Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 39.18 Billion |

| Market Size (2031) | USD 50.07 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Care Packaging Market Analysis by Mordor Intelligence

The home care packaging market size in 2026 is estimated at USD 39.18 billion, growing from 2025 value of USD 37.3 billion with 2031 projections showing USD 50.07 billion, growing at 5.03% CAGR over 2026-2031. This expansion reflects steady demand for hygiene products, widening e-commerce penetration, and policy support for sustainable solutions. Momentum is reinforced by the European Union’s Packaging and Packaging Waste Regulation, effective February 2025, which requires all packs to be recyclable by 2030.[1]Hazel O'Keeffe, “The New EU Packaging and Packaging Waste Regulation – Highlights and Challenges Ahead,” PackagingLaw.com, packaginglaw.com Material-price swings, especially in polyethylene and polypropylene, add cost volatility yet stimulate lightweighting and bio-based innovation. Asia-Pacific retains dominance thanks to urbanisation and rising disposable incomes, while the Middle East posts the quickest regional growth on the back of economic diversification. Corporate consolidation—illustrated by Amcor’s USD 8.4 billion takeover of Berry Global—signals a push for scale as producers tackle raw-material inflation and looming Extended Producer Responsibility (EPR) fees.

Key Report Takeaways

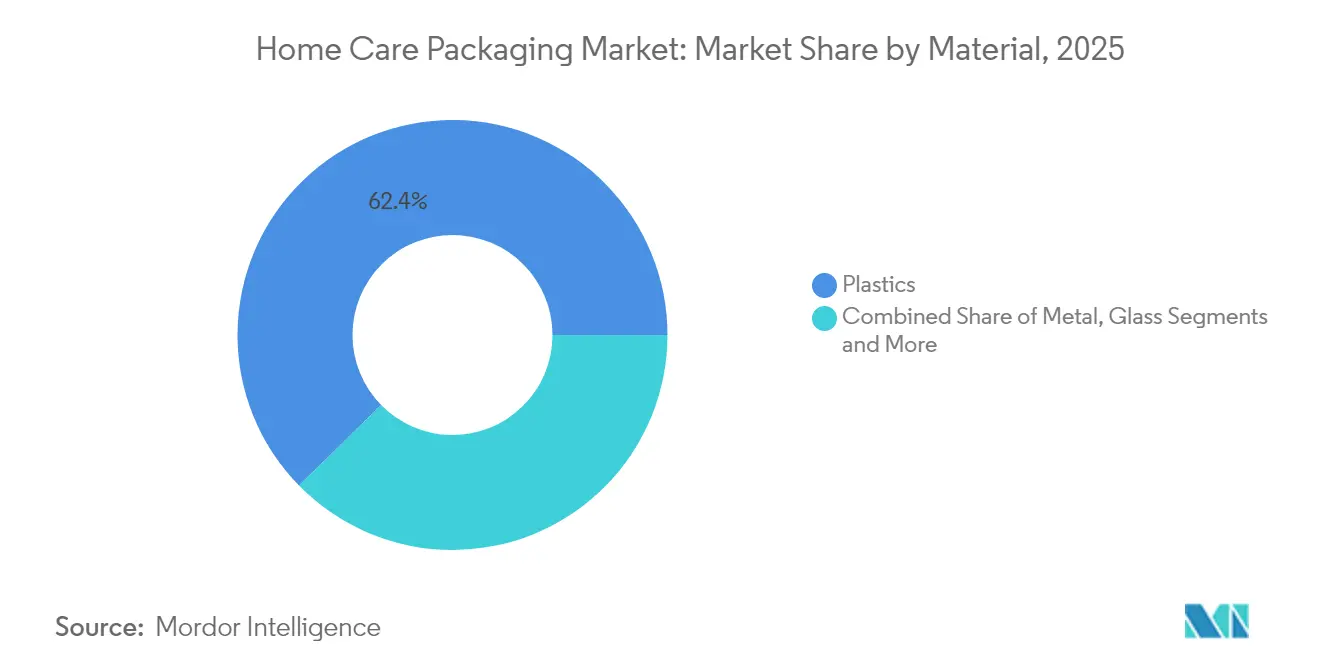

- By material, plastics led with 62.35% of home care packaging market share in 2025; bioplastics are projected to climb at a 11.55% CAGR to 2031.

- By packaging type, bottles and rigid containers held 46.40% revenue in 2025, while refill pouches and dispensing systems are set to expand at a 9.42% CAGR through 2031.

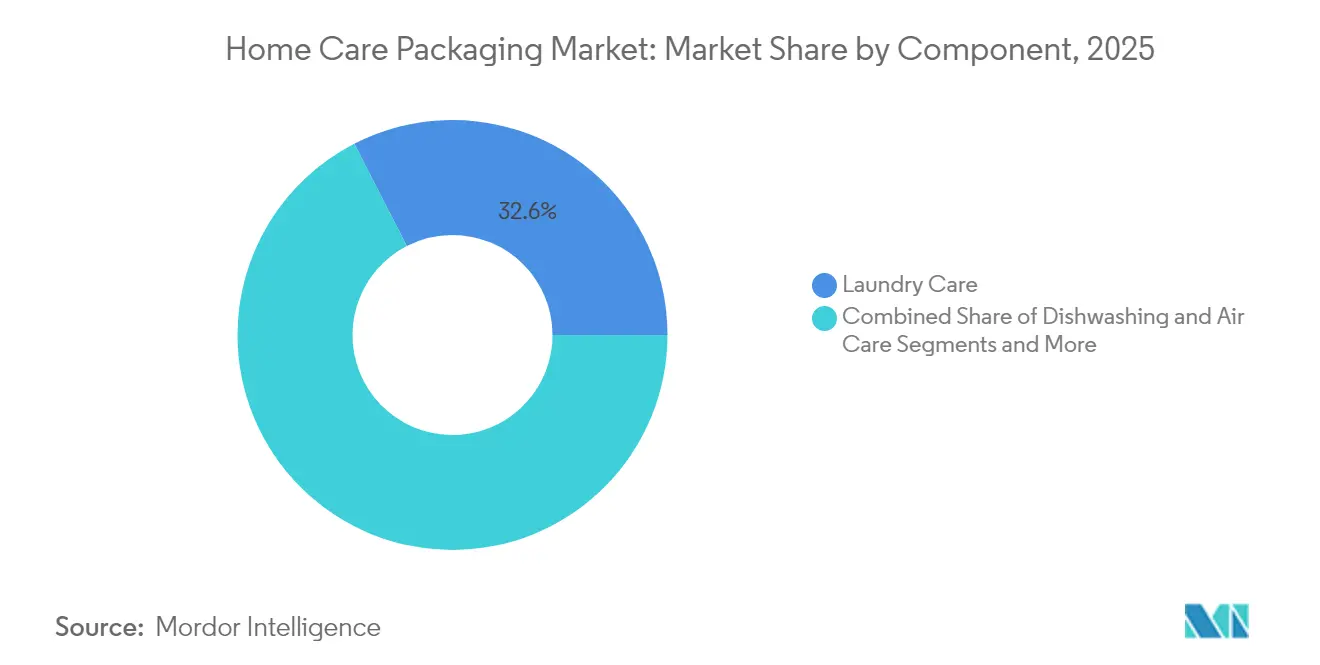

- By product category, laundry care captured 32.55% of the home care packaging market size in 2025; air care is the fastest-growing segment with an 7.88% CAGR between 2026-2031.

- By form factor, liquids dominated with 45.05% share of the home care packaging market size in 2025; capsules and tabs will rise at an 10.43% CAGR over the forecast horizon.

- Regionally, Asia-Pacific accounted for 38.45% of the home care packaging market share in 2025, while the Middle East is forecast to record a 7.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Home Care Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising premiumisation and brand-led SKU proliferation | +1.2% | Global (North America, APAC) | Medium term (2-4 years) |

| Circular-economy mandates for recyclable mono-material packs | +0.8% | Europe, North America expanding to APAC | Long term (≥ 4 years) |

| E-commerce boom accelerating demand for shatter-proof formats | +0.9% | Global (North America, APAC) | Short term (≤ 2 years) |

| Urban Asian households favouring single-dose convenience packs | +0.6% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| IoT-enabled smart dispensers and refill ecosystems | +0.4% | North America & EU, pilots in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Premiumisation and Brand-Led SKU Proliferation

Demand for upscale cleaning products drives packaging innovation beyond functional containment. Brands deploy advanced barriers, smart closures, and distinctive aesthetics to justify higher price points. Tide evo fibre tiles, launched in 2024, replace plastic with a dissolvable six-layer fibre structure and target premium shoppers.[2]Melissa Griffen, “Plastic Packaging Eliminated with New Tide Detergent Tiles,” Packaging World, packworld.com Middle East beauty spending, set to hit USD 47 billion by 2027, fuels similar expectations for home-care packs. Manufacturers of dispensing and specialty closures benefit, as evidenced by Silgan’s Q4 2024 sales jump to USD 639.4 million. Premiumisation simultaneously promotes smaller, design-rich formats and boosts margin resilience against resin cost swings. The trend cuts across developed and emerging markets, reshaping shelf competition within the home care packaging market.

Circular-Economy Mandates for Recyclable Mono-Material Packs

Regulators push producers toward designs that enable straightforward recycling. The EU’s PPWR stipulates 100% recyclability by 2030 and 30% recycled content for single-use plastic beverage bottles, compelling shifts to mono-material structures. Unilever’s paper-based detergent bottle underscores how corporate R&D aligns with looming quotas. Sixty-three countries now run formal EPR schemes, moving disposal costs from municipalities to producers and rewarding design-for-recycling approaches. Converters positioned in mono-material films gain pricing power, whereas multi-layer barrier suppliers must retool or face declining order books. Over the long term, compliance investments are expected to stabilise and support the broader home care packaging market trajectory.

E-commerce Boom Accelerating Demand for Shatter-Proof Formats

Online retail channels require packs capable of surviving extra handling, temperature swings, and longer distribution cycles. Returnable transport packaging in Asia-Pacific alone is projected to add USD 1.40 billion from 2023-2028 at 8.87% CAGR. Packaging lightweighting reduces shipping costs, yet corrugated prices rose USD 70 per ton in 2025, pushing converters to optimise designs. Damage-resistant flexible films, reinforced PET bottles, and dual-purpose secondary packs gain traction. Personal care packaging—closely related to the home care packaging market—reached USD 38.88 billion in 2025, with 27% of sales online. The requirement for omnichannel readiness accelerates demand for shatter-proof solutions within the home care packaging market.

Urban Asian Households Favouring Single-Dose Convenience Packs

Smaller living spaces, busy lifestyles, and heightened hygiene awareness propel single-dose formats in Asia. Unit-dose laundry capsules minimise wastage and ease storage, matching the needs of Japan’s 7.2 million caregiving households forecast for 2024. Water-soluble films, precise dispensing caps, and compact rigid containers underpin growth. Higher per-unit margins compensate for lower volumes, appealing to brands seeking value growth in the home care packaging market. As convenience culture spreads to Southeast Asia and the Middle East, unit-dose popularity is likely to broaden beyond laundry into dish- and surface-care segments. Machinery suppliers focused on small-format filling lines, thus encountering new revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petro-chemical resin price volatility | -0.7% | Global (North America, Europe) | Short term (≤ 2 years) |

| Extended-producer-responsibility fees in Europe | -0.3% | Europe expanding to North America | Medium term (2-4 years) |

| Scarcity of food-grade PCR resin for brand pledges | -0.4% | Global, developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petro-chemical Resin Price Volatility

Fluctuating polyethylene and polypropylene prices compress converter margins and complicate pricing strategy. PE registered several 5 ¢/lb hikes in 2024 - 2025 due to outages and feedstock spikes. PET saw a 1.1% jump after Tropical Storm Alberto disrupted supply. Smaller converters lack hedging tools, forcing cost-pass through or margin erosion in the home care packaging market. Volatility accelerates interest in lightweighting and alternative substrates. Converters able to shift to bio-based or recycled inputs faster can cushion against fossil-fuel price swings.

Extended-Producer-Responsibility Fees in Europe

EPR rules recast packaging economics by assigning waste-management costs to producers. France now mandates detailed consumer information, while Spain requires sorting symbols on packs. Fees range EUR 50-200 per ton, lifting total packaging outlay by 2-5%. Oregon and Colorado introduce similar frameworks by mid-2025, signalling global adoption. Brands must invest in compliance databases and redesign hard-to-recycle formats. Near-term cost pressure trims profitability but drives long-run alignment with circular-economy goals, supporting healthier growth prospects for the home care packaging industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bioplastics Gain Ground Amid Plastic Dominance

Plastics captured 62.35% of the home care packaging market share in 2025, underlining their entrenched role in cost-effective, barrier-rich applications. The segment continues to leverage mature supply chains and versatile processing techniques. However, bioplastics, propelled by a 11.55% CAGR, increasingly command design conversations as regulators and brands prioritise renewable feedstocks.

Paper and paperboard regain relevance through high recycling rates and lower carbon footprints, yet weight and moisture sensitivity keep them from mainstream liquid detergents. Metal retains niche importance in pressurised aerosols, and glass sees marginal use due to breakage risks in e-commerce. Bioplastics’ momentum spurs investment in PLA and PHA resins, with converters trialling mono-material films that still meet oxygen-barrier demands. As recycled-content mandates tighten, compatibilised blends of PCR and bio-based inputs can bolster supply stability and cost competitiveness for the home care packaging market.

By Packaging Type: Refill Systems Disrupt Rigid Containers

Bottles and rigid containers accounted for 46.40% of the home care packaging market size in 2025, reflecting legacy production lines and consumer familiarity with traditional formats. Lightweight HDPE and PET bottles remain prevalent thanks to excellent drop-impact resistance and brand-billboard capability. Yet refill pouches and dispensing systems, expanding at a 9.42% CAGR, are redefining value propositions through material savings and circular-loop convenience. Aptar’s recyclable airless bottle for dermocosmetics and B-CAP’s eco dosing cap demonstrate how innovation modernises even established formats.

Pouches deliver logistics efficiencies, shaving freight weight and cubic volume, crucial for e-commerce profitability. Reusable dispensers coupled with lightweight refill sachets reduce life-cycle emissions, resonating with EPR fee structures. Meanwhile, metal cans and stick packs maintain roles in specialty cleaners requiring specific delivery modes. Across all types, converters integrate QR codes for recycling instructions, aiming to ease consumer participation in circular schemes and boost compliance metrics that underpin the future growth of the home care packaging market.

By Product Category: Air Care Accelerates in a Laundry-Led Market

Laundry care secured 32.55% of the home care packaging market size in 2025, bolstered by frequent-use cycles and brand loyalty. Capsules, concentrated liquids, and refill packs permeate the segment, while P&G’s Tide evo tiles hint at a plastic-free future. Air care, tracking an 7.88% CAGR to 2031, capitalises on fragrance innovation and heightened indoor-air-quality focus. Scent booster revenues in Europe alone are forecast to reach EUR 3 billion by 2028.

Dishwashing, surface, and toilet cleaners post steady gains via compact concentrates and antimicrobial claims. Insecticides confront tighter regulations, spurring a shift to bio-actives and child-safe closures. Cross-category functionality emerges, with products combining cleaning, fragrance, and sanitising benefits, placing new performance demands on barrier films and vented caps. These dynamics keep pack developers busy sustaining differentiation within the competitive home care packaging market.

By Form Factor: Capsules Challenge Liquid Supremacy

Liquids represented 45.05% of the home care packaging market share in 2025, anchored by established filling infrastructure and consumer familiarity. Yet capsules and tabs, advancing at 10.43% CAGR, offer spill-free handling and exact dosing, limiting overuse while elevating unit economics. Water-soluble polyvinyl alcohol films eliminate secondary waste, aligning with sustainability pledges. Powder, gel, and foam formats hold niche relevance for heavy-duty cleaners and cling applications. Smart freshness sensors embedded in caps or sachets provide real-time quality assurance, enhancing value perception.

Continuous-thread from liquids to capsules accelerates demand for high-precision dosing equipment and moisture-barrier pouches. Form factor diversity also helps brands segment price tiers, keeping entry-level SKUs accessible while upselling premium convenience packs. This breadth supports revenue stability and encourages ongoing R&D investment inside the home care packaging market.

Geography Analysis

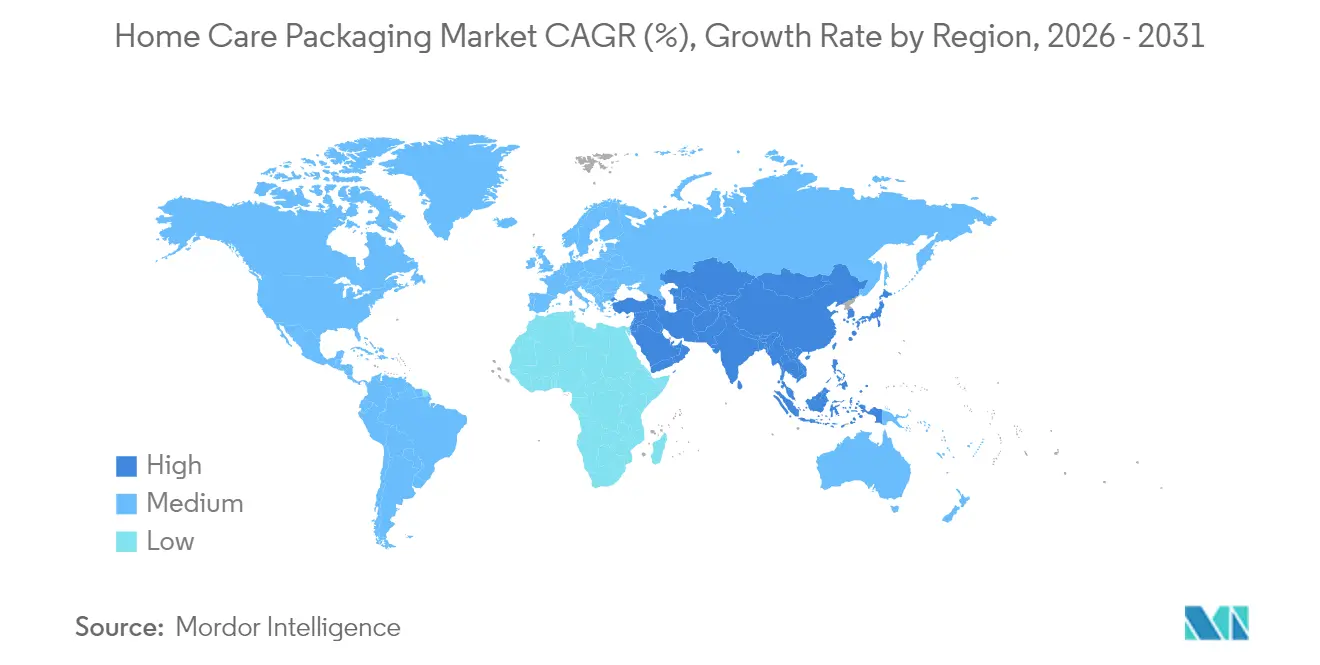

Asia-Pacific dominated with 38.45% home care packaging market share in 2025, reflecting rapid urbanisation, e-commerce growth, and middle-class expansion in China, India, and Southeast Asia. China’s forthcoming rules for recycled food-contact plastics will set new compliance benchmarks regionally. Japan’s ageing society drives demand for easy-open packs and single-dose detergents suited to smaller households. Investment in regional packaging machinery is forecast to surpass USD 18 billion by 2024, underpinning scale-up for converters.

The Middle East is the fastest-growing territory, with a 7.41% CAGR through 2031, supported by premiumisation in Gulf Cooperation Council markets. Regional beauty and personal-care outlays—from which spillover demand for upscale home-care packs emerges—will hit USD 47 billion by 2027. Hot climates necessitate barrier enhancements and UV-stable pigments, shaping supplier specifications. Saudi Arabia’s 34.6% share of GCC pharmaceutical sales highlights parallel opportunities for hygienic primary packs.

North America and Europe remain pivotal yet face tightening regulatory nets. The EU PPWR alone drives redesign budgets for global brand owners. Meanwhile, Oregon and Colorado introduce EPR schemes by July 2025, broadening producer-funded recycling models. Latin America shows emerging promise: higher raw-material costs push paper-pack prices up in 2025, signalling market maturation fastmarkets.com. Collectively, region-specific rules and consumer behaviours maintain nuanced growth paths across the home care packaging market.

Competitive Landscape

Industry consolidation is reshaping rivalry. Amcor’s integration of Berry Global forms a USD 24 billion revenue leader and captures anticipated USD 650 million in synergies. 2024 also saw Smurfit Kappa agree to buy WestRock for USD 12.7 billion and International Paper acquire DS Smith for USD 7.2 billion, illustrating a quest for scale and geographic breadth. These deals enable procurement leverage, wider technology portfolios, and stronger bargaining power against fluctuating resin costs—advantages critical in the home care packaging market.

Technology capability increasingly separates leaders from followers. Silgan’s purchase of Weener Packaging, boosting its dispensing-solution pipeline, led to a 22% year-on-year sales jump in Q4 2024. Patent filings for connected dispensers, automated inventory systems, and recyclable airless pumps underscore R&D intensity. Companies able to merge smart functionalities with recyclability gain first-mover edge.

Resource security and recycling capacity emerge as battlegrounds. Scarcity of food-grade PCR propels pre-buy contracts and joint ventures with recyclers. Firms investing in advanced sorting technologies or chemical recycling will lock in circular-economy readiness. White-space opportunities exist in bio-based barrier coatings, closed-loop refill infrastructures, and AI-driven predictive maintenance for filling lines, offering pathways to differentiation within the home care packaging industry.

Home Care Packaging Industry Leaders

Amcor PLC

Sonoco Products Company

Ball Corporation

RPC Group

Winpak Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Green Bay Packaging committed USD 1 billion to expand its Morrilton, Arkansas facilities, signalling long-term confidence in demand.

- May 2025: Amcor and Fedrigoni introduced fully recyclable wet-wipe packs aimed at circular-economy targets

- April 2025: Amcor finalised its USD 8.4 billion all-stock acquisition of Berry Global

- December 2024: Smurfit WestRock invested USD 40 million in plant expansion in Warwick, Quebec

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the homecare packaging market as the sale value of primary and secondary packs, bottles, pouches, boxes, cans, and related closures devoted to day-to-day household cleaning and hygiene consumables. We track plastic, paper, metal, glass, and emerging bioplastic formats that enter retail or direct-to-consumer channels worldwide.

Scope Exclusion: Industrial or institutional bulk packs exceeding ten-liter capacity are outside our frame.

Segmentation Overview

- By Material

- Plastics

- Paper and Paperboard

- Metal

- Glass

- Bioplastics

- By Packaging Type

- Bottles and Rigid Containers

- Pouches and Bags

- Cartons and Corrugated Boxes

- Metal Cans and Aerosols

- Refill Pouches and Dispensing Systems

- Stick Packs and Sachets

- By Product Category

- Laundry Care

- Dishwashing

- Surface and Toilet Cleaners

- Air Care

- Insecticides

- Polishes and Specialty Cleaners

- By Form Factor

- Liquids

- Powders

- Capsules/Tabs

- Gels

- Sprays/Foams

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview converters, resin suppliers, private-label buyers, and e-commerce fulfillment specialists across Asia-Pacific, Europe, North America, and the Middle East. These conversations validate ASP progression, refill adoption, recycled-content premiums, and region-specific pack-size preferences that secondary data alone cannot reveal.

Desk Research

We begin with structured mining of reputable, open data such as UN Comtrade shipment codes for HS 3402 and 3403, Eurostat packaging-waste filings, the US Census Quarterly Plastics Report, and Japan's METI resin demand bulletins. Company 10-Ks, retailer sell-out disclosures, and trade-body dashboards from the Flexible Packaging Association or Plastics Europe help us refine pack mix and average selling price (ASP) assumptions. Our analysts complement these with paid datasets, notably D&B Hoovers for converter revenue splits and Volza for shipment-level cross-checks, before constructing an initial demand baseline. This source list is illustrative, not exhaustive, and many other references feed our desk analysis.

Market-Sizing & Forecasting

A top-down model transforms retail sales of laundry, surface cleaners, and air-care products into pack demand using product-level fill-rate ratios, which are then reconciled with converter capacity disclosures and sampled ASP x volume roll-ups for critical formats. Key variables like household penetration of automatic washing machines, HDPE and PET resin price trends, e-commerce parcel volumes, refill pouch take-up, and regional recycling mandates feed multivariate regression forecasts, while an ARIMA overlay captures seasonality. Gaps in bottom-up estimates are bridged by applying weighted margin factors derived from expert interviews.

Data Validation & Update Cycle

Mordor analysts triangulate outputs against import bills, converter earnings calls, and resin off-take stats, flagging anomalies for senior review. Models refresh annually, with mid-cycle tweaks if raw-material shocks or regulation shifts exceed predefined thresholds.

Why Mordor's Home Care Packaging Baseline Commands Reliability

Published values often diverge because firms pick different product baskets, pricing bases, and refresh cadences. We acknowledge these realities upfront.

Key gap drivers include: a) some publishers fold personal-care packs into totals; b) others apply uniform ASP growth, whereas our model layers material-specific pricing; c) refresh lags longer than twelve months elsewhere, while Mordor Intelligence updates yearly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 37.30 B (2025) | Mordor Intelligence | - |

| USD 35.82 B (2025) | Global Consultancy A | Broader material basket, limited primary validation |

| USD 22.34 B (2024) | Regional Consultancy B | Excludes refill pouches and online-only SKUs |

| USD 15.00 B (2023) | Trade Journal C | Uses producer shipment volume without retail ASP cross-check |

Taken together, the comparison shows that our disciplined scope selection, mixed-method pricing curves, and annual refresh give decision-makers a balanced, transparent starting point that can be traced to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the home care packaging market?

The market is valued at USD 39.18 billion in 2026 and is projected to reach USD 50.07 billion by 2031 at a 5.03% CAGR.

Which region leads the home care packaging market?

Asia-Pacific accounts for 38.45% of global revenue owing to urbanisation, rising incomes, and rapid e-commerce growth.

Why are refill pouches growing faster than rigid bottles?

Refill pouches cut material use, align with circular-economy regulations, and support IoT-enabled dispenser systems, propelling a 9.42% CAGR over 2026-2031.

How do EPR fees affect packaging producers?

Extended Producer Responsibility shifts waste-management costs to brands, raising packaging spend by 2-5% yet incentivising recyclable mono-material designs.

What challenges surround recycled content in home care packs?

Limited availability of food-grade PCR, lengthy regulatory approvals, and higher costs—20-40% above virgin resin—hamper fulfilment of public sustainability pledges.

Page last updated on: