Phenylketonuria Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.01 Billion |

| Market Size (2031) | USD 1.66 Billion |

| Growth Rate (2026 - 2031) | 10.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phenylketonuria Treatment Market Analysis by Mordor Intelligence

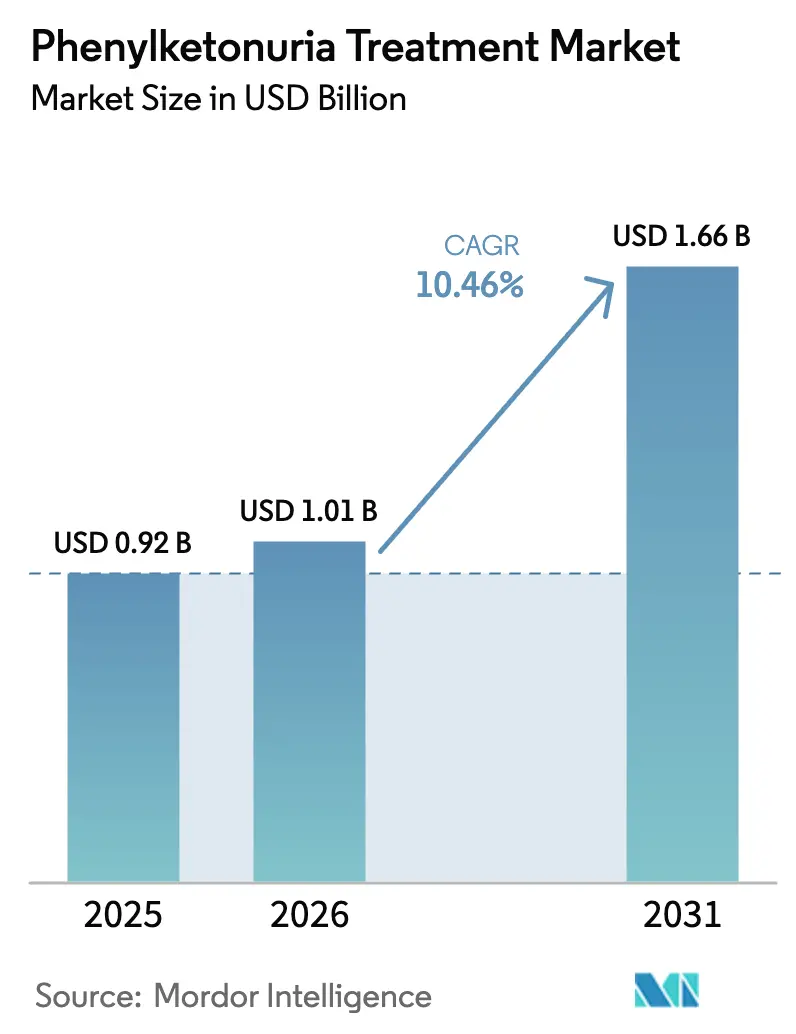

The Phenylketonuria Treatment Market size is expected to grow from USD 0.92 billion in 2025 to USD 1.01 billion in 2026 and is forecast to reach USD 1.66 billion by 2031 at 10.46% CAGR over 2026-2031.

Higher newborn-screening coverage, payer acceptance of enzyme therapies priced above USD 300,000, and expedited orphan-drug reviews anchor this expansion. Injectable pegvaliase continues to dominate early revenue because 75% of treated adults achieve metabolic control and resume normal protein intake, a clinical milestone that diet-only regimens seldom reach. At the same time, the first oral sepiapterin approvals shorten the dose initiation window and improve adherence, especially in pediatric patients. Gene-transfer candidates that promise one-time cures advance through late-phase trials, signaling a future shift from annuity-style drug sales to outcomes-based lump-sum payments. Regional momentum is most pronounced in Asia-Pacific, where universal screening roll-outs in China, South Korea, and Japan expand the diagnosed population and accelerate reimbursement for specialty drugs.

Key Report Takeaways

- By drug type, pegvaliase led with 66.32% of phenylketonuria treatment market share in 2025, while gene-therapy candidates are forecast to post the fastest 11.09% CAGR through 2031.

- By route of administration, parenteral formulations accounted for 54.07% of revenue in 2025; oral therapies are projected to grow at a 13.11% CAGR through 2031.

- By PKU severity, classic PKU accounted for 41.84% of spending in 2025, yet mild PKU is expected to expand at an 11.84% CAGR as BH4 analogs unlock an untreated cohort.

- By end user, hospital pharmacies accounted for 52.24% of turnover in 2025, and online pharmacies are poised to grow at a 13.21% CAGR, driven by mail-order dispensing of oral drugs.

- By geography, North America accounted for 49.11% of revenue in 2025, whereas Asia-Pacific is forecast to register the fastest CAGR of 14.69% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Phenylketonuria Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Newborn-Screening Momentum | +2.1% | Global, with APAC expansion in China, India, South Korea | Medium term (2-4 years) |

| Regulatory Tailwinds for Orphan Drugs | +1.8% | North America & EU, spillover to Japan, Australia | Short term (≤ 2 years) |

| Diet-Liberalizing Enzyme Therapies Gain Adoption | +2.5% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Oral Sepiapterin Approvals Broaden Treatable Genotypes | +1.9% | Global, strongest in North America & EU | Short term (≤ 2 years) |

| Gene-Transfer One-Time Cures Approach Late-Phase Trials | +1.4% | North America & EU, limited near-term APAC access | Long term (≥ 4 years) |

| Silk-Film Oral PAL Technology Removes Cold-Chain Burden | +0.9% | Emerging markets (Latin America, MEA, Southeast Asia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Newborn-Screening Momentum

Universal screening programs in North America, Europe, Japan, and South Korea detect phenylketonuria within 2 days of birth, but China’s 2024 expansion to 31 provincial capitals added 14,000 annual diagnoses previously missed.[1]National Health Commission of China, “Policy Expansion Circular 2024,” nhc.gov.cn India’s 2025 pilots in three large states screened 1.2 million babies and identified a prevalence of 1 in 18,000, underscoring the unmet demand for affordable medical foods and future access to enzymes. Early detection lessens cognitive-impairment risk yet exposes wide treatment inequities: high-income markets migrate to enzyme and gene platforms, whereas low-income regions struggle to finance even phenylalanine-free formula. Prevention-driven payback models increasingly influence payer calculus, because averting disability yields lifetime productivity gains that offset screening costs.

Regulatory Tailwinds for Orphan Drugs

The FDA’s March 2024 breakthrough-therapy tag for sepiapterin compressed review to six months, enabling a July 2025 market debut in the United States.[2]U.S. Food and Drug Administration, “Orphan Drug Approvals 2025,” fda.gov Orphan exclusivity through 2032 blocks generic entry, letting sponsors command premium pricing while mandating quarterly real-world phenylalanine reporting. The EMA waived parts of pegvaliase’s pediatric program in July 2024, accelerating an adolescent label expected in early 2026. Faster pathways reduce clinical cost but heighten post-approval risk, because payers can claw back revenue if real-world metabolic control lags trial endpoints. Japan mirrored these incentives in 2025, giving rare-disease developers a harmonized tripolar market.

Diet-Liberalizing Enzyme Therapies Gain Adoption

At 36 months, 75% of pegvaliase-treated adults kept phenylalanine below 600 µmol/L and 68% resumed unrestricted protein intake, a lifestyle upgrade that payers equate with productivity and mental-health gains.[3]BioMarin Pharmaceutical, “Investor Presentation Q4 2025,” biomarin.com Sepiapterin’s 97% response in the APHENITY trial doubles sapropterin’s historical efficacy because it replenishes tetrahydrobiopterin more efficiently. Uptake is migrating from salvage therapy for non-adherent adults to first-line use in newly diagnosed adolescents whose families prize normal eating. Caution remains over long-term cardiovascular and bone-health data, but demand momentum suggests diet-liberating drugs have crossed the payer-value threshold.

Oral Sepiapterin Approvals Broaden Treatable Genotypes

Sepiapterin’s distinct biochemical pathway targets patients with dihydropteridine reductase or GTP cyclohydrolase I mutations about 2% of the global cohort previously considered untreatable with enzyme replacement. The July 2025 FDA label covers patients as young as two, positioning sepiapterin as a child-friendly alternative to injections. Oral delivery reduces the risk of hypersensitivity and training burdens, boosting six-month persistence rates. In rural areas of the United States and Latin America, where infusion capacity is limited, convenience is driving faster conversion from diet-only care to pharmacologic therapy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Specialty-Drug Pricing Pressure & Payer Step Edits | -1.6% | North America & Western Europe | Short term (≤ 2 years) |

| Adult Adherence Drop-Off to Rigid Dietary Regimens | -0.9% | Global, most acute in North America & EU | Medium term (2-4 years) |

| Cold-Chain Logistics for Injectable Biologics in LMICs | -0.7% | Latin America, MEA, Southeast Asia | Medium term (2-4 years) |

| Low BH4-Response Rates in High-Consanguinity Regions | -0.5% | Middle East, North Africa, South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Specialty-Drug Pricing Pressure & Payer Step Edits

92% of U.S. pegvaliase claims required diet-failure documentation in 2025, generating a 4.3-month approval lag and 18% abandonment before the first dose. Germany’s G-BA judged pegvaliase a “minor additional benefit,” capping reimbursement at EUR 180,000 (USD 195,000) and requiring a 38% discount compared with the United States. Similar scrutiny in France and the United Kingdom sets a continental benchmark that lowers net revenue per patient and increases dependence on outcomes-based rebates.

Adult Adherence Drop-Off to Rigid Dietary Regimens

Only 48% of European adults aged 25-40 maintained safe phenylalanine levels in 2024, compared with 81% of children, as self-managed diets prove difficult without parental supervision. Enzyme therapy could close this gap, yet payer-mandated dietary failure delays access until irreversible cognitive damage emerges. A policy shift that waives step edits for documented non-adherence would accelerate conversion, but budget-impact fears stall reform.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Enzyme Dominance Faces Gene-Therapy Upswing

Pegvaliase secured 66.32% of phenylketonuria treatment market revenue in 2025 and underpins the largest single-product franchise in the space. However, gene-therapy candidates have the prospective 11.09% CAGR between 2026 and 2031, signaling an eventual reshuffle once one-time cures clear regulatory hurdles. Small-molecule and synthetic-biotic programs remain experimental and risk culling if Phase 2 data fail to demonstrate durable phenylalanine reduction.

Sapropterin generics, now price-eroded, stay relevant in health systems that favor step-therapy ladders, but sepiapterin’s higher response rates and oral convenience will cannibalize this legacy niche. A biosimilar pegvaliase expected in Europe by 2028 could compress branded margins and force incumbents to compete on patient support services rather than price.

By Route of Administration: Oral Convenience Accelerates Share Capture

Parenteral formats retained 54.07% of 2025 turnover on the back of pegvaliase, yet oral therapies are on track for a 13.11% CAGR through 2031 as families gravitate toward pills over injections. The phenylketonuria treatment market share for oral drugs should exceed 45% by 2031 once sepiapterin approaches peak uptake and silk-film PAL secures at-scale manufacturing. Ambient-stable formats matter most in tropical regions and among highly mobile adult patients who face burdensome refrigeration requirements.

Even so, injectable supremacy persists in classic PKU cases that require higher enzyme activity than current oral bioavailability allows. Future market equilibrium will likely stratify: oral drugs for mild-to-moderate genotypes, injectables for severe phenotypes, and gene infusions for those eligible and antibody-negative.

By PKU Severity: Mild Cases Propel Volume Growth

Classic PKU generated 41.84% revenue in 2025, driven by average annual patient spending exceeding USD 300,000. Yet mild PKU’s projected 11.84% CAGR means that incremental volume originates from genotypes newly eligible for oral BH4 therapy.

Variant and hyperphenylalaninemia cases mostly consume medical foods today, but gradual price declines and digital adherence monitoring could make low-dose oral enzymes economically viable, opening a fresh micro-segment by the decade’s end.

By End User: Online Pharmacies Scale With Chronic Care

Hospital pharmacies captured 52.24% of revenue under REMS obligations for pegvaliase in 2025, but as oral uptake rises, online channels will clock a 13.21% CAGR through 2031. Digital fulfillment slashes USD 200-300 per dose in handling fees and supports refill-reminder platforms that improve persistence. Retail outlets remain relevant in countries with strict e-pharmacy rules, yet policy liberalization trends favor mail-order expansion, especially for chronic, rare-disease populations.

Geography Analysis

North America accounted for 49.11% of global turnover in 2025, yet growth moderates as payers step in to cap therapy initiation, and patient penetration sits near 7% of the diagnosed population. The upcoming FDA adolescent approval for pegvaliase could add 1,500 U.S. patients, but widespread budget scrutiny tempers upside. Canada’s single-payer model negotiates lower net pricing, further restraining revenue growth.

Europe ranks second in revenue but is highly price-sensitive; Germany’s EUR 180,000 cap and France’s similar ceiling anchor EU-wide negotiations. Registration-based patient tracking shows adult metabolic control well below guideline targets, a clinical unmet need that enzyme therapies can fix if payers relax step edits.

Asia-Pacific is forecast to grow at a 14.69% CAGR as China scales universal screening and Japan leverages its 2025 orphan-drug pathway to reimburse pegvaliase. India’s pilots hint at untapped prevalence but lack national funding for specialty drugs. Australia and South Korea mirror Western Europe in both coverage and willingness to reimburse high-cost therapies, making them early adopters of gene infusions later in the decade.

Middle East & Africa and South America remain underpenetrated due to low screening rates and cold-chain gaps. Brazil’s inclusion of PKU in its 2024 neonatal panel creates latent demand for medical foods but leaves enzyme access to private insurers. Ambient-stable oral enzymes could leapfrog injectables in these regions once late-stage data read out.

Regulatory Landscape

PKU therapies are shaped by orphan-drug frameworks and specialty-biologic risk controls, with regulatory actions between 2024 and 2026 expanding access across age groups and regions. In the United States, the FDA approved Sephience (sepiapterin) in July 2025 for hyperphenylalaninemia in adult and pediatric patients 1 month of age and older with sepiapterin-responsive PKU. BioMarin also received an FDA label expansion for PALYNZIQ (pegvaliase-pqpz) in February 2026 to include pediatric patients aged 12 years and older. These approvals operate alongside controls such as PALYNZIQ REMS distribution and physician-supervised initiation for higher-risk biologics.

In Europe, the European Commission granted marketing authorization for Sephience in June 2025 for adult and pediatric patients with PKU, under post-authorization pharmacovigilance requirements that include Periodic Safety Update Reports (with an initial submission timeline triggered shortly after authorization). EMA process also supports lifecycle label updates, including the CHMP positive opinion in May 2026 for extending Palynziq to patients 12 years of age and older. For pipeline entrants, Otsuka initiated a global Phase 3 trial for repinatrabit (JNT-517) in December 2025, supported by U.S. FDA orphan drug and rare pediatric disease designations, reinforcing how expedited rare-disease programs influence development and access strategy.

Competitive Landscape

The phenylketonuria treatment market shows moderate concentration: BioMarin and PTC Therapeutics jointly command significant prescription revenue through pegvaliase and sepiapterin. High capital requirements, orphan-drug exclusivities, and REMS distribution deter smaller entrants. Homology Medicines and Synlogic withdrew programs following unfavorable data, narrowing their late-stage pipelines.

Forthcoming biosimilar pegvaliase in Europe (2028) and Asia-Pacific (2029) will compress margins and push incumbents toward service-oriented differentiation, such as adherence apps, home nursing, and outcomes-based contracts. The technology race now tilts toward delivery innovations such as silk-film PAL and nanoparticle-encapsulated long-acting enzymes. Cost, convenience, and supply-chain resilience, rather than incremental efficacy, are set to define competitive advantage.

Phenylketonuria Treatment Industry Leaders

Vitaflo International (Nestlé Health Science)

Nutricia Advanced Medical Nutrition

APR Applied Pharma Research (PKU GOLIKE)

Orpharma Pty Ltd

BioMarin Pharmaceutical Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Pediatric and adolescent expansion is a defined whitespace where regulators and sponsors have shifted from adult-only positioning toward earlier intervention. The FDA approval in February 2026 expanding PALYNZIQ (pegvaliase-pqpz) to patients aged 12 years and older, alongside the EMA CHMP positive opinion in May 2026 for a similar age extension, increases the addressable treated cohort and pushes demand toward specialized metabolic centers that can support monitoring and risk-management workflows. At the same time, Sephience (sepiapterin) approvals in the United States (July 2025) and European Union (June 2025) add an on-label oral option across broad pediatric age ranges, improving conversion potential from diet-only management where injection training, hypersensitivity concerns, and infusion-site capacity limit adoption.

The pipeline also points to modality-specific opportunities that can change competitive dynamics beyond current enzyme and BH4-alternative paradigms. Otsuka starting a global Phase 3 program for repinatrabit (JNT-517) in December 2025 indicates that sponsors are funding late-stage, multinational development for oral candidates. Agios initiating a Phase 1 trial for AG-181 (noted as ongoing in 2026) further reflects continued entry of differentiated small-molecule approaches. Separately, published 2026 preclinical work showing in vivo adenine base editing with lipid nanoparticles to correct a PAH variant in PKU mouse models highlights ongoing innovation that could later shift reimbursement discussions toward outcomes-linked payments, especially in markets already requiring real-world metabolic control reporting for premium orphan-drug pricing.

Recent Industry Developments

- February 2026: BioMarin announced that the U.S. FDA approved the supplemental Biologics License Application for PALYNZIQ (pegvaliase-pqpz) to treat pediatric patients aged 12 years and older with PKU. The expanded label moves enzyme therapy earlier in the treatment pathway and can increase utilization in hospital-based specialty channels that support REMS distribution and monitoring.

- October 2025: BioMarin reported that the U.S. FDA accepted for priority review its sBLA to expand PALYNZIQ use to adolescents aged 12-17, setting an action date in late February 2026. The priority review designation reinforced the near-term regulatory catalyst for earlier-age penetration and supported planning for broader patient support and payer engagement.

- April 2025: Vitaflo (Nestle Health Science) disclosed a multi-million-euro expansion project at its Rosbach vor der Hoehe, Germany, site to modernize manufacturing for specialist infant formula and protein substitutes used in metabolic disorders including PKU. The investment targets capacity and operational resilience for medical nutrition supply, a key complement to drug therapy as diagnosed populations rise with expanding newborn screening.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers spending on managing phenylketonuria (PKU) in diagnosed patients through approved drug therapy and PKU-specific nutritional products that are used to control phenylalanine levels and related symptoms.

Scope exclusions: It excludes general low-protein groceries not formulated for PKU, phenylalanine monitoring devices, and pre-approval pipeline gene-editing trials.

Segmentation Overview

- By Drug Type

- Sapropterin & Analogues

- Pegvaliase

- Gene Therapy Candidates

- Synthetic Biotics & Small-Molecule Transport Inhibitors

- Other Drug Type

- By Route of Administration

- Oral

- Parenteral / Injectable

- By PKU Severity

- Classic PKU

- Moderate / Variant PKU

- Mild PKU

- Hyperphenylalaninemia

- By End User

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We first set the disease and treatment context using public health and clinical references, since PKU is closely tied to newborn screening and diet management. Sources such as the US CDC, the NIH Genetic and Rare Diseases Information Center, and the National Library of Medicine are used to confirm diagnosis pathways, treated-patient logic, and how therapy routines are described over time.

For market shaping, we also review regulator and policy signals and real-world care standards, including US FDA drug labels, the European Commission and EMA public assessment reports, and payer or health system publications where available. These desk inputs are then supported by company filings, investor presentations, and reputable press for launch timing, geography coverage, and pricing narratives. Where needed, we apply selective checks from paid subscriptions for company financials and patent activity. The desk sources listed here are not exhaustive, and we used additional public references for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

To validate what is actually used in practice, we conduct expert interviews and structured surveys with clinicians managing metabolic disorders, dietitians working in PKU clinics, payers, and distributors that handle rare-disease therapies. Respondent input is collected across APAC, EMEA, and the Americas, and then used to pressure-test the link between prevalence and treated patients, therapy switching patterns, and the typical split between drugs and PKU-specific nutritional products.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 16% | APAC: 42% |

| Mid tier: 46% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 19% | Managers: 53% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs demand from the diagnosed and treated PKU pool, then links it to typical therapy patterns by age group and disease severity across major geographies. To keep totals realistic, we corroborate with selective bottom-up approximations, including sampled price points for key therapies and nutrition formulas, and a reasonableness check on supplier presence by region.

In the model, a few inputs carry most of the weight, including newborn screening coverage and diagnosis rates, the estimated share of patients on drug therapy versus diet-based management, therapy persistence and discontinuation, average annual cost by therapy type (including patient support effects where they change net pricing), and region-level access factors such as reimbursement breadth. Forecasting uses scenario analysis backed by expert consensus for adoption curves, since inflection points often track guideline updates, label expansions, and access decisions rather than smooth linear growth. When bottom-up signals are incomplete for smaller countries, we use proxy adoption rates anchored to comparable health system maturity, followed by an expert recheck before finalizing.

Data Validation & Update Cycle

Before publishing, outputs are tested against independent signals, including therapy approval timelines, public pricing references, and whether the treated-patient counts implied by the model look feasible for rare-disease care infrastructure. Variances are flagged, investigated, and corrected through step-by-step analyst reviews, and we re-contact contributors when a key assumption moves outside an agreed range.

The report is refreshed annually, and interim updates are triggered when material events occur, such as major reimbursement changes or meaningful product approvals. Right before delivery, a final review pass is performed so clients receive the latest updated view, with figures that still tie back to clear inputs and documented checks.

Mordor Intelligence's Phenylketonuria Treatment Market Estimate Compared With Other Published Estimates

Published PKU treatment market values can look far apart even when the topic is described similarly, because each publisher chooses its own coverage for therapies, nutrition products, and what counts as treatment-related spend. Differences in base years and currency timing, and how adoption is ramped in forecasts, also change totals, particularly in a rare-disease market where access can shift quickly.

Some estimates add broader lifestyle and monitoring add-ons, while others also treat pre-approval gene therapy research as part of the commercial market. In the split used by Mordor Intelligence, only regulator-approved prescription therapies and PKU-specific medical products are counted, and general low-protein staples and phenylalanine monitoring devices are kept out of scope to avoid inflating treatment spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.01 B (2026) | |

| Global Consultancy A | USD 0.52 B (2024) | Uses an earlier base year and is presented mainly as a drug-focused split, with limited clarity on whether PKU-specific nutritional formulas are included, which can pull down the total versus a broader treatment basket. |

| Industry Publisher B | USD 1.10 B (2025) | Appears to include adjacent components such as dietary management solutions and treatment-support tools, and it references gene therapy research in scope, which can raise the market value even if near-term commercialization is not consistent across regions. |

The spread across the table is mainly driven by what each publisher counts as treatment spend and how fast adoption is assumed to rise after access improves. By keeping the demand pool tied to diagnosed and treated patients, and by separating approved treatment items from broader support categories, our approach is easier to audit and replicate across years.

Key Questions Answered in the Report

What is the current value of the phenylketonuria treatment market?

It stands at USD 1.01 billion in 2026 and is projected to reach USD 1.66 billion by 2031.

Which therapy currently generates the largest revenue?

Pegvaliase, with 66.32% phenylketonuria treatment market share in 2025.

How fast will gene therapies grow?

Gene-transfer candidates are forecast to post an 11.09% CAGR between 2026 and 2031.

Why is Asia-Pacific the fastest-growing region?

Universal newborn screening in China, Japan’s orphan-drug policy, and rising per-capita income drive a 14.69% CAGR through 2031.

What limits immediate enzyme-therapy uptake?

Payer step edits that require dietary failure documentation and stringent REMS protocols for injectable biologics.

Page last updated on: