Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

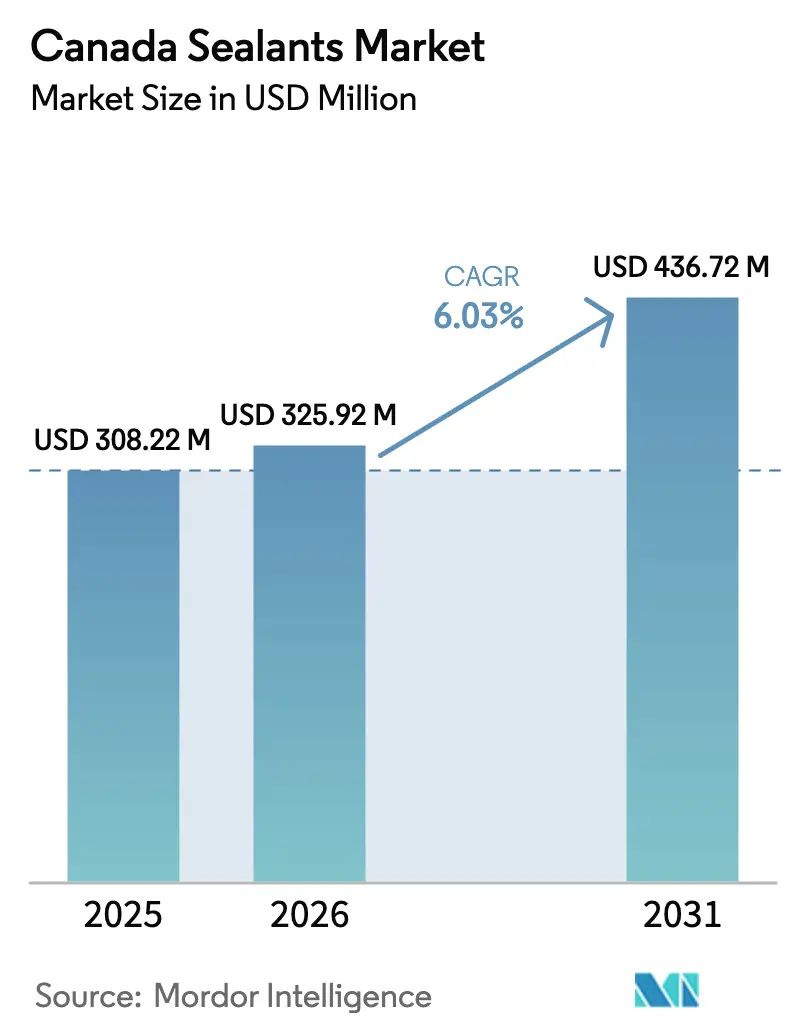

| Base Year Market Size (2025) | USD 308.22 Million |

| Market Size (2026) | USD 325.92 Million |

| Market Size (2031) | USD 436.72 Million |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Sealants Market Analysis by Mordor Intelligence

The Canada Sealants Market size is expected to grow from USD 308.22 million in 2025 to USD 325.92 million in 2026 and is forecast to reach USD 436.72 million by 2031 at 6.03% CAGR over 2026-2031. Federal infrastructure outlays, stricter volatile-organic-compound (VOC) rules, and the formation of electric-vehicle (EV) and aerospace clusters are reshaping product specifications, channel economics, and regional demand patterns. Ottawa’s USD 159 billion infrastructure pipeline for 2025-2030 is accelerating civil and institutional starts, while the January 2024 VOC limits have shifted share toward silicone and hybrid chemistries that innately meet the 10% w/w ceiling for acoustical sealants. Modular and panelized construction is expanding as contractors confront a shrinking skilled-trades pool, prompting greater reliance on factory-applied gaskets and heat-activated tapes.

Key Report Takeaways

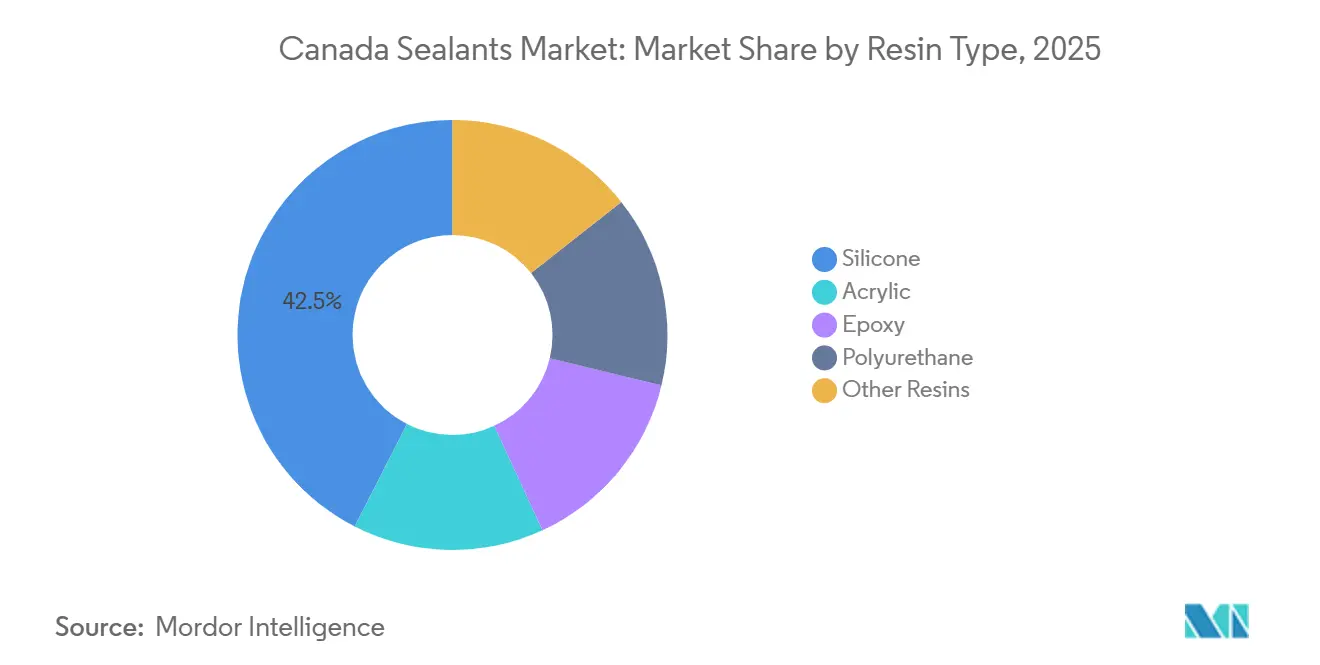

- By resin type, silicone formulations led with 42.50% of Canada sealants market share in 2025; polyurethane products are forecast to expand at a 7.34% CAGR through 2031.

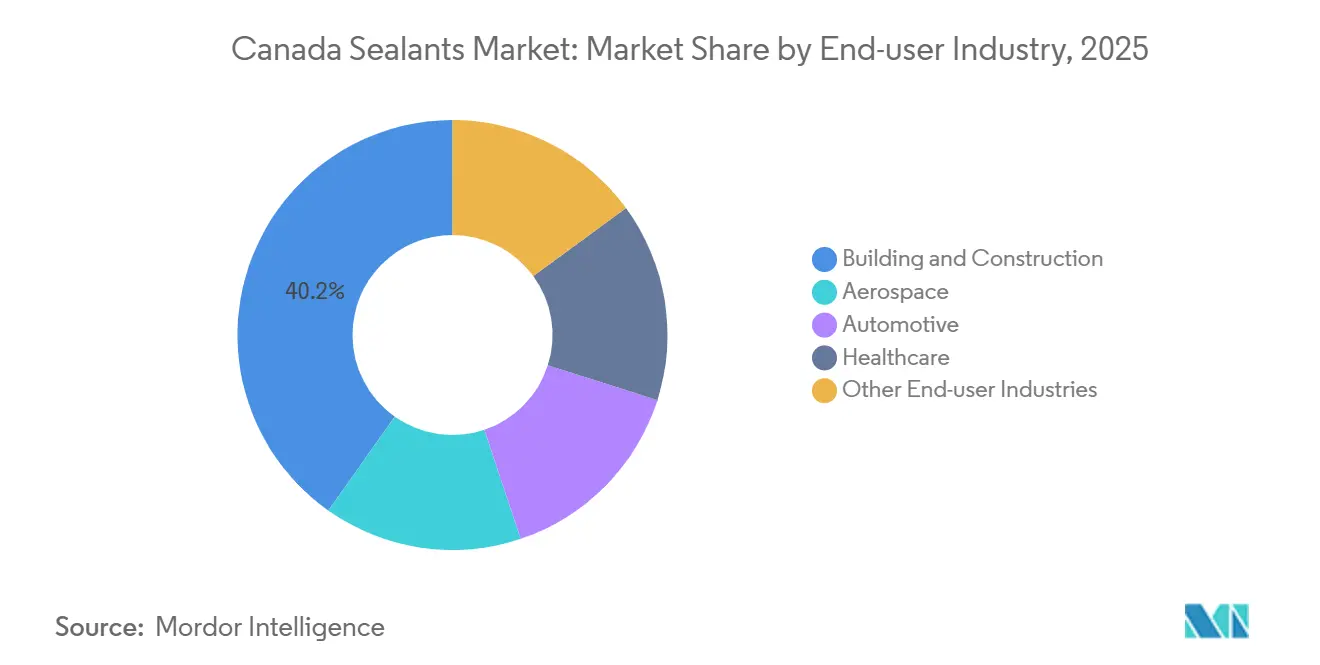

- By end-user industry, building and construction captured 40.20% of the Canada sealants market size in 2025, while healthcare is projected to advance at a 7.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Sealants Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation wave and energy-retrofit boom | +1.2% | British Columbia, Ontario, Quebec | Medium term (2-4 years) |

| Tightening VOC limits favoring silicone | +0.9% | National | Short term (≤ 2 years) |

| Federal infrastructure spend | +1.5% | National, Arctic and trade corridors | Long term (≥ 4 years) |

| Quebec composite-airframe cluster | +0.4% | Quebec with Ontario spillover | Medium term (2-4 years) |

| Ontario EV-battery gigafactories | +0.8% | Ontario with possible Quebec pull-through | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renovation Wave and Energy-Retrofit Boom

Deep retrofits targeting 50%-70% energy cuts are boosting demand for flexible expansion-joint sealants and vapor-tight air barriers. The Reframed Initiative in British Columbia logged energy reductions as high as 90% by integrating seismic upgrades, roof reinforcements, and additional floors, all of which require higher-spec sealing products. Provincial incentive programs lower upfront costs and favor factory-applied tapes that cure within 24 hours, helping modular housing deliver 25%-50% faster completion and up to 46% waste reduction.

Tightening VOC Limits Favoring Silicone and Hybrid Chemistries

The federal VOC regulations covering 130 product categories took effect in January 2024, trimming national emissions by an estimated 25 kilotons yearly[1]Government of Canada, “VOC Concentration Limits for Certain Products Regulations,” canada.ca. Compliance choices include reformulation or trading VOC compliance units, yet silicone and silane-modified polymers already meet the limits, sustaining their 42.50% share. Henkel’s Teroson MS 949 FR, commercialized in March 2026, illustrates the shift: it is tin-free, isocyanate-free, and cures in 30 minutes while satisfying EN 45545-2 flame-retardancy rules.

Federal Infrastructure Spend Under Investing in Canada

The Parliamentary Budget Officer expects USD 159 billion in federal infrastructure disbursements during 2025-2030, with Budget 2025 earmarking USD 115 billion for large projects. Transport Canada’s USD 5 billion Trade Diversification Corridors Fund and USD 1 billion Arctic Infrastructure Fund, launched in March 2026, focus on ports, bridges, and permafrost-prone corridors, spurring demand for low-temperature, salt-resistant industrial sealants[2]Transport Canada, “Trade Diversification Corridors Fund,” tc.canada.ca.

Quebec Composite-Airframe Cluster Needs Aerospace-Grade Sealants

More than 200 aerospace firms clustered around Montréal and Mirabel require sealants that pass Airbus ABD 031 and Boeing BSS 7238/7239 smoke-density standards. Fuel-tank and firewall applications lean on advanced polysulfide or silicone materials, while the active maintenance, repair, and overhaul segment pulls recurring quantities of quick-cure formulations.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicon-metal price volatility | –0.6% | National, silicone producers | Short term (≤ 2 years) |

| Price pressure from PU-hybrid alternatives | –0.4% | Construction, automotive | Medium term (2-4 years) |

| Labor shortage pushing pre-gasketed parts | –0.3% | British Columbia, Ontario, Quebec | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Silicon-Metal Price Volatility

Silicon metal faces renewed dumping risk if Canadian trade measures lapse, as the CBSA noted weighted-average Chinese subsidies of 21.1% in its 2024 sunset review. Feedstock instability complicates long-term contracts; Wacker Chemie has already announced a global silicone price increase effective April 2026 to offset energy and logistics inflation.

Price Pressure from PU-Hybrid Alternatives

Expanding North American MDI capacity, BASF will reach 600 kilotons a year in Geismar by 2026, supporting cost-competitive polyurethane sealants that challenge silicones in multi-substrate joints. Hybrids like Henkel’s Teroson MS 949 FR merge silicone-like elasticity with PU adhesion, compelling contractors to evaluate total installed cost rather than resin group loyalty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Leads on Regulatory Compliance

Silicone resins held 42.50% of Canada sealants market share in 2025 owing to inherent low-VOC emissions and superior UV and freeze-thaw durability. Polyurethane grades, particularly silane-terminated hybrids, are projected to grow at a 7.34% CAGR through 2031, outpacing the 6.03% Canada sealants market size CAGR as builders seek rapid skin-forming and primerless adhesion. Acrylics remain common in interior joints yet face cost and reformulation pressure after the 10% w/w VOC cap on small-package adhesives, a shift that could narrow their Canada sealants market share further. Epoxies and specialty resins such as polysulfides serve niche infrastructure and glazing needs where chemical or gas-barrier performance is critical.

Hybrid launches underscore the evolution. Henkel’s Teroson MS 949 FR and Dow’s DOWSIL EG-4175 Gel target rail and power-electronics users, respectively, with faster cure and higher thermal resistance than legacy blends, indicating how innovation supports Canada sealants market growth. BASF’s biogenic Acronal BC 5036 also shows that sustainability labeling is entering this resin category, aligning with public procurement criteria and further diversifying supplier offers.

By End-User Industry: Healthcare Fastest, Construction Largest

Building and construction captured 40.20% of the Canada sealants market size in 2025 because envelope sealing, joint filling, and glazing dominate volume. Healthcare is poised for the quickest expansion at 7.46% CAGR through 2031. The USD 200 million Critical Medicines Production Centre in Edmonton, opening in 2026, illustrates the clean-room opportunity set that relies on low-outgassing, microbiologically inert sealants. Surgical sealants are another specialty pocket, with biodegradable films such as Sealantium Medical’s sFilm-FS completing Phase II trials in August 2025.

Automotive demand is accelerating as Ontario’s EV battery corridor scales. Thermal-management gap fillers, flame-retardant gaskets, and structural adhesives are specified for battery modules weighing 600-700 kg. Aerospace needs in Quebec for fuel-tank and firewall sealing continue to rely on polysulfide and high-temperature silicones that meet MIL-PRF-81733 and BSS 7239 toxicity thresholds, sustaining a stable yet specialized revenue stream for suppliers.

Geography Analysis

Regional climates and industrial patterns shape product demand. British Columbia’s marine climate and seismic codes elevate requirements for moisture-barrier and flexible-joint sealants. Retrofit pilots around Vancouver recorded energy cuts up to 90%, catalyzing uptake of high-performance air barriers that align with the Canada sealants market sustainability narrative. Ontario’s EV and aerospace clusters push advanced thermal and flame-retardant chemistries, while its construction employment slide of 8,700 workers in 2025 speeds modular adoption using factory-applied sealing systems. Quebec’s aerospace concentration demands aerospace-grade materials that meet stringent smoke-density and toxicity metrics, whereas Alberta’s temperature swings and clay soils sustain growth in flexible expansion-joint sealants for infrastructure and pharmaceutical facilities. Together these provincial drivers ensure balanced growth across the Canada sealants market.

Competitive Landscape

The Canada sealants market is moderately consolidated. Henkel leverages its rail-certified Teroson portfolio to win compliance-driven projects, while Dow invests in net-zero ethylene capacity at Fort Saskatchewan that could secure domestic feedstock for silicone intermediates. H.B. Fuller is consolidating its plant network and targets >20% EBITDA margin, indicating future pricing discipline. Digital tools also raise the bar: 3M’s Adhesive Mix Monitor provides real-time dispense analytics that cut rework, adding a data-driven differentiator in the Canada sealants industry.

Canada Sealants Industry Leaders

Sika AG

3M

Dow

Henkel AG & Co. KGaA

H.B. Fuller Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Henkel introduced Teroson MS 949 FR, a one-part silane-modified polymer rail sealant compliant with EN 45545-2 and free of tin, isocyanate, solvents, bisphenol A, and PFAS.

- March 2026: Sika entered a global partnership with Canada-based Giatec Scientific to embed AI sensors and software into concrete workflows, aiming for CHF 150 million-CHF 200 million incremental EBITDA by 2028.

Canada Sealants Market Report Scope

Sealants are elastomeric materials used to fill gaps, joints, or cracks, preventing water, air, dust, and fluid passage. Widely applied in construction and industrial sectors, they ensure waterproofing and structural flexibility in buildings, windows, automotive components, and appliances, typically using caulking guns.

The Canada sealants market is segmented by resin type and end-user industry. By resin type, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD) and volume (tons).

By Resin Type

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms