Body Contouring Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

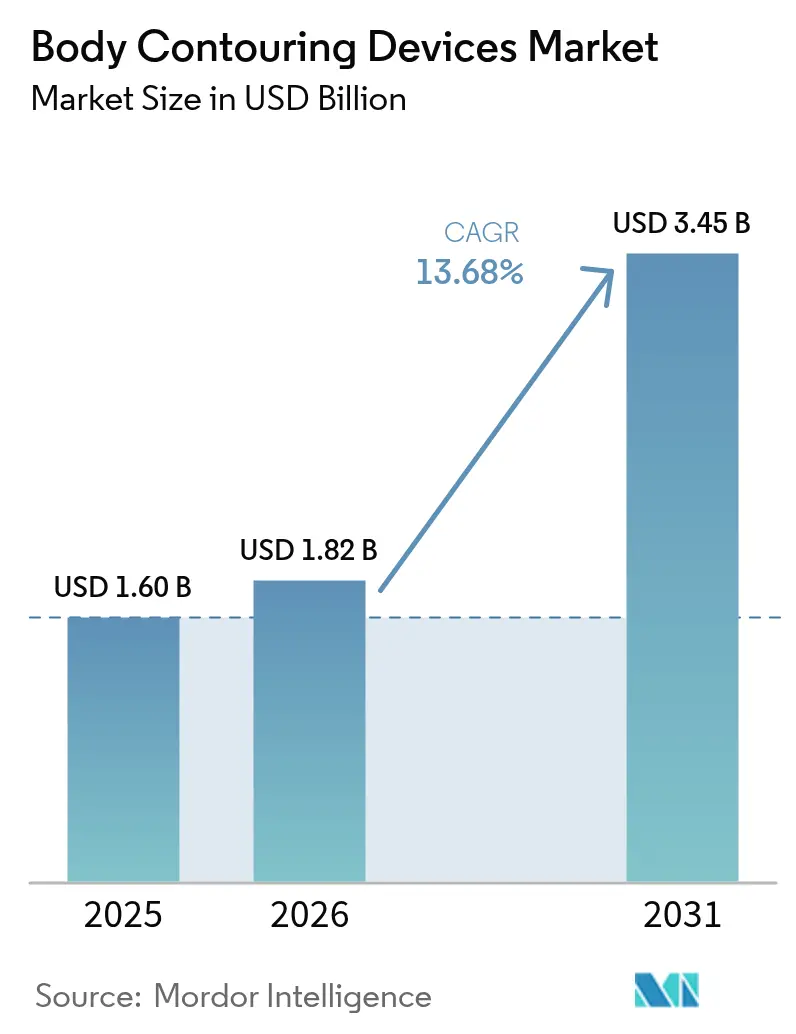

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 3.45 Billion |

| Growth Rate (2026 - 2031) | 13.68% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Body Contouring Devices Market Analysis by Mordor Intelligence

The body contouring devices market size was valued at USD 1.60 billion in 2025 and estimated to grow from USD 1.82 billion in 2026 to reach USD 3.45 billion by 2031, at a CAGR of 13.68% during the forecast period (2026-2031). Rapid uptake of non-invasive technologies, rising aesthetic awareness among younger adults and converging radiofrequency, cryolipolysis and high-intensity focused electromagnetic (HIFEM) capabilities are energising growth. Providers now bundle fat reduction, muscle toning and skin tightening into single sessions, shortening recovery times and widening the consumer base. Medical spas are formalising subscription programmes that lower per-visit fees while locking in recurring revenue. Meanwhile, hospitals invest in multi-application platforms to protect market share, and vendors integrate artificial-intelligence-driven dose settings that improve procedural consistency. Persistent supply-chain pressures and evolving regulatory demands temper momentum but do not alter the structural shift toward convenience-led, technology-enhanced body shaping solutions.

Key Report Takeaways

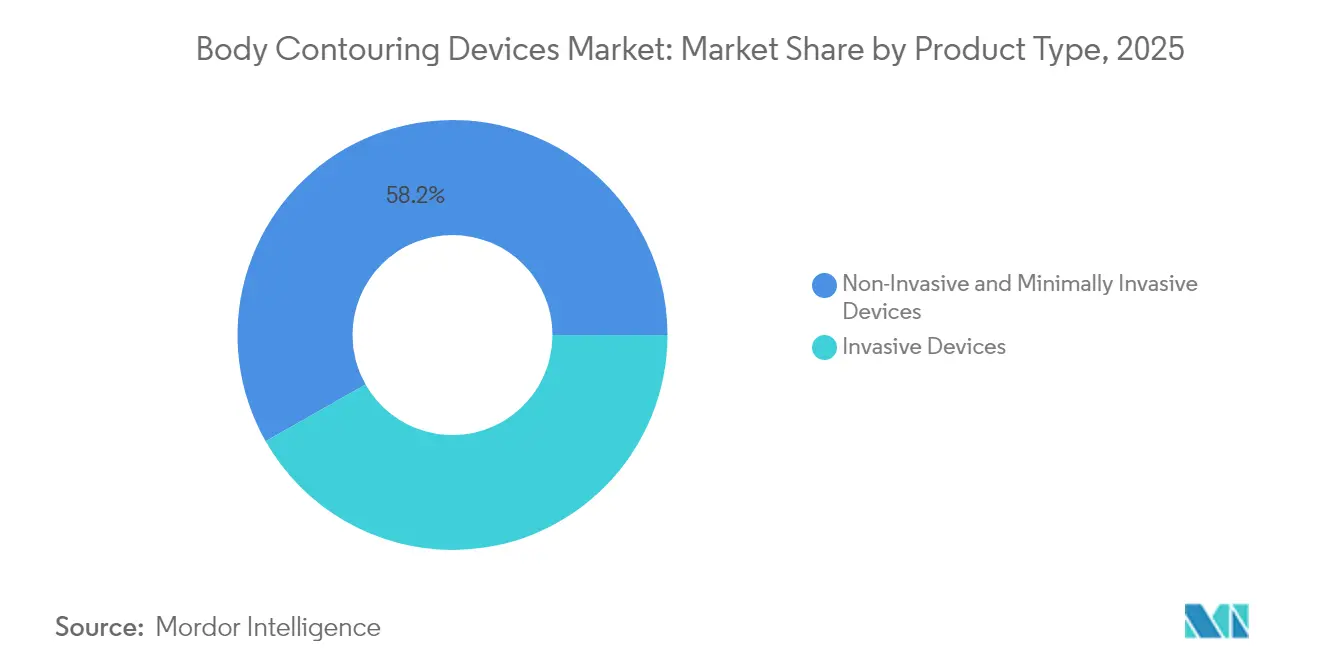

- By product type, non-invasive and minimally invasive systems captured 58.23% body contouring devices market share in 2025, and their 17.95% CAGR up to 2031 is the fastest among all categories.

- By application, skin tightening and cellulite reduction held 41.93% of the body contouring devices market size in 2025; muscle toning and definition is projected to accelerate at 18.33% CAGR through 2031.

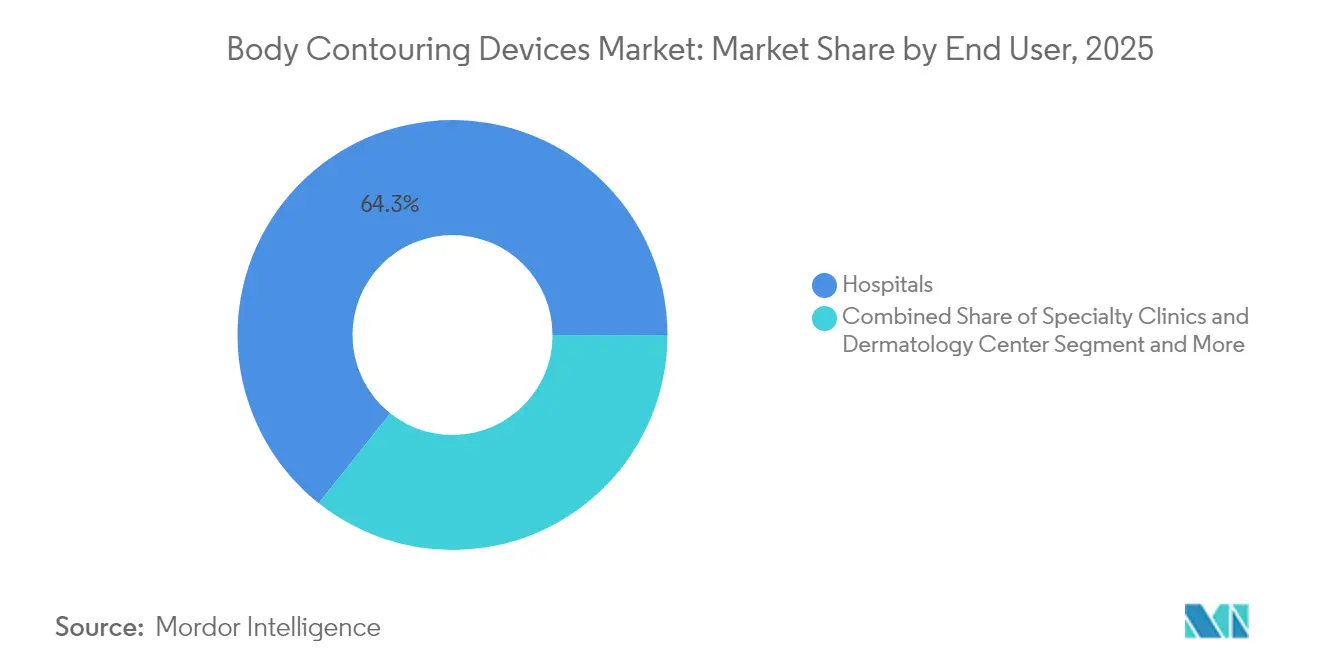

- By end user, hospitals retained 64.31% revenue in 2025, whereas medical spas record the strongest expansion at 16.9% CAGR to 2031.

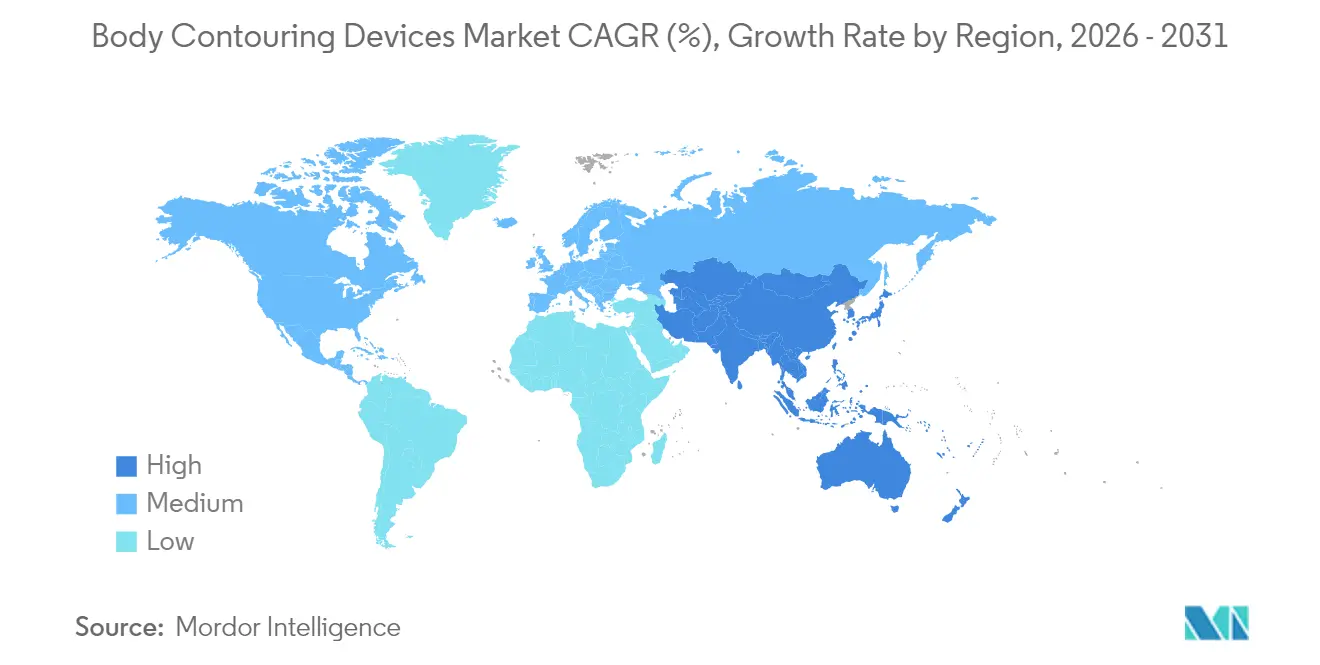

- By geography, North America dominated with 39.42% revenue in 2025, yet Asia-Pacific is forecast to rise at 17.05% CAGR, the highest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Body Contouring Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Minimally Invasive & Non-Invasive Procedures | +3.2% | Global, with North America & Europe leading | Medium term (2-4 years) |

| Technological Advancements in RF, Cryolipolysis & HIFEM | +2.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Rising Prevalence of Obesity & Aesthetic Consciousness | +2.1% | Global, particularly Asia-Pacific & North America | Long term (≥ 4 years) |

| Expanding Medical Tourism in Emerging Economies | +1.9% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| AI-Enabled Personalised Treatment Protocols | +1.5% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Subscription-Based Med-Spa Business Models | +1.3% | North America & Europe primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Minimally Invasive & Non-Invasive Procedures

Patient preference has pivoted firmly toward less disruptive approaches that reduce downtime and visible bruising. Cryolipolysis devices, for example, can trim 20–25% of subcutaneous fat after a single session, while patient-reported pain scores remain low[1]Allergan Aesthetics, “CoolSculpting | Fat Freezing Technology,” Allergan Aesthetics, allerganaesthetics.com. Post-pandemic self-scrutiny amplified demand, and a 2024 survey showed that 63% of facial-aesthetic clients were first-time entrants to medical aesthetics. Multi-modality workstations now fuse HIFEM with radiofrequency, letting clinicians offer simultaneous muscle toning and fat lysis in under 30 minutes. Medical spas scale these offerings through loyalty memberships, and early trials of at-home suction-RF-EMS gadgets demonstrate measurable circumference loss, suggesting a future omnichannel ecosystem.

Technological Advancements in RF, Cryolipolysis & HIFEM

Engineering improvements focus on deeper, more uniform energy delivery and broader patient suitability. A next-generation HIFEM platform recently secured two additional FDA clearances covering darker Fitzpatrick skin types and lateral-thigh lipolysis, with MRI studies confirming 1.4 cm average fat-layer reduction. Fractionated RF handpieces now penetrate variable tissue depths, enabling precise collagen remodelling. Laboratory work on cerium-doped calcium carbonate particles paired with low-intensity ultrasound hints at a non-thermal pathway for adipocyte apoptosis[2]Jhih-Ni Lin et al., “Cerium-Doped Calcium Carbonate Microparticles Combined with Low-Intensity Ultrasound for Efficient Sonodynamic Therapy,” Journal of Biological Engineering, springeropen.com. These breakthroughs underpin the body contouring devices market as manufacturers race to patent differentiated heat, cold or electromagnetic algorithms that promise consistent outcomes.

Rising Prevalence of Obesity & Aesthetic Consciousness

Obesity affects more than 1 billion adults worldwide, generating a large pool of individuals seeking adjunct procedures after pharmacological or surgical weight loss. Up to 96% of bariatric-surgery recipients experience redundant skin folds that impact mobility and hygiene, fuelling demand for tightening technologies. Concurrently, adoption of GLP-1 agonists such as semaglutide often reveals residual contour irregularities, motivating clients to pursue non-invasive sculpting to refine body lines. Demographically, 54% of female med-spa visitors fall between 35-54 years, indicating a prolonged consumer runway.

Expanding Medical Tourism in Emerging Economies

Affordable pricing, reputable surgeons and favourable visa policies make several Asia-Pacific nations popular for elective aesthetic care. India now ranks among the top three countries for liposuction volume. Thailand bundles hospital stays with recovery-hotel packages to capture high-spending travellers, while regional governments actively market medical hubs at international trade shows. Although post-procedure follow-up complexity persists, cross-border patient flows enlarge the addressable customer base for equipment vendors and service providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Devices & Procedures | -2.1% | Global, particularly emerging markets | Medium term (2-4 years) |

| Stringent Regulatory & Safety Compliance Requirements | -1.8% | North America & EU primarily | Long term (≥ 4 years) |

| Shortage of Qualified Aesthetic Practitioners | -1.5% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Semiconductor Supply-Chain Volatility | -1.2% | Global, concentrated in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Devices & Procedures

Premium multi-modality systems can exceed USD 100,000, a figure that rises once training, disposables and annual maintenance contracts are included. Public filings from a leading manufacturer revealed that supply-chain expenses now equate to 20% of revenue, forcing aggressive cost-optimisation programmes. Smaller clinics in emerging economies struggle to attain payback within the typical 18-month horizon, hindering penetration into price-sensitive segments.

Stringent Regulatory & Safety Compliance Requirements

The FDA’s 2024 draft guidance on thermal-effect evaluation introduced additional pre-market testing layers for devices that heat or cool tissue[3]U.S. Food and Drug Administration, “Medical Device Supply Chain and Shortages,” FDA, fda.gov. In parallel, the European Union Medical Device Regulation mandates continuous post-market clinical follow-up, extending certification cycles and lifting compliance budgets. Cyber-security risk assessments have also become compulsory, adding documentation overhead that disproportionately burdens start-ups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Invasive Technologies Drive Market Evolution

Non-invasive platforms owned 58.23% of 2025 revenue, and this share is forecast to widen as the category propels an 17.95% CAGR through 2031 in the body contouring devices market. Cryolipolysis heads the field, with real-world studies confirming 20–25% single-session fat volume reduction. HIFEM-RF hybrids further expand use-cases by delivering concurrent adipocyte apoptosis and myofibril hypertrophy. Invasive devices such as power-assisted liposuction remain vital for substantial debulking but grow at a slower clip as patients increasingly favour lunchtime procedures.

The competitive edge within non-invasive systems now lies in applicator ergonomics, cooling efficiency and electromagnetic field homogeneity. Vendors file rapid-fire patents around sensor-based temperature cut-offs and closed-loop impedance monitoring. Meanwhile, ultrasound-assisted lipoplasty evolves to address dense fibrous fat with lower ecchymosis, keeping an important albeit niche foothold in the body contouring devices industry.

By Application: Muscle Toning Emerges as Growth Driver

Skin tightening and cellulite reduction retained 41.93% of 2025 revenue, yet muscle-toning treatments will accelerate fastest at 18.33% CAGR, mirroring consumer interest in athletic aesthetics. MRI assessments document up to 25% muscle growth after a standard four-session HIFEM protocol, which lifts repeat-purchase intent. Fat-reduction applications sustain demand thanks to continual improvements in selective adipolysis and post-lipolysis lymphatic mobilisation.

Integration with pharmacological weight-management regimens enlarges total market opportunity. Practitioners pair GLP-1 treatments with non-invasive tightening to tackle lax skin, creating combined packages that command premium pricing. Post-bariatric patients, numbering more than 350,000 annually worldwide, often undergo staged contouring, underscoring long-tail demand inside the body contouring devices market.

By End User: Medical Spas Challenge Hospital Dominance

Hospitals generated 64.31% of 2025 sales due to broad service portfolios and established referral channels. Yet medical spas will outpace all other settings at 16.9% CAGR to 2031, reflecting consumer appetite for boutique experiences and membership discounts. Repeat-visit ratios exceed 70%, and the subscription model boosts utilisation of high-capital devices.

Specialty dermatology clinics bridge medical rigour and spa-like ambience, offering physician oversight with flexible scheduling. Home-use handhelds that pair suction with low-power RF extend basic contouring into living rooms, although professional supervision remains central for deeper tissue-remodelling objectives. Collectively, these shifts reshape procurement patterns and training curricula within the body contouring devices market.

Geography Analysis

North America accounted for 39.42% of 2025 revenue, underpinned by sophisticated aesthetic-medicine infrastructure and robust discretionary spending. United States physicians increasingly embed body contouring into multidisciplinary obesity-care pathways, aided by the surge in weight-loss drug prescriptions. Canada smooths device adoption through technology-specific regulatory fast-tracks, while cross-border clients from Mexico bolster procedure volumes.

Europe offers a deeply regulated yet opportunity-rich landscape. Uniform MDR rules elevate safety standards and filter sub-par devices, fostering practitioner trust. Germany, France and the United Kingdom anchor demand, and rising retirement-age populations with higher disposable savings pursue combined tightening and fat-reduction packages. Clinics leverage pan-European distributor networks to secure service cover and parts supply, safeguarding uptime amid supply-chain uncertainties.

Asia-Pacific delivers the fastest trajectory at a projected 17.05% CAGR to 2031 in the body contouring devices market. Rapid urbanisation and social-media-driven beauty ideals propel procedure counts in China, South Korea and Japan. India’s speciality hospitals capture international clients seeking competitively priced liposuction and sculpting bundles, while Thailand positions itself as a recovery-tourism haven. Domestic manufacturers in China pilot cost-competitive RF machines that could challenge incumbents if international certifications are achieved.

Competitive Landscape

Competition is moderate: the top five players jointly hold significant revenue, leaving room for regional challengers. AbbVie’s CoolSculpting franchise leverages brand recognition and a service-heavy consumable model to defend pricing. BTL Industries dominates HIFEM intellectual property, supporting premium positioning. InMode cross-sells RF platforms into plastic-surgery and dermatology channels, maximising system utilisation.

Strategic mergers focus on pooling R&D pipelines and global distribution. Several manufacturers introduce AI-guided pulse algorithms to lock in future competitive moats, and at least two vendors have shifted to device-rental or per-treatment-fee schemes that lower customer cap-ex barriers. Companies with strong service footprints bundle extended warranties and technician training, reinforcing stickiness. Financially, the industry remains capital-intensive; recent debt restructurings highlight the need for cash-flow resilience when economic cycles soften equipment demand in the body contouring devices market.

Body Contouring Devices Industry Leaders

Hologic Inc. (Cynosure)

Bausch Health Companies Inc

Boston Scientific Corp. (Lumenis)

AbbVie Inc. (Allergan Aesthetics)

Candela Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Rejuva Fresh LLC introduced EMSHAPE NEO PLUS, an enhanced electromagnetic platform emphasising operator-free muscle toning.

- March 2025: Apyx Medical Corporation obtained 510(k) clearance for the AYON Body Contouring System, integrating ultrasound-assisted aspiration with bipolar RF.

Global Body Contouring Devices Market Report Scope

Body contouring devices are used in procedures that alter the body shape. It includes various steps that eliminate excess skin and fat, which remains after losing weight in people who are obese earlier. Body contouring helps reduce fat in different places such as the arms, breasts, tummy, thighs, face, etc. The body contouring devices market is segmented by product type (minimally invasive and non-invasive devices (radiofrequency body contouring devices, ultrasound body contouring devices, laser-assisted body contouring devices), invasive devices), application (fat reduction, skin tightening, others), end-user (hospitals, clinics, others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Non-Invasive & Minimally Invasive Devices | Cryolipolysis Systems |

| Radiofrequency Devices | |

| Laser-Assisted Lipolysis Devices | |

| HIFEM Devices | |

| Ultrasound Cavitation Devices | |

| Other Emerging Modalities | |

| Invasive Devices | Power-Assisted Liposuction Systems |

| Ultrasound-Assisted Liposuction | |

| Laser-Assisted Liposuction | |

| Tumescent Liposuction Systems | |

| Other Invasive Systems |

| Fat Reduction |

| Skin Tightening & Cellulite Reduction |

| Muscle Toning & Definition |

| Post-Bariatric Body Contouring |

| Other Niche Applications |

| Hospitals |

| Specialty Clinics & Dermatology Centers |

| Medical Spas |

| Ambulatory Surgical Centers |

| Home-Use / At-Home Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Non-Invasive & Minimally Invasive Devices | Cryolipolysis Systems |

| Radiofrequency Devices | ||

| Laser-Assisted Lipolysis Devices | ||

| HIFEM Devices | ||

| Ultrasound Cavitation Devices | ||

| Other Emerging Modalities | ||

| Invasive Devices | Power-Assisted Liposuction Systems | |

| Ultrasound-Assisted Liposuction | ||

| Laser-Assisted Liposuction | ||

| Tumescent Liposuction Systems | ||

| Other Invasive Systems | ||

| By Application | Fat Reduction | |

| Skin Tightening & Cellulite Reduction | ||

| Muscle Toning & Definition | ||

| Post-Bariatric Body Contouring | ||

| Other Niche Applications | ||

| By End-User | Hospitals | |

| Specialty Clinics & Dermatology Centers | ||

| Medical Spas | ||

| Ambulatory Surgical Centers | ||

| Home-Use / At-Home Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the body contouring devices market?

The market is worth USD 1.82 billion in 2026 and is projected to reach USD 3.45 billion by 2031.

Which technology segment is growing fastest?

Non-invasive and minimally invasive devices, led by cryolipolysis and HIFEM platforms, are expanding at an 17.95% CAGR.

Why are medical spas gaining share?

Subscription plans, shorter treatment times and a lifestyle-oriented environment make medical spas attractive, driving a 16.9% CAGR for the channel.

Which region offers the highest growth potential?

Asia-Pacific is projected to advance at a 17.05% CAGR, underpinned by rising disposable incomes and medical-tourism inflows.

How do regulatory changes affect device manufacturers?

Stricter FDA and EU MDR guidelines increase testing costs and prolong approval timelines, imposing a heavier burden on smaller innovators.

Page last updated on: