Digital Assistants In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.07 Billion |

| Market Size (2031) | USD 12.7 Billion |

| Growth Rate (2026 - 2031) | 32.84% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

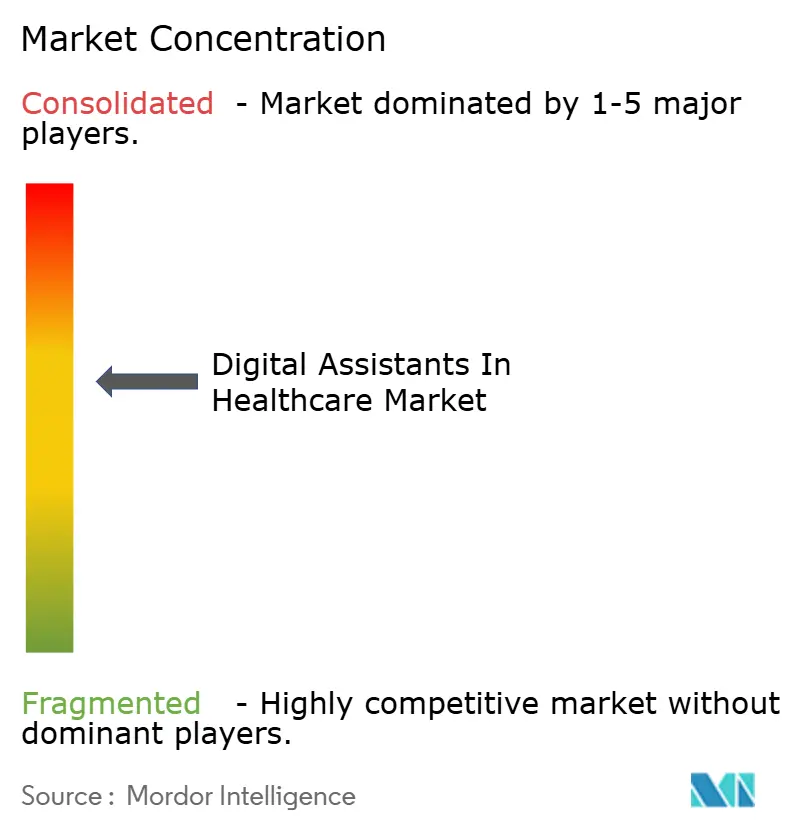

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Assistants In Healthcare Market Analysis by Mordor Intelligence

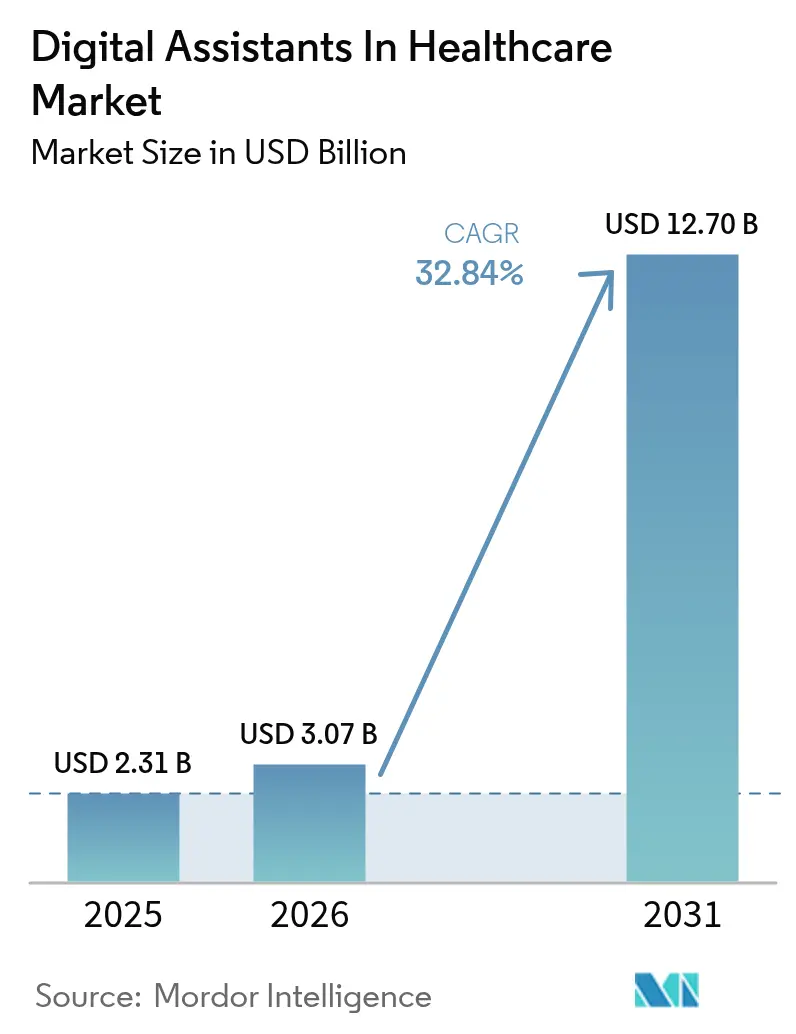

The digital assistants in healthcare market size was valued at USD 2.31 billion in 2025 and estimated to grow from USD 3.07 billion in 2026 to reach USD 12.7 billion by 2031, at a CAGR of 32.84% during the forecast period (2026-2031). Momentum stems from hospitals’ urgent need to ease staff shortages, the rise of value-based payments, and rapid advances in generative AI that now match clinical terminology with near-human fluency. Health systems view ambient intelligence as a strategic lever to automate documentation, triage, and monitoring, thereby cutting cost per encounter while improving safety. Converging reimbursement pathways—in particular Medicare’s hospital-at-home and remote-care codes—create clear return-on-investment signals that accelerate enterprise adoption. Competitive intensity is rising as technology giants layer healthcare-specific features onto their existing voice ecosystems, while specialist vendors differentiate through HIPAA-compliant data pipelines and EHR integration. Collectively, these forces point to sustained double-digit growth even as macro-economic conditions tighten across provider budgets.

Key Report Takeaways

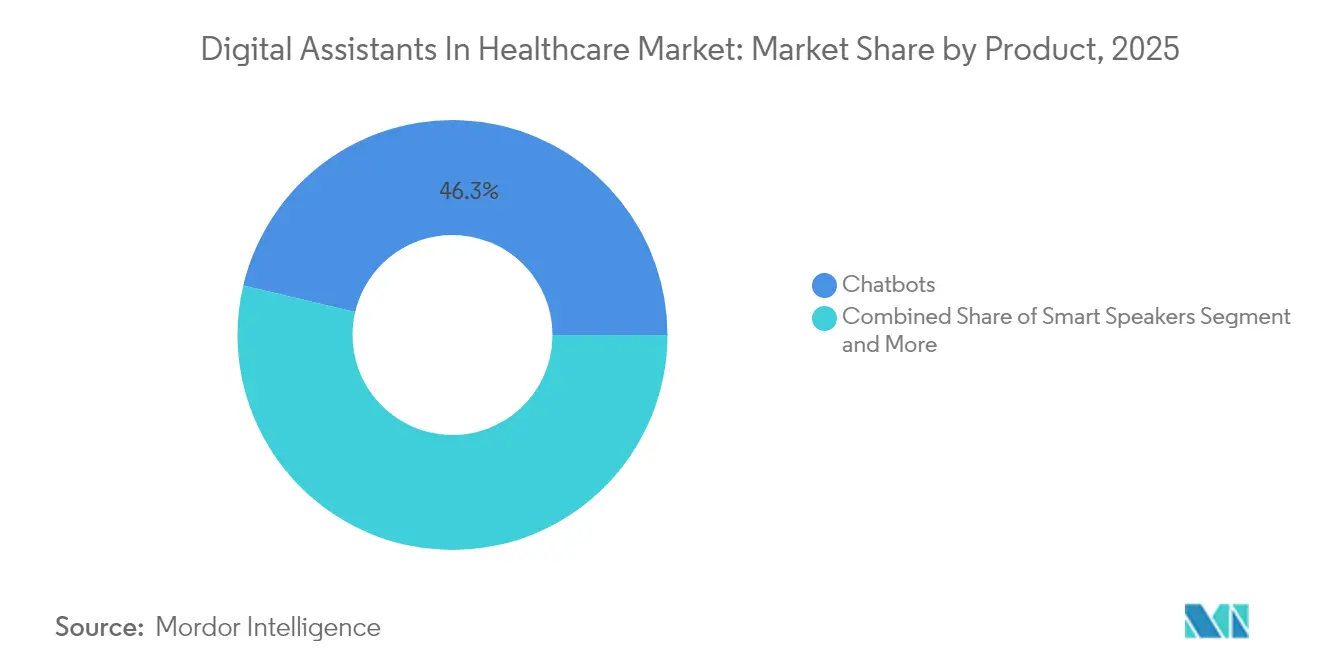

- By product, chatbots led with 46.30% revenue share in 2025; ambient AI sensors are projected to expand at a 43.9% CAGR through 2031.

- By user interface, automatic speech recognition held 50.90% of the digital assistants in healthcare market share in 2025, while multimodal systems post the fastest 46.2% CAGR to 2031.

- By application, symptom checking and triage accounted for 35.40% of the digital assistants in healthcare market size in 2025 and administrative workflow automation is advancing at a 40.3% CAGR.

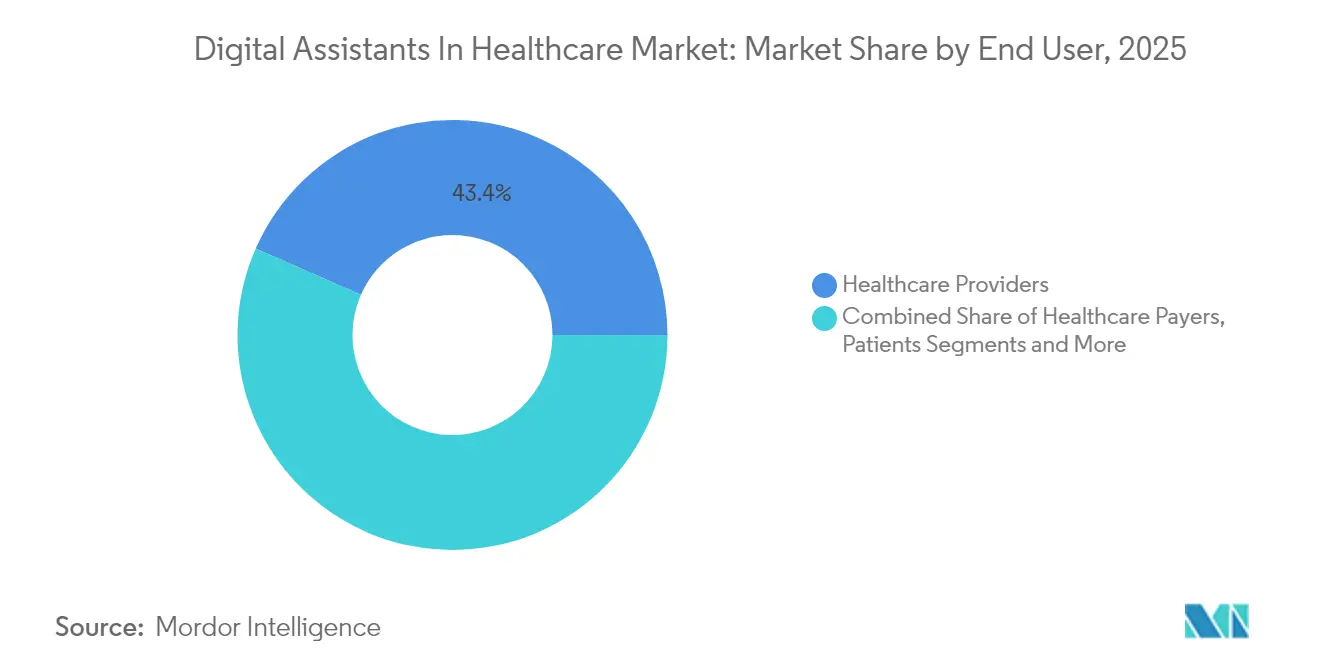

- By end user, healthcare providers captured 43.40% of 2025 revenue; pharmaceutical and med-tech companies chart the highest 38.1% CAGR to 2031.

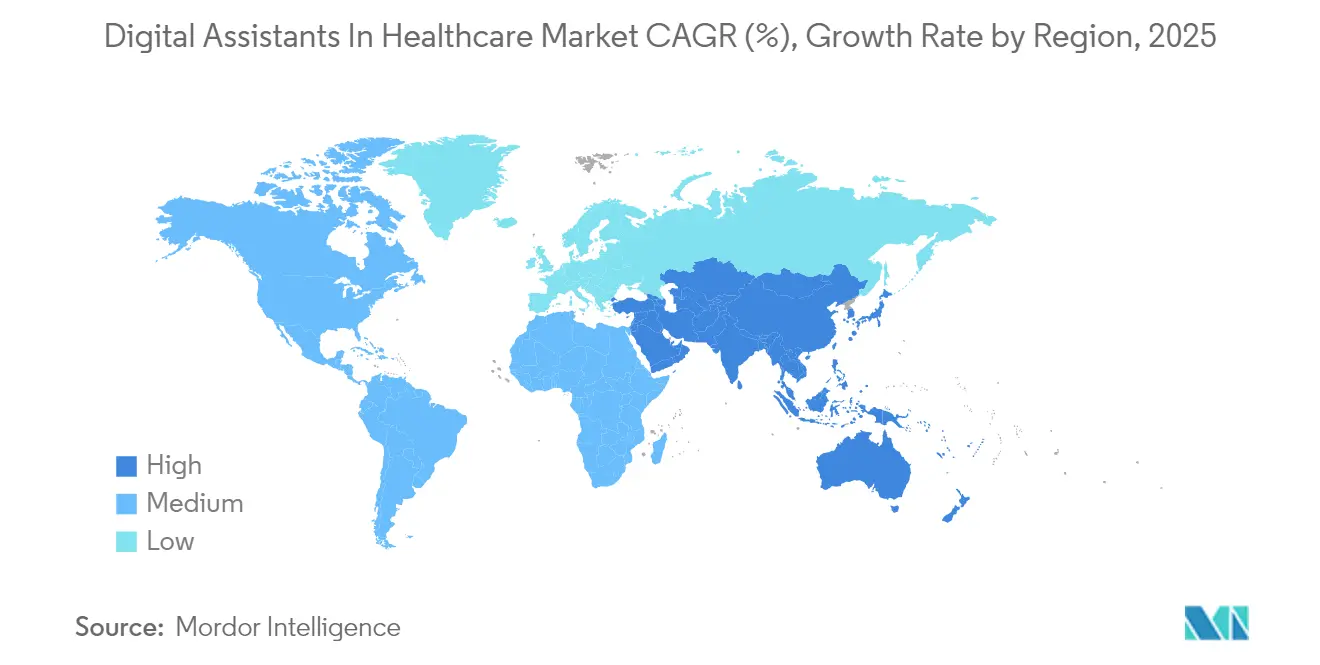

- By geography, North America commanded 37.60% of 2025 revenue, whereas Asia-Pacific is forecast to grow at 35.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Assistants In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing smartphone penetration and voice-AI familiarity | 6.2% | Global, with stronger adoption in APAC emerging markets | Medium term (2-4 years) |

| Rising chronic disease burden and remote-care demand | 8.1% | Global, concentrated in aging populations of North America, Europe, Japan | Long term (≥ 4 years) |

| Value-based care incentives for digital triage | 5.8% | North America and EU, with pilot programs in Australia | Medium term (2-4 years) |

| Generative-AI upgrades boost conversational accuracy | 7.3% | Global, led by US tech hubs with spillover to developed markets | Short term (≤ 2 years) |

| Provider workforce shortages accelerate virtual assistants | 9.2% | Global, most acute in rural areas of developed countries | Long term (≥ 4 years) |

| Hospital-at-home reimbursement fuels ambient AI nursing | 4.7% | North America, expanding to select EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Smartphone Penetration and Voice-AI Familiarity

Widespread consumer exposure to voice interfaces underpins smoother clinical adoption. Global smartphone penetration tops 85% across developed markets, and voice assistant users exceeded 4.2 billion in 2024, establishing habits that healthcare apps now leverage for onboarding and adherence.[1]Centers for Disease Control and Prevention, “Chronic Diseases in America,” cdc.gov Familiarity trims staff training outlays and accelerates go-live cycles, letting providers redeploy resources to high-acuity care. As patients increasingly expect healthcare encounters to echo consumer technology experiences, organizations prioritize natural language front ends over legacy portals. This shift explains why digital assistants in healthcare market deployments frequently center on mobile and smart-speaker channels that can serve multi-lingual populations.

Rising Chronic Disease Burden and Remote-Care Demand

Chronic conditions affect 6 in 10 US adults, driving payer penalties for avoidable admissions.[2]Centers for Disease Control and Prevention, “Chronic Diseases in America,” cdc.gov AI assistants deliver automated check-ins, medication nudges, and vitals escalation that collectively lower readmissions and emergency visits. Value-based contract structures magnify the financial upside: reduced acute events translate directly into shared-savings payments and quality bonuses. Remote monitoring programs aided by conversational AI have documented double-digit gains in adherence and earlier intervention windows. Consequently, providers view digital assistants not as optional add-ons but as core population-health infrastructure, pushing the digital assistants in healthcare market further into mainstream budgets.

Value-Based Care Incentives for Digital Triage

Medicare’s quality payment reforms reward hospitals that steer non-urgent cases away from emergency departments.[3]Centers for Medicare & Medicaid Services, “Innovation Center Strategy Refresh,” cms.gov AI-powered triage tools guide patients to telehealth, urgent care, or self-care, cutting ED overload by up to 30%. This immediate cost-avoidance fully offsets subscription fees in under 12 months for many systems, establishing a clear business case. Pilot programs in Australia and several EU states mirror US savings, signalling global scalability. As payers extend risk-sharing contracts to independent physician groups, demand broadens beyond IDNs, enlarging total addressable scope for the digital assistants in healthcare market.

Generative-AI Upgrades Boost Conversational Accuracy

Domain-tuned large language models launched in 2024–2025 now achieve near-expert comprehension of SNOMED and ICD-10 vocabularies, slashing transcription error rates. Faster inference on GPUs drops latency below 250 milliseconds, supporting real-time scribe and bedside queries. Clinicians report higher trust when AI can detect context such as medication allergies and social determinants, mitigating safety concerns. Vendors that bundle guardrails—automatic citation to drug databases and audit logs—gain accelerated security sign-offs. These breakthroughs expand addressable use cases from patient FAQs to order-set generation, turbo-charging the digital assistants in healthcare market’s revenue mix.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented EHR data limiting interoperability | -4.8% | Global; US most acute | Long term (≥ 4 years) |

| Regulatory uncertainty around AI clinical decisions | -3.2% | Global; national variance | Medium term (2-4 years) |

| High training cost for domain-specific language models | -2.9% | Global; impacts small providers | Short term (≤ 2 years) |

| Accent- and language-bias in voice UX | -1.7% | Diverse linguistic markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented EHR Data Limiting Interoperability

Siloed records force hospitals to build custom connectors before any assistant can retrieve allergies, meds, or discharge notes. Integration projects inflate budgets and delay ROI, discouraging smaller practices from deployment. Although the Trusted Exchange Framework progresses, competing EHR schemas still inhibit seamless read/write flows. Lack of unified data further limits algorithm accuracy, as assistants cannot surface full patient context. Until FHIR adoption becomes universal, fragmentation will temper the otherwise steep trajectory of the digital assistants in healthcare market.

Regulatory Uncertainty Around AI Clinical Decisions

The FDA’s evolving Software-as-a-Medical-Device guidance leaves grey zones around adaptive algorithms. Providers worry about malpractice exposure if AI output skews clinical judgment without clear liability rules. Vendors must bankroll rigorous validation studies, raising entry costs and weeding out under-capitalized startups. Different national stances, from EU AI Act risk-tiering to Japan’s sandbox approach, complicate multiregional roll-outs. Until harmonized frameworks emerge, many buyers restrict assistants to documentation and logistics rather than high-stakes diagnostic support, slightly damping near-term expansion of the digital assistants in healthcare market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Ambient AI Sensors Redefine Proactive Care

Chatbots retained 46.30% revenue in 2025, reflecting early-mover utility for symptom triage and FAQs. Ambient sensors, however, are scaling at a 43.9% CAGR as hospitals embed ceiling-mounted LIDAR and microphone arrays to flag falls, pain expressions, and code-blue precursors. North American hospital-at-home programs reimbursed by CMS now bundle ambient kits, lifting unit volumes sharply. Vendors integrate sensors with EHR alerts that auto-populate vitals and nursing notes, freeing scarce staff hours. As large health systems standardize ambient platforms, the digital assistants in healthcare market size for edge devices will exceed USD 4.6 billion by 2031. Meanwhile, smart speakers and voice apps continue penetrating outpatient and wellness use cases, ensuring chatbots remain an indispensable front door rather than a sunset technology.

Second-generation ambient solutions fuse radar, thermal imaging, and directional sound, capturing patient behaviors without wearables. Privacy-preserving on-device processing alleviates HIPAA risk and speeds response when deterioration is detected. The resulting data trove trains predictive algorithms that flag sepsis hours earlier than nurse rounds. Pharmacy chains piloting ambient booths for blood-pressure checks further widen adoption beyond hospitals. Collectively, these developments secure ambient sensors as the fastest compounder inside the digital assistants in healthcare market.

By User Interface: Multimodal Flexibility Becomes Table Stakes

Automatic speech recognition commanded 50.90% in 2025 due to physicians’ need for hands-free charting. Yet voice-plus-text systems log a 46.2% CAGR as vendors unify chat, email, and voice threads into a single patient record. Integration with mobile secure-messaging apps lets nurses escalate voice snippets with embedded vitals, minimizing hand-off friction. Sign-language avatars and real-time translation modules are entering pilots, addressing health-equity mandates. The digital assistants in healthcare market size for multimodal platforms is projected to surpass USD 3.55 billion by 2031.

Clinicians increasingly switch modalities mid-interaction: a bedside voice query becomes a text follow-up after rounds, all captured by the same LLM. This fluidity boosts satisfaction and eliminates duplicative entry. Vendors that expose open APIs for modality plug-ins achieve faster formulary approvals because hospital CIOs can swap in new accessibility features without core-system rewrites. As ambient microphones proliferate, silent alerts via tablet overlays balance noise-reduction initiatives, reinforcing multimodal dominance.

By Application: Administrative Automation Unlocks Immediate ROI

Symptom checking and triage retained 35.40% of 2025 spend, spring-boarding from consumer chat momentum. Administrative workflow automation, however, is expanding at a 40.3% CAGR, as CFOs tally the USD 100 billion annual clerical overhead dragging US healthcare. AI scribes now pre-populate 80% of encounter notes and suggest ICD-10 codes, shrinking average documentation time by 45%. That productivity translates into two extra patient slots per physician per day, a direct revenue lift that pays for licenses within weeks.

Hospitals also deploy assistants for prior-authorization forms, admission bed-matching, and discharge instructions, collectively shaving length-of-stay. Meanwhile, medication-adherence bots send personalized refill nudges, elevating pharmacy margins and Star ratings for payers. As reimbursement parity for virtual visits persists, triage chatbots shift toward self-service pre-visit intake, routing data straight to the EHR. These synergies cement administrative tasks as the prime engine powering the digital assistants in healthcare market.

By End User: Pharma and Med-Tech Surge Past Provider Growth

Providers still delivered 43.40% of 2025 revenue because systemic workflow pain sits squarely in hospitals and clinics. Yet pharma and med-tech companies are compounding at 38.1% as they embed conversational agents into patient-support programs and clinical-trial portals. Medication-specific bots walk patients through cold-chain handling, side-effect logging, and digital consent, raising adherence rates and lowering trial drop-outs. Digital twins generated by assistants guide R&D scientists through compound libraries, compressing early-stage discovery timelines.

Payers, though smaller today, invest in member-service chat that integrates benefits, provider search, and prior-auth status. Direct-to-consumer wellness apps build subscription-based care coaching, expanding the digital assistants in healthcare market beyond reimbursed channels. Vendors now package vertical-specific modules—prior-auth for payers, trial-recruit for pharma—enabling cross-sector expansion without custom code rewrites.

By Deployment Mode: Edge Computing Safeguards Data Sovereignty

Cloud remains mainstream thanks to elastic scaling and turnkey updates, yet edge and on-premise nodes are gaining share where data-residency laws tighten. European hospitals in France and Germany shift voice-transcription models onto local GPU appliances to satisfy GDPR’s minimal-transfer principles. Latency-sensitive use cases such as fall detection also benefit when processing happens bedside, avoiding 200-millisecond cloud hops. Hybrid architectures now dominate RFPs: capture and inference run on-prem, while model retraining occurs in regional clouds.

Cost curves improve as chip vendors release hospital-ready edge accelerators that fit standard server racks and draw sub-300 watts. Software containers orchestrate updates overnight without pulling sensitive data outside the firewall. These advances help edge instances scale from single wards to multi-facility networks, supporting the digital assistants in healthcare market where privacy and uptime trump raw cloud convenience.

Geography Analysis

North America retained 37.60% revenue share in 2025, buoyed by Medicare’s explicit reimbursement for remote monitoring codes that embed AI-generated vitals summaries directly into claims files. US health systems, pressured by a projected 200,000-nurse deficit through 2030, roll out ambient documentation across inpatient units, while Canada pilots province-wide triage chatbots to manage universal-care queues. Mexico’s IMSS digitization roadmap opens new tenders for Spanish-language AI navigators, hinting at broader regional growth.

Asia-Pacific posts the fastest 35.8% CAGR, propelled by China’s 2025 National AI-in-Healthcare action plan, which subsidizes hospital deployments of bedside voice assistants. India’s IT-services sector customizes low-cost multilingual models for domestic state hospitals and exports to Southeast Asia, balancing cost and vernacular nuance. Japan combats an aging population by outfitting nursing homes with edge-based fall-detection sensors, while South Korea’s 5G backbone enables hospital-wide real-time voice charting that feeds national health-insurance analytics.

Europe adopts cautiously yet steadily. Germany’s Gematik e-health agency mandates FHIR interoperability, giving compliant vendors an early advantage. The United Kingdom’s NHS invests in ambient scribe pilots tied to its Frontline Digitisation program, measuring clinician burnout reductions as key ROI. France and Italy emphasize multilingual, bias-audited models to serve immigrant populations under strict GDPR oversight. Nordic systems, already paper-free, experiment with AI-driven mental-health triage integrated into primary-care portals. Emerging Middle East and Africa markets pivot to digital assistants for tele-consult routing, especially in Saudi Arabia’s Vision 2030 clinics and the UAE’s smart-hospital builds, signaling fresh corridors for the digital assistants in healthcare market.

Competitive Landscape

Market structure is moderately fragmented: no single vendor commands more than one-fifth of global revenue, yet the top five collectively hold close to 55%. Microsoft’s 2024 completion of the Nuance integration positions its Dragon-powered DAX Copilot as the reference ambient documentation suite, now embedded in Epic and Cerner connectors. Amazon leverages Alexa Health’s new HIPAA secure-skill kit to penetrate elder-care deployments, while Google equips its MedLM suite with UpToDate citations for clinician trust.

Specialist players differentiate on niche depth. Abridge automates cardiology visit transcripts with accuracy tuned for murmurs and ejection fractions, winning Cleveland Clinic’s ambulatory rollout. Suki AI targets small practices with an affordable subscription bundle pairing voice dictation and CPT coding. Meanwhile, AvaSure partners with Oracle and NVIDIA to extend virtual nursing carts with bedside computer-vision analytics, combining GPU edge boxes for sub-second fall alerts.

Capital markets signal consolidation: Commure and Athelas acquired Augmedix for USD 340 million, creating a combined 20,000-facility footprint. Venture funding now favors scale-ups that secure multi-year IDN contracts over experimental point solutions. Vendors with robust compliance teams gain pricing power as FDA’s algorithm-change monitoring looms. Given these dynamics, the digital assistants in healthcare market is likely to tilt toward an oligopoly of platform providers supplemented by a vibrant layer of clinical-domain micro-vendors.

Digital Assistants In Healthcare Industry Leaders

Amazon.com Inc.

Microsoft Corporation

Google LLC

Apple Inc.

Babylon Healthcare Services Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Transcarent completed its merger with Accolade for USD 621 million, combining generative AI navigation with advocacy services.

- March 2025: AvaSure, Oracle, and NVIDIA launched an AI virtual care assistant to streamline hospital operations through ambient intelligence.

- March 2025: April Health and Wysa merged to unify behavioral-health conversational AI capabilities.

- February 2025: Commure and Athelas agreed to acquire Augmedix for roughly USD 340 million, forming the largest dedicated AI software provider in healthcare.

Global Digital Assistants In Healthcare Market Report Scope

A digital assistant is a computer program designed to assist users by answering questions and performing basic tasks. A Digital Assistant can speak different languages and can be controlled via voice or text messages. It can handle the user input and is able to memorize and process the data for self-learning.

The digital assistants in healthcare market is segmented by product (smart speakers and chatbots), user interface(automatic speech recognition, text-based, and text-to-speech), application (patient tracking, medical reference, diagnostic guides, drug dosage, medical calculators, nursing reference, and other applications), end user(healthcare providers, healthcare payers, and patients), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa).The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Smart Speakers |

| Chatbots |

| Voice-enabled Mobile Apps |

| Ambient AI Sensors |

| Automatic Speech Recognition |

| Text-based |

| Text-to-Speech |

| Multimodal (Voice + Text) |

| Patient Tracking and Monitoring |

| Medical Reference and Drug Info |

| Symptom Checking and Triage |

| Medication Adherence and Dosage |

| Administrative Workflow Automation |

| Others |

| Healthcare Providers |

| Healthcare Payers |

| Patients |

| Pharma and MedTech Companies |

| Others |

| Cloud-based |

| On-premise / Edge |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product | Smart Speakers | ||

| Chatbots | |||

| Voice-enabled Mobile Apps | |||

| Ambient AI Sensors | |||

| By User Interface | Automatic Speech Recognition | ||

| Text-based | |||

| Text-to-Speech | |||

| Multimodal (Voice + Text) | |||

| By Application | Patient Tracking and Monitoring | ||

| Medical Reference and Drug Info | |||

| Symptom Checking and Triage | |||

| Medication Adherence and Dosage | |||

| Administrative Workflow Automation | |||

| Others | |||

| By End User | Healthcare Providers | ||

| Healthcare Payers | |||

| Patients | |||

| Pharma and MedTech Companies | |||

| Others | |||

| By Deployment Mode | Cloud-based | ||

| On-premise / Edge | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the digital assistants in healthcare market?

The market stands at USD 3.07 billion in 2026 and is projected to reach USD 12.7 billion by 2031.

Which region holds the largest revenue share today?

North America leads with 37.60% of global revenue, supported by favorable Medicare reimbursement.

Which product segment is growing the fastest?

Ambient AI sensors are expanding at a 43.9% CAGR as hospitals deploy passive monitoring for safety and documentation.

How quickly is Asia-Pacific expanding in this space?

Asia-Pacific registers a strong 35.8% CAGR through 2031 on the back of government digitization programs and aging demographics.

Why are pharmaceutical companies adopting digital assistants at a high rate?

They leverage conversational AI for clinical-trial recruitment, patient education, and adherence support, producing a 38.1% CAGR within the segment.

What is the main barrier limiting broader adoption?

Fragmented EHR data interoperability remains the top hurdle, shaving an estimated 4.8% from the potential CAGR until standards mature.

Page last updated on: