Gaskets And Seals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

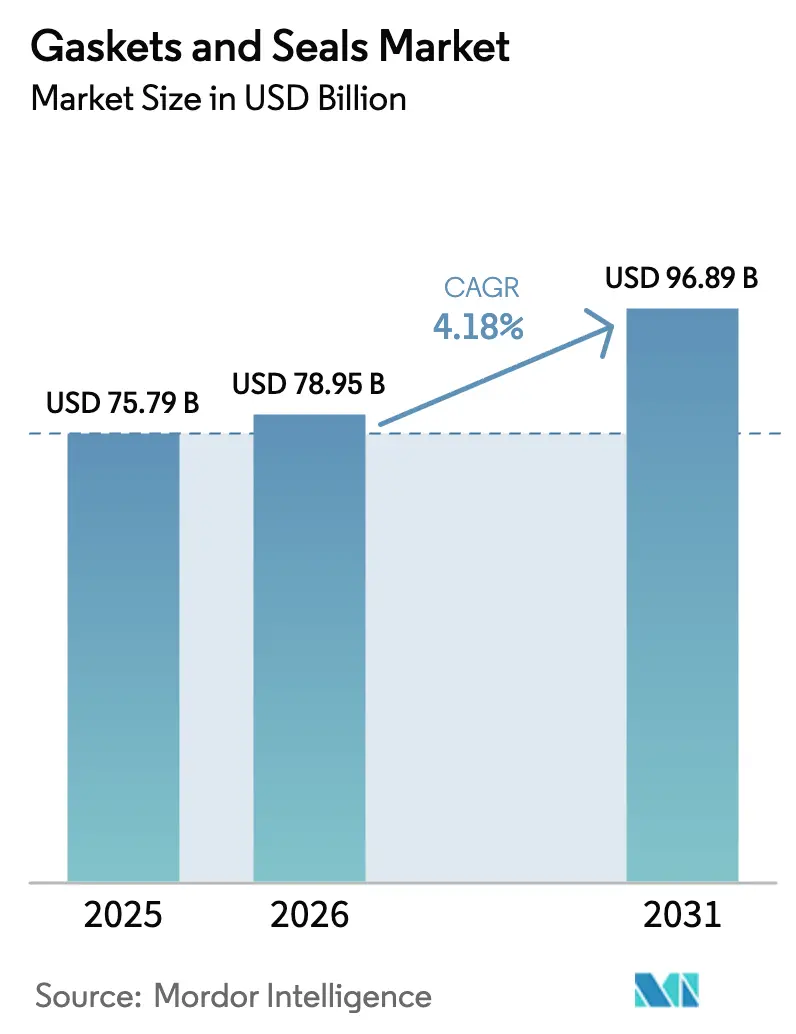

| Market Size (2026) | USD 78.95 Billion |

| Market Size (2031) | USD 96.89 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gaskets And Seals Market Analysis by Mordor Intelligence

The Gaskets And Seals Market size is projected to be USD 75.79 billion in 2025, USD 78.95 billion in 2026, and reach USD 96.89 billion by 2031, growing at a CAGR of 4.18% from 2026 to 2031. Heightened maintenance activity across liquefied-natural-gas (LNG) facilities, accelerating electric-vehicle (EV) production, and emerging hydrogen-pipeline retrofits are reshaping material preferences and design requirements. Asia-Pacific, anchored by China’s new-energy-vehicle build-out, leads revenue generation, while North America benefits from wind-turbine repowering programs and hydrogen pilot lines. Metallic spiral-wound gaskets remain essential in LNG and petrochemical turnarounds, yet rubber and PTFE compounds gain ground as automakers specify high-temperature, low-permeation seals for battery enclosures. Vertical integration into fluoro-rubber compounding and the roll-out of sensor-enabled “smart” gaskets illustrate how suppliers defend margins and differentiate offerings. Compliance with ISO 23936 for hydrogen service and SAE J3277 for battery safety is turning regulatory mandates into predictable replacement cycles.

Key Report Takeaways

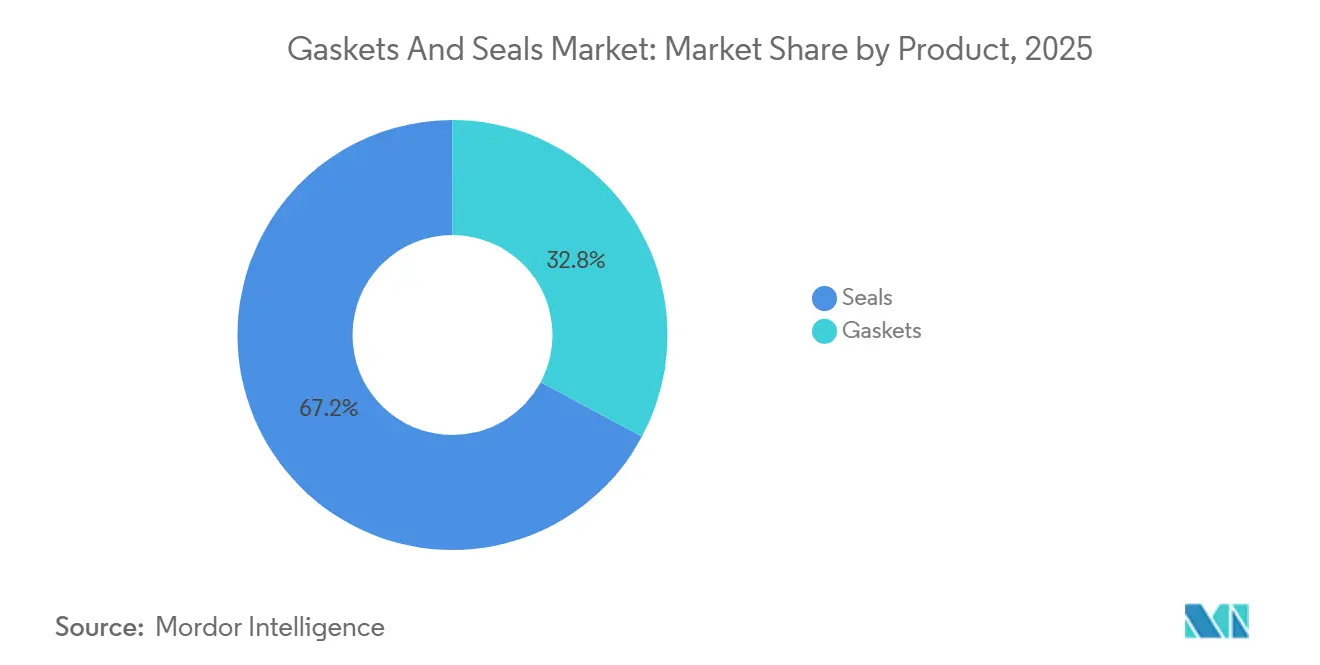

- By product, seals led with 67.18% revenue in 2025 and are advancing at a 5.54% CAGR through 2031 while gaskets record slower growth at 3.1%.

- By material, metals commanded 35.45% of the gasket and seals market share in 2025, whereas rubber is forecast to expand at 6.12% CAGR owing to new fluoro-silicone and perfluoroelastomer grades.

- By sales channel, OEM shipments represented 65.12% of 2025 turnover, but aftermarket purchases will rise at a 4.91% pace as petrochemical operators extend asset life cycles.

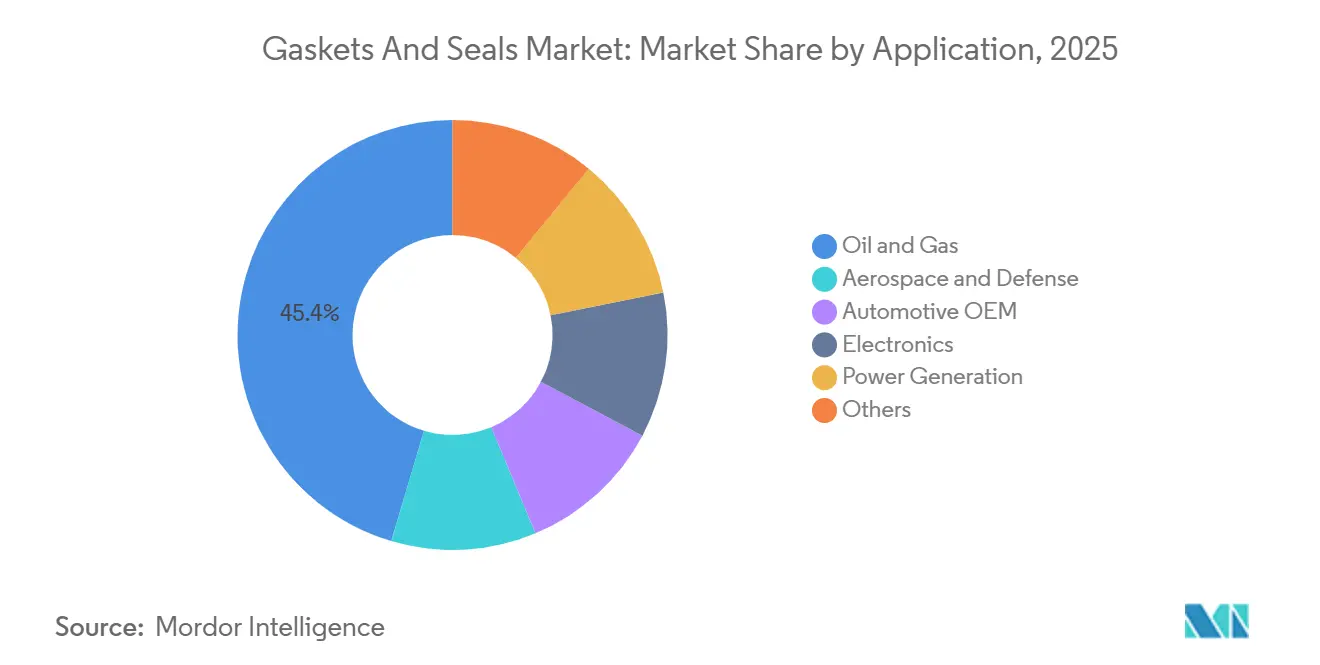

- By application, oil and gas held 45.39% of 2025 value; electrification pushes automotive OEM demand to the fastest 6.8% CAGR to 2031.

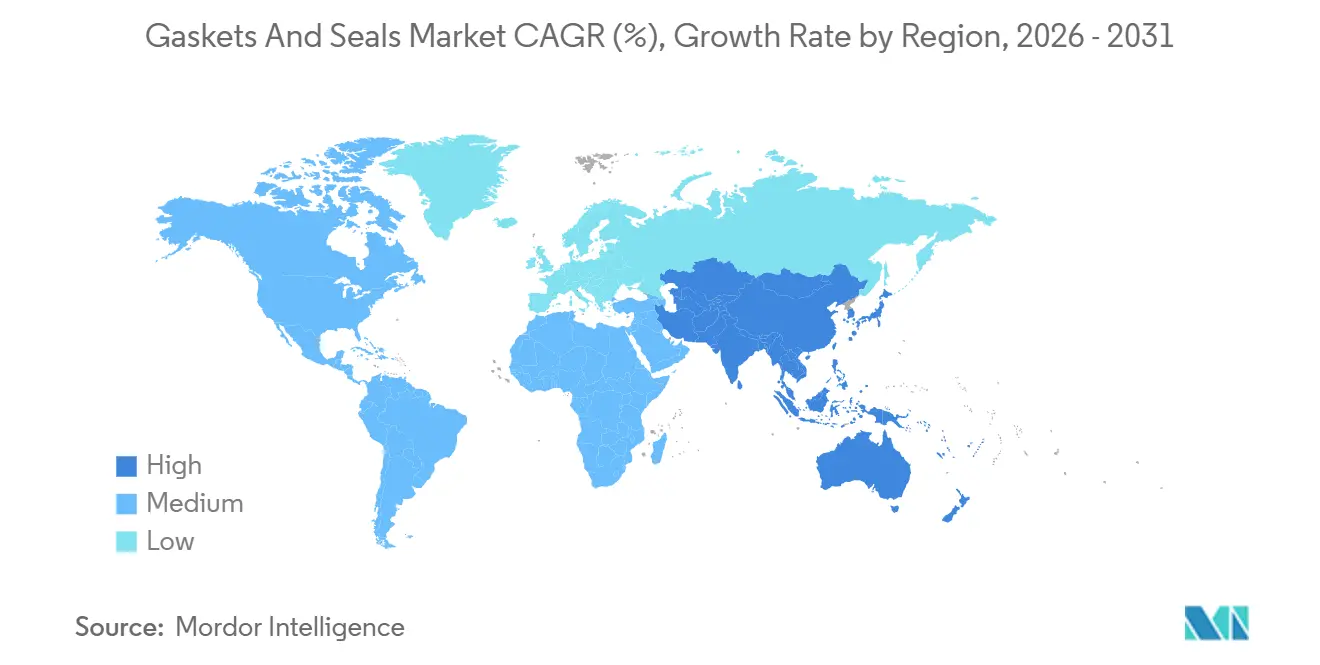

- By geography, Asia-Pacific generated 47.76% of 2025 revenue and is set to climb at 6.31% CAGR, the quickest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gaskets And Seals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of LNG mid-stream and downstream maintenance cycles | +0.8% | Middle East, Asia-Pacific, North America | Medium term (2-4 years) |

| Surging chemical and petrochemical plant refurbishments | +0.7% | Asia-Pacific, Middle East and Africa | Medium term (2-4 years) |

| Automotive electrification boosting e-power-train sealing | +1.2% | China, Europe, North America | Short term (≤ 2 years) |

| Sensor-enabled “smart” gaskets enabling predictive maintenance | +0.5% | North America, Europe | Long term (≥ 4 years) |

| Hydrogen-ready pipeline retrofits demanding novel metallic gaskets | +0.6% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of LNG Mid-Stream and Downstream Maintenance Cycles

Turnarounds now scheduled for LNG complexes commissioned between 2015 and 2020 are triggering large-scale gasket replacement programs. For example, Shell’s Pearl gas-to-liquids plant removed and reinstalled about 14,000 flange gaskets during its 2024 outage. U.S. regulations under 49 CFR Part 193 require gasket inspection every 36–60 months, locking in a recurring market for ASME B16.20 Class 2500 spiral-wound units. Cryogenic liquefaction trains favor graphite-filled metallic gaskets to survive –162 °C cycles, whereas ambient regasification terminals select shore-A 70–90 rubber variants to handle thermal expansion. With 40 million tpa of new LNG export nameplate added in 2024, demand correlates more with plant count than throughput, cushioning revenues from commodity-price swings.

Surging Chemical and Petrochemical Plant Refurbishments

Deferred maintenance during 2020–2022 has created a backlog now being cleared, notably in Saudi Aramco’s Jazan complex, where ethylene crackers underwent complete re-gasketing in 2024. Asia-Pacific capacity additions funded by India’s USD 6 billion Production-Linked Incentive scheme each consume 5,000–8,000 gaskets at start-up, with 10–15% yearly replacements thereafter. European steam-cracker retrofits, driven by stricter emissions limits, switch compressed-fiber gaskets to PTFE and flexible graphite to achieve sub-500 ppm leak thresholds. This refurbishment wave supports steady aftermarket volumes across high-pressure and high-temperature services.

Automotive Electrification Boosting E-Power-Train Sealing

Battery-electric vehicles require immersion-tested seals that survive IP67 and IP69K spray conditions mandated by SAE J3277 and GB 38031-2025. BYD’s 3 million NEVs built in 2024 each integrate 12–18 m of extruded EPDM or silicone profiles around battery trays and inverter housings. E-axle shaft temperatures of 150 °C necessitate low-friction fluoro-elastomer lip seals, while premium models embed encoders for condition monitoring. Adhesive bonding, such as Ford’s urethane technology, removes the perimeter gasket but still leaves multiple dynamic sealing points across coolant loops and drive units. As EV output crosses 10 million units a year, specification creep toward higher thermal and chemical resistance increases unit value per vehicle.

Hydrogen-Ready Pipeline Retrofits Demanding Novel Metallic Gaskets

Converting natural-gas lines requires metallic gaskets with hydrogen permeation below 1 × 10⁻⁸ cm³/(s·cm²·Pa) per ASME B31.12. The European Hydrogen Backbone project will upgrade 11,600 km of pipe by 2030, calling for 50,000–70,000 compatible flanges. The U.S. Hydrogen Shot aligns with the same goal, with pilot sites in the Gulf Coast and California testing Inconel 625 lens-ring designs[1]U.S. Department of Energy, “Hydrogen Shot Fact Sheet 2025,” Energy.gov. Japan’s USD 3.4 billion budget backs spiral-wound prototypes treated with corrosion inhibitors to mitigate hydrogen-induced cracking. Retrofits concentrate in North America and Europe, regions accounting for 75% of announced conversions.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility in elastomers and fluoro-rubbers | -0.6% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Adhesive bonding replacing gaskets in EV battery packs | -0.4% | China, North America, Europe | Medium term (2-4 years) |

| Prolonged vendor-qualification cycles | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility in Elastomers and Fluoro-Rubbers

Natural rubber prices jumped 15–20% in 2024 after supply disruptions in Thailand and Indonesia. Fluoro-elastomer costs climbed further as China curtailed fluorspar exports, squeezing hydrofluoric-acid feedstock. Lead times for EPDM and nitrile compounds extended to 10–14 weeks by mid-2025, straining cash flow for small gasket fabricators. Some end-users switched to PTFE-envelope gaskets to sidestep elastomer spikes, despite higher upfront prices. Vertical integration moves, such as Freudenberg’s 2025 acquisition of a German FKM compounder, seek to blunt this volatility.

Adhesive Bonding Replacing Gaskets in EV Battery Packs

Structural adhesives now seal 20–25% of global passenger-EV battery covers, a share forecast to exceed 40% by 2030. Ford’s UV-curable urethane cuts assembly time by 30 seconds per pack and removes a compression gasket from the bill of materials. Tesla’s 4680 structural pack uses adhesive joints that also contribute to crash-energy absorption, making conventional perimeter gaskets redundant. Commercial-vehicle platforms still prefer bolted covers for serviceability, retaining gasket demand in that sub-segment. As lightweighting and throughput remain paramount, adhesive encroachment will trim a gasket application that represented about 8–10% of automotive sealing revenue in 2023.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Seals Dominate Across Dynamic Applications

Seals generated 67.18% of 2025 revenue, and are projected to grow at 5.54% through 2031. Shaft seals thrive on the expanding installed base of wind turbines, each turbine containing 15–25 units that need replacement every 5–7 years[2]Global Wind Energy Council, “Global Wind Report 2025,” Gwec.net. Molded seals enjoy uptake in battery-electric vehicles, where stringent ingress-protection drives higher-grade EPDM and silicone profiles. Traditional gaskets grow more slowly because static joints are tied to turnarounds rather than new-equipment shipments.

Metallic spiral-wound designs still dominate high-pressure LNG and refinery joints, but cork and non-asbestos variants linger in legacy HVAC and low-pressure oil-pan assemblies. Sensor-enabled smart gaskets, although under 2% of installed units, signal a shift toward value-added static sealing products. The product mix, therefore, skews progressively toward dynamic seals as electrification and wind-power capacity accelerate, raising replacement frequency and average selling price within the gasket and seals market.

By Material: Rubber Gains on Electrification and Hydrogen Uptake

Metallic materials accounted for 35.45% of 2025 revenue, yet rubber compounds will post the fastest 6.12% CAGR, lifting their contribution to the gasket and seals market share. Fluoro-silicone blends tolerate 200 °C exhaust gas and resist coolants in hybrid drivetrains, widening their automotive footprint. Perfluoroelastomers, despite prices of USD 500–1,000 per kg, dominate semiconductor wet benches where a single hour of downtime exceeds USD 10,000 in lost wafers.

PTFE and expanded-PTFE secure mid-teen percentages of the gasket and seals market size by providing near-universal chemical resistance up to 260 °C. Flexible-graphite sheets remain indispensable in steam turbines that run at 650 °C, especially as utilities repower combined-cycle plants. The research spotlight now falls on hydrogen-compatible rubbers engineered to resist rapid-gas-decompression damage, a potential USD 500–700 million incremental opportunity before 2030.

By Sales Channel: Aftermarket Momentum Rises with Asset Life Extensions

OEM shipments accounted for 65.12% of 2025 revenue, yet aftermarket and maintenance-repair-operation orders will expand at a 4.91% CAGR, slightly eclipsing overall gasket and seals market growth. Petrochemical complexes built in the late 1990s are reaching 30 years of service, prompting major gasket replacement every four to five years. Fugitive-emission rules in the European Union and California are driving compliance-driven swap-outs of graphite and PTFE gaskets, independent of plant age.

Distributors such as Applied Industrial Technologies stock more than 10,000 SKUs for rapid fulfillment, commanding 20–40% price premiums over factory-direct OEM sales. E-commerce challenges these margins for commodity O-rings but cannot yet replicate technical support for complex geometries. As equipment run-times intensify, the aftermarket channel’s share of the gasket and seals market size will converge toward parity with OEM demand.

By Application: Oil and Gas Remains the Anchor Amid Transition

Oil and gas applications held 45.39% of 2025 revenue and will post a 5.67% CAGR, underpinned by subsea developments requiring metal-to-metal seals rated to API 6A pressures above 15,000 psi. Each FPSO carries 8,000–12,000 gaskets, refreshed during periodic shutdowns. Hydrogen-sulfide-laden sour-gas lines specify NACE MR0175-compliant gaskets, pushing demand for high-nickel alloys.

Automotive OEM applications, though now smaller in dollars, will grow fastest at 6.8% as EV output scales. Power generation contributes a mid-teens share through combined-cycle turbine builds and offshore wind fleets, while aerospace maintains stringent qualification barriers that lock in incumbent suppliers. Semiconductor tools, tiny in volume yet rich in value, rely on FFKM O-rings priced 10–20 times above nitrile counterparts, safeguarding profitability within the gasket and seals market.

Geography Analysis

Asia-Pacific contributed 47.76% of 2025 revenue and will post a brisk 6.31% CAGR through 2031. China’s 9.5 million NEVs built in 2024 underpin large-volume seal demand, and BYD’s local sourcing compresses costs and lead times. India’s USD 6 billion incentive plan for electronics and automotive plants multiplies gasket use in cleanroom HVAC ducts and cooling loops. Japan and South Korea continue to export high-precision PTFE and non-asbestos sheets, while ASEAN nations lure diversified production that needs localized sealing solutions.

North America accounted for a significant market share in 2025. The United States added 15 GW of wind capacity in 2024, and each turbine’s gearbox seals face five-year change-out schedules. Hydrogen pilot pipelines along the Gulf Coast require ASME B31.12-compliant Inconel ring-joints, lifting specialty-metallic demand. Canada’s 3 million bpd oil-sands throughput calls for high-temperature SAGD well seals, and Mexico’s export-oriented vehicle builds anchor OEM shipments, albeit with fewer parts per EV.

Europe captured a high-teens slice, with growth constrained by mature auto output. Yet the 11,600 km hydrogen backbone conversion program will install up to 70,000 hydrogen-ready gaskets. Offshore wind in the United Kingdom surpasses 14 GW, catalyzing MRO seal replacements at mid-life. Nordic district-heating grids pilot sensor-enabled gaskets, although penetration remains under 5%.

South America and the Middle East and Africa combined for a low-teens portion in 2025. Saudi Aramco’s Jazan complex and Nigeria’s Dangote refinery both initiated gasket-intensive turnarounds after commissioning. Brazilian pre-salt fields, alongside UAE petrochemical upgrades, supply recurring aftermarket demand, stabilizing regional revenues despite commodity price swings.

Regulatory Landscape

Compliance is increasingly shaped by chemical-content and end-use safety standards that drive material choice and documentation across global supply chains. In the United States, LNG facilities operate under 49 CFR Part 193 inspection requirements (with gasket inspection cycles referenced at 36 to 60 months), supporting recurring replacement demand tied to regulated maintenance rather than discretionary capex. In automotive electrification, sealing designs are also governed by battery safety and ingress protection requirements referenced in SAE J3277 and China’s GB 38031-2025, pushing OEMs toward validated low-permeation elastomers and higher-temperature formulations for battery enclosures and coolant loops.

For Europe and parts of Asia, chemicals regulation is a direct design constraint for conductive gaskets, PTFE-based components, and high-performance elastomers. In 2026, ECHA Candidate List updates and related REACH obligations increased the burden of substance tracking and supplier declarations for additives used in gasket and seal formulations, including lower concentration thresholds referenced for certain SVHCs in conductive gasket applications. Alongside PFAS reporting and restriction activity, the US EPA’s TSCA Section 8(a)(7) PFAS reporting timeline being moved to a 31 January 2027 start for submissions (effective April 2026) reinforces the shift toward traceable bills of materials and reformulation programs for fluorinated chemistries used in high-end sealing.

Value Chain Analysis

The value chain runs from (1) raw materials (metals, specialty alloys, expanded graphite, aramid fibers, and elastomers such as NBR, EPDM, and FKM) to (2) compound formulation and mixing, then (3) conversion and precision manufacturing (calendering, molding, machining, and multi-material assembly), (4) distribution and kitting (including MRO-focused stocking and rapid fulfillment), and (5) end users across oil and gas, automotive OEM, power generation, electronics, and aerospace. Differentiation concentrates upstream in compounding know-how and downstream in application engineering, where suppliers co-design seals for EV thermal management, hydrogen service, and fugitive-emissions performance, while commodity O-rings and sheet-gasket cutting face the strongest price pressure.

Supply risk is most visible in elastomer and additive inputs, where dependence on globally concentrated rubber-chemical supply adds lead-time and availability volatility for smaller fabricators. Qualification and compliance documentation extend time-to-substitute materials, particularly where EU customer approvals can take 12 to 18 months for new formulations, amplifying the impact of feedstock disruptions and REACH-driven reformulations. Leading suppliers have worked to improve resilience and service levels by building regional manufacturing and distribution footprints, including Freudenberg Sealing Technologies expanding capacity and automation through new production and warehousing assets cited in 2025, alongside channel partners that hold broad SKU inventories to serve turnaround-driven demand in LNG, refining, and petrochemicals.

Competitive Landscape

The gaskets and seals market is moderately consolidated. Investments target engineered solutions: Henkel’s LOCTITE Pulse wireless system outfits spiral-wound gaskets with bolt-load sensors, while Parker Hannifin expanded Indian capacity to serve EV and renewable-energy customers. Patent filings reveal a technology arms race. Ford’s structural adhesive eliminates cover gaskets in EV packs, hinting at application displacement, whereas Additive-manufacturing startups print custom gasket geometries within 48 hours, trimming tooling costs for short runs. Certification like ISO 9001, IATF 16949, and AS9100 remains a price premium lever, especially for aerospace and automotive buyers. Consolidation is expected as electrification, hydrogen adoption, and predictive-maintenance functions raise research and development thresholds that favor scale operators.

Gaskets And Seals Industry Leaders

Freudenberg Sealing Technologies

Trelleborg AB

SKF

Dana Limited

Flowserve Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hydrogen and electrification are creating a clear whitespace for sealing materials and processes that meet permeation, rapid-gas-decompression, and thermal-cycling requirements while reducing unit cost at scale. On the production side, WEVO-CHEMIE GmbH and Laufenberg GmbH disclosed a June 2026 roll-to-roll approach for continuous, higher-throughput manufacturing of flat elastomer gaskets used in fuel cell and electrolyser stacks, which provides a pathway for lower-cost, repeatable gasket supply as stack volumes increase. On the materials side, suppliers are expanding higher-temperature, chemically resistant elastomers for harsh duty cycles; Syensqo’s October 2025 expansion of non-fluorosurfactant perfluoroelastomer (FFKM) grades (up to 320 degrees C) reflects the push to maintain performance headroom while responding to evolving PFAS scrutiny.

A second opportunity cluster focuses on compliance-driven substitution and traceability services, as REACH and PFAS-related actions increase the need for reformulated compounds, supplier transparency, and documentation support for OEM and MRO buyers. Companies that can offer validated alternatives to restricted additives, along with application engineering for battery sealing standards and hydrogen service specifications (for example, ASME B31.12-referenced permeation requirements in pipeline conversions), gain share in premium segments where downtime and leakage penalties outweigh component cost. This favors vertically integrated compounders and manufacturers with in-house test capability, as well as suppliers that can bundle sealing products with condition monitoring (smart gaskets) for predictive maintenance programs in process industries and power generation.

Recent Industry Developments

- June 2026: Trelleborg completed the acquisition of Gomet, an Italian producer of polymer components for automotive systems, from Huntsman for around EUR 43 million. The deal strengthens Trelleborgs polymer component base for vehicle platforms where sealing and molded elastomer parts are specified together, supporting cross-selling into automotive OEM supply chains.

- February 2026: Flowserve entered a definitive agreement to acquire the Valves Division of Trillium Flow Technologies for USD 490 million to expand its position in nuclear and broader power markets. The move broadens Flowserves installed equipment footprint, which supports pull-through demand for engineered sealing solutions such as mechanical seals and associated aftermarket service content in power generation.

- May 2024: Freudenberg Sealing Technologies acquired the Trygonal Group to expand capabilities in CNC-turned sealing products. The acquisition enhances rapid customization for short-run and high-spec applications, improving responsiveness for industrial MRO and OEM programs that require tight tolerances and shorter lead times.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers the value of newly manufactured gaskets and seals used to prevent fluid or gas leakage in equipment and systems across industrial, transport, and energy uses, with revenue measured at the factory-gate level in USD.

Scope exclusions: Rebuilt, reused, or re-conditioned sealing products and adhesive-only sealants are excluded from the market totals.

Segmentation Overview

- By Product

- Gaskets

- Metallic Gasket

- Rubber Gasket

- Cork Gasket

- Non-asbestos Gasket

- Spiral Wound Gasket

- Other Gaskets (Semi-Metallic Gasket)

- Seals

- Shaft Seals

- Molded Seals

- Motor Vehicle Body Seals

- Other Seals (Fork Seal and Piston Seal)

- Gaskets

- By Material

- Fiber

- Graphite and Flexible Graphite

- PTFE

- Rubbers

- Others

- By Sales Channel

- OEM

- After-market / MRO

- By Application

- Aerospace and Defense

- Automotive OEM

- Electronics

- Oil and Gas

- Power Generation

- Others

- Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Nordics

- Rest of Europe

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Nigeria

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the structure of the model and anchor key demand and supply signals that can be checked in public data. We referred to sources such as US Census Bureau manufacturing statistics, US International Trade Commission import and export tables, Eurostat industrial production series, Japan METI manufacturing indicators, and trade association publications linked to fluid sealing and engineered materials.

Beyond official statistics, we reviewed company filings and investor presentations to understand product mix and end-market exposure, then cross-checked commentary through reputable press and association websites. Where needed, a paid subscription covering company financials and intelligence, a patent database, and an import and export shipment-level database were used to validate supplier footprints and trade flows. The desk research sources listed here are illustrative only, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with manufacturers, distributors, and large end users who buy sealing solutions for maintenance and new builds. We covered demand-side views from automotive, industrial machinery, chemicals, power, and oil and gas, and then used responses to confirm assumptions on replacement cycles, price realization, and mix shifts across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 43% |

| Mid tier: 55% | Functional/Unit leaders: 39% | EMEA: 36% |

| Smaller Players: 15% | Managers: 48% | Americas: 21% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where industrial output and trade data help reconstruct the demand pool for sealing products, which is then adjusted using end-market activity indicators. We anchored the value build with inputs such as vehicle production and parc servicing intensity, industrial machinery output, oil and gas and power maintenance activity, and the installed base of process plants where leak prevention drives steady replacement demand.

To keep totals realistic, the results were corroborated with selective bottom-up checks, including sampled supplier revenue splits, channel checks across OEM versus aftermarket, and volume by typical unit usage multiplied by average selling prices for common gasket and seal families. When direct volume signals were thin for a niche use, we filled gaps using proxied indicators like equipment shipments, maintenance schedules, and trade flow direction, and then re-tested the implied ASP against interview feedback.

For forecasting, scenario analysis was used so the outlook can flex with changes in industrial production, energy project cycles, and automotive build rates. The chosen path was also aligned to what primary respondents described as the most likely operating environment for sealing demand. Assumptions were kept simple and reproducible, and we avoided inputs that cannot be consistently tracked year to year.

Data Validation & Update Cycle

Validation was done by triangulating modeled totals against independent signals like production trends, trade flows, and disclosed revenue exposure to sealing products, and then checking whether the implied per-unit consumption looked reasonable. Outliers were investigated through follow-up checks, and any large variance by region or end use was reviewed before sign-off.

Reports are refreshed annually, and interim updates are made when material events affect demand, pricing, or supply availability. Before delivery, we run a fresh pass on key assumptions and spot-check recent public data so clients receive an up-to-date view.

Mordor Intelligence's Gaskets and Seals Market Estimate Compared With Other Published Estimates

Published market values for gaskets and seals often do not match because each publisher sets its own scope lines, pricing point, and timing for currency and inflation updates, which changes the final dollar total. Differences also show up when one estimate blends adjacent items or counts services that sit next to product sales.

The main gap comes from whether rebuilt or re-conditioned sealing parts and adhesive-only sealants are folded into the value. Mordor Intelligence treats the market as newly manufactured gaskets and seals priced at the factory gate, covering both OEM and aftermarket demand in the same total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 78.95 B (2026) | |

| Industry Research Publisher A | USD 63.09 B (2024) | Uses a different base year and pricing stack, and the scope may be anchored to end-use reporting periods that do not fully align with factory-gate product value for the full gasket and seal universe. |

| Industry Research Publisher B | USD 64.11 B (2024) | Reports a 2024 base-year total with a longer forecast window, and the spread is typically driven by how OEM versus aftermarket is handled and how currency timing and inflation adjustments are applied across regions. |

Taken together, the spread in figures is mostly explained by scope and timing choices rather than a single demand driver. By tying the model to traceable activity indicators and then sanity-checking price and mix through interviews, we keep the estimate balanced and repeatable even when public data is uneven.

Key Questions Answered in the Report

How large is the gasket and seals market in 2026 and how fast will it grow?

The gasket and seals market size is estimated at USD 78.95 billion in 2026 and is projected to reach USD 96.89 billion by 2031 at a 4.18% CAGR.

Which region contributes the most revenue?

Asia-Pacific generates 47.76% of global revenue and is expanding at a 6.31% CAGR thanks to strong automotive, electronics, and infrastructure demand.

Which product category leads the market?

Seals command 67.18% of revenue in 2025 and grow faster than gaskets because dynamic equipment such as EV drivetrains and wind-turbine gearboxes require frequent replacements.

Why are hydrogen-pipeline retrofits important for suppliers?

Hydrogen conversions need metallic gaskets that resist permeation and embrittlement, creating a specialty niche projected to add up to USD 700 million in new demand before 2030.

How are suppliers managing raw-material price swings?

Leading vendors are integrating backward into fluoro-rubber compounding, locking long-term supply contracts, and passing surcharges to OEM and aftermarket buyers to maintain margins.

What impact will adhesive bonding have on gasket demand in EVs?

Structural adhesives already seal about one-quarter of passenger-EV battery covers and could exceed 40% penetration by 2030, reducing perimeter-gasket revenue but not affecting dynamic shaft, coolant, and thermal-interface seals.

Page last updated on: