Corporate Compliance Training Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

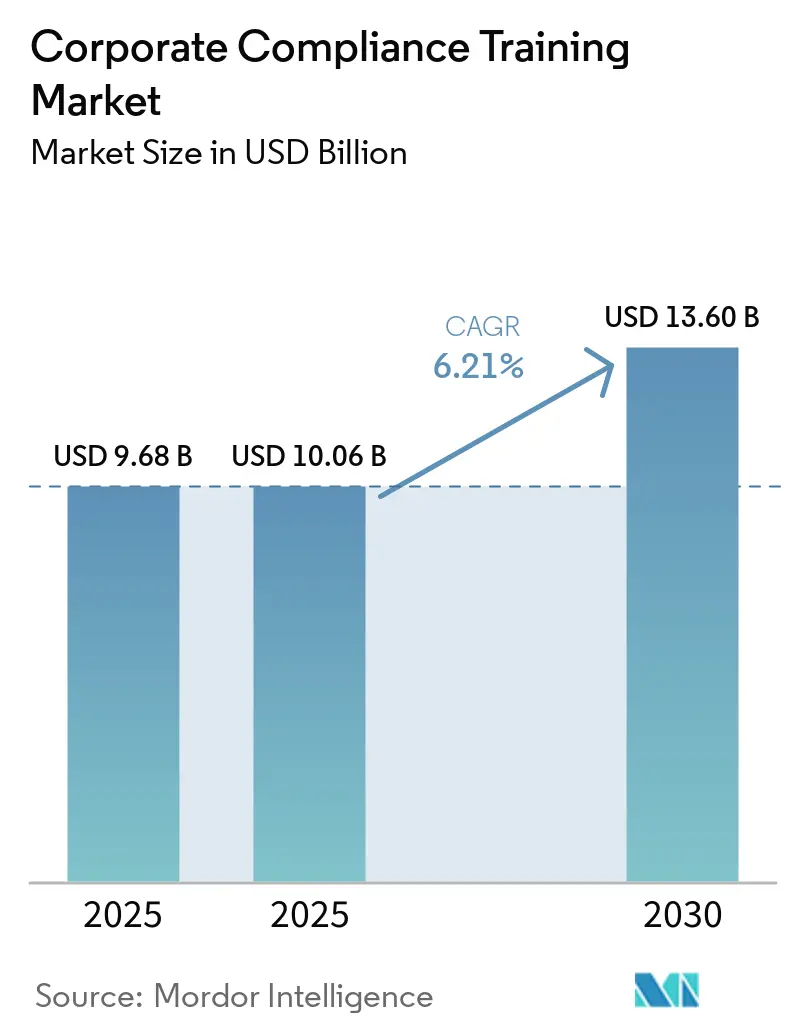

| Market Size (2025) | USD 10.06 Billion |

| Market Size (2030) | USD 13.60 Billion |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

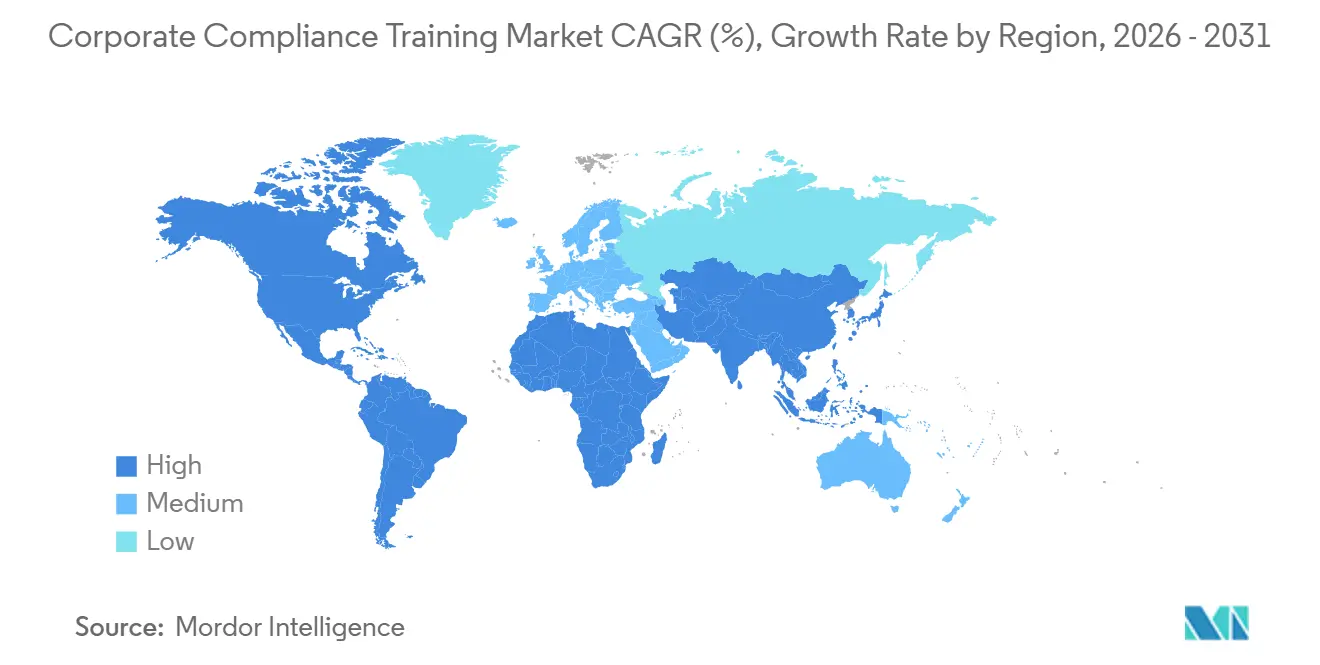

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corporate Compliance Training Market Analysis by Mordor Intelligence

The Corporate Compliance Training Market size is expected to grow from USD 9.68 billion in 2025 to USD 10.06 billion in 2025 and is forecast to reach USD 13.60 billion by 2030 at 6.21% CAGR over 2025-2030.

The Corporate Compliance Training market is moving from checkbox activities to programs that reduce enterprise risk, as penalties rise and reporting timelines for breaches and violations tighten. European data protection authorities issued fines totaling EUR 1.15 billion (USD 1.35 billion) under the GDPR in 2025, and expectations around cross-border data governance now define the enforcement posture [1]European Data Protection Board, “Annual Report 2025,” European Data Protection Board, edpb.europa.eu . California’s privacy regulator increased scrutiny of opt-out signal compliance, data broker registration, and dark patterns in 2025, raising the bar for operational accountability even for mid-sized firms. The United States Securities and Exchange Commission’s four-business-day disclosure requirement for material cybersecurity incidents shifted responsibility from IT to boards, linking incident training and role clarity to securities compliance expectations. These changes push the Corporate Compliance Training market toward evidence-based learning with analytics, microlearning, and blended sessions that can demonstrate understanding and readiness to regulators.

Key Report Takeaways

- By training type, cybersecurity & IT compliance led with 26.37% revenue share in 2025. Cybersecurity & IT compliance is projected to expand at a 10.56% CAGR through 2031.

- By delivery mode, online/digital commanded 72.74% share in 2025. Blended/advanced digital learning is forecast to grow at a 9.53% CAGR through 2031.

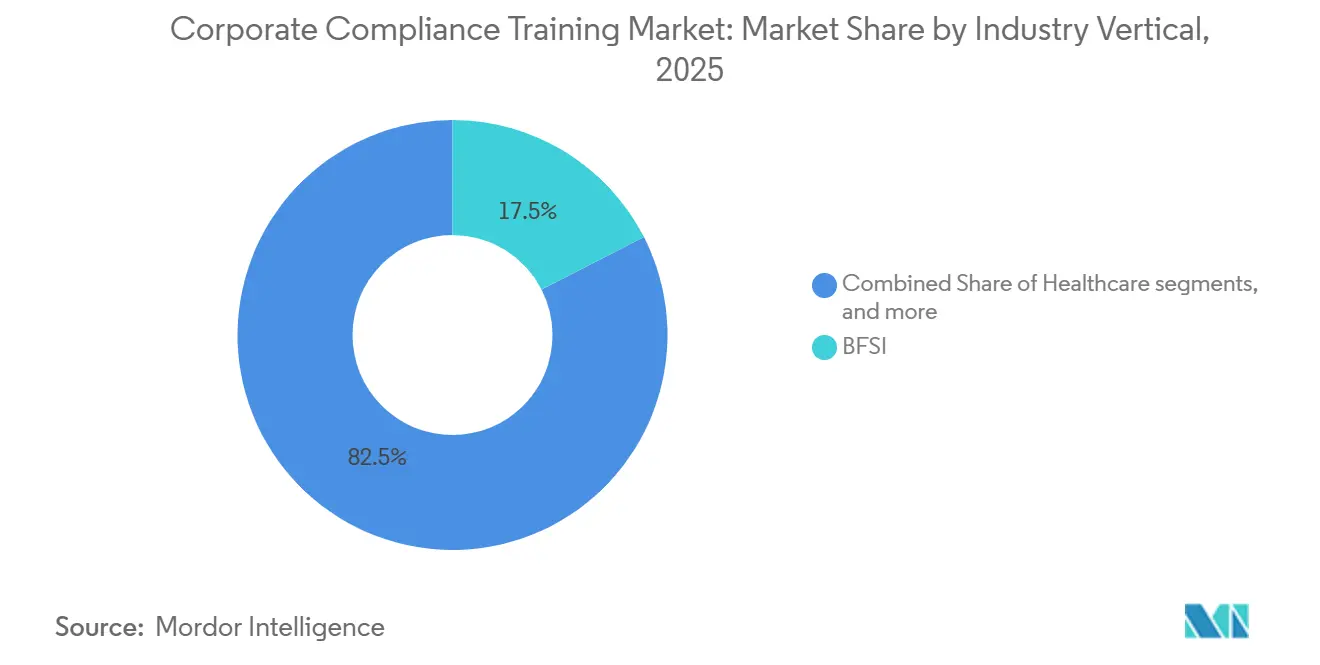

- By industry vertical, banking, financial services & insurance accounted for 17.47% of the market in 2025. Healthcare and BFSI are each expected to grow at a 9.64% CAGR through 2031.

- By organization size, large enterprises represented 58.37% of demand in 2025. Small and medium enterprises are projected to grow at a 8.55% CAGR through 2031.

- By geography, North America accounted for 36.88% in 2025. Asia Pacific is expected to post the fastest growth at a 9.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Corporate Compliance Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter data privacy enforcement worldwide | +1.8% | Global, concentrated in the EU, California, and Brazil | Medium term (2-4 years) |

| Rising cyber threats targeting employees | +2.1% | Global, highest in North America, Asia-Pacific | Short term (≤ 2 years) |

| Mandated anti-harassment training expansions | +0.9% | North America (state-level), Europe (national) | Medium term (2-4 years) |

| ESG reporting & supply-chain due diligence | +1.1% | EU (CSRD, LkSG), spill-over to APAC suppliers | Long term (≥ 4 years) |

| LMS-GRC integration eases audit readiness | +0.7% | Global, early adoption in BFSI, Healthcare | Medium term (2-4 years) |

| Microlearning boosts completion, reduces risk | +0.6% | Global, strongest in SMEs, digital-native sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Data Privacy Enforcement Worldwide

Supervisory action accelerated in 2025 and 2026, which redefined how the Corporate Compliance Training market prioritizes data protection programs. European data protection authorities imposed fines totaling EUR 1.15 billion (USD 1.35 billion) in 2025, and cross-border enforcement highlighted the consequences of weak transfer controls. California’s privacy regulator reported rising complaint volumes and formed a multistate collaboration that coordinated enforcement expectations across jurisdictions, including a focus on Global Privacy Control signals and data broker obligations. A 2025 multistate sweep in the United States specifically examined failure to honor opt-out preference signals, elevating technical compliance as a frontline training topic for data controllers and processors. These developments reward programs that teach frontline teams how to recognize privacy design gaps and how to escalate suspected violations before they become reportable events [2]California Privacy Protection Agency, “California Finalizes Regulations to Strengthen Consumers’ Privacy,” California Privacy Protection Agency, cppa.ca.gov . In France, the national authority continued to invest in practitioner education through updated GDPR training resources that help close knowledge gaps that fines alone cannot address. As oversight becomes more data-driven, the Corporate Compliance Training market is shifting toward content that blends legal interpretation with hands-on workflows for consent management, data subject requests, and vendor due diligence.

Rising Cyber Threats Targeting Employees

Cybersecurity governance has shifted from operational risk to securities disclosure risk in the United States, reshaping program design across the Corporate Compliance Training market. The SEC’s four-business-day incident disclosure requirement shifted accountability to the board level, so incident playbooks now emphasize role-specific training on materiality judgments and escalation. Vendors also pivoted to integrate live threat telemetry with employee simulations, as shown by KnowBe4’s acquisition of Egress to tie adaptive email defenses to awareness training. Risk management teams are folding this telemetry into targeted refresher content that reflects actual phishing patterns rather than generic templates. Japan’s emphasis on whistleblowing and psychological safety is supporting early-warning systems for both cyber and ethics violations, which require recurring employee education on safe reporting and non-retaliation norms. Financial services regulators in the United States also proposed risk-based, ongoing training as a pillar of AML and CFT programs in 2026. That proposal explicitly encouraged the use of AI and machine learning, which aligns the training cadence with real-time monitoring needs. As cyber threats test human judgment first, the Corporate Compliance Training market is prioritizing behavioral reinforcement over one-time annual courses.

Mandated Anti-Harassment Training Expansions

State and city rules in the United States expanded the scope of mandatory training, increasing demand for localized content in the Corporate Compliance Training market. Illinois requires annual sexual harassment prevention training for all employees, whereas neighboring states do not mandate it for all roles. Chicago added a bystander intervention requirement to its three-hour annual training requirement for city employers, creating obligations beyond the state mandate for organizations with a Chicago workforce. New York State and New York City require interactive training and extend coverage to certain contractors, which expands administrative tasks for gig-enabled operating models [3]American Society of Employers, “Harassment Training Requirements by Jurisdiction,” ASE, aseonline.org . Vendors responded by releasing jurisdiction-specific modules in 2026 that reflect distinct definitions, thresholds, and case law, with new harassment prevention content mapped to state- and city-specific nuances. Program leaders are adding role-play, scenario practice, and bystander intervention techniques to improve recall and on-the-job response quality. This direction favors blended and microlearning paths that keep content fresh without sacrificing local compliance accuracy in the Corporate Compliance Training market.

ESG Reporting & Supply Chain Due Diligence

Sustainability reporting and supply chain due diligence rules are turning voluntary statements into auditable obligations, thereby increasing the breadth of the Corporate Compliance Training curriculum. Germany’s supply chain due diligence regime covers larger employers. It extends attention to indirect suppliers when substantiated risks are present, thereby raising training needs for procurement, legal, and supplier management teams across tiers. The European Corporate Sustainability Reporting Directive adds structured disclosure across environmental and social metrics, so firms are building curricula that document competence and controls alongside emissions and diversity data. China’s 2025 guidance from 15 ministries positioned compliance as a competitive advantage for SMEs and directed companies to build systems across labor, quality, safety, IP, data, and supply chain areas, thereby increasing training demand across APAC supplier networks. Buyers in Europe are already extending due diligence expectations to APAC sub-tiers, reshaping supplier onboarding and verification curricula for exporters. The Corporate Compliance Training market is therefore adding ESG and supplier ethics modules to legacy code of conduct and anti-bribery programs to keep pace with audit requirements.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Training fatigue lowers learner engagement | -0.8% | Global, acute in mature markets with layered mandates | Short term (≤ 2 years) |

| Fragmented global regulations hinder standardization | -1.2% | Global, most severe for multinational corporations | Long term (≥ 4 years) |

| Budget constraints in SMEs | -0.6% | Global, most acute in developing markets and post-pandemic recovery | Medium term (2-4 years) |

| Poor localization undermines policy alignment | -0.4% | Emerging markets in Asia-Pacific, Latin America, and MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Training Fatigue Lowers Learner Engagement

Time pressure and cognitive load remain barriers that temper gains in the Corporate Compliance Training market. Many employees and learning leaders cite workload as a top reason for low training participation, which weakens the link between completion and behavior change when content is delivered in long blocks. In multi-jurisdictional environments, layered mandates can expand seat time and trigger disengagement when content overlaps but cannot be consolidated due to rule differences. This environment elevates microlearning and blended formats that reduce friction while preserving coverage of statutory elements. Japan’s training practices emphasize psychological safety and values-based discussions, which help counter cynicism that can arise when training is perceived as performative rather than protective. Program owners are therefore aligning cadence and relevance more precisely to business rhythms to maintain engagement throughout the year.

Fragmented Global Regulations Hinder Standardization

Divergent rules across privacy, AI, and financial crime create parallel compliance tracks that resist a single curriculum, increasing costs and complexity in the Corporate Compliance Training market. State privacy regimes in the United States continue to evolve, with different enforcement emphases, including opt-out signal treatment and data broker registration, which require state-specific training paths. Financial services proposals in 2026 introduced explicit expectations for program establishment and maintenance, which differ in construction from those in other jurisdictions and complicate one-size-fits-all training for cross-border banks. EU guidance interacts with digital market rules in ways that large platforms must interpret and implement locally, adding depth to training on advertising transparency and recommender controls. China’s SME-focused guidance frames compliance as an opportunity and market access, which contrasts with the United States' risk-first practices and requires content that recognizes national business culture. Vendors are expanding localization by tailoring language and scenarios, including new EU AI Act employee guides to reflect 2026 deadlines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Training Type: Cybersecurity Dominates, but ESG Accelerates

Cybersecurity & IT Compliance captured 26.37% of the Corporate Compliance Training market share in 2025, reflecting the shift to board-level accountability for cyber incidents and heightened AML and CFT expectations for digital assets and suspicious activity response. The segment is projected to expand at a 10.56% CAGR through 2031, supported by proposals that formalize ongoing, risk-based training and encourage the careful use of AI and machine learning to improve program effectiveness. The Corporate Compliance Training market increasingly treats phishing simulation, role-specific breach escalation, and secure data handling as recurring competencies rather than annual refresh topics [4]The CPA Journal Editorial Staff, “The SEC Finalizes Rule on Cybersecurity Disclosures,” The CPA Journal, cpajournal.com . Vendors are pairing adaptive threat intelligence with training that responds to active attack campaigns in real time. Data Protection & Privacy programs are growing amid state and EU enforcement, as teams need operational skills to handle opt-out signals, privacy requests, and data broker obligations. Workplace Safety programs gained urgency with national emphasis actions in manufacturing, which require documentation of both training completion and real-world competency. Anti-harassment content aligns with city and state standards, including bystander techniques and supervisor responsibilities.

ESG, Sustainability & Responsible Business is the fastest-rising non-cybersecurity area as environmental, social, and supplier due diligence disclosures become auditable and traceable to training and controls. The Corporate Compliance Training market is investing in modules for supply chain risk identification, grievance handling, and remediation planning in response to European rules that extend responsibility across complex vendor networks. Procurement, logistics, and operations teams require training on supplier onboarding, document collection, and monitoring expectations that match buyer demands. China’s guidance for SMEs reinforced that compliance maturity is now part of competitive positioning, extending ESG-linked training to mid-market exporters. The Corporate Compliance Training market is also aligning ethics and anti-bribery content with sustainability themes, so that frontline actions support both legal and customer requirements. Over the forecast period, cross-functional ESG literacy will be a differentiator in regulated supply chains serving European buyers.

By Delivery Mode: Blended Learning Emerges from Digital’s Shadow

Online/Digital delivery commanded 72.74% of demand in 2025, anchored by the ability to produce audit-ready records and to scale instruction across distributed workforces. Blended and advanced digital learning is forecast to be the fastest-growing format, with a 9.53% CAGR through 2031, as organizations add live practice for topics where interpersonal dynamics and judgment calls drive outcomes. The Corporate Compliance Training market is converging on a combined model in which asynchronous modules establish baselines, while live sessions focus on role-play, escalation drills, and nuanced scenario analysis. Financial services expectations for ongoing AML and CFT training indicate that periodic refreshers alone cannot sustain vigilance. Microlearning is also boosting completion rates while preserving knowledge checks, which makes it easier to maintain records that stand up to enforcement review. This combination is pushing buyers to platforms that manage live and digital content within a unified learner record.

Vendors emphasize orchestration of ILT, vILT, and self-paced learning to reflect how risk owners prefer to learn and how auditors expect evidence to be structured. Core features now include SSO, automated enrollments, recertification scheduling, reporting templates, and deep integrations with HRIS and case management systems. Platforms also promote streamlined administration, helping SMEs match the cadence and documentation quality of large enterprise programs without adding headcount. In high-risk contexts such as machine safety, live demonstrations remain necessary to affirm competency, which shapes blended program design. Content roadmaps in 2025 and 2026 increased focus on jurisdiction-tailored modules, which help centralized teams deliver standardized experiences that still comply with local law. Over the forecast window, the Corporate Compliance Training market will reward vendors that make blended delivery simple, measurable, and auditable at scale.

By Industry Vertical: Regulated Sectors Pull Ahead

Banking, Financial Services & Insurance held 17.47% of demand in 2025, and both BFSI and Healthcare are projected to post the fastest growth at 9.64% through 2031. Financial services training is expanding in response to proposed changes that mandate risk-based, ongoing education as a pillar of AML and CFT programs and endorse the use of advanced analytics under appropriate controls. Healthcare training demand reflects renewed enforcement of manufacturing quality expectations, where inspection findings called out training gaps and documentation that failed to confirm competence. The Corporate Compliance Training market also sees steady pull from cross-industry privacy, security, and anti-harassment obligations that extend to third-party contractors and franchise workforces. In both BFSI and Healthcare, governance teams are aligning LMS data with GRC dashboards to connect training to control effectiveness.

Manufacturing and industrial companies face heightened scrutiny from safety regulators, which drives role-specific training on machine guarding, lockout/tagout, and incident reporting. Information Technology and Telecom firms are preparing for AI-related governance obligations, and buyers are showing growing interest in modules that cover human oversight and transparency aligned with Europe’s AI framework. Government and public sector buyers look for platforms with documented security compliance and alignment with federal standards, which favors vendors with a long history of supporting agency requirements. Retail, consumer goods, and food and beverage prioritize front-line training that is short, mobile-friendly, and localized, especially where cities set standards that exceed state floors. Transportation and logistics require training that aligns with hours-of-service and hazardous materials rules, as well as supplier due diligence, where European buyers require documented ethics compliance. Across sectors, the Corporate Compliance Training market is trending toward role-specific pathways that align with regulatory artifacts and inspection checklists.

By Organization Size: SMEs Close the Gap

Large Enterprises accounted for 58.37% of demand in 2025, consistent with thresholds that place heavier obligations on bigger employers. European supply chain due diligence rules focus first on larger entities and require attention to indirect suppliers where risk is substantiated, thereby elevating governance and training spend in large firms. The Corporate Compliance Training market also reflects the phasing in of sustainability reporting that emphasizes program documentation and audit evidence. Large multinationals tend to centralize content and delivery on enterprise LMS platforms while delegating local customization to in-country teams. Vendors offer multilingual authoring, approval workflows, and data residency options for global rollouts. In parallel, privacy enforcement in large United States states reinforces the need to track training completion and comprehension for roles that handle personal data.

SMEs are projected to grow fastest at an 8.55% CAGR as cloud platforms reduce setup complexity and automate recurring tasks. Providers highlight a single login, learner records, automated assignments, and turnkey reporting to reduce administrative time for teams without dedicated L&D staff. Subscription models now bundle privacy, cybersecurity, and anti-harassment content with policy templates, compressing time-to-value for smaller firms. China’s 2025 guidance explicitly targeted SMEs and called for comprehensive compliance systems in data security, governance, and supply chain, expanding the addressable base for training platforms in APAC. As SMEs build maturity, they adopt microlearning and blended approaches that deliver steady reinforcement without taking staff offline for extended periods. Over time, the Corporate Compliance Training market will reflect a narrower capability gap as simplified tooling and modular content bring SME programs closer to enterprise standards.

Geography Analysis

North America held 36.88% of the Corporate Compliance Training market share in 2025. The region’s position rests on several forces that continue in 2026, including enforcement escalations that add pressure on programs to demonstrate effectiveness rather than mere completion. The SEC’s cyber disclosure rule made material incident training a board-relevant requirement and raised the bar for documenting readiness and escalation pathways. State privacy regulators pursued actions on opt-out signal compliance and data broker registration, which expanded training content for marketing, IT, and customer operations teams. Mandated anti-harassment training across multiple states and cities added jurisdiction-specific modules, increasing administrative tasks for national employers. Buyers in North America also show a strong preference for microlearning to maintain engagement and reduce productivity impacts. As these patterns persist, the Corporate Compliance Training market in the United States and Canada will continue to favor platforms that centralize control while enabling local tailoring.

Asia Pacific is the fastest-growing region, with a projected 9.22% CAGR through 2031. China’s 15-ministry directive positioned compliance maturity as a competitive advantage for SMEs and outlined a broad scope of required systems, which drive training needs across governance, data, quality, and supply chain functions. Japan’s emphasis on whistleblower systems and psychological safety has increased interest in training that supports internal reporting and respectful communications. The Corporate Compliance Training market in APAC is also benefiting from the spread of microlearning and mobile delivery, which suits frontline and distributed workforces. Suppliers connected to European buyers are expanding ESG and due diligence training as part of onboarding and ongoing verification, which pulls new users onto digital platforms. As APAC regulators publish guidance and buyers embed audit expectations, the Corporate Compliance Training market gains momentum through both top-down and customer-driven requirements.

Europe blends centralized rulemaking with member-state enforcement variation, which shapes local demand patterns. GDPR fines in 2025 demonstrated the scale of the risk for firms that mismanage cross-border data or ignore supervisory guidance, which renewed interest in multilingual, scenario-based privacy instruction. National safety, harassment, and sector regulations continue to add content variants that require jurisdictional accuracy. France invests in public education through updated GDPR training, which supports smaller firms seeking to improve compliance literacy. European sustainability and supply chain rules are expanding demand for ESG and due diligence training, especially in export-intensive markets with complex vendor networks. The Corporate Compliance Training market in Europe is therefore broadening beyond privacy and anti-bribery into sustainable operations and supplier oversight content that aligns with audit expectations.

Competitive Landscape

The Corporate Compliance Training market remains moderately fragmented, and leaders compete by moving beyond content catalogs to analytics, role-specific personalization, and integration with GRC systems. Vendors expanded capabilities during 2025 and 2026 that demonstrate training effectiveness with dashboards on engagement, knowledge checks, and retention, which helps executives link programs to control outcomes. NAVEX also attracted strategic investors in 2025 that backed continued product innovation and global expansion, reflecting buyer demand for unified platforms. Skillsoft reported strong uptake of AI-enabled practice tools and expanded compliance curricula, signaling an industry shift from static modules to interactive learning paths. These moves indicate that leadership now depends on measurable impact and the ability to adapt content rapidly when rules change.

Product roadmaps across leaders converged on AI native authoring, conversational practice, and blended delivery that joins vILT with asynchronous modules. Cornerstone offers advanced AI-driven learner and admin experiences that support skills-based transformations aligned with compliance requirements. KnowBe4’s acquisition of Egress integrated live threat intelligence with employee simulations to tailor phishing scenarios to each organization's actual risk. NAVEX rolled out Training Insights to clarify where learners struggle, which enables targeted remediation before issues escalate to incidents. The Corporate Compliance Training market is also adapting to federal and public-sector requirements through dedicated product lines and security-focused positioning.

Competition also plays out in delivery and administration convenience, which matters for SMEs and distributed enterprises. Litmos and Bridge emphasize unified learner records, automated assignments, reminders, and broad integrations that reduce administration time and error risk. These capabilities help smaller buyers meet documentation expectations common in larger firms, such as SSO controls, automated provisioning, and standardized reports for auditors. Skillsoft’s 2026 roadmap added jurisdiction-specific harassment prevention modules and safety content aligned with current rules, demonstrating the pace at which top vendors can localize at scale. Udemy expanded certification pathways, including Microsoft exams, that combine compliance adjacent technical skills with governance relevant credentials for enterprise learners. As buyers consolidate spend, the Corporate Compliance Training market will favor vendors that prove risk reduction with data, not only content breadth.

Corporate Compliance Training Industry Leaders

Skillsoft

NAVEX Global

SAI360

Cornerstone OnDemand

SAP Litmos

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The U.S. Financial Crimes Enforcement Network and federal banking agencies proposed a comprehensive overhaul of AML/CFT program requirements, mandating risk-based, ongoing employee training and encouraging the use of AI and blockchain monitoring, subject to appropriate controls.

- April 2026: Udemy expanded its end-to-end certification journey with Microsoft, enabling learners to purchase more than 50 certification exam vouchers on the platform.

- December 2025: NAVEX launched Training Insights to give compliance leaders dashboards for engagement, scoring, and knowledge retention, enabling targeted remediation and audit-ready reporting.

- February 2025: NAVEX announced a strategic partnership with BDO to integrate NAVEX One’s GRC platform with BDO’s client services to standardize processes and reduce risk.

Global Corporate Compliance Training Market Report Scope

| Data Protection & Privacy |

| Workplace Safety & OSHA Compliance |

| Anti-Harassment, DEI & Workplace Conduct |

| Anti-Bribery & Corruption |

| Ethics & Code of Conduct |

| Cybersecurity & IT Compliance |

| ESG, Sustainability & Responsible Business |

| Industry-Specific Compliance |

| Online / Digital |

| Classroom / On-Site |

| Blended Learning |

| Banking, Financial Services & Insurance (BFSI) |

| Healthcare & Life Sciences |

| Manufacturing & Industrial |

| Energy & Utilities |

| Information Technology & Telecom |

| Government & Public Sector |

| Retail & Consumer Goods |

| Food & Beverage |

| Transportation & Logistics |

| Other Industry Verticals |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Training Type | Data Protection & Privacy | |

| Workplace Safety & OSHA Compliance | ||

| Anti-Harassment, DEI & Workplace Conduct | ||

| Anti-Bribery & Corruption | ||

| Ethics & Code of Conduct | ||

| Cybersecurity & IT Compliance | ||

| ESG, Sustainability & Responsible Business | ||

| Industry-Specific Compliance | ||

| By Delivery Mode | Online / Digital | |

| Classroom / On-Site | ||

| Blended Learning | ||

| By Industry Vertical | Banking, Financial Services & Insurance (BFSI) | |

| Healthcare & Life Sciences | ||

| Manufacturing & Industrial | ||

| Energy & Utilities | ||

| Information Technology & Telecom | ||

| Government & Public Sector | ||

| Retail & Consumer Goods | ||

| Food & Beverage | ||

| Transportation & Logistics | ||

| Other Industry Verticals | ||

| By Organization Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the Corporate Compliance Training market growth outlook to 2031?

The Corporate Compliance Training market size is forecast to reach USD 13.60 billion by 2031 at a 6.21% CAGR from 2026 to 2031.

Which training type leads growth within the Corporate Compliance Training market?

Cybersecurity & IT Compliance leads with a 26.37% share in 2025 and is projected to grow at a 10.56% CAGR through 2031, reflecting board level focus on incident readiness and ongoing AML/CFT training expectations.

Which delivery model will expand fastest in the Corporate Compliance Training market?

Blended and advanced digital learning is set to grow at a 9.53% CAGR as organizations combine microlearning with live role play to reinforce judgment skills and produce audit ready records.

Which regions will shape demand in the Corporate Compliance Training market?

North America holds the largest share at 36.88% due to enforcement intensity, while Asia Pacific is the fastest growing region at a projected 9.22% CAGR as regulators and buyers expand due diligence requirements.

How are vendors differentiating in the Corporate Compliance Training market?

Leaders are moving beyond content catalogs to analytics, AI native authoring, blended delivery, and LMS GRC integration, with examples including NAVEX Training Insights, Skillsoft CAISY enabled content, and Cornerstone’s AI Galaxy.

What are the main barriers to effectiveness in the Corporate Compliance Training market?

The biggest headwinds are training fatigue and rule fragmentation, which vendors address through microlearning, localization, and automated administration features aligned with evolving AML, privacy, and ESG obligations.

Page last updated on: