Healthcare Chatbots Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

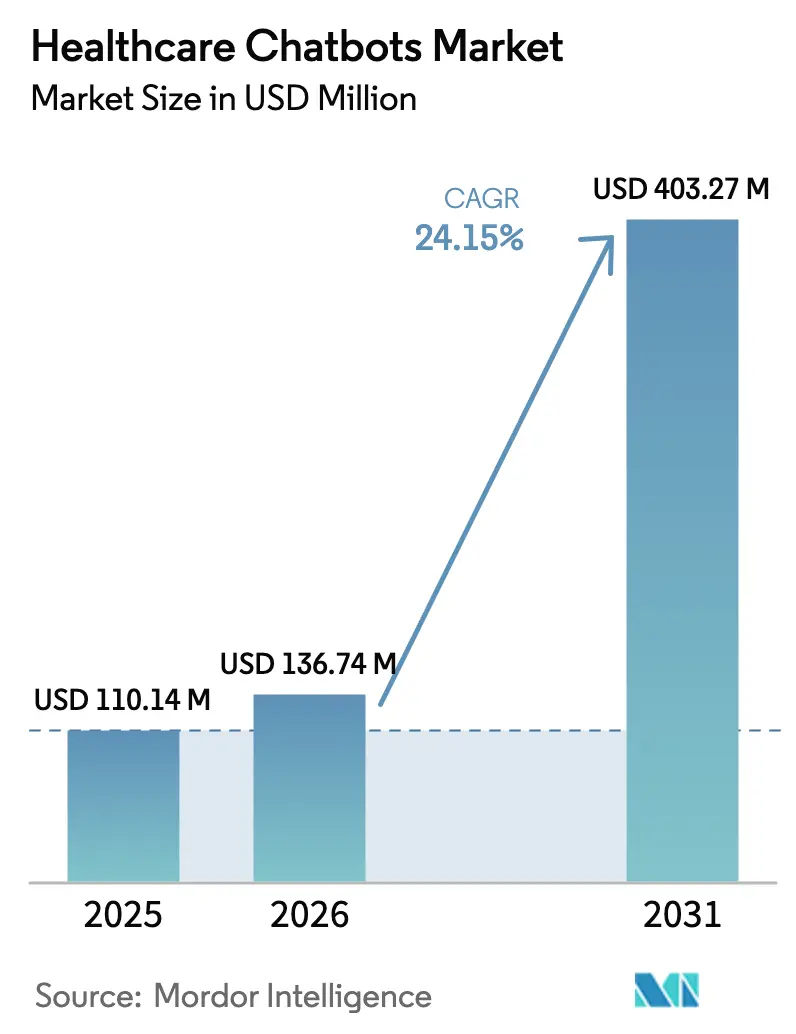

| Market Size (2026) | USD 136.74 Million |

| Market Size (2031) | USD 403.27 Million |

| Growth Rate (2026 - 2031) | 24.15% CAGR |

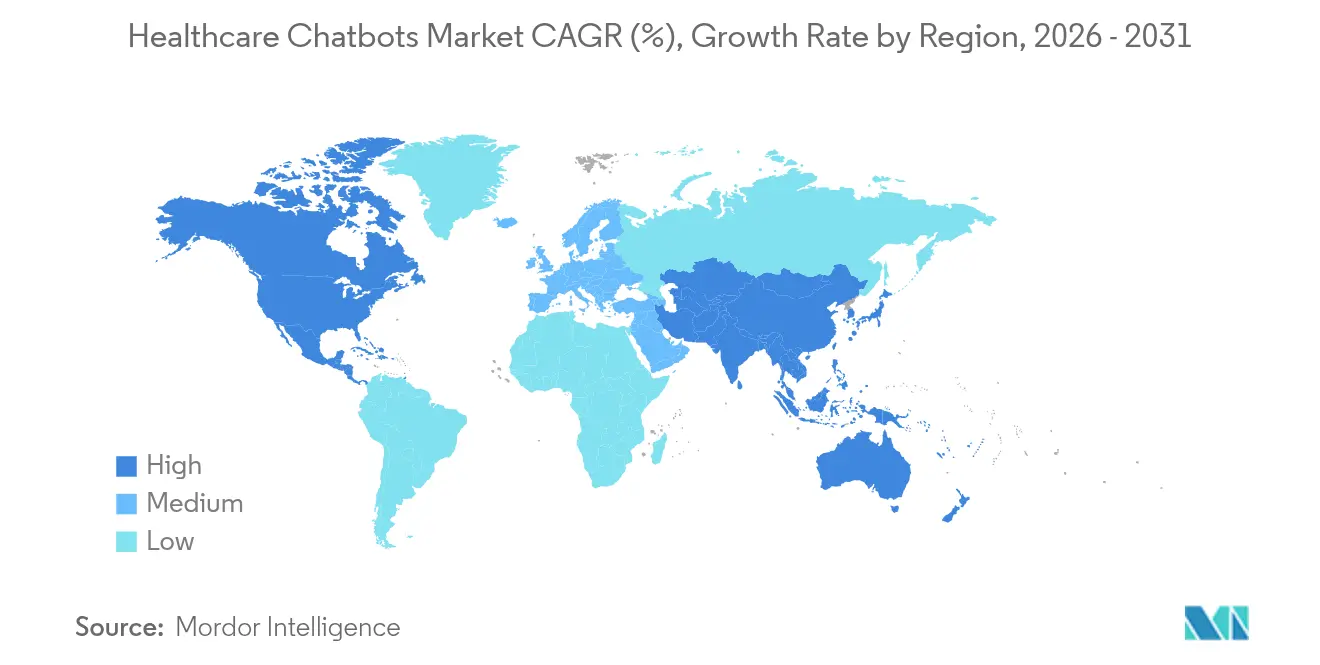

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Chatbots Market Analysis by Mordor Intelligence

healthcare chatbots market size in 2026 is estimated at USD 136.74 million, growing from 2025 value of USD 110.14 million with 2031 projections showing USD 403.27 million, growing at 24.15% CAGR over 2026-2031. Robust artificial-intelligence innovation, rising clinician shortages, and clear reimbursement pathways elevate conversational AI from pilot projects to core digital front-door infrastructure for hospitals and payers. North America sustains its leadership on the back of mature EHR connectivity, while Asia-Pacific becomes the fastest-growing region as smartphone penetration bridges care-access gaps. Software remains the principal revenue engine, yet service-oriented revenues accelerate as providers seek implementation partners to navigate HIPAA, GDPR, and FDA requirements. Meanwhile, hybrid deployments gain ground because large health systems want cloud elasticity without surrendering data-sovereignty control.

Key Report Takeaways

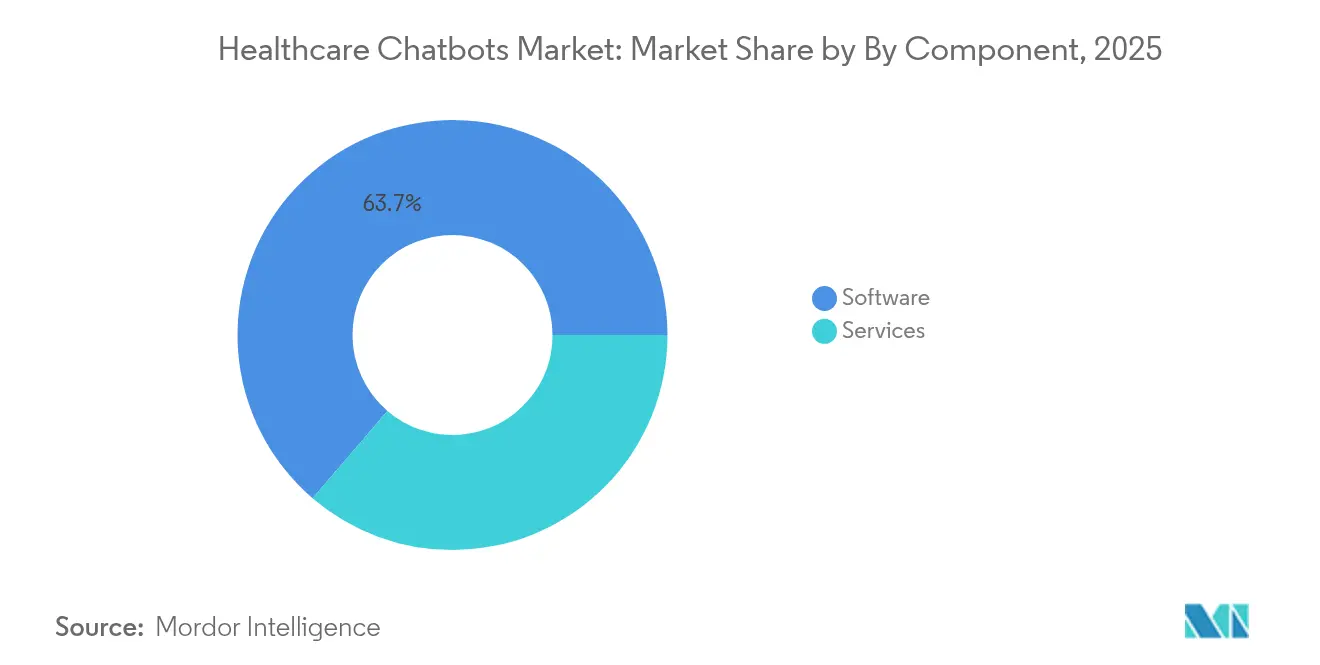

- By component, software captured 63.72% revenue in 2025; services are forecast to grow at a 23.12% CAGR to 2031.

- By deployment, cloud accounted for 69.35% of the healthcare chatbots market share in 2025; hybrid architectures are expanding at 27.05% CAGR through 2031.

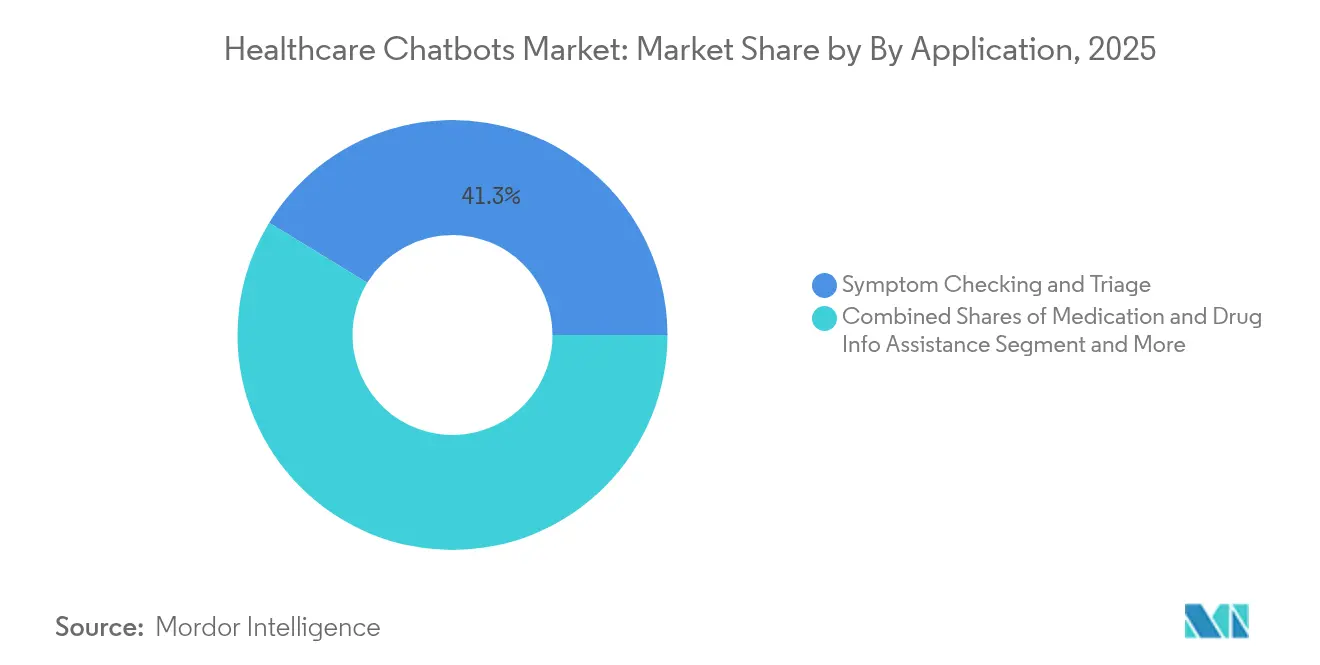

- By application, symptom checking held 41.25% of the healthcare chatbots market size in 2025, while mental-health coaching is advancing at a 30.65% CAGR between 2026-2031.

- By end-user, providers led with 46.05% share of the healthcare chatbots market in 2025; the patients & caregivers segment posts the fastest projected CAGR at 24.48%.

- By geography, North America retained 36.96% revenue share in 2025; Asia-Pacific is set to grow at 25.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Chatbots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI and NLP breakthroughs | +6.2% | Global; North America and Asia-Pacific lead | Medium term (2-4 years) |

| Growth of remote-care ecosystems | +5.8% | Global; strongest in rural areas | Short term (≤ 2 years) |

| Smartphone and broadband penetration | +4.1% | Asia-Pacific core; spill-over to MEA | Long term (≥ 4 years) |

| Reimbursement codes for digital front doors | +3.9% | North America and EU | Medium term (2-4 years) |

| Workforce burnout driving triage adoption | +3.2% | Global; acute in developed markets | Short term (≤ 2 years) |

| Newly introduced CPT reimbursement codes | +2.5% | North America; spreading to EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI and NLP breakthroughs enable clinical-grade conversational interfaces

Large language models trained on medical corpora now achieve diagnostic accuracy above 80%, letting chatbots shift from FAQ bots to decision-support companions[1]Microsoft, “Azure Health Bot Documentation,” microsoft.com. Microsoft’s integration of generative AI into Azure Health Bot embeds safety guardrails and EHR hooks, while Hippocratic AI’s Polaris constellation architecture assigns sub-models to empathy, safety, and compliance tasks, yielding nuanced yet regulated exchanges. This evolution underpins the healthcare chatbots market’s migration toward clinician-facing workflows.

Growth of remote-care ecosystems accelerates digital front-door adoption.

Hospitals facing staffing gaps now use chatbots as first-line triage to cut phone queues and streamline scheduling. The 2025 AMA CPT update added seven AI taxonomy codes that reimburse chatbot-mediated triage, flipping the business case from cost center to revenue source. TatvaCare’s Azure OpenAI rollout processes 180,000 prescriptions monthly at 95% accuracy, illustrating scale achievable once reimbursement risk is removed.

Smartphone and broadband penetration enables multilingual patient engagement.

Emerging-market health systems deploy mobile-first chatbots to bypass clinician shortages. The Medical City Clinic’s Med-C handles 10,400 chats each month across Tagalog, Cebuano, and Taglish, lifting patient engagement by 273% in its first quarter. China’s virtual-hospital pilots show how self-evolving AI doctors will extend care to areas with sparse physician density by 2025.

Reimbursement codes for digital front doors create sustainable business models

Payers such as UnitedHealthcare now reimburse AI-mediated touchpoints if clinicians supervise documentation, anchoring chatbot investments in predictable revenue streams. Northwestern Medicine reports 40% radiology efficiency gains after deploying Microsoft-backed conversational agents, tying financial returns to measurable clinical outcomes.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cyber-security concerns | -4.8% | Global; heightened in EU | Short term (≤ 2 years) |

| Limited clinical-grade validation | -3.6% | Global; strictest in US | Medium term (2-4 years) |

| Liability ambiguity in algorithmic triage | -2.9% | North America and EU | Long term (≥ 4 years) |

| Multilingual training-data scarcity | -2.1% | APAC and MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and cyber-security concerns constrain enterprise adoption.

Two JAMA viewpoints warn that generative chatbots can infer protected health information absent business-associate agreements, exposing providers to HIPAA penalties. A 2025 survey shows 67% of health institutions feel unprepared for looming security mandates, deterring full-scale deployments beyond low-risk use cases[2]SPRY, “Healthcare Security Readiness Survey 2025,” spry.com. This leads smaller providers to restrict chatbots to appointment reminders until clearer liability frameworks emerge.

Limited clinical-grade validation creates adoption hesitancy.

FDA guidance on clinical decisions support still clashes with rapid AI iteration, leaving most language models without clearance for diagnostic recommendations. Over 1,200 patents have been filed for medical chatbots since 2022, yet large-scale randomized trials remain scarce, keeping many provider boards cautious and limiting expansion of the healthcare chatbots market into high-stakes therapeutic arenas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Faces Services Acceleration

Software generated 63.72% of the healthcare chatbots market revenue in 2025 as providers sought ready-made NLP engines and integration toolkits. The healthcare chatbots market size for software is projected to continue expanding, yet services are catching up at a 23.12% CAGR because health systems need partners for HIPAA audits, workflow tuning, and post-go-live optimization.

Managed-service contracts now have bundle model monitoring, bias checks, and periodic domain-retraining. Microsoft’s Azure Health Bot, which ships pre-configured triage templates and regulator-approved ontologies, exemplifies the shift toward platform-plus-services packages.

By Deployment: Cloud Leadership Challenged by Hybrid Growth

Cloud deployments held 69.35% healthcare chatbots market share in 2025 thanks to elastic scaling and pay-as-you-go economics. Hybrid models are growing 27.05% annually as CIOs marry cloud NLP processing with on-premises data stores to satisfy GDPR and state privacy statutes. Hybrid adoption pushes vendors to offer containerized inference runtimes that allow edge inference for PHI while routing anonymized intent data to public clouds for retraining.

Saga Prefecture’s Oda Hospital runs its nursing-summary generator fully on-premises, proving that small facilities can harness large models without outbound data flow. DeepSeek’s appliance-style deployments cater to similar sovereignty demands, underlining the strategic role of hybrid models.

By Application: Symptom Checking Leads, Mental Health Accelerates

Symptom-checker bots claimed 41.25% of 2025 revenue as they directly relieve call-center congestion. The healthcare chatbots market size for mental-health coaching is forecast to expand fastest at 30.65% CAGR, mirroring clinician shortages in psychiatry. Chatbots now supply evidence-based CBT scripts in multiple languages, widening access for underserved populations.

Yet scaling mental-health bots also underscores validation gaps. Woebot Health, once consumer-facing, shuttered its public app in 2025 to refocus on regulated clinical pathways, demonstrating that proof of efficacy remains pivotal.

By End-User: Providers Lead, Patients Accelerate Adoption

Providers captured 46.05% of demand in 2025, motivated by labor-savings targets and value-based reimbursement. Patients and caregivers, however, are the fastest growers at 24.48% CAGR as millennials and Gen Z prefer self-service triage before scheduling.

Stanford Health Care’s ChatEHR shows how clinician-facing bots cut documentation time, while direct-to-consumer symptom-checker apps now integrate pharmacy fulfillment, reinforcing patient segment momentum.

Geography Analysis

North America retained 36.96% healthcare chatbots market share in 2025, buoyed by integrated EHR ecosystems and reimbursement policies that treat AI triage like billable telehealth encounters. Collaborations such as Microsoft’s Healthcare Agent Orchestrator give US health systems fast-track playbooks for scaled deployments. Asia-Pacific is posting a 25.15% CAGR, the highest worldwide, as governments embrace chatbots to offset clinician shortages. China’s self-evolving virtual hospital initiative debuts publicly in 2025, and Japan’s AI Sakura pilot automates reception tasks, foreshadowing mainstream adoption. The Philippines’ multilingual Med-C success underscores regional appetite for culturally conscious bot experiences. Europe grows steadily amid GDPR constraints that slow clinical-grade rollouts; nevertheless, single-payer systems in Scandinavia and the UK are piloting chatbots to manage chronic-disease follow-up. The Middle East and Africa leverage mobile ubiquity for vaccination reminders, and Brazil in South America explores bots for maternal-health outreach, indicating future addressable-market upside.

Competitive Landscape

The healthcare chatbots market is moderately fragmented yet trending toward consolidation. Platform leaders Microsoft and Google supply cloud NLP backbones, letting niche firms specialize in cardiology, oncology, or mental health scripts. Microsoft-Northwestern Medicine collaboration improved radiology throughput 40%, exemplifying outcome-based differentiation.

Acquisitions are rising: Mediktor bought Sensely for global reach; Sagility picked up BirchAI for generative design; Transparent purchased Accolade for USD 621 million to fuse navigation with benefits management. Intellectual-property filings around safety-layer orchestration, such as Hippocratic AI’s Polaris patent, add defensible moats. As regulatory demands escalate, firms with combined clinical and technical muscle are gaining share while pure-tech entrants lacking HIPAA expertise struggle to scale.

Public cloud providers pursue healthcare-specific blueprints—Azure Health Bot now ships pre-validated intents, and Google Cloud’s Vertex AI Search and Conversation for healthcare launched secure context windows that respect PHI boundaries. These moves consolidate power around infrastructure vendors while keeping the application layer open for innovators.

Healthcare Chatbots Industry Leaders

Ada Health GmbH

Babylon Inc.

Microsoft Corporation

Infermedica Sp. z o.o.

Sensely, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TXP Medical began a generative-AI voice-input pilot at Japan’s National Center for Child Health and Development, converting spoken notes into structured records to curb clinician workload TXP Medical.

- May 2025: Microsoft introduced Healthcare Agent Orchestrator to coordinate multi-agent workflows across patient journeys HIT Consultant.

- April 2025: Google Cloud expanded AI agent tools tailored to healthcare operations Healthcare Dive.

- April 2025: Omi Japan announced hospital-ready AI agents to automate reception and nursing tasks, with EMR integration slated for 2025 PR Times.

Global Healthcare Chatbots Market Report Scope

Chatbots are automated tools that simulate intelligent conversations with human users. In the healthcare sector, AI-powered chatbots efficiently manage simple inquiries, offering users a convenient means to access information.

The healthcare chatbots market is segmented by component (software, services [managed services, professional services]), deployment (cloud, on premises), end-user (patients, healthcare providers, insurance companies, others), geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). the market size and forecasts are provided in terms of value (USD) for all the above segments.

| Software | NLP Engine |

| ML/Deep-Learning Framework | |

| Integration and UX Layer | |

| Services | Managed Services |

| Professional Services |

| Cloud |

| On-premise |

| Hybrid |

| Symptom Checking and Triage |

| Medication and Drug Info Assistance |

| Appointment Scheduling and Reminders |

| Mental-Health and CBT Coaching |

| Remote Patient Monitoring Support |

| Claims and Insurance Assistance |

| Others |

| Healthcare Providers |

| Payers / Insurance Companies |

| Patients and Caregivers |

| Life-Science and CROs |

| Others (Employers, Public Health Agencies) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| By Component | Software | NLP Engine | |

| ML/Deep-Learning Framework | |||

| Integration and UX Layer | |||

| Services | Managed Services | ||

| Professional Services | |||

| By Deployment | Cloud | ||

| On-premise | |||

| Hybrid | |||

| By Application | Symptom Checking and Triage | ||

| Medication and Drug Info Assistance | |||

| Appointment Scheduling and Reminders | |||

| Mental-Health and CBT Coaching | |||

| Remote Patient Monitoring Support | |||

| Claims and Insurance Assistance | |||

| Others | |||

| By End-user | Healthcare Providers | ||

| Payers / Insurance Companies | |||

| Patients and Caregivers | |||

| Life-Science and CROs | |||

| Others (Employers, Public Health Agencies) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

How big is the healthcare chatbots market today?

The market is valued at USD 136.74 million in 2026 and is set to climb to USD 403.27 million by 2031 at a 24.15% CAGR.

Which region grows fastest over the forecast period?

Asia-Pacific leads growth with a 25.15% CAGR through 2031, fueled by smartphone ubiquity and government digital-health initiatives.

What application segment records the highest CAGR?

Mental-health and cognitive-behavioral therapy coaching posts the fastest rise at 30.65% CAGR, responding to behavioral-health clinician shortages.

Why are hybrid deployments gaining traction?

Hybrid models address data-sovereignty and privacy mandates by keeping PHI on-premise while leveraging public-cloud compute for NLP scalability.

How are reimbursement changes influencing adoption?

New AMA CPT and payer policies now reimburse AI-mediated triage, turning chatbots from cost centers into revenue-generating services for providers.

Page last updated on: