Hepatitis Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.03 Billion |

| Market Size (2031) | USD 21.29 Billion |

| Growth Rate (2026 - 2031) | 3.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

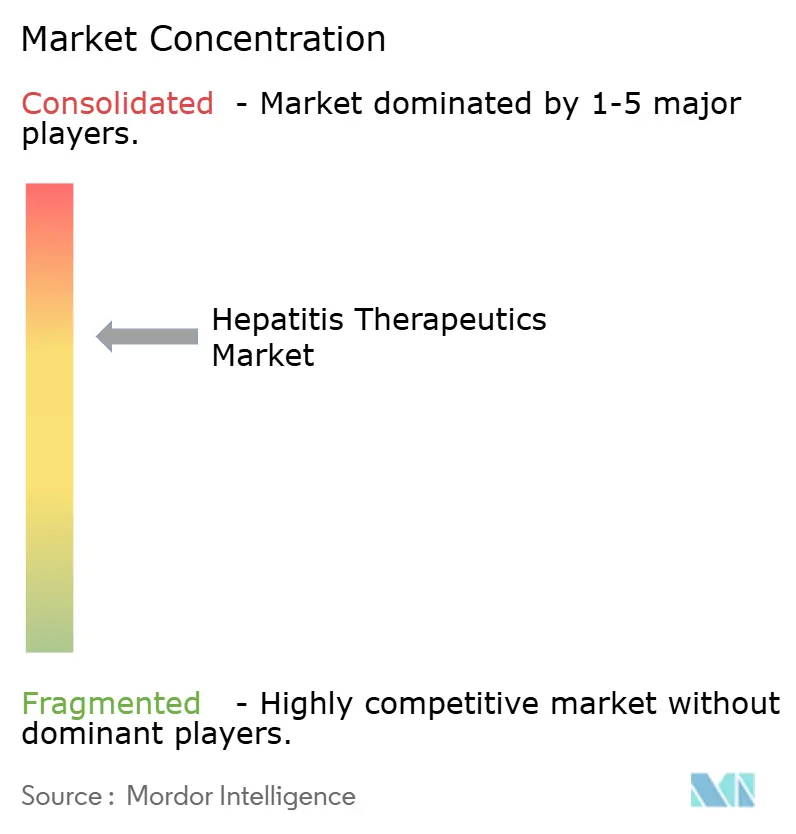

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hepatitis Therapeutics Market Analysis by Mordor Intelligence

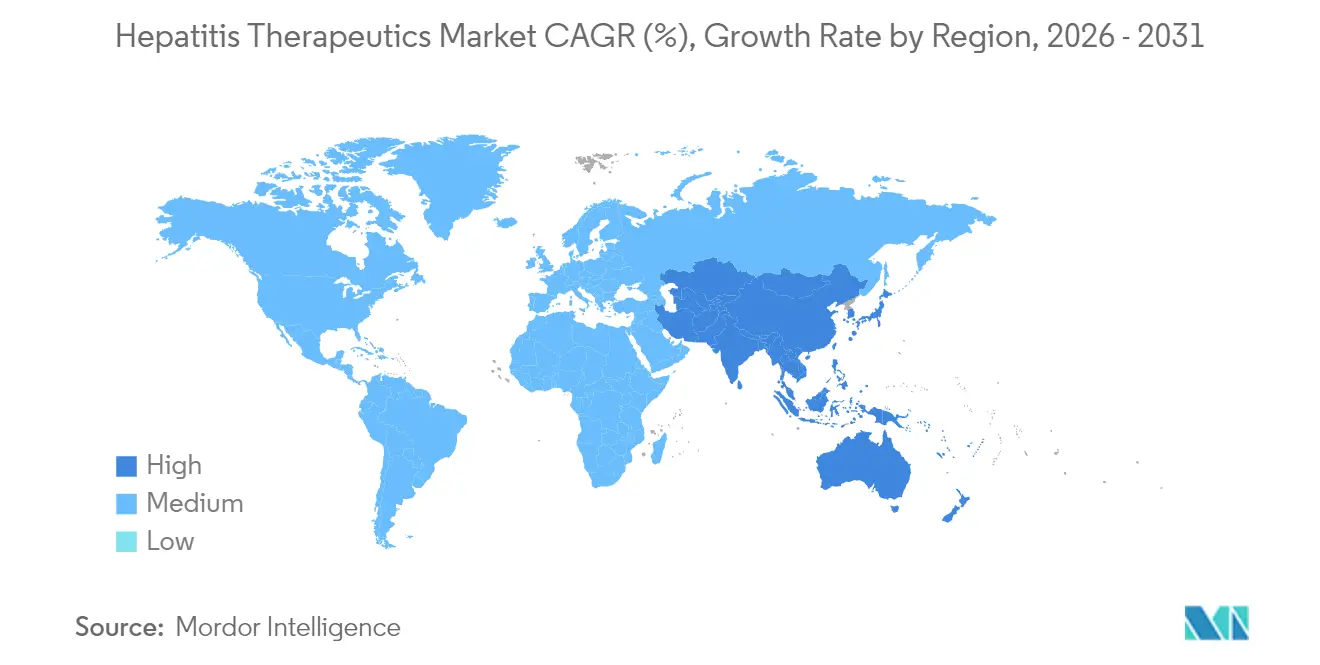

The hepatitis therapeutics market size is expected to grow from USD 17.44 billion in 2025 to USD 18.03 billion in 2026 and is forecast to reach USD 21.29 billion by 2031 at 3.39% CAGR over 2026-2031. This growth trajectory hides a structural pivot from suppressive regimens toward functional-cure combinations that attack viral replication, immune evasion, and host-factor interactions in parallel. Subscription-style procurement in Louisiana, which treated more than 11,000 residents at negotiated prices, demonstrates how value-based models can unlock latent demand while containing budget impact. In parallel, the WHO’s 2024 report that viral hepatitis now causes 1.3 million annual deaths, second only to tuberculosis, has accelerated elimination roadmaps and lifted diagnosis targets worldwide. North America continues to anchor 40.59% of global revenue. Yet, Asia-Pacific delivers the fastest regional expansion at 4.64% CAGR thanks to China and India’s combined hepatitis B and C caseload exceeding 35 million.

Key Report Takeaways

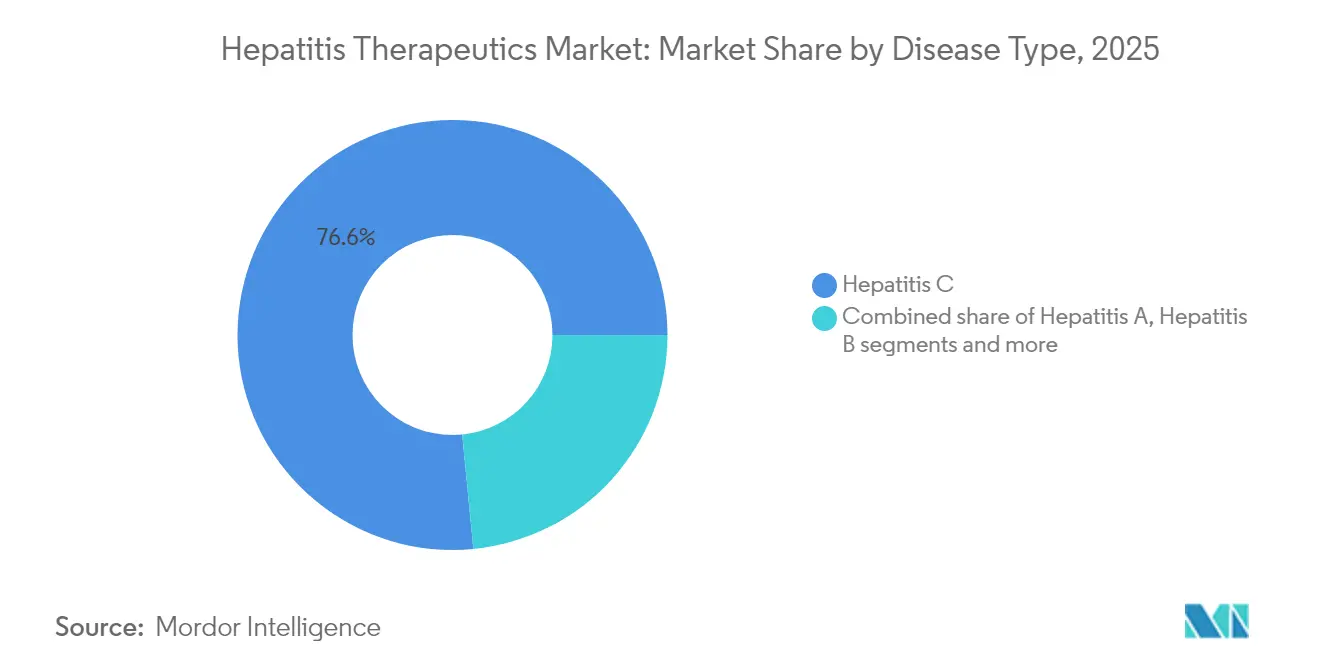

- By disease type, hepatitis C led with 76.55% revenue share in 2025, while hepatitis B is projected to expand at a 4.78% CAGR through 2031.

- By drug class, NS5A inhibitors commanded 34.61% of the hepatitis therapeutics market share in 2025; monoclonal antibodies post the highest forecast CAGR at 4.16%.

- By route of administration, oral therapies accounted for 94.12% of revenue in 2025; injectables lag but remain essential in combination regimens.

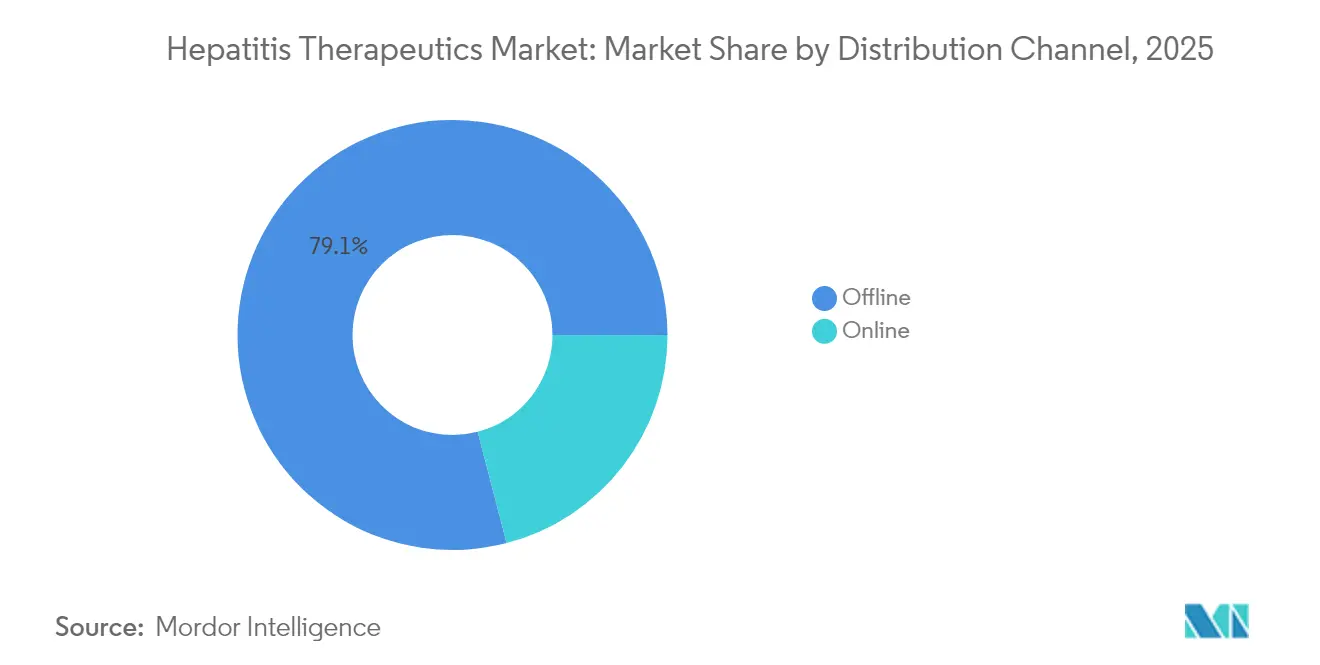

- By distribution channel, the offline segment held 79.05% share of the hepatitis therapeutics market size in 2025, whereas the online segment is set to record a 5.05% CAGR to 2031.

- By end-user, hospitals captured 61.62% revenue share in 2025; home-care settings represent the fastest-growing end-user cohort with 4.51% CAGR to 2031.

- By geography, North America accounted for 40.15% of the hepatitis therapeutics market size in 2025, while Asia-Pacific is the fastest-advancing region, forecast at 4.42% CAGR, propelled by intensified screening and treatment campaigns in China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hepatitis Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of viral hepatitis | +0.8% | Global, concentrated in Asia-Pacific and Sub-Saharan Africa | Long term (≥ 4 years) |

| Rapid launch of pan-genotypic DAA regimens | +0.7% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Government-led awareness campaigns | +0.6% | Global, with accelerated impact in LMICs | Medium term (2-4 years) |

| Expanding reimbursement in high-income countries | +0.5% | North America & EU primarily | Medium term (2-4 years) |

| Rise of pay-for-cure value-based contracts | +0.4% | North America, pilot programs in EU | Short term (≤ 2 years) |

| AI-enabled drug-repurposing pipelines | +0.3% | Global, led by North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Viral Hepatitis

More than 304 million people live with chronic hepatitis B or C, a pool that sustains long-run demand independent of economic fluctuations. China and India contribute over 35 million cases, positioning Asia-Pacific as the principal growth engine for the hepatitis therapeutics market. Only 13% of chronic hepatitis B infections are diagnosed[1]UN News, “Hepatitis Killing Thousands Daily, WHO Warns in New Report,” news.un.org., and a mere 3% receive antiviral therapy, underscoring how underdiagnosis continues to inflate unmet need. Mortality is rising even where incidence is falling, revealing gaps in screening and linkage-to-care pathways that governments now frame as public-health emergencies. These epidemiological realities fortify long-term volume growth for companies able to scale affordable, decentralized treatment models.

Rapid Launch of Pan-Genotypic DAA Regimens

Eight-week pan-genotypic combinations have condensed treatment courses and removed the need for genotype testing in most settings. AbbVie’s MAVYRET received FDA clearance as the first 8-week therapy for acute hepatitis C, recording a 96% cure rate while slashing clinic visits. Atea Pharmaceuticals’ bemnifosbuvir-ruzasvir combo[2]Atea Pharmaceuticals, “Atea Pharmaceuticals Announces Positive Results from Phase 2 Study of Bemnifosbuvir and Ruzasvir Regimen for Treatment of Hepatitis C Virus,” ir.ateapharma.com. posted a 98% sustained virologic response in Phase 2 and is moving into Phase 3 in 2025. Shorter regimens reduce loss-to-follow-up and ease scale-up in rural clinics, enhancing the hepatitis therapeutics market’s penetration potential.

Government-Led Awareness Campaigns & Vaccination Drives

National hepatitis elimination plans are shifting from aspirational policies to operational rollouts that couple integrated screening with universal-access treatment. West Bengal’s “Triple Elimination” initiative, which targets vertical transmission of hepatitis B alongside HIV and syphilis by 2026, is emblematic of programs that create immediate spikes in newly diagnosed patients. The WHO’s 2024 call for a mid-decade progress check has pushed ministries of health to budget for expanded diagnostic capacity and broader drug formularies. As eligibility widens, manufacturers with simple oral dosing and broad genotype coverage enjoy first-mover advantages in newly formed procurement pools.

Expanding Reimbursement in High-Income Countries

Ninety-one percent of countries have authorized at least one DAA, yet only 68% reimburse therapy, making payer decisions the final gateway to market volume. Australia’s risk-share pact for DAAs and the United States’ multiyear budget line for a national hepatitis C elimination plan showcase how outcomes-based financing transforms episodic access into predictable demand pipelines. Such frameworks lower out-of-pocket costs, lift initiation rates, and provide manufacturers with clearer revenue visibility that justifies continued R&D spending.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uneven reimbursement in emerging economies | -0.6% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Stringent regulatory approval timelines | -0.4% | Global, most acute in North America & EU | Medium term (2-4 years) |

| Stigma-driven under-diagnosis in PWID populations | -0.3% | Global, particularly acute in LMICs | Long term (≥ 4 years) |

| API supply-chain concentration risk in LMICs | -0.2% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uneven Reimbursement in Emerging Economies

Only 52% of low- and middle-income countries reimburse DAA therapy, with many imposing specialist-only prescribing rules that narrow access channels. Development Impact Bond pilots in Cameroon achieved 96% cure rates but remain localized, indicating innovative finance alone cannot overcome systemic funding gaps. These disparities create a two-tier hepatitis therapeutics market where ability to pay, not disease burden, dictates uptake, limiting upside in regions with the largest patient pools.

Stringent Regulatory Approval Timelines

Functional-cure candidates must demonstrate durable antigen clearance, extending trial follow-up and complicating endpoint selection. Bulevirtide secured European approval for hepatitis D in 2020, yet a 2024 FDA complete-response letter shows how divergent standards delay U.S. entry. The emergence of combination therapies targeting multiple viral mechanisms[3]Maria Buti, “Sequential Peg-IFN after Bepirovirsen May Reduce Post-Treatment Relapse in Chronic Hepatitis B,” PubMed, pubmed.ncbi.nlm.nih.gov simultaneously compounds regulatory complexity. Longer timelines inflate capital needs and tilt competitive advantage toward firms with deep balance sheets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Hepatitis C Dominance Masks Accelerating B Momentum

Hepatitis C retained 76.55% revenue in 2025, underpinned by pan-genotypic regimens exceeding 95% cure rates. Nevertheless, hepatitis B is projected to outpace all other indications at 4.78% CAGR through 2031 as RNA interference, monoclonal antibodies, and capsid-assembly modulators converge in multi-agent protocols aimed at surface-antigen loss. The hepatitis therapeutics market size for hepatitis B therapies is on a steady growth trajectory, with multiple Phase 2 and 3 trials targeting HBsAg clearance through novel mechanisms, reinforcing the strategic shift underway.

As functional-cure expectations rise, manufacturers are reprioritizing pipeline capital toward B-specific platforms. Clinical programs such as Arbutus Biopharma’s imdusiran, which delivered a 50% functional cure rate in Phase 2a, highlight the commercial upside available to successful entrants. Hepatitis D, while niche, offers a precedent for accelerated adoption once first-in-class therapies clear regulatory hurdles.

By Drug Class: NS5A Leadership Gives Way to Monoclonal Upswing

NS5A inhibitors accounted for 34.61% revenue in 2025, anchored by sofosbuvir/velpatasvir’s 98% cure performance across genotypes. Yet monoclonal antibodies are forecast to grow 4.16% CAGR, the fastest among classes, propelled by candidates such as GIGA-2339, which combines more than 1,000 anti-HBs antibodies and exhibits 2,000-fold greater potency than current options. Multi-class cocktails pairing nucleo(t)ide reverse-transcriptase inhibitors with novel agents form the centerpiece of future filings.

For late-entry competitors, platform breadth outweighs single-asset strength. Firms able to assemble NS5A, siRNA, and antibody assets under one roof can tailor regimens to genotype, fibrosis stage, and prior therapy resistance, deepening share of wallet across the hepatitis therapeutics market.

By Route of Administration: Oral Formulations Sustain Decentralized Care

Oral drugs generated 94.12% of 2025 sales and are projected at 3.60% CAGR through 2031. Once-daily glecaprevir/pibrentasvir delivers 97-100% sustained virologic response rates without injections, aligning perfectly with tele-hepatology models. Injectable agents preserve relevance in functional-cure combos where long-acting delivery can dampen viral rebound post-antigen clearance.

The hepatitis therapeutics market now blends clinical efficacy with service design: Oregon’s telemedicine trial enrolled 85% of eligible patients remotely, quadrupling initiation versus standard referral pathways. Manufacturers who co-develop oral regimens with remote monitoring kits stand to capture outsized loyalty among payers seeking cost-efficient scale-up.

By Distribution Channel: Offline Dominance, Online Velocity

Offline segment held 79.05% of global revenue in 2025, reflecting specialist counseling mandates and cold-chain dependencies for certain injectables. Online segment, however, are on track for 5.05% CAGR as regulatory reforms permit e-prescribing of specialty antivirals and as integrated telehealth ecosystems gain physician trust. Amazon Pharmacy and CVS Health have invested in virtual consult plus doorstep delivery programs that compress initiation timeframes, improving adherence and real-world cure rates.

A multi-node supply chain offers manufacturers superior pharmacovigilance data, enhancing post-market surveillance and payer negotiations. As electronic platforms mature, the hepatitis therapeutics market is expected to witness hybrid distribution models where first fill happens through specialty hubs and refills migrate online.

By End-User: Hospital Leadership, Home-Care Upsurge

Hospitals generated 61.62% of revenue in 2025 because advanced fibrosis, cirrhosis, and co-infection cases still demand multidisciplinary oversight. Yet home-care settings will compound at 4.51% CAGR as simplified dosing and remote monitoring lower clinical-visit burdens. Australia’s nurse-led telehealth initiative recorded an 88% treatment rate and 67% completion among rural patients, cutting travel costs and expediting viral clearance timelines.

The hepatitis therapeutics industry is increasingly designing patient-starter packs that include drug, adherence tools, and virtual support. Such kits allow payers to shift care away from high-cost tertiary centers toward primary-care or home-based management without sacrificing outcomes, strengthening total addressable volume.

Geography Analysis

North America held 40.15% of revenue in 2025 and advances at 3.30% CAGR to 2031. Subscription contracts, value-based reimbursement, and generous Medicaid carve-outs underpin demand and insulate volumes from list-price deflation. The proposed federal carve-out program would replicate Louisiana’s flat-fee model nationally, establishing predictable multi-year procurement windows that favor companies with broad portfolios. Canada’s centralized purchasing and Mexico’s emergent generic hubs complement the region’s volume stability.

Europe posts a steady 3.10% CAGR, powered by coordinated elimination plans and early adoption of novel modalities such as bulevirtide for hepatitis D. Risk-sharing payment contracts in Italy and Germany tie reimbursement to sustained virologic response, ensuring therapy access while safeguarding budgets. Regional reference pricing pressures margins, but centralized approvals expedite multi-country launches, allowing quicker payback on development costs.

Asia-Pacific is the growth pacesetter at 4.42% CAGR. The hepatitis therapeutics market size for the region is projected to expand quickly as China rolls out national screening and as India integrates antivirals into public insurance. China documented a 31.54% fall in hepatitis C incidence but a 28.60% mortality increase, underscoring diagnostic lag. Japan and South Korea furnish high-value demand through aggressive screening of aging populations, while Australia’s outcomes-based DAA deal has become a case study for neighboring health ministries. Governments across Southeast Asia are earmarking special budgets to meet the WHO 2030 elimination milestone, further amplifying regional momentum.

Competitive Landscape

The hepatitis therapeutics market shows moderate concentration around a handful of large-cap incumbents yet is rapidly diversifying as functional-cure pipelines mature. Gilead, AbbVie, and GSK control the bulk of commercialized regimens, leveraging global access programs and deep regulatory experience to defend share. GSK’s USD 2 billion acquisition of efimosfermin and its USD 37.5 million AI alliance with Ochre Bio illustrate how big pharma is buying platform technology to future-proof portfolios.

Biotechnology challengers are forcing incumbents to accelerate innovation cycles. GigaGen’s Phase 1 dosing of GIGA-2339 underscores how hyper-potent monoclonals can redefine therapeutic benchmarks. Assembly Biosciences brought four next-generation core inhibitors into clinical testing by end-2024, signaling that multi-asset continuity—not single-shot discoveries—will dictate staying power. Across the hepatitis therapeutics market, competitive advantage is shifting toward companies able to integrate siRNA, monoclonal antibodies, and small-molecule capsid inhibitors into seamless cure-oriented regimens.

Digital-health partnerships now matter as much as chemistry. Firms that embed adherence analytics, remote liver-function monitoring, and AI-enabled resistance detection into drug launches lock in payer preference and command price premiums. This ecosystem approach is expected to redraw competitive maps, making cross-sector alliances an imperative rather than an option.

Hepatitis Therapeutics Industry Leaders

AbbVie Inc.

Bristol Myers Squibb

Gilead Sciences

GSK plc

Merck & Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AbbVie secured FDA approval for an 8-week MAVYRET regimen to treat acute hepatitis C, posting 96% cure rates.

- May 2025: GSK announced a USD 2 billion acquisition of efimosfermin, enhancing its late-stage liver-disease pipeline.

- January 2025: Arbutus Biopharma initiated a Phase 2b study of imdusiran after earlier trials achieved a 50% functional cure rate in chronic hepatitis B.

- December 2024: Atea Pharmaceuticals reported 98% sustained virologic response in Phase 2 trials of its bemnifosbuvir-ruzasvir combo.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hepatitis therapeutics market as prescription antiviral and immune-modulating medicines used to treat acute or chronic hepatitis A, B, C, D, and other less common viral forms across all care settings. Products are tracked at ex-manufacturer prices and then converted to end-user value through standard trade and mark-up assumptions.

Scope exclusion: Prophylactic hepatitis vaccines, diagnostic test kits, liver-transplant procedures, and nutraceutical liver tonics are excluded from this therapeutic tally.

Segmentation Overview

- By Disease Type

- Hepatitis A

- Hepatitis B

- Hepatitis C

- Hepatitis D

- Other Types

- By Drug Class

- Interferons

- Monoclonal Antibodies

- NS5A Inhibitors

- Nucleotide Analog RT Inhibitors

- Nucleotide Analog NS5B Inhibitors

- Multi-class Combinations

- Other Drug Classes

- By Route of Administration

- Oral

- Injectable

- By Distribution Channel

- Offline

- Online

- By End-User

- Hospitals

- Specialty Clinics

- Home-care Settings

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held structured interviews with hepatologists, infectious-disease pharmacists, regional payers, and sourcing managers across North America, Europe, Asia-Pacific, Latin America, and the Middle East. These conversations clarified treatment initiation thresholds, generic substitution speed, procurement discounts, and patient adherence realities, letting us close information gaps highlighted during desk work.

Desk Research

Our analysts sifted through tier-1 public sources such as WHO's Global Hepatitis Reports, the CDC's Viral Hepatitis Surveillance, ECDC's disease bulletins, WTO customs data, peer-reviewed papers in the Lancet, and World Bank health expenditure tables. Company 10-Ks, investor decks, and reputable press releases added pipeline and pricing color, while paid platforms including D&B Hoovers, Dow Jones Factiva, and Questel helped verify corporate revenues, news flow, and patent trends. The listed references illustrate the breadth of material; many additional sources supported data checks.

Market-Sizing & Forecasting

A top-down epidemiology model starts with country-level chronic infection prevalence, treatment eligibility ratios, and therapy initiation rates, which are then multiplied by blended daily therapy costs to derive base-year value. Results are corroborated through bottom-up cross-checks that roll up leading supplier revenues and channel audits to fine-tune totals. Key variables guiding projections include incident infection trends, adoption of pangenotypic DAAs, reimbursement expansion, price erosion curves for generics, pipeline approval timelines, and macroeconomic health spending. Multivariate regression, stress tested through scenario analysis, generates five-year forecasts; gaps in supplier roll-ups are bridged using analog markets and sampled invoice benchmarks.

Data Validation & Update Cycle

We triangulate every output against external epidemiology dashboards and import-export flags, flag anomalies for senior review, and adjust before sign-off. Reports refresh annually, with interim updates when material regulatory or clinical events arise, and an analyst rereads the model before each client delivery to ensure our latest view.

Why Our Hepatitis Therapeutics Baseline Commands Credibility

Published market values often diverge because providers pick different disease scopes, price stacks, and refresh cadences. We remind clients that hepatitis vaccines, diagnostic revenue, or supportive care drugs can inflate a figure, whereas narrow antiviral only definitions may deflate it.

Key gap drivers include scope breadth, currency conversion dates, assumed generic price drops, and the year in which treated patient pools are frozen. Mordor's disciplined inclusion rules, blended ASP logic, and yearly refresh mean our 2025 baseline aligns with real-world prescribing and spending.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.44 B (2025) | Mordor Intelligence | - |

| USD 17.36 B (2025) | Global Consultancy A | Omits fourteen emerging economies and freezes price erosion after year one |

| USD 17.02 B (2024) | Industry Association B | Tracks only three antiviral classes and fixes exchange rates at 2022 averages |

| USD 22.20 B (2023) | Regional Consultancy C | Bundles prophylactic vaccines and liver support agents into therapeutic spend |

The comparison shows that numbers swing when scope or pricing logic changes. By anchoring estimates to clear variables, cross-checked assumptions, and a transparent update rhythm, Mordor Intelligence delivers a dependable baseline that decision makers can confidently cite.

Key Questions Answered in the Report

How are government subscription-style contracts shaping access to hepatitis therapies?

State-level subscription models lock in flat annual payments for unlimited drug supply, giving payers budget certainty while allowing manufacturers dependable volumes. This arrangement accelerates treatment initiation among underserved populations and is inspiring similar frameworks in other high-income markets.

Why is the industry pivoting from viral suppression toward functional cure strategies?

Suppressive regimens require lifelong adherence and ongoing monitoring, whereas functional cure protocols aim to clear viral antigens and re-establish durable immune control. Achieving this outcome can shorten or eliminate therapy, reduce long-term liver-disease costs, and open competitive space for next-generation modalities.

What role do monoclonal antibodies play in emerging hepatitis B regimens?

New polyclonal and bispecific antibodies can neutralize circulating surface antigens and enhance immune recognition of infected hepatocytes. When paired with capsid inhibitors or siRNA agents, they form multi-mechanism combinations that raise the probability of sustained antigen loss.

How is tele-hepatology changing patient engagement and treatment adherence?

Virtual consultation programs integrate screening, prescription, and follow-up visits on a single platform, cutting travel burdens and wait times. Early pilots report markedly higher enrollment and completion rates compared with traditional referral pathways, making digital delivery a key competitive differentiator.

In what ways are reimbursement policies influencing therapy selection in Europe?

Outcomes-based agreements tie payment to real-world viral clearance, pushing clinicians to favor regimens with robust effectiveness across genotypes and patient profiles. This has encouraged rapid uptake of short-course pan-genotypic options and created incentives for companies to generate post-marketing evidence.

What supply-chain considerations are critical for hepatitis drug manufacturers targeting emerging economies?

Active-pharmaceutical-ingredient production is heavily concentrated in a handful of countries, making localized disruptions a significant risk. Diversifying sourcing, building regional formulation hubs, and adopting blockchain-based tracking help assure continuity and bolster payer confidence in long-term access.

Page last updated on: