Food Processing Seals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

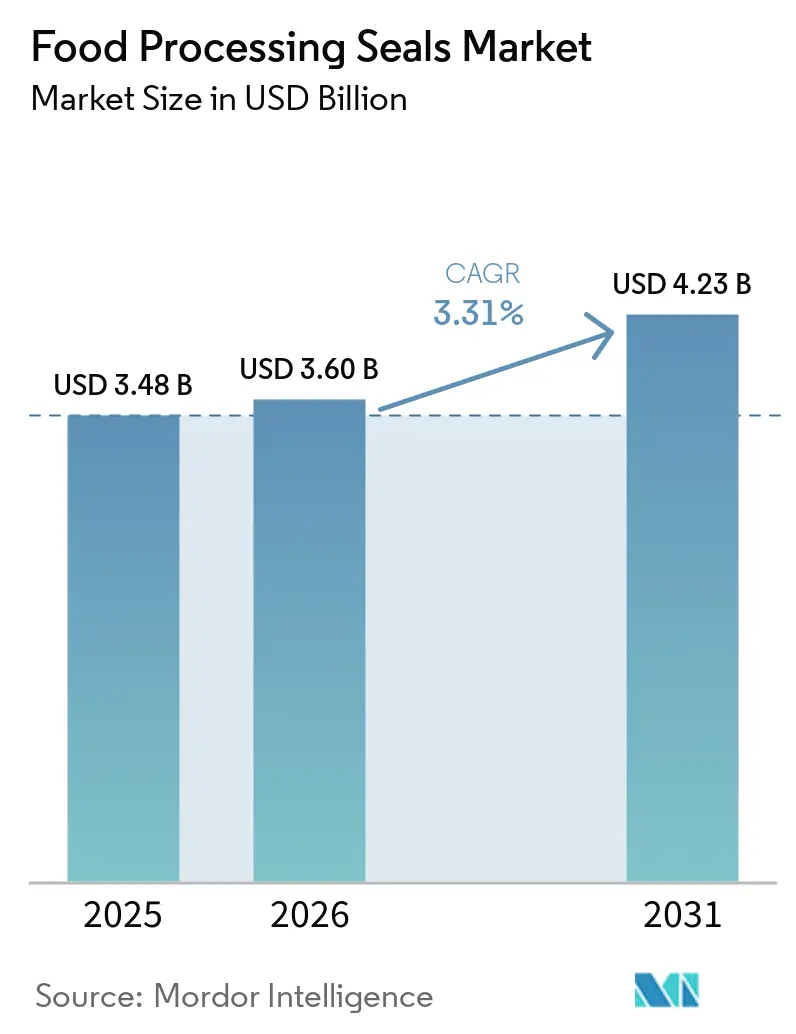

| Market Size (2026) | USD 3.60 Billion |

| Market Size (2031) | USD 4.23 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Processing Seals Market Analysis by Mordor Intelligence

The Food Processing Seals Market size is projected to expand from USD 3.48 billion in 2025 and USD 3.60 billion in 2026 to USD 4.23 billion by 2031, registering a CAGR of 3.31% between 2026 to 2031. Rapid compliance with global food-contact regulations, rising adoption of fully automated production lines, and the expansion of micro cold-chain infrastructure in the Asia-Pacific are reshaping the Food processing seals market. Processors are replacing generic elastomers with FDA-grade perfluoro-elastomers for aseptic high-viscosity lines, while plant-based protein manufacturers are standardizing on alkaline-resistant FFKM and PTFE seals. Equipment OEMs are integrating clean-in-place and steam-in-place capabilities that demand zero-leakage mechanical seals, which shifts revenue toward premium materials and engineered assemblies. Competitive intensity is moderate because tier-one suppliers leverage hygienic-design certifications to secure multi-year agreements with global equipment manufacturers, leaving regional molders to compete on speed and customized compounds.

Key Report Takeaways

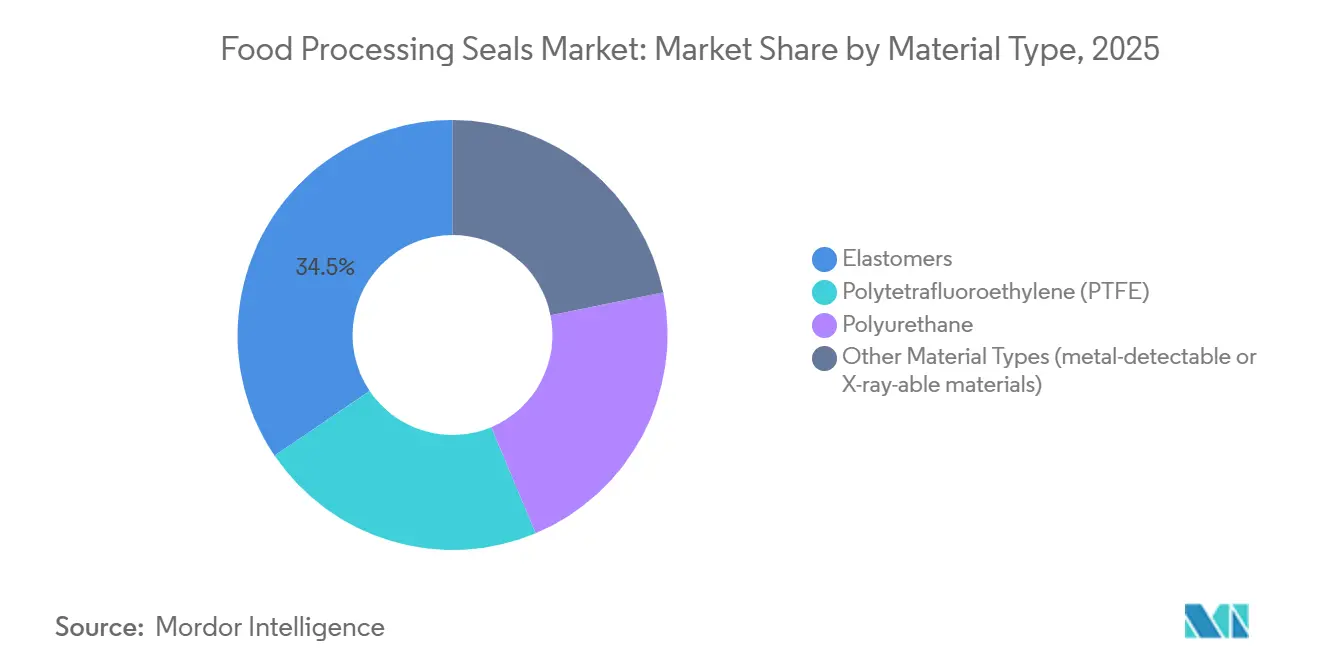

- By material type, elastomers led with 34.47% of the food processing seals market share in 2025, and the segment is advancing at a 3.56% CAGR through 2031.

- By seal type, O-rings retained 37.78% share of the food processing seals market in 2025, while mechanical seals are forecast to register the fastest 3.66% CAGR through 2031.

- By application, processing equipment accounted for 55.12% of the food processing seals market share in 2025, whereas cleaning systems posted the highest 4.14% CAGR through 2031.

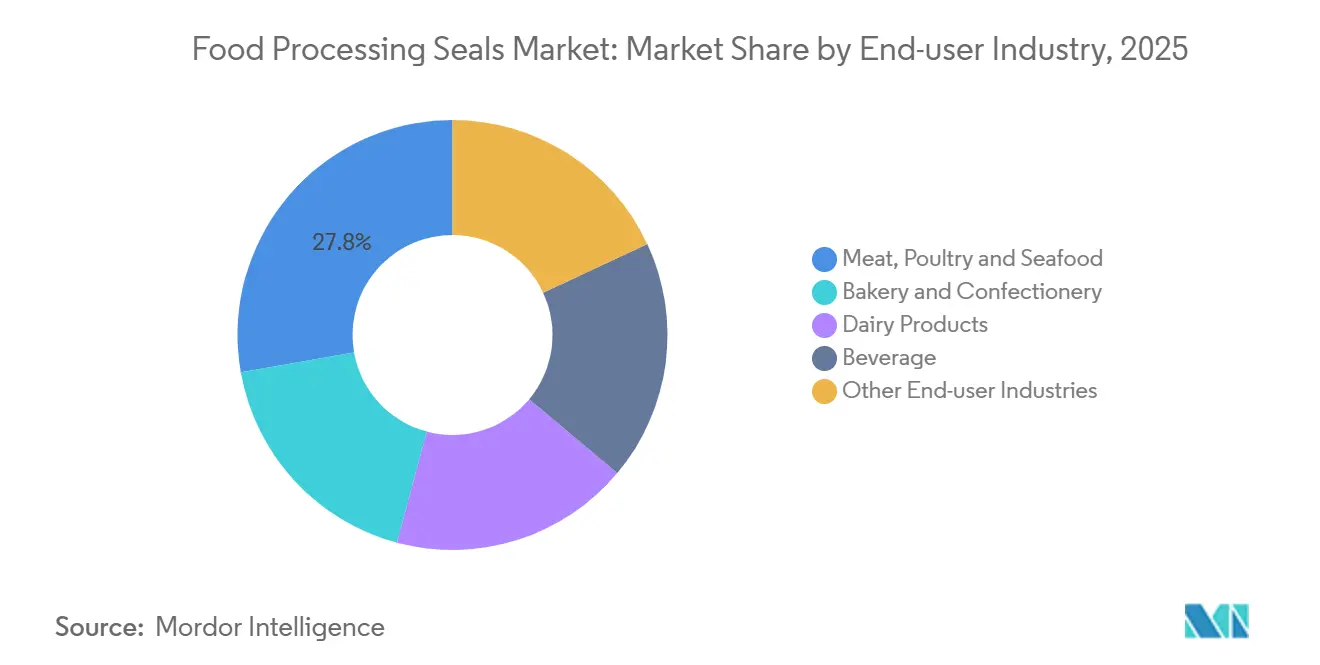

- By end-user industry, meat, poultry, and seafood represented 27.78% of the food processing seals market share in 2025, while other end-user industries segment is growing at a 4.10% CAGR through 2031.

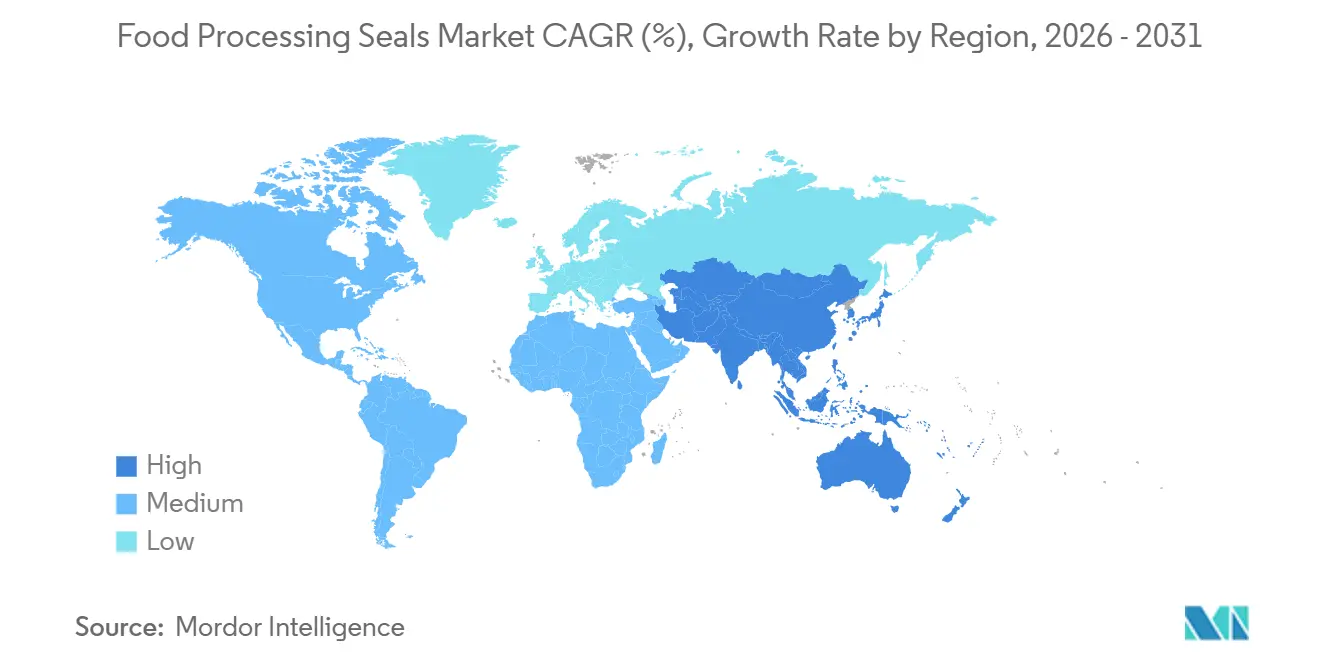

- By geography, Asia-Pacific captured 43.34% of the food processing seals market share in 2025 and is expanding at a 4.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Processing Seals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enforcement of global food-contact regulations | +0.9% | Global, with North America and EU leading compliance | Medium term (2–4 years) |

| Adoption of fully-automated processing systems | +0.8% | North America, Europe, APAC (China, Japan, South Korea) | Long term (≥4 years) |

| Shift toward plant-based protein processing | +0.5% | North America, Europe, APAC urban centers | Medium term (2–4 years) |

| Aseptic high-viscosity lines needing FDA-grade perfluoro-elastomers | +0.4% | Global, concentrated in dairy and beverage hubs | Short term (≤2 years) |

| Regional micro-cold-chain expansion boosting cryogenic seal grades | +0.6% | APAC core (India, China, ASEAN), spill-over to MEA | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Enforcement of Global Food-Contact Regulations

Convergence of U.S. 21 CFR 177.2600 and EU Regulation 1935/2004 obliges processors to document seal compliance, favoring suppliers with clean-room molding and batch-record systems[1]U.S. Food and Drug Administration, “21 CFR 177.2600 Rubber Articles for Repeated Use,” fda.gov. Recall exposure drives adoption of certified seals despite higher unit prices, and Saudi Arabia’s updated Food Law extends this pressure across the Middle-East.

Adoption of Fully Automated Processing Systems

High-speed fillers and robotic deboners now run continuous sterilization cycles that require FFKM lip seals and silicon-carbide mechanical faces capable of 6+-year duty. Inline metal detectors spur demand for X-ray-detectable seal materials, locking processors into long-term service contracts.

Shift Toward Plant-Based Protein Processing

Alkaline cleaning at pH 11-13 degrades standard nitrile and EPDM within a year. Processors therefore specify FFKM compounds such as Kalrez and Perlast that sustain performance under high-pH and thermal cycling, even at a 5× cost premium. Alfa Laval's plant-protein extraction systems utilize sodium hydroxide CIP solutions at high temperatures, which can lead to increased elastomer swelling and hardness degradation.

Aseptic High-Viscosity Lines Needing FDA-Grade Perfluoro-Elastomers

UHT and aseptic cheese-spread fillers operate at 135 °C and 6 bar, which only perfluoro-elastomers can withstand while maintaining sterility and low extractables. Krones' VarioAsept M UHT system utilizes direct steam injection and aseptic buffer tanks pressurized to 6 bar. This design subjects mechanical seals to cyclic thermal and pressure loads, which only FFKM compounds can endure without compromising sterility. The FDA's emphasis on process validation and sterility assurance is driving processors to document seal performance through challenge testing and extractables/leachables studies. This trend benefits suppliers with comprehensive regulatory dossiers and robust technical support capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aggressive alkaline CIP cleaners degrading elastomers | -0.3% | Global, acute in plant-based and dairy processing | Short term (≤2 years) |

| Shortage of certified clean-room molding capacity | -0.2% | North America, Europe | Medium term (2–4 years) |

| Rise of adhesive-less, gasket-less equipment designs | -0.1% | Europe, North America (ultra-hygienic segments) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Aggressive Alkaline CIP Cleaners Degrading Elastomers

Sodium hydroxide at pH 12-13 cuts seal life to under 12 months, inflating maintenance costs until alkaline-resistant EPDM and FFKM grades scale.Trelleborg's technical bulletins report an increase in EPDM hardness by 10–15 Shore A points and volume swelling exceeding 20% after 500 hours of exposure to 2% NaOH at 80°C. Similarly, BASF's cleaning-agent compatibility matrices indicate that standard Viton (FKM) compounds experience a 30% reduction in tensile strength under comparable conditions.

Shortage of Certified Clean-Room Molding Capacity

ISO-Class 7 facilities are limited to a handful of tier-one suppliers, pushing lead times for custom FFKM parts to 16 weeks and delaying new aseptic line commissioning. Precision Polymer Engineering operates a clean-room facility dedicated to producing pharmaceutical and food-grade seals. However, lead times for custom FFKM parts can extend to 12–16 weeks during periods of high demand. Processors planning aseptic line expansions are now required to secure seal supply agreements 6–9 months in advance, which complicates project timelines and increases inventory carrying costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Elastomers Balance Cost and Compliance

Elastomers held 34.47% of the food processing seals market revenue in 2025 and are on track for a 3.56% CAGR to 2031, supported by EPDM dominance in dairy and beverage plants that steam clean up to 150 °C. Nitrile serves meat lines where fat exposure is high, while alkaline cleaning in plant-based facilities accelerates migration to FKM and FFKM. Raw fluorspar inflation lifted fluoro-elastomer pricing by 12% in 2025, tightening budgets but reinforcing the switch because replacement downtime costs remain higher. PTFE occupies the high-temperature niche, providing chemical inertness to 260 °C, critical for UHT systems, and it is integral to PTFE-bellows mechanical seals used in dairy fillers. Detectable compounds embedded with ferrite particles are the fastest-growing sub-segment as retailers tighten foreign-object detection protocols.

By Seal Type: Mechanical Seals Gain as Automation Advances

O-rings retained 37.78% of the market revenue in 2025 given their ubiquity and standardization, yet mechanical seals are registering a 3.66% CAGR through 2031 as processors automate CIP/SIP. EagleBurgmann’s silicon-carbide faced seals deliver six-year service in UHT lines and illustrate how premium assemblies capture growth. Clamp gaskets remain vital for tool-free disassembly, particularly in bakery and snack plants where rapid flavor changeovers are routine. Shaft and lip seals serve mixers and conveyors, and diaphragm seals in aseptic valves must survive millions of cycles while maintaining sterility.

By Application: Processing Equipment Dominates, Cleaning Systems Surge

Processing equipment captured 55.12% of the food processing seals market share in 2025 and continues to anchor demand owing to the capital intensity of homogenizers, heat exchangers, and UHT lines. Packaging equipment, especially in high-speed carton and pouch fillers requires sterilizable seals. Cleaning systems are expanding at a 4.14% CAGR through 2031 as water-scarce regions mandate longer CIP cycles; FFKM seals in spray balls and valves enable 90-minute recirculated cleaning without leakage. Refrigeration and freezing equipment depend on cryogenic-rated PTFE and FKM to tolerate –40 °C operation in Asia-Pacific’s fast-growing cold-chain facilities.

By End-user Industry: Meat, Poultry, and Seafood Leads, Other End-user Industries Accelerate

Meat, poultry, and seafood industry represented 27.78% demand in 2025, led by robotic deboners and high-pressure washdown that use silicone-carbide mechanical seals for lubricant isolation. The other end-user industries segment, including fruits, vegetables, ready meals, snacks, posts a 4.10% CAGR through 2031 as tray-sealing lines adopt metal-detectable gaskets to satisfy retailer audits. Dairy and beverage processors align on FDA and 3-A compliant elastomers for UHT milk and plant-based drinks, with single-use changeovers driving seal consumption during flavor shifts.

Geography Analysis

Asia-Pacific held 43.34% revenue in 2025 and is advancing at a 4.08% CAGR to 2031, powered by India’s PLISFPI and China’s double-digit cold-chain warehouse growth[2]Ministry of Food Processing Industries, Government of India, “Production Linked Incentive Scheme,” mofpi.gov.in. India’s ₹40,000 crore AI-driven food parks and 394 sanctioned cold-chain projects each specify cryogenic PTFE seals for blast-freezers. China’s exporters demand FDA and EU-certified gaskets to access premium markets, while ASEAN seafood processors retrofit plants to EHEDG standards, fueling regional after-market demand.

North America’s demand is also growing as processors upgrade legacy equipment to comply with FSMA preventive controls, replacing undocumented seals with traceable FFKM parts. Capital programs such as Nestlé Purina’s USD 500 million wet pet-food plant in Brazil still mirror U.S. material standards, reinforcing cross-border demand for high-grade seals.

Europe’s mature processors emphasize specialty compounds for ultra-hygienic dairy and confectionery plants, and the Nordic region targets seals with extended service life to meet sustainability metrics. South America’s growth pivots on Brazil’s frozen-potato and dairy expansions, where blast freezers require low-temperature fluoro-elastomers. The Middle-East upgrades seal inventories in line with SFDA’s digital HACCP tools, and South Africa’s beverage sector adopts FFKM seals for long-life UHT milk distributed in rural areas without continuous refrigeration.

Competitive Landscape

The market exhibits moderate concentration, with top players including Parker Hannifin, Freudenberg, Trelleborg, Flowserve Corporation, and John Crane. Their advantage stems from certified clean-room production, in-house compound development, and the ability to supply identical parts across continents under FDA, EU, 3-A, and EHEDG approvals. Mid-tier firms such as James Walker and Precision Polymer Engineering compete by offering custom detectable elastomers and rapid prototypes, while scores of regional molders fight on lead time and price for standard EPDM O-rings.

Technology differentiation centers on alkaline-resistant EPDM, low-temperature FKM, and metal-detectable FFKM. John Crane’s 2026 QOGI survey collected real-time reliability data that feed back into seal-monitoring dashboards linked to predictive maintenance systems. Trelleborg’s FoodPro portfolio underlines full regulatory dossiers that shorten customer audits and speed qualification cycles.

Emerging disruptors include 3D-printed FFKM prototype houses and startups exploring bio-based elastomers to satisfy sustainability mandates. Adhesive-less hygienic clamps pose a structural threat in ultra-hygienic niches, but machining cost and stringent flatness tolerances limit scale for now. Compliance frameworks remain a formidable moat, as processors rarely risk uncertified components given the recall ramifications.

Food Processing Seals Industry Leaders

Trelleborg AB

Flowserve Corporation

John Crane

Freudenberg Sealing Technologies

PARKER HANNIFIN CORP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Freudenberg Sealing Technologies in India announced the establishment of a new manufacturing facility in Bengaluru, Karnataka. This greenfield investment enhanced production capacity by 30% and spanned 30,000 square meters (323,000 square feet), integrating advanced manufacturing capabilities, including polytetrafluoroethylene (PTFE) products, rotary shaft seals, mechanical face seals, polyurethane (PU), and other sealing solutions for various industries globally.

- June 2025: Trelleborg AB announced advancements in environmentally friendly sealing materials, emphasizing reduced environmental impact and the transition away from PFAS. The company introduced improved surface coating technologies, including Seal-Glide, which were PFAS-free and designed for durability in automotive, aerospace, and medical applications.

Global Food Processing Seals Market Report Scope

Food processing seals are specialized food-grade components, such as O-rings, gaskets, and lip seals, designed to prevent contamination, endure high-temperature sanitation processes like CIP (Clean-in-Place) and SIP (Sterilize-in-Place), and resist exposure to food fats and cleaning chemicals. Key standards include FDA, 3-A Sanitary Standards, and EHEDG, which ensure the absence of crevices that could promote bacterial growth.

The Food Processing Seals Market is segmented into material type, seal type, application, end-user industry, and geography. By material type, the market is segmented into elastomers, polytetrafluoroethylene (PTFE), polyurethane, and other material types (e.g., metal-detectable or X-ray-detectable materials). By seal type, the market is segmented into O-rings, gaskets, lip seals, mechanical seals, diaphragms, shaft/rotary seals, and hygienic clamp seals and tri-clamp gaskets. By application, the market is segmented into processing equipment, packaging equipment, cleaning systems (CIP/SIP), and refrigeration and freezing equipment. By end-user industry, the market is segmented into meat, poultry, and seafood, bakery and confectionery, dairy products, beverage, and other end-user industries (e.g., fruits and vegetables, ready meals, and snacks). The report also covers the market size and forecasts for food processing seals in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Elastomers |

| Polytetrafluoroethylene (PTFE) |

| Polyurethane |

| Other Material Types (metal-detectable or X-ray-able materials) |

| O-rings |

| Gaskets |

| Lip Seals |

| Mechanical Seals |

| Diaphragms |

| Shaft/Rotary Seals |

| Hygienic Clamp Seals and Tri-Clamp Gaskets |

| Processing Equipment |

| Packaging Equipment |

| Cleaning Systems (CIP/SIP) |

| Refrigeration and Freezing Equipment |

| Meat, Poultry and Seafood |

| Bakery and Confectionery |

| Dairy Products |

| Beverage |

| Other End-user Industries (Fruits and Vegetables, Ready Meals and Snacks, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Elastomers | |

| Polytetrafluoroethylene (PTFE) | ||

| Polyurethane | ||

| Other Material Types (metal-detectable or X-ray-able materials) | ||

| By Seal Type | O-rings | |

| Gaskets | ||

| Lip Seals | ||

| Mechanical Seals | ||

| Diaphragms | ||

| Shaft/Rotary Seals | ||

| Hygienic Clamp Seals and Tri-Clamp Gaskets | ||

| By Application | Processing Equipment | |

| Packaging Equipment | ||

| Cleaning Systems (CIP/SIP) | ||

| Refrigeration and Freezing Equipment | ||

| By End-user Industry | Meat, Poultry and Seafood | |

| Bakery and Confectionery | ||

| Dairy Products | ||

| Beverage | ||

| Other End-user Industries (Fruits and Vegetables, Ready Meals and Snacks, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the food processing seals market?

The food processing seals market stands at USD 3.60 billion in 2026 and is projected to reach USD 4.23 billion by 2031.

Which region contributed the largest revenue in 2025?

Asia-Pacific contributed 43.34% of 2025 revenue.

What segment holds the highest market share by seal type in 2025?

O-rings commanded 37.78% share in 2025.

Why are FFKM seals gaining popularity in food plants?

FFKM withstands alkaline cleaning, high temperatures, and aseptic conditions that degrade standard elastomers, enabling longer service life.

Page last updated on: