Urethral Stricture Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

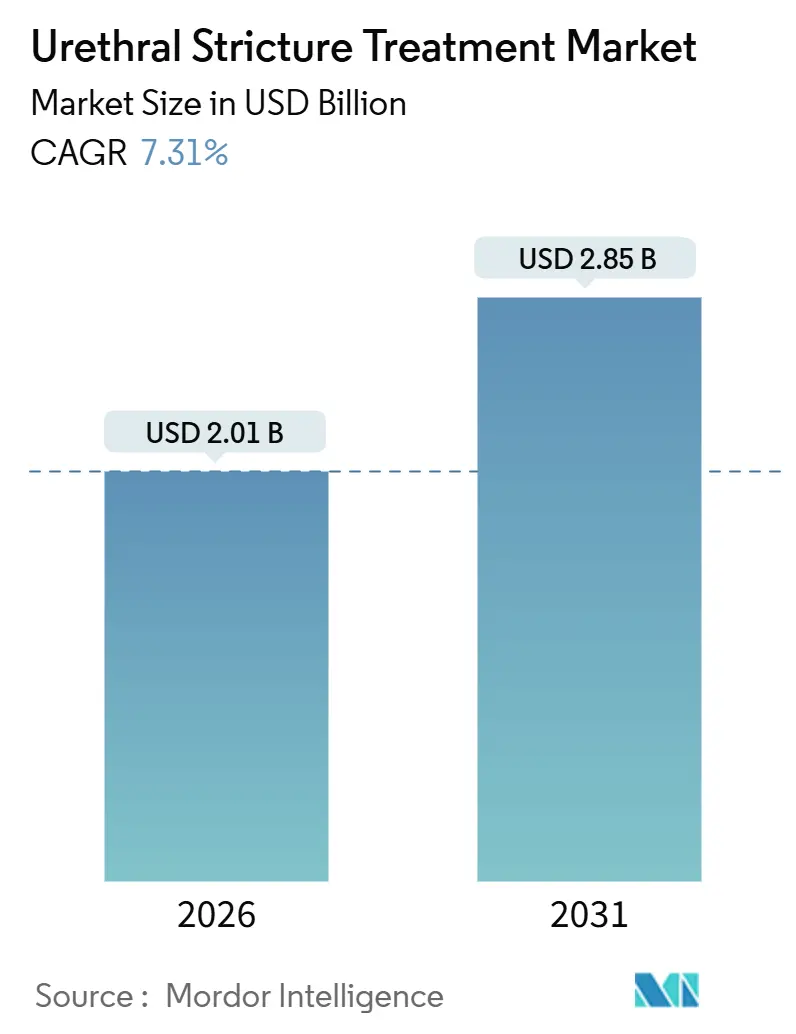

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.85 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urethral Stricture Treatment Market Analysis by Mordor Intelligence

The Urethral Stricture Treatment Market size is estimated at USD 2.01 billion in 2026, and is expected to reach USD 2.85 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031).

Uptake accelerates as revised American Urological Association and European Association of Urology guidelines now conditionally recommend urethroplasty as the first-line option for recurrent disease, moving clinical practice away from serial dilations. Population aging reinforces procedure growth; men aged 65 and older already account for stricture rates exceeding 900 per 100,000, and this cohort is set to reach 16% of the world’s population by 2050.[1]World Health Organization, “Ageing and Health,” WHO, who.int Increased catheter and endoscopy volumes add iatrogenic cases, while single-use digital cystoscopes reduce reprocessing barriers and expand ambulatory surgical center (ASC) capacity. Drug-coated balloons such as Optilume, which showed 71.9% freedom from re-intervention at three years, illustrate how minimally invasive devices can delay recurrence and open new outpatient revenue streams.

Key Report Takeaways

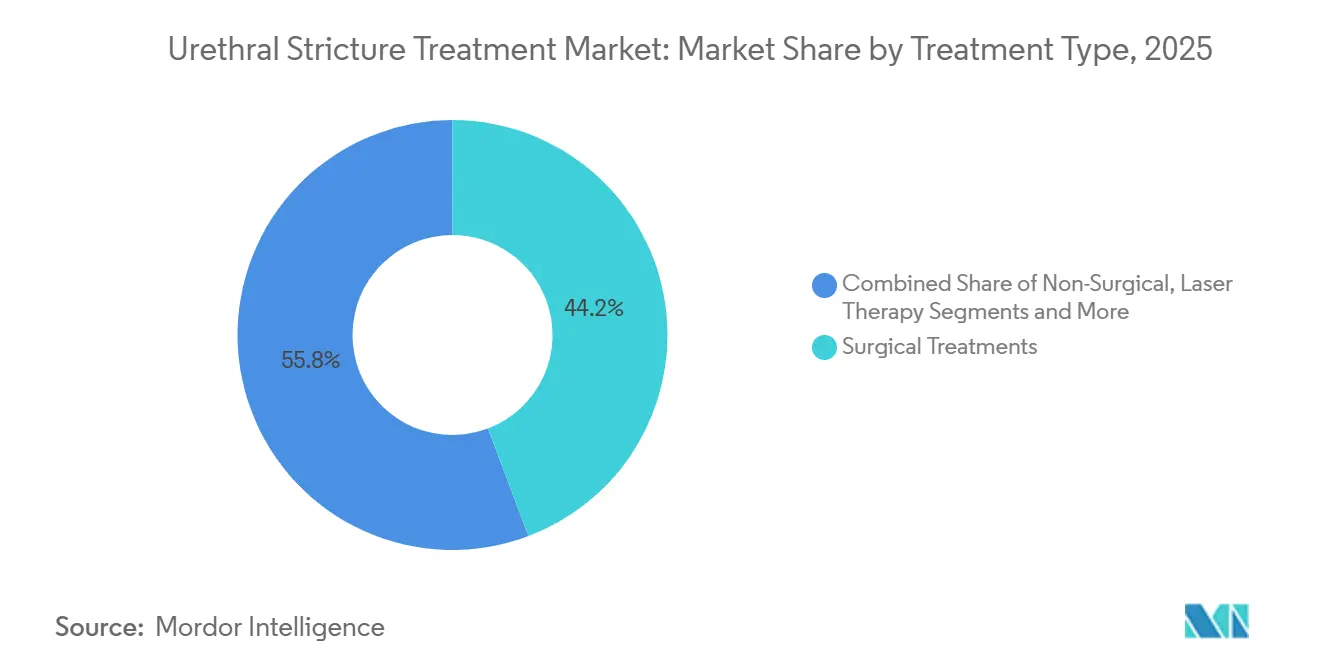

- By treatment type, surgical procedures led with a 44.24% urethral stricture treatment market share in 2025, whereas endoscopic options are advancing at a 9.72% CAGR to 2031.

- By product type, urethral dilators captured 34.53% of the urethral stricture treatment market size in 2025, while drug-coated balloons post the highest 10.44% CAGR through 2031.

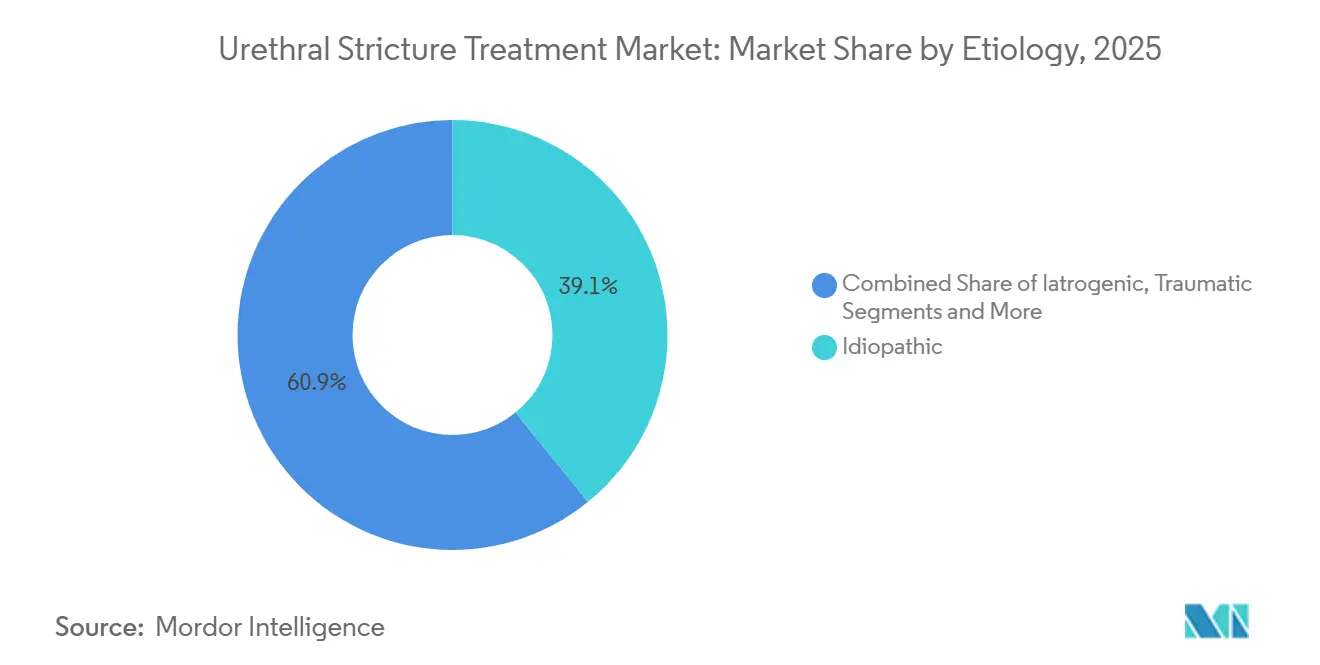

- By etiology, idiopathic cases held 39.14% of 2025 volume, yet iatrogenic strictures represent the fastest-growing category at a 9.25% CAGR.

- By patient type, male patients accounted for 88.22% share in 2025; transgender individuals are expanding at an 11.56% CAGR on the back of higher stricture rates after gender-affirming surgery.

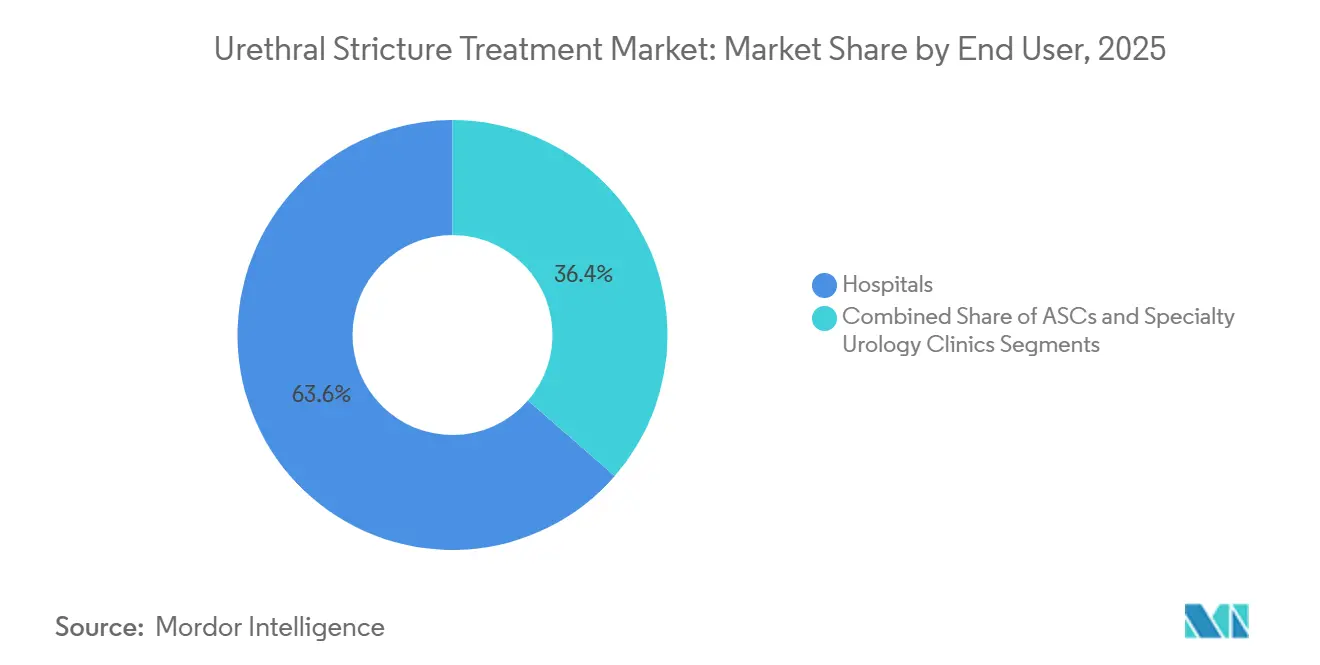

- By end user, hospitals retained 63.62% share in 2025, but ASCs are expanding at a 9.31% CAGR as reimbursement widens.

- By geography, North America dominated with 32.68% revenue share in 2025, while Asia-Pacific records the highest 9.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Urethral Stricture Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence among ageing male population & iatrogenic injuries | +1.2% | Global, with focus on North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Guideline shifts favoring definitive urethroplasty | +0.9% | North America, Europe, urban APAC and Latin America | Medium term (2–4 years) |

| Technological advances in minimally invasive devices | +1.1% | Global; early adoption in North America, Europe, GCC, urban China | Medium term (2–4 years) |

| Reimbursement expansion for outpatient endoscopic procedures | +0.8% | India, China, Brazil, Mexico, GCC | Long term (≥ 4 years) |

| Rapid adoption of digital single-use endoscopes | +0.7% | North America ASCs, Western Europe outpatient clinics, select GCC sites | Short term (≤ 2 years) |

| Integration of AI-assisted imaging | +0.5% | North America academic centers, Europe research hospitals, pilot APAC programs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Among Ageing Male Population & Iatrogenic Injuries

Urethral stricture incidence jumps from 229–627 per 100,000 men overall to more than 900 per 100,000 in those older than 65.[2]Ajay B. Kulkarni, “Urethral Stricture: Epidemiology and Natural History,” Journal of Urology, ncbi.nlm.nih.gov With the population aged 65+ set to reach 16% globally by 2050, demand will remain resilient even in countries with flat birth rates. Iatrogenic damage from prolonged catheterization or endoscopic instrumentation affects 0.3%–2.4% of patients, and absolute case numbers rise as hospitals scale minimally invasive cardiac and critical-care procedures.[3]Michael T. Czerny, “Iatrogenic Urethral Injuries: Etiology and Management,” Urology Annals, ncbi.nlm.nih.gov Lichen sclerosus complicates this picture, causing urethral involvement in up to 40% of affected males and adding chronic inflammatory pressure. Together, demographic and procedural drivers underpin steady growth for the urethral stricture treatment market.

Guideline Shifts Favoring Definitive Urethroplasty

The 2024 American Urological Association guideline and the 2025 European Association of Urology update both recommend urethroplasty after a single failed endoscopic attempt, citing 85%–95% five-year success versus 20%–40% for repeated dilations. CMS followed with a 2025 rule that reimburses outpatient urethroplasty in ASCs, lowering costs and widening access. Hospitals are therefore investing in graft-harvesting tools and robotic systems, while urologists pursue reconstructive fellowships to capture the higher-value procedures.

Technological Advances in Minimally Invasive Devices

Paclitaxel-coated drug-balloon platforms such as Optilume deliver localized antiproliferative therapy and extend patency to 71.9% at three years, well above historical balloon performance. Ambu’s single-use cystoscopes remove capital and reprocessing bottlenecks for outpatient sites and drop per-case costs to USD 200–300. Robotic assistance improves anastomotic precision in complex urethroplasty, and AI algorithms now segment imaging studies with 92% accuracy to aid surgical planning.

Reimbursement Expansion for Outpatient Endoscopic Procedures

India’s Ayushman Bharat program insures 500 million residents and covers endoscopic stricture therapy in empaneled centers. China’s universal coverage, achieved in 2025, adds urology to provincial formularies as part of Healthy China 2030. Brazil and Saudi Arabia likewise channel public funds into ASC infrastructure, shrinking wait lists and accelerating device uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device costs & uneven reimbursement in LMICs | −0.6% | Sub-Saharan Africa, South Asia (ex-India), much of Latin America | Long term (≥ 4 years) |

| Recurrence risk causing repeat interventions & patient dissatisfaction | −0.5% | Markets dependent on repeated dilations | Medium term (2–4 years) |

| Shortage of fellowship-trained reconstructive urologists | −0.4% | Rural North America, Eastern Europe, sub-Saharan Africa, rural APAC | Long term (≥ 4 years) |

| Regulatory concerns over paclitaxel exposure | −0.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device Costs & Uneven Reimbursement in LMICs

List prices for premium balloons exceed USD 4,000 in many African markets—four times the U.S. price—because of tariffs and distributor mark-ups, while annual per-capita health spend sits below USD 150. Public insurance rarely pays more than USD 200 per case, forcing hospitals to use basic dilators with poorer coatings. The cost gap limits adoption of curative technologies and suppresses the urethral stricture treatment market in low-resource settings.

Recurrence Risk Causing Repeat Interventions & Patient Dissatisfaction

Endoscopic dilation shows only 30%–40% durable patency beyond 24 months, and 35% of patients regret deferring surgery after multiple failed attempts. High-frequency re-intervention erodes payer confidence and encourages watchful waiting or permanent suprapubic catheterization, stalling volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Endoscopic Options Accelerate Outpatient Care

Endoscopic and minimally invasive modalities are expanding at a 9.72% CAGR, outpacing surgical approaches despite the latter’s 44.24% share in 2025. This shift reflects growing acceptance of drug-coated balloons as an intermediate option between dilation and urethroplasty, coupled with single-use cystoscope economics that favor ASCs. Laser incision, while still niche, attracts centers with existing holmium or thulium platforms and could widen access as capital costs fall.

Surgical urethroplasty remains the gold standard for long or recurrent strictures, achieving 85%–95% success at five years but requiring specialty training and longer operating times. Robotic assistance improves posterior repairs yet carries a USD 1.5–2.5 million capital hurdle. As guidelines push earlier surgery after failed endoscopy, the urethral stricture treatment market size for surgical devices should rise steadily in tertiary centers.

By Product Type: Drug-Coated Balloons Challenge Dilator Dominance

Urethral dilators held 34.53% of the urethral stricture treatment market size in 2025, but drug-coated balloons deliver the fastest 10.44% CAGR as clinicians seek longer patency without full reconstruction. Stents are now largely palliative because of migration and encrustation concerns, while silicone catheters reduce trauma during self-dilation.

Single-use digital imaging systems underpin growth by reducing infection risk and sterilization labor. AI add-ons that map strictures in real time could further enlarge the urethral stricture treatment market if vendors prove interoperability with mainstream PACS solutions.

By Etiology: Iatrogenic Strictures Rising Fast

Idiopathic strictures controlled 39.14% volume in 2025, yet iatrogenic cases post catheterization or endoscopy are growing at 9.25% CAGR as instrumentation surges worldwide. Traumatic and lichen sclerosus-related disease remains clinically challenging given higher recurrence rates despite urethroplasty.

Lichen sclerosus biopsy is now advised for all anterior strictures in Europe, driving earlier diagnosis and specialist referral. These protocols could expand the urethral stricture treatment market share for pathology and imaging services as well.

By Patient Type: Transgender Segment Shows Double-Digit Growth

Male cases account for 88.22% of procedures, but neourethral strictures after phalloplasty push the transgender segment to an 11.56% CAGR. Female strictures remain rare but require unique flap-based repairs.

Insurance gaps and limited surgical expertise still bottleneck transgender access, suggesting untapped urethral stricture treatment market potential for centers of excellence that combine urology and gender-affirmation teams.

By End User: ASCs Capture Outpatient Momentum

Hospitals retained 63.62% of 2025 revenue, anchored by complex reconstructions. Yet ASCs expand at 9.31% CAGR after CMS raised ASC payments 3.1% and added outpatient urethroplasty codes. Specialty clinics leverage single-use scopes to offer same-day diagnostics at lower cost, capturing surveillance and dilation volumes.

Hospital systems still dominate urethral stricture treatment market share for multistage grafting and high-risk patients, reinforcing their role as referral hubs while outpatient sites handle routine endoscopy.

Geography Analysis

North America generated 32.68% of global revenue in 2025, propelled by favorable reimbursement, 12 reconstructive fellowships, and rapid adoption of drug-coated balloons. Workforce shortages in rural counties keep serial dilation volumes high, but ASC penetration widens access in suburban markets. Canada and Mexico trail the U.S. in procedure counts, though Mexico’s medical-tourism corridors attract price-sensitive U.S. patients.

Asia-Pacific is the fastest-growing region at a 9.74% CAGR. China’s 95% universal coverage and USD 850 billion Healthy China 2030 investment boost device uptake, while India’s Ayushman Bharat plan opens endoscopic reimbursement for 500 million citizens. Japan’s super-aged profile heightens demand, though reimbursement caps still limit premium device use in parts of Southeast Asia.

Europe, combining strong public health financing with early technology adoption. Germany, France, and the U.K. lead in per-capita spend, whereas Eastern Europe relies on cross-border referrals to urban centers. Middle East growth is bifurcated—GCC states invest heavily under Vision 2030, but many African nations face acute urologist shortages. South America narrows wait times through ASC roll-outs in Brazil, though remote regions remain underserved.

Competitive Landscape

Boston Scientific, Cook Medical, and Coloplast anchor a moderately concentrated landscape by bundling dilators, stents, catheters, and imaging systems into long-standing hospital contracts. They protect share through clinician training, evidence generation, and vertical integration. Urotronic broke in with Optilume, achieving three-year data that drove inclusion in practice guidelines and boosted formulary acceptance.

Ambu attacks reusable incumbents with the aScope 5 Cysto, cutting capital outlay for ASCs and enabling urethral stricture treatment market expansion in low-volume sites. Intuitive Surgical adapts its robotic platforms to complex reconstructions, leveraging existing urologic oncology installs to penetrate a new indication. Patent filings rose 22% between 2024 and 2025, mainly in drug-delivery coatings and single-use optic design.

Regulatory scrutiny of paclitaxel residuals slows drug-balloon rollout, creating white-space for sirolimus-based alternatives. Emerging start-ups explore bioabsorbable stents and AI-guided imaging overlays that could redefine procedure planning and postoperative surveillance.

Urethral Stricture Treatment Industry Leaders

BD

Boston Scientific

Coloplast

Cook Medical

Teleflex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA cleared UroGen Pharma’s Zusduri (mitomycin) as the first therapy for recurrent low-grade, intermediate-risk non-muscle invasive bladder cancer.

- May 2025: Laborie published three-year ROBUST III data in the Journal of Endourology, confirming the long-term durability of the Optilume drug-coated balloon for anterior urethral strictures.

Global Urethral Stricture Treatment Market Report Scope

Urethral stricture treatment refers to medical procedures aimed at addressing the narrowing of the urethra caused by scar tissue, which obstructs urine flow.

The Urethral Stricture Treatment Market Report is segmented by Treatment Type, Product Type, Etiology, Patient Type, End User, and Geography. By Treatment Type, the market is segmented into Surgical, Endoscopic/Minimally-Invasive, Non-Surgical/Dilation-Based, and Laser. By Product Type, the market is segmented into Dilators, Stents, Drug-Coated Balloons, Catheters, and Endoscopic Systems. By Etiology, the market is segmented into Idiopathic, Iatrogenic, Traumatic, and Inflammatory. By Patient Type, the market is segmented into Male, Female, and Transgender. By End User, the market is segmented into Hospitals, ASCs, and Specialty Clinics. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Surgical Treatments |

| Endoscopic / Minimally-Invasive Treatments |

| Non-Surgical / Dilation-Based Management |

| Laser Therapy |

| Urethral Dilators |

| Urethral Stents |

| Drug-Coated Balloons |

| Catheters |

| Endoscopic & Imaging Systems |

| Idiopathic |

| Iatrogenic |

| Traumatic |

| Inflammatory / Lichen Sclerosus |

| Male |

| Female |

| Transgender (FtM / MtF) |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Urology Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Surgical Treatments | |

| Endoscopic / Minimally-Invasive Treatments | ||

| Non-Surgical / Dilation-Based Management | ||

| Laser Therapy | ||

| By Product Type | Urethral Dilators | |

| Urethral Stents | ||

| Drug-Coated Balloons | ||

| Catheters | ||

| Endoscopic & Imaging Systems | ||

| By Etiology | Idiopathic | |

| Iatrogenic | ||

| Traumatic | ||

| Inflammatory / Lichen Sclerosus | ||

| By Patient Type | Male | |

| Female | ||

| Transgender (FtM / MtF) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Urology Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the urethral stricture treatment market?

The urethral stricture treatment market size is USD 2.01 billion in 2026 and is forecast to reach USD 2.85 billion by 2031 at a 7.31% CAGR.

Which treatment method is growing fastest?

Endoscopic and minimally invasive options, led by drug-coated balloons and single-use cystoscopes, are expanding at a 9.72% CAGR through 2031.

Why are drug-coated balloons gaining interest?

Optilume showed 71.9% freedom from re-intervention at three years, greatly extending patency compared with standard dilation.

Which region offers the highest growth potential?

Asia-Pacific posts the fastest 9.74% CAGR, supported by expanding insurance coverage in China and India.

What limits adoption in low-income markets?

High import tariffs and low reimbursement caps keep premium device prices far above local spending capacity.

Page last updated on: