Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 448.90 Billion |

| Market Size (2031) | USD 726.78 Billion |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare BPO Market Analysis by Mordor Intelligence

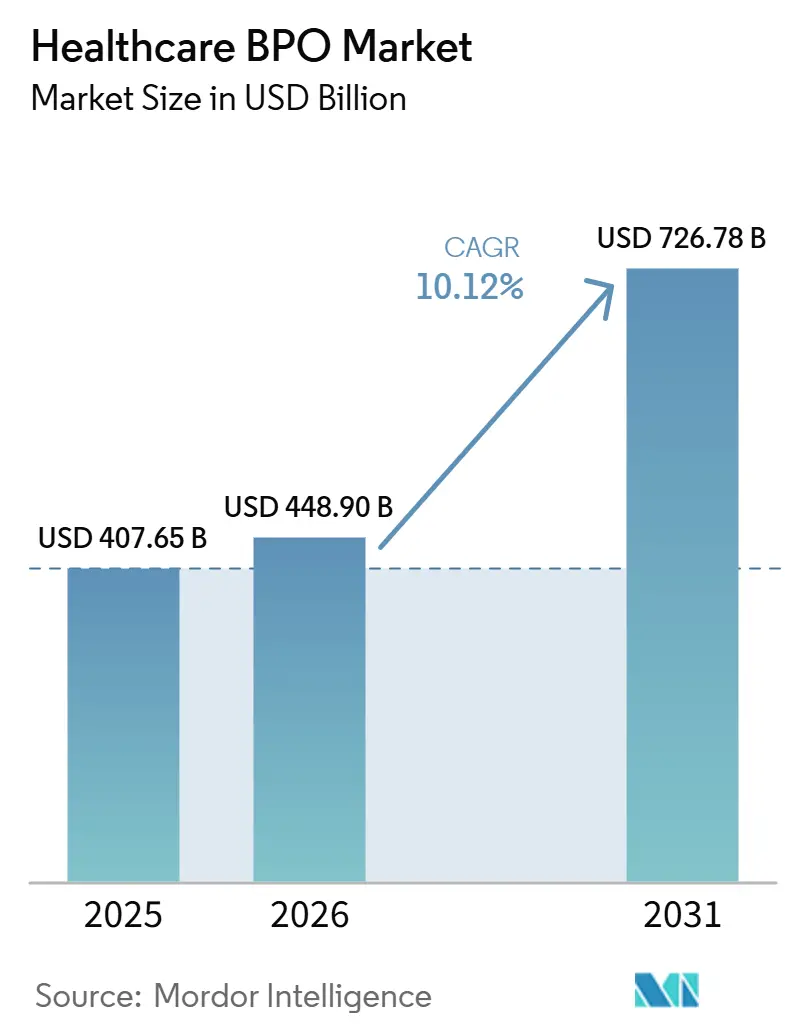

The Healthcare BPO Market size is expected to grow from USD 407.65 billion in 2025 to USD 448.90 billion in 2026 and is forecast to reach USD 726.78 billion by 2031 at 10.12% CAGR over 2026-2031.

This expansion reflects a shift from labor-only contracts toward technology-enabled transformation platforms that address systemic clinical and administrative inefficiencies. Demand is rising as hospitals and insurers confront tighter reimbursement, persistent labor shortages, and stricter data-protection laws. Private-equity ownership is accelerating platform investments, and the combination of generative AI with domain expertise is reshaping price–value equations. Rising interest rates have not dampened investor appetite, largely because AI-driven productivity gains allow providers to commit to outcome-based pricing that protects margins in a turbulent funding environment.

Key Report Takeaways

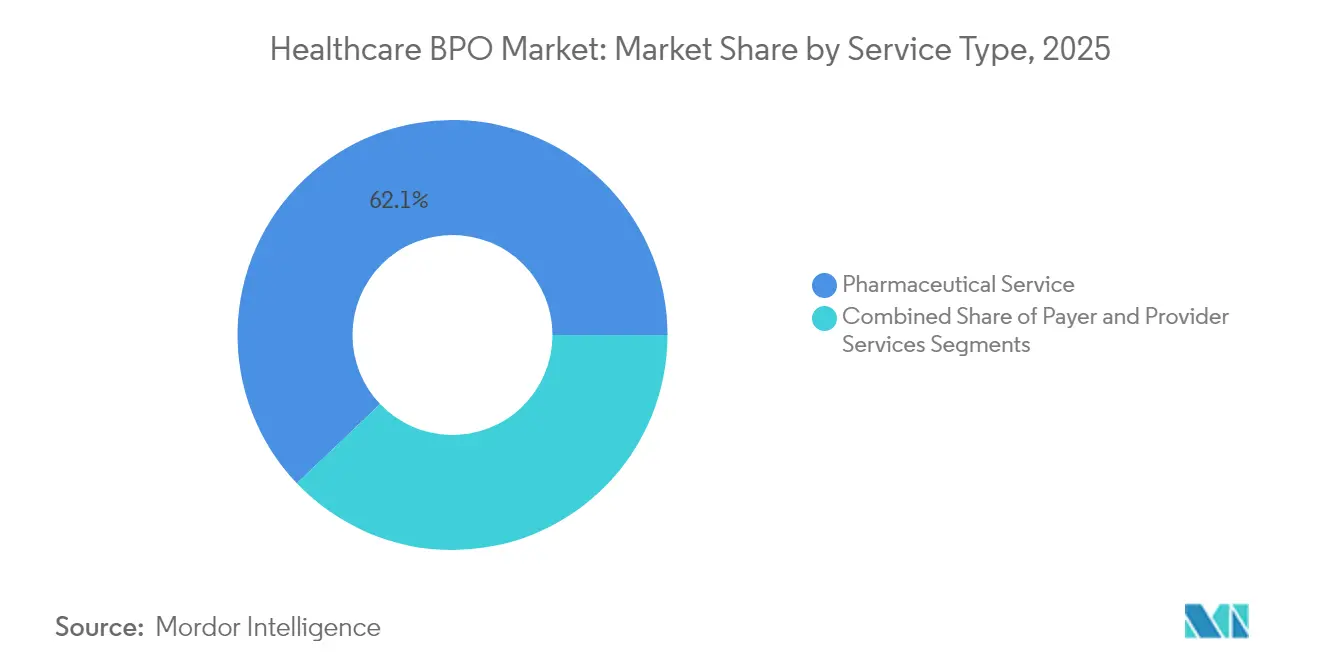

- By service type, pharmaceutical services held 62.12% of Healthcare BPO market share in 2025, while Provider services are poised for the fastest 14.78% CAGR through 2031.

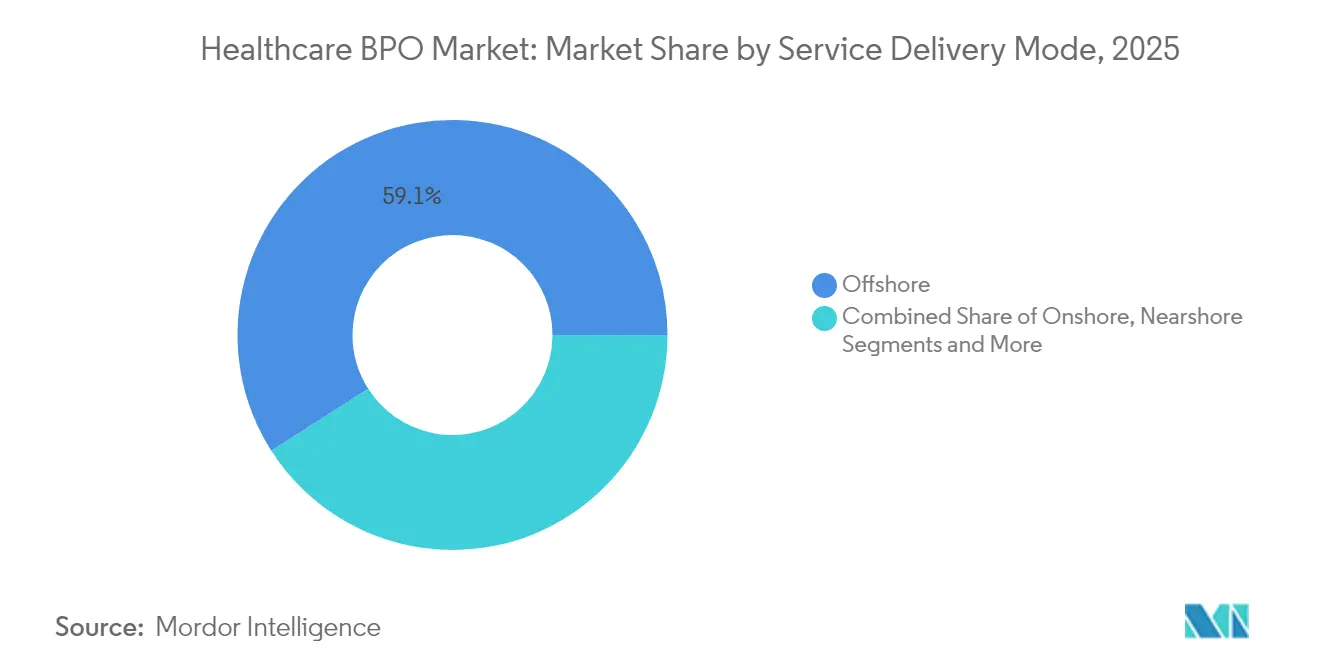

- By service delivery model, Offshore operations represented 59.05% of the Healthcare BPO market revenue in 2025; Nearshore delivery will register the highest 14.21% CAGR through 2031.

- By technology adoption model, Traditional Lift-and-Shift retained 52.88% of 2025 revenue, yet Generative-AI-embedded delivery is climbing 11.95% CAGR.

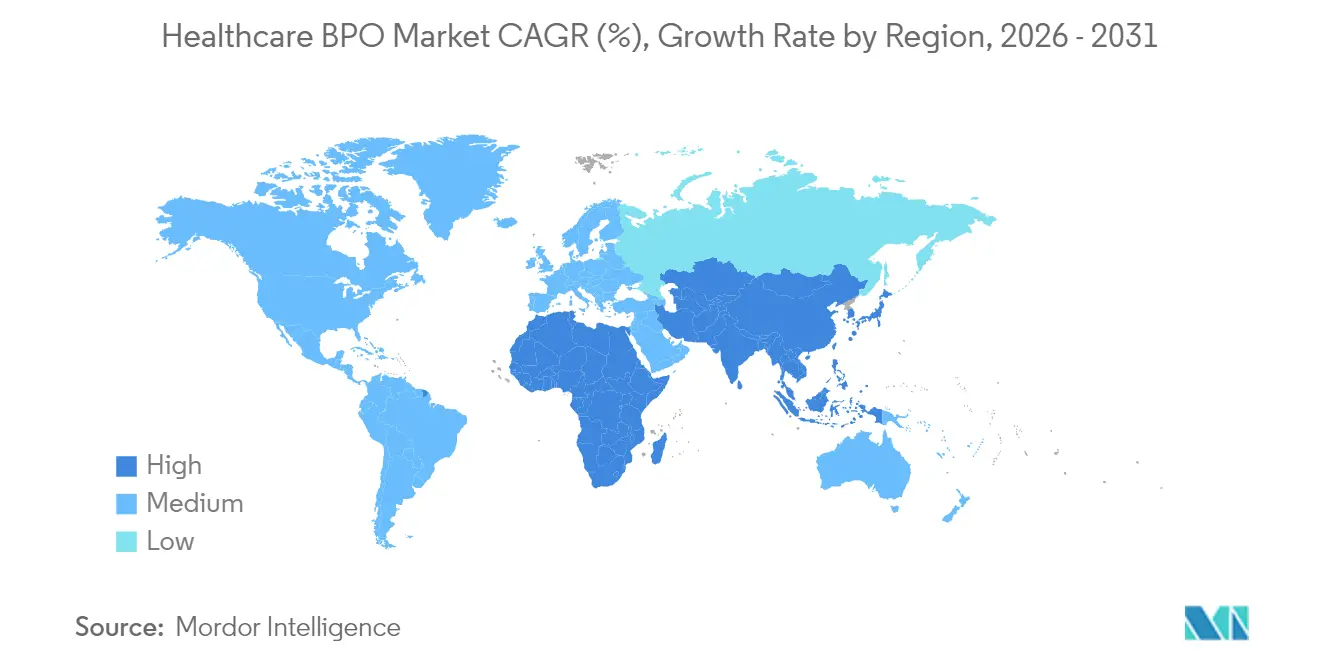

- By geography, North America contributed 48.15% of 2025 revenue, whereas Asia-Pacific is pacing the field with a 12.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare BPO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshore outsourcing and access to technology | +1.8% | North America & Latin America | Medium term (2-4 years) |

| Rapid clinical process outsourcing | +2.1% | Global | Long term (≥ 4 years) |

| Healthcare reforms drive outsourcing | +1.5% | North America & Europe | Medium term (2-4 years) |

| Generative-AI coding automation | +2.3% | Global | Short term (≤ 2 years) |

| Payvider convergence | +1.2% | North America | Long term (≥ 4 years) |

| PE-fuelled roll-ups | +1.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Near-shore outsourcing enables real-time collaboration

Academic research shows that healthcare organizations shifting work to nearby countries reduce operational risk by 35% while still saving 20-30% compared with on-shore delivery.[1]Miguel Ramirez, “Risk and Cost Outcomes of Near-Shore Outsourcing in Healthcare,” University of California San Diego, ucsd.edu Heightened data-residency laws such as Florida’s requirement that electronic health records stay in the United States, its territories, or Canada make proximate sites more attractive than far-shore hubs. Mexico’s 10.5% annual rise in near-shore IT and business services revenue further strengthens its position as a preferred location, particularly for revenue cycle and clinical documentation contracts. The USMCA’s digital-trade chapter provides legal certainty regarding cross-border data flows and intellectual property protection, giving payers and providers confidence to award multi-year deals to suppliers in the region. Stanford University findings indicate that proximity-based models enhance compliance outcomes by 40% and reduce communication errors by 25%. Together, these factors accelerate a geographic shift that favors the healthcare BPO market, especially for mid-cycle revenue functions.

Rapid uptake of clinical process outsourcing (CPO)

A five-year longitudinal study reported that sponsors using external partners short-ened clinical trials by 18 months without sacrificing compliance.[2]Karen Mitchell, “Decentralized Trials and Outsourcing Trends,” Journal of Clinical Research and Bioethics, omicsonline.org Post-pandemic interest in decentralized studies increases the need for patient-engagement tools and data-integration platforms that specialized BPO firms already operate. Harvard Medical School researchers observed 22% higher enrollment and 15% better data-quality scores in outsourced trials versus in-house programs. As artificial-intelligence engines automate data capture and regulatory-submission tasks, vendors can layer value-added analytics on top of traditional monitoring. Outsourcing also frees biotech teams to focus on core R&D while accessing global patient pools and dedicated regulatory expertise. This combination positions CPO as the fastest-expanding slice of the healthcare business process outsourcing market.

Healthcare reforms propel specialized outsourcing

Value-based-care mandates and ongoing PPACA updates create complex reporting rules that many hospitals struggle to meet internally. The Commonwealth Fund found that providers using external administrative partners achieved 28% better quality outcomes and 19% lower back-office costs. ICD-11 adoption and frequent coding updates require continual staff training, an area where BPO suppliers already maintain certified talent pools. Health Affairs documented 45% fewer audit findings and 30% faster regulatory responses among systems that outsource compliance functions. Predictable rule changes translate into steady demand, allowing vendors to bundle analytics, care coordination, and technology under multiyear contracts that support premium pricing, strengthening the healthcare bpo industry.

Generative-AI automation unlocks mid-cycle revenue deals

Peer-reviewed evidence shows that AI-enabled coding reaches 94% accuracy while slashing processing time by 75%.[3]P. Kannan, “Accuracy of Autonomous Coding Engines,” jmir.org Autonomous engines scale to millions of encounters with minimal human oversight, which lowers unit costs and expands addressable volume among mid-sized hospitals. Baptist Health used natural-language models to automate prior-authorizations and physician notes, cutting administrative bottlenecks and boosting throughput. MIT CSAIL researchers report 32% stronger cash-flow and 41% fewer claim denials when AI augments revenue-cycle work. Vendors combining these tools with seasoned compliance experts now pursue medium-tier providers that previously lacked the scale to justify outsourcing, enlarging the healthcare BPO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex multi-jurisdictional regulations | -1.3% | Global | Long term (≥ 4 years) |

| Hidden total cost and vendor lock-in | -0.9% | North America & Europe | Medium term (2-4 years) |

| Sovereign data-residency laws | -1.1% | Global | Short term (≤ 2 years) |

| Shortage of medically trained coders in tier-2 hubs | -0.8% | Asia-Pacific & Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Multi-Jurisdictional Regulations

Ever-evolving HIPAA clauses intersect with GDPR, forcing vendors to juggle encryption, multifactor authentication, and localized breach protocols. Suppliers incur legal reviews for every new cross-border hosting scenario. Florida’s prohibition on non-domestic storage increases onboarding cost and delays for multistate systems. Smaller vendors struggle to fund parallel compliance teams, which tempers new-logo growth across the Healthcare Business Process Outsourcing (BPO) Services market.

Hidden Total Cost and Vendor Lock-in

Clients often underestimate transition fees, productivity ramp-up, and change-management spend, leading to TCO overruns beyond headline unit prices. Monolithic proprietary platforms can restrict data portability, trapping payers or providers into multi-year renewals on legacy rates. These experiences feed board-level skepticism that elongates purchasing cycles, especially for first-time outsourcers in Europe and Canada.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Pharmaceutical Service Dominate Amid R&D Acceleration

By pharmaceutical services, manufacturing commands a dominant share in the healthcare business process outsourcing market. Manufacturing investments are shifting toward high-potency and cell-therapy facilities, driven by the growing complexity of biologicals. This trend is fostering long-term master service agreements that bundle technology transfer and regulatory lot-release services. Sales and Marketing outsourcing focuses on omnichannel physician engagement and compliant patient-support programs, while R&D outsourcing addresses specialized bioinformatics, toxicology, and companion-diagnostic analytics that smaller biotech firms cannot scale internally. Tightening serialization and anti-counterfeit mandates are driving the orchestration of non-clinical supply chains. Digital twin modeling and real-world-evidence platforms are expediting trial close-outs by mapping adverse-event triggers in near real time. Consolidating clinical and commercial data lakes enhances product-launch speed, while private equity-backed CRO roll-ups streamline site monitoring and central lab services, enabling sponsors to focus on pipeline science and maintain healthy margins.By provider services is the fastest growing service with a 14.78% CAGR over 2031. Revenue cycle management services support hospital fiscal stability amid labor shortages by automating clinical notes, charge capture, and payer edits, reducing cash-on-hand volatility. Patient Care Services integrates virtual nursing with contact-center triage to enhance experience scores, while Strategic Planning services analyze referral patterns and payer mixes to guide service-line investments. Advanced AI, such as predictive algorithms used by Ensemble Health, routes complex invoices to senior coders only when rules engines cannot resolve them on their own, enabling hospitals to increase net revenue without proportional headcount growth. This productivity shift positions outsourcing as a revenue driver rather than just a cost-cutting tool, reinforcing the healthcare bpo industry.

By Service Delivery Model: Offshore Dominance Challenged by Nearshore Growth

Offshore centers accounted for 59.05% of 2025 revenue, anchored by India and the Philippines. Even so, nearshore delivery, expanding 14.21% CAGR, now wins sensitive mid-cycle coding and prior-authorization queues where real-time clinician collaboration matters. Onshore units remain critical for high-value analytics and audits tied to Centers for Medicare & Medicaid Services updates. Hybrid models blend all three to hedge geopolitical or regulatory shifts, making sourcing strategies more resilient.

Mexico’s Guadalajara-Monterrey corridor benefits from USMCA digital protections and visa pathways that ease nurse licensure reciprocity. Meanwhile, Florida’s domestic-storage law nudges East-Coast providers to Tampa and San Juan facilities. This geographical recalibration signifies a diversification trend that keeps the Healthcare Business Process Outsourcing (BPO) Services market close to end-user care settings.

By Technology Adoption Model: Traditional Models Face AI Disruption

Traditional Lift-and-Shift services retained 52.88% of 2025 revenue because risk-averse hospitals still prioritize proven playbooks. Generative-AI-embedded delivery, growing 11.95% CAGR, pairs large language models with governed prompt frameworks that maintain PHI safeguards. Platform BPaaS contracts blend subscription software with outcome guarantees, particularly attractive to mid-sized community hospitals. Intelligent-automation engagements inject targeted bots into single workflows such as prior authorization, yielding immediate savings without system-wide overhaul.

Sagility’s Nurse Assist platform routes symptom descriptions to scripts that recommend next steps, proving AI can elevate care-experience benchmarks. Vendors that quantify accuracy and regulatory defense will accelerate adoption, raising the technological baseline across the Healthcare BPO market.

Geography Analysis

North America contributed 48.15% of global revenue in 2025 as the region’s complex reimbursement environment required extensive expert support. Hospitals continue to outsource mid-cycle operations to offset chronic staffing gaps. Optum’s leadership reshuffle toward value-based care underscores growth in bundled outsourcing contracts that integrate clinical documentation with network steering. Canada’s drive for pan-Canadian EHR interoperability and Mexico’s rise as nearshore hub extend regional dynamism. The Healthcare BPO market therefore focuses on platform investments and regulatory depth in this geography rather than price competition alone.

Asia-Pacific records the fastest 12.62% CAGR, buoyed by population-health initiatives and digital-health funding in India, China, and Southeast Asia. Indian vendors add nearshore centers in Malaysia and the UAE to meet data-localization clauses. The Philippines expands patient-engagement centers, while China’s private providers lean on domestic BPOs versed in new data-security law requirements. Talent supply remains a draw, yet escalating privacy expectations mean firms must invest in advanced cyber defenses. Consequently, the Healthcare BPO market adapts by distributing centers closer to end-markets and embedding multilingual compliance teams.

Europe maintains steady growth as GDPR limits offshore traffic. Germany and the United Kingdom favor domestic analytics partners able to manage NHS or Krankenkasse standards. Southern European countries modernize claims clearinghouses, outsourcing to regional integrators that understand cross-border reimbursement across the Schengen area. Vendors embed EU Cloud Code of Conduct principles, gaining premium pricing and long-term contracts. The Healthcare BPO market continues to mature through specialized offerings such as e-prescription auditing and outcome measurement aligned with the EU Pharmaceutical Strategy.

Competitive Landscape

The competitive field shows moderate concentration. Accenture, Cognizant, and Optum combine end-to-end portfolios with AI accelerators, defending wallet share. Mid-tier players focus on niches—such as clinical documentation or member engagement—where depth takes precedence over breadth. Private-equity dry powder funds multi-asset roll-ups that standardize processes, as seen in EQT–GeBBS. Valuations near 17 times EBITDA assume double-digit growth from AI-driven labor leverage, propelling platform refreshes across incumbents.

Disruptors such as Sagility Health pitch generative AI nurse-triage and plan an IPO around USD 3 billion valuation on tech leadership. Contract structures are shifting to throughput-based pricing that rewards zero-touch claims completion. Meanwhile, megadeals like Cognizant’s USD 1 billion renewal with UnitedHealth prove incumbents can defend scale when they demonstrate productivity lifts. The Healthcare BPO market thus rewards firms balancing innovation speed with proven compliance.

Strategic moves underscore the race: VisiQuate bought Etyon to enhance autonomous analytics; Huron acquired Eclipse Insights to bolster revenue-cycle consulting; and Harvest Partners invested in Med-Metrix for point-solution depth. Expect further vertical integration that links advisory, platform, and managed services under one cap table, tightening customer lock-in across the Healthcare BPO market.

Healthcare BPO Industry Leaders

Accenture

Genpact

IQVIA

Parexel International Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: VisiQuate acquired Etyon to enhance AI-powered revenue-cycle capabilities, adding advanced automation and predictive analytics for financial operations.

- June 2025: Cognizant secured a USD 1 billion renewal and expansion with UnitedHealth Group focused on AI productivity gains.

- June 2025: Harvest Partners invested in Med-Metrix, signaling PE appetite for specialized revenue-cycle platforms.

- June 2025: Huron agreed to purchase Eclipse Insights, deepening its revenue-cycle consulting bench.

Global Healthcare BPO Market Report Scope

As per the scope, business process outsourcing (BPO) is a process that enables healthcare providers to select the most suited third-party vendors for specific business processes. It allows hospitals and medical professionals to spend their valuable time on patient care over other mundane jobs in the office. The Healthcare BPO Market is Segmented by Service Type (Payer Service (Human Resource Management, Claims Management, Customer Relationship Management (CRM), Operational/Administrative Management, Care Management, Provider Management, Other Payer Services), Provider Service (Patient Enrollment and Strategic Planning, Patient Care Service, Revenue Cycle Management), Pharmaceutical Service (Research and Development, Manufacturing, Non-clinical Service(Supply Chain Management and Logistics, Sales and Marketing Services, Other Non-clinical Services) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD million) for the above segments.

By Service Type

| By Payer Service | Human Resource Management | |

| Claims Management | ||

| Customer Relationship Management (CRM) | ||

| Operational / Administrative Management | ||

| Care Management | ||

| Provider Management | ||

| Other Payer Services | ||

| By Provider Service | Patient Enrollment & Strategic Planning | |

| Patient Care Service | ||

| Revenue Cycle Management | ||

| By Pharmaceutical Service | Research & Development | |

| Manufacturing | ||

| Non-clinical Service | Supply-Chain Management & Logistics | |

| Sales & Marketing Services | ||

| Other Non-clinical Services | ||

By Service Delivery Model

| Onshore |

| Nearshore |

| Offshore |

| Hybrid / Multishore |

By Technology Adoption Model

| Traditional Lift-and-Shift BPO |

| Platform-based BPaaS |

| Intelligent-Automation-led BPO |

| Generative-AI-embedded BPO |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | By Payer Service | Human Resource Management | |

| Claims Management | |||

| Customer Relationship Management (CRM) | |||

| Operational / Administrative Management | |||

| Care Management | |||

| Provider Management | |||

| Other Payer Services | |||

| By Provider Service | Patient Enrollment & Strategic Planning | ||

| Patient Care Service | |||

| Revenue Cycle Management | |||

| By Pharmaceutical Service | Research & Development | ||

| Manufacturing | |||

| Non-clinical Service | Supply-Chain Management & Logistics | ||

| Sales & Marketing Services | |||

| Other Non-clinical Services | |||

| By Service Delivery Model | Onshore | ||

| Nearshore | |||

| Offshore | |||

| Hybrid / Multishore | |||

| By Technology Adoption Model | Traditional Lift-and-Shift BPO | ||

| Platform-based BPaaS | |||

| Intelligent-Automation-led BPO | |||

| Generative-AI-embedded BPO | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the Healthcare BPO market by 2031?

The sector is expected to reach USD 726.78 billion by 2031, expanding at a 10.12% CAGR.

Which segment currently leads payer-side outsourcing?

Claims Management leads with 34.21% revenue share, reflecting its central role in accurate claims adjudication.

Why is nearshore delivery growing faster than offshore delivery?

Nearshore centers meet HIPAA storage rules and enable real-time clinician collaboration, driving a 14.21% CAGR for the model.

How is generative AI changing revenue cycle management?

Peer-reviewed studies show 94% coding accuracy and 75% faster processing, enabling mid-size hospitals to outsource economically.

Which region shows the highest growth outlook?

Asia-Pacific is forecast to grow at 12.62% CAGR thanks to expanding healthcare infrastructure and digital-health adoption.

Page last updated on: