Hazmat Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.11 Billion |

| Market Size (2031) | USD 16.96 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

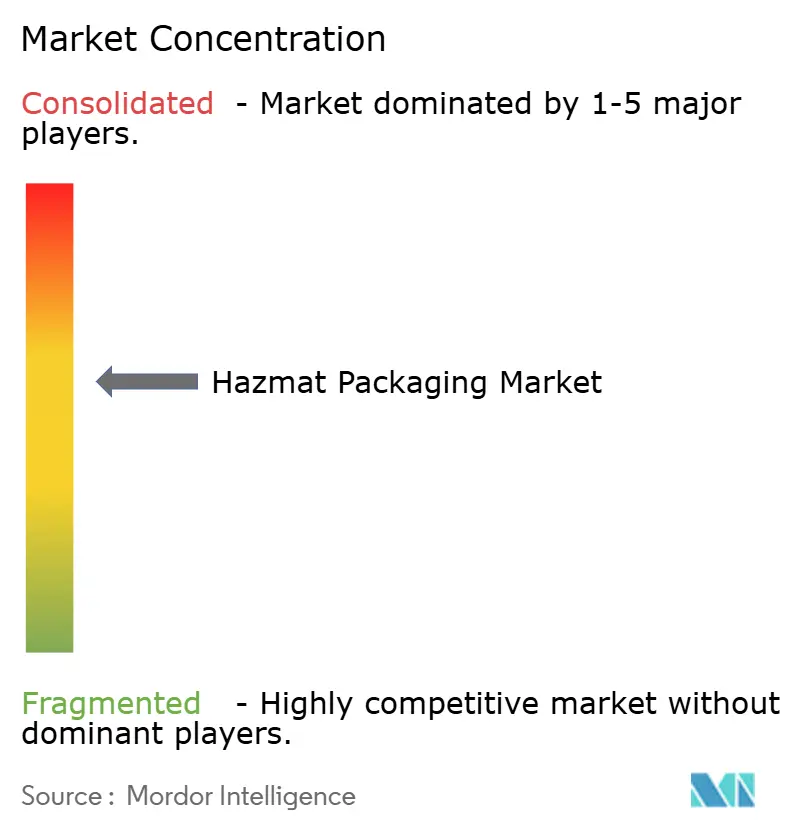

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hazmat Packaging Market Analysis by Mordor Intelligence

The Hazmat Packaging Market size was valued at USD 12.45 billion in 2025 and estimated to grow from USD 13.11 billion in 2026 to reach USD 16.96 billion by 2031, at a CAGR of 5.29% during the forecast period (2026-2031). This growth is based on converging global rules that align land- and sea-based transport codes, sustained expansion of chemical output, and stronger demand for smart containers that reduce product loss. Standardization under the ADR 2025 and IMDG 2024 updates lowers compliance friction for multinational shippers while creating entry barriers for small local firms. Supply-side rationalization continued in 2024, when raw material price swings of up to 27% compressed margins, accelerating consolidation among vertically integrated suppliers. Smart-ready packaging generates service revenues and helps large incumbents differentiate themselves, while the pharmaceutical sector’s above-market 6.16% expansion channels additional demand toward cold-chain formats and serialized labels under the Drug Supply Chain Security Act.

Key Report Takeaways

- By product type, drums captured 38.05% of the hazmat packaging market share in 2025.

- By material, the hazmat packaging market size for plastic is projected to grow at a 5.81% CAGR from 2026 to 2031.

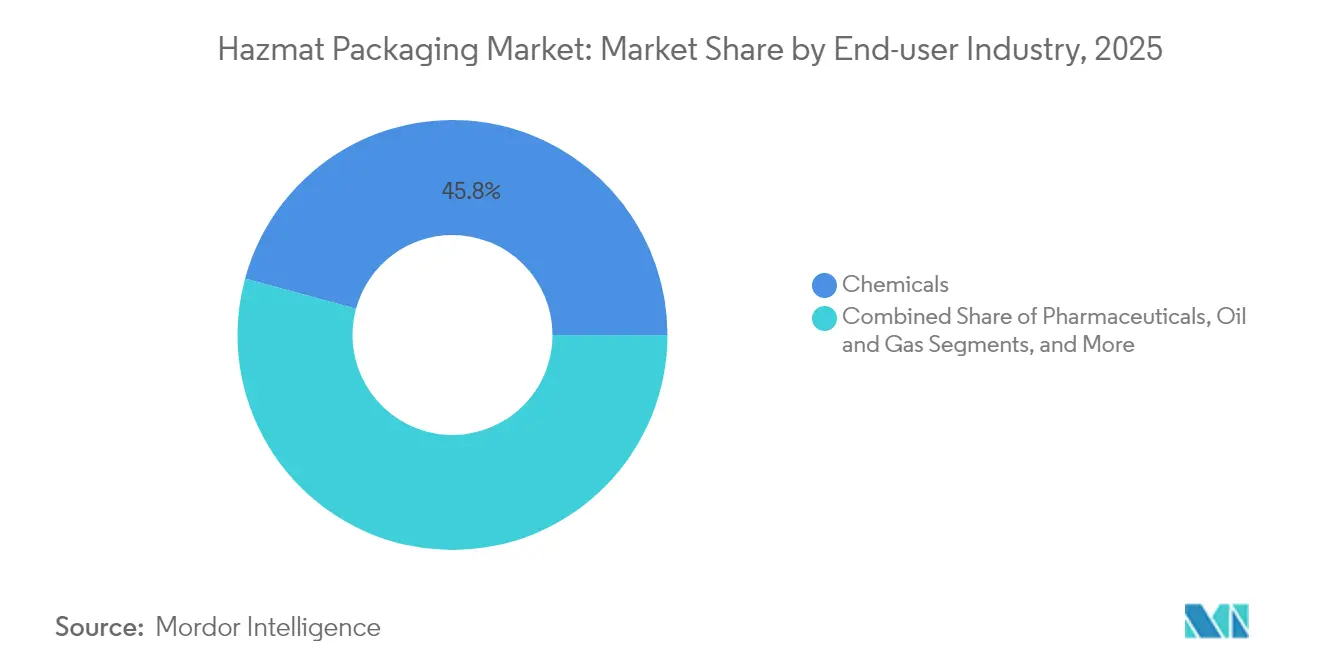

- By end-user industry, chemicals captured 45.76% of the hazmat packaging market share in 2025.

- By geography, Asia-Pacific captured 45.05% of the hazmat packaging market share in 2025 and is projected to grow at a 6.55% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hazmat Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global Regulations on Hazardous-Goods Transport and Storage | +1.2% | Global, with strongest impact in EU and North America | Medium term (2-4 years) |

| Expanding Chemical and Petrochemical Production Capacity Worldwide | +1.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Growth In Cross-Border E-Commerce of Regulated Chemicals | +0.9% | Global, early gains in North America and Europe | Short term (≤ 2 years) |

| Shift Toward Reusable UN-Certified Drums and IBC Reconditioning | +0.7% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Adoption Of Smart Packaging with IoT Sensors for Real-Time Condition Monitoring | +0.5% | North America and EU initially, APAC adoption following | Long term (≥ 4 years) |

| Venture Funding for Innovative Barrier Materials and Corrosion-Resistant Composites | +0.3% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent global regulations on hazardous-goods transport and storage

Harmonization between ADR 2025 and the IMDG 2024 code tightens marking, documentation, and testing norms, prompting USD 2.8 billion in manufacturer compliance upgrades during 2024. Large enterprises absorb these costs across diversified lines, gaining scale economy advantages, whereas regional specialists often face certification delays that limit export eligibility. More uniform rules reduce shipment rejections at borders and shorten customs dwell times, encouraging shippers to consolidate volumes through suppliers with proven audit records. The measurable payoff is evident in falling accident rates and lower insurance premiums, reinforcing customer preference for fully certified packaging providers.

Expanding chemical and petrochemical production capacity worldwide

China added 47 petrochemical plants in 2024, raising nameplate output by 12 million metric tons and lifting local demand for high-capacity drums and IBCs. India’s active-pharmaceutical-ingredient hub expanded output 11% in the same year, translating into larger orders for corrosion-resistant composite containers that satisfy both domestic and export controls.[1]China Petroleum and Chemical Industry Federation, “Industry Development Report 2024,” cpcia.org.cn Extra capacity incentivizes bulk shipment policies; continuous-process sites favor 1,000-liter IBCs over 200-liter drums to trim labor and pallet movements. This pivot toward bulk solutions underpins the steady value growth of the hazardous materials packaging market through 2030.

Growth in cross-border e-commerce of regulated chemicals

Customs data show a 23% surge in online chemical transactions in 2024, with midsize laboratories and specialty coatings formulators purchasing directly from overseas sellers. These smaller-lot trades demand right-sized, multi-certified packs such as 20-liter pails or 5-liter bottles, each labeled for air, road, and sea compliance. Online buyers also insist on granular track-and-trace status, which intensifies the uptake of embedded QR codes and sensor badges that feed shipment data into cloud dashboards. This digital backbone blurs the line between packaging supplier and logistics service provider, nudging incumbents toward end-to-end visibility offerings.

Shift toward reusable UN-certified drums and IBC reconditioning

Volatile steel and polymer prices in 2024 heightened customer demand for multi-trip containers, which spread the cost across several cycles. Reconditioning specialists now offer certified cleaning services that return steel drums to service within 48 hours, meeting stringent UN performance tests while cutting per-trip cost by up to 35%. Sustainability goals complement this economic logic; multinational chemical producers are increasingly setting reuse targets that favor standardized returnable fleets. Early adopters in Europe report double-digit reductions in carbon footprint compared to single-use packaging, validating the reuse model and anchoring its medium-term impact on demand patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Steel and Polymer Resin Prices Impacting Container Costs | -0.8% | Global, most severe in regions with limited raw material access | Short term (≤ 2 years) |

| Fragmented Global Regulatory Landscape Raising Compliance Complexity | -0.6% | Global, particularly affecting cross-border trade | Medium term (2-4 years) |

| Limited Recycling Infrastructure for Contaminated Plastic Drums | -0.4% | EU and North America primarily, expanding globally | Long term (≥ 4 years) |

| Counterfeit UN Certification Marks Eroding End-user Confidence | -0.3% | APAC and MEA regions primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in steel and polymer resin prices impacting container costs

Steel price swings of up to 27% in 2024, mirrored by high-density polyethylene variability, forced many suppliers to adopt surcharge clauses or hedge positions to protect their margins. Shippers reacted by renegotiating contract durations and substituting materials where feasible, adding forecasting complexity across the value chain. Price instability also incentivized greater interest in reusable fleets and alternative composites, slightly dampening short-term unit demand growth even as long-term value prospects remain solid.

Fragmented global regulatory landscape raising compliance complexity

Although major regimes are converging, more than 65 sovereign authorities still publish unique packaging interpretations that can apply to a single multimodal shipment. Documentation errors can lead to shipment delays, non-compliance fines, or forced product recalls, resulting in hidden costs that deter new entrants. Established providers invest in proprietary regulatory databases and in-house compliance teams to navigate this maze, but the cumulative burden slows transaction velocity and modestly suppresses market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bulk Solutions Drive Market Evolution

Drums retained a 38.05% share in 2025, driven by their universal familiarity, broad chemical compatibility, and well-established reverse logistics networks. Within the hazmat packaging market, large petrochemical shippers continue to favor 200-liter steel drums for flammable liquids that require fire resistance, while corrosive-acid producers are migrating to plastic variants that minimize residue contamination. IBCs, offering capacities from 500 to 1,250 liters, captured momentum with a 6.14% CAGR outlook through 2031, reflecting their role in cutting pallet movements and warehouse touches. The hazmat packaging market size for IBCs is projected to expand by at least USD 1.07 billion between 2026 and 2031, aligning with continuous process upgrades in the Asia-Pacific region.

Pails and bottles fill niche demand where metered dosing or laboratory testing are not feasible. Pharmaceutical compounders specify tight-tolerance, small-volume bottles compatible with clean-room handling, reinforcing premium unit pricing. Composite packs combine metal, plastic, and fiber layers to meet stringent performance requirements for oxidizers or temperature-sensitive materials, although this hybrid category accounts for less than 4.88% of 2025 sales. Across formats, suppliers emphasize compatibility charts, stacking strength data, and leakage test certifications to help shippers simplify material selection under evolving global codes. Innovation attention now turns to collapsible IBC bladders that shrink return freight costs, promising incremental share gains over the forecast horizon.

By Material Type: Plastics Dominance Faces Sustainability Pressure

Plastics accounted for 55.31% of turnover in 2025, with high-density polyethylene favored for its resistance to acids and bases, and polypropylene for its solvent compatibility. Lightweight design, low corrosion risk, and moldability underpin the plastic packaging market’s leadership in hazardous materials. The segment’s 5.81% forecast CAGR is derived from chemical capacity additions in the Asia-Pacific region and the pharmaceutical industry’s need for non-reactive containers. However, regulatory and brand pressure surrounding the disposal of contaminated plastics intensifies, nudging buyers toward recyclable resins and certified reconditioning loops.

Metal, primarily carbon steel drums, retains an indispensable role for flammable and high-pressure chemicals where thermal stability is paramount. Drum makers address weight and rust concerns by incorporating advanced inner coatings that extend life cycles by an average of 18 months. Fiber and corrugated solutions contribute a modest volume but occupy strategic niches in combination packaging kits, especially for air transport, where stringent inner-pack requirements are applied. The hazmat packaging market share for metal remains resilient at roughly 23.82% thanks to oil-field service contracts and hazardous waste transport duties. Market entrants explore aluminum-polymer hybrids aimed at weight reduction while preserving spark resistance, though commercial adoption will hinge on cost parity with steel.

By End-user Industry: Pharmaceutical Sector Accelerates Growth

Chemicals accounted for 45.76% of 2025 revenue, reflecting the sector’s breadth across aromatics, solvents, and specialty intermediates. Bulk chemical logistics platforms place consistent volume through established drum and IBC networks, generating steady replacement cycles. The pharmaceutical vertical, although smaller today, posts the highest 6.03% CAGR, driven by rising active-ingredient output and the cold chain’s strict temperature and serial-number tracking mandates. The hazmat packaging market size for pharma-grade packs is expected to climb from around USD 2.02 billion in 2026 to over USD 2.71 billion in 2031.

Oil and gas exploration specifies ruggedized containers for drilling fluids and well-stimulation chemicals that must resist extreme field conditions. Agriculture relies on UN-certified pails and bottles for pesticides and herbicides, subject to national environmental agencies’ labeling rules. Electronics manufacturing demands ultrapure solvent packs, prompting suppliers to adopt clean-room assembly lines and ISO-class filters. Collectively, these sectors diversify risk for container makers while elevating customization demands. Suppliers with multi-material portfolios and in-house design labs are best positioned to capture growth across technologically intensive niches.

Geography Analysis

Asia-Pacific led 2025 sales with a 45.05% share, powered by China’s USD 2.3 trillion chemical sector and India’s pharmacy build-out that added 127 manufacturing plants in 2024. The region’s 6.55% CAGR projection reflects sustained industrialization, the Belt and Road trade lanes, and regional agencies' efforts to align packaging norms with UN models, thereby reducing certification duplication. Continuous capacity additions funnel large orders into the hazardous materials packaging market, while government incentives for smart-factory upgrades encourage adoption of IoT-enabled drums among Tier-1 shippers.

North America and Europe together captured roughly 34.72% of 2025 revenue. Mature regulatory frameworks under the Toxic Substances Control Act and REACH demand exhaustive documentation and periodic retesting, favoring suppliers with dedicated compliance teams. [2]European Chemicals Agency, “REACH Regulation Compliance Guide,” echa.europa.eu. Growth remains slower than in the Asia-Pacific region, yet per-unit values are higher because buyers prioritize advanced coatings, sensor integration, and closed-loop reuse programs that align with corporate net-zero targets. The hazmat packaging market share for returnable steel drums already tops 60% of total drum volume shipped in Germany, underscoring regional leadership in circular economy adoption.

Middle East and Africa and South America jointly command a modest but rising slice of the hazmat packaging market. Saudi Arabia and the United Arab Emirates expand petrochemical clusters to monetize hydrocarbon feedstocks, generating demand for large IBC fleets with corrosion-resistant linings. Infrastructure deficits and nascent rulebooks, however, curb short-term uptake of advanced smart-pack solutions. South America’s growth rests on Brazil’s chemicals complex and Argentina’s farm-chemicals exports, but currency volatility and political risk complicate capital investment timelines.

Competitive Landscape

The global supply chain displays a moderate concentration, with the five largest vendors accounting for roughly 42% of revenue, blending steel-drum heritage with emerging smart-container portfolios. Greif Inc. champions the ModCan line, which logs temperature, pressure, and shock data every 10 seconds across 15,000 units, thereby paring customer product-loss claims by 15%. Mauser Packaging Solutions scales its Infinity Series recycled-content drum using robotic welding lines, which increase throughput by 18%, highlighting cost leadership through automation.[3]Greif Inc., “SEC 10-K Filing 2024,” sec.gov Schütz Container Systems maintains regional strongholds in Europe and the Asia-Pacific after its 2025 investment in China, which increased IBC output by 40%.

Technology defines competitive edge. IoT-ready closures, blockchain-verified certification, and predictive-maintenance dashboards differentiate premium offering tiers. Patent filings for barrier-material nanocoatings increased to 247 in 2024, representing a 31% year-over-year rise, indicating sustained research and development (R&D) intensity. Vertical integration into steel mills or resin compounding plants buffers leading firms against raw material volatility, whereas smaller fabricators struggle to hedge their commodity exposure. Consolidation accelerated in 2024 when margin compression prompted family-owned specialists to seek strategic buyers; Greif’s USD 340 million takeover of Plastimex broadened its geographic reach and enhanced its pharmaceutical credentials.

Niche plays survive by focusing on region-specific regulations or customer-defined container geometries. Time Technoplast leverages intimate knowledge of India’s Central Pollution Control Board rules to secure multi-year pharmaceutical contracts, while Berlin Packaging’s life-science unit caters to micro-batch research needs. Overall, competition is migrating from pure container supply toward bundled compliance, lifecycle management, and data services, boosting switching costs and deepening customer lock-in.

Hazmat Packaging Industry Leaders

Greif Inc.

Mauser Packaging Solutions

Sonoco Products Company

Amcor plc

Schütz Container Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Greif Inc. completed its USD 340 million acquisition of European IBC maker Plastimex, adding 2.8 million units of annual capacity.

- September 2025: Mauser Packaging Solutions rolled out its ModDrum RFID-enabled steel drum, initially deployed by 12 major chemical producers.

- August 2025: Schütz Container Systems invested EUR 180 million (USD 195 million) in new Chinese IBC lines tailored for pharmaceutical applications.

- July 2025: Time Technoplast Ltd. won a USD 67 million packaging contract for India’s largest pharmaceutical export program.

Global Hazmat Packaging Market Report Scope

| Drums |

| Intermediate Bulk Containers (IBCs) |

| Pails |

| Bottles |

| Other Product Types |

| Plastic |

| Metal |

| Corrugated |

| Chemicals |

| Pharmaceuticals |

| Oil and Gas |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Drums | ||

| Intermediate Bulk Containers (IBCs) | |||

| Pails | |||

| Bottles | |||

| Other Product Types | |||

| By Material Type | Plastic | ||

| Metal | |||

| Corrugated | |||

| By End-user Industry | Chemicals | ||

| Pharmaceuticals | |||

| Oil and Gas | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the hazmat packaging market in 2026?

It is valued at USD 13.11 billion.

What is the projected CAGR for hazmat packaging through 2031?

The market is expected to grow at a 5.29% CAGR.

Which region leads to demand for hazmat containers?

The Asia-Pacific region accounts for approximately 45% of global sales.

Which product type is expanding fastest?

Intermediate bulk containers are forecast to grow at a 6.14% CAGR.

What factor most restrains short-term growth?

Volatile steel and polymer prices that squeeze supplier margins.

How are suppliers adding value beyond the container itself?

They are integrating IoT sensors for real-time tracking and compliance documentation.

Page last updated on: