Health Intelligent Virtual Assistant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

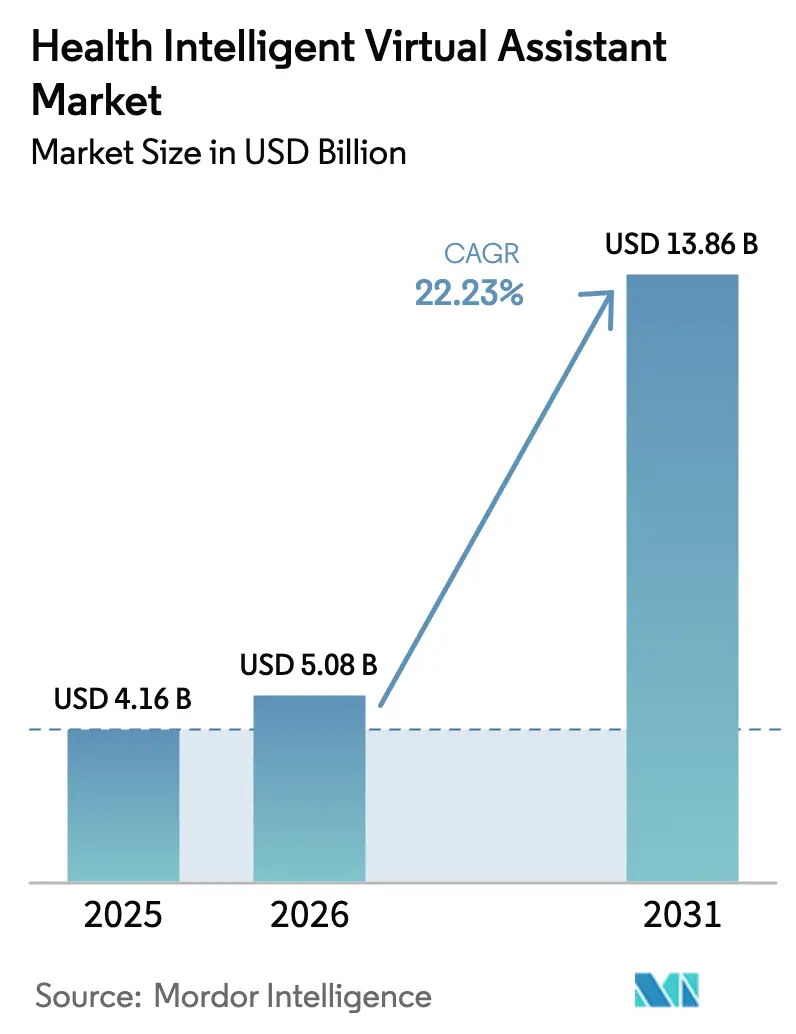

| Market Size (2026) | USD 5.08 Billion |

| Market Size (2031) | USD 13.86 Billion |

| Growth Rate (2026 - 2031) | 22.23% CAGR |

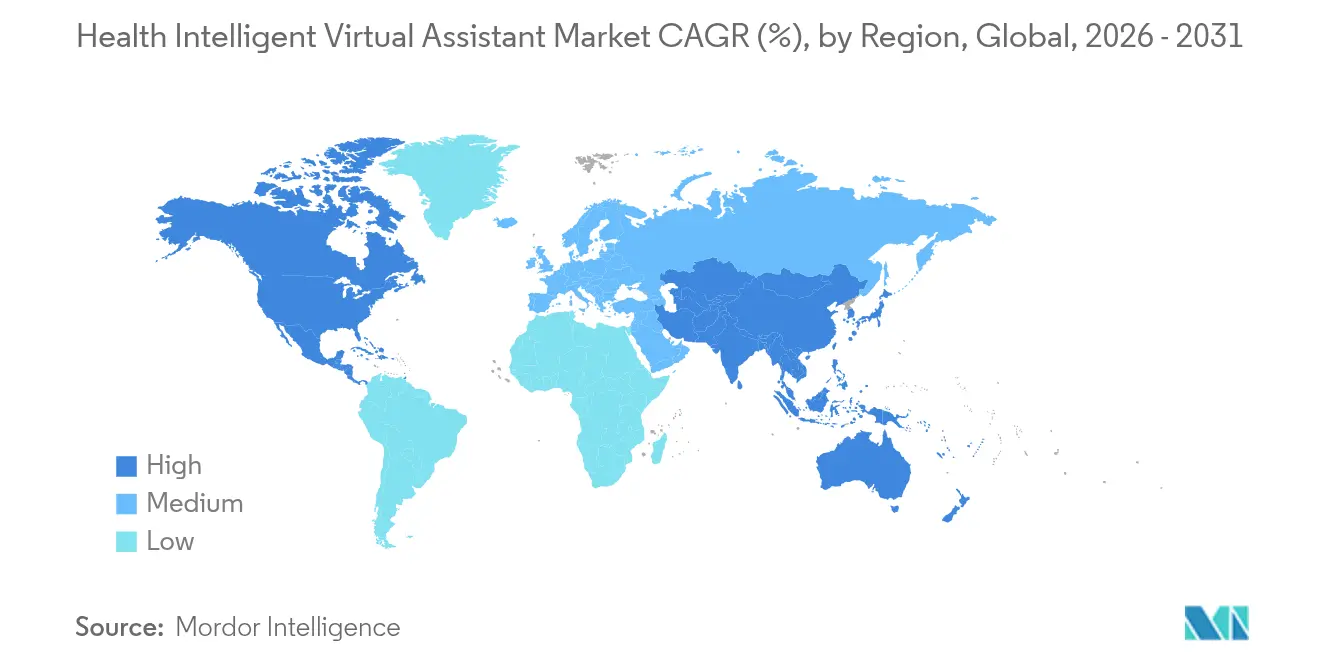

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

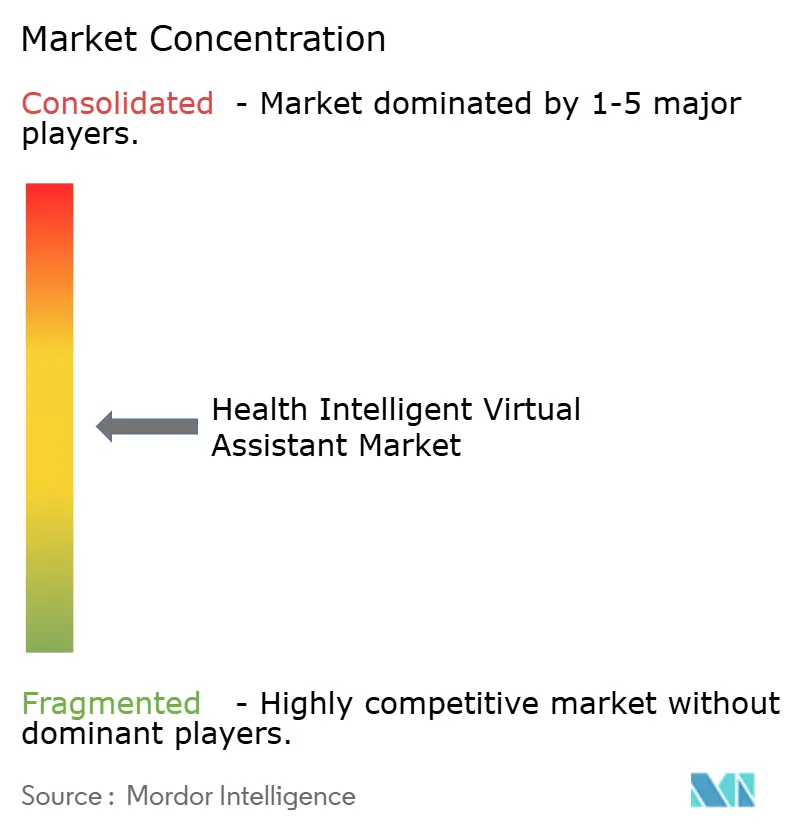

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Health Intelligent Virtual Assistant Market Analysis by Mordor Intelligence

The Health Intelligent Virtual Assistant market size is expected to grow from USD 4.16 billion in 2025 to USD 5.08 billion in 2026 and is forecast to reach USD 13.86 billion by 2031 at 22.23% CAGR over 2026-2031. Demand acceleration comes from large language model breakthroughs, clearer device regulations, and workforce shortages that raise the urgency for automated clinical and administrative tasks. Early adopters have documented cost savings above 90% in high-volume workflows, giving the market clear financial proof points. Voice recognition remains the workhorse interface, yet rapid investments in multimodal emotion-recognition systems point to a broader shift toward empathetic patient engagement. Momentum is most visible in North America, but Asia-Pacific is quickly closing the gap through state-sponsored digital health programs and multilingual AI platforms that unlock non-English patient populations.

Key Report Takeaways

- By technology, voice recognition led with 43.10% revenue share of the Health Intelligent Virtual Assistant market in 2025, while multimodal and emotion-AI interfaces are expanding at an 17.65% CAGR through 2031.

- By product, chatbots held 57.80% of the Health Intelligent Virtual Assistant market share in 2025, whereas smart speakers are growing at a 16.1% CAGR to 2031.

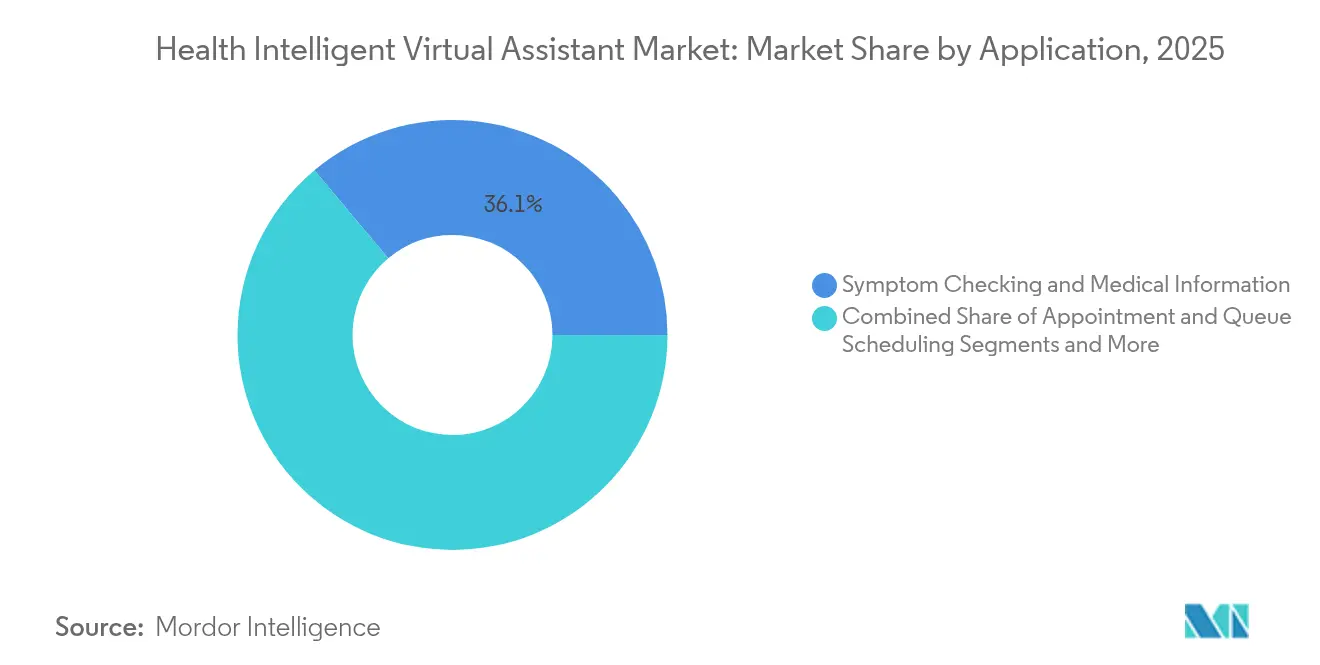

- By application, symptom checking and medical information accounted for 36.10% share of the Health Intelligent Virtual Assistant market size in 2025; medication and care-plan reminders are projected to grow at 19.3% CAGR between 2026 and 2031.

- By end user, healthcare providers captured 52.10% of the Health Intelligent Virtual Assistant market share in 2025, while the patients and caregivers segment is advancing at a 18.9% CAGR through 2031.

- By geography, North America commanded 41.95% share of the Health Intelligent Virtual Assistant market in 2025, yet Asia-Pacific is on track for the fastest 15.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Health Intelligent Virtual Assistant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of AI-enabled care workflows | +6.2% | Global with early gains in North America and Europe | Medium term (2–4 years) |

| Escalating demand for patient-centric digital front doors | +5.8% | North America and EU expanding to Asia-Pacific | Short term (≤2 years) |

| Cost-containment pressure on providers and payers | +4.1% | Global | Long term (≥4 years) |

| Proliferation of connected health and IoT devices | +3.7% | Asia-Pacific core with spill-over to MEA | Medium term (2–4 years) |

| Multilingual LLM integration unlocking non-English markets | +2.9% | Asia-Pacific, MEA, Latin America | Long term (≥4 years) |

| Value-based reimbursement rewarding virtual triage | +2.1% | North America expanding to Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of AI-enabled care workflows

Health systems are embedding virtual assistants into documentation, triage, and care coordination. Providence Health reported a 30% gain in triage efficiency and a meaningful drop in physician message load, illustrating operational relief and reduced burnout[2]Becker’s Hospital Review, “Providence Health’s Grace Chatbot Cuts Physician Messages,” beckershospitalreview.com. Emergency departments adopt similar tools to route patients to the appropriate setting, reducing avoidable visits and freeing scarce specialist capacity. The Health Intelligent Virtual Assistant market therefore benefits from a clear alignment between ROI and clinical quality gains. Vendor roadmaps now prioritize deeper EHR integration to minimize manual clicks and to deliver structured notes directly into health records. These workflow improvements are reshaping staffing models by allowing nurses to supervise multiple AI-guided interactions concurrently.

Escalating demand for patient-centric digital front doors

Consumers expect frictionless access to scheduling, symptom checks, and claims information. OSF HealthCare saved USD 2.4 million within one year after deploying an AI assistant that deflected routine calls and enabled self-service. Virtual assistants now complete tasks such as insurance verification and benefit eligibility, which further simplifies patient onboarding. The Health Intelligent Virtual Assistant market thus capitalizes on a broader pivot toward platform-level engagement where the assistant becomes the brand’s primary interface. Younger demographics reward providers that offer conversational access over legacy voice menus, accelerating competitive replacement cycles for dated call-center technology.

Cost-containment pressure on providers and payers

Non-clinical administration costs in the United States exceed USD 600 billion annually. AI voice agents now automate up to 70% of scheduling calls and claims inquiries, demonstrating material savings potential. Providers also cite fewer denied claims because virtual assistants capture more complete documentation at the point of service. Savings extend to decreased overtime, better resource utilization, and lower readmission penalties. The Health Intelligent Virtual Assistant market therefore gains from both expense reduction and revenue capture through cleaner coding and faster reimbursements.

Proliferation of connected health and IoT devices

Asia-Pacific health systems integrate smart speakers, wearables, and home monitoring hubs with virtual assistants that interpret real-time vitals and behavioral cues. These devices push structured data into clinical dashboards and trigger proactive outreach when anomalies arise. The Health Intelligent Virtual Assistant market benefits since each additional device increases conversational touchpoints and expands the data lake required for predictive analytics. Hospitals now pilot fall-detection sensors linked to voice assistants that call nurses automatically, reducing injury incidence and associated costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy and cybersecurity risks | -3.8% | Global with emphasis on EU and North America | Short term (≤2 years) |

| Limited clinician trust and workflow mis-alignment | -2.9% | Global | Medium term (2–4 years) |

| Algorithmic bias jeopardizing clinical safety | -2.1% | Global | Long term (≥4 years) |

| Regulatory uncertainty around AI explainability mandates | -1.7% | Global with varied regional impact | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Data privacy and cybersecurity risks

Virtual assistants need broad access to medical records, yet that same data makes them prime targets. The EU AI Act classifies most healthcare AI as high risk, imposing strict governance and transparency obligations that raise compliance costs. Multicloud deployments add complexity because every interface becomes a new attack surface. Health systems respond with zero-trust architectures and privacy-enhancing technologies, but those upgrades slow procurement cycles and lengthen deployment timelines for the Health Intelligent Virtual Assistant market.

Limited clinician trust and workflow mis-alignment

While top algorithms now outperform the average clinician in differential diagnosis accuracy, physicians remain wary of black-box recommendations. A comparative study found patient satisfaction scores lower for AI interactions than for physician consults, underscoring the importance of human empathy. Implementations that ignore local protocols often generate duplicate tasks, causing frustration rather than relief. Vendors now embed feedback loops that allow clinicians to correct AI outputs in real time, gradually improving trust yet extending rollout durations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Voice recognition leads yet multimodal analytics rise

Voice recognition commanded 43.10% of Health Intelligent Virtual Assistant market revenue in 2025. Hospitals prefer hands-free dictation that pushes structured notes into electronic records, freeing clinicians from keyboards. Epic paired with Nuance Dragon Medical to add ambient scribing, which cut after-hours documentation by 75%. Growth continues as vendors augment models with specialty vocabularies for radiology and oncology. Advances in diarization separate multiple speakers, enabling accurate transcripts of group rounds.

Multimodal emotion-recognition interfaces forecast an 17.65% CAGR through 2031, making them the fastest technology line. These systems blend voice tone, facial micro-expressions, and behavioral patterns to flag depression or cognitive decline earlier than traditional tools. Emerging vocal biomarker research links pitch and cadence signatures with metabolic and neurological disorders, moving virtual assistants from conversational aids to diagnostic collaborators. The Health Intelligent Virtual Assistant market size for multimodal solutions will therefore expand as payers reimburse remote monitoring that reduces hospital readmissions.

By Product: Chatbots dominate while smart speakers accelerate

Chatbots secured 57.80% market share in 2025 through simple text or voice workflows that resolve scheduling, refills, and claim status. Their low implementation cost and cloud delivery make them the default entry for most providers. AI updates now personalize responses with context from prior chats, raising completion rates for complex tasks. The Health Intelligent Virtual Assistant market benefits because each successful transaction reinforces patient confidence in digital tools.

Smart speakers present the highest 16.1% CAGR. Hospitals mount voice units in patient rooms for meal orders, nurse calls, and environmental controls, generating immediate staff time savings. Hippocratic AI’s Polaris platform layers multi-model safety checks that prevent hallucinations and provide verified medication guidance. Vendors also integrate fall-detection microphones and respiratory sound analysis that alert care teams. The Health Intelligent Virtual Assistant market size for smart speakers will grow as infection-control policies favor touchless devices and as reimbursement broadens for at-home monitoring.

By Application: Adherence support outpaces symptom checking

Symptom checking and medical information retained 36.10% share in 2025 as consumers used chatbots to assess fever or rash before clinic visits. The domain fuels triage engines that channel low-acuity cases toward self-care content, easing clinician workload. Yet medication and care-plan reminders are forecast for a 19.3% CAGR, the highest among applications. AI prompts now adjust timing based on real-time glucose or blood pressure data, boosting chronic disease adherence. For diabetes, virtual assistants that cross-reference glucometer feeds can suggest insulin dose changes with accuracy near endocrinologist levels.

The Health Intelligent Virtual Assistant market share for adherence solutions climbs as payers link reimbursement to outcome metrics. Behavioral nudges delivered via text, voice, or smart speaker improve refill rates and decrease costly complications. Platforms also offer multilingual scripts that respect cultural norms, which widens patient reach in diverse regions.

By End User: Provider dominance meets patient-led expansion

Healthcare providers held 52.10% of Health Intelligent Virtual Assistant market revenue in 2025. Hospitals deploy assistants for documentation relief, pre-visit questionnaires, and discharge education. Intermountain Health noted a 30% drop in call-center volumes after rolling out an Epic-integrated voice agent, freeing staff for higher acuity needs. Payers and life-science firms use similar tools for member support and trial recruitment.

Patients and caregivers represent the fastest 18.9% CAGR. Direct-to-consumer apps give families round-the-clock coaching for asthma, hypertension, or mental health. Subscription models bundle virtual assistant chats, wearable data dashboards, and pharmacy delivery. The Health Intelligent Virtual Assistant industry therefore sees new revenue pools outside institutional procurement cycles, especially in markets where out-of-pocket spending is high and where telehealth regulations now permit AI-only visits for minor conditions.

Geography Analysis

North America led with 41.95% Health Intelligent Virtual Assistant market share in 2025. The FDA has cleared more than 1,000 AI-enabled devices, giving providers regulatory clarity. Providence, OSF, and Intermountain each published ROI cases that validate investment. Venture capital flows remain strong even after wider tech pullbacks, keeping the innovation pipeline full. Privacy scrutiny is rising, so vendors invest in on-premise inference and de-identification to satisfy HIPAA.

Europe follows with steady momentum. The EU AI Act imposes strict risk assessment, yet it also outlines compliance routes that ease procurement anxiety. Providers in Germany and the United Kingdom emphasize multilingual digital front doors for migrant populations, which pushes demand for LLMs fluent in more than 20 languages. Regional funding programs under Digital Europe support startups that design privacy-by-design virtual assistants, aligning commercial goals with policy priorities.

Asia-Pacific records the highest 15.85% CAGR. China’s virtual hospital plans to launch 42 AI doctors in 2025, covering cardiology to dermatology. Over 1 million Chinese clinicians already use AI for imaging and decision support, anchoring a deep dataset for conversational engines. Japan advances remote eldercare, leveraging smart speakers that provide fall detection and medication prompts. India’s National AI Mission funds chatbot pilots in primary care centers, aiming to expand doctor reach in rural zones. Funding volatility remains a risk, as medical AI investment in China dropped from CNY 11.5 billion in 2021 to CNY 2.96 billion in 2023. Still, government mandates for paperless hospitals and multilingual support maintain solid tailwinds for the Health Intelligent Virtual Assistant market.

Competitive Landscape

The market is moderately fragmented. Microsoft, Google, and Amazon leverage hyperscale clouds and pre-trained language models. Microsoft deepened its moat by embedding GPT-4 into Epic, giving 2,950 hospitals a ready-made assistant inside existing workflows. Google links Med-PaLM to its Care Studio interface, providing stepwise reasoning for clinical questions, while Amazon adapts Alexa Smart Properties for hospitals.

Specialists occupy high-growth niches. Hippocratic AI raised USD 141 million and targets voice nurses for chronic care calls. Nuance, now part of Microsoft, pairs its Dragon Medical One with ambient listening that drafts notes in real time. Ada Health focuses on symptom triage through a regulated medical device framework. Sensely integrates insurance cards and benefits checks, positioning itself for payer contracts.

Strategic alliances shape market entry. Cisco’s Webex and Talkdesk both added Epic connectors in 2025 to bring AI voice agents into omnichannel contact centers. Patent filing volume grew 34% per year since 2015, signaling rising barriers to entry. Vendors pursue vertical integration that spans data ingestion, model training, and front-end chat to secure usage data and refine algorithms. The Health Intelligent Virtual Assistant market therefore sees increased merger and acquisition activity as large players buy niche innovators for unique clinical datasets or multimodal assets.

Health Intelligent Virtual Assistant Industry Leaders

Nuance Communications, Inc.

Microsoft Corporation

Amazon Inc.

Infermedica Sp. z o.o.

Sensely, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Zocdoc launched “Zo” voice agent that manages 70% of scheduling calls.

- March 2025: Webex Contact Center integrated with Epic to streamline AI-driven patient outreach.

- February 2025: Talkdesk released new Epic connector for AI virtual assistant deployments.

- January 2025: FDA issued draft guidance for AI medical devices that covers lifecycle monitoring and change control.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the health intelligent virtual assistant market as every AI driven conversational solution, whether voice, text, or multimodal, that supports clinical, administrative, or wellness tasks across provider, payer, and patient touchpoints. The definition includes embedded software in smart speakers, mobile apps, web chatbots, and edge devices that apply natural language processing, machine learning, and secure integration with electronic health records to deliver real-time support.

Scope Exclusions: generic productivity bots not trained on medical data, on-premise voice recognition used only for radiology dictation, and stand-alone speech engines sold without a conversational layer are outside this scope.

Segmentation Overview

- By Technology

- Voice (Speech Recognition)

- Text-to-Speech

- Text-based / NLP

- Multimodal and Emotion-AI Interfaces

- By Product

- Chatbots

- Smart Speakers

- Mobile App-based Assistants

- Wearable / Edge Devices

- Kiosk and Bedside Terminals

- By Application

- Symptom Checking and Medical Information

- Appointment and Queue Scheduling

- Patient Triage and Management

- Medication and Care-plan Reminders

- Mental-health and Well-being Coaching

- Billing, Claims and Admin Support

- By End User

- Healthcare Providers (Hospitals and Clinics)

- Patients and Caregivers

- Healthcare Payers and TPAs

- Life-Sciences and Pharma Companies

- Telehealth / Digital-health Platforms

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed hospital IT chiefs, payer innovation leads, clinicians, and digital health entrepreneurs across North America, Europe, and Asia Pacific. These conversations tested our adoption assumptions, clarified average selling prices, and confirmed likely regulatory inflection points that secondary sources could not capture.

Desk Research

We began with open datasets from agencies such as the World Health Organization, Centers for Medicare & Medicaid Services, and Eurostat, which signal provider digital spend and patient volumes. Usage metrics from the Federal Communications Commission on broadband penetration, FDA device listings for cleared conversational tools, and peer reviewed papers on chatbot accuracy supplied adoption and performance clues. Company filings, IPO prospectuses, and reputable press helped verify revenue run-rates of major platform vendors. Select insights from D&B Hoovers and Dow Jones Factiva filled financial or regional gaps. This list is illustrative; numerous other sources informed each variable we validated.

Market-Sizing & Forecasting

A top-down demand pool based on active smartphone users, telehealth visit volumes, and provider IT budgets established the potential addressable market, which we then reconciled with selective bottom-up roll ups of supplier revenues and sampled ASP × deployment counts. Key variables include average chatbot sessions per patient, annual AI funding into digital health, HIPAA compliant cloud penetration, share of appointments booked through self-service portals, and regional clinician-to-population ratios. Multivariate regression with these drivers, followed by scenario analysis on regulatory pace, produced the 2025-2030 curve. Where bottom-up estimates under or overstated totals, weights were adjusted until both views converged within +/-5 percent.

Data Validation & Update Cycle

Outputs pass anomaly and variance checks; then a second analyst reviews assumptions. Reports refresh every twelve months, with interim revisions whenever a material event, such as a reimbursement code change or a major vendor acquisition, shifts baseline demand. A final pass is completed just before delivery so clients receive the freshest picture.

Why Mordor's Health Intelligent Virtual Assistant Baseline Commands Reliability

Published figures often diverge because firms differ on what counts as an intelligent assistant, the breadth of end users, and the cadence of refreshes.

Key gap drivers include whether payer facing bots are tallied, how aggressively average selling prices are trended, and if currency conversions use spot or annual averages. Mordor's scope captures all medically trained assistants and applies weighted ASP progression validated by current contracts, whereas several publishers limit counts to chatbots or freeze prices. Annual model refresh and on-call analyst reviews further tighten error bands.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.16 B (2025) | Mordor Intelligence | - |

| USD 1.73 B (2024) | Global Consultancy A | Counts chatbots only and omits payer deployments, relying on desktop data pulls |

| USD 0.32 B (2022) | Industry Journal B | Older base year, no inflation update, sample survey substituting for volume modeling |

Taken together, the comparison shows that Mordor's balanced scope, live pricing checks, and yearly updates yield a dependable baseline clients can trace to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the Health Intelligent Virtual Assistant market?

The market is valued at USD 5.08 billion in 2026 and is set to climb to USD 13.86 billion by 2031.

Which technology holds the largest Health Intelligent Virtual Assistant market share today?

Voice recognition leads with 43.10% revenue share in 2025 due to strong integration with clinical documentation systems.

Which product category is growing fastest within the Health Intelligent Virtual Assistant market?

Smart speakers show the highest 16.1% CAGR from 2026 to 2031 as hospitals and home-care providers adopt ambient voice interfaces.

Why is Asia-Pacific the fastest growing region?

Government investment in digital health, large multilingual populations, and rising chronic disease burdens fuel a 15.85% CAGR through 2031.

What are the main barriers to wider adoption of virtual assistants in healthcare?

Data privacy concerns, clinician trust issues, and evolving AI explainability regulations currently restrain growth.

How do virtual assistants help reduce healthcare costs?

They automate high-volume tasks such as scheduling, documentation, and triage, which removes administrative overhead and prevents unnecessary hospital visits.

Page last updated on: