Hemoglobin Feed Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.27 Billion |

| Market Size (2030) | USD 3.09 Billion |

| Growth Rate (2025 - 2030) | 6.39% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

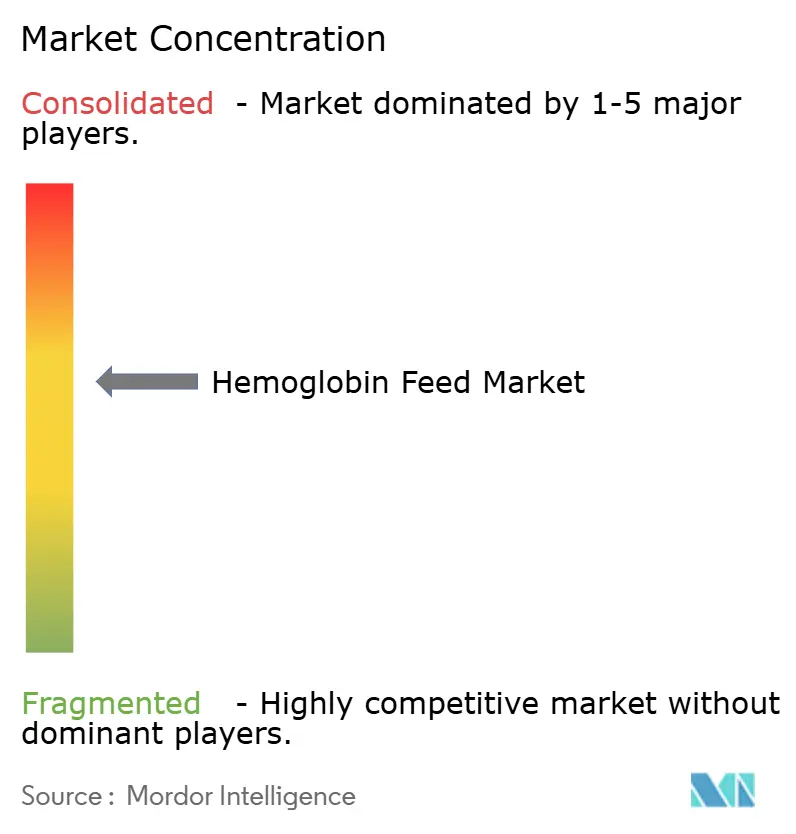

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemoglobin Feed Market Analysis by Mordor Intelligence

The hemoglobin feed market size stands at USD 2.27 billion in 2025, and it is expected to advance at a 6.39% CAGR to reach USD 3.09 billion by 2030. Growth is anchored by rapid aquaculture expansion, sustained protein demand from commercial pig farming, and processing innovations that improve cost-competitiveness against fishmeal.[1]Fisheries and Aquaculture Division, “Fisheries and Aquaculture Projections 2022–2032,” Food and Agriculture Organization, fao.org Rising regulatory clarity in Europe, technology upgrades in Asia, and pet-food premiumization add momentum, while disease-transmission concerns and complex North American approval pathways temper the outlook. Competitive intensity is moderate; established renderers leverage scale and vertically integrated supply chains, whereas niche entrants focus on enzymatic hydrolysis and precision fermentation to address sustainability and functionality requirements. Long-term opportunities center on marine-derived hemoglobin, bioactive peptide development, and region-specific formulations that align with evolving livestock production models.

Key Report Takeaways

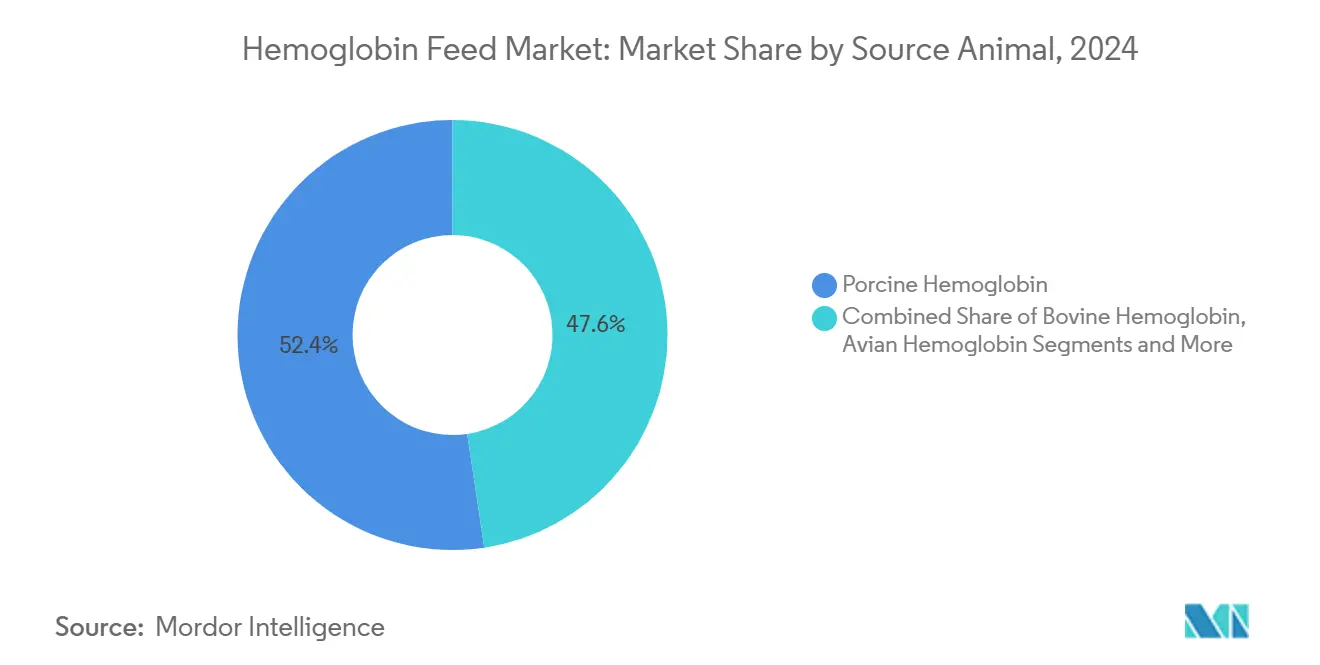

- By source animal, porcine hemoglobin led with 52.36% hemoglobin feed market share in 2024, while fish hemoglobin is projected to expand at a 9.25% CAGR through 2030.

- By form, spray-dried powder commanded 68.44% of the hemoglobin feed market size in 2024; liquid formats are forecast to post a 9.49% CAGR to 2030.

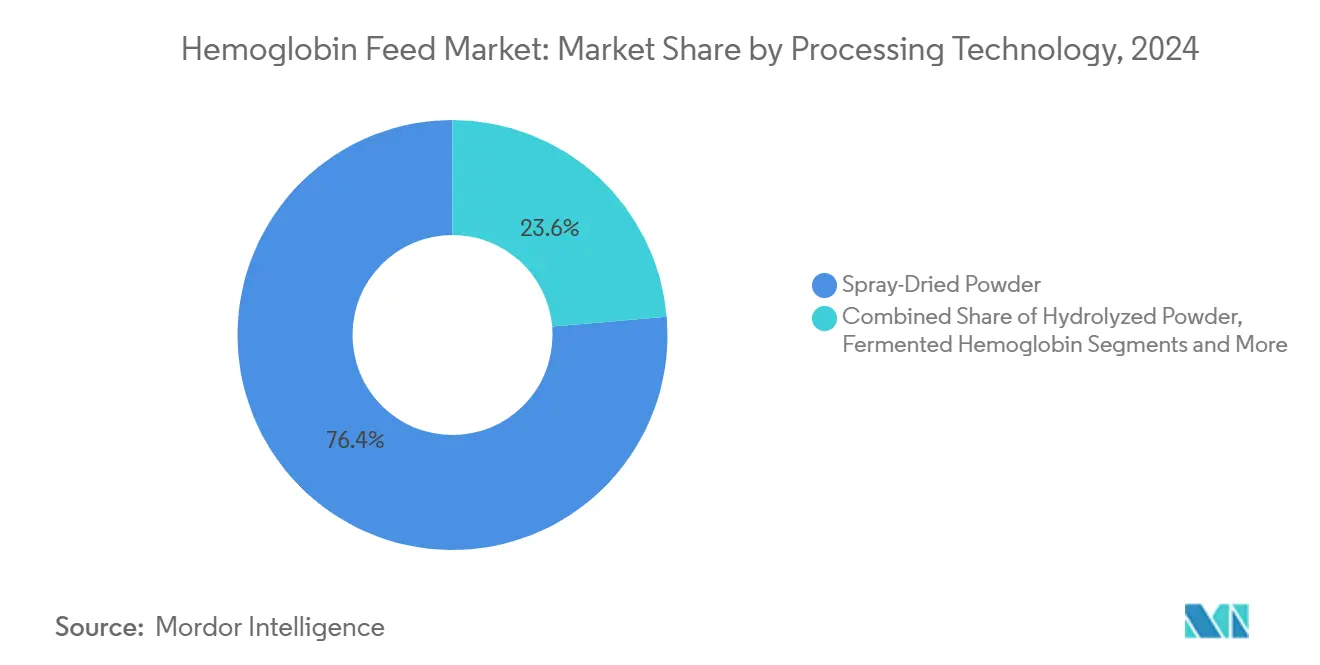

- By processing technology, spray-dried powder held 76.36% revenue share in 2024, whereas enzymatic hydrolysate liquid is advancing at a 10.27% CAGR.

- By application, aquaculture feed accounted for a 44.62% share of the hemoglobin feed market size in 2024; pet food and specialty segments are growing at an 8.36% CAGR.

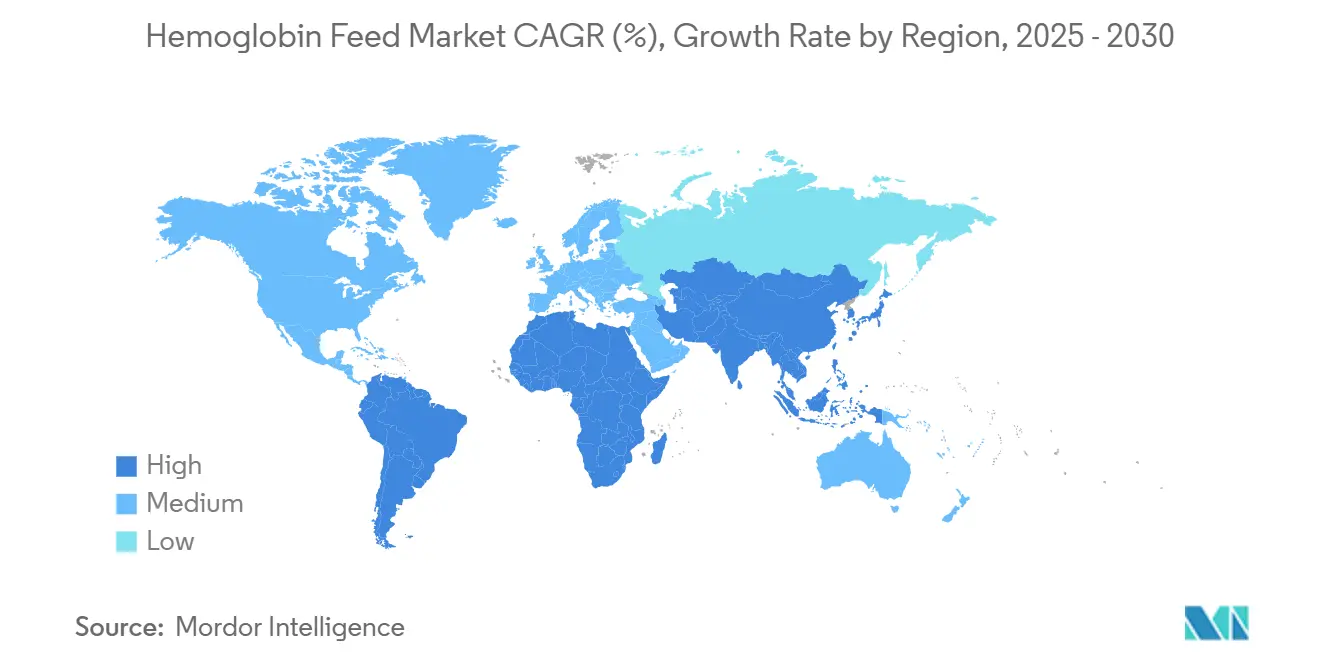

- By geography, Asia-Pacific maintained leadership with 36.48% share in 2024, while South America records the fastest regional CAGR at 8.53% through 2030.

Global Hemoglobin Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Protein Demand From Aquaculture Sector | +1.8% | Global, with APAC leadership | Long term (≥ 4 years) |

| Cost-Competitiveness Versus Fishmeal | +1.2% | Global, particularly emerging markets | Medium term (2-4 years) |

| Rapid Growth Of Commercial Pig Farming In Asia | +0.9% | APAC core, spill-over to Latin America | Medium term (2-4 years) |

| Digestibility & Feed-Conversion Efficiency Advantages | +0.7% | Global | Short term (≤ 2 years) |

| EU Approval Of Non-Ruminant Processed Animal Proteins In Aquafeed | +0.5% | Europe, with global regulatory influence | Short term (≤ 2 years) |

| Advances In Blood Fractionation & Spray-Drying Technology | +0.4% | North America & EU innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Protein Demand From Aquaculture Sector

Global aquaculture production is forecast to exceed 100 million tonnes in 2027, lifting the need for alternative proteins that can supplement dwindling fishmeal supplies. Hemoglobin powder offers a digestible amino acid profile and heme iron that supports growth and pigmentation in farmed species, thereby closing nutritional gaps while easing pressure on marine stocks.[2]Joana Silva, “Does Iron Supplementation Improve Post-Smolts Atlantic Salmon Performance and Health?” BioMar, biomar.com Intensive production systems amplify feed conversion requirements, positioning hemoglobin as a cost-effective bridge ingredient between traditional fishmeal and newer plant or insect proteins. Research confirms that partial fishmeal replacement with hemoglobin maintains performance across shrimp, tilapia, and salmon, underscoring broad applicability. Sustainability certifications pursued by major aquafeed producers further encourage adoption because hemoglobin leverages existing slaughterhouse streams and reduces waste. As aquaculture’s share of global seafood consumption climbs, demand for hemoglobin feed is expected to escalate across Asia, Latin America, and eventually Africa.

Cost-Competitiveness Versus Fishmeal

Tight fishmeal supply––driven by El Niño disruptions and stricter South American quotas––has pushed average global prices above USD 1,800 per metric ton in 2025, widening the gap with spray-dried hemoglobin powder that trades about 30% lower on a protein-adjusted basis. Enzymatic hydrolysis breakthroughs cut processing energy by 25%, shrinking production costs and allowing suppliers to price aggressively without sacrificing margins. In emerging Asian aquaculture hubs where feed accounts for 70% of production expenses, formulators are substituting 10%–15% fishmeal with hemoglobin to stabilize ration costs. The same economics hold for intensive pig and poultry operations in Latin America, where protein-price volatility materially affects farm profitability. As supply chains scale, unit costs are expected to fall a further 8% by 2030, reinforcing hemoglobin’s price advantage and solidifying its role as a mainstream ingredient.

Rapid Growth Of Commercial Pig Farming In Asia

Pig herds in Asia expanded 30.6% from 2014 to 2024 and are projected to grow another 16% by 2034, lifting total regional sow inventories and feed requirements. Large integrators in China and Vietnam are shifting from back-yard farms to multi-site systems that rely on precision nutrition to optimize litter size and survival. Trials show maternal diets fortified with hemoglobin-derived heme iron increase live births by 0.6 piglets per litter and boost average birth weight by 5%. The Philippines’ successful African swine fever repopulation demonstrates renewed optimism, while Vietnamese smart-pig initiatives embed automated feed dispensers calibrated for hemoglobin-enriched rations. Growing demand for antibiotic alternatives also plays in hemoglobin’s favor because bioactive peptides generated during hydrolysis exhibit antioxidant and anti-inflammatory properties, improving gut health and reducing mortality. These benefits make hemoglobin an attractive option for Asia’s expanding commercial pig sector.

Digestibility & Feed-Conversion Efficiency Advantages

Hemoglobin contains 94% digestible protein and a balanced essential amino acid profile comparable to fishmeal, enabling efficient nitrogen utilization in monogastric species. Its heme-bound iron delivers higher absorption than inorganic salts, reducing anemia risk and enhancing immune function. Feed conversion improvements of 5%–7% have been documented in broilers and weaned piglets when 2%–4% hemoglobin powder replaces plant protein. Lower inclusion rates translate into smaller diet footprints and less manure nitrogen, aligning with environmental mandates in Europe and North America. Because energy costs represent up to 30% of feed production expenses, the ability to use hemoglobin at low temperatures without extensive heat treatment further strengthens its efficiency credentials. These nutritional and operational gains collectively contribute to lower production costs and better profitability for livestock producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zoonotic & Disease-Transmission Concerns | -0.8% | Global, heightened in developed markets | Short term (≤ 2 years) |

| Stringent Regulatory Approvals In North America & EU | -0.6% | North America & EU, with global influence | Medium term (2-4 years) |

| Consumer Aversion To Animal By-Products In Feed | -0.4% | Developed markets, premium segments | Long term (≥ 4 years) |

| Emerging Competition From Insect-Based Proteins | -0.3% | Global, concentrated in innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Zoonotic & Disease-Transmission Concerns

The 2024 H5N1 outbreak in U.S. dairy cattle raised awareness of cross-species disease risks, prompting regulators to scrutinize blood-derived inputs more closely. Studies show that Babesia microti can infect hosts at densities as low as 1.09 parasites/µL, illustrating the need for ultra-low pathogen detection in blood streams destined for feed.[3]Yuchun Cai, “Transmission Risk Evaluation of Transfusion Blood Containing Low-Density Babesia microti,” Frontiers in Cellular and Infection Microbiology, frontiersin.org Implementing pathogen-reduction steps such as UV treatment, filtration, and post-drying heat stabilization increases processing complexity and cost. Supply chains may experience temporary raw-blood shortages when slaughterhouses enforce stricter biosecurity measures after disease alerts. While these protocols ultimately improve safety, they add friction that slows adoption in risk-averse markets like the United States and Germany.

Stringent Regulatory Approvals In North America & EU

FDA Guidance #293, issued in October 2024, shifts the review of AAFCO-defined ingredients to an independent framework, lengthening approval timelines and raising dossier costs for new hemoglobin formats. In Europe, novel-food rules require species-specific toxicology data and a minimum two-year evaluation, delaying launches and favoring incumbents with extensive regulatory resources. Compliance with HARPC plans under the U.S. Food Safety Modernization Act demands continuous hazard analysis and documentation, stretching manpower for small and mid-size processors. These hurdles elevate entry barriers and can deter innovation, particularly in highly specialized peptides or hydrolysates that fall outside existing definitions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Animal: Porcine Strength Meets Marine Momentum

Porcine streams dominated the hemoglobin feed market, holding a 52.36% share in 2024 because slaughterhouse networks and rendering infrastructure are well established across North America, Europe, and China. Fish hemoglobin, however, is projected to grow at a 9.25% CAGR as aquaculture formulators favor marine-sourced ingredients that align with species-specific dietary profiles. Robust supply of porcine blood offers cost stability, yet its perception as a terrestrial by-product can limit inclusion in fish diets seeking marine certificates. Fish hemoglobin benefits from inherent acceptance among salmon and shrimp producers and carries lower sulfide content, reducing off-odor risks during extrusion. Bovine and avian sources fill niche veterinary or specialty applications; their shares remain small because regulatory restrictions and disease-outbreak volatility hamper consistent collection. Precision-fermentation research, featuring engineered Bacillus subtilis strains yielding 1,034 mg/L heme, hints at a future hybrid supply model that offsets animal-source constraints while preserving functional equivalence.

Second-generation blood-fractionation plants in Denmark and the United States now separate plasma, globin, and heme fractions with near-zero water discharge, improving resource efficiency and generating high-purity porcine hemoglobin powders for performance diets. At the same time, Chilean salmon processors are piloting integrated fish-blood capture systems to upcycle processing effluents, creating new marine hemoglobin supply. As both terrestrial and marine channels evolve, suppliers capable of offering traceable, pathogen-screened material stand to capture premium buyers in Europe and Japan. The twin drivers of cost and sustainability will therefore determine how quickly fish hemoglobin gains share from porcine incumbents over the forecast horizon.

By Form: Powder Holds Ground While Liquid Gains Traction

Spray-dried powder accounted for 68.44% of the hemoglobin feed market share in 2024 thanks to superior shelf life, low water activity below 0.2, and bulk-density uniformity that suits automated feed lines. Liquid formats, registering a 9.49% CAGR, appeal to premix plants and wet-mash systems because they eliminate milling losses and enhance mixing homogeneity. Granular products, formed via agglomeration, address aquaculture’s sinking-rate requirements but remain a small niche. Recent electrohydrodynamic drying advances produce low-temperature powders with higher peptide integrity, blurring functional differences between legacy powders and emerging hydrolysate liquids. Feed mills in Vietnam report a 15% reduction in energy use when switching from conventional powder to stabilized liquid because fewer mechanical conveying steps are required.

Despite easier logistics, powders face rehydration challenges in high-fat aquatic pellets, prompting formulators to experiment with oil-based liquid hemoglobin emulsions for better adhesion. Packaging innovations such as recyclable IBC totes mitigate storage limitations for liquids and support adoption in Europe’s carbon-footprint-focused supply chains. Over time, high-concentrate liquids exceeding 45% solids are expected to erode powder’s volume dominance, particularly in regions where cold-chain logistics and just-in-time delivery are well developed.

By Processing Technology: Hydrolysis Redefines Functional Boundaries

Spray-dried powder remained the cornerstone technology, securing 76.36% of revenues in 2024 due to sunk-cost advantages and high throughput capacity exceeding 3 t/h per tower. Enzymatic hydrolysate liquids, however, deliver a 10.27% CAGR by unlocking bioactive peptides that enhance immune response and gut integrity in monogastric species. Sequential hydrolysis with Alcalase, Flavourzyme, and Protana Prime has been optimized to achieve a 33.39% degree of hydrolysis, producing peptide fractions below 3 kDa that display antioxidant and hypoglycemic activities [IJMS.ORG]. Hydrolyzed powders, a midpoint option, combine the shelf stability of powder with the solubility of hydrolysates and are gaining favor in swine creep feeds. Fermented hemoglobin represents an emergent pathway that leverages lactic acid bacteria to improve digestibility and aroma, although commercial output is presently limited.

Capital costs for enzymatic lines have fallen 12% since 2020, and enzyme suppliers now offer tailored blends that minimize bitter-peptide formation, improving palatability in pet food. Adoption is further supported by EU regulatory recognition of bioactive claims, allowing feed labels to list antioxidant or gut-health benefits tied to peptide content. As precision-nutrition platforms in aquaculture and pet food gain traction, demand for differentiated hydrolysates is set to absorb a growing slice of the hemoglobin feed market.

By Application: Aquaculture Dominates, Pet Food Surges

Aquaculture absorbed 44.62% of the hemoglobin feed market size in 2024 as salmon, shrimp, and tilapia producers sought cost-effective protein replacements for fishmeal amid tightening quotas. Trials replacing 25% fishmeal with hemoglobin maintained weight gain and feed conversion while improving fillet coloration, supporting broad formulation uptake. Swine feed remains the second-largest outlet, benefiting from hemoglobin’s heme iron that mitigates anemic conditions in piglets. Avian influenza disruptions constrain poultry usage, but integrators continue small-scale trials to leverage improved amino-acid balance.

Pet food logs the fastest growth at an 8.36% CAGR as owners gravitate toward high-protein, functional diets that enhance vitality and coat health. Hemoglobin supplies digestible iron and confers a natural red hue desired in raw and freeze-dried treats. Specialty segments such as zoo and exotic animals create additional but niche demand for custom hemoglobin blends tailored to carnivorous species’ needs. Formulators targeting sustainability goals highlight hemoglobin’s upcycling credentials, resonating with environmentally conscious consumers. Overall, multi-species versatility and functional benefits secure hemoglobin a stable role across diverse feed categories.

Geography Analysis

Asia-Pacific led the hemoglobin feed market with a 36.48% revenue share in 2024, powered by China’s scale, Vietnam’s digitized pig farms, and Japan’s leadership in biotechnological processing. Strong domestic demand for animal protein, combined with government-backed bio-manufacturing initiatives, supports continuous capacity investment in blood fractionation plants. Southeast Asian aquaculture growth, particularly in Indonesia and Malaysia, drives import demand for marine hemoglobin, while Australia’s salmon industry pilots porcine-derived peptides to optimize pellet durability.

South America is poised to register an 8.53% CAGR as Brazil’s integrated pork and tilapia clusters seek high-quality protein ingredients to serve domestic and export markets. Favorable currency dynamics and USDA-aligned quality standards make U.S. hemoglobin attractive despite freight costs. Emerging Argentine ventures are exploring low-carbon rendering facilities that recover heat for spray-drying, aligning with local sustainability mandates. Regional expansion is tempered by macroeconomic volatility, but strategic partnerships between slaughterhouses and feed manufacturers are mitigating investment risk.

North America and Europe exhibit slower growth due to stringent approval processes, yet they remain innovation hubs. The FDA’s evolving guidance raises costs, but it also elevates product standards, enabling American suppliers to command premiums in export markets. European salmon producers accelerate adoption following regulatory clearance for non-ruminant proteins, and Scandinavian startups are experimenting with fish-blood capture for in-house hemoglobin extraction. Disease-related supply interruptions, such as H5N1-linked plant shutdowns, underscore the need for diversified sourcing and robust biosecurity in these mature regions.

Competitive Landscape

The hemoglobin feed market comprises vertically integrated renderers, specialized hydrolysate producers, and technology-driven newcomers. Darling Ingredients generated USD 4.47 billion in feed-ingredient sales during 2023, representing 65.9% of total company revenue and illustrating the economies of scale large processors wield. Its 150-plus U.S. plants and 80 facilities elsewhere ensure raw-blood collection synergies and logistical efficiency that smaller players struggle to match. European processors leverage advanced spray-drying and membrane systems to differentiate on peptide functionality and color uniformity, appealing to premium aquaculture and pet-food customers.

Innovation is an increasingly important battleground. The Danish Technological Institute’s enzymatic protocol eliminates metallic off-flavors and improves heme bioavailability, attracting licensing interest from Asian plants. Chinese biotech firms invest in precision fermentation and enzyme-assisted extraction to create hybrid hemoglobin products with consistent quality regardless of slaughter fluctuations. North American startups develop electrospraying techniques that combine low-temperature drying with encapsulation to enhance stability and control iron release.

Strategic moves underscore consolidation and capability expansion. In 2025, a leading U.S. renderer acquired a Brazilian spray-drying plant to secure access to Latin American pig-blood streams and hedge disease-related supply risks. European aquafeed companies entered multi-year offtake agreements with Scandinavian fish-blood processors to guarantee marine-sourced hemoglobin volumes. Meanwhile, pet-food firms signed exclusivity contracts for enzymatic hydrolysates rich in antioxidant peptides, reinforcing value-added segmentation. The competitive field remains dynamic, with differentiation rooted in technology, regulatory acumen, and supply-chain reach.

Hemoglobin Feed Industry Leaders

Darling Ingredients

Bioiberica S.A.U.

Lican Food

Daka Denmark A/S

Kraeber & Co GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The European Commission authorized UV-treated powder of whole Tenebrio molitor larvae as a novel food, expanding the roster of alternative proteins that compete indirectly with hemoglobin feed

- October 2024: The FDA issued Guidance #293 outlining enforcement policy for AAFCO-defined animal feed ingredients, altering compliance pathways for hemoglobin feed producers.

Global Hemoglobin Feed Market Report Scope

| Porcine Hemoglobin |

| Bovine Hemoglobin |

| Avian Hemoglobin |

| Fish Hemoglobin |

| Powder |

| Granules |

| Liquid |

| Spray-Dried Powder |

| Enzymatic Hydrolysate (Liquid) |

| Hydrolyzed Powder |

| Fermented Hemoglobin |

| Aquaculture Feed |

| Swine Feed |

| Poultry Feed |

| Pet Food & Specialty Animal Feed |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source Animal | Porcine Hemoglobin | |

| Bovine Hemoglobin | ||

| Avian Hemoglobin | ||

| Fish Hemoglobin | ||

| By Form | Powder | |

| Granules | ||

| Liquid | ||

| By Processing Technology | Spray-Dried Powder | |

| Enzymatic Hydrolysate (Liquid) | ||

| Hydrolyzed Powder | ||

| Fermented Hemoglobin | ||

| By Application | Aquaculture Feed | |

| Swine Feed | ||

| Poultry Feed | ||

| Pet Food & Specialty Animal Feed | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hemoglobin feed market?

The hemoglobin feed market size is USD 2.27 billion in 2025.

How fast is the hemoglobin feed market expected to grow?

It is projected to expand at a 6.39% CAGR, reaching USD 3.09 billion by 2030.

Why are aquaculture companies adopting hemoglobin in feed?

Hemoglobin supplies digestible protein and heme iron, partially replacing costly fishmeal without sacrificing growth or pigmentation performance.

Which processing technology is growing the fastest?

Enzymatic hydrolysate liquid is the fastest, registering a 10.27% CAGR due to superior bioactive peptide content.

Which region holds the largest share of demand?

Asia-Pacific leads with 36.48% of global revenue thanks to its sizeable aquaculture and pig-farming sectors.

What is the main regulatory hurdle in North America?

FDA Guidance #293 requires extensive safety dossiers for new feed ingredients, lengthening approval timelines and increasing compliance costs.

Page last updated on: