Digital Fitness Apps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

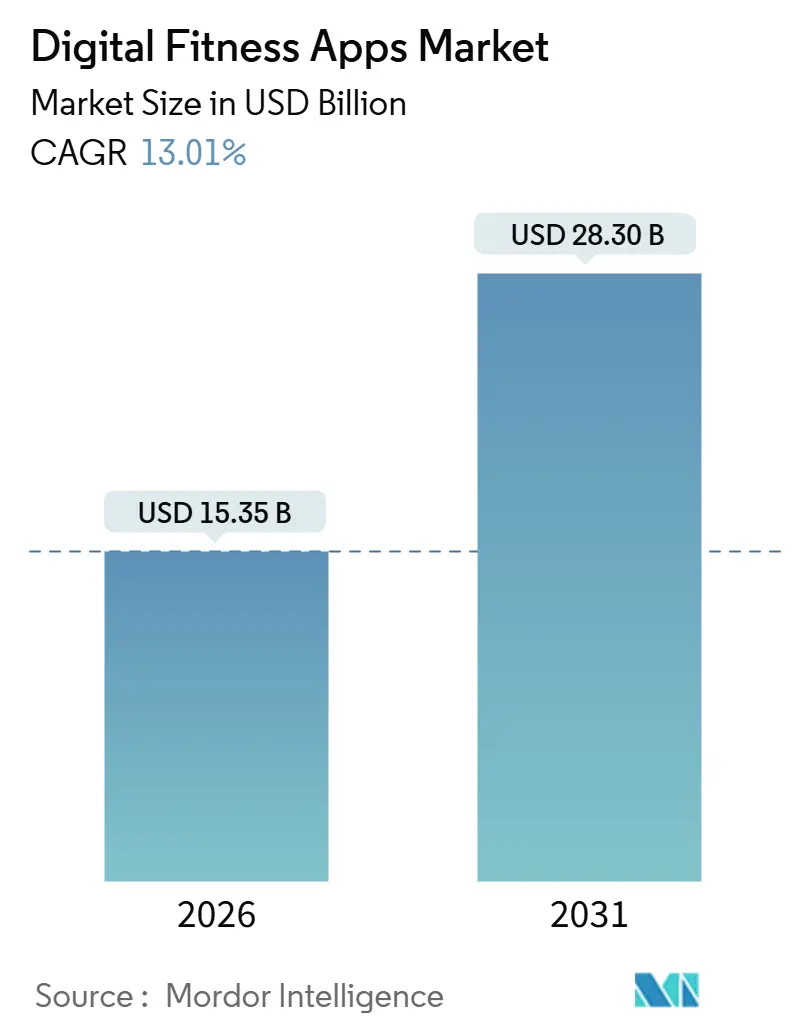

| Market Size (2026) | USD 15.35 Billion |

| Market Size (2031) | USD 28.30 Billion |

| Growth Rate (2026 - 2031) | 13.01% CAGR |

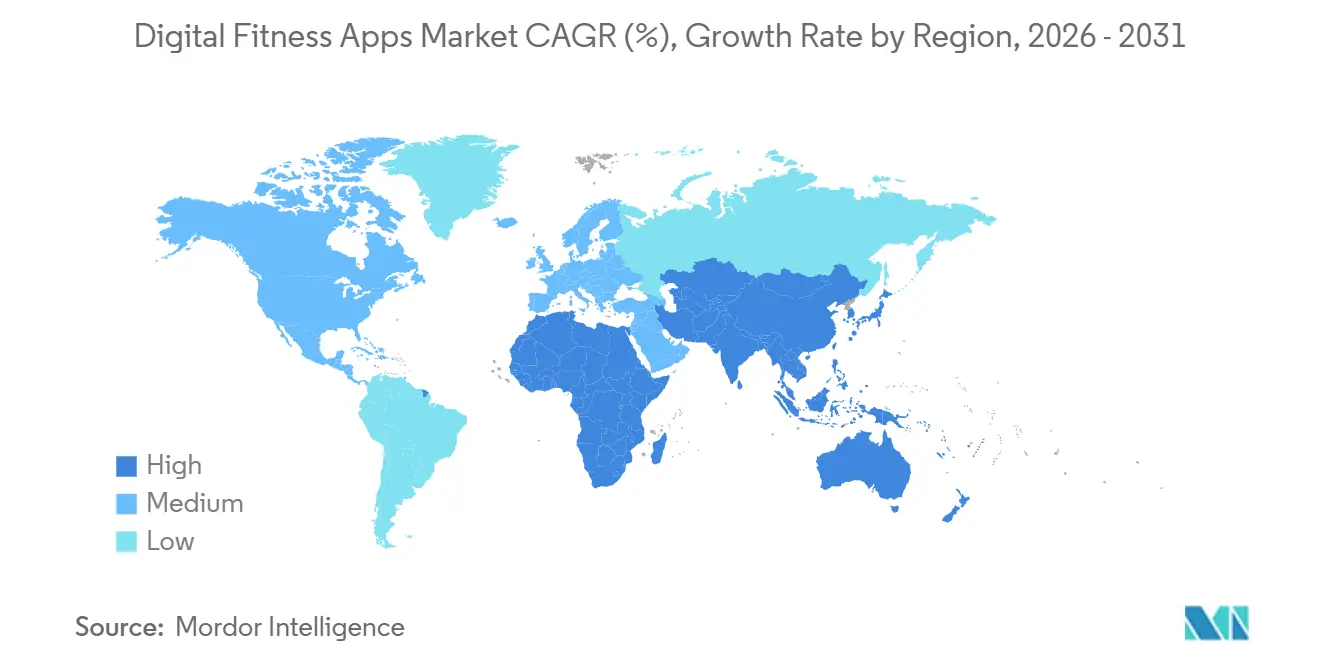

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

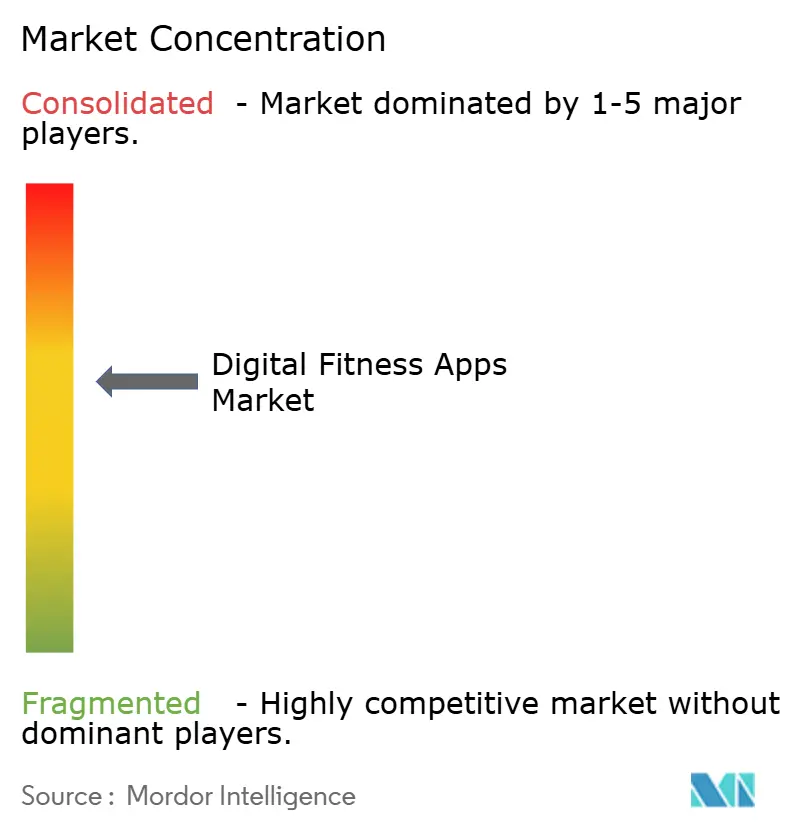

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Fitness Apps Market Analysis by Mordor Intelligence

The digital fitness apps market size stands at USD 15.35 billion in 2026 and is projected to reach USD 28.30 billion by 2031, translating into a 13.01% CAGR over the forecast period. Continued alignment with GLP-1 weight-loss therapies, rapid advances in on-device AI voice coaching, and the steady expansion of employer-funded wellness benefits are repositioning digital apps from discretionary lifestyle add-ons to core preventive-health tools. Device makers that embed FDA-cleared sensors in watches, rings, and bands are deepening data pipelines that feed generative-AI models, improving real-time personalization and raising switching costs. In parallel, insurers and self-insured employers are underwriting premium subscriptions, cushioning developers from volatile consumer churn while tightening clinical-validation requirements. Heightened data-privacy scrutiny and rising acquisition costs temper momentum, yet sustained hardware penetration and drug-software convergence keep the digital fitness apps market on a doubling trajectory through 2031.

Key Report Takeaways

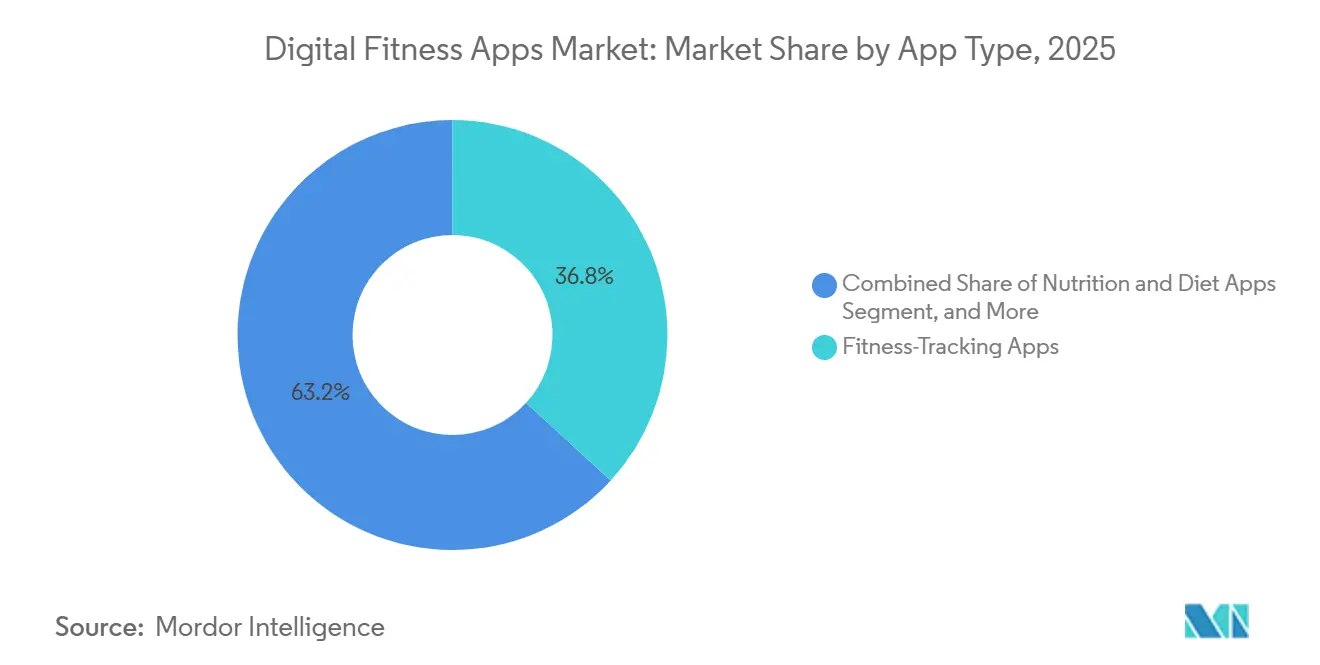

- By app type, fitness-tracking applications led with 36.83% revenue share in 2025, while fertility and contraception offerings are expanding at a 13.88% CAGR to 2031.

- By platform, iOS commanded 55.73% of the 2025 base, whereas wearable-OS native titles are advancing at a 14.67% CAGR through 2031.

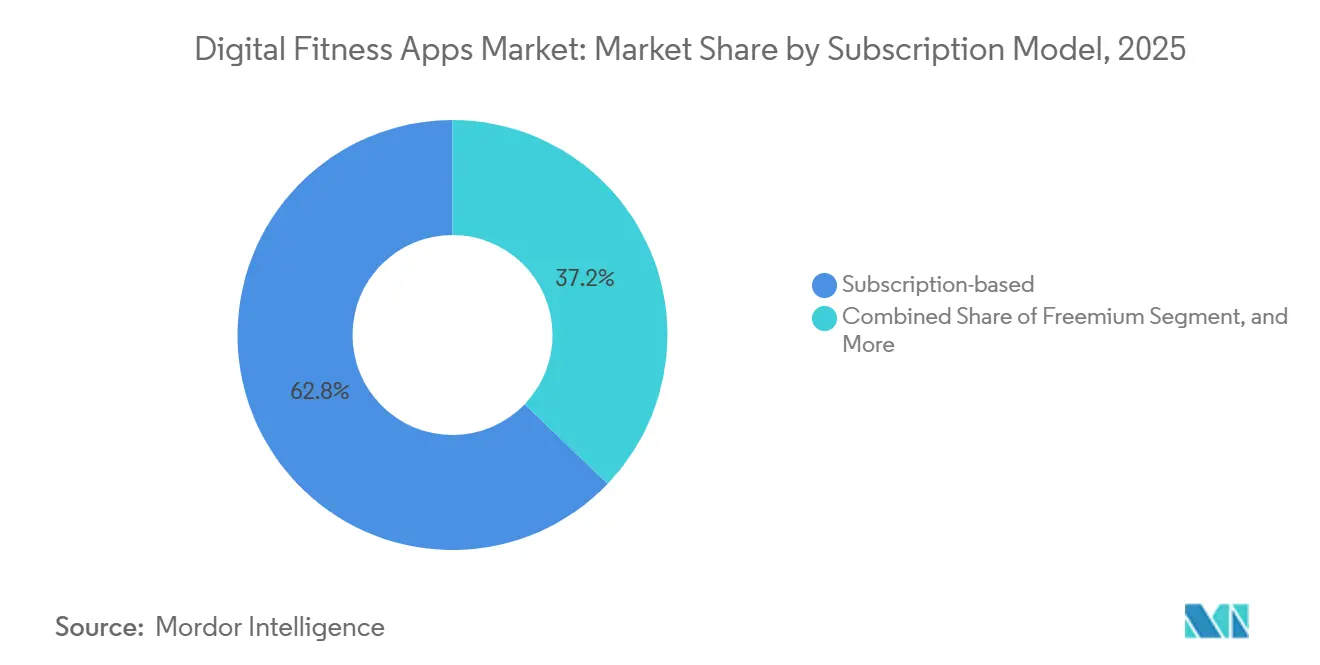

- By subscription model, subscription-based services represented 62.83% of 2025 revenue, yet freemium propositions are growing at 14.89% CAGR as acquisition efficiency erodes.

- By end user, individual consumers held 56.82% share in 2025, while healthcare providers and insurers post the fastest 14.78% CAGR as value-based-care reimbursement accelerates.

- By geography, North America captured 38.73% share in 2025, whereas Asia-Pacific is forecast to pace the field with a 14.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Fitness Apps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (∼) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GLP-1 weight-loss program integrations | +3.2% | North America, Europe, with early adoption in urban Asia-Pacific markets | Medium term (2-4 years) |

| Generative-AI voice-coach differentiation | +2.8% | Global, with premium-tier penetration in North America and Western Europe | Short term (≤ 2 years) |

| Rising insurer and employer incentives for app-based wellness | +2.5% | North America, Europe, with pilot programs in Japan and South Korea | Medium term (2-4 years) |

| Explosive smartphone and wearable penetration | +2.1% | Asia-Pacific core, with spillover to Middle East and Africa | Long term (≥ 4 years) |

| Gamification and social-fitness network effects | +1.3% | Global, with highest engagement in North America and Europe | Short term (≤ 2 years) |

| Elder-fitness demand from 55+ cohort | +1.1% | North America, Europe, Japan, with emerging interest in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GLP-1 Weight-Loss Program Integrations

Prescription therapies built on semaglutide and tirzepatide are being stitched into leading platforms, blending medication adherence tools with activity coaching. WeightWatchers began issuing GLP-1 prescriptions inside its app, funneling members to telehealth providers and streamlining home delivery. Apple Fitness+ added workout plans that sync to dosing schedules, mitigating muscle-loss risk flagged by endocrinologists. Omada Health expanded its reimbursed diabetes-prevention pathway to include GLP-1 support, shifting payment liability from users to insurers. Embedding pharmacotherapy elevates apps into hybrid care coordinators, lengthens engagement cycles well beyond the typical 90-day churn horizon, and unlocks insurer funding once confined to clinical visits.

Generative-AI Voice-Coach Differentiation

Large-language models are morphing static tutorials into two-way dialogues that adjust form, intensity, and rest intervals on the fly. WHOOP’s Coach leverages GPT-4 to parse overnight recovery data and issue real-time prompts during exercise. Fitbit’s Gemini integration adds conversational Q&A, grounding answers in peer-reviewed science.[1]Umar Shakir, “Fitbit Taps Gemini AI,” The Verge, theverge.com Strava’s Athlete Intelligence estimates race-day pacing using cohort comparisons. Voice interaction frees users from screen glances, narrows the gap with human trainers, and compresses coaching costs, all while generating granular behavioral datasets that enrich personalization engines.

Rising Insurer and Employer Incentives for App-Based Wellness

Payers are moving beyond passive reimbursement toward proactive subsidization. UnitedHealthcare now disburses up to USD 1,000 annually to members who hit activity milestones tracked via connected wearables. JPMorgan Chase covers Peloton and Calm subscriptions for 250,000 employees after observing a 12% drop in mental-health-linked absences. Aetna funds Noom’s diabetes-prevention program contingent on 16-week completion rates. Subsidies transfer cost risk away from consumers, expand enterprise licensing revenue, and create multiyear contracts that dampen churn, but they intensify demand for clinical validation and HIPAA compliance.

Explosive Smartphone and Wearable Penetration

Global smartwatch shipments hit significant growth in terms of units in 2024, a hardware surge feeding continuous data loops into apps. Apple Watch Series 10 gained FDA-cleared sleep apnea detection, reframing the device as a diagnostic-grade monitor.[2]Apple Newsroom Staff, “Apple Watch Series 10 Introduces Sleep Apnea Detection,” apple.com Samsung’s USD 399 Galaxy Ring offers all-day vitals tracking in a ring form factor, easing compliance among users who find wrist-wear obtrusive. Garmin revealed that 80% of its 2024 wearables synced data to third-party apps, underscoring the role of open APIs in app discovery. Deeper sensor reach enriches AI models, raises accuracy, and lowers friction, directly fueling retention and premium upsells.

Restraints Impact Analysis*

| Restraint | (∼) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened data-privacy regulations (GDPR, DMA, ADPPA) | -1.8% | Europe (GDPR, DMA), North America (ADPPA proposals), with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Post-pandemic app-fatigue and retention drop-off | -1.5% | Global, with most acute impact in North America and Europe | Short term (≤ 2 years) |

| Rising customer-acquisition costs on saturated ad channels | -0.9% | Global, with highest CAC inflation in North America | Medium term (2-4 years) |

| Accuracy gaps vs. clinical-grade wearables | -0.7% | Global, with regulatory scrutiny concentrated in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Data-Privacy Regulations

Regulators are tightening stewardship around sensitive health telemetry. The Irish Data Protection Commission fined Meta EUR 91 million (USD 98 million) in 2024 for mishandling fitness data. The European Union’s Digital Markets Act bars gatekeepers from auto-installing their own apps, forcing Apple and Google to compete on merit.[3]European Commission Directorate-General for Competition, “Digital Markets Act Takes Effect,” ec.europa.eu Proposed U.S. legislation would mandate explicit consent for data sharing, a hurdle that 40% of users decline when prompted. Compliance raises engineering overhead, complicates cross-platform personalization, and pushes subscale developers toward consolidation.

Post-Pandemic App-Fatigue and Retention Drop-Off

Initial lockdown-era download spikes proved fleeting. Thirty-day retention for most health apps fell to 3-8% in 2024. Day-1 stickiness hovers at 30-35%, sliding to sub-2% paid conversion within a month. Peloton’s connected-fitness subscribers slipped from 3 million in 2023 to 2.9 million by Q3 FY2024, prompting a USD 1.4 billion debt refinance and a strategic pivot toward content and corporate plans. Shrinking engagement windows compel front-loaded onboarding, yet overly aggressive prompts risk backlash, amplifying churn and rising CAC.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By App Type: Regulatory Clearances Propel Fertility Apps

Fertility and contraception titles, while a smaller slice of the digital fitness apps market, are expanding at a 13.88% CAGR, outstripping the 36.83% 2025 dominance held by fitness trackers. Flo Health’s CE-marked ovulation engine lets European insurers reimburse subscriptions, while Natural Cycles’ FDA-cleared protocol drew 2.5 million paying users in 2024. Integration with temperature sensors on Apple Watch and Samsung Galaxy Ring boosts prediction accuracy toward 95%, aligning app outputs with clinical benchmarks. The digital fitness apps market size for fertility solutions deepens as employers roll these tools into fertility-benefit budgets, attaching subscription revenue to corporate wallets. Competitive intensity in generic trackers is prompting vendor consolidation, whereas regulatory pathways in fertility apps create defensible moats.

Clinical functionality is elevating reimbursement potential across other categories too. Nutrition apps tie GLP-1 taper programs to macro dashboards, while meditation brands such as Calm secure enterprise contracts by bundling stress-management metrics. Sleep and posture trackers leverage insurer programs that reward biometric milestones, extending user journeys beyond the typical 90-day horizon. Conversely, pure workout-log apps without clinical hooks struggle for differentiation against ecosystem giants that subsidize subscriptions with device sales. Overall, regulatory progression and medical-device alignment are reshaping the app-type hierarchy inside the digital fitness apps market.

By Platform: Native Wearable Operating Systems Extend Utility

iOS retained a 55.73% share in 2025, but watchOS and Wear OS instances are compounding at 14.67% through 2031 as processing shifts directly onto the wrist. Apple’s watchOS 11 Vitals app surfaces overnight HRV and respiratory-rate deviations, nudging users toward preventive behaviors without phone intervention. Google’s Wear OS 5 improved battery life by 20%, a threshold that turns multi-day tracking into reality for Android cohorts. Samsung’s Energy Score aggregates sleep, activity, and heart-rate signals into a readiness index, translating complex biometrics into a single actionable metric.

The digital fitness apps market share migrates alongside these OS trends because always-on sensors feed richer data to AI models, reinforcing personalization cycles that tether users to specific hardware lines. Non-native web apps lag, restricted by sensor permissions and absent background processing. For developers, building natively unlocks on-device inference and streamlines privacy compliance by keeping raw data local. Consequently, wearable-first roadmaps are increasingly central to monetization discussions inside the digital fitness apps industry.

By Subscription Model: Freemium Strategy Balances CAC Pressures

Subscription formats captured 62.83% of revenue in 2025, yet freemium cohorts are climbing at a 14.89% CAGR as acquisition costs jump 40-60% on saturated ad channels. Strava converts 1.7% of a 150 million user base into paid tiers, still generating USD 275 million in 2024 through value-added features such as segment leaderboards. MyFitnessPal’s 200 million downloads fuel an upsell funnel for its USD 80 annual plan, covering meal planning and macro analytics.

Digital fitness apps market size expansion relies on balancing free reach with infrastructure overhead. Enterprise licenses offer a hedge, with Cigna funding Headspace access for 16 million members and securing an 8% drop in mental-health claims. One-time-payment niches persist, but their limited cash flow constrains feature velocity. As CAC inflation persists, freemium economics that harvest behavioral data for AI engines are poised to dominate, especially for well-capitalized incumbents.

By End User: Healthcare Entities Expand Digital Prescriptions

Individual users still represented 56.82% of the 2025 base, yet healthcare providers and insurers are accelerating at 14.78% CAGR, positioning the channel as the long-term growth engine. UnitedHealthcare’s rewarded-steps model disbursed USD 1,000 per compliant member, proving that targeted incentives can shift actuarial outcomes. Omada Health’s per-member-per-month contracts now span 10 million covered lives, illustrating the scalability of clinical-grade digital therapeutics.

For the digital fitness apps market, provider adoption changes product-development calendars, foregrounding HIPAA compliance, interoperable EHR links, and randomized-control-trial evidence. Platforms that satisfy these hurdles enjoy multiyear contracts and reduced churn. Meanwhile, fitness studios leverage white-label apps to stay connected with members off-site, using Mindbody’s infrastructure across 60,000 locations. The dual tailwinds of insurer endorsement and enterprise wellness budgets anchor a durable end-user mix shift away from pure consumer playbooks.

Geography Analysis

North America retained 38.73% of 2025 revenue, powered by Medicare Advantage subsidies and employer mandates that weave digital subscriptions into benefits packages. U.S. seniors engage with SilverSneakers’ fall-prevention modules, while Apple Fitness+ populates its “Older Adults” library to capture the same reimbursement streams. Canada’s growth remains urban-centric due to patchy rural broadband, and Mexico’s expanding middle class is onboarding via mobile-first ecosystems.

Asia-Pacific is the fastest riser at a 14.66% CAGR through 2031. India and Indonesia leapfrog desktop computing, adopting mobile-centric health platforms that thrive on low-cost Android handsets. China’s WeChat Sports amassed 300 million monthly users by embedding activity feeds within an everyday super-app, and South Korea’s Samsung-led hardware dominance ensures pre-installation of Samsung Health on two-thirds of domestic devices. Emerging ASEAN markets such as Thailand and Vietnam gain momentum as 4G coverage widens and carrier billing unlocks paid-app conversion without credit cards.

Europe accounts for 22% of 2025 value, with Germany, the United Kingdom, and France driving 60% of regional spend. The Digital Markets Act levels the discovery field for midsize players by banning default installs, enhancing visibility for brands like Strava. Middle East and Africa trails due to data-cost frictions yet pockets of opportunity exist, notably Saudi Arabia’s USD 500 million Vision 2030 fund that underwrites telehealth pilots. South Africa’s carrier-bundled data packs that include fitness apps illustrate an emerging model for price-sensitive markets.

Competitive Landscape

Digital fitness apps remain moderately fragmented, yet device-ecosystem giants are tightening share. Apple bundles Fitness+ within an iOS walled garden and uses the A18 chip for on-device inference that mitigates privacy concerns. Samsung courts clinical credibility through FDA-cleared sleep-apnea screening on Galaxy Watch and positions the Galaxy Ring for users who dislike wristwear. Alphabet integrates Gemini AI across Google Fit and Fitbit, marrying open APIs with premium AI nudges.

Specialists still carve defensible niches. WHOOP’s USD 30 monthly hardware-plus-software bundle eliminates upfront capex, winning serious athletes craving recovery analytics. Strava sustains network effects via 5.3 million annual group-challenge participants, and Zwift fuses cycling with gaming mechanics to triple retention relative to solo rides. White-space opportunities persist in elder-fitness content and chronic-care digital therapeutics, where Omada Health and Livongo pursue FDA pathways that many consumer apps avoid due to regulatory expense.

Pricing power correlates with proprietary sensors and clinical validation. Vendors without hardware stacks rely on open-platform data, which the Digital Markets Act threatens to limit. Midsize developers seek acquisition by hardware majors or insurers eager to own engagement touchpoints. The competitive equilibrium therefore oscillates between horizontal platform bundling and vertical integration that spans device, data, and content layers.

Digital Fitness Apps Industry Leaders

Apple Inc.

Alphabet Inc. (Google Fit)

Fitbit LLC (Google)

Nike Inc.

Adidas AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Apple previewed watchOS 26, adding cuff-free blood-pressure readings and a streamlined interface to enhance clinical usability.

- May 2025: Apple partnered with Cal AI to roll out a photo-based calorie-tracking feature delivering 90% accuracy on iPhone and Watch devices.

- April 2025: Google removed Google Assistant support from the Fitbit Versa and Sense lines, underlining a transition to the Pixel Wear ecosystem.

- February 2025: Apple launched a multi-year study using combined iPhone and Apple Watch data to investigate population health trends.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the digital fitness apps market as all paid or freemium software applications that help users track, plan, or enhance physical activity, nutrition, or mindfulness on smartphones, tablets, wearables, or web interfaces; revenues refer to gross in-app purchases, subscription fees, and one-time downloads processed through official app stores and enterprise licenses.

Scope Exclusion: Revenues from dedicated hardware (smartwatches, heart-rate straps, connected mirrors) and brick-and-mortar gym memberships are excluded.

Segmentation Overview

- By App Type

- Fitness-Tracking Apps

- Nutrition and Diet Apps

- Meditation and Mind-wellness Apps

- Fertility and Contraception Apps

- Medication and Pill-Reminder Apps

- Other Wellness Apps (sleep, posture, etc.)

- By Platform

- iOS

- Android

- Web / Progressive-Web-App

- Wearable-OS Native (watchOS, Wear OS, etc.)

- By Subscription Model

- Freemium

- Subscription-based

- One-time Purchase

- Enterprise Licensing

- By End User

- Individual Consumers

- Corporate Wellness Programs

- Fitness Centres and Studios

- Healthcare Providers and Insurers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple interviews were conducted with fitness coaches offering white-label apps, product managers at leading publishers across North America, Europe, and Asia-Pacific, and enterprise wellness coordinators. Their insights refined churn assumptions, average revenue per paying user, and freemium-to-paid conversion rates, filling gaps left by desk work.

Desk Research

Mordor analysts first gathered quantitative clues from public sources such as the U.S. Centers for Disease Control's Physical Activity Data, Eurostat's ICT Usage tables, India's Telecom Regulatory Authority smartphone base, and filings compiled on the SEC EDGAR system. Trade bodies, such as the Global Wellness Institute, the Mobile Marketing Association, and country-level app developer associations, helped establish app monetization norms. Our team then tapped paid repositories like Dow Jones Factiva for earnings transcripts, D&B Hoovers for company financials, and Questel for patent momentum to triangulate adoption signals across regions. These sources, while illustrative, are not exhaustive; many additional databases and journal articles informed the evidence base.

A follow-up sweep of health regulations (GDPR, HIPAA updates, India's DPDP Act) and import-export data for wearables supplied context for price corridors and uptake triggers.

Market-Sizing & Forecasting

We applied a top-down penetration-rate build-up, starting with the active smartphone base and regional physical-activity prevalence, which are then multiplied by paid app adoption ratios; selective bottom-up supplier roll-ups and sampled ASP × active-user calculations served as guardrails. Key variables include monthly active users, paid conversion rates, average subscription price, smartphone penetration, and corporate wellness budgets. A multivariate regression with lagged GDP per capita and health insurance incentives underpins the 2025-2030 forecast, stress-tested through optimistic and conservative adoption scenarios before finalizing the 12.7% CAGR. Where partial bottom-up estimates showed data gaps, region-specific ARPU proxies were imputed using three-year moving averages.

Data Validation & Update Cycle

Every model iteration passes variance checks against independent spend trackers and app-store download dashboards; anomalies above two standard deviations trigger re-verification. Two analyst reviews precede sign-off, and the dataset is refreshed annually, with interim updates if material events, such as major app-store policy shifts, arise.

Why Mordor's Digital Fitness Apps Baseline Earns Stakeholder Trust

Published figures often diverge because agencies pick different inclusion criteria, currency bases, and refresh cadences. We recognize these factors and preview them for clients up front.

Key gap drivers include whether mindfulness apps are counted, how freemium users are monetized, and the cadence at which app-store fees are adjusted for currency moves. Some publishers fold hardware revenue into software totals or freeze assumptions for two-plus years, whereas Mordor revisits inputs each quarter and omits hardware entirely.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.59 B (2025) | Mordor Intelligence | - |

| USD 12.12 B (2025) | Global Consultancy A | Excludes corporate wellness licenses; uses static ARPU from 2022 |

| USD 17.81 B (2025) | Industry Association B | Blends wearable device revenue and applies fixed USD-local FX rates |

This comparison shows that Mordor's disciplined scope selection, live currency updates, and dual-path validation yield a balanced, transparent baseline that decision-makers can reproduce with publicly traceable inputs.

Key Questions Answered in the Report

How large is the digital fitness apps market in 2026?

The market is valued at USD 15.35 billion in 2026 and is on track to reach USD 28.30 billion by 2031.

What CAGR is expected for digital fitness apps through 2031?

The sector is forecast to expand at a 13.01% CAGR during 2026-2031.

Which app category is growing fastest?

Fertility and contraception apps are rising at a 13.88% CAGR, supported by regulatory clearances that unlock insurance reimbursement.

Why are insurers and employers funding subscriptions?

Evidence of reduced healthcare claims has led payers such as UnitedHealthcare and corporates like JPMorgan Chase to subsidize premium fitness, nutrition, and mental-wellness apps.

What role do GLP-1 drugs play in app adoption?

Integrations with semaglutide and tirzepatide protocols extend user engagement, shift costs to insurers, and create hybrid care models that bundle medication with behavioral coaching.

Page last updated on: