Prothrombin Complex Concentrate Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

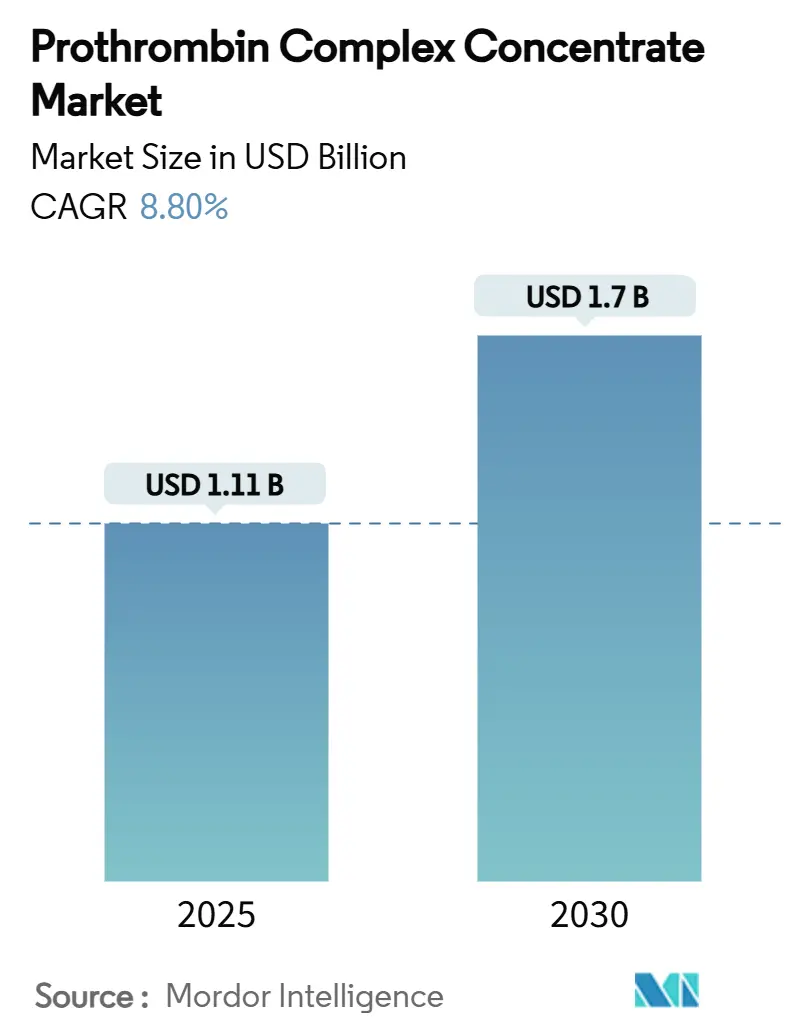

| Market Size (2025) | USD 1.11 Billion |

| Market Size (2030) | USD 1.7 Billion |

| Growth Rate (2025 - 2030) | 8.80% CAGR |

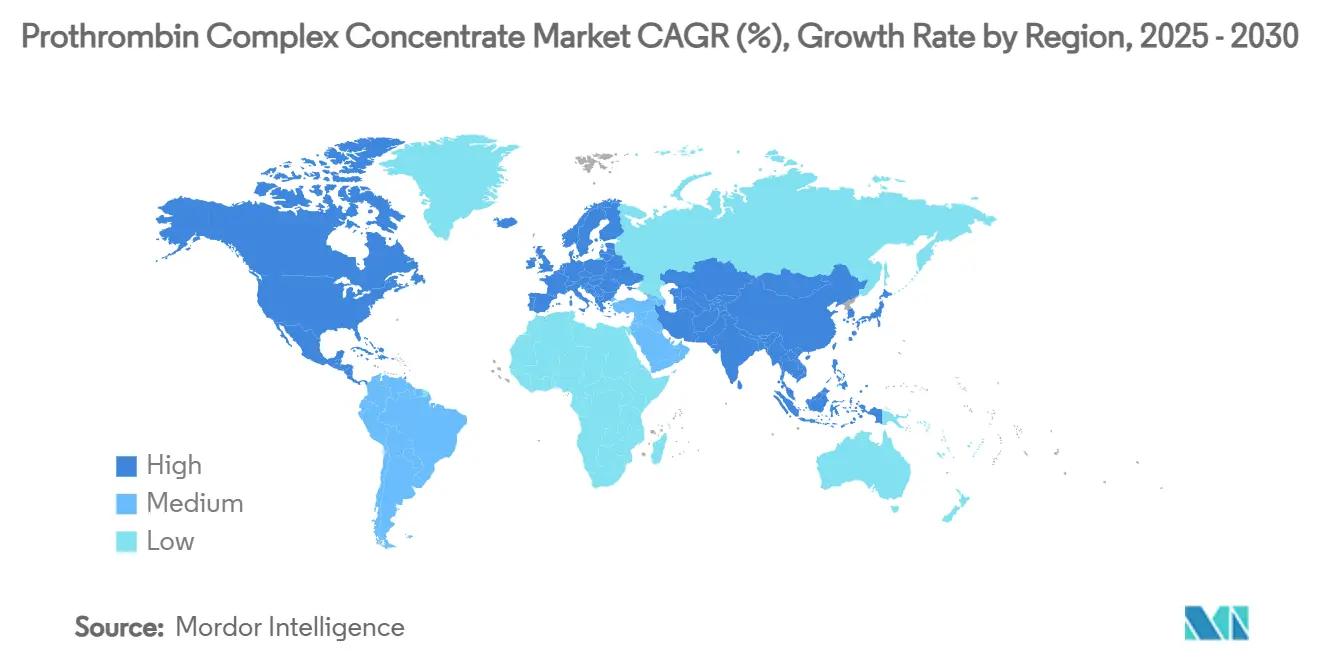

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prothrombin Complex Concentrate Market Analysis by Mordor Intelligence

The prothrombin complex concentrate market size stands at USD 1.11 billion in 2025 and is forecast to reach USD 1.7 billion by 2030, reflecting an 8.8% CAGR over the period. Increasing clinical preference for concentrated coagulation factors over fresh frozen plasma, faster infusion times that ease emergency-department crowding, and guideline revisions that endorse four-factor products are accelerating adoption. Regulatory tailwinds are visible through the 2024 approval of Balfaxar, the second four-factor PCC cleared in the United States, which intensifies competition and broadens prescriber choice. Hospitals are also attracted by lower infusion volumes—roughly one-seventh that of plasma—which help mitigate staff shortages and shorten ICU stays. Trauma-center protocols that prioritize rapid hemostasis further propel usage, while expanding indications such as direct oral anticoagulant (DOAC)-related bleeding unlock new revenue streams. Heightened plasma-fractionation investments in Asia and the Middle East promise longer-term supply security, though near-term capacity often remains tight.

Key Report Takeaways

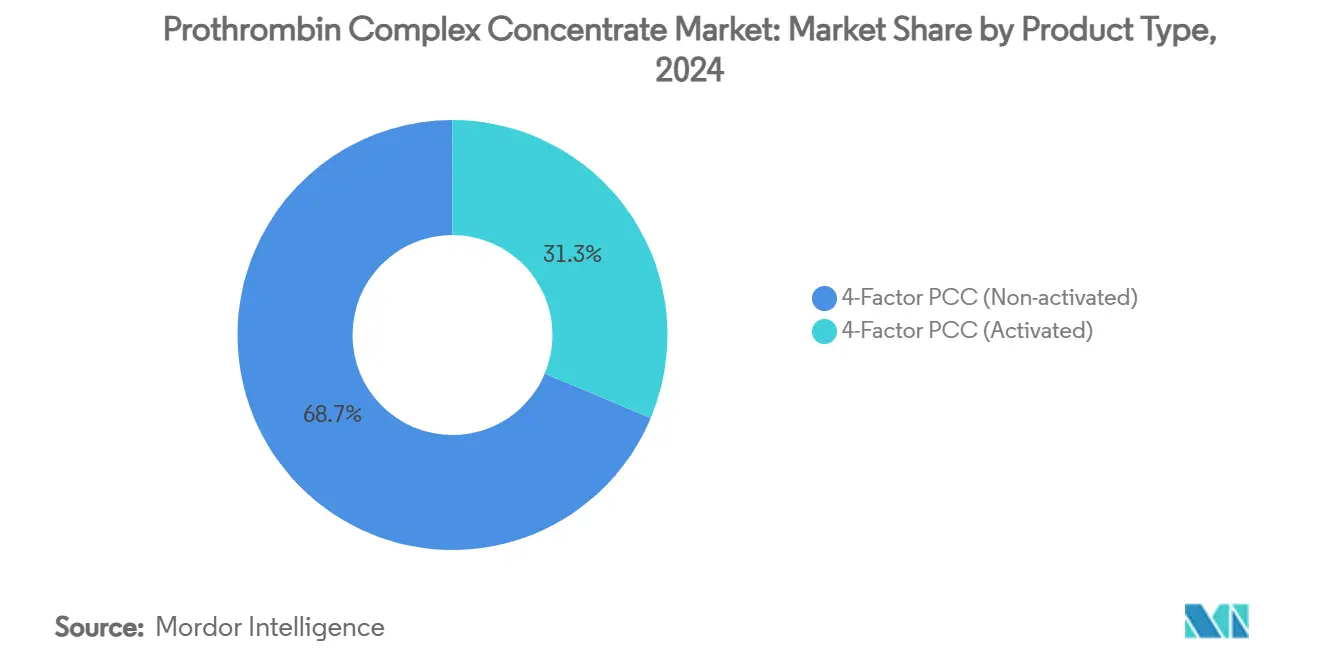

- By product type, four-factor PCC led with 68.7% revenue share in 2024; the activated variant is projected to expand at a 12.4% CAGR through 2030.

- By indication, vitamin K antagonist reversal accounted for 62.3% of demand in 2024; trauma and major bleeding are forecast to grow at 13.1% CAGR to 2030.

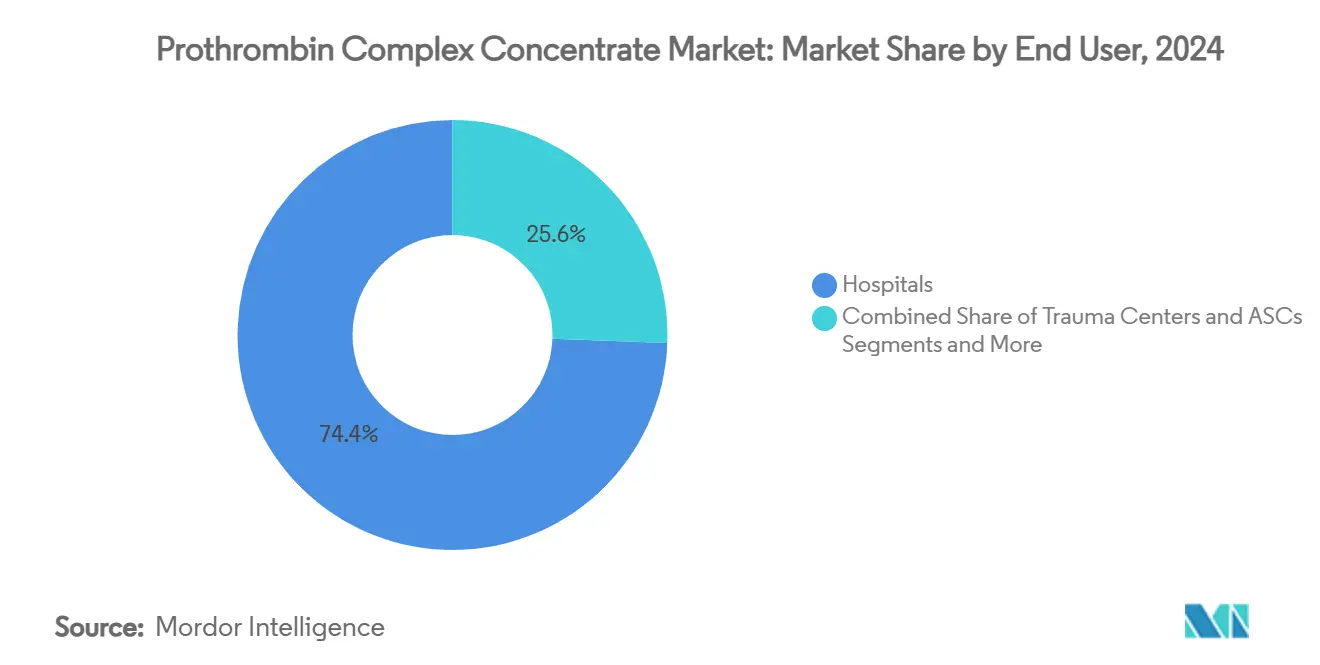

- By end user, hospitals commanded a 74.4% share in 2024; trauma centers are projected to post an 11.8% CAGR through 2030.

- By region, North America retained 40.8% revenue share in 2024; Asia-Pacific is expected to advance at a 10.9% CAGR through 2030.

Global Prothrombin Complex Concentrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift From Fresh Frozen Plasma (FFP) To 4-Factor PCC In High-Income Markets | +2.10% | North America & EU | Medium term (2-4 years) |

| Growing Trauma & Emergency Surgery Caseloads Worldwide | +1.80% | Global, with concentration in urban centers | Long term (≥ 4 years) |

| Expanding Indications Beyond VKA Reversal (E.G., DOAC Bleed Management) | +1.50% | Global | Medium term (2-4 years) |

| Hospital Formulary Preference For Lower Infusion Volume Products | +1.20% | Global | Short term (≤ 2 years) |

| Plasma-Fractionation Capacity Additions In Developing Countries | +0.90% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| AI-Driven Clotting-Factor Dose Calculators Accelerating PCC Adoption | +0.70% | North America & EU initially | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift From Fresh Frozen Plasma to Four-Factor PCC

Four-factor PCC achieves 77.9% hemostatic effectiveness in cardiac surgery versus 60.4% for plasma, giving clinicians a clear outcomes advantage.[1]Danielle Robinson et al., “Updated Recommendations for Warfarin Reversal in the Setting of Four-Factor Prothrombin Complex Concentrate,” Medical Journal of Australia, mja.com.au Infusion can be completed in roughly 15 minutes, compared with more than an hour for plasma, freeing emergency beds and nursing hours. Updated Australian-New Zealand guidelines now position four-factor PCC ahead of three-factor products, citing higher factor VII levels and elimination of plasma thawing delays. Trauma-care consensus statements likewise recommend early PCC administration in damage-control resuscitation, reflecting a circulation-first philosophy that improves survival. Collectively, these clinical and operational gains accelerate uptake in the prothrombin complex concentrate market.

Growing Trauma & Emergency Surgery Caseloads Worldwide

Urbanization, motor-vehicle density, and ageing populations continue to lift trauma volumes, especially in middle-income economies. A nationwide study found that PCC use in trauma hemorrhage cut mortality to 17.5% versus 27.7% with plasma. European registry analysis has yielded pre-hospital algorithms such as phTASH to predict transfusion need, enabling earlier PCC deployment. Machine-learning models now estimate clot strength from serum proteins, guiding precise dosing and reducing waste.[2]Amor A. Menezes, “Model-Based Viscoelastic Clot Strength Predictions,” Nature Communications, nature.comCertification bodies increasingly require advanced coagulation resources for Level I trauma designation, embedding PCC into institutional standards, and growing the prothrombin complex concentrate market further.

Expanding Indications Beyond VKA Reversal

DOAC prescriptions among US Medicare beneficiaries climbed from 7.4% in 2011 to 66.8% in 2019, broadening the pool of patients who may require urgent factor reversal. Although andexanet alfa serves as a specific antidote for factor Xa inhibitors, PCC remains vital when availability or contraindications limit use, with guidelines endorsing its role in life-threatening bleeds. Off-label uptake is also expanding in liver-transplant surgery, where PCC minimizes circulatory overload while ensuring rapid factor correction.[3]Giovanni Punzo et al., “Goal-Directed Use of Prothrombin Complex Concentrates in Liver Transplantation,” Hematology Reports, mdpi.comSuch diversification enhances revenue resilience across the prothrombin complex concentrate market.

Hospital Formulary Preference for Lower Infusion Volume Products

Hospitals under staffing pressure and value-based payment models gravitate toward therapies that shorten infusion time and ICU stay. Economic analyses show total hemostasis costs of USD 7,771 for four-factor PCC compared with USD 5,559 for three-factor products, yet administrators often accept the premium because shorter stays counterbalance acquisition expense. Room-temperature stability and minimal preparation further cut pharmacist workload, reinforcing formulary inclusion. Patient blood-management programs that target transfusion reduction now view PCC as a cornerstone intervention, aligning clinical outcomes with cost-control imperatives and strengthening the prothrombin complex concentrate market trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement Caps Versus High PCC ASPs In Cost-Constrained Health Systems | -1.40% | Global, acute in developing markets | Short term (≤ 2 years) |

| Risk Of Thrombo-Embolic Events Limiting Broader Prophylactic Use | -0.80% | Global | Medium term (2-4 years) |

| Volatile Plasma Collection Volumes Post-Pandemic | -0.60% | North America & EU primarily | Medium term (2-4 years) |

| Emerging Recombinant Bypass Agents As Competitive Substitutes | -0.50% | North America & EU initially, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Caps Versus High PCC Prices

Tight public-budget environments pressure hospitals to justify specialty-drug spending, particularly where average selling prices remain well above plasma alternatives. European policymakers must balance cost with supply security as voluntary-donor models constrain domestic plasma collection, and the region still needs an extra 2 million donors to reduce import dependence. In emerging markets, budget ceilings delay formulary approvals despite clinical superiority, slowing the prothrombin complex concentrate market’s near-term penetration. Although US Medicare offers clotting-factor furnishing fees, these offsets rarely cover full acquisition costs, obliging hospitals to absorb substantial inventory risk.

Risk of Thrombo-Embolic Events Limiting Broader Prophylactic Use

Thrombotic complications occur in 1.4%–8% of PCC recipients, depending on dose and comorbidity profile. FDA reviewers for Balfaxar underscored elevated event rates versus comparators, mandating post-marketing surveillance. Concentrated delivery of factors II, VII, IX, and X can transiently overwhelm natural anticoagulant pathways, deterring prophylactic or repeat dosing. Physicians, therefore, reserve PCC for life-threatening bleeds, limiting volume expansion until safer algorithms and monitoring tools mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Four-Factor Dominance Faces Activated Momentum

Four-factor, non-activated formulations captured 68.7% of the prothrombin complex concentrate market share in 2024, buoyed by broad regulatory clearances and strong clinician familiarity. The same year, these products represented the largest single slice of the prothrombin complex concentrate market size for therapeutic coagulation, reflecting entrenched protocol status in North America and Europe. Activated PCCs, though starting from a smaller base, are forecast to post a 12.4% CAGR through 2030 because their faster factor VIIa activity appeals in complex coagulopathies. Recent clinical work shows no significant efficacy gap between three- and four-factor products for DOAC reversal, suggesting activation status may prove the next competitive differentiator.

Moving forward, plasma-fractionation innovators are testing recombinant blends that could combine the immediacy of activation with lower thrombotic risk, potentially redefining competitive boundaries within the prothrombin complex concentrate industry. Supply-chain enhancements—such as higher-yield caprylate chromatography—may also narrow cost gaps between activated and non-activated variants, enabling wider hospital adoption across the prothrombin complex concentrate market.

By Indication: Warfarin Reversal Leads as Trauma Surges

Warfarin reversal constituted 62.3% of the prothrombin complex concentrate market size in 2024 on the strength of decades-old cardiology and oncology protocols. Nevertheless, trauma-related hemorrhage, boosted by double-digit growth in urban emergency surgeries, is projected to deliver a 13.1% CAGR to 2030. Evidence of mortality reduction compared with plasma has already prompted guideline updates in the United States and Europe. DOAC-related bleeding further widens the candidate pool as clinicians rely on PCC when specific antidotes are unavailable.

Liver-transplant centers and hematology clinics managing rare factor deficiencies also contribute incremental demand, but expansion is tempered by reimbursement scrutiny and thrombosis concerns. As real-world registries accumulate safety data, prescribers may gain confidence to broaden usage, bolstering long-run revenues across the prothrombin complex concentrate market.

By End User: Hospital Control Meets Trauma-Center Expansion

Hospitals held 74.4% of the prothrombin complex concentrate market share in 2024, reflecting centralized purchasing authority and established blood-bank logistics. Within these institutions, stewardship committees increasingly bundle PCC into patient-blood-management pathways to curb allogeneic transfusions. Trauma centers, however, are slated for an 11.8% CAGR, propelled by accreditation standards that require rapid coagulation correction capacity and by emergent “circulation-first” resuscitation doctrines that favor concentrated factors.

Ambulatory surgical centers and specialty clinics represent a smaller slice of the prothrombin complex concentrate industry but are trending upward as minimally invasive procedures grow more complex. Portable point-of-care viscoelastic testing may ease on-site monitoring, allowing outpatient units to adopt PCC safely and adding another layer of demand diversity to the prothrombin complex concentrate market.

Geography Analysis

North America accounted for 40.8% of the prothrombin complex concentrate market size in 2024, supported by widespread trauma-center infrastructure, established reimbursement codes, and early approvals of Kcentra and Balfaxar. Physician familiarity and room-temperature stability have driven adoption even in mid-tier community hospitals, although payer pressure on high-cost biologics moderates volume acceleration. The Medicare clotting-factor furnishing-fee framework eases acquisition burden but does not fully shield providers from budget headwinds, underscoring the need for cost-offset evidence.

Asia-Pacific is the fastest-growing geography, projected at 10.9% CAGR through 2030. Japan’s clinical data demonstrating rapid factor restoration after four-factor PCC infusions have spurred broader regional acceptance. Local regulators are streamlining approval pathways under forums such as the Asia Partnership Conference of Pharmaceutical Associations, reducing time-to-market for imported and domestic products. China’s emerging fractionation infrastructure introduces price-tiering dynamics, with premium imports co-existing alongside cost-effective domestic brands.

Europe forms a mature yet evolving landscape. The European Commission’s proposed SoHO regulation aims to raise plasma-collection self-sufficiency, but the region still needs roughly 2 million more donors to cut reliance on US imports. Guideline updates recommending four-factor PCC over three-factor alternatives confirm clinical consensus, yet hospital budget caps require robust pharmacoeconomic justifications. Supply-chain vulnerabilities tied to voluntary donation models may sustain premium pricing, supporting margins in the prothrombin complex concentrate market despite reimbursement scrutiny.

Competitive Landscape

The prothrombin complex concentrate market is oligopolistic, led by CSL Behring, Grifols, and Octapharma, all of which own vertically integrated networks spanning donor centers to finished-dose packaging. CSL Behring leverages its plasma-collection scale to secure raw-material reliability and has diversified into gene therapy with HEMGENIX, strengthening brand recognition across bleeding-disorder portfolios. Octapharma’s 2025 FDA clearance of Balfaxar enhances US competition and provides hospitals a second four-factor option with 94.6% hemostatic efficacy.

Strategic moves increasingly target manufacturing agility. Thermo Fisher’s acquisition of CSL’s Lengnau site adds 12,000 L of bioreactor capacity and supports next-generation hemophilia products while allowing CSL to re-allocate capital to plasma and gene-therapy franchises. Partnerships with device firms developing AI-driven dosing tools signal a pivot toward integrated care solutions, positioning incumbents to lock in clinical pathways and deepen switching costs.

Competitive threats arise from recombinant bypassing agents like concizumab, which cut bleeding episodes by 86% in inhibitor-positive hemophilia, potentially siphoning niche demand. Nonetheless, complex purification steps, virus-inactivation requirements, and evolving regulatory standards impose formidable entry barriers, helping sustain pricing power for existing plasma-derived PCCs. Continued investment in high-yield fractionation technology and supply-chain digitization should keep leaders ahead in the prothrombin complex concentrate market.

Prothrombin Complex Concentrate Industry Leaders

CSL Behring

Grifols S.A.

Octapharma AG

Takeda Pharmaceutical Company Limited

Kedrion Biopharma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CSL Behring treated the first hemophilia B patient in Austria with HEMGENIX, reporting 94% of recipients remaining prophylaxis-free four years post-therapy.

- March 2025: Thermo Fisher Scientific acquired CSL’s Lengnau biomanufacturing site, adding 12,000 L capacity to its CDMO network.

- February 2025: Octapharma’s Balfaxar won FDA approval for urgent warfarin reversal in adults requiring surgery or invasive procedures.

Global Prothrombin Complex Concentrate Market Report Scope

| 4-Factor PCC (Non-activated) |

| 4-Factor PCC (Activated) |

| VKA (Warfarin) Reversal |

| Hemophilia B & Rare Factor Deficiencies |

| Trauma & Major Bleeding |

| Liver-Disease-Related Coagulopathy |

| Other Off-label Applications |

| Hospitals |

| Trauma Centers |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | 4-Factor PCC (Non-activated) | |

| 4-Factor PCC (Activated) | ||

| By Indication | VKA (Warfarin) Reversal | |

| Hemophilia B & Rare Factor Deficiencies | ||

| Trauma & Major Bleeding | ||

| Liver-Disease-Related Coagulopathy | ||

| Other Off-label Applications | ||

| By End User | Hospitals | |

| Trauma Centers | ||

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the prothrombin complex concentrate market in 2025?

The prothrombin complex concentrate market size is USD 1.11 billion in 2025.

What is the expected growth rate through 2030?

Revenue is projected to rise at an 8.8% CAGR, reaching USD 1.7 billion by 2030.

Which product type currently leads demand?

Four-factor, non-activated PCC holds 68.7% share of 2024 sales.

Why are trauma centers a high-growth end-user segment?

Accreditation standards and circulation-first resuscitation protocols drive an 11.8% CAGR for trauma centers.

Which region is expanding fastest?

Asia-Pacific is forecast to grow at a 10.9% CAGR owing to healthcare modernization and regulatory harmonization.

What safety issue limits wider prophylactic use of PCC?

Thrombo-embolic events, occurring in up to 8% of recipients, necessitate careful dosing and monitoring.

Page last updated on: