Maple Syrup Urine Disease Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

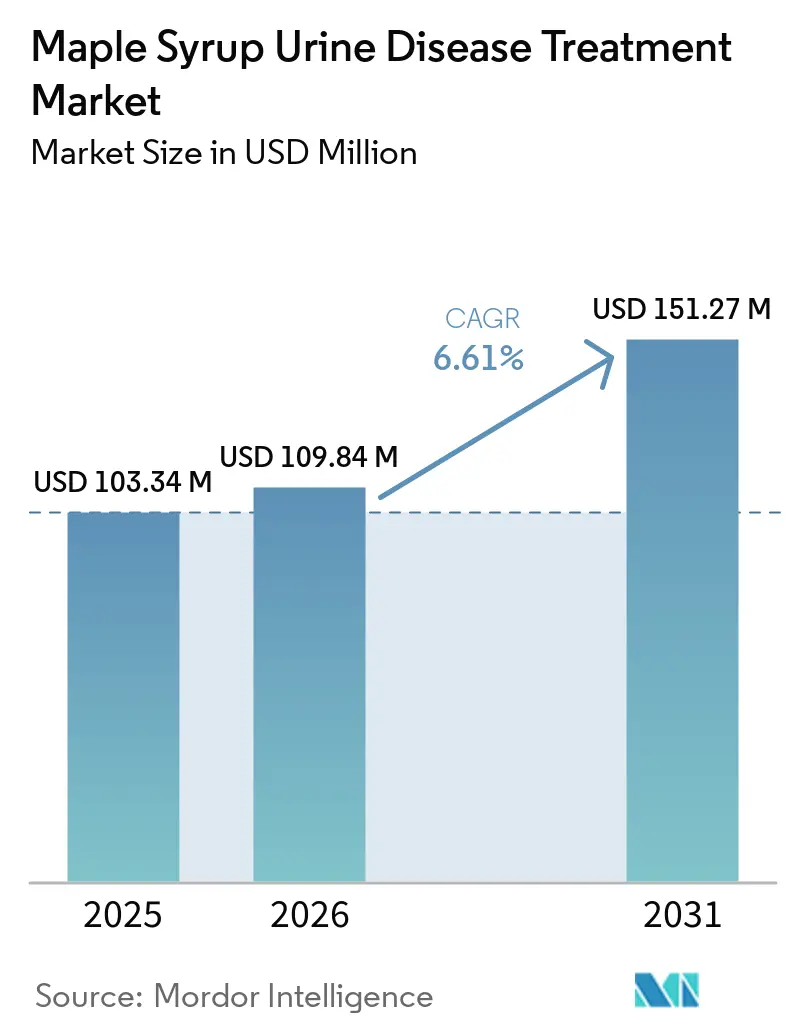

| Market Size (2026) | USD 109.84 Million |

| Market Size (2031) | USD 151.27 Million |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maple Syrup Urine Disease Treatment Market Analysis by Mordor Intelligence

The Maple Syrup Urine Disease Treatment Market size is expected to increase from USD 103.34 million in 2025 to USD 109.84 million in 2026 and reach USD 151.27 million by 2031, growing at a CAGR of 6.61% over 2026-2031.

The maple syrup urine disease treatment market is shaped by two forces that now move in parallel: the stabilization of medical-food supply chains after the 2022 infant formula crisis and the early development of gene therapy modalities that may shift a portion of lifetime dietary management to a one-time intervention within the forecast window’s horizon[1]U.S. Food and Drug Administration, “The U.S. Food and Drug Administration’s Long-Term National Strategy to Increase the Resiliency of the U.S. Infant Formula Market,” U.S. Food and Drug Administration, fda.gov. Newborn screening mandates and lab protocol refinements in major regions compress time-to-diagnosis to within the first week of life, which protects neurocognitive outcomes and increases formula initiation at the neonatal stage. At the same time, adeno-associated virus platforms now show preclinical durability and survival benefits in classic MSUD animal models, prompting preparations for human studies that could reshape pediatric volumes in the next planning cycle.

Unlike orphan categories centered on one molecule, the maple syrup urine disease treatment market maintains parallel product ecosystems across life stages, with formulations from Abbott, Nutricia, and Vitaflo spanning infant to adult needs as clinicians match format and palatability to phenotype and age. Supply-risk mitigation remains core to competitive execution as regulators retain import flexibilities and redundancy planning to prevent a repeat of six-month disruptions that previously rippled across specialized metabolic formulas.

Key Report Takeaways

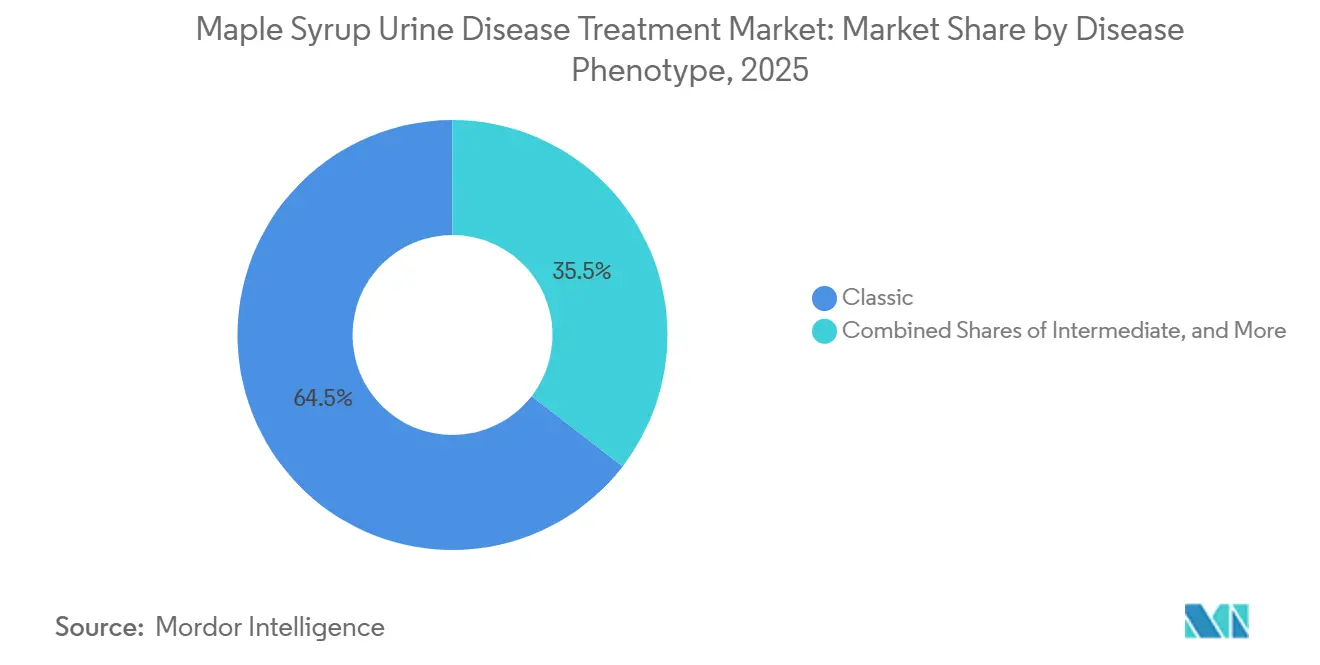

- By disease phenotype, classic MSUD led with 64.53% revenue share in 2025, while thiamine-responsive is projected to expand at a 7.57% CAGR to 2031.

- By age group, pediatrics held 40.12% share in 2025, while neonates and infants are forecast to grow at a 6.63% CAGR through 2031.

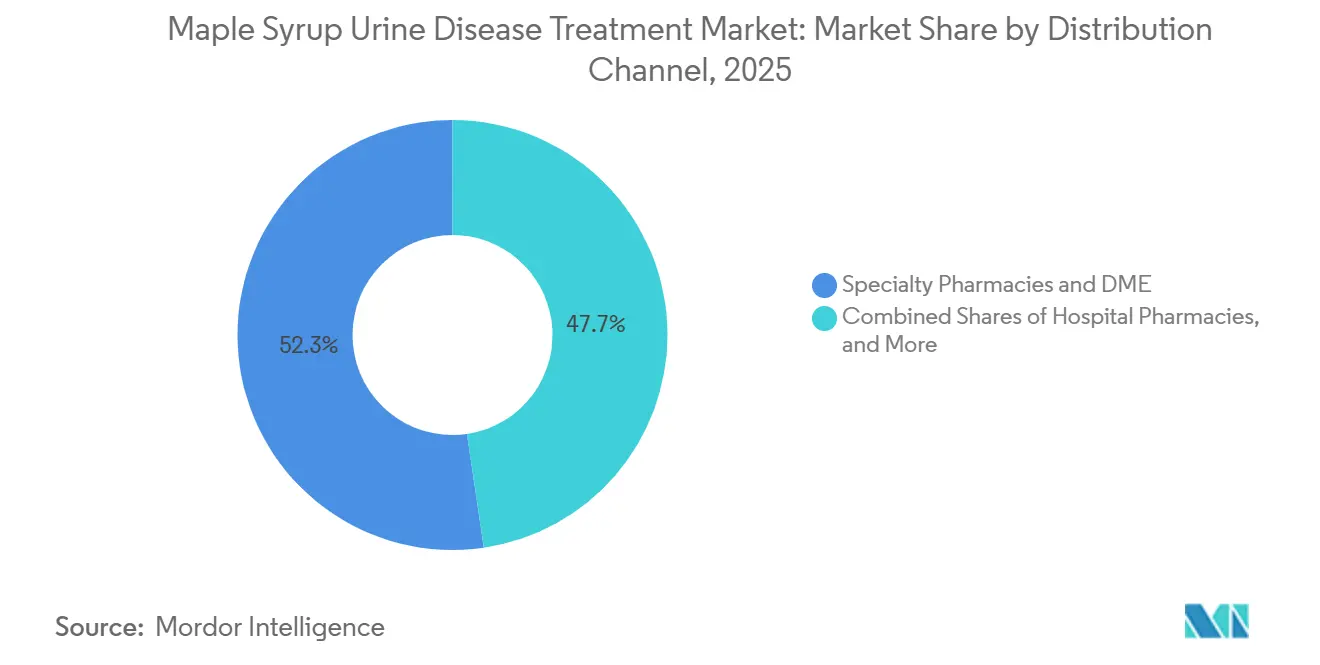

- By distribution channel, specialty pharmacies and DME captured 52.32% share in 2025, while direct-to-consumer e-commerce records the highest projected CAGR at 7.34% to 2031.

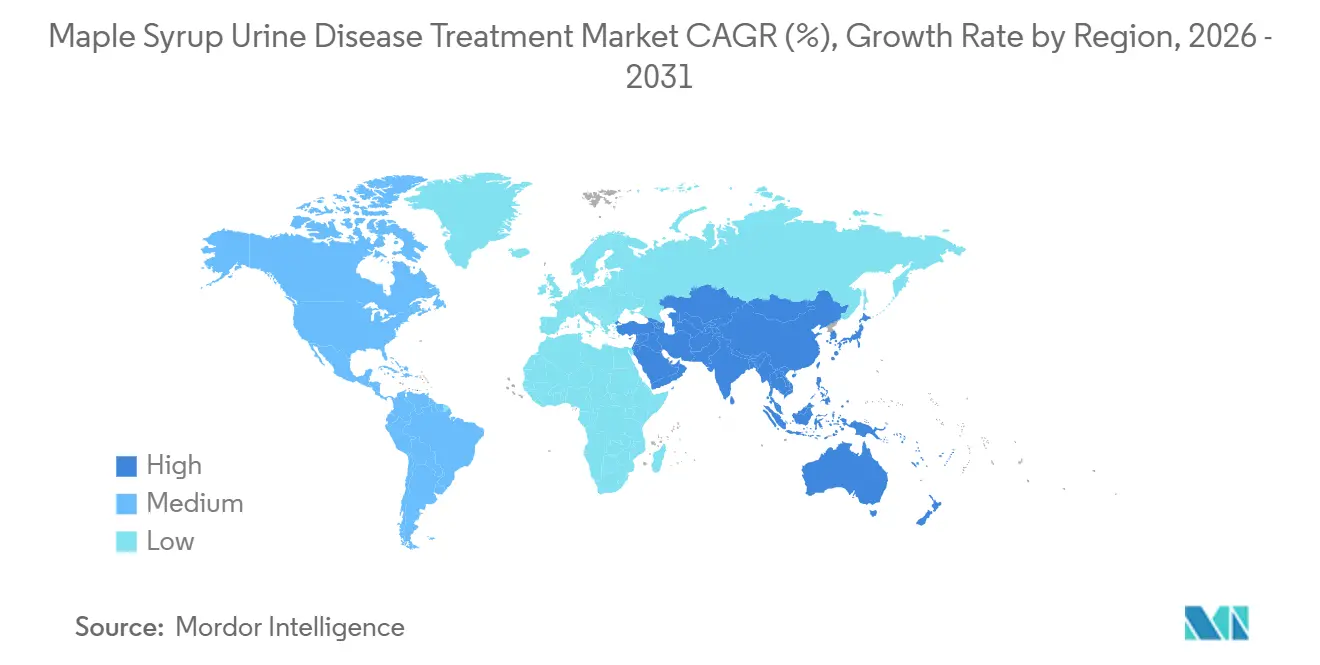

- By geography, North America led with 43.23% revenue share in 2025, while Asia-Pacific is forecast to post the fastest growth with 7.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Maple Syrup Urine Disease Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of newborn screening and earlier diagnosis | +1.8% | Global, with accelerated uptake in APAC, and select U.S. states | Short term (≤ 2 years) |

| Standard-of-care reliance on BCAA-free medical foods and supplements | +2.1% | North America, Europe | Long term (≥ 4 years) |

| Adoption of liver transplantation as curative option in severe cases | +0.9% | MENA core, spillover to Europe and North America | Medium term (2-4 years) |

| Broader availability of MSUD-specific products across global nutrition majors | +1.2% | Global | Medium term (2-4 years) |

| Domino liver transplantation expanding donor pool | +0.6% | MENA, Brazil, select U.S. centers, early gains in APAC | Medium term (2-4 years) |

| Supply-resilience actions post-2022 formula crisis and import flexibilities | +0.5% | North America primary, spillover to EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Newborn Screening and Earlier Diagnosis

Tandem mass spectrometry embedded in routine newborn screening programs has reduced time-to-diagnosis for classic MSUD to within the first week of life in jurisdictions that strengthened their panels between 2024 and 2026, which improves crisis prevention when BCAA-free nutrition is started immediately. Guidance updates from clinical genetics bodies in 2026 refined laboratory thresholds to reduce false positives, which may still produce a two-tier landscape where some intermediate phenotypes are identified during follow-up rather than at the initial screen.

Regional data from Xinjiang’s expanded screening showed very low incidence detection in a large birth cohort, highlighting the challenge of sustaining high-quality coverage in low-prevalence regions and the value of bundling multiple inborn errors to maintain cost-effectiveness. Public payer coverage frameworks vary, so even with early diagnosis, families experience different out-of-pocket exposure depending on how medical foods are classified by state or provincial policy. In practice, earlier detection and aligned reimbursement codes shorten the window to nutritional intervention, improve adherence, and reduce neurological injury risk across classic presentations.

Standard-of-Care Reliance on BCAA-Free Medical Foods and Supplements

BCAA-free formulas remain the backbone of therapy for most diagnosed patients, and supply strength, palatability, and micronutrient profiles that influence daily adherence and clinical stability. Manufacturers continue to refine omega-3 and condition-specific formulations, reflected in updated product references and guides that align with pediatric and adult nutritional needs by life stage. Vitaflo expanded capacity and introduced co-extrusion technology in Germany to improve ease of preparation and support adherence, with the line-up spanning gels, powders, and ready-to-drink options to match taste and preparation preferences. Price transparency across distributors shows clear tiering by brand, format, and fortification, which nudges family preferences and subscription choices in the outpatient setting. Post-crisis regulatory expectations require redundancy and risk planning that add fixed costs but also reduce the likelihood of prolonged shortages that jeopardize care in highly time-sensitive neonatal and pediatric use cases.

Adoption of Liver Transplantation as Curative Option in Severe Cases

Orthotopic liver transplantation restores sufficient BCKDH activity to maintain leucine homeostasis without strict dietary restrictions in classic MSUD, and recent single-center data report excellent short-term survival in pediatric recipients[2]Ibrahim Hassan et al., “Pediatric Liver Transplant for Maple Syrup Urine Disease, A Single Center Experience,” Frontiers in Pediatrics, frontiersin.org. Expanded use of established exception pathways improves access for patients who experience recurrent decompensations, though allocation committees still weigh timing carefully to balance perioperative risks against cognitive protection.

Domino models that re-transplant explanted MSUD livers into non-MSUD recipients increase donor utility and sustain survival in adult populations when properly selected, which supports broader system efficiency where wait-list pressure is acute. Ethical acceptance differs by jurisdiction, so program growth concentrates in regions with established protocols and oversight bodies comfortable with the clinical logic of domino sequences. As transplant data mature, centers continue to refine candidacy criteria and perioperative monitoring for metabolic stability to reduce ICU days and accelerate return to normal diet.

Broader Availability of MSUD-Specific Products Across Global Nutrition Majors

Distribution strategies now blend specialty pharmacy with e-commerce models that verify prescriptions and automate documentation, which shortens time from order to first fill and raises adherence. Programs designed by manufacturers to navigate prior authorization and coordinate across contracted distributors improve first-fill success in complex reimbursement environments. Public programs in some provinces and states list covered SKUs and define reimbursement rules, which reduces household financial risk when coverage is comprehensive and transparent. Health plans and medical policy bulletins specify the benefit category and coding for metabolic formulas and enteral nutrition, which determines eligibility and claim processing paths. Parallel investments in compounding, warehousing, and temperature-controlled logistics among specialty providers increase resilience when branded SKUs face temporary supply pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-rare prevalence limits commercial viability and trial enrollment | -1.1% | Global | Long term (≥ 4 years) |

| High lifetime cost of specialized medical foods and transplant care | -0.8% | North America, Europe | Medium term (2-4 years) |

| Uneven medical food reimbursement due to non-drug regulatory status | -0.6% | North America primary, select EU markets | Medium term (2-4 years) |

| Transplant capacity and ethics constraints with variable program acceptance | -0.4% | Europe, select U.S. academic centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-Rare Prevalence Limits Commercial Viability and Trial Enrollment

MSUD’s low incidence limits the number of diagnosable and treatable patients, which raises the bar for sponsors attempting prospective studies that require multicenter coordination[4]Syed Adeel Hassan and Vikas Gupta, “Maple Syrup Urine Disease,” StatPearls, ncbi.nlm.nih.gov. European regulators addressed this for acute decompensation care by granting authorization for a parenteral BCAA-free solution under exceptional circumstances, allowing an alternative evidentiary model anchored in retrospective data when conventional trials are not feasible.[3]European Medicines Agency, “Maapliv,” European Medicines Agency, ema.europa.eu

For gene therapy, preclinical survival and biomarker gains in animal models support the case for an initial pediatric cohort, yet early human trials still need sufficient numbers across phenotypes central to clinical need. Enrollment strategies must also consider phenotype heterogeneity, since intermediate and intermittent forms express variant enzyme activity levels that may not reflect classic endpoints, which influences study design and analysis plans. As regulators balance feasibility with rigor, companies are likely to rely on global networks of metabolic centers with established newborn screening linkages to identify eligible candidates efficiently.

High Lifetime Cost of Specialized Medical Foods and Transplant Care

Specialized medical foods represent a significant and recurring expense throughout childhood and into adulthood, and coverage rules differ by jurisdiction because formulas are not universally treated as drugs for policy purposes. State-level policies require detailed medical necessity documentation and, at times, restrict coverage to specific delivery methods, which shapes access and creates uneven financial burdens across families in adjacent states. Newer legislation in select states has broadened coverage terms for amino acid-based formulas, although caps and rate-linked limits still leave gaps for higher-dosage patients who need more units per month. For patients eligible for transplantation, cost profiles shift toward a larger up-front procedure with long-term immunosuppression, which payers evaluate against expected lifetime spending on formulas and acute care. The policy environment continues to evolve as agencies and insurers refine classifications, coding, and medical-necessity criteria to better match clinical standards of care in inherited metabolic disorders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Phenotype: Classic Drives Volume, Thiamine-Responsive Disrupts Margins

Classic MSUD accounted for 64.53% in 2025, reflecting neonatal presentation and lifelong reliance on BCAA-free formulas; within the same segmentation, the thiamine-responsive subtype is forecast to grow at 7.57% to 2031 as more centers implement standardized B-vitamin challenge protocols. The maple syrup urine disease treatment market share is concentrated in classic presentations because near-zero residual BCKDH activity requires consistent nutritional therapy under metabolic supervision beginning soon after birth. Intermediate phenotypes, with partial enzyme activity, rely on pediatric-friendly formulations tailored to taste and preparation convenience to support adherence during early childhood. Clinical adoption of molecular testing enables earlier subtype confirmation, which supports phenotype-specific nutrition planning and reduces the risk of crisis events arising from delayed or inappropriate dietary adjustments. Across the phenotype mix, acute decompensation care now includes an authorized parenteral option, which strengthens hospital protocols for intermittent and intermediate forms when oral or enteral formulation cannot be used during crisis.

In the thiamine-responsive phenotype, the maple syrup urine disease treatment market size tied to oral supplementation grows with better genotype–phenotype mapping and standardized challenge testing, which shifts a share of intermediate cases from transplant pathways to medically supervised vitamin therapy when feasible. European diagnostic regulations that took effect in 2025 add conformity and labeling standards, which consolidate testing among qualified labs and yield more consistent reporting across countries. Research on genotype variation since 2024 has broadened the documented spectrum and informs clinical risk assessment as families and clinicians plan nutrition and monitoring intensity. As adoption spreads, payers and clinics may see lower transplant referrals among those with confirmed responsiveness, though long-term neurocognitive outcomes require continued tracking. Overall, phenotype-driven care pathways continue to anchor how products are positioned by brand, age, and preparation format across the maple syrup urine disease treatment market.

By Age Group: Neonatal Screening Fuels Infant Surge, Adult Segment Lacks Innovation

Pediatrics held 40.12% share in 2025, and neonates and infants are projected to grow at 6.63% through 2031 as newborn screening policies compress diagnostic lag and bring dietary management forward into the first week of life. The maple syrup urine disease treatment market benefits from early initiation because it stabilizes leucine levels during critical developmental windows, and product portfolios reflect this with infant-appropriate fat profiles and micronutrients. Public program documents and medical policies outline eligibility rules, coding, and prior authorization processes, which are central to maintaining a consistent supply in the first year of life. As children enter school age, taste, convenience, and format choice remain critical, and vendors have expanded lines to include powders, gels, and ready-to-drink options tailored to pediatric routines. Hospital availability of parenteral BCAA-free amino acids for acute care strengthens safety nets when intercurrent illness or feeding intolerance interrupts oral and enteral intake.

Among adults, gaps persist in formulations designed for mental health and bone health needs that often surface in long-term management, where many still consume pediatric-intended SKUs due to limited adult-specific alternatives. Specialty pharmacy channels continue to support adult adherence through documentation services and patient support programs, while DTC options simplify reordering for stable patients. As adults gain independence, routines that reduce preparation time and simplify dosing may raise adherence, which shapes value propositions for new SKUs directed at the over-18 population. Transplant pathways remain an option for a subset of adults with recurrent decompensations, and system-level capacity decisions influence referral timing and uptake. On balance, the maple syrup urine disease treatment industry has room to expand adult-focused nutrition innovation while preserving robust infant and pediatric pipelines.

By Distribution Channel: Specialty Pharmacy Dominates, DTC E-Commerce Scales Fastest

Specialty pharmacies and DME suppliers captured 52.32% in 2025 due to defined benefit categories and coding that position metabolic formulas for reimbursement under established medical policies, while direct-to-consumer e-commerce reported the highest projected CAGR at 7.34% to 2031. The maple syrup urine disease treatment market size, supported by specialty channels, benefits from prior authorization expertise and stocking practices that match refill cycles for infants and children with higher monthly usage. Hospital pharmacies remain essential for handling acute decompensation cases with parenteral solutions, which require formulary decisions and stocking protocols that align with pediatric emergency care. DTC e-commerce is the fastest-growing channel as prescription verification and documentation workflows move online and compress order-to-delivery timelines for stable patients. Manufacturer programs that coordinate distributor networks and pre-populate documentation improve first-fill rates and reduce administrative friction for families and clinics.

Regional and program-level rules, including public coverage lists and single-vendor distribution frameworks, shape how families access products and which brands are dispensed. Specialty providers that invest in compounding, storage, and rapid fulfillment can bridge gaps when branded formulas face temporary constraints, which stabilizes adherence across vulnerable cohorts. Product-level price differentials across brands and SKUs continue to influence channel selection and subscription choices, especially when personal budgets interact with coverage caps. As channel strategies evolve, the maple syrup urine disease treatment market will likely maintain a hybrid model that balances payer-aligned specialty pharmacy with convenience-driven DTC platforms. Robust risk management and supply duplication across nodes remain central to preventing the cascading shortages that previously disrupted this category.

Geography Analysis

North America held 43.23% of the maple syrup urine disease treatment market share in 2025, supported by WIC-linked and Medicaid-aligned coverage frameworks that classify metabolic formulas as pharmacy-dispensed medical foods across most states. State and plan-level documents detail eligibility and coding, which drive claim routing and influence continuity of care for infants and children. The 2022 crisis prompted a federal long-term strategy that now requires redundancy planning and supports import flexibilities so foreign-made specialized formulas can stabilize U.S. supply during shocks. Newborn screening programs in states like Texas brought MSUD squarely into core panels, which shortens diagnostic lag and raises prompt access to formula therapy in the neonatal stage. Commercial policy updates in some states have expanded coverage, although benefit caps and delivery-method clauses still generate variance in out-of-pocket costs for households. As manufacturers and specialty providers strengthen U.S. capacity and logistics, the maple syrup urine disease treatment market in North America remains anchored by infant and pediatric demand with hospital backup for acute decompensation.

Europe leads in acute-care innovation with the approval of the first EU-authorized parenteral BCAA-free amino acid solution for MSUD crises under exceptional circumstances. The region’s diagnostic regime fully aligned with new IVD rules in 2025, which add conformity and labeling discipline across MSUD genetic panels and consolidate testing among accredited labs. European health systems dispense MSUD formulas through hospital-linked pharmacy channels, which ensures clinical oversight and reliable refills for families under care. Manufacturing investments in Germany doubled local capacity and introduced production technologies that improve preparation time and adherence-friendly formats for pediatric patients. The region’s market structure blends centralized dispensing with specialty distributors, and formulary rules define which SKUs are reimbursable, which in turn shapes brand-level share by country. As clinical trial pathways and post-market evidence expand, the maple syrup urine disease treatment market in Europe benefits from stronger hospital readiness and harmonized diagnostics.

Asia-Pacific accounts 7.17% CAGR and is positioned for the fastest growth through 2031 as provincial screening expansions and improved referral networks identify cases earlier and start nutrition therapy in the first week of life. Data from Xinjiang illustrate how low measured incidence still warrants sustained MS/MS screening when programs are bundled with other inborn errors to meet public health thresholds. APAC’s hospital systems strengthen care pathways for acute decompensation in tertiary centers, with parenteral options improving the ability to bridge patients during episodes where oral or enteral intake is not possible. In the Middle East and North Africa, single-center pediatric transplant programs reported 100% one-year survival in 2025 cohorts and expanded domino utilization to stretch donor supply, which reduces wait times and supports metabolic stability post-transplant. As public screening policies scale and hospital capabilities strengthen across these regions, the maple syrup urine disease treatment market gains from earlier initiation of nutritional care, tighter crisis management, and modest uptake of surgical pathways where programs are established.

Competitive Landscape

The maple syrup urine disease treatment market displays moderate concentration with three nutrition majors that manage life-stage ecosystems from infant to adult, while specialty providers and hospital pharmacies reinforce acute care and compounding-led customization. Product portfolios emphasize adherence and clinical fit by phenotype and age, and brand loyalty builds over time as families align on preparation routines and micronutrient profiles under dietitian guidance. In practical terms, this reduces frequent switching and sustains within-brand progression between infant, pediatric, and adolescent SKUs for many households. Specialty distribution investments expand sterile compounding and warehousing capacity, which improves the resilience of the overall channel during branded supply interruptions.

Three strategic moves exemplify current positioning. First, Vitaflo completed a USD 9.03 German expansion in 2025, doubling capacity and deploying new co-extrusion technology to speed preparation and support adherence in pediatric cohorts. Second, Recordati Rare Diseases secured EU authorization for an IV BCAA-free amino acid solution to address acute decompensation events, opening a specialized hospital segment that complements outpatient formula use. Third, Pentec Health broadened sterile compounding and distribution infrastructure to deliver custom BCAA-free blends within tight turnaround times, which targets patients whose tolerance profiles require tailored formulations. These moves strengthen the supply spine that underpins the maple syrup urine disease treatment market and reduce failure points that previously triggered emergency substitution and variable adherence.

Maple Syrup Urine Disease Treatment Industry Leaders

Nestlé Health Science (Vitaflo)

Danone (Nutricia)

Abbott Laboratories

Reckitt (Mead Johnson Nutrition)

Ajinomoto Cambrooke, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Researchers at UMass Chan Medical School developed a gene therapy aimed at correcting mutations responsible for two distinct genetic forms of maple syrup urine disease (MSUD). This innovative treatment has been licensed to biotech firm Plowshare Therapies.

- May 2025: Recordati Rare Diseases received European Commission marketing authorization for Maapliv, a branched-chain amino acid-free intravenous solution indicated for acute decompensation episodes in MSUD patients from birth who cannot tolerate oral or enteral formulations. The approval, granted under exceptional circumstances, is the first EU authorization for a parenteral therapy designed for MSUD metabolic crises.

Global Maple Syrup Urine Disease Treatment Market Report Scope

The maple syrup urine disease treatment market comprises therapies and nutritional interventions used to manage maple syrup urine disease, a rare inherited metabolic disorder characterized by impaired breakdown of branched-chain amino acids. The market includes specialized medical formulas, supplements, and supportive treatments distributed through hospital, specialty, and direct-to-consumer channels across developed and emerging healthcare systems worldwide.

The maple syrup urine disease treatment market is segmented by disease phenotype, including classic, intermediate, intermittent, and thiamine-responsive forms; by age group, comprising neonates and infants, pediatrics, and adults; by distribution channel, covering specialty pharmacies and durable medical equipment providers, hospital pharmacies, and direct-to-consumer e-commerce. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Classic |

| Intermediate |

| Intermittent |

| Thiamine-responsive |

| Neonates/Infants |

| Pediatrics |

| Adults |

| Specialty Pharmacies & DME |

| Hospital Pharmacies |

| Direct-to-Consumer E-Commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Phenotype | Classic | |

| Intermediate | ||

| Intermittent | ||

| Thiamine-responsive | ||

| By Age Group | Neonates/Infants | |

| Pediatrics | ||

| Adults | ||

| By Distribution Channel | Specialty Pharmacies & DME | |

| Hospital Pharmacies | ||

| Direct-to-Consumer E-Commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the maple syrup urine disease treatment market and how fast is it growing?

The maple syrup urine disease treatment market size was USD 103.34 million in 2025 and is projected to reach USD 151.27 million by 2031 at a 6.61% CAGR over 2026-2031.

Which phenotype segment is the largest and which grows the fastest in this space?

Classic MSUD is the largest with 64.53% in 2025, while the thiamine-responsive subtype is forecast to grow at 7.57% to 2031.

Which channels are most important for access and adherence in the maple syrup urine disease treatment market?

Specialty pharmacies and DME are the largest due to reimbursement alignment, while direct-to-consumer e-commerce grows fastest as documentation and verification move online.

What are the most important policy and regulatory drivers for this category?

Expanded newborn screening, FDA supply-resilience requirements including redundancy plans, and EU authorizations for parenteral crisis care shape access and hospital readiness.

How could gene therapy change the outlook for nutritional products?

If AAV9-based approaches succeed in human trials, a portion of pediatric patients could transition from lifelong formula reliance to a one-time intervention, which would rebalance long-term volumes.

Which regions are most significant for near-term demand?

North America currently leads by share due to coverage frameworks and screening, while Asia-Pacific is positioned for the fastest growth as screening and referral networks expand.

Page last updated on: