Global Blood Warmer Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

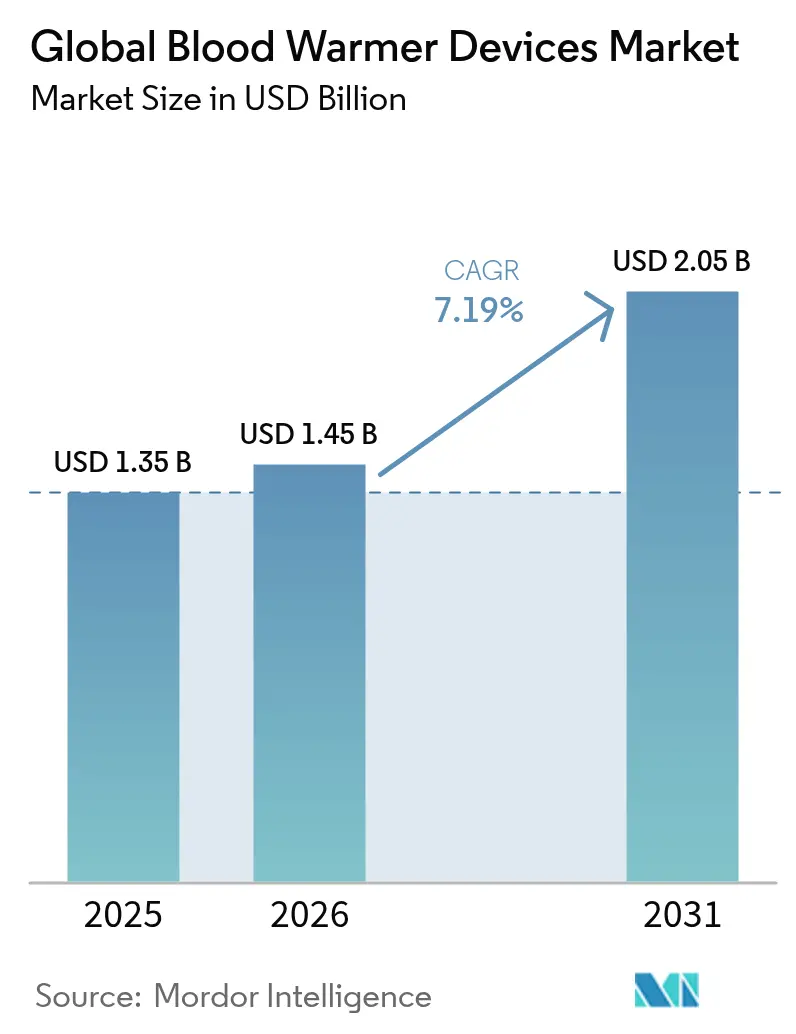

| Market Size (2026) | USD 1.45 Billion |

| Market Size (2031) | USD 2.05 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

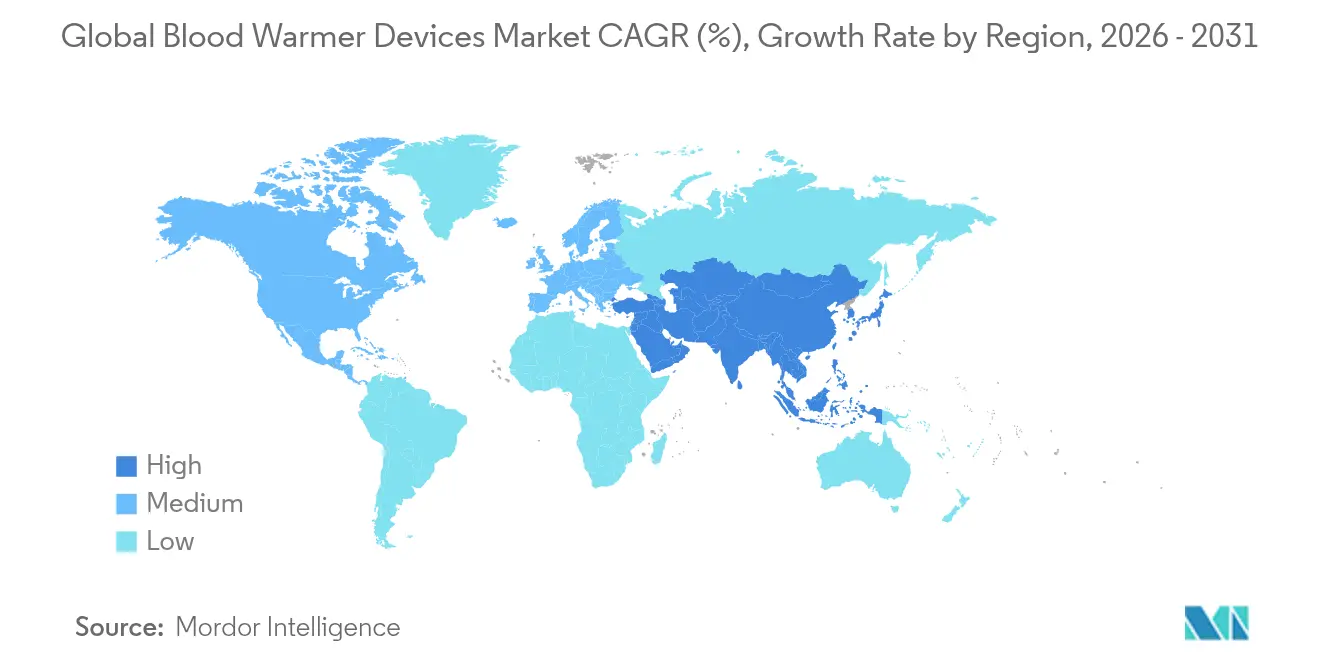

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Blood Warmer Devices Market Analysis by Mordor Intelligence

The blood warmer devices market size is expected to grow from USD 1.35 billion in 2025 to USD 1.45 billion in 2026 and is forecast to reach USD 2.05 billion by 2031 at 7.19% CAGR over 2026-2031. Strong momentum comes from the push to keep surgical and trauma patients normothermic, escalating trauma procedure volumes, and rapid military uptake of portable systems. Continuous-warming mandates issued by the Association of periOperative Registered Nurses in March 2025 have heightened hospital compliance efforts, while recent FDA guidance on medical-device supply-chain resilience has sharpened focus on uninterrupted product availability. Manufacturers respond with integrated IoT logging, battery life extensions, and battlefield-grade ruggedisation—features that win new contracts from defense and emergency-medical service (EMS) buyers.

Key Report Takeaways

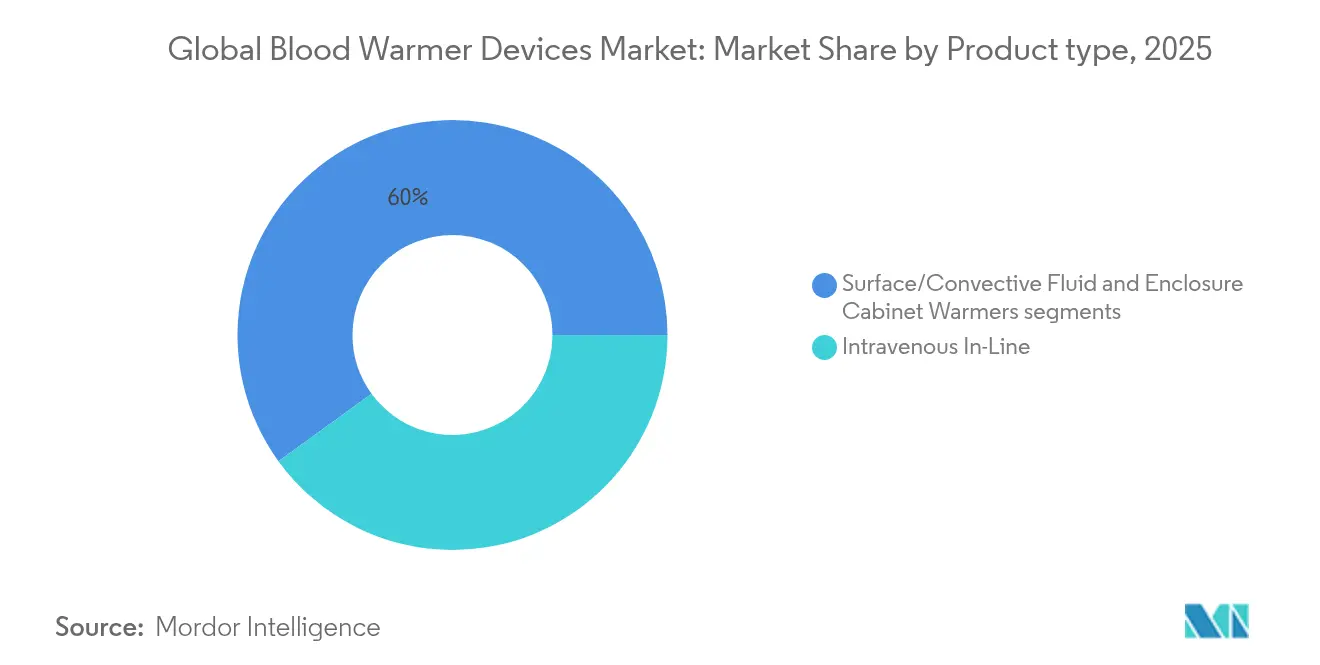

- By product type, intravenous in-line systems led with 40.02% revenue share in 2025, whereas surface warmers are projected to expand at an 8.05% CAGR to 2031.

- By modality, portable units commanded 60.05% of the blood warmer devices market share in 2025, and this modality is forecast to post an 8.62% CAGR through 2031.

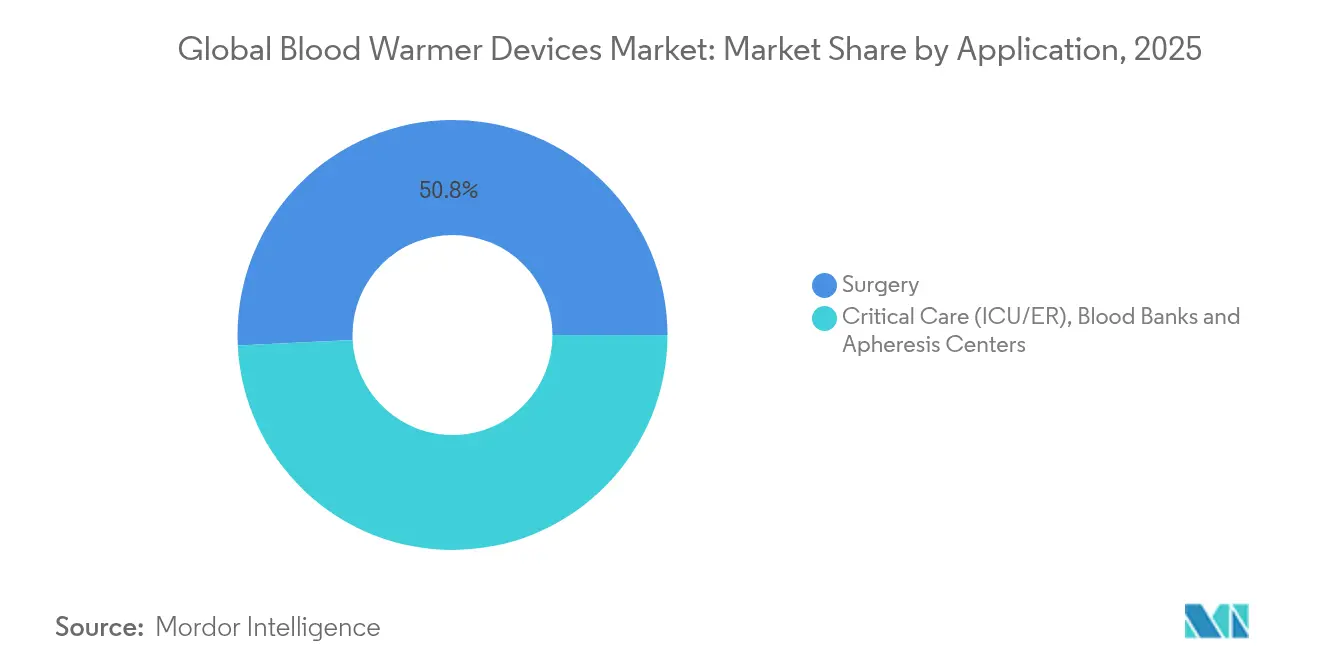

- By application, surgery accounted for a 50.78% share of the blood warmer devices market size in 2025, while military & EMS adoption is advancing at a 9.18% CAGR to 2031.

- By geography, North America held 44.68% of the blood warmer devices market in 2025; the Asia-Pacific region is expected to grow the fastest at a 9.98% CAGR over the period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Warmer Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising trauma & emergency surgery volumes | +1.8% | Global, with concentration in North America & Europe | Short term (≤ 2 years) |

| Stringent peri-operative normothermia guidelines | +1.2% | Global, led by North America & EU regulatory frameworks | Medium term (2-4 years) |

| Adoption of portable, battery-operated warmers in military & EMS | +0.9% | North America, Europe, with expansion to APAC | Medium term (2-4 years) |

| Integration of IoT temperature logging for compliance | +0.6% | North America & EU primarily, gradual APAC adoption | Long term (≥ 4 years) |

| AI-assisted real-time perfusion monitoring | +0.4% | North America & Europe advanced healthcare systems | Long term (≥ 4 years) |

| Stem-cell & apheresis therapy growth needing large-volume warming | +0.3% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Trauma & Emergency Surgery Volumes

Global trauma caseloads keep climbing, driven by road accidents, ageing populations and prolonged conflict zones. The U.S. Joint Trauma System recorded a 44% drop in battlefield deaths once automated blood-warming logistics became standard practice health.mil. Emergency-department studies show prehospital transfusion programs could benefit as many as 900,000 U.S. patients annually, underscoring the need for reliable warmers that avert hypothermia-related mortality. Mass-transfusion protocols now embed warming requirements, making the blood warmer devices market central to hospital trauma-care budgets.

Stringent Peri-operative Normothermia Guidelines

Updated AORN guidelines mandate continuous warming from pre-induction through recovery, threatening legal exposure for facilities that fail to comply[1]Source: Association of periOperative Registered Nurses, “Patient Temperature Management Guideline,” aorn.org. Complementary FDA test-protocols released in March 2024 standardise thermal-effect evaluation, accelerating procurement of systems with automatic shut-off and ±0.1 °C accuracy. Clinical evidence ties uncorrected peri-operative hypothermia to 9% higher complication rates and a 14% lift in acute kidney injury, further motivating hospitals to deploy state-of-the-art devices.

Adoption of Portable Warmers in Military & EMS

The MEQU portable system secured FDA clearance and a UK Ministry of Defence order in 2024, catalysing demand for battery-powered units that operate for up to 19 hours in austere settings. U.S. EMS agencies in 23 states now run blood-on-board programs, though they represent <1% of national services, signaling ample headroom for growth. Portable devices satisfy Committee on Tactical Combat Casualty Care protocols requiring 38-42 °C output regardless of ambient conditions.

Integration of IoT Temperature Logging for Compliance

January 2025 FDA interoperability rules oblige medical devices to export time-stamped temperature data, spurring embedded-sensor adoption. The ISO/IEEE 11073-10206 framework finalised in 2024 lets warmers feed hospital information systems directly, cutting paperwork and easing audits. Early field data show connected units can predict divergence events six minutes ahead of loss of normothermia, helping clinicians adjust flow rates proactively.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of hemolysis & protein denaturation at supra-physiologic temps | -0.8% | Global, particularly in quality-sensitive markets | Short term (≤ 2 years) |

| Capital cost sensitivity in LMIC hospitals | -1.2% | LMIC regions, concentrated in Sub-Saharan Africa & South Asia | Medium term (2-4 years) |

| Disposable set incompatibility across brands | -0.6% | Global, with higher impact in multi-vendor healthcare systems | Medium term (2-4 years) |

| Supply-chain fragility for heating elements rare-earths | -0.7% | Global, with acute impact in Asia-Pacific manufacturing hubs | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Risk of Hemolysis & Protein Denaturation

Temperatures exceeding 46 °C cause measurable red-cell rupture, while proteins begin denaturing at 43 °C after two-hour exposure. Trials on irradiated leukoreduced units warmed to 60 °C recorded sharp potassium release, elevating cardiac-arrest risk in neonates. Device makers now integrate triple sensors, automatic bypass and instant shut-off, which add cost and raise validation hurdles but are essential for patient safety.

Capital-Cost Sensitivity in LMIC Hospitals

Resource-constrained hospitals often face device downtime when blood stocks appear only 26-50% of the time, as documented in Ethiopia. A cost study at a leading Indian neurosurgery centre found machinery and equipment drive 43.6% of operating expenses, a burden not offset by user fees. Faced with budget trade-offs, many facilities prioritise ventilators over blood warmers, restraining adoption despite clinical need.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: In-line Precision Sets the Standard

Intravenous in-line systems controlled 40.02% of 2025 revenue, demonstrating the blood warmer devices market preference for seamless integration and tight temperature control. Units such as 3M’s Ranger 245 reach set-point in 45 seconds and manage concurrent infusions between 37 °C and 41 °C, making them the workhorse for operating-theatre and trauma-bay protocols. Surface warmers, although niche in absolute sales, register an 8.05% CAGR, propelled by EMS crews that value flexible wrapping pads deployable inside ambulances or aircraft.

Clinical evidence underlines why in-line models dominate. Comparative trials show fresh blood warmed at 47 °C for one hour displayed no cell damage, whereas immersion baths showed higher variability. Cabinet units such as Sarstedt’s SAHARA-III still serve blood banks needing large-volume processing without water immersion, yet growth pivots to smaller, agile devices for point-of-care use.

By Modality: Portables Power Field Medicine

The portable format accounted for 60.05% of global turnover in 2025, underscoring how battlefield and ambulance environments shape the blood warmer devices market. Systems like MEQU’s compact cartridge design can warm 4 units at flow rates up to 150 mL/min while running on a single rechargeable pack. Stationary models stay relevant in ICUs and OR suites where grid power is constant and higher throughput is required.

Portable systems post an 8.62% CAGR through 2031 as defense spending and civilian EMS programs converge around rapid transfusion protocols. Committee on Tactical Combat Casualty Care specifications demand devices withstand -20 °C to +50 °C and a 1.2 m drop, criteria driving ruggedised build quality wms.org. Stationary installations, conversely, evolve through software integrations that auto-populate electronic medical records, simplifying audits and maintenance scheduling.

By Application: Surgery Still Largest, Military & EMS Surge Fastest

Surgical use retained 50.78% share of the blood warmer devices market size in 2025, backed by escalating procedure counts and zero-tolerance norms for peri-operative hypothermia. Military and EMS segments climb at a 9.18% CAGR as 152 U.S. agencies now carry whole blood, validating prehospital transfusion economics.

Continuous-warming forced-air blankets remain the gold standard in theatre, yet ICU guidelines for traumatic brain injury patients now prioritise steady 37 °C perfusion, boosting ward-based demand. Blood-bank and apheresis settings rely on specialised cabinets that gently thaw stem-cell grafts while maintaining cryoprotectant integrity, a niche albeit steadier revenue stream.

Geography Analysis

North America led with 44.68% of 2025 revenue, reflecting mature reimbursement, stringent FDA oversight and a well-funded EMS network that already fields blood on board in 23 states. Medicare payment updates for 2025-2026 increase quality incentives tied to normothermia compliance, driving new hospital upgrades federalregister.gov. Pentagon innovations such as the Automated Battlefield Trauma System, which delivered a 44% mortality reduction, spill over into civilian care and sustain upstream demand.

Europe shows balanced expansion as harmonised Medical Device Regulation and intensive-care society guidelines reinforce thermal-management standards. Consensus on targeted temperature control for traumatic brain injury, adopted by leading centres in Germany, France and the United Kingdom, secures a steady cadence of procurement despite supply-chain frictions triggered by regional geopolitical tensions

Asia-Pacific delivers the fastest compound growth at 9.98%, propelled by massive trauma caseloads and government infrastructure programmes in China, India and Southeast Asia. While venture funding dips curtailed some local start-ups, state procurement of battlefield-grade equipment after natural-disaster responses keeps the adoption curve steep. Price-sensitive public hospitals increasingly trial lower-cost portable units, opening new avenues for manufacturers that can tier offerings without diluting accuracy.

Competitive Landscape

Market concentration is moderate. 3M, Stryker and ICU Medical together hold good portion of revenue, leveraging established distribution and regulatory depth. Competitive thrust focuses on differentiated accuracy, IoT connectivity and military-grade portability. The Defense Health Agency secured five FDA clearances in 2024, including the MEQU Portable Blood and IV Fluid Warmer System, validating a fast-track defence origin pipeline.

Pricing pressure remains secondary to performance, but capital-expenditure shy hospitals in lower-income markets incentivise stripped-down, single-use cartridge innovations. Larger vendors respond with financing packages and swap-out programmes that offset up-front costs. Strategic M&A shapes product breadth: Stryker’s June 2025 agreement to buy Inari Medical for USD 4.9 billion extends its vascular reach, reinforcing adjacent use-cases that rely on warmed blood during complex interventions[2]Source: Stryker Corporation, “Inari Medical Acquisition Press Release,” stryker.com .

Global Blood Warmer Devices Industry Leaders

3M

Geratherm Medical

Stryker Corporation

Smiths Group

The 37Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FDA cleared Giotto Monza automated blood component separator and AHC Platelet Concentrate Separator, bolstering temperature-controlled processing capacity.

- April 2024: Babson Diagnostics unveiled a hand-warming tool to improve capillary blood collection.

Global Blood Warmer Devices Market Report Scope

As per the scope of the report, Blood Warmer Devices are basically designed for warming fluids, colloids, crystalloids, or blood products, prior to administration to prevent hypothermia inpatient. Hypothermia causes complications in surgeries such as coma or cardiac arrest. The Blood Warmer Devices Market is Segmented by Product (Surface Warming System, Intravenous Warming System, and Patient Warming Accessories), By End User (Hospitals, Blood Banks, and Others), and by Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Intravenous In-Line |

| Surface/Convective Fluid |

| Enclosure Cabinet Warmers |

| Portable |

| Stationary |

| Surgery & Peri-operative Care |

| Critical Care (ICU/ER) |

| Blood Banks & Apheresis Centers |

| Military & EMS Use |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| by Product Type (Value) | Intravenous In-Line | |

| Surface/Convective Fluid | ||

| Enclosure Cabinet Warmers | ||

| by Modality (Value) | Portable | |

| Stationary | ||

| by Application (Value) | Surgery & Peri-operative Care | |

| Critical Care (ICU/ER) | ||

| Blood Banks & Apheresis Centers | ||

| Military & EMS Use | ||

| Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What temperature window do blood warmers typically maintain?

Most devices target 37-42 °C, keeping well below the 43 °C threshold at which protein denaturation becomes significant.

How long can modern portable warmers operate without mains power?

Current battery designs deliver up to 19 hours of continuous function while holding temperature within ±6.47%.

Which market segment is expanding the quickest?

Military and EMS applications grow at a 9.18% CAGR, propelled by broader prehospital transfusion programmes and defence spending.

Are special regulatory clearances required for portable battlefield warmers?

Yes. Devices need FDA 510(k) clearance and must meet Committee on Tactical Combat Casualty Care specifications for ruggedisation and output temperature.

Page last updated on: