Non-alcoholic Steatohepatitis Therapeutics And Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

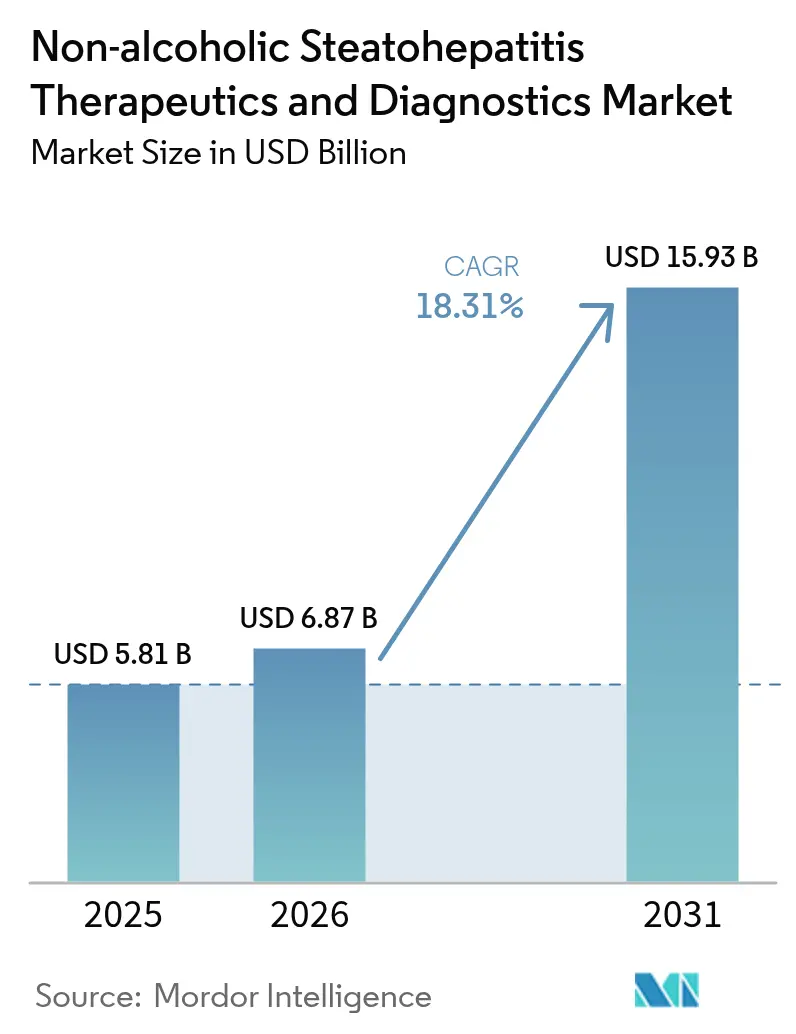

| Market Size (2026) | USD 6.87 Billion |

| Market Size (2031) | USD 15.93 Billion |

| Growth Rate (2026 - 2031) | 18.31% CAGR |

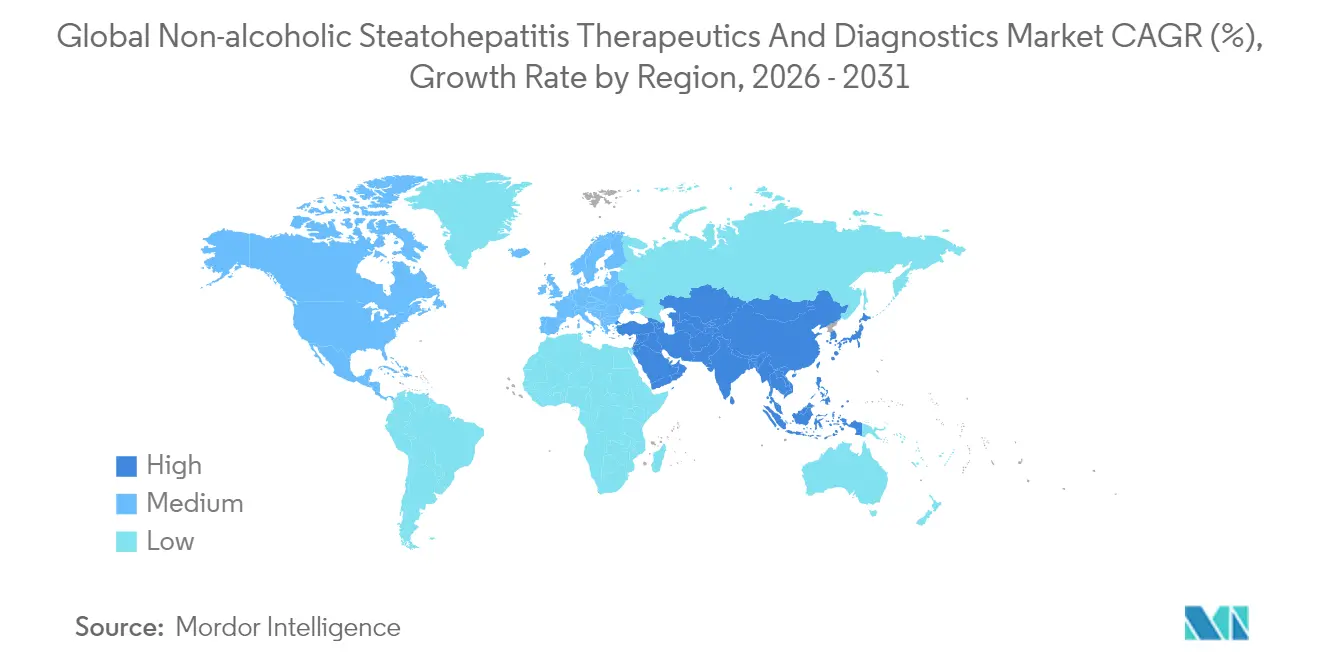

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

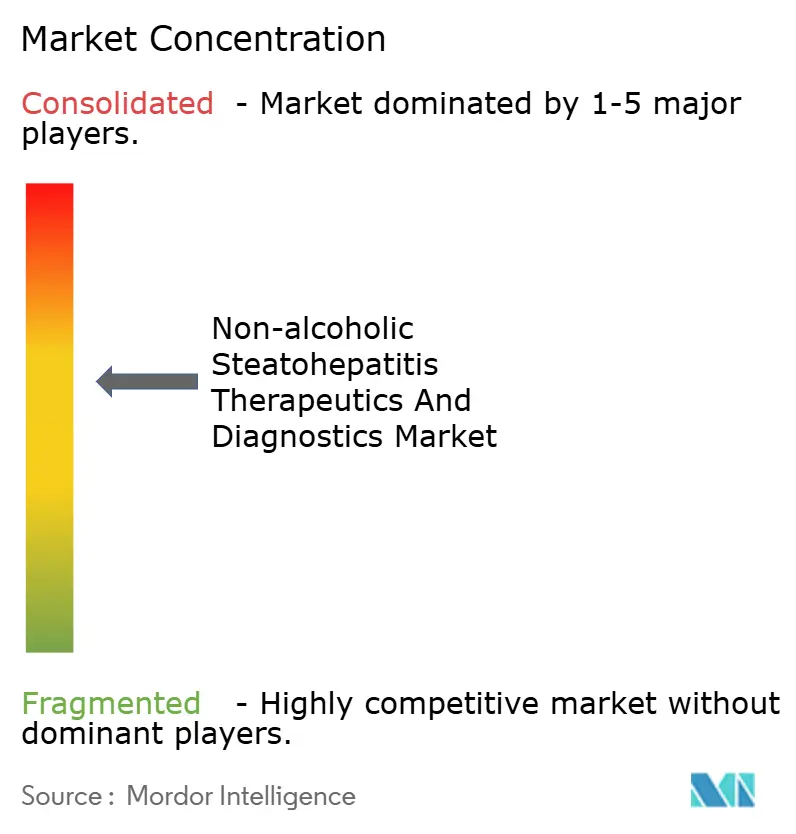

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-alcoholic Steatohepatitis Therapeutics And Diagnostics Market Analysis by Mordor Intelligence

The Nonalcoholic Steatohepatitis therapeutics and diagnostics market size is expected to grow from USD 5.81 billion in 2025 to USD 6.87 billion in 2026 and is forecast to reach USD 15.93 billion by 2031 at 18.31% CAGR over 2026-2031. Escalating global prevalence of metabolic syndrome, the March 2024 FDA approval of resmetirom, and payer support for non-invasive testing collectively reposition the Nonalcoholic Steatohepatitis therapeutics and diagnostics market for sustained double-digit growth. Diagnostic solutions currently dominate revenues, yet the therapeutics pipeline is converting into commercial launches at a record pace, tilting future value creation toward treatment-centred models. Hospital demand remains robust, but specialized diagnostic centers are scaling rapidly on the back of AI-enabled workflows. Competitive intensity is heightened by fast-track drug designations, strategic licensing in Asia, and the race to integrate blood-based biomarkers into routine care pathways.

Key Report Takeaways

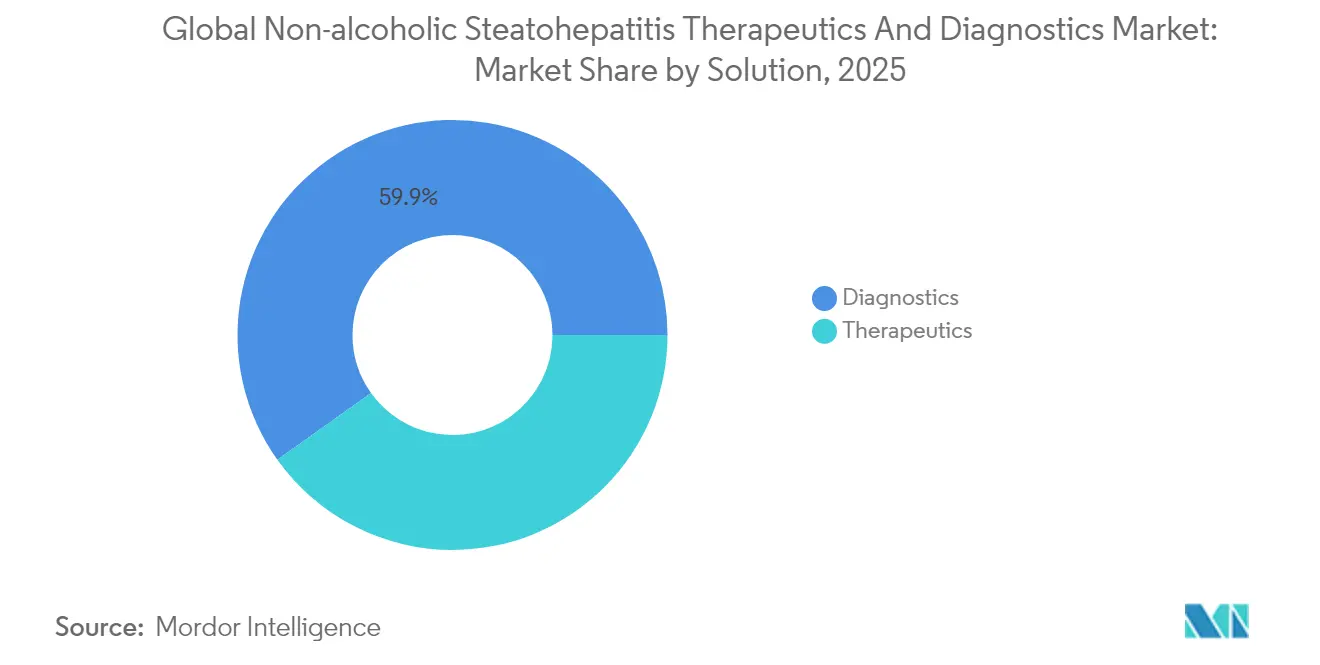

- By solution, diagnostics held 59.85% of the Nonalcoholic Steatohepatitis therapeutics and diagnostics market share in 2025, while therapeutics are advancing at a 19.11% CAGR to 2031.

- By end user, hospitals and clinics accounted for 44.52% of the Nonalcoholic Steatohepatitis therapeutics and diagnostics market size in 2025; diagnostic centers post the fastest growth at an 18.42% CAGR through 2031.

- By geography, North America led with 36.78% revenue share in 2025; Asia-Pacific is forecast to expand at a 18.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-alcoholic Steatohepatitis Therapeutics And Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of obesity & metabolic syndrome | +4.2% | Global, with highest impact in North America & Asia-Pacific | Long term (≥ 4 years) |

| Advancement in non-invasive diagnostic technologies | +3.8% | Global, early adoption in North America & Europe | Medium term (2-4 years) |

| Accelerated clinical trials & fast-track designations | +3.1% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Payer willingness to reimburse biomarker tests | +2.9% | North America & Europe | Medium term (2-4 years) |

| Combination-therapy pipeline expansion | +2.4% | Global | Medium term (2-4 years) |

| AI-enabled imaging partnerships with liver clinics | +1.8% | North America & Europe, selective Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity & Metabolic Syndrome

Obesity and metabolic dysfunction now affect close to one-third of the global population, creating an expanding clinical pool for MASLD and, by progression, nonalcoholic steatohepatitis. The demographic tilt toward younger cohorts accelerates fibrosis at earlier ages and stretches lifetime treatment windows. Latin America illustrates the trend as prevalence nears 24%, driving payer interest in community-level screening programs. U.S. projections indicate 27 million affected adults by 2030, a 63% jump versus 2015, redefining transplant-planning models and stimulating commercial urgency. Governments and professional societies respond by integrating fibrosis scores into primary-care check-ups, further enlarging addressable volumes for both diagnostics and therapeutics.

Advancement in Non-Invasive Diagnostic Technologies

Market momentum pivots around rapid adoption of blood-based panels and elastography that replace invasive liver biopsy. Roche’s Elecsys PRO-C3 returns fibrosis staging in 18 minutes, enabling same-visit clinical decisions and widening provider acceptance. AI algorithms now mine electronic health records to flag undiagnosed MASLD with 83% accuracy, adding scale without incremental imaging capacity. FibroScan, ELF, and FIB-4 scores are embedded in new treatment guidelines across the U.S. and Europe, prompting laboratories to upgrade equipment portfolios. Earlier detection increases therapeutic eligibility pools and underpins value-based reimbursement arguments that emphasize avoided transplant costs.

Payer Willingness to Reimburse Biomarker Tests

Commercial insurers increasingly reimburse ELF and NIS4 panels once linked to reduced downstream expenditures. Labcorp’s NASHnext™ secured broad coverage in early 2024, signalling payer readiness to reward diagnostics that avert high-cost cirrhosis care. Medicare’s 2025 National Coverage Determination for non-invasive fibrosis testing further normalizes reimbursement pathways. Europe follows with country-level health technology assessments validating clinical utility. The resulting financial clarity encourages diagnostic-centric startups to scale distribution and accelerates hospital procurement of elastography devices.

Combination-Therapy Pipeline Expansion

Clinical rationale for multi-target regimens strengthens as monotherapies struggle to deliver dual endpoints of fibrosis improvement and NASH resolution. Novo Nordisk’s GLP-1 plus FXR agonist research and Gilead’s paired FGF21 analogue strategy widen therapeutic possibilities without requiring de-novo modes of action. Combination paradigms appeal to regulators when mechanistic synergy addresses heterogeneity in disease pathways, motivating collaborative trials and intellectual-property cross-licensing. Successful proof-of-concept data would expand addressable market value by enabling tailored regimens across fibrosis stages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High late-stage drug-trial failure rate | -2.8% | Global, particularly impacting North America & Europe | Medium term (2-4 years) |

| Uncertain reimbursement for novel diagnostics | -2.1% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Limited patient awareness & under-diagnosis | -1.9% | Global, most pronounced in Asia-Pacific & emerging markets | Long term (≥ 4 years) |

| Stringent histological endpoint requirements | -1.6% | North America & Europe, regulatory-driven impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Late-Stage Drug-Trial Failure Rate

Historical attrition has eroded investor sentiment each time a promising candidate underperformed in Phase 2b or Phase 3. Akero’s efruxifermin missed key fibrosis endpoints with response rates of 18–29% versus 13% placebo, reviving concerns over surrogate markers versus hard histological outcomes. Companies react by tightening inclusion criteria, but smaller sample sizes raise statistical-power questions that regulators scrutinize. The cyclical pattern of hype and disappointment elongates development timelines, tempers deal valuations, and moderates the Nonalcoholic Steatohepatitis therapeutics and diagnostics market growth curve despite headline breakthroughs.

Uncertain Reimbursement for Novel Diagnostics

Emerging AI and multi-omic panels confront fragmented payer frameworks, especially in Latin America and parts of Asia where public budgets prioritize primary care. Health technology assessment agencies demand longitudinal outcome data, lengthening approval cycles beyond what venture-backed diagnostic firms can often fund. Europe’s differential acceptance benches novel panels against well-established FIB-4 or FibroScan, forcing companies to conduct added head-to-head studies. Until consistent coverage materializes, adoption curves in cost-sensitive regions remain shallow, partially offsetting growth elsewhere.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Therapeutics Drive Future Growth Despite Diagnostic Dominance

Diagnostics retained 59.85% revenue share in 2025 on the strength of widespread use of elastography and blood-based panels across primary and secondary care sites. Nevertheless, therapeutics exhibit the fastest momentum, expanding at a 19.11% CAGR, powered initially by resmetirom’s launch. Within the solution stack, imaging tests and biomarker assays continue to diversify, while biopsy volumes contract as clinicians shift to guideline-endorsed non-invasive monitoring. Resmetirom generated USD 137 million in Q1 2025 alone, proving willingness to pay even at an annual USD 47,400 price point. Pipeline depth in GLP-1, THR-β, and FGF21 classes suggests sustained innovation cycles that can progressively narrow fibrosis progression rates.

Expanded therapeutic access is expected to rebalance spending patterns such that therapeutics account for the larger share of the nonalcoholic Steatohepatitis therapeutics and diagnostics market size by late-decade. The current gap between diagnosis and treatment adoption generates pent-up demand suited to first-in-class entrants. Diagnostics still accrue steady transactional revenue from repeat fibrosis monitoring; however, growth rates taper as market saturation rises in high-income countries. Technology suppliers pivot to value-added analytics and longitudinal patient-management platforms to protect margins. Multimodal diagnostic algorithms that integrate imaging, serum biomarkers, and electronic health record data differentiate service offerings and lock-in provider relationships.

By End User: Diagnostic Centers Emerge as Growth Leaders

Hospitals and clinics generated 44.52% of Nonalcoholic Steatohepatitis therapeutics and diagnostics market revenue in 2025, reflecting entrenched referral pathways and bundled billing practices. Yet diagnostic centers are tracking an 18.42% CAGR, outpacing all other settings as patients gravitate toward convenience and shorter appointment backlogs. Urban Asia-Pacific illustrates the shift, where standalone imaging chains add dedicated liver units supported by AI-enabled interpretation and cloud-based reporting. Academic institutes continue to shape clinical guidelines and attract early-stage trials, making them critical gatekeepers for technology validation.

Integration between diagnostic centers and hepatology specialists accelerates care coordination, leading to higher therapy conversion rates. Telehealth follow-up, remote FibroScan vans, and mobile phlebotomy further erode hospital dominance for routine monitoring. For providers, profitability hinges on high throughput and pay-for-performance contracts that reward early disease interception.

Geography Analysis

North America retained its 36.78% revenue lead in 2025, underpinned by early regulatory approvals, broad insurance coverage, and high obesity prevalence. U.S. hepatologists rapidly incorporated resmetirom into practice after March 2024 approval, elevating prescription volumes even before full guideline integration. Canada mirrors trends on a smaller scale, benefitting from centralized health-technology assessments that green-light non-invasive diagnostics for provincial coverage. The region’s innovation ecosystem, anchored by Boston and San Diego biotech clusters, ensures a continual influx of trial candidates and venture capital, reinforcing first-mover advantages in therapeutics and AI-powered diagnostics.

Europe contributes steady, mid-teen revenue shares with Germany, the United Kingdom, and France accounting for the bulk of uptake. EMA approval of resmetirom, anticipated mid-2025, will unlock pent-up demand. National reimbursement agencies are already modeling budget impacts, suggesting quicker formulary listings than seen with earlier metabolic drugs. Non-invasive diagnostic penetration is mature, yet opportunities remain in integrating AI-triaged imaging into regional liver networks to tackle workforce shortages. Parallel import regulations may exert mild downward pressure on launch prices, but volume growth is expected to compensate.

Asia-Pacific is the fastest-growing theatre, set to surge at a 18.67% CAGR as diabetes and obesity climb across China, India, and Southeast Asia. Multinational companies localize clinical trials to satisfy diverse ethnic profiles and streamline China’s National Medical Products Administration approvals. Madrigal’s July 2025 USD 2 billion licensing pact with CSPC exemplifies route-to-market strategies that combine local manufacturing with multinational science. Government prevention programs and growing middle-class awareness enlarge screening volumes for fibrosis tests. Australia and South Korea, with advanced reimbursement systems, act as gateway markets for new diagnostics before broader regional rollout.

South America and the Middle East & Africa collectively represent nascent but rising prospects. Brazil’s public-private hospital model experiments with capitated payments that reward early fibrosis detection. GCC nations invest in specialty liver centers, leveraging high per-capita health spending to adopt latest diagnostics. However, reimbursement fragmentation and workforce imbalances temper near-term gains, keeping their combined share in single digits through 2031.

Competitive Landscape

The Nonalcoholic Steatohepatitis therapeutics and diagnostics market features moderate concentration as the leading ten companies control roughly half of therapeutic and diagnostic revenues. Madrigal, Novo Nordisk, and Eli Lilly headline therapeutics, each advancing differentiated mechanisms backed by large-scale outcome data. Madrigal leverages the first-mover benefits of resmetirom while negotiating regional deals such as the CSPC partnership to amplify its footprint. Novo Nordisk extends its metabolic franchise by positioning semaglutide as a dual obesity-liver disease solution, a narrative that resonates with payers seeking holistic risk reduction. Eli Lilly’s tirzepatide, exhibiting 52-73% MASH resolution in Phase 2, signals competitive pressure on incumbent GLP-1 players.

Diagnostic leadership rests with Roche, Siemens Healthineers, and Abbott, each bundling assay reagents, instrumentation, and decision-support software. Roche’s Elecsys PRO-C3 launch adds a rapid fibrosis tool to laboratories already using its core chemistry analyzers, enhancing switching costs. Siemens integrates AI-based elastography analysis into its ultrasound portfolio, while Abbott advances multi-analyte panels leveraging its immunoassay footprint. Competitive dynamics pivot on ecosystem lock-in, where proprietary algorithms and reagent leases secure annuity streams.

Strategic collaboration defines recent activity. Pharmaceutical-diagnostic pairing speeds companion-diagnostic development, illustrated by Labcorp’s alignment with multiple therapeutics sponsors to co-validate biomarker endpoints. Acquisition activity focuses on filling mechanism or technology gaps; GSK’s USD 1.2 billion buyout of an FGF19 analogue signaled willingness to pay premiums for late-stage hepatic assets. Overall, players mix organic R&D, in-licensing, and geographic expansion to construct defensible growth runways against a backdrop of accelerating scientific advances.

Non-alcoholic Steatohepatitis Therapeutics And Diagnostics Industry Leaders

Genfit SA

Intercept Pharmaceuticals, Inc.

General Electric Company (GE Healthcare)

Siemens Healthineers

Tawazun Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Madrigal Pharmaceuticals entered a potential USD 2 billion-plus licensing deal with China’s CSPC to commercialize resmetirom in Greater China, securing upfront cash and milestone-linked payments

- May 2025: Novo Nordisk’s Phase 3 ESSENCE study showed semaglutide 2.4 mg resolved MASH in 62.9% of patients, with FDA granting Priority Review

Global Non-alcoholic Steatohepatitis Therapeutics And Diagnostics Market Report Scope

As per the scope of the report, non-alcoholic steatohepatitis (NASH) is an advanced form of non-alcoholic fatty liver disease (NAFLD). NASH is liver inflammation and damage caused by the buildup of fat in the liver. It is part of a group of conditions called non-alcoholic fatty liver disease (NAFLD). The Non-alcoholic Steatohepatitis Therapeutics and Diagnostics Market is segmented by Product (Therapeutics and Diagnostics(Imaging Techniques, Diagnostic Tests, Biopsy) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Therapeutics | By Drug Class | FXR Agonists |

| THR-β Agonists | ||

| GLP-1 Agonists | ||

| Others | ||

| Diagnostics | By Diagnostic Modality | Imaging Tests |

| Biomarker-based Blood Tests | ||

| Liver Biopsy | ||

| Elastography | ||

| Hospitals & Clinics |

| Diagnostic Centers |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Solution (Value) | Therapeutics | By Drug Class | FXR Agonists |

| THR-β Agonists | |||

| GLP-1 Agonists | |||

| Others | |||

| Diagnostics | By Diagnostic Modality | Imaging Tests | |

| Biomarker-based Blood Tests | |||

| Liver Biopsy | |||

| Elastography | |||

| By End User (Value) | Hospitals & Clinics | ||

| Diagnostic Centers | |||

| Academic & Research Institutes | |||

| Others | |||

| By Geography (Value) | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

How large is the global Nonalcoholic Steatohepatitis therapeutics and diagnostics market in 2026?

The Nonalcoholic Steatohepatitis therapeutics and diagnostics market size stands at USD 6.87 billion in 2026.

What is the expected CAGR for the sector through 2031?

Market value is forecast to rise at an 18.31% CAGR to reach USD 15.93 billion by 2031.

Which solution category is growing fastest?

Therapeutics expand at a 19.11% CAGR, overtaking diagnostics later in the decade.

Which region shows the highest growth momentum?

Asia-Pacific posts the strongest trajectory with a 18.67% CAGR to 2031.

Why are diagnostic centers gaining share?

AI-enabled workflows, shorter wait times, and payer support for non-invasive tests drive an 18.42% CAGR for diagnostic centers.

Page last updated on: