Clinical Healthcare IT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

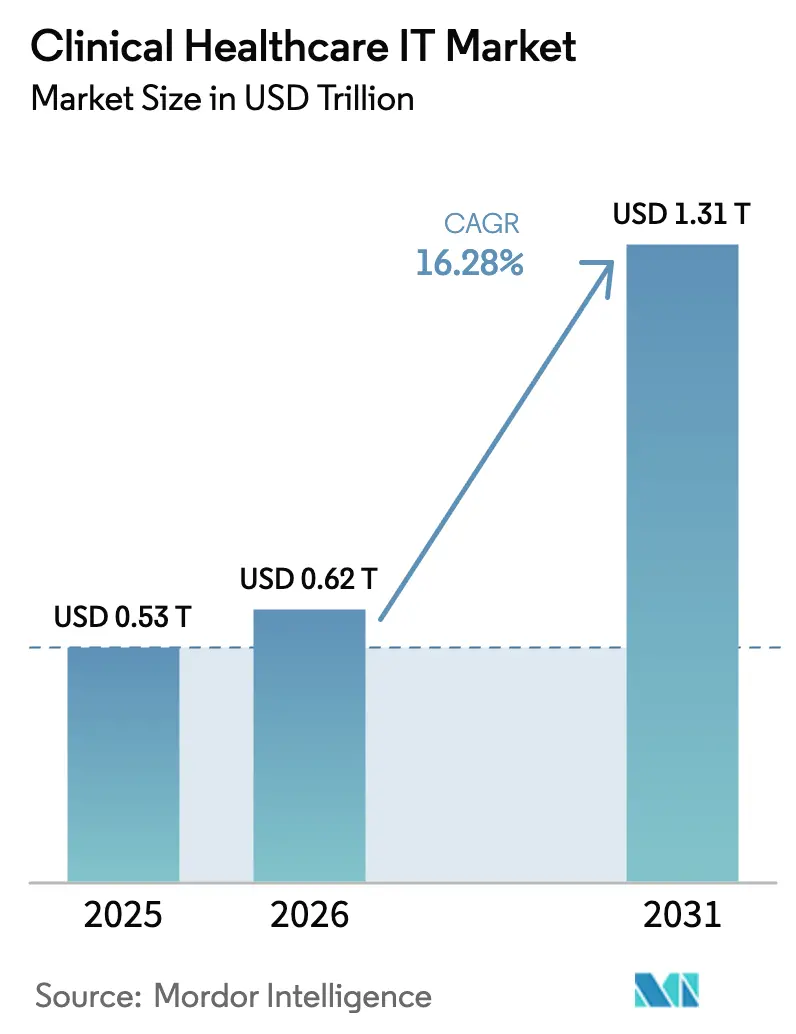

| Market Size (2026) | USD 0.62 Trillion |

| Market Size (2031) | USD 1.31 Trillion |

| Growth Rate (2026 - 2031) | 16.28% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Healthcare IT Market Analysis by Mordor Intelligence

The clinical healthcare IT market size is expected to grow from USD 0.530 trillion in 2025 to USD 0.62 trillion in 2026 and is forecast to reach USD 1.31 trillion by 2031 at 16.28% CAGR over 2026-2031. Demand accelerates as hospitals replace aging systems, adopt artificial intelligence for predictive care, and shift workloads to cloud-native environments. Vendors able to demonstrate seamless interoperability, strong cybersecurity postures, and scalable SaaS economics win preferential consideration, especially where regulatory mandates such as the 21st Century Cures Act and Japan’s FHIR-based EMR program tighten compliance timelines.[3]U.S. Department of Health and Human Services, “Health Data, Technology, and Interoperability,” federalregister.gov Deepening reliance on data-intensive analytics also pushes organizations toward high-performance infrastructure, with 61.8% of new deployments already cloud or hybrid. Competitive dynamics remain fluid; Epic’s widening footprint, Oracle Health’s integration setbacks, and a surge of niche AI documentation tools collectively reshape the clinical healthcare IT market landscape.[1]Fierce Healthcare, “New Mountain Capital Launches AI-Enabled RCM Platform,” fiercehealthcare.com

Key Report Takeaways

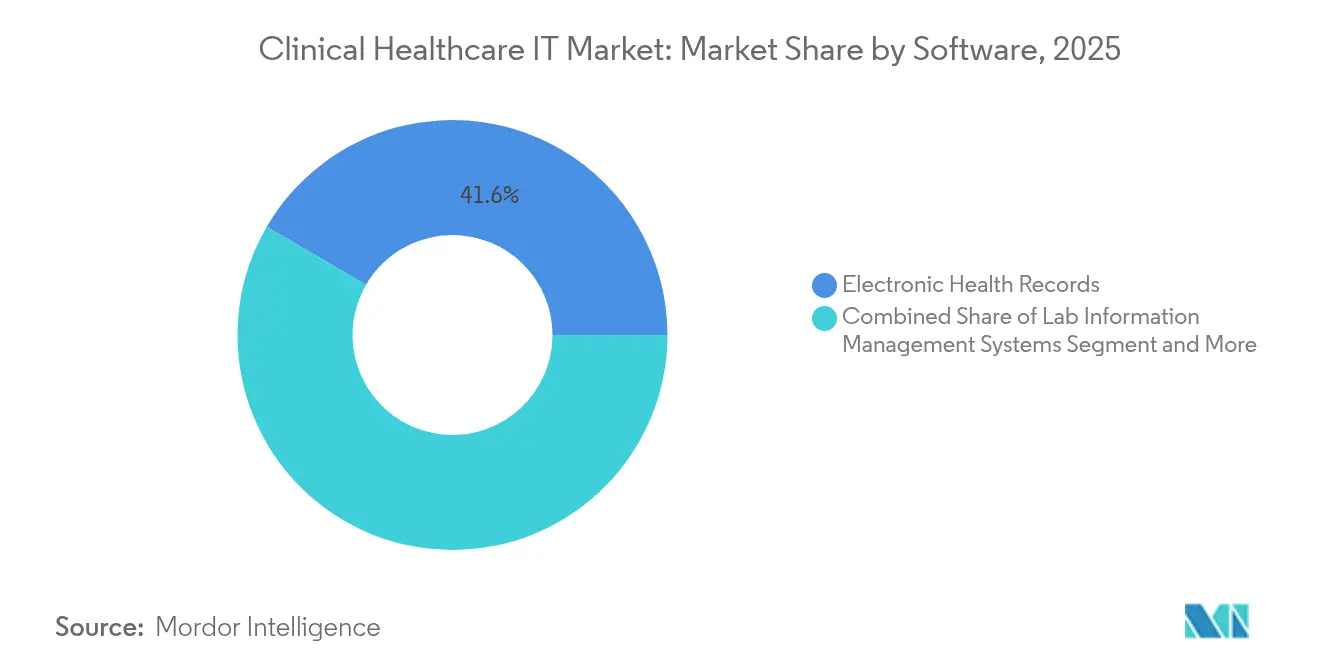

- By software category, Electronic Health Records led with 41.60% revenue share in 2025, while Telemedicine platforms are projected to grow at 18.57% CAGR to 2031.

- By end user, private hospitals and diagnostic centers held 52.70% of the clinical healthcare IT market share in 2025; public agencies register the fastest 15.12% CAGR through 2031.

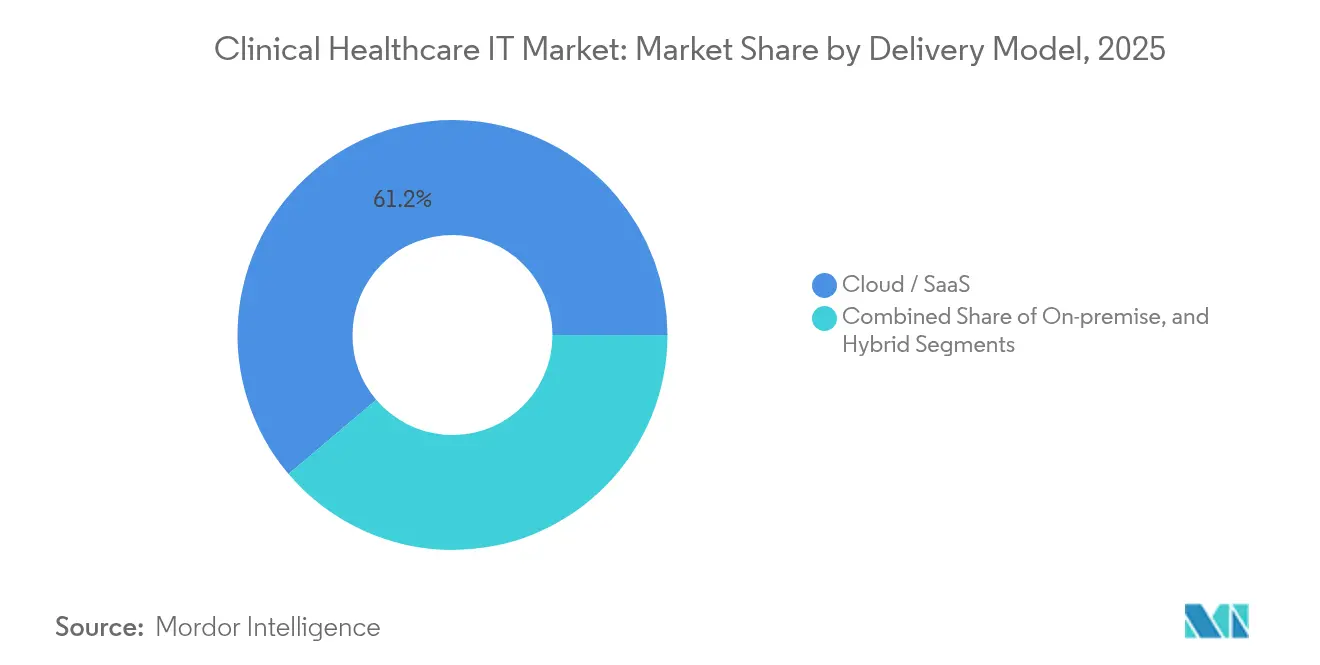

- By delivery model, cloud and SaaS captured 61.20% share of the clinical healthcare IT market size in 2025 and are expanding at a 18.64% CAGR over the forecast period.

- By application, Revenue Cycle Management accounted for 29.10% of the clinical healthcare IT market size in 2025, while Patient Engagement solutions advance at a 20.41% CAGR.

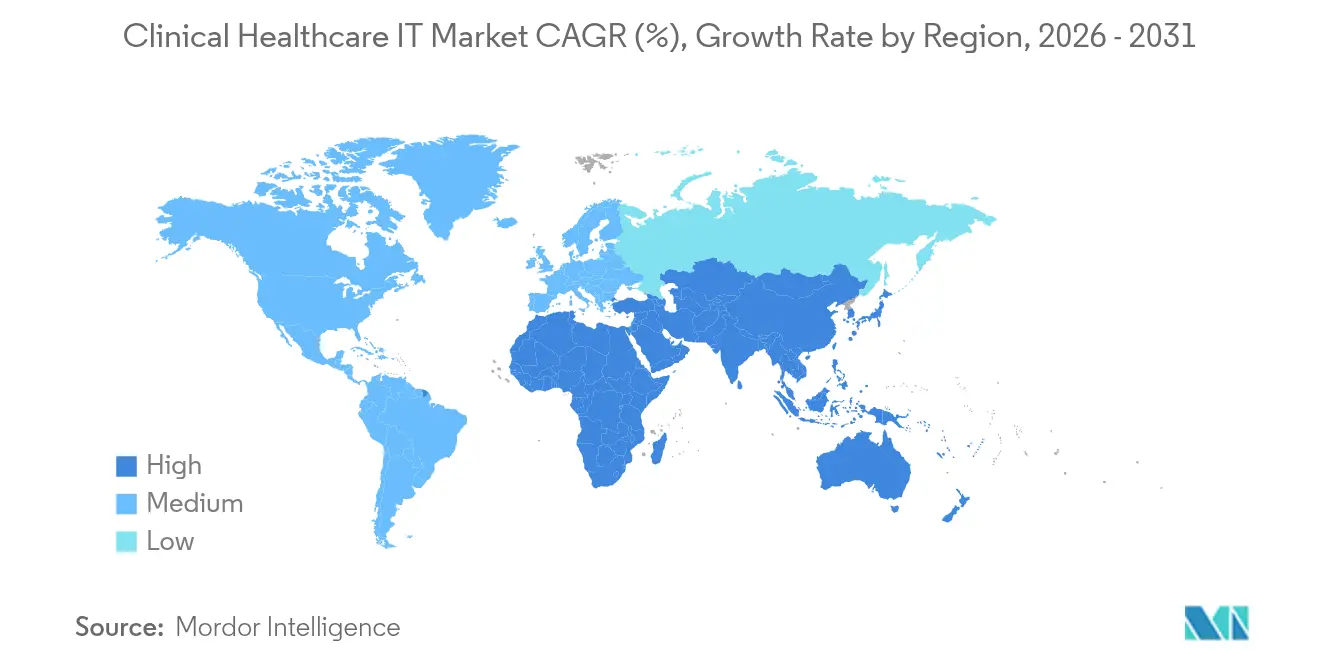

- By geography, North America commanded 43.60% of the clinical healthcare IT market share in 2025, but the Asia-Pacific region is poised for the fastest expansion with a 16.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Clinical Healthcare IT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing complexity of healthcare data and AI/ML uptake | +4.2% | North America, Europe | Medium term (2-4 years) |

| Accelerating cloud-based deployment | +3.8% | North America, Asia Pacific | Short term (≤ 2 years) |

| Government EHR-interoperability mandates | +2.9% | US, EU, Japan | Long term (≥ 4 years) |

| FHIR-based open APIs and micro-services | +2.1% | Developed markets worldwide | Medium term (2-4 years) |

| Digital-payment and RCM automation catalysts | +1.7% | North America, emerging Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Complexity of Healthcare Data and AI/ML Uptake

Expanding data volumes overwhelm legacy platforms, prompting 73% of hospitals to deploy machine-learning models for tasks ranging from sepsis alerts to bed management. Nearly half of US facilities already use AI to automate revenue cycle workflows, while ambient clinical scribes now appear in more than 60 health systems, easing documentation burdens and clinician burnout. Case studies at Auburn Community Hospital and Banner Health show billing error reductions of 50% after AI rollouts. Nevertheless, adoption gaps persist in disadvantaged regions, raising equity concerns that national digital-health roadmaps aim to mitigate. As compute-intensive models proliferate, the clinical healthcare IT market increasingly ties procurement to access to GPUs and scalable data lakes.

Accelerating Cloud-Based Deployment

Hybrid-cloud architectures help organizations keep sensitive data on-premises while exploiting public-cloud elasticity for analytics. US healthcare data-storage spend is on track to rise from USD 25.5 billion in 2024 to nearly USD 70 billion by 2032. Veterans Affairs Lighthouse FHIR API illustrates how cloud hosting can enable real-time data exchange without duplicating medical records va. Germany’s EUR 4.3 billion (USD 4.97 billion) hospital digitalization fund shows comparable momentum, lifting digital maturity scores 27% in three years.[2]Ärzteblatt, “Hospitals Improve Digital Maturity,” aerzteblatt.de Cloud share already exceeds 61.8% of clinical deployments, and a 19.2% CAGR signals a decisive infrastructure pivot that underpins the future growth of the clinical healthcare IT market.

Government EHR-Interoperability Mandates

Regulators transform interoperability from an optional feature to a legal obligation. The ONC proposal to embed USCDI v4, Japan’s nationwide FHIR rollout scheduled by 2026, and Germany’s Digital Act targeting universal electronic patient records by 2025 all tighten vendor requirements. Compliance timelines motivate providers to standardize purchases around platforms with proven data-exchange toolkits, reinforcing consolidation in the clinical healthcare IT market. Vendors boasting turnkey APIs and automated quality-measure reporting typically shorten implementation cycles, giving them an edge in competitive bids.

FHIR-Based Open APIs & Micro-Services

Fast Healthcare Interoperability Resources supports modular development and vendor-agnostic data sharing. Projects like EBMonFHIR link research evidence to bedside decisions, while patient-facing apps such as Andaman7 facilitate portable personal records. European agencies now reference FHIR as a default for cross-border data flows, and US federal rules penalize information blocking when APIs are absent. Health systems adopting API-first strategies report faster onboarding of specialty apps, positioning them for innovation cycles that will shape the clinical healthcare IT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability gaps and lack of standards | −2.8% | Fragmented in emerging markets | Long term (≥ 4 years) |

| Market consolidation toward integrated platforms | −1.9% | North America, Europe | Medium term (2-4 years) |

| Rising cyber-insurance premiums | −1.4% | Highest in North America | Short term (≤ 2 years) |

| AI-regulatory uncertainty | −1.1% | US, EU focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps and Lack of Standards

Even where 80% of physicians use EHRs, inconsistent data models, high exchange fees, and privacy rules impede friction-free information sharing, eroding the expected ROI on digitization. Germany’s productivity paradox shows that technology investment does not always translate into efficiency gains when data cannot travel seamlessly between departments.[4]Wirtschaftsdienst, “Productivity Paradox of Hospital Digitalization,” wirtschaftsdienst.eu The situation is more acute in low-resource markets that lack well-defined frameworks, stalling cross-border telehealth and medical-tourism ambitions. Until standards harmonize, the clinical healthcare IT market forfeits some potential CAGR.

Market Consolidation Toward Integrated Platforms

Epic’s rise to 42.3% share, coupled with Oracle Health’s client losses, underscores a shift toward single-vendor ecosystems that promise fewer interfaces to manage. While consolidation simplifies governance for large systems, it limits choice and may lock providers into proprietary data structures. Startups offering best-of-breed modules find entry barriers higher, potentially stifling innovation at the edges of the clinical healthcare IT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software: EHR Dominance Faces Telemedicine Disruption

Electronic Health Records maintained 41.60% share in 2025, anchoring core clinical workflows and satisfying Meaningful Use criteria. The clinical healthcare IT market size for EHR platforms is expected to expand steadily but cede growth momentum to telemedicine suites, advancing at 18.57% CAGR. Telehealth capability gained permanence when US legislation removed most geographic restrictions for behavioral services, encouraging vendors to embed video consultation modules natively within EHR dashboards.

Epic’s rapid client wins highlight the scale advantages of tightly integrated platforms, yet specialized Picture Archiving and Laboratory Information Management systems remain indispensable for radiology and pathology. Providers pursue a dual-track strategy: standardize on a single record backbone while layering niche apps that address imaging, e-prescribing, or precision-medicine needs. This hybrid sourcing pattern keeps competitive doors open for focused innovators and sustains diversity in the clinical healthcare IT market.

By End-User: Private Sector Leadership Amid Public Acceleration

Private hospitals and diagnostic centers captured 52.70% of 2025 revenue, benefiting from stronger capital reserves and faster decision cycles. Their share of the clinical healthcare IT market size is forecast to grow more slowly, however, as public agencies accelerate at 15.12% CAGR on the back of stimulus programs like Germany’s Krankenhauszukunftsgesetz. Government entities prioritize interoperability and population-health dashboards that support national policy goals.

Federally qualified health centers in the US, for example, explore AI coding tools to offset staffing shortages, while Japan’s clinic-level EMR subsidy scheme advances equitable access to digital records. Rising public-sector demand introduces new procurement criteria around open standards and data sovereignty, reshaping vendor evaluation matrices across the clinical healthcare IT market.

By Delivery Model: Cloud Migration Transforms Infrastructure

Cloud and SaaS deployments constituted 61.20% of new installations in 2025 and are expanding at a 18.64% CAGR. Elastic capacity enables GPU-intensive analytics without costly on-premise hardware, a critical advantage as decision-support models grow in complexity. The clinical healthcare IT market share for on-premise models will narrow but not vanish; certain specialty hospitals keep sensitive imaging archives onsite to meet regional privacy laws.

Hybrid strategies dominate large systems that blend private-cloud control with burst-to-public scalability. Germany’s national patient record hinges on cloud-hosted services that still let insurers restrict data residency within the EU. This architectural flexibility unlocks multi-tenant cost efficiencies and keeps the cloud in pole position within the clinical healthcare IT market.

By Application: RCM Leadership Yields to Patient Engagement Innovation

Revenue Cycle Management accounted for 29.10% of spending in 2025, driven by reimbursement cuts and complex payer rules. Its slice of the clinical healthcare IT market size expands in lockstep with hospital revenue pressures, yet Patient Engagement solutions register the fastest 20.41% CAGR. Regulatory pushes for data transparency and consumer demand for app-based care coordination elevate portal, messaging, and wearable-integration modules from nice-to-have to strategic necessities.

Integrated billing-plus-engagement suites now bundle automated estimates, e-consents, and digital payments into a single workflow, closing the loop between clinical and financial touchpoints. As a result, differentiators shift from point functionality to user-experience coherence, prompting RCM vendors to acquire or build patient-facing layers, further concentrating the clinical healthcare IT market.

Geography Analysis

North America retained a 43.60% share in 2025. Hospital care alone consumed USD 1.5 trillion, creating a fertile addressable base for software, infrastructure, and services solutions. Interoperability rules under the Cures Act and extended telehealth reimbursement underpin sustained IT outlays, even as cyber incidents drive parallel investment in zero-trust architectures. Epic’s acute-care dominance illustrates the region’s inclination toward integrated platforms, a factor that molds competitive strategies throughout the clinical healthcare IT market.

Asia Pacific is the fastest-growing territory at 16.32% CAGR, propelled by Japan’s mandate for 100% EMR adoption by 2030, widespread 5G availability, and expanding smart-hospital pilots. Government subsidies ease upfront costs for smaller clinics, fostering inclusive growth that broadens the clinical healthcare IT market. China and India leverage large developer workforces to export digital-health services region-wide, propelling API ecosystems and lowering software price points.

Europe shows steady progress. Germany’s Digital Act commits all insured citizens to electronic patient records by 2025, while the EU-AI Act sets a harmonized risk framework for clinical algorithms. Strong data-protection norms sustain demand for sovereign-cloud configurations, favouring vendors that can guarantee regional hosting. Peripheral regions like Latin America and the Middle East begin to scale telehealth networks under national transformation plans, though infrastructure gaps and payment-model rigidity temper near-term expansion.

Competitive Landscape

High concentration characterizes the clinical healthcare IT market. Epic Systems holds 42.3% of US acute-care deployments after onboarding 176 multi-specialty hospitals in 2024. Oracle Health’s Cerner unit suffered high-profile outages that obscured 11,000 medical orders, leading to multiple defections and negative brand equity. Meditech and Altera retain niche strongholds, but their aggregate share trails Epic by a wide margin.

Consolidation trends persist as health systems favor fewer suppliers for enterprise contracts. Private-equity groups inject capital into automation niches such as AI RCM and ambient documentation, betting on carve-out opportunities where mega-vendors lack depth. Partnerships between cybersecurity specialists and EHR providers signal a move toward platform stewardship encompassing clinical functionality, financial integrity, and threat defense. The resulting environment keeps barriers high for new entrants yet rewards differentiated point solutions that can integrate cleanly into prevailing ecosystems across the clinical healthcare IT market.

Clinical Healthcare IT Industry Leaders

Epic Systems Corporation

Oracle Health (Cerner)

GE Healthcare

Cognizant Technology Solutions

Athenahealth

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: New Mountain Capital created Smarter Technologies, a USD 1.45 billion AI-driven revenue-cycle platform serving 500,000 providers.

- April 2024: Censinet, KLAS, and the American Hospital Association published a cybersecurity benchmarking study highlighting persistent supply-chain risk gaps.

- March 2025: Japan’s Ministry of Health released an alpha version of the standard electronic medical record for nationwide rollout by 2026.

- February 2025: American Relief Act extended Medicare telehealth flexibilities and hospital-at-home waivers for 90 days.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the clinical healthcare IT market as all spending on purpose-built software platforms and managed services that directly support patient-facing clinical workflows, including electronic health records, laboratory information management systems, tele-health platforms, picture archiving and communication systems, computerized provider order entry, billing, and e-prescribing modules. Revenues counted include new licenses, subscription fees, implementation, and maintenance services.

Scope exclusion: Purely administrative IT, such as HR, payroll, or supply-chain software, is not included.

Segmentation Overview

- By Software

- Electronic Health Records (EHR)

- Lab Information Management Systems (LIMS)

- Telemedicine and Tele-health Platforms

- Picture Archiving and Communication Systems (PACS)

- Computerized Provider Order Entry (CPOE)

- Other: Billing, Portals, E-Prescriptions

- By End-user

- Government and Public Health Agencies

- Private Hospitals and Diagnostic Centers

- By Delivery Model

- On-premise

- Cloud / SaaS

- Hybrid

- By Application

- Revenue-Cycle Management

- Clinical Decision Support

- Patient Engagement

- Population-Health and Analytics

- Tele-consultation

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Aisa-Pacific

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and surveys with hospital CIOs, pathology lab heads, payer informatics leads, cloud service integrators, and regional health authorities across the Americas, Europe, Asia-Pacific, and the Middle East validate adoption timing, price dispersion, and preferred deployment models, plugging the gaps that published statistics leave open before triangulation.

Desk Research

We start with structured desk work that mines OECD Health Statistics, CMS National Health Expenditure tables, Eurostat eHealth dashboards, and World Bank health outlays. Adoption ratios and maturity levels come from sources such as the Healthcare Information and Management Systems Society, national hospital federations, and peer-reviewed journals. Company 10-Ks, investor decks, and patent filings give price cues and technology lifecycles.

To deepen coverage, Mordor analysts reference D&B Hoovers for vendor financial splits, Dow Jones Factiva for contract news, and Questel for workflow-relevant patents. These illustrate the wider pool of secondary inputs; many other references are consulted during data collection and verification.

Market-Sizing & Forecasting

Our model applies a top-down build that begins with national health expenditure, extracts provider IT budgets, and allocates the clinical share using current adoption ratios and spend per bed. Bottom-up checks, including supplier roll-ups of EHR seats, tele-consult volumes, and sampled average selling price times volume, calibrate the totals. Inputs monitored include hospital bed additions, specialist visit volumes, interoperability mandates, subscription pricing trends, cloud penetration rates, and relevant currency conversions. Forecasts employ multivariate regression combined with scenario analysis to reflect macro health spending, regulatory shifts, and technology refresh cycles. Gap handling procedures adjust sampled ASPs or adoption curves when bottom-up variance exceeds five percent.

Data Validation & Update Cycle

Analysts run automated outlier scans, variance checks against vendor revenue, and multi-step peer reviews before sign-off. We refresh the dataset every twelve months, issuing interim revisions when policy changes, major M&A, or unforeseen public health events materially shift our assumptions.

Why Mordor's Clinical Healthcare IT Baseline Earns Trust

Published numbers for clinical healthcare IT diverge because firms differ on scope boundaries, price deflators, and refresh cadence. By sticking to a consistent clinical-only definition and annual data updates, Mordor Intelligence limits noise from administrative add-ons or outdated adoption ratios.

Key gaps arise when other publishers fold consumer apps into totals, ignore mixed-service contract splits, or apply static pricing across regions, which inflates or deflates values relative to our disciplined baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 530 B (2025) | Mordor Intelligence | |

| USD 420 B (2024) | Global Consultancy A | Excludes tele-health services and applies five-year-old adoption ratios |

| USD 760 B (2024) | Industry Journal B | Blends administrative IT and consumer wellness apps; uses PPP adjustments without currency-year alignment |

In summary, the disciplined scope, multi-source validation, and annual refresh that Mordor Intelligence follows give decision-makers a balanced, transparent baseline that traces directly to verifiable variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the clinical healthcare IT market?

The market is valued at USD 0.62 trillion in 2026 and is projected to reach USD 1.31 trillion by 2031.

Which software category holds the largest clinical healthcare IT market share?

Electronic Health Records lead with 41.60% share in 2025, reflecting their role as the core clinical documentation platform.

Why is cloud deployment growing so quickly in the clinical healthcare IT market?

Cloud and SaaS models already account for 61.20% of installations because they offer elastic compute for AI workloads and lower capital costs, supporting a 18.64% CAGR.

Which region is expanding fastest in the clinical healthcare IT market?

Asia Pacific shows a 16.32% CAGR, driven by government mandates such as Japan’s plan for nationwide EMR adoption by 2030.

How concentrated is vendor competition in the clinical healthcare IT market?

Epic Systems alone controls 42.3% of US acute-care EHR deployments, and the top five suppliers hold more than 80% of global revenue, indicating a highly concentrated landscape.

What role do interoperability regulations play in technology purchasing decisions?

Rules under the US 21st Century Cures Act, Germany’s Digital Act, and Japan’s FHIR standards require seamless data exchange, pushing providers toward vendors with proven API toolkits and compliance certifications.

Page last updated on: