Aircraft Seals Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

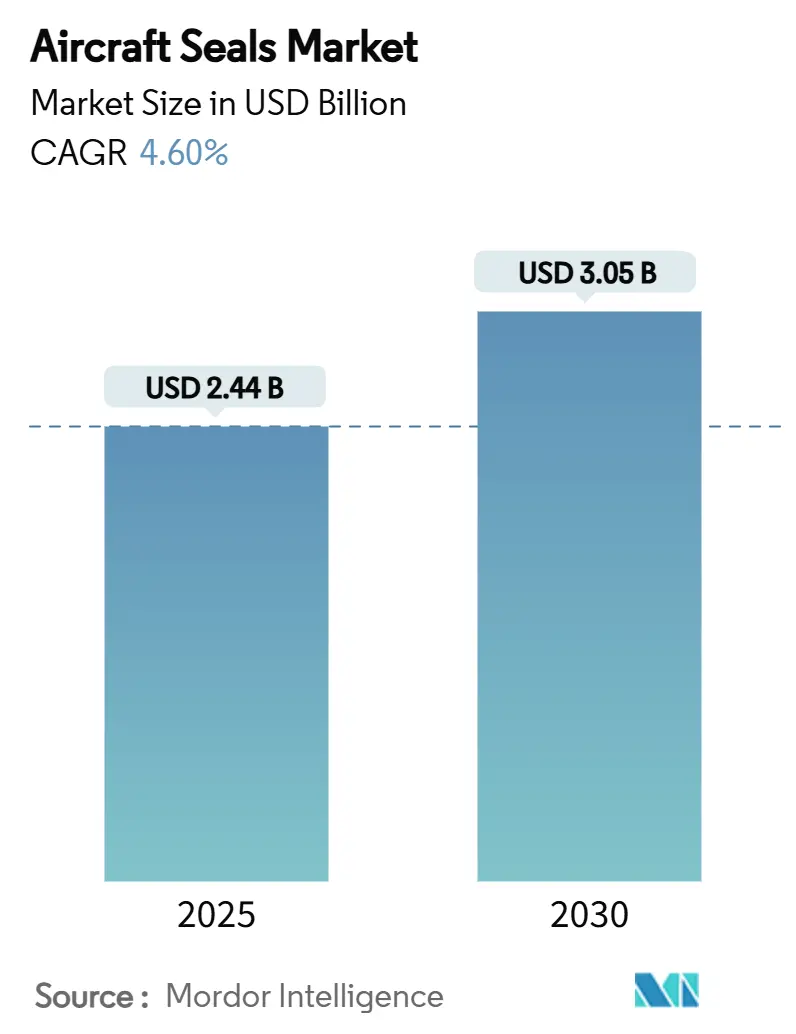

| Market Size (2025) | USD 2.44 Billion |

| Market Size (2030) | USD 3.05 Billion |

| Growth Rate (2025 - 2030) | 4.60% CAGR |

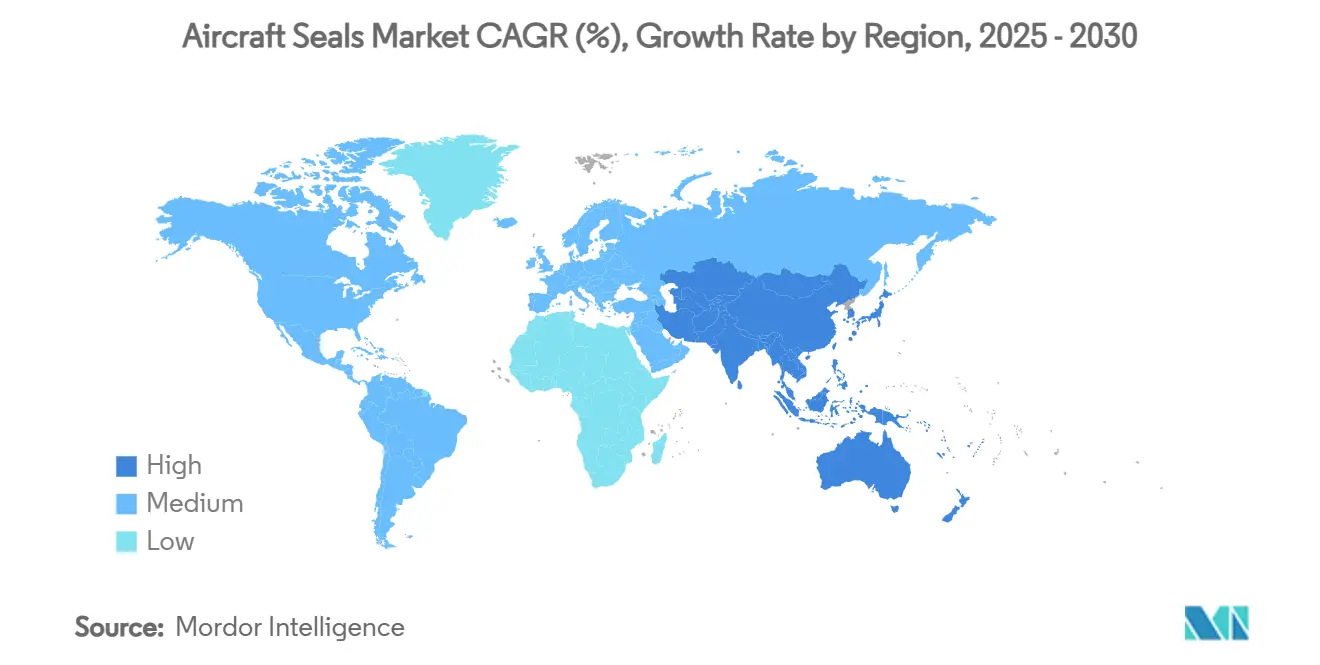

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

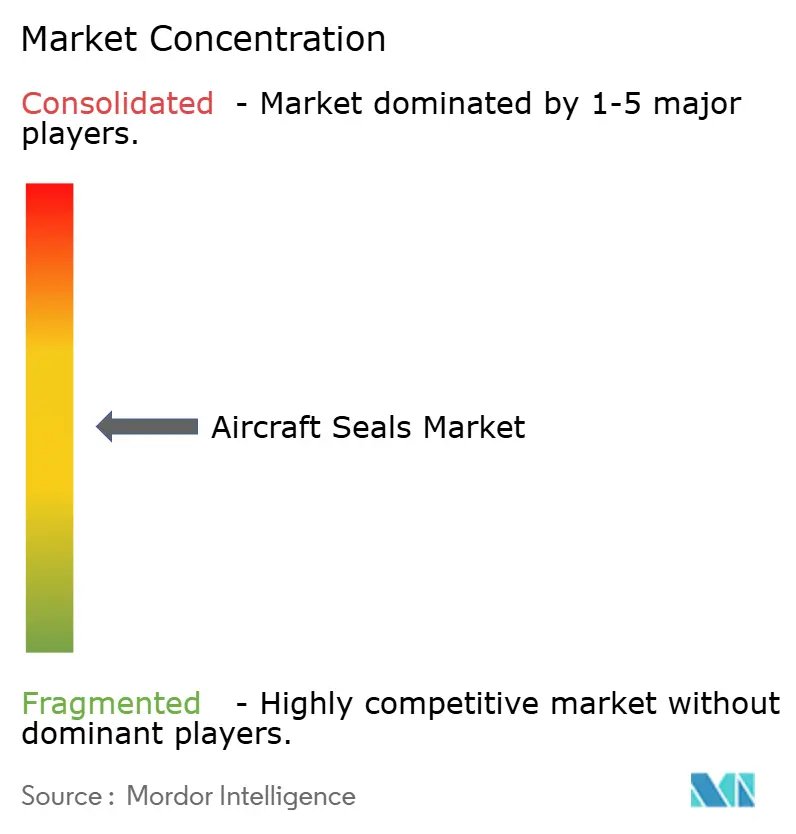

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Seals Market Analysis by Mordor Intelligence

The aircraft seals market stood at USD 2.44 billion in 2025 and is forecasted to reach USD 3.05 billion by 2030, advancing at a 4.60% CAGR. Demand is sustained by record commercial-aircraft backlogs, with Boeing projecting 44,000 new jet deliveries through 2043 as passenger traffic recovers.[1]Source: Boeing, “Boeing Forecasts Demand for Nearly 44,000 New Airplanes Through 2043,” investors.boeing.com Hydrogen-propulsion research and Advanced Air Mobility (AAM) certification timelines converge, creating dual pull for specialized cryogenic and rapid-turnaround sealing solutions. Material innovation is accelerating because regulators tighten zero-leakage and fire-safe rules, while proposed PFAS restrictions threaten legacy fluoropolymer dominance. Consolidation among incumbent suppliers increases scale and certification leverage, yet emerging additive-manufacturing processes shorten lead times and cut installation labor in new programs.

Key Report Takeaways

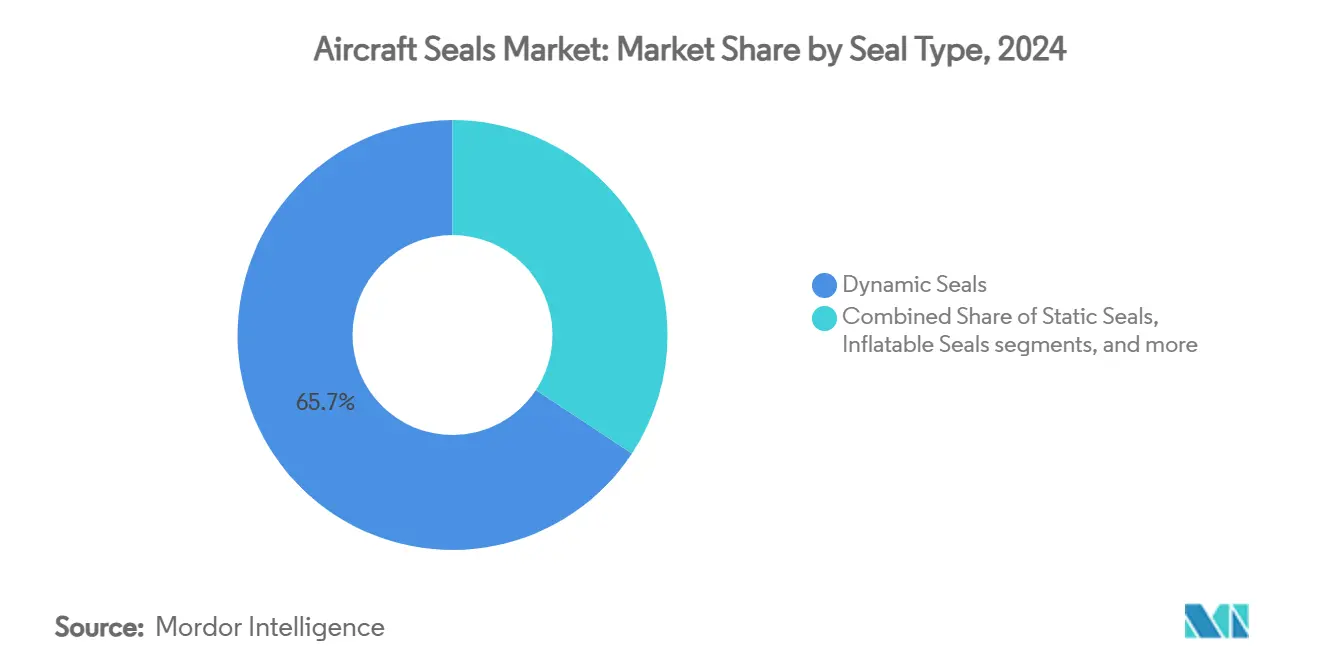

- By seal type, dynamic solutions led with 65.72% of the aircraft seals market share in 2024, while inflatable formats are forecasted to expand at a 6.12% CAGR to 2030.

- By application, engine systems held a 46.10% share of the aircraft seals market in 2024; environmental control and fuel systems are projected to grow at a 6.78% CAGR through 2030.

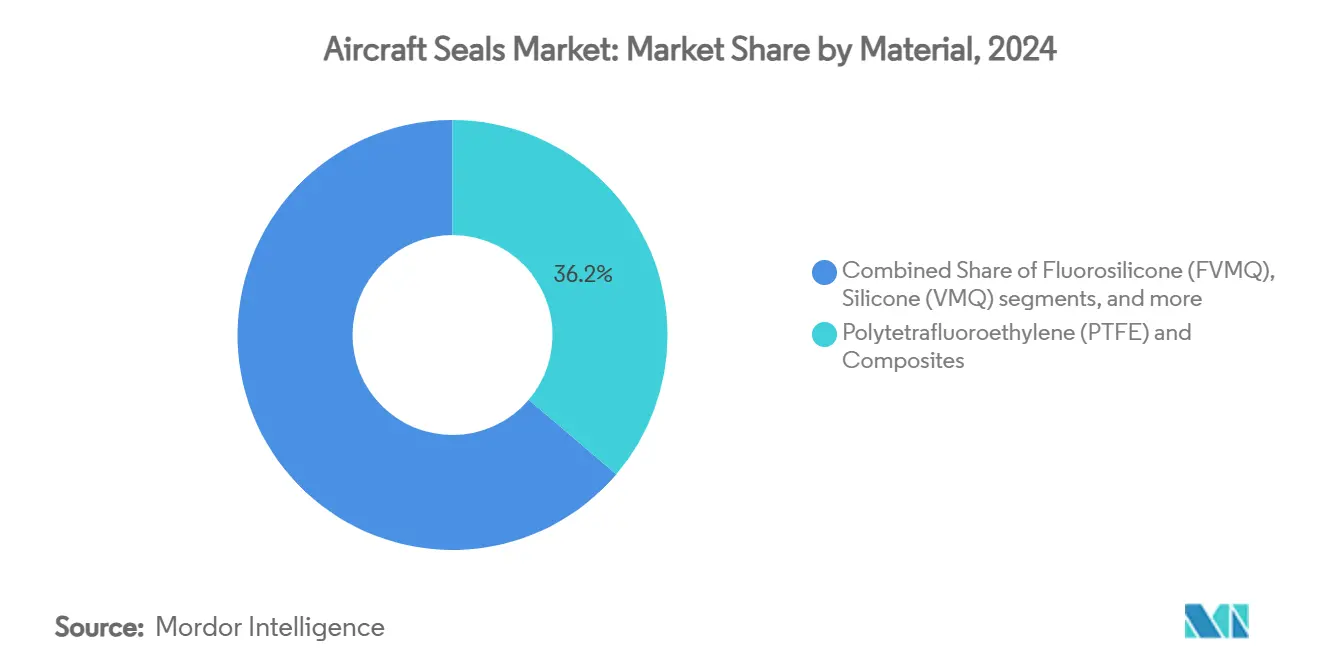

- By material, PTFE and composite grades held 36.22% share of the aircraft seals market size in 2024, yet fluorosilicone is poised for the fastest 7.01% CAGR.

- By aircraft type, fixed-wing platforms commanded a 68.50% share of the aircraft seals market in 2024, whereas unmanned aerial vehicles (UAVs) are advancing at an 8.56% CAGR in the same horizon.

- By geography, North America dominated with a 42.34% share of the aircraft seals market in 2024, while Asia-Pacific is set to post a 7.34% CAGR to 2030.

Global Aircraft Seals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing commercial aircraft production and deliveries | +1.2% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of MRO aftermarket and fleet life-cycle | +0.8% | Global, strongest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Regulatory pressure for zero-leakage and fire-safe sealing | +0.6% | Global, led by FAA and EASA jurisdictions | Short term (≤ 2 years) |

| Lightweight composite airframes raising seal performance needs | +0.5% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Hydrogen propulsion creating demand for cryogenic seals | +0.4% | Europe and North America, early adoption markets | Long term (≥ 4 years) |

| 3D printed elastomeric seals for Advanced Air Mobility (AAM) | +0.3% | North America and Europe, urban mobility corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Commercial Aircraft Production and Deliveries

Order books remain at record highs, and each narrow-body jet incorporates hundreds of critical sealing components across engines, airframes, and environmental-control systems. Single-aisle models dominate future deliveries, concentrating requirements in standardized geometries that maximise scale economies. Production ramp-ups stretch supply chains, so seal makers keep buffer inventories to offset castings and specialty-material bottlenecks. Consistent monthly output plans by the leading OEMs translate directly into steady pull for dynamic and static seals. Suppliers that align capacity with firm delivery schedules secure preferred-provider status on multi-year platforms.

Expansion of the MRO Aftermarket and Fleet Life-Cycle

Airlines extend aircraft service lives because new-build slots are scarce, increasing heavy-maintenance visits where seals are routinely replaced. Ageing fleets experience more frequent leakage risks, prompting proactive overhaul to maintain airworthiness. Aftermarket providers are opening facilities closer to growth corridors in Southeast Asia, improving turnaround times and easing logistics costs for operators. Predictive-maintenance software now integrates seal-health data from embedded sensors, allowing replacements based on condition rather than calendar interval. The shift rewards products that install quickly, reduce engineer hours, and keep asset downtime minimal.

Regulatory Pressure for Zero-Leakage and Fire-Safe Sealing

Investigations into recent in-service engine events have intensified scrutiny of any component that could permit flammable fluid escape. Updated FAA fuel-tank guidance and EASA CS-25 harmonisation leave negligible tolerance for seepage under thermal and pressure extremes.[2]Source: Federal Aviation Administration, “Fuel Tank Ignition Source Prevention Guidelines,” faa.gov Special conditions applied during the A321neo XLR program illustrate rising compliance thresholds that directly reshape seal specifications. New standards such as AS5316 for storage traceability and AS4716 for high-pressure gland design increase testing costs but protect incumbents already possessing certified data packages. Companies able to demonstrate flawless traceability gain a competitive edge in future tenders.

Lightweight Composite Airframes Raising Seal Performance Needs

Next-generation wide-body aircraft contain over 50% composite by weight, introducing differential thermal expansion between carbon-fibre skins and metallic sub-structures. Seals must flex repeatedly without losing compression set, even when the joint expands or contracts during long-haul cycles. Thermoplastic wings welded without fasteners create continuous seams that require environmental isolation, pushing demand for integrated seal-tapes co-cured during lamination. Re-use and recycling projects for carbon fibre alter resin chemistry, so material compatibility studies are essential. Innovations that maintain integrity across the entire cabin-pressure envelope command premium placements on upcoming single-aisle programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile fluoro-/silicone raw material prices | -0.7% | Global, most acute in Europe and North America | Short term (≤ 2 years) |

| Lengthy certification cycles for novel seal materials | -0.5% | Global, most restrictive in FAA and EASA regions | Medium term (2-4 years) |

| Limited recyclability of high-performance fluoropolymers | -0.3% | Europe and North America, driven by sustainability mandates | Long term (≥ 4 years) |

| Supply-chain fragility of per- and polyfluoro-elastomer precursors | -0.4% | Global, concentrated risk in select Asia-Pacific clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Fluoro-/Silicone Raw-Material Prices

Specialty elastomer feedstocks are concentrated within a handful of producers, exposing the aircraft seals market to abrupt price swings when factories halt or trade measures constrain exports. Proposed PFAS restrictions in Europe may force rapid formula changes, adding qualification costs and increasing demand for scarce substitute chemistries. Manufacturers pursue process scrap recycling to ease dependence on virgin material, yet aerospace-grade purity targets remain stringent.[3]Source: Daikin Industries, “Recovery and Recycling Activity of Fluoropolymers,” daikinchemicals.com Near-shoring strategies improve resilience but raise operating expenses in the short run. Contract clauses that link seal prices to commodity indices push volatility up the chain to airline maintenance budgets. Long-term supply agreements backed by inventory buffers help stabilize deliveries but tie up working capital.

Lengthy Certification Cycles for Novel Seal Materials

Any composition change triggers a full battery of mechanical, flammability, and ageing tests that can last several years and cost millions. While the FAA modernisation initiative seeks to streamline paperwork, the underlying requirement for demonstrated equivalence remains strict. Smaller firms struggle with funding long-term campaigns, reinforcing incumbent dominance. Digital-twin simulation promises faster analysis, yet regulators only accept physical evidence for safety-critical functions. Consequently, even high-potential PFAS-free compounds face delayed market entry, limiting the pace of material transition across the aircraft seals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Seal Type: Dynamic dominance and inflatable momentum

Dynamic products retained 65.72% of total demand in 2024, reflecting their pivotal role wherever shafts, blades, or actuators rotate at high temperature and pressure. The aircraft seals market size for dynamic designs is projected to expand steadily as core-engine volumes rise and turbofan architectures integrate higher bypass ratios that intensify thermal gradients. Premium fluoropolymer jackets and spring-energised lips continue to command price premiums because certification data already cover long-term creep and fuel-resistance performance. In contrast, inflatable solutions deliver the fastest 6.12% CAGR by 2030, led by AAM platforms whose doors, canopies, and variable-geometry surfaces must seal quickly yet release without manual tools.

Development programs now fuse sensors into dynamic ring carriers so operators can measure friction and predict overhaul windows, supporting condition-based maintenance strategies. For inflatables, additive manufacturing permits complex hollow geometries that collapse evenly, cutting assembly time on composite cabins. Static, lip, and ring formats still populate airframe joints, although their share declines as integrated structural seals are co-cured into wing and fuselage skins. Collectively, these trends embed at least three sealing technologies on every new aircraft variant, preserving multi-product revenue streams for tier-one suppliers across the wider aircraft seals market.

By Application/System: Engines lead while fuel-system nodes accelerate

Engines captured 46.10% revenue 2024, underscoring how extreme temperatures and rotating speeds enforce premium-grade materials. After several in-flight shutdown events, zero-leakage mandates keep qualification thresholds high, so substitution risk remains low. The aircraft seals market share for engines is expected to stay above 45% through 2030. Environmental-control and fuel-system circuits are forecast to post a 6.78% CAGR, buoyed by hydrogen prototypes that demand cryogenic glands capable of withstanding –253 °C cycles.

Hydraulic and flight-control lines show modest growth as more-electric architectures replace legacy fluid power, yet critical nose-wheel steering and brake accumulators still rely on elastomer diaphragms. Airframe joints migrate toward integrated composite-edge tapes, trimming discrete part counts but elevating qualification effort for the remaining seals. Landing-gear cavities require dirt-exclusion lips with abrasion-resistant PTFE liners, particularly on harsh runways in emerging markets. As each system evolves, adjacent sealing nodes proliferate, maintaining long-tail demand across the aircraft seals market.

By Material: PTFE resilience tempered by fluorosilicone surge

PTFE and composite blends commanded a 36.22% share in 2024 because decades of data back their chemical stability under Skydrol, jet fuel, and flame exposure. The aircraft seals market size linked to PTFE remains material-cost sensitive, yet OEMs favour it for life-limit predictability. Proposed PFAS rules in Europe threaten this hierarchy, prompting dual-track R&D, where thermoplastics and polyimides are tested as drop-in replacements. Fluorosilicone volumes are set to climb at a 7.01% CAGR since the polymer stays flexible at cryogenic temperatures and resists hydrogen embrittlement.

Silicone VMQ grades retain niche roles inside cabins and service doors with low fire load, while FKM serves auxiliary power units and bleed-air valves beyond 200 °C. Nitrile survives mainly in ground-support hoses. Few materials combine the impermeability and elasticity necessary for long-haul cycles, so hybrid stacks pair PTFE jackets with silicone energisers to reconcile regulation and performance. Each formula change demands a full retest, prolonging incumbent advantage yet inviting new entrants with PFAS-free chemistries that could reshape competition within the aircraft seals market.

By Aircraft Type: Fixed-wing scale confronts UAV disruption

Fixed-wing programmes accounted for 68.50% of the aircraft seals market in 2024, driven by single-aisle jets whose production cadence surpasses any other category. Certification commonality keeps the bill of materials stable, allowing seal makers to amortise tooling over large volumes. Business jet backlogs recovered strongly after 2024, sustaining mid-size lots of cabin and environmental seals. Rotary-wing platforms remain a steady niche where vibration tolerance outweighs volume.

Unmanned Aerial Vehicles (UAVs), however, log an 8.56% CAGR to 2030 as defense ministries procure high-endurance drones and commercial operators trial cargo delivery solutions. These airframes favour lighter, cheaper seals, opening doors for automotive-style elastomers and 3D-printed quick-change gaskets. The forthcoming wave of electric Vertical Take-off and Landing (VTOL) craft will borrow UAV manufacturing discipline, intensifying throughput expectations. Suppliers that can pivot between high-spec fixed-wing parts and cost-optimised UAV lines will secure the broadest footprint across the aircraft seals market.

Geography Analysis

North America remained the anchor, supplying 42.34% of global revenue in 2024 due to deep tier-ones clustered around prime OEM final-assembly lines. High defense budgets stabilise ordering across engine and missile programmes, sustaining premium margins on legacy PTFE rings. Most suppliers run vertically integrated moulding and machining to guarantee ITAR traceability, an attribute that ensures stickiness within the aircraft seals market.

Asia-Pacific posts the quickest 7.34% CAGR as India and Southeast Asia court aerostructure transfers under "China + 1" diversification strategies. Local firms escalate from rubber compounding to complete gasket assembly, reducing import spends and qualifying for offset quotas. Indigenous programmes such as India's regional jet concept will multiply domestic seal consumption once prototypes mature. China keeps investing in wide-body variants but imports many critical fluoropolymers; policy drives for material self-sufficiency could realign supply routes.

Europe balances Airbus's production strength with stringency in environmental policy. PFAS proposals push research into recyclable thermoplastics, potentially raising costs yet spurring first-mover patents. Meanwhile, the Middle East and Africa modestly enlarge their share through fleet growth and new MRO specials at hub airports. South America shows sporadic demand tied to regional jet overhauls. Overall, relative spend shifts eastward, but high-value cryogenic and fire-safe seals still concentrate where advanced R&D labs reside, preserving a multi-pole structure inside the aircraft seals market.

Competitive Landscape

The market retains moderate concentration. The key players of the market are Parker-Hannifin Corporation, Saint-Gobain Groups, Trelleborg Sealing Solutions, Trelleborg Sealing Solutions (Trelleborg AB), and Freudenberg Sealing Technologies (Freudenberg FST GmbH), holding a strong position in the market, giving them a defensive moat built on certification archives, captive compounding, and global service centres. Parker-Hannifin posted USD 1.57 billion segment revenue in Q3 2025 with a record 28.7% margin, illustrating the pricing power embedded in proprietary profiles. Trelleborg acquired Magee Plastics and will open a Morocco facility to widen thermoplastic capacity near European assembly plants, signalling geographic hedging against supply-chain shocks.

Freudenberg invested EUR 604.4 million (USD 708.59 million) in R&D in 2024, expanding German and Costa Rican aerospace and battery seals plants to cross-pollinate material science between sectors. Eaton’s joint venture in Malaysia embeds overhaul capability close to fast-growing fleets, providing pull-through for replacement rings. Smaller specialists differentiate via hydrogen-ready fluorosilicone blends or brush-seal geometries that extend turbine-disk life. Although additive manufacturing garners headlines, few players have scaled 3D-printed elastomer output beyond niche runs; incumbents hold the advantage through integrated moulding lines.

Regulation is the wild card. If PFAS bans arrive without grandfather clauses, many qualified PTFE parts will require urgent redesign, opening share opportunities for innovators with certified substitutes. Conversely, stringent validation could cement the incumbent status quo. Against this backdrop, vertical integration into compounding, testing, and MRO logistics is becoming the dominant strategy to preserve margin and customer lock-in across the aircraft seals market.

Aircraft Seals Industry Leaders

Parker-Hannifin Corporation

Freudenberg Sealing Technologies (Freudenberg FST GmbH)

Hutchinson S.A. (TotalEnergies SE)

Trelleborg Sealing Solutions (Trelleborg AB)

Saint-Gobain Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The US Defense Logistics Agency Land and Maritime awarded a USD 53,340 contract for aircraft seals, which are specifically designed for aircraft applications.

- July 2025: The US Defense Logistics Agency Aviation announced its intent to procure 52 air seals for F100 aircraft engines. These seals, crafted from PWA 1016 Nickel Alloy, must adhere to precise dimensions: 20.50" in length, 20.50" in width, 6.50" in height, and weigh 13.20 lbs. All 52 units are scheduled for delivery by May 2026.

Global Aircraft Seals Market Report Scope

| Dynamic Seals |

| Static Seals |

| Inflatable Seals |

| Lip and Ring Seals |

| Engine Systems |

| Airframe (Fuselage, Wings) |

| Flight-Control and Hydraulic Systems |

| Landing Gear |

| Environmental Control and Fuel Systems |

| Fluoroelastomer (FKM) |

| Fluorosilicone (FVMQ) |

| Silicone (VMQ) |

| Nitrile (NBR) |

| Polytetrafluoroethylene (PTFE) and Composites |

| Fixed Wing | Commercial Fixed Wing |

| Military Fixed Wing | |

| Business Jets | |

| Piston and Turboprop Aircraft | |

| Rotary Wing | Commercial Helicopters |

| Military Helicopters | |

| Unmanned Aerial Vehicles |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Seal Type | Dynamic Seals | ||

| Static Seals | |||

| Inflatable Seals | |||

| Lip and Ring Seals | |||

| By Application/System | Engine Systems | ||

| Airframe (Fuselage, Wings) | |||

| Flight-Control and Hydraulic Systems | |||

| Landing Gear | |||

| Environmental Control and Fuel Systems | |||

| By Material | Fluoroelastomer (FKM) | ||

| Fluorosilicone (FVMQ) | |||

| Silicone (VMQ) | |||

| Nitrile (NBR) | |||

| Polytetrafluoroethylene (PTFE) and Composites | |||

| By Aircraft Type | Fixed Wing | Commercial Fixed Wing | |

| Military Fixed Wing | |||

| Business Jets | |||

| Piston and Turboprop Aircraft | |||

| Rotary Wing | Commercial Helicopters | ||

| Military Helicopters | |||

| Unmanned Aerial Vehicles | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the aircraft seals market be by 2030?

The aircraft seals market size is projected to reach USD 3.05 billion by 2030, reflecting a 4.60% CAGR from 2025.

Which segment is growing fastest within aircraft sealing?

Inflatable seals are forecasted to post a 6.12% CAGR because Advanced Air Mobility designs prefer rapid-deploy, low-maintenance solutions.

What material changes could reshape future aerospace sealing?

Fluorosilicone demand is rising at a 7.01% CAGR as hydrogen propulsion requires cryogenic-capable elastomers that remain flexible at –253 °C.

Why are PFAS regulations significant to seal suppliers?

Proposed PFAS bans target fluoropolymer chemistries such as PTFE, forcing redesign and recertification of many existing aerospace seals.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a projected 7.34% CAGR, driven by expanding manufacturing capacity in India and accelerating fleet growth.

How are additive-manufactured seals influencing maintenance cycles?

3D-printed elastomer parts cut installation time by up to 90%, enabling condition-based maintenance compatible with high-utilisation urban-air-taxi fleets.

Page last updated on: