Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

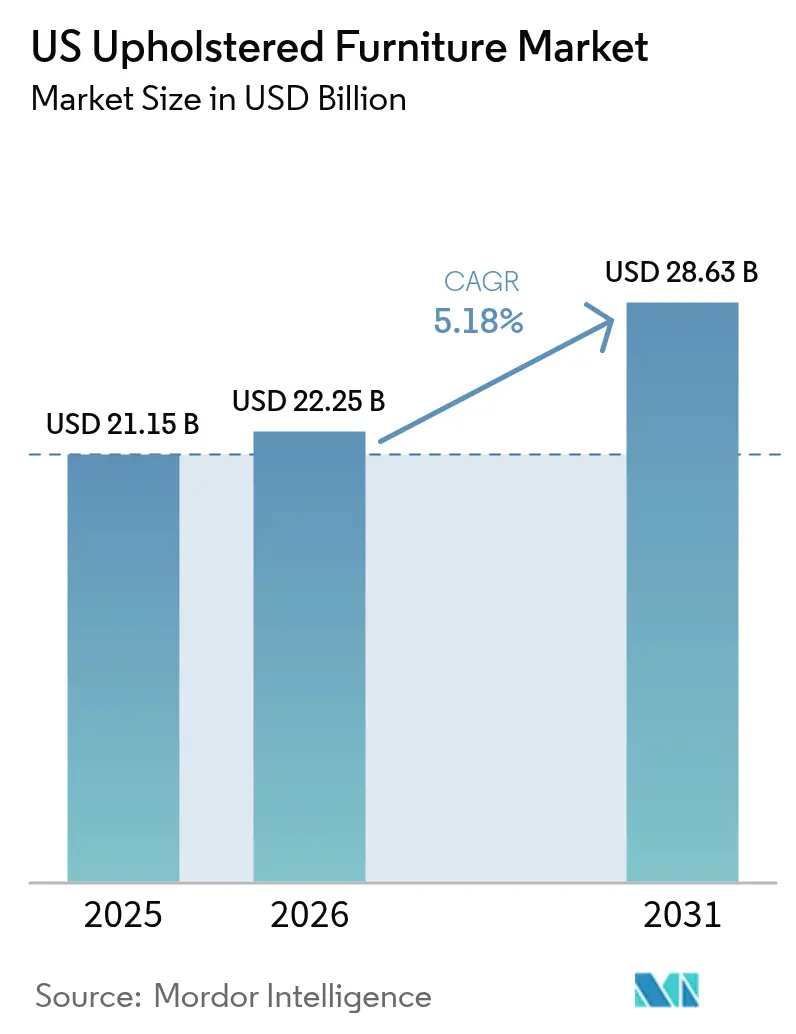

| Base Year Market Size (2025) | USD 21.15 Billion |

| Market Size (2026) | USD 22.25 Billion |

| Market Size (2031) | USD 28.63 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

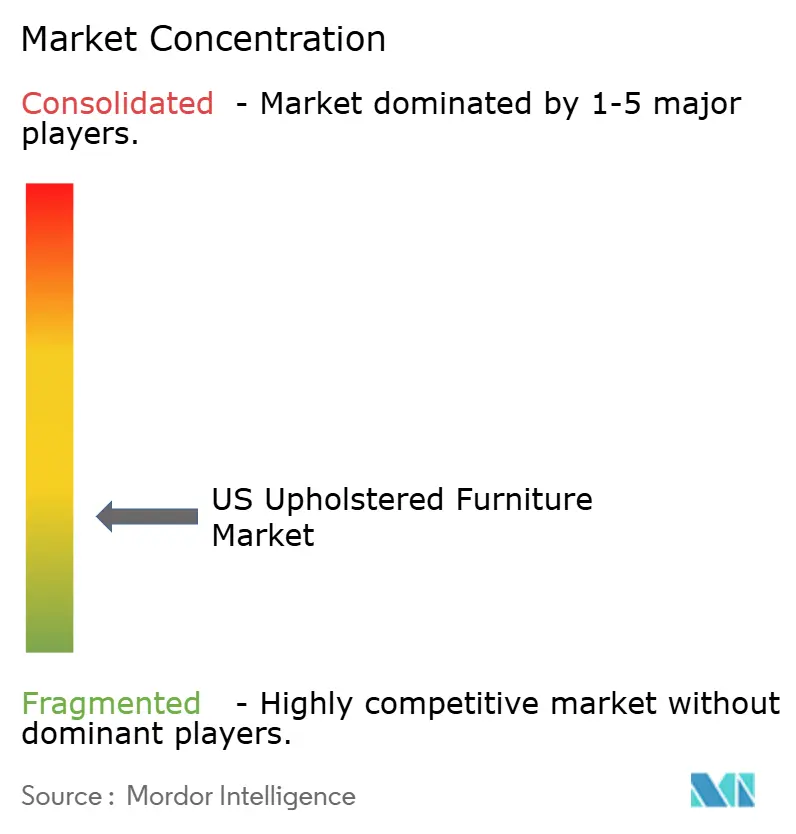

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Upholstered Furniture Market Analysis by Mordor Intelligence

United States upholstered furniture market size in 2026 is estimated at USD 22.25 billion, growing from 2025 value of USD 21.15 billion with 2031 projections showing USD 28.63 billion, growing at 5.18% CAGR over 2026-2031. The rebound reflects stable consumer spending, reshoring that narrows the landed-cost gap on imports, and e-commerce penetration that lowers distribution friction. Tariffs introduced in early 2025—10% on all imported furniture and 145% on Chinese shipments—have reduced price advantages enjoyed by Asian suppliers, encouraging domestic production while preserving choice for value-oriented buyers. Demand also benefits from Sun Belt migration, quick-ship programs that appeal to millennials, and higher outlays on premium pieces that align with sustainability and wellness values. Competitive intensity remains low, leaving room for niche entrants and digital natives to gain visibility through direct-to-consumer models.

Key Report Takeaways

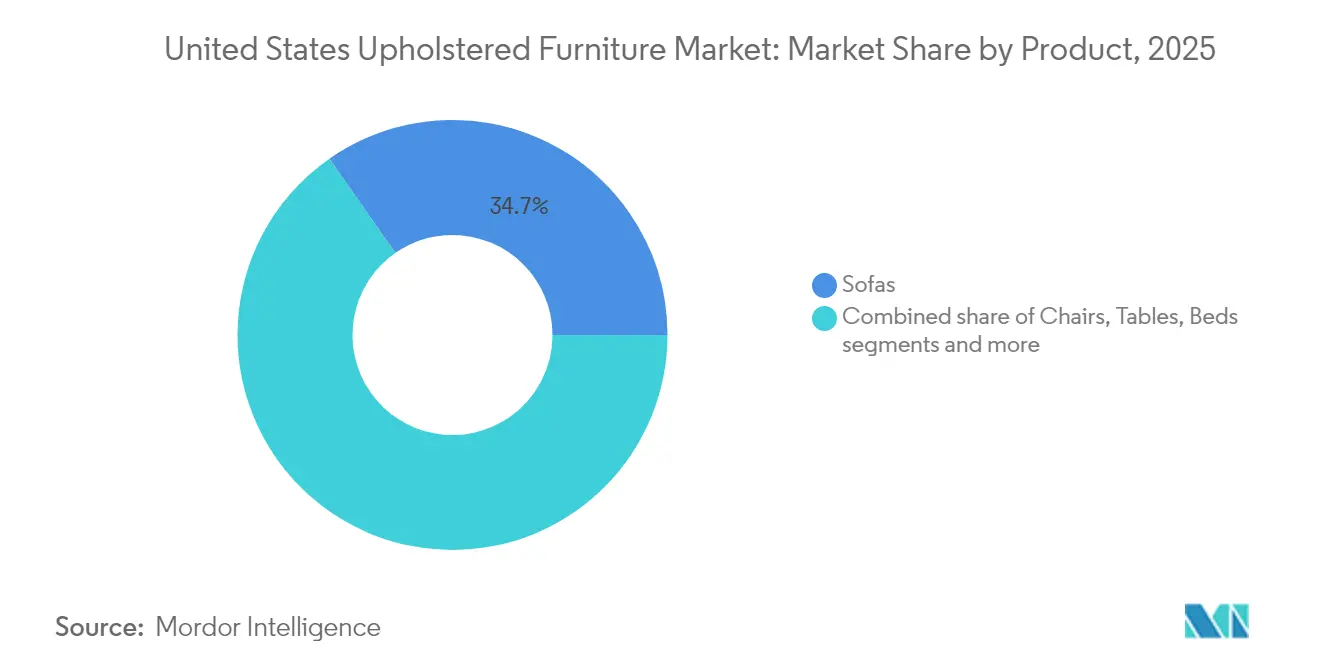

- By product, sofas led with 34.70% revenue share in 2025, while chairs are projected to grow the fastest at a 6.23% CAGR through 2031.

- By material, fabric commanded a 54.60% share in 2025; leather is set to expand at a 5.78% CAGR to 2031.

- By price range, the mid-range bracket accounted for 49.30% of the US upholstered furniture market size in 2025; the premium bracket is projected to advance at a 5.55% CAGR.

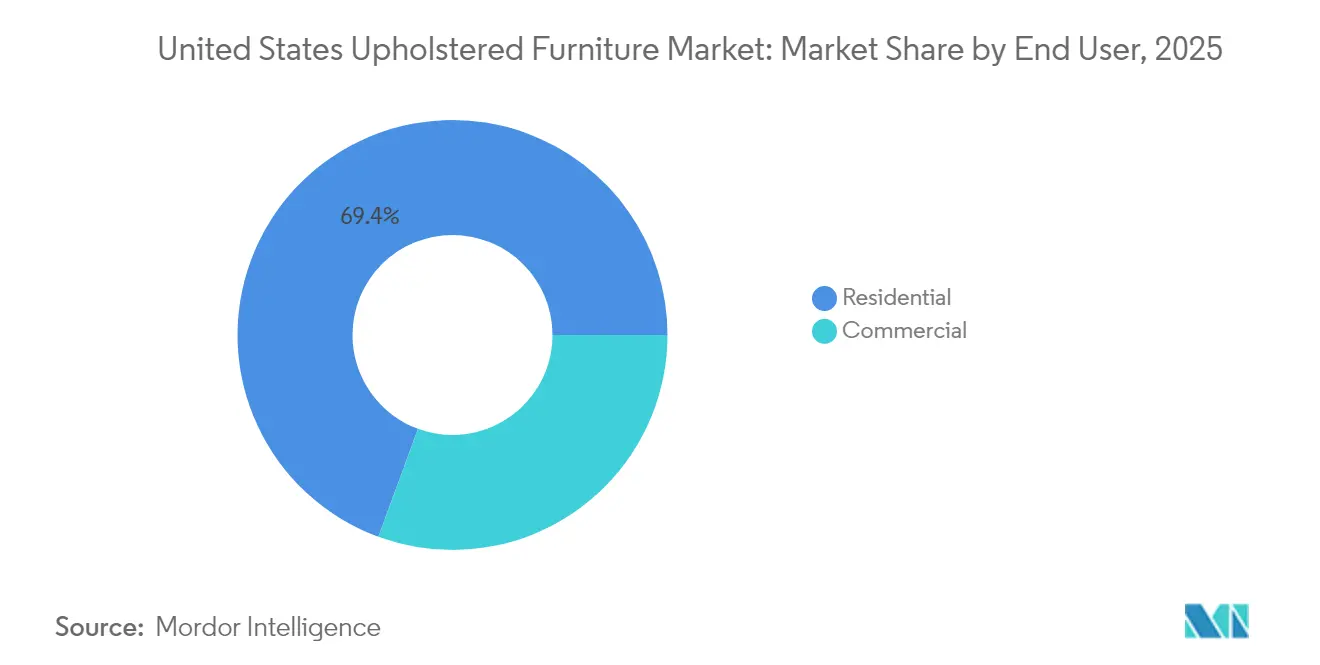

- By end user, residential captured 69.40% of the US upholstered furniture market share in 2025; commercial applications are expected to grow at a 6.05% CAGR.

- By distribution channel, specialty furniture stores held a 39.20% share in 2025, whereas online sales are forecast to rise at a 6.38% CAGR.

- By region, the South contributed 39.60% of sales in 2025, while the West is on track for the highest regional CAGR of 5.95%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Upholstered Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-led direct-to-consumer penetration | +1.2% | National, early gains in urban centers | Medium term (2-4 years) |

| Mass-customization & quick-ship programs | +0.8% | National, millennial hubs | Medium term (2-4 years) |

| Housing starts & renovation boom in Sun Belt | +1.5% | South and West | Long term (≥ 4 years) |

| ‘Made-in-USA’ reshoring initiatives | +1.0% | National, manufacturing clusters | Long term (≥ 4 years) |

| Rising spend on luxury furnishing | +0.7% | Northeast and West Coast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce-led Direct-to-Consumer Penetration Accelerating Upholstery Sales

Online home-furnishing revenue is reshaping the US upholstered furniture market as millennials gravitate toward digital channels. Younger shoppers favor sectionals, driving online sofa searches, while 3D visualization and AI recommendations address the tactile gap that once hindered large-ticket e-commerce. Fragmented brand concentration encourages digitally native labels to build direct relationships that bypass costly showrooms. Although personalization options remain available, many shoppers now prioritize faster delivery over bespoke features, prompting suppliers to refine configurable SKUs rather than fully customized builds.

Mass-Customization & Quick-Ship Programs Attracting Millennial Buyers

Domestic factories exploit proximity to offer two-week ship windows, an advantage amplified by tariff-related import delays. While customization tools allow fabric and finish choices, uptake has eased as consumers trade breadth for delivery speed. Vertical integration and lean production help manufacturers keep promise dates without heavy inventory. Sustainability expectations also shape preferences, with Generation Z rewarding brands that disclose material provenance and carbon use. Suppliers that combine modest customization with clear eco-attributes are positioned to expand share.

‘Made-in-USA’ Reshoring Initiatives Shortening Lead Times & Boosting Domestic Orders

A decline in imports from Asian low-cost nations signaled momentum toward local sourcing. Tariffs imposed in 2025 further reduced the cost delta, and marquee investments such as a USD 80 million Ashley Furniture expansion in Mississippi underline confidence in the US upholstered furniture market. Challenges persist: upholstery shops still face skilled-labor gaps that may slow capacity ramp-ups, and infrastructure upgrades will be essential if reshoring continues.

Increasing Spending on Luxury Furnishing Is Driving the Market

Premium pieces are forecast to outpace the broader US upholstered furniture market, advancing at a 5.8% CAGR. Consumers, having revalued home comfort during the pandemic, now seek heirloom durability and articulation of personal style. Design forecasts for 2025–2026 highlight craft aesthetics, quiet minimalism, and blended digital-physical spaces, motivating buyers to accept higher tickets for ethically sourced hides and hand-finished frames. Brands with vertical control over fabric mills, leather tanneries, or cushioning inputs protect margins while offering transparency that luxury shoppers reward.

Restraints Impact Analysis*

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled upholsterer shortage | -1.8% | National, acute in legacy hubs | Long term (≥ 4 years) |

| Volatile raw-material prices are compressing margins | -1.2% | National | Short term (≤ 2 years) |

| Low-cost imports from Vietnam & China | -0.9% | National, price-sensitive niches | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw Material Prices Compressing Margins

Commodity swings in cotton, steel, and polyurethane foam continue to unsettle input budgets. While lumber prices stabilized, steel and cotton remain above pre-2020 averages, and the CPI for household furnishings rose 0.4% in February 2025[1]U.S. Bureau of Labor Statistics, “Consumer Price Index: Household Furnishings and Operations,” bls.gov. Retailers mitigate exposure through surcharge line items or flash promotions. Some global brands have enacted three price cuts within 12 months to hold traffic, accepting thinner margins in the near term. Manufacturers respond with multi-sourcing strategies and R&D on bio-based foams that lower dependence on petrochemicals.

Low-Cost Imports from Vietnam & China Eroding Domestic Share

Vietnam’s share of US furniture imports climbed as suppliers shifted capacity from China. Even with new tariffs, discount channels still favor import programs to defend entry-level price points. Domestic plants must improve automation and scale to match cost expectations, especially in the economic tier. Continued vigilance on anti-dumping actions and evolving trade policy will shape the final balance between imported and local stock.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Sofas Lead Market Share, While Chairs Drive Growth Acceleration

Sofas generated 34.70% of 2025 sales, making them the anchor category in the US upholstered furniture market. Fabric options dominate sofa purchases; shoppers choose comfort and variety. Chairs, including recliners and accent seats, are forecast to expand at a 6.23% CAGR as hybrid work normalizes secondary seating in home offices. The US upholstered furniture market size for chairs is projected to widen in absolute dollar terms as consumers buy task-oriented pieces alongside living-room ensembles.

Millennial demand for sectionals now drives sofa category traffic and supports modular designs that scale from apartments to single-family homes. At the same time, niche formats such as poufs and ottomans grow as space-saving add-ons. Commercial applications also contribute to chair momentum, with hospitality brands refreshing lounge areas to encourage longer stays. The diversified product mix dilutes reliance on a single category and allows manufacturers to balance high-ticket sofas with volume-driven accent lines.

By Material: Fabric Dominance Faces Leather’s Premium Growth Trajectory

Fabric maintained a 54.60% share in 2025 on the strength of stain-resistant finishes and upgradeable color palettes. Synthetic linen and recycled polyester blends help suppliers address sustainability claims without premium pricing. Leather is projected to outpace overall market growth with a 5.78% CAGR, benefiting from consumer perception of longevity and luxury aesthetics. Full-grain hides combined with high-resilience foam satisfy premium buyers who equate heft with durability.

The US upholstered furniture market share of fabric remains steady, yet leather’s upswing lifts average selling prices and margin dollars. Eco-leather and plant-based alternatives serve shoppers who want leather visuals without animal content, reflecting broader green priorities. Suppliers that maintain dual material strategies can hedge commodity risk and serve both cost-sensitive and premium segments.

By Price Range: Mid-Range Stability Contrasts with Premium Acceleration

Mid-range pieces captured 49.30% of the US upholstered furniture market size in 2025, underscoring the pull of balanced value and quality. Efficient domestic production and containerized imports meet this price ceiling, keeping the average spent window attractive to millennials. Promotions around holiday events stabilize throughput and clear seasonal inventory.

Premium items are tracking a 5.55% CAGR through 2031 as buyers reward craftsmanship, heritage branding, and sustainable sourcing. Vertical integration—owning tanneries, fabric mills, or foam plants—helps luxury labels control costs despite volatile inputs. Economy products remain essential for first-time buyers yet face the greatest tariff exposure, pressing suppliers to engineer lower-material-content SKUs while preserving perceived quality.

By End User: Residential Dominance Meets Commercial Growth Potential

Residential purchases yielded 69.40% of 2025 revenue and continue to anchor the US upholstered furniture market. Existing-home transactions historically trigger new-furnishing demand; a forecast 3.7% rise in resales through 2025 supports steady sofa and sectional throughput. Renovation activity, buoyed by remote work and multigenerational living, extends the replacement cycle and encourages upgrades to higher quality.

Commercial demand is projected to climb to 6.05% CAGR, fueled by hospitality refurbishments and office reconfigurations that emphasize collaborative zones. Code compliance, notably CAL 133 flammability, drives material choices and costs in public-use pieces. Restaurant lounge concepts and co-working venues also favor plush seating, broadening the specification base beyond traditional corporate settings.

By Distribution Channel: Specialty Stores Face Digital Disruption

Specialty furniture retailers held a 39.20% share in 2025 through curated showrooms, white-glove delivery, and financing offers that simplify big-ticket decisions. The model remains central for high-involvement purchases, yet web-influenced research means many shoppers visit showrooms only after forming a preference set online. Omnichannel investments now include augmented-reality apps that overlay fabrics on in-home photos, merging physical validation with digital convenience. Retail sales at furniture and home-furnishings stores reached USD 11.0 billion in March 2024, up from USD 10.3 billion in February, signalling a rebound in brick-and-mortar traffic even as e-commerce penetration rises .

Online sales are forecast to grow at 6.38% CAGR and already generate double-digit gains for hybrid brands. Improved last-mile logistics and free returns ease risk perceptions. The US upholstered furniture market benefits from this dual-channel model: brands capture margin uplift online and use stores for service-heavy interactions. Big-box home centers and department stores maintain relevance in suburban corridors but compete on traffic rather than depth, pressuring assortments to remain price competitive.

Geography Analysis

The South accounted for 39.60% of 2025 revenue, underpinned by 4.3% GDP growth from 2020 to 2024 and sustained in-migration that lifted residential permit volume above half the national total. Lower median home prices leave households with greater discretionary funds, translating into higher ticket averages for living-room seating. Southern states accounted for 52% of all new residential building permits issued nationwide in 2024, underscoring why the South remains the largest regional demand engine for living-room seating and other upholstered pieces

The West is projected to post the fastest regional CAGR at 5.95% through 2031, owing to tech-center payroll expansion and consumer affinity for premium, eco-labeled furnishings. High housing costs compress entry-level spending but elevate demand for sectional versatility and multi-functional pieces among affluent cohorts. The region’s early adoption of e-commerce tools further accelerates online furniture sales, positioning digital natives to test innovations before scaling nationwide.

The Midwest and Northeast remain mature yet stable contributors. Heritage factories, skilled craft clusters, and established corporate campuses sustain baseline demand for both residential and commercial seating. Population aging tempers volume growth, but higher disposable incomes in the Northeast support above-average unit prices. Institutional orders from education and health-care complexes offset softer household formation, ensuring a balanced but slower growth curve across these regions.

Competitive Landscape

The US upholstered furniture market remains fragmented. This dispersion indicates limited switching costs and fosters opportunity for entrants capable of brand storytelling and rapid fulfillment. Direct-to-consumer startups leverage social media engagement and transparent pricing to gain traction without the capital burden of large showrooms.

Established brands pursue vertical integration to defend margins and consistency. American Leather maintains internal control over frame cutting and foam molding to guarantee quality across premium SKUs. Expansion strategies center on store rollouts in growth corridors and R&D hubs that prototype modular frames and recycled-fabric lines. La-Z-Boy recently added ten stores in Arizona and Massachusetts and opened an innovation center to accelerate product launches.

Technology adoption serves as the new battleground. AI-driven demand forecasting, 3D commerce platforms, and chat-based room planners enhance customer engagement while trimming inventory risk. Brands integrating these tools report higher conversion and fewer returns. Market fragmentation implies that digital competence, sustainability claims, and agile supply chains are the decisive levers for share gains over the next five years.

US Upholstered Furniture Industry Leaders

Ashley Furniture Industries

La-Z-Boy Incorporated

Bassett Furniture Industries

Flexsteel Industries

Hooker Furnishings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Prepac Manufacturing closed its Delta, British Columbia plant, relocating production to North Carolina to mitigate tariff risk and shorten delivery windows

- March 2025: Hooker Furnishings reported Q4 net sales of USD 104.5 million, up 8%, and outlined a warehouse exit that should save USD 4–5.7 million annually starting 2027

- March 2025: Klaussner confirmed plans for a new North Carolina factory and showroom to scale domestic capacity

- January 2025: Hooker Furnishings launched a designer-focused program and debuted its Collected Living by HF concept at Las Vegas Market

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States upholstered furniture market as all new, factory-finished seating and bedding pieces whose outer surfaces contain integrated padding covered by fabric, leather, microfiber, or other upholstery materials. The scope spans sofas, sectionals, chairs, stools, ottomans, headboards, and upholstered bedframes sold through retail and contract channels, valued at first domestic sale or import entry.

Scope exclusion: Patio-only outdoor seating, standalone mattresses, and refurbishment services are not considered.

Segmentation Overview

- By Product

- Chairs

- Sofas

- Tables

- Beds

- Stools

- Other Products (poufs, ottoman, etc.)

- By Material

- Fabric

- Leather

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Furniture Stores (including exclusive brand outlets)

- Online

- Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, warehouse clubs, departmental stores, etc.)

- B2B/Projects (directly to businesses)

- B2C/Retail

- By Geography

- South

- Midwest

- West

- Northeast

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed upholstery manufacturers, component suppliers, specialty retailers, and interior designers across the South, Midwest, West, and Northeast. These conversations clarified average selling prices, e-commerce share, and planned capacity additions, filling key gaps flagged during secondary review.

Desk Research

We began by mapping supply and demand through tier-one public datasets such as U.S. Census Monthly Retail Trade, Bureau of Economic Analysis personal consumption tables, U.S. International Trade Commission HS-9401 import statistics, and the American Housing Survey, which anchors penetration rates. White papers from the American Home Furnishings Alliance, alongside Bureau of Labor Statistics producer-price indices, sharpened cost trends, while paid feeds from D&B Hoovers and Dow Jones Factiva provided company revenue splits and news flows. The sources noted are illustrative; many other open and proprietary references informed the desk work.

Market-Sizing & Forecasting

We employ a top-down and bottom-up hybrid. The model starts with domestic production plus net imports, then adjusts for inventory shifts and channel mark-ups. Selective bottom-up roll-ups of major players and sampled ASP × volume checks validate totals. Core drivers include new housing starts, disposable personal income, furniture-store sales index, average upholstery import price, and renovation spend per household. A multivariate regression blended with scenario analysis generates the 2025-2030 outlook and flags sensitivity to housing and income swings.

Data Validation & Update Cycle

Each run passes automated variance checks, peer review, and senior sign-off before release. Reports refresh annually, with interim updates triggered by material events; a final review immediately precedes delivery to ensure clients receive the latest view.

Why Mordor's US Upholstered Furniture Baseline Earns Decision-Maker Trust

Published estimates diverge because firms stretch product baskets, apply broad regional averages, or refresh data less often. Mordor's disciplined scope, annual update cadence, and dual-path modeling keep the baseline tightly aligned with category realities.

Key gap drivers include inclusion of mattresses or outdoor sets, reallocating North America figures to the U.S. and using total furniture proxies. For instance, our 2025 demand stands at USD 21.15 billion. Other 2024 studies quote USD 31.4 billion and USD 45.2 billion, while a broad furniture overview lists USD 180.55 billion for 2025.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.15 B (2025) | Mordor Intelligence | |

| USD 45.2 B (2024) | Global Consultancy A | Scope folds in mattresses and outdoor seating, inflating value |

| USD 31.4 B (2024) | Regional Consultancy B | Uses North America revenue then allocates share to the U.S. |

| USD 180.55 B (2025) | Trade Journal C | Reports total furniture sales without isolating upholstery |

The comparison shows that Mordor's clear scope choices, variable selection, and yearly validation deliver a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current size of the US upholstered furniture market?

The US upholstered furniture market was valued at USD 22.25 billion in 2026.

How fast is the market expected to grow?

The market is forecast to expand at a 5.18% CAGR, reaching USD 28.63 billion by 2031.

Which product category holds the largest share?

Sofas lead with 34.70% of 2025 sales, while chairs are the fastest-growing segment at 6.23% CAGR.

Why is reshoring important for US producers?

Tariffs and higher freight costs have narrowed the import cost advantage, making domestic manufacturing more competitive and reducing delivery times.

Which sales channel is expanding the quickest?

Online channels are set to grow at a 6.38% CAGR, supported by 3D commerce and direct-to-consumer strategies.

Page last updated on: