Chronic Kidney Disease Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 89.29 Billion |

| Market Size (2031) | USD 115.26 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

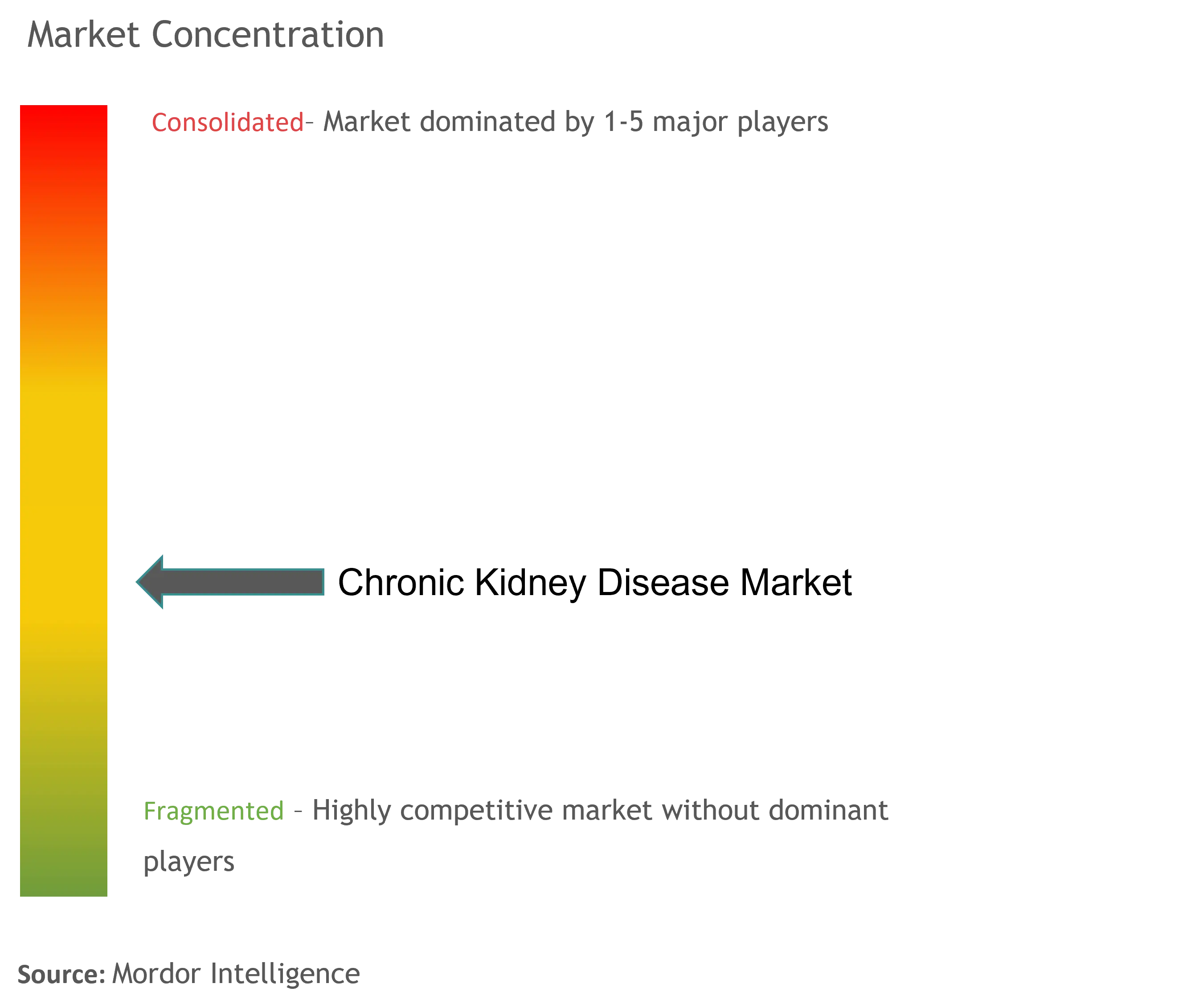

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chronic Kidney Disease Market Analysis by Mordor Intelligence

Chronic kidney disease market size in 2026 is estimated at USD 89.29 billion, growing from 2025 value of USD 84.85 billion with 2031 projections showing USD 115.26 billion, growing at 5.24% CAGR over 2026-2031. This expansion reflects the convergence of rising diabetes and hypertension prevalence, demographic aging, and expanding value-based payment models that reward early intervention. Demand remains resilient because diabetes and hypertension together cause about 70% of chronic kidney disease cases, creating a large, stable treatment base. Continuous FDA approvals of precision drugs such as atrasentan and iptacopan are accelerating therapeutic uptake. Hospitals still perform most care coordination, yet dialysis centers and home-based modalities are scaling quickly as technology makes decentralized treatment feasible. Competitive pressure is intensifying, especially in diagnostics, where AI-powered risk tools and point-of-care biomarker tests shorten detection times and support preventive care adoption.

Key Report Takeaways

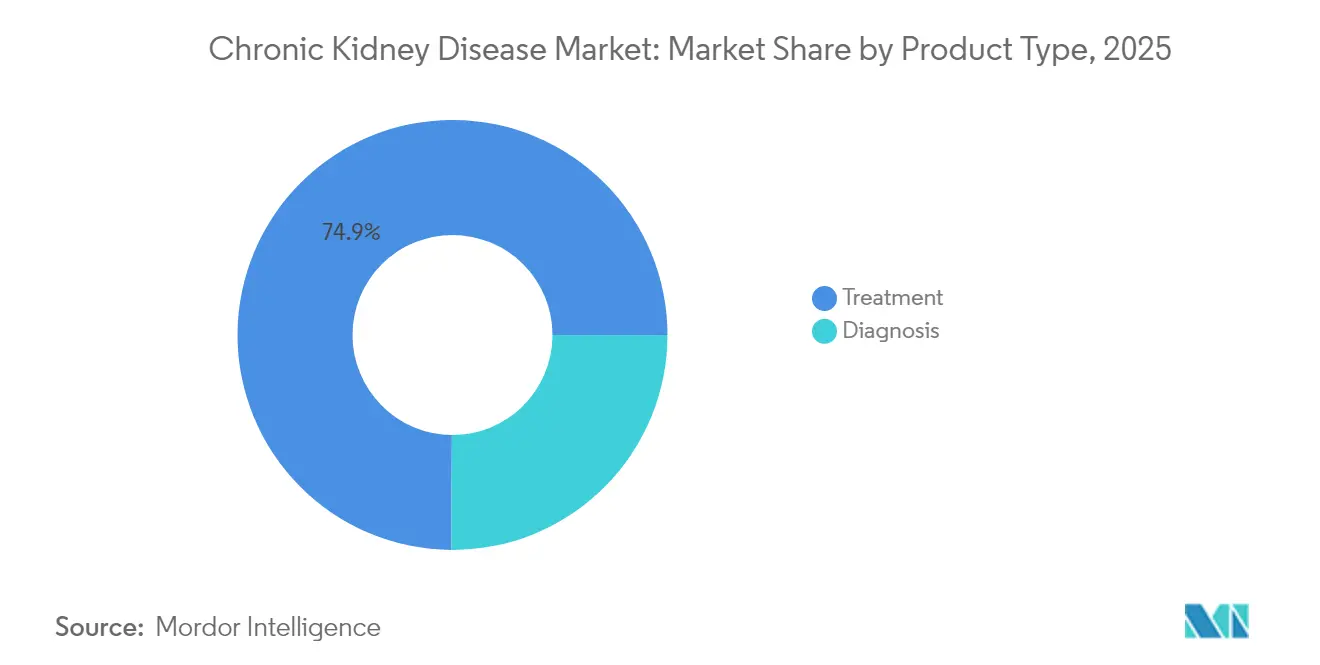

- By product type, treatment products held 74.90% of chronic kidney disease market share in 2025, while diagnosis products are forecast to expand at a 6.75% CAGR through 2031.

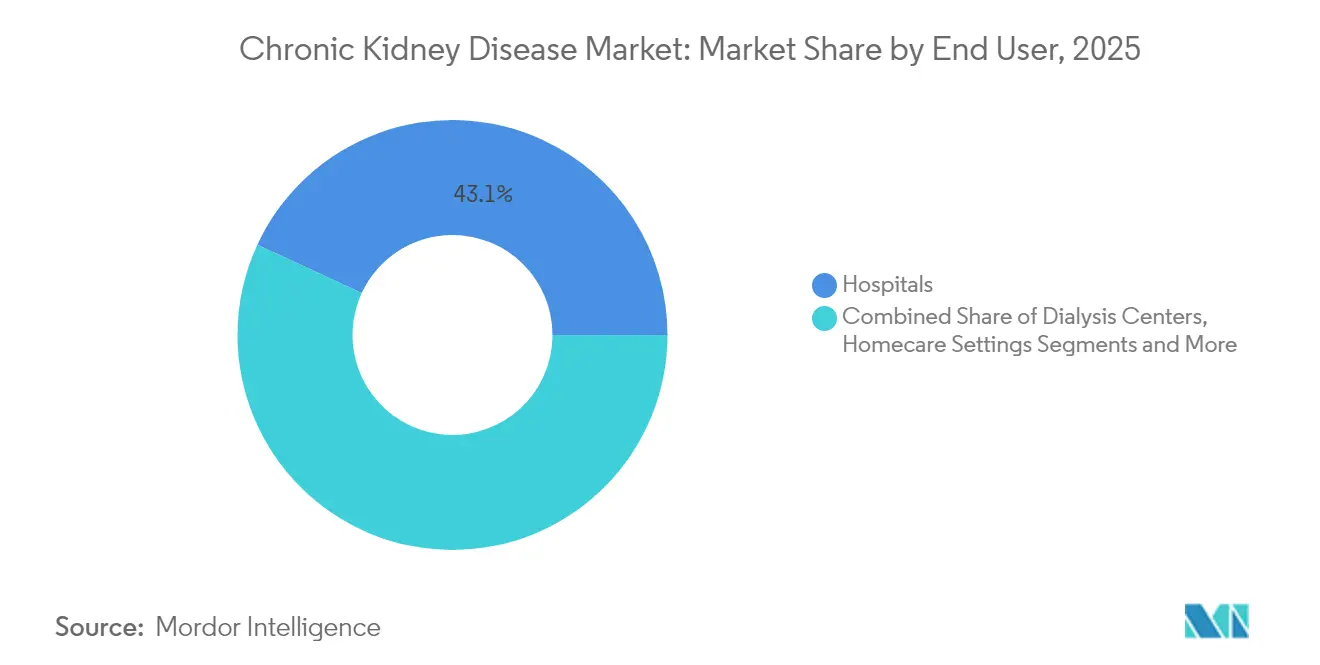

- By end user, hospitals commanded 43.10% of the chronic kidney disease market share in 2025; dialysis centers post the fastest projected CAGR at 6.12% to 2031.

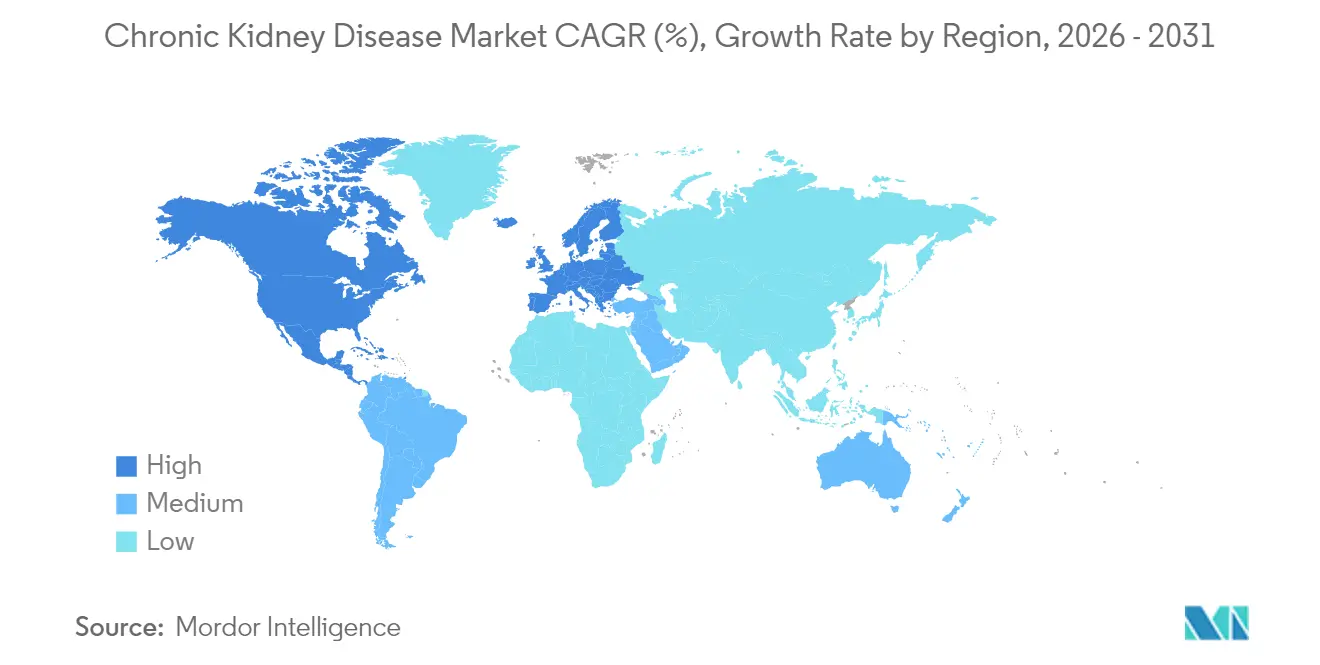

- By geography, North America led with 42.20% revenue share in 2025, whereas Asia-Pacific is projected to grow at 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chronic Kidney Disease Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetes & hypertension | +1.8% | Global, highest in APAC & North America | Long term (≥ 4 years) |

| Aging population escalating CKD incidence | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Technological advances in early diagnostics | +0.9% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Value-based kidney-care payment incentives | +0.7% | North America core, expanding to EU | Medium term (2-4 years) |

| AI-Driven Risk Stratification Tools | +0.6% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Growth Of Low-Carbon/Home Dialysis Devices | +0.4% | Global, with premium market focus initially | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes & Hypertension

Diabetes affects 537 million adults and hypertension another 1.28 billion, creating a vast at-risk pool for kidney damage. AstraZeneca modelling indicates up to 16.5% of populations in eight major countries may develop chronic kidney disease by 2032, with advanced-stage cases rising 59.3%. FDA expansion of semaglutide in 2025 demonstrated a 24% drop in kidney failure risk, linking endocrine and renal markets. These patterns elevate demand for preventive drugs, integrated care, and long-term monitoring. Medicare already spends USD 8.8 billion yearly on dialysis, underlining cost pressure for early action. As comorbid patients age into Medicare, the chronic kidney disease market is primed for solutions that delay progression and avoid costly renal replacement therapy.

Aging Population Escalating CKD Incidence

Kidney function declines about 1% yearly after age 40. In nations with rapid aging, such as Japan, diagnosis rates have surged, stressing capacity. Baby boomers entering their 70s and 80s present growing demand for dialysis and transplant services. Developing regions face the same demographic curve, but often lack infrastructure, prompting interest in home-based dialysis. Elderly patients require multidisciplinary management, raising demand for coordinated hospital, primary care, and specialized services. This demographic driver ensures steady volume growth well beyond the forecast horizon.

Technological Advances in Early Diagnostics

Point-of-care biomarker kits that detect KIM-1 or NGAL, AI-driven risk engines embedded in electronic records, and wearable patches such as the Alio SmartPatch bring detection earlier in the disease course. Earlier identification enables lifestyle and pharmacologic interventions that can slow decline, creating revenue streams for diagnostics vendors and drug makers. FDA reimbursement approvals for remote monitoring further widen adoption incentives. Providers now pivot from reactive treatment to proactive screening, reshaping resource allocation inside the chronic kidney disease market.

Value-Based Kidney-Care Payment Incentives

The Kidney Care Choices Model aligns reimbursement with outcomes. CMS set the 2026 ESRD base rate at USD 281.06 and introduced bonuses for quality and rural access. Providers investing in telehealth, risk analytics, and home dialysis gain financially when they reduce hospital visits. Commercial payers are mirroring these contracts, pushing the industry toward integrated networks that manage a patient from Stage 2 through transplantation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Dialysis & Treatment | -1.1% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Generic Erosion In Mature Drug Classes | -0.8% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Drug Safety & Adverse-Effect Concerns | -0.6% | Global, regulatory focus in North America & EU | Medium term (2-4 years) |

| ESG-Linked Supply-Chain Cost Pressures | -0.4% | Global, premium impact in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Dialysis & Treatment

Annual dialysis outlays can exceed USD 90,000 per patient, limiting access in lower-income economies and straining public budgets. Medicare already allocates USD 8.8 billion to dialysis each year [1]Clinical Journal of the American Society of Nephrology, “Economic Impact of Dialysis on Medicare,” cjasn.asnjournals.org . Many emerging markets lack broad insurance, so patients forgo or delay therapy, capping unit growth. Cost barriers spur exploration of bundled payments and portable devices, yet upfront investments remain challenging for under-resourced systems.

Generic Erosion in Mature Drug Classes

Patent cliffs for SGLT2 inhibitors such as Jardiance and Farxiga arrive in 2025. When generics hit, branded prices often fall 80-90%, shrinking revenue even as prescription volumes rise. Innovators pivot to rare-disease drugs like atrasentan or iptacopan where exclusivity lasts longer. Until pipelines replace lost income, pricing erosion slows overall chronic kidney disease market value growth in developed regions that mandate generic substitution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Treatment Dominance Drives Innovation

Treatment products generated 74.90% revenue in 2025, illustrating their central role across disease stages. The chronic kidney disease market size for treatment reached USD 63.55 billion and is projected to expand alongside new precision drugs and next-generation dialysis. FDA clearance of atrasentan for IgA nephropathy and iptacopan for complement 3 glomerulopathy underscores a shift to targeted therapy that can carry premium pricing . Dialysis technology is also evolving toward portable and wearable systems, reducing facility dependence and widening patient choice. Treatment manufacturers now bundle digital adherence tools to prove outcome gains in value-based contracts.

Diagnosis products hold a smaller slice yet post the fastest CAGR at 6.75%. Early detection kits, imaging advances, and AI-based risk models support this upswing. Rapid biomarker panels enable clinicians to stage disease well before serum creatinine rises, opening an expanding preventive market. Blood tests still account for most diagnostic revenue, but urine biomarker panels and imaging upgrades gain share as clinicians adopt multi-modal assessment pathways. Continuous monitoring devices could soon allow real-time eGFR tracking, fostering subscription revenue models for device makers.

By End User: Hospitals Lead While Dialysis Centers Accelerate

Hospitals captured 43.10% revenue in 2025 by offering multidisciplinary care. The chronic kidney disease market size attributed to hospitals is set to rise steadily, although growth will lag specialized centers as reimbursement shifts to bundled payments. Hospitals focus investments on coordinated clinics that manage cardiovascular and metabolic comorbidities in one visit, reinforcing their referral control over later-stage therapies.

Dialysis centers post the fastest 6.12% CAGR through 2031, powered by specialization and operational efficiency. Integrated digital platforms streamline scheduling, vascular access tracking, and quality reporting, helping centers outperform hospital units on clinical metrics. Homecare shows emerging momentum because portable devices permit self-administration with tele-supervision. As patient education improves, a hybrid model blending in-center training with home sessions may become standard, reshaping the chronic kidney disease industry over the decade.

Geography Analysis

North America led with 42.20% revenue in 2025, underpinned by broad insurance coverage and early uptake of novel drugs and devices. The United States anchors this lead; its duopoly dialysis structure imparts economies of scale but invites antitrust review. Canada follows with universal coverage, while Mexico’s recent CKD screening campaigns expand diagnosis volumes.

Asia-Pacific is the fastest-growing region at 6.98% CAGR. China invests heavily in chronic disease clinics and domestic generic production that cuts therapy costs. India’s manufacturing base drives affordable SGLT2 inhibitors, widening access across low-income states. Japan, with the world’s oldest population, continues to deploy advanced home hemodialysis systems and invests in wearable artificial kidney trials. South Korea and Australia reinforce regional momentum through proactive tele-nephrology programs.

Europe, the Middle East & Africa, and South America offer moderate growth. Europe benefits from universal payer systems but seeks cost-savings via generics and home therapies. Gulf Cooperation Council states invest in transplant centers to offset regional dialysis demand. Africa faces strained infrastructure yet gains from public-private partnerships introducing low-cost peritoneal dialysis. South America, led by Brazil, incrementally raises CKD awareness and funds screening in primary care.

Competitive Landscape

Dialysis services remain concentrated: DaVita and Fresenius Medical Care controlled major of US treatments in 2024, prompting FTC scrutiny on competitive practices. Both firms pursue vertical integration by acquiring nephrology groups and launching Medicare Advantage plans that align with value-based metrics.

Pharmaceutical competition is more fragmented. AstraZeneca, Boehringer Ingelheim, and Novo Nordisk advance SGLT2 inhibitor life-cycle strategies, while Chinook and Novartis focus on rare disease biologics. Private equity demonstrates growing interest; Baxter divested its kidney unit to Carlyle for USD 3.8 billion, and InterWell Health formed from a three-way merger to scale integrated care.

Technology entrants target white-space opportunities. Vantive committed over USD 1 billion to next-generation home dialysis. United Therapeutics secured FDA clearance for xenotransplantation trials, aiming to solve organ shortages [3]United Therapeutics, “FDA Clears Xenotransplantation Kidney Trial,” ir.unither.com . AI diagnostic startups partner with health systems to embed predictive tools into standard workflows, creating acquisition targets for strategic buyers seeking digital capabilities.

Chronic Kidney Disease Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche Ltd

Siemens Healthineers

Pfizer Inc

AbbVie Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: FDA approved a new indication for semaglutide to reduce kidney and cardiovascular events in adults with type 2 diabetes and chronic kidney disease.

- March 2025: FDA expanded Furoscix to treat edema in chronic kidney disease, including nephrotic syndrome, with availability slated for Apr 2025.

- March 2025: FDA cleared an expanded furosemide injection indication covering edema in adult chronic kidney disease patients.

- November 2024: FDA accepted Unicycive’s NDA for Oxylanthanum Carbonate with PDUFA date Jun 2025.

Global Chronic Kidney Disease Market Report Scope

Chronic kidney disease is a condition that causes reduced kidney function over time. Various tests, such as kidney function tests and diagnostic imaging tests, detect the proper function of the kidney and check for the presence of lesions, obstructions, kidney stones, and fluid accumulation around the kidneys. The Chronic Kidney Disease Market is Segmented by Product Type (Diagnosis (Blood Tests, Urine Tests, Imaging Tests, and Other Diagnostic Products), Treatment (Drug Class, Dialysis, and Other Product Types), End User (Hospital, Diagnostic Laboratories, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Diagnosis | Blood Tests | |

| Urine Tests | ||

| Imaging Tests | ||

| Point-of-Care Kidney Tests | ||

| Other Diagnosis Products | ||

| Treatment | Drug Class | ACE Inhibitors |

| Angiotensin-II Receptor Blockers | ||

| Diuretics | ||

| SGLT2 Inhibitors | ||

| Mineralocorticoid Receptor Antagonists | ||

| Erythropoiesis Stimulating Agents | ||

| Phosphate Binders | ||

| HIF-PH Inhibitors (Vadadustat etc.) | ||

| Other Drug Classes | ||

| Dialysis | Hemodialysis | |

| Peritoneal Dialysis | ||

| Home Dialysis Systems | ||

| Wearable & Portable Dialysis | ||

| Other Treatment Products | ||

| Hospitals |

| Dialysis Centers |

| Homecare Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Diagnosis | Blood Tests | |

| Urine Tests | |||

| Imaging Tests | |||

| Point-of-Care Kidney Tests | |||

| Other Diagnosis Products | |||

| Treatment | Drug Class | ACE Inhibitors | |

| Angiotensin-II Receptor Blockers | |||

| Diuretics | |||

| SGLT2 Inhibitors | |||

| Mineralocorticoid Receptor Antagonists | |||

| Erythropoiesis Stimulating Agents | |||

| Phosphate Binders | |||

| HIF-PH Inhibitors (Vadadustat etc.) | |||

| Other Drug Classes | |||

| Dialysis | Hemodialysis | ||

| Peritoneal Dialysis | |||

| Home Dialysis Systems | |||

| Wearable & Portable Dialysis | |||

| Other Treatment Products | |||

| By End User | Hospitals | ||

| Dialysis Centers | |||

| Homecare Settings | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How big is the Chronic Kidney Disease Market?

The Chronic Kidney Disease Market size is expected to reach USD 89.29 billion in 2026 and grow at a CAGR of 5.24% to reach USD 115.26 billion by 2031.

Which product segment contributes the most revenue?

Treatment products dominate with 74.90% revenue share in 2025, supported by lifelong drug and dialysis needs.

Who are the key players in Chronic Kidney Disease Market?

Abbott Laboratories, F. Hoffmann-La Roche Ltd, Siemens Healthineers, Pfizer Inc and AbbVie Inc are the major companies operating in the Chronic Kidney Disease Market.

Why is Asia-Pacific the fastest-growing region?

Rapid aging, rising diabetes prevalence, and major infrastructure investments drive a 6.98% CAGR through 2031.

Which region has the biggest share in Chronic Kidney Disease Market?

In 2025, the North America accounts for the largest market share in Chronic Kidney Disease Market.

Page last updated on: