Heparin Market Size and Share

Market Overview

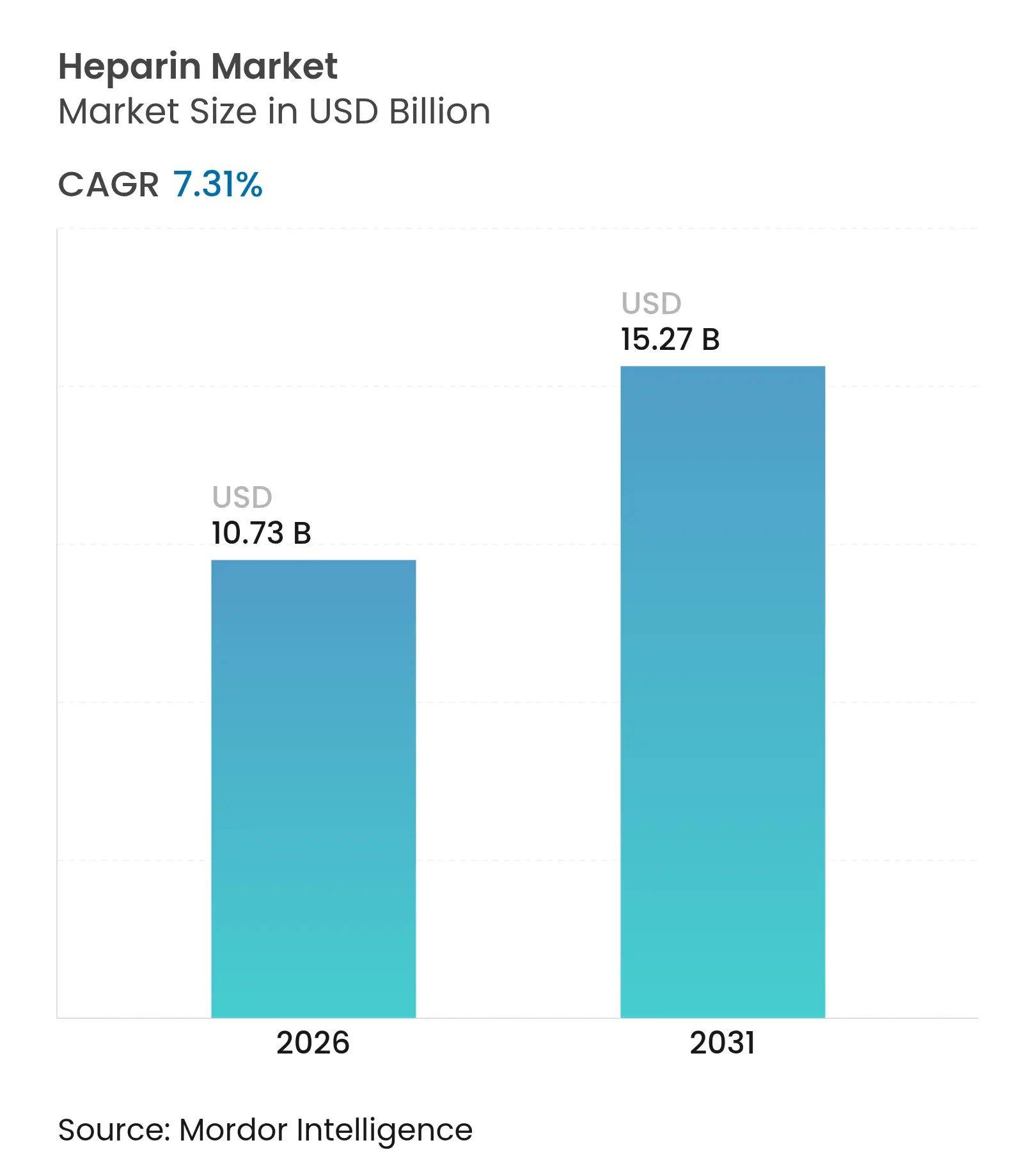

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.73 Billion |

| Market Size (2031) | USD 15.27 Billion |

| Growth Rate (2026 - 2031) | 7.31 % CAGR |

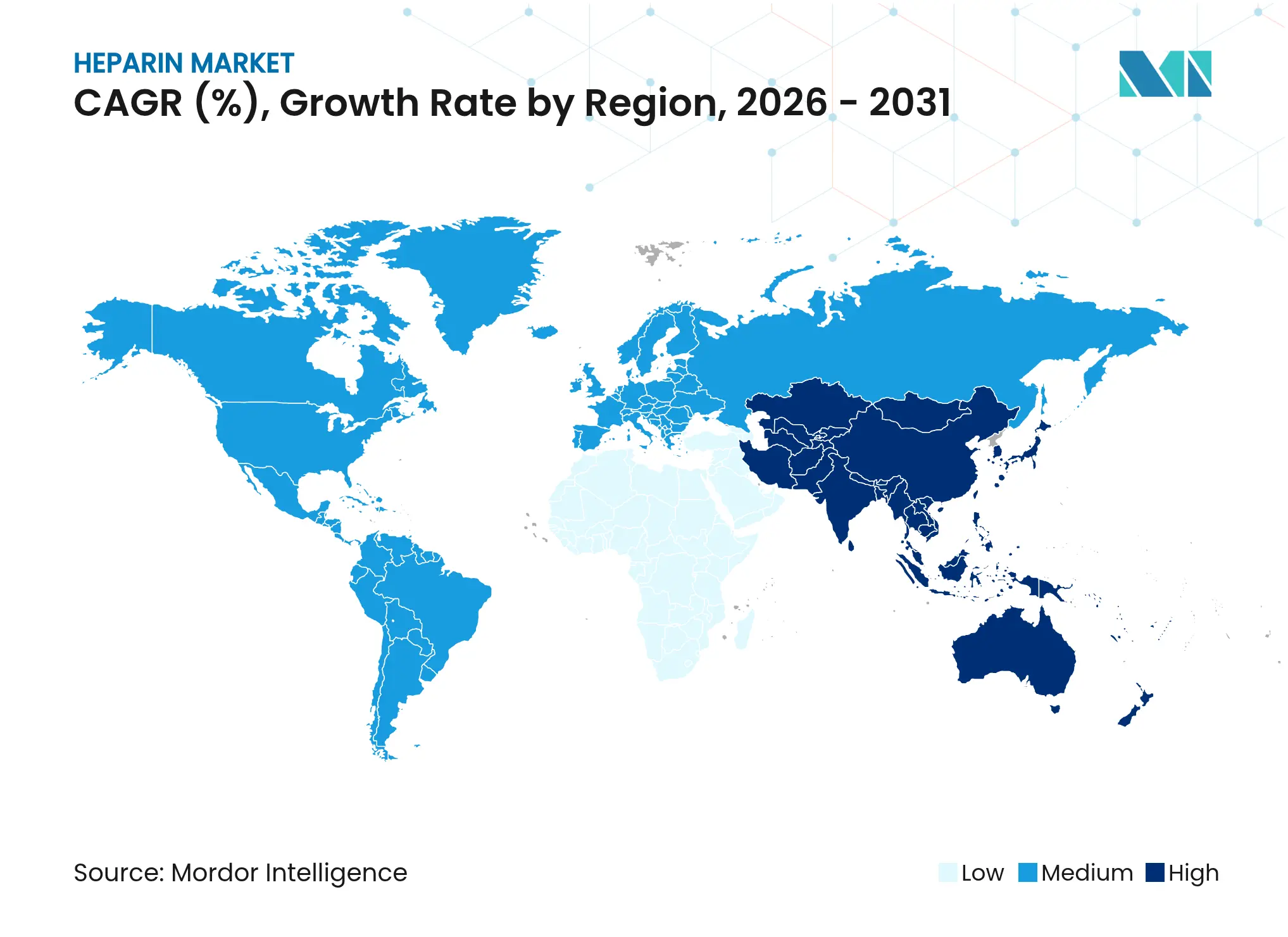

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Heparin Market Analysis by Mordor Intelligence

Rising surgical volumes, growth in dialysis procedures, and broader applications in oncology care and medical devices keep demand strong. Supply-chain diversification, particularly the move toward biosynthetic production, is emerging as a strategic priority as African Swine Fever–related shortages revealed the risks of heavy porcine dependence. Regulatory support for re-introducing bovine-sourced heparin and funding for bioengineered alternatives further strengthen the outlook. Competitive activity centers on portfolio expansion and geographic reach, while hospitals remain the largest buying segment.

Key Report Takeaways

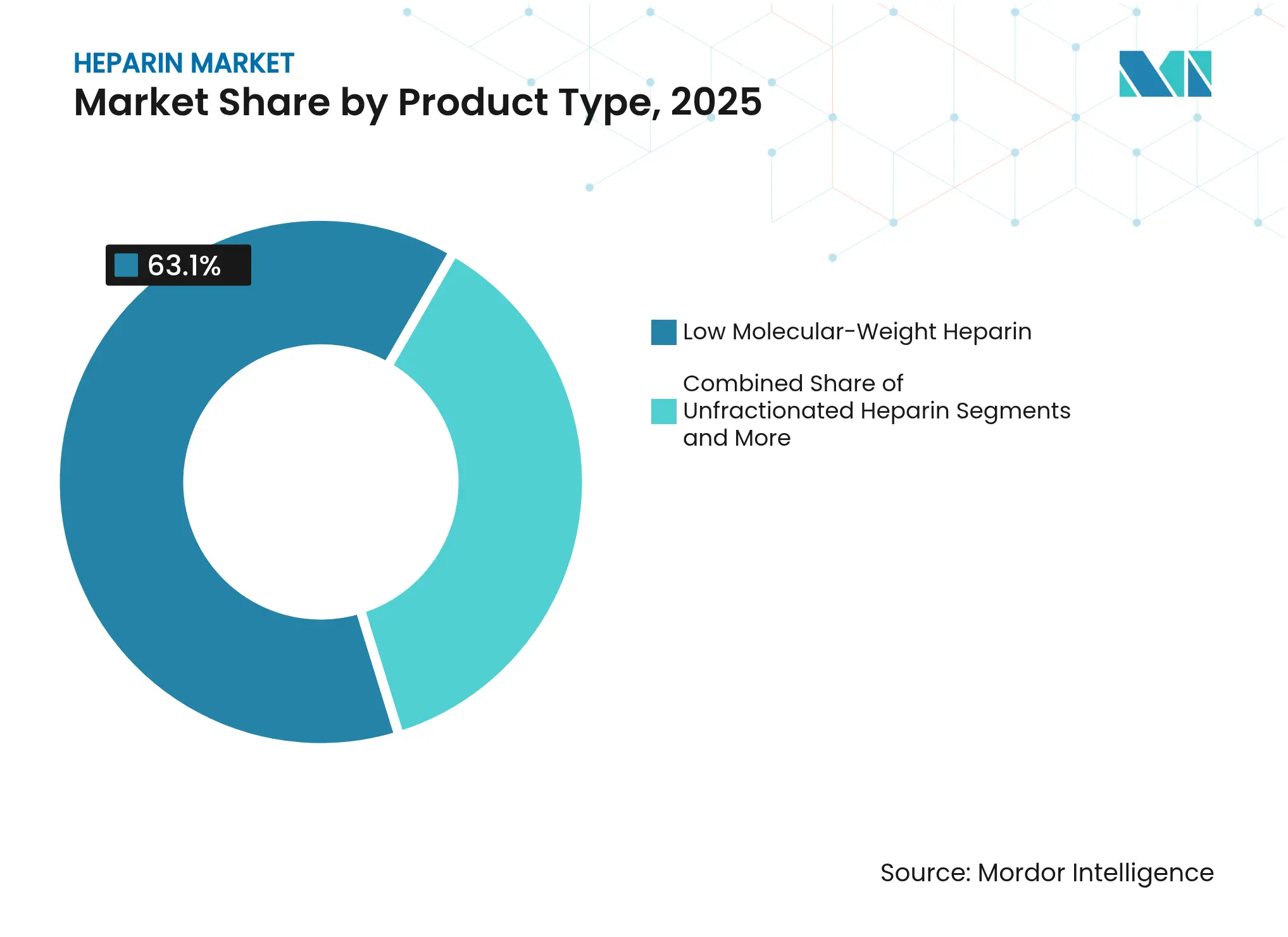

- By product type, low-molecular-weight heparin held 63.1% of heparin market share in 2025, while synthetic/biosynthetic heparin is forecast to grow at 8.40% CAGR to 2031.

- By source, porcine material accounted for 87.50% of the heparin market size in 2025; recombinant microbial sources are advancing at 9.10% CAGR through 2031.

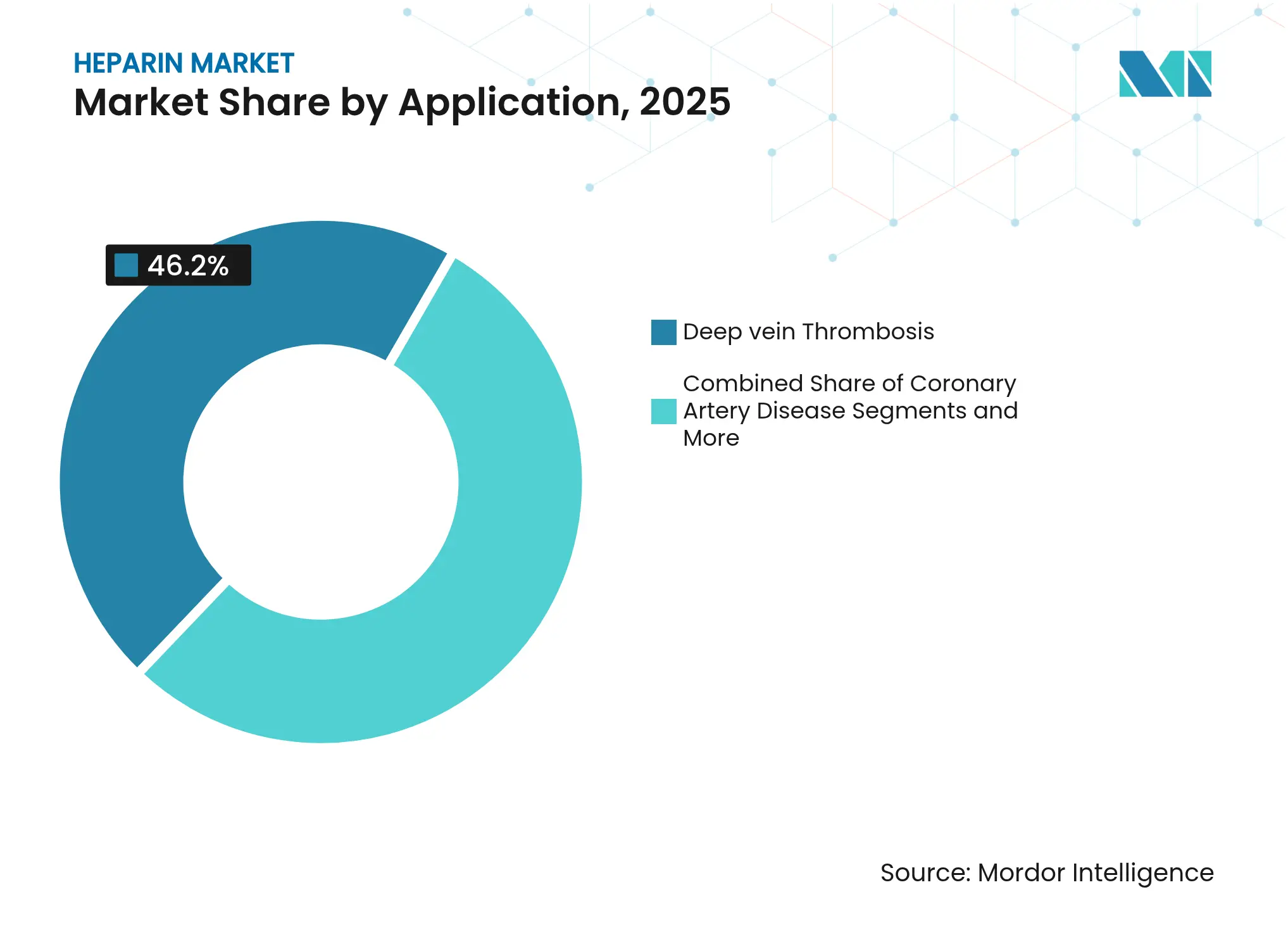

- By application, deep vein thrombosis led with a 46.20% share of the heparin market size in 2025 and hemodialysis is growing fastest at 7.80% CAGR.

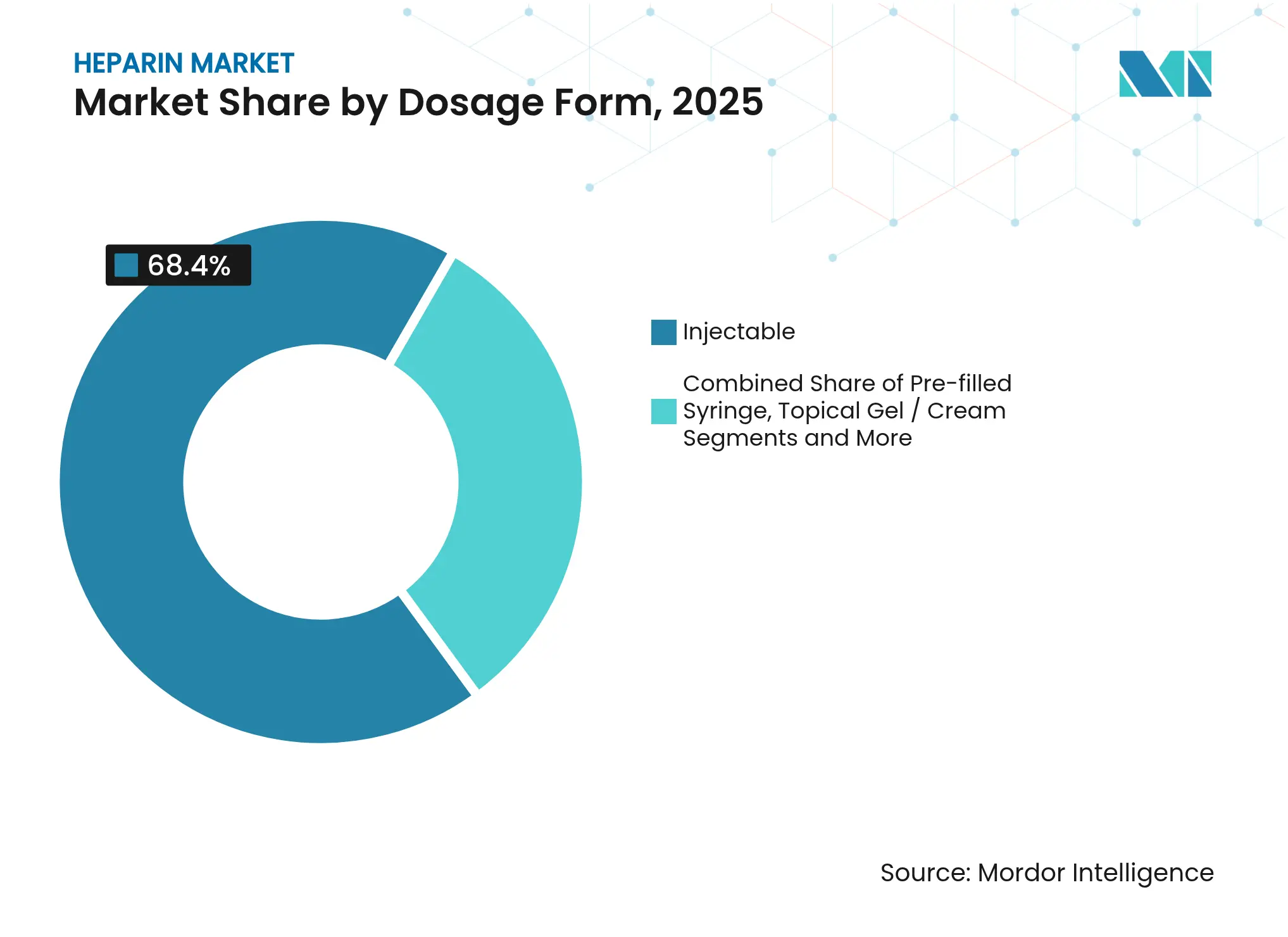

- By dosage form, injectable solutions captured 68.40% revenue share in 2025; pre-filled syringes are expanding at a 7.40% CAGR.

- By route of administration, subcutaneous delivery represented 54.60% of 2025 revenues, while intravenous delivery progresses at 7.09% CAGR to 2031.

- By end user, hospitals commanded 72.30% of 2025 revenue and home-care settings post the highest CAGR at 8.60%.

- By region, Asia-Pacific led with a 32.10% share in 2025, and the same region is forecast to expand at 8.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Heparin Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating surgical procedure

volumes and dialysis procedures

Escalating surgical procedure

volumes and dialysis procedures

| +1.7% | Global, with higher impact in North America, Europe, and developed Asia-Pacific regions | Short term (≤ 2 years) | (~)

% Impact on CAGR Forecast:

+1.7%

|

Geographic

Relevance

:

Global, with higher impact in

North America, Europe, and developed Asia-Pacific regions

|

Impact

Timeline

:

Short term (≤ 2 years)

|

Rapid adoption of

low-molecular-weight heparin coupled with expansion of biosynthetic heparin

programs

Rapid adoption of

low-molecular-weight heparin coupled with expansion of biosynthetic heparin

programs

| +1.4% | North America, Europe, and developed Asia-Pacific markets | Medium term (2-4 years) | |||

High burden of targeted diseases

and ageing population

High burden of targeted diseases

and ageing population

| +1.2% | Global, with pronounced effect in regions with rapidly aging populations (Europe, North America, Japan, China) | Long term (≥ 4 years) | |||

Expanding application in medical

devices

Expanding application in medical

devices

| +0.8% | North America, Europe, and advanced healthcare markets in Asia-Pacific | Medium term (2-4 years) | |||

Increasing application in

oncology care

Increasing application in

oncology care

| +0.7% | North America, Europe, and emerging applications in Asia-Pacific | Medium term (2-4 years) | |||

Escalating use of heparin in

extracorporeal membrane oxygenation (ECMO) and cardiopulmonary bypass

circuits

Escalating use of heparin in

extracorporeal membrane oxygenation (ECMO) and cardiopulmonary bypass

circuits

| +0.5% | Primarily North America and Europe, with growing adoption in advanced Asian healthcare systems | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating Surgical Procedure Volumes and Dialysis Procedures

Cardiovascular and orthopedic surgeries continue to increase, and both settings rely on prophylactic anticoagulation, keeping heparin demand high. Dialysis sessions are also rising as end-stage renal disease prevalence climbs. Recent trials show that heparin-coated dialyzers plus intermittent saline flushing eliminated clotting events in high-bleeding-risk patients. Regional anticoagulation techniques now allow acid and heparin-free dialysis for select cases, yet overall procedure growth sustains volume through 2027.

Rapid Adoption of Low-Molecular-Weight Heparin and Biosynthetic Programs

Clinicians favor LMWH for its predictable pharmacokinetics and limited monitoring needs, supporting steady share gains. Parallel advances in bioengineered heparin show E. coli-based systems producing material chemically comparable to porcine products and convertible to LMWH[1]Marc Douaisi, “Synthesis of Bioengineered Heparin Chemically and Biologically Similar to Porcine-Derived Products,” pnas.org. In 2025, the NHLBI funded a US USD 306,656 project to scale microbial production, underlining momentum for non-animal sources.

High Disease Burden and Aging Population

Atrial fibrillation affects an estimated 2% of people worldwide and far more among the elderly driving acute heparin therapy in hospital settings. Updated 2024 venous-thromboembolism guidelines introduced 78 new perioperative recommendations, reinforcing routine anticoagulation protocols that favor heparin in many acute scenarios. Coupled with rising life expectancy in Asia-Pacific and Europe, patient pools will widen across the forecast horizon.

Expanding Application in Medical Devices

Device makers increasingly coat vascular grafts and reservoirs with immobilized heparin to improve hemocompatibility. FDA clearance of the GORE PROPATEN vascular graft in March 2024 underscored regulatory confidence in such technology[2]W. L. Gore & Associates, “GORE PROPATEN Vascular Graft 510(k) Summary,” fda.gov. Medtronic’s venous reservoir bag, granted in May 2024, uses non-leaching heparin to reduce clot risk during bypass surgery. Research into heparin-binding silk proteins also suggests antimicrobial plus anticoagulant catheters for dialysis.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Supply-chain vulnerability due

to dependence on animal-derived raw material

Supply-chain vulnerability due

to dependence on animal-derived raw material

| −1.1% | Global, with severe impact in regions dependent on imports (North America, Europe) and production regions (China) | Short term (≤ 2 years) | (~)

% Impact on CAGR Forecast:

−1.1%

|

Geographic

Relevance

:

Global, with severe impact in

regions dependent on imports (North America, Europe) and production regions

(China)

|

Impact

Timeline

:

Short term (≤ 2 years)

|

Risk and adverse bleeding events

Risk and adverse bleeding events

| −0.8% | Global, with higher impact in regions with stricter pharmacovigilance (North America, Europe) | Medium term (2-4 years) | |||

Stringent regulatory

requirements

Stringent regulatory

requirements

| −0.7% | North America, Europe, and increasingly in Asia-Pacific markets adopting stricter regulations | Medium term (2-4 years) | |||

Therapeutic shift toward direct

oral anticoagulants in long-term thromboprophylaxis

Therapeutic shift toward direct

oral anticoagulants in long-term thromboprophylaxis

| −0.9% | Primarily North America and Europe, with gradual adoption in advanced Asian healthcare markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Supply-Chain Vulnerability due to Animal-Derived Raw Material

About 80% of active pharmaceutical ingredient volumes originate in China, leaving markets exposed to disease outbreaks and geopolitical actions. The 2019-2021 African Swine Fever crisis tightened supplies and lifted costs. In 2025, the FDA encouraged bovine-sourced heparin to diversify supply, citing improved purification that removes BSE prions.

Risk and Adverse Bleeding Events

Heparin-induced thrombocytopenia affects up to 5% of treated patients and can result in serious complications. Comparative studies show bovine and porcine variants trigger similar platelet aggregation in HIT antibodies[3]Gia Kapur, “Induced Platelet Aggregation in Porcine and Bovine Heparin,” angiology.org. Direct oral anticoagulants offer alternative therapy and feature in 2025 hematology guidelines, putting pressure on traditional heparin use.

Segment Analysis

By Product: LMWH Leads, Biosynthetic Gains

Low-molecular-weight heparin held 63.1% of revenues in 2025, supported by once-daily dosing that suits outpatient use. The heparin market reports consistent switching from unfractionated heparin to LMWH in surgical prophylaxis and oncology settings. The segment’s steady volume has prompted manufacturers to expand syringe formats for safer bedside administration.

Synthetic and biosynthetic heparin is the fastest-growing product line at 8.40% CAGR, reflecting investment in microbial and chemo-enzymatic pathways that bypass porcine inputs. As these alternatives reach scale, they may reshape overall heparin market share by the decade’s end.

Note: Segment shares of all individual segments available upon report purchase

By Source: Porcine Dominates, Microbial Ascends

Porcine mucosa supplied 87.50% of global value in 2025, anchoring production hubs in China’s coastal provinces. The heparin market size for porcine source is sensitive to herd-health shocks and tariffs that raise cost for importing countries. Recombinant microbial sources, growing at 9.10% CAGR, attract private capital and public grants aimed at supply-chain resilience.

Bovine material is returning to regulated markets after updated FDA guidance demonstrated that modern purification removes BSE agents. Early adopters aim to smooth volatility in porcine supply while maintaining pharmacologic equivalence.

By Dosage Form: Injectable Solutions Prevail

Injectable solutions commanded 68.40% of 2025 sales, confirming continued reliance on parenteral delivery for inpatient therapies. Pre-filled syringes rank as the fastest adopter at 7.40% CAGR, helped by simplified handling and lower contamination risk. Fresenius Kabi’s Simplist syringes underline how packaging innovation drives both safety and uptake.

Topical gels serve niche indications but benefit from over-the-counter visibility in Europe and Asia. Heparin-coated devices and depot formulations remain in pilot stages, yet they expand the dosage-form spectrum that underpins future heparin market growth.

Note: Segment shares of all individual segments available upon report purchase

By Route of Administration: Subcutaneous Rules

Subcutaneous delivery contributed 54.60% of 2025 value as LMWH dominates prophylactic regimens outside the hospital. Patient self-administration supports shorter hospital stays, aligning with cost-containment goals. Intravenous delivery is essential for acute interventions and is projected to grow at a 7.09% CAGR, driven by procedural demand in cardiology and cardiac surgery.

Administration protocols are adapting to new ablation techniques and extracorporeal life support, ensuring both routes remain integral to the long-term heparin market.

By Application: DVT Prevention Dominates

Deep vein thrombosis accounted for 46.20% of 2025 revenues, anchored by guideline-mandated prophylaxis after major orthopedic and abdominal surgeries. Hemodialysis usage is rising at 7.80% CAGR as global renal-failure prevalence intensifies. New dialyzer coatings reduce systemic anticoagulation yet retain heparin as the cornerstone for circuit patency.

Atrial fibrillation procedures and acute coronary syndromes round out high-volume indications, keeping the heparin market diversified across clinical specialties.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals Dominate, Home Care Expands

Hospitals absorbed 72.30% of heparin purchases in 2025, where intensive monitoring and rapid dose titration remain critical. Yet home-care adoption, growing at 8.60% CAGR, benefits from user-friendly syringes and telehealth follow-up. Ambulatory centers and specialty clinics deepen penetration in oncology, cardiology, and nephrology, broadening distribution channels.

Geography Analysis

North America recorded sizable demand in 2025, driven by high surgical procedure volumes and chronic dialysis populations. FDA encouragement for bovine sourcing seeks to stabilize supplies while tariffs on Chinese imports highlight procurement risks. Classification of new heparin test systems into Class II special controls exemplifies the tightening regulatory climate.

Asia-Pacific delivered 32.10% of global revenue in 2025 and posted the fastest CAGR at 8.19% during 2026-2031. China’s processing base remains indispensable, though recent policy reviews urge stronger R&D and quality oversight to ensure enduring competitiveness. Emerging self-sufficiency programs in India and Southeast Asia aim to localize API production, potentially expanding regional heparin market supply.

Europe maintains a stable share as aging demographics and well-funded health systems support steady consumption. EMA conformity assessments for device-drug combinations enforce rigorous safety standards. Biosimilar pathways differ from US practice, influencing launch timelines and competitive intensity among low-molecular-weight brands.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The heparin market features moderate consolidation, with Pfizer, Baxter International, and Sanofi anchoring global supply and maintaining broad therapeutic portfolios. Asian specialists including Hebei Changshan and Shenzhen Hepalink scale exports to capture incremental share. Strategic moves revolve around localizing manufacturing, forming supply agreements, and launching pre-filled delivery systems.

Supply-chain resilience is a pivotal competitive factor. Companies are evaluating dual sourcing, increased inventory buffers, and in-house bioengineering platforms to hedge porcine volatility. BIOPARIN’s US grant funding underscores growing institutional support for microbial pathways that promise controlled quality and geographic flexibility.

Regulatory shifts further shape rivalry. FDA support for bovine sourcing opens space for new entrants versed in ruminant purification, while EMA’s differentiated biosimilar requirements may slow follow-on approval compared with the US. Coupled with heightened oversight after past contamination events, firms that demonstrate traceability and analytical control can gain lasting advantage.

Heparin Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: BIOPARIN secures a USD 306,000 NHLBI STTR grant to scale bio-manufacturing of microbial heparin.

- January 2025: FDA guidance encourages re-introduction of bovine-sourced heparin, signaling policy support for diversified raw materials

- August 2024: Baxter recalls a lot of heparin sodium due to elevated endotoxin levels; no adverse events reported.

- May 2024: Medtronic gains FDA clearance for venous reservoir bag with non-leaching heparin coating.

Table of Contents for Heparin Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Escalating Surgical Procedure Volumes and Dialysis Procedures

- 4.2.2Rapid Adoption of Low-Molecular-Weight Heparin Coupled with Expansion of Biosynthetic Heparin Programs

- 4.2.3High Burden of Targeted Diseases and Ageing Population

- 4.2.4Expanding Application in Medical Devices

- 4.2.5Increasing Application in Oncology Care

- 4.2.6Escalating Use of Heparin in Extracorporeal Membrane Oxygenation (ECMO) and Cardiopulmonary Bypass Circuits

- 4.3Market Restraints

- 4.3.1Supply-Chain Vulnerability due to Dependence on Animal Derived Raw Material

- 4.3.2Risk and Adverse Bleeding Events

- 4.3.3Stringent Regulatory Requirements

- 4.3.4Therapeutic Shift Toward Direct Oral Anticoagulants in Long-term Thromboprophylaxis

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Outlook

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value in USD)

- 5.1By Product

- 5.1.1Unfractionated Heparin

- 5.1.2Low-Molecular-Weight Heparin (LMWH)

- 5.1.3Ultra-Low-Molecular-Weight Heparin (ULMWH)

- 5.1.4Synthetic / Biosynthetic Heparin

- 5.2By Source

- 5.2.1Porcine

- 5.2.2Bovine

- 5.2.3Recombinant Microbial

- 5.3By Dosage Form

- 5.3.1Injectable Solution

- 5.3.2Pre-filled Syringe

- 5.3.3Topical Gel / Cream

- 5.3.4Others

- 5.4By Route of Administration

- 5.4.1Intravenous

- 5.4.2Sub-cutaneous

- 5.5By Application

- 5.5.1Deep Vein Thrombosis (DVT)

- 5.5.2Atrial Fibrillation and Heart Attack

- 5.5.3Coronary Artery Disease

- 5.5.4Hemodialysis

- 5.5.5Other Applications

- 5.6By End User

- 5.6.1Hospitals

- 5.6.2Ambulatory Surgical Centers

- 5.6.3Specialty Clinics

- 5.6.4Home-care Settings

- 5.7Geography

- 5.7.1North America

- 5.7.1.1United States

- 5.7.1.2Canada

- 5.7.1.3Mexico

- 5.7.2Europe

- 5.7.2.1Germany

- 5.7.2.2United Kingdom

- 5.7.2.3France

- 5.7.2.4Italy

- 5.7.2.5Spain

- 5.7.2.6Rest of Europe

- 5.7.3Asia-Pacific

- 5.7.3.1China

- 5.7.3.2Japan

- 5.7.3.3India

- 5.7.3.4South Korea

- 5.7.3.5Australia

- 5.7.3.6Rest of Asia-Pacific

- 5.7.4Middle East and Africa

- 5.7.4.1GCC

- 5.7.4.2South Africa

- 5.7.4.3Rest of Middle East and Africa

- 5.7.5South America

- 5.7.5.1Brazil

- 5.7.5.2Argentina

- 5.7.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1B. Braun Melsungen AG

- 6.3.2Baxter International Inc.

- 6.3.3Dr. Reddy's Laboratories Ltd.

- 6.3.4Hebei Changshan Biochemical Pharmaceutical Co. Ltd.

- 6.3.5Leo Pharma A/S

- 6.3.6Opocrin S.p.A.

- 6.3.7Pfizer Inc.

- 6.3.8Fresenius Kabi AG

- 6.3.9Gland Pharma Ltd.

- 6.3.10Hikma Pharmaceuticals PLC

- 6.3.11Techdow Pharma USA Inc.

- 6.3.12Viatris Inc.

- 6.3.13Abbott

- 6.3.14Smiths Medical (ICU Medical)

- 6.3.15Sanofi S.A.

- 6.3.16Shenzhen Hepalink Pharmaceutical Co. Ltd.

- 6.3.17Bioiberica S.A.U.

- 6.3.18Nanjing King-Friend Biochemical Pharmaceutical Co. Ltd.

- 6.3.19Cipla

- 6.3.20Emcure Pharmaceuticals Ltd

7. Market Opportunities and Future Outlook

- 7.1White-space and Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the heparin market as all pharmaceutical-grade unfractionated, low-molecular-weight, ultra-low-molecular-weight, and emerging synthetic heparin APIs and finished dosage forms that are administered intravenously or subcutaneously for prophylaxis and treatment of thromboembolic disorders across hospital, clinic, and home-care settings. According to Mordor Intelligence analysts, ancillary items such as heparin-coated devices, DOACs, and veterinary formulations fall outside this scope.

Scope Exclusion: Heparin-impregnated catheters, rinsing solutions, and anticoagulants other than heparin are not sized in this report.

Segmentation Overview

- By Product

- Unfractionated Heparin

- Low-Molecular-Weight Heparin (LMWH)

- Ultra-Low-Molecular-Weight Heparin (ULMWH)

- Synthetic / Biosynthetic Heparin

- Unfractionated Heparin

- By Source

- Porcine

- Bovine

- Recombinant Microbial

- Porcine

- By Dosage Form

- Injectable Solution

- Pre-filled Syringe

- Topical Gel / Cream

- Others

- Injectable Solution

- By Route of Administration

- Intravenous

- Sub-cutaneous

- Intravenous

- By Application

- Deep Vein Thrombosis (DVT)

- Atrial Fibrillation and Heart Attack

- Coronary Artery Disease

- Hemodialysis

- Other Applications

- Deep Vein Thrombosis (DVT)

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Home-care Settings

- Hospitals

- Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed formulary managers in the United States, purchasing heads at leading Asian contract API producers, and interventional cardiologists across five EU countries. These conversations validated average daily dose assumptions, clarified post-COVID protocol changes, and benchmarked price pass-through rates that secondary data could not capture.

Desk Research

We began by mapping demand fundamentals through open datasets such as the WHO Global Health Observatory, UN Population Prospects, the World Bank's hospital procedure series, and U.S. CDC National Center for Health Statistics, which together quantify the prevalence of VTE, cardiac surgeries, and renal dialysis sessions. Regulatory and trade signals were pulled from European Medicines Agency shortage notices, U.S. FDA drug-recall archives, and UN Comtrade codes tracking porcine mucosa exports that underpin crude heparin supply.

To test revenue realism, our team extracted recent vial and pre-filled syringe ASP trends from hospital procurement portals, triangulated them with company financial snapshots on D&B Hoovers and news hits on Dow Jones Factiva. Key insights from the International Society on Thrombosis and Haemostasis white papers further contextualized dosing shifts toward LMWH. The sources listed illustrate but do not exhaust the wider body reviewed.

Market-Sizing & Forecasting

A top-down patient-flow model converts procedure volumes, dialysis counts, and VTE prevalence into treated patient pools, which are then multiplied by therapy duration and weight-adjusted dosing norms. Selective bottom-up cross-checks, supplier revenue roll-ups, and channel ASP x volume samples tune totals before finalization. Key variables tracked include porcine mucosa availability, LMWH penetration, synthetic heparin pipeline launches, cardiovascular surgery rates, and regional reimbursement ceilings. Forecasts to 2030 rely on multivariate regressions blended with scenario analysis for raw material shocks, with coefficient ranges vetted by our primary experts. Data gaps on unreported hospital buys are bridged using conservative utilization ratios derived from sentinel facilities.

Data Validation & Update Cycle

Every iteration passes variance checks against historical price and volume corridors, with anomalies escalated for senior review. Models refresh annually; interim touchpoints trigger if FDA recalls, ASF outbreaks, or guideline revisions materially shift supply or demand. A final analyst pass is completed just before report dispatch to clients.

Why Our Heparin Market Baseline Earns Unmatched Trust

Benchmark comparison

Published values often diverge because firms choose different product mixes, raw material assumptions, and refresh cadences. We acknowledge these levers upfront so decision makers see how scope and variables steer the math.

Key gap drivers include: some publishers stop at LMWH while our scope adds ultra-low and synthetic variants; others freeze exchange rates at study launch, whereas Mordor applies rolling averages; a few rely solely on manufacturer revenues, missing unreported hospital compounding volumes.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 10.04 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 10.21 B (2024) | Global Consultancy A | Update cycle ends Q1 2024; excludes ultra-low-weight products | ||

USD 7.72 B (2024) | Regional Consultancy B | Uses manufacturer revenue only; omits topical and price escalator adjustments | ||

USD 5.40 B (2024) | Industry Journal C | Counts North America and Europe volumes only, ignoring Asia-Pacific uptake |