must upgrade their seals and implement new monitoring protocols. Entering the fray in June 2025, John Crane unveiled its Type 93AX coaxial separation seal. This innovative seal slashes nitrogen usage and maintains integrity, making it a prime choice for operators grappling with leakage and resilience challenges. While Europe aligns with U.S. standards, the Asia-Pacific region lags behind. This delay permits the continued use of cost-effective, high-leak designs until local regulations become more stringent.

Capacity Expansion in Chemical and Petrochemical Complexes

Saudi petrochemical revenue exceeded expectations in 2025, and announced projects will nearly double capacity within five years. Commodity crackers favor standardized cartridge seals, whereas specialty plants demand customized solutions for corrosive or high-purity streams. Suppliers with regional service hubs enjoy margin upside by offering rapid response and engineered variants, whereas centralized producers face freight penalties and longer lead times.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High life-cycle cost in abrasive slurry services | -0.5% | Global, with concentration in mining (Australia, Latin America, Africa) and pulp and paper (North America, Scandinavia) | Short term (≤ 2 years) |

| Seal-less mag-drive and canned-motor pumps eroding addressable market | -0.7% | North America, Europe; expanding to Asia-Pacific chemical and pharmaceutical sectors | Medium term (2-4 years) |

| SiC face-material price volatility and supply-chain risk | -0.4% | Global, with acute impact on high-performance seal manufacturers sourcing from limited SiC wafer suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Life-Cycle Cost in Abrasive Slurry Services

Mining and pulp operators frequently opt for packed glands or expeller devices, shunning the premium on slurry seals. Their choice underscores a preference for inventory simplicity over longevity. Meanwhile, John Crane's SB2 dual-cartridge technology, which eliminates the need for an external flush and extends service life, sees its field adoption largely dependent on bundled technical support and performance guarantees. These assurances aim to counterbalance the initial investment. Vendors who solely push products without added services find themselves sidelined in abrasive tasks.

Seal-Less Mag-Drive and Canned-Motor Pumps Eroding Addressable Market

Mag-drive units, priced at a premium over single-seal pumps, sidestep the need for dual-seal support systems and mitigate leak risks[2]American Fuel & Petrochemical Manufacturers, “Question 73: Criteria to Justify Seal-Less Pumps,” afpm.org. This advantage has helped them capture a significant share in services like LPG, alkylate, and acid reruns. While these units can face failures due to sludge blockages or magnet demagnetization, such challenges simultaneously create opportunities for premium mechanical seals. These seals are particularly sought after in applications prone to high temperatures, solid blockages, or dry runs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Seal Type: Pump Seals Maintain Dominance while Dry-Gas Variants Gain Traction

Pump seals generated 64.35% revenue in 2025 and will track a 4.56% CAGR to 2031. Retrofits into existing centrifugal pumps underpin stable aftermarket sales, but the installed base is vulnerable to seal-less migration in clean chemical services. Non-contacting spiral-groove designs and upstream-pumping faces now headline innovation, allowing suppliers to frame upgrades around energy savings and emissions compliance. Compressor seals, though lower in volume, achieve higher average selling prices via technical complexity and rising regulatory enforcement. Mixer seals remain niche yet mission-critical in hygiene-sensitive reactors, sustaining premium margins.

While the mechanical seals market size for pump applications will expand steadily, competitive intensity is sharpening as Asian manufacturers offer low-cost contact-face cartridges. Established brands differentiate through digital diagnostics, performance warranties, and rapid local service.

By Design Type: Cartridge Convenience vs. Field-Service Flexibility

Cartridge designs held 43.61% revenue share in 2025, valued for alignment accuracy and quick change-outs during turnarounds. However, component seals are on pace for a 4.62% CAGR because remote mines and pulp mills favor rebuildable assemblies that cut downtime and inventory. Split seals, though small in number, command hefty premiums when equipment teardown is impractical, such as large pipeline pumps.

As digitalization reshapes the landscape, sensor-equipped cartridges are now streaming data to cloud platforms. Vendors who overlook the importance of data services may find themselves trapped in a relentless price competition. However, there's a silver lining: independent sensor retrofits offer component-seal specialists a viable route to maintain their significance in the evolving market.

By End-User Industry: Power Generation Surges as Oil-and-Gas Share Slides

Oil and gas remained the largest buyer at 32.83% in 2025, but seal-less migration and upstream capex cuts trim its future slice. Power producers lead growth at 4.88% CAGR, spurred by turbine retrofits and auxiliary equipment in gas-fired, nuclear, and renewable plants. Chemical complexes are split between standardized cartridge seals for bulk ethylene and engineered variants for corrosive specialties. Water and wastewater utilities steadily convert packed glands to mechanical designs to conserve water, albeit at commoditized pricing. Mining enjoys episodic windfalls tied to battery-metal booms; suppliers with modular platforms adaptable across sectors buffer such cyclicality.

Geography Analysis

Asia-Pacific captured 36.35% of the mechanical seals market revenue in 2025 and is projected to post the fastest 4.68% CAGR through 2031. China's expansions in refining, petrochemicals, and power sectors drive a significant demand. Additionally, China's leadership in electrolyser manufacturing has spurred an early adoption of hydrogen-ready seals. Following closely, India is ramping up its refinery and water infrastructure projects. However, due to price sensitivities, the standard pump business is leaning towards domestic producers. Meanwhile, Japan and South Korea, despite their smaller size, are investing in high-performance seals for LNG and semiconductor applications, carving out premium-margin niches.

North America commanded a notable market share in 2025. The EPA's methane regulations are driving retrofits of dry-gas seals throughout the Gulf Coast's midstream network. Capital orders are bolstered by LNG export terminals and petrochemical debottlenecks, while an aging installed base ensures stability in the aftermarket. In Canada, duties on oil sands are pushing the demand for abrasion-resistant dual seals, yet delays in pipeline projects introduce volatility in capital expenditures.

Europe represented a considerable portion of the market value. Projects focused on energy transition—like carbon capture, hydrogen electrolysers, and offshore wind—are fostering growth, though progress is often slowed by permitting delays. Germany and the UK are taking the lead in hydrogen pipelines, yet the bulk of revenues from 2026 to 2028 are anticipated to stem from upgrades in industrial gas and specialty chemicals. While the Middle East and Africa hold a smaller market share, they are involved in some of the industry's largest projects. Notable undertakings include Saudi Arabia's push from crude to chemicals, ADNOC's venture in carbon capture and storage, and South Africa's mining sector—all of which demand hundreds of seals per project. However, suppliers face challenges with longer logistics routes and extended receivables.

Competitive Landscape

The mechanical seals market is moderately consolidated. Technology leadership is the key moat. John Crane’s Performance Plus service suite, launched in November 2025, bundles remote monitoring, analytics, and guaranteed reliability contracts, positioning the firm as a performance partner rather than a component vendor. Vendors doubling down on hydrogen-compatible materials, non-contacting faces, and digital diagnostics command pricing power, whereas producers anchored in wet-seal portfolios face margin compression as customers opt for dry seals or eliminate seals.

Mechanical Seals Industry Leaders

John Crane

EagleBurgmann

Flowserve Corporation

AESSEAL

A.W. Chesterton Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Flowserve secured a dry-gas-seal order for ADNOC’s 1.5 million-tons-per-year carbon-capture project in the UAE, marking its largest CCS sealing award to date.

- August 2024: John Crane landed a five-year gas-seal management contract with SK Advanced in South Korea, encompassing maintenance during scheduled turnarounds.

Global Mechanical Seals Market Report Scope

Mechanical seals are devices that provide a seal at the point of entry or exit of a rotating shaft. Typically, it is used to prevent the leakage of one high-pressure fluid into a lower-pressure fluid.

The mechanical seals market is segmented by seal type, design type, end-user industry, and geography. By seal type, the market is segmented into pump seals, compressor seals, and mixer seals. By design type, the market is segmented into component/pusher, cartridge, and split. By end-user industry, the market is segmented into oil and gas, power generation, chemical, water and wastewater, and other end-user industries (mining and mineral processing, food, pharma, etc.). The report also covers the market sizes and forecasts in 16 countries. For each segment, the market sizing and forecasts were made based on revenue (USD).

| Pump Seals |

| Compressor Seals |

| Mixer Seals |

| Component/Pusher |

| Cartridge |

| Split |

| Oil and Gas |

| Power Generation |

| Chemical |

| Water and Waste-water |

| Other End-user Industries (Mining and Mineral Processing, Food, Pharma, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Seal Type | Pump Seals | |

| Compressor Seals | ||

| Mixer Seals | ||

| By Design Type | Component/Pusher | |

| Cartridge | ||

| Split | ||

| By End-user Industry | Oil and Gas | |

| Power Generation | ||

| Chemical | ||

| Water and Waste-water | ||

| Other End-user Industries (Mining and Mineral Processing, Food, Pharma, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the mechanical seals market expected to grow through 2031?

The mechanical seals market is projected to expand at a 4.58% CAGR from 2026 to 2031, rising from USD 7.97 billion in 2026 to USD 9.97 billion by 2031.

Which region leads demand for mechanical seals?

Asia-Pacific held 36.35% of global revenue in 2025 and will remain the largest, expanding at a forecast 4.68% CAGR thanks to large investments in refining, petrochemicals, and power.

What end-user segment offers the fastest growth outlook?

Power generation is forecast to post the highest 4.88% CAGR as utilities retrofit turbines and build new hybrid plants that rely on advanced dry-gas and steam-turbine seals.

How are seal-less pumps impacting mechanical seal suppliers?

Magnetic-drive and canned-motor pumps eliminate dynamic seals in many chemical and LPG services, trimming the addressable market and pushing seal vendors to focus on duties where high temperature, solids, or dry-run risk favor mechanical seals.

Why are silicon-carbide faces a supply concern?

Rising electric-vehicle and power-electronics demand extends SiC wafer lead times and inflates prices, forcing seal OEMs to secure long-term supply agreements or qualify alternate ceramics to protect margins.

Page last updated on: