Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

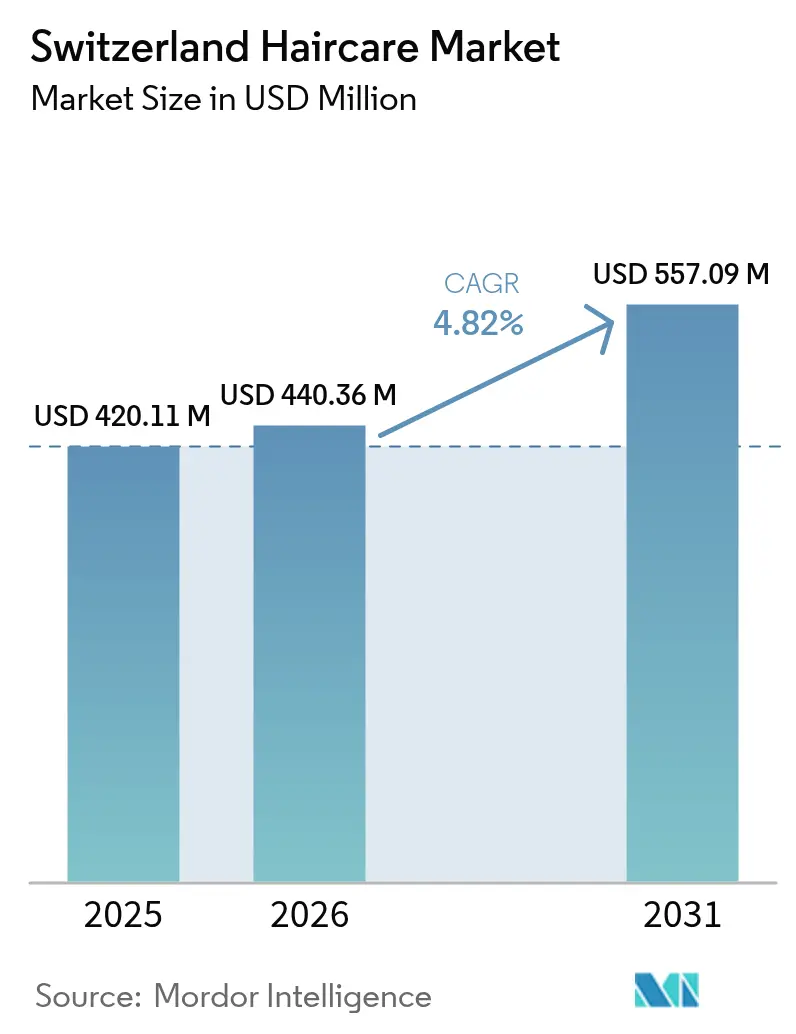

| Base Year Market Size (2025) | USD 420.11 Million |

| Market Size (2026) | USD 440.36 Million |

| Market Size (2031) | USD 557.09 Million |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

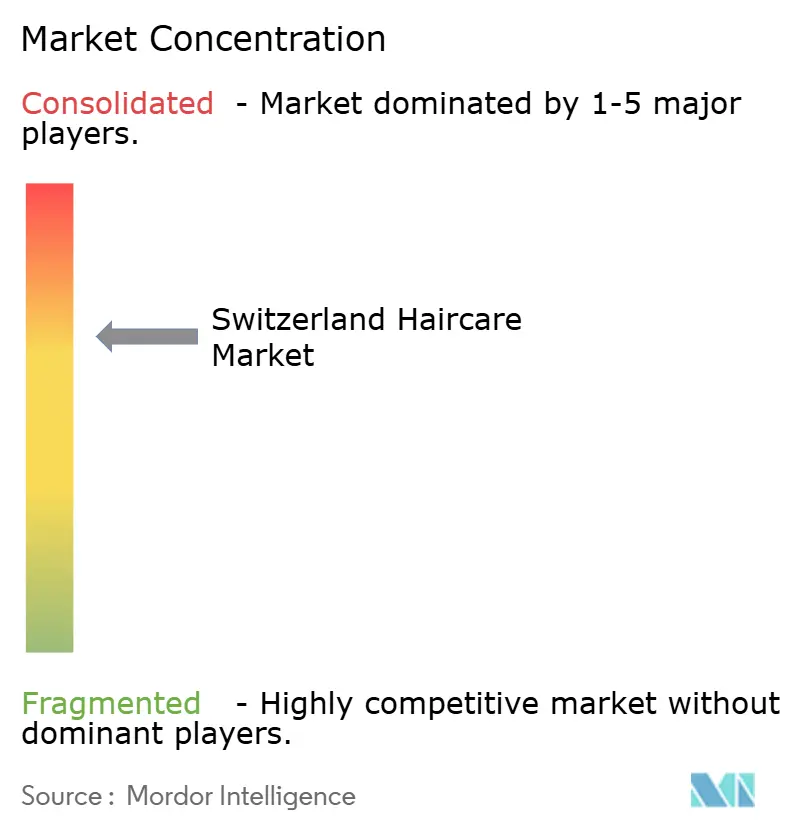

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Switzerland Haircare Market Analysis by Mordor Intelligence

The Swiss Hair Care Market size was valued at USD 420.11 billion in 2025 and estimated to grow from USD 440.36 billion in 2026 to reach USD 557.09 billion by 2031, at a CAGR of 4.82% during the forecast period (2026-2031). The market expansion is attributed to heightened consumer consciousness regarding hair health, increased demand for premium and customized products, and a substantial shift toward natural and organic formulations. Switzerland's concentrated urban demographic, characterized by substantial purchasing power, generates significant demand for specialized hair care products and professional salon services. The proliferation of e-commerce platforms has enhanced product accessibility and distribution efficiency, resulting in accelerated online sales growth. Market dynamics are further influenced by sustainability initiatives and technological advancements, encompassing AI-driven personalization solutions and environmentally conscious packaging innovations. These factors, in conjunction with Switzerland's robust economic framework, indicate sustained market development in the forthcoming years.

Key Report Takeaways

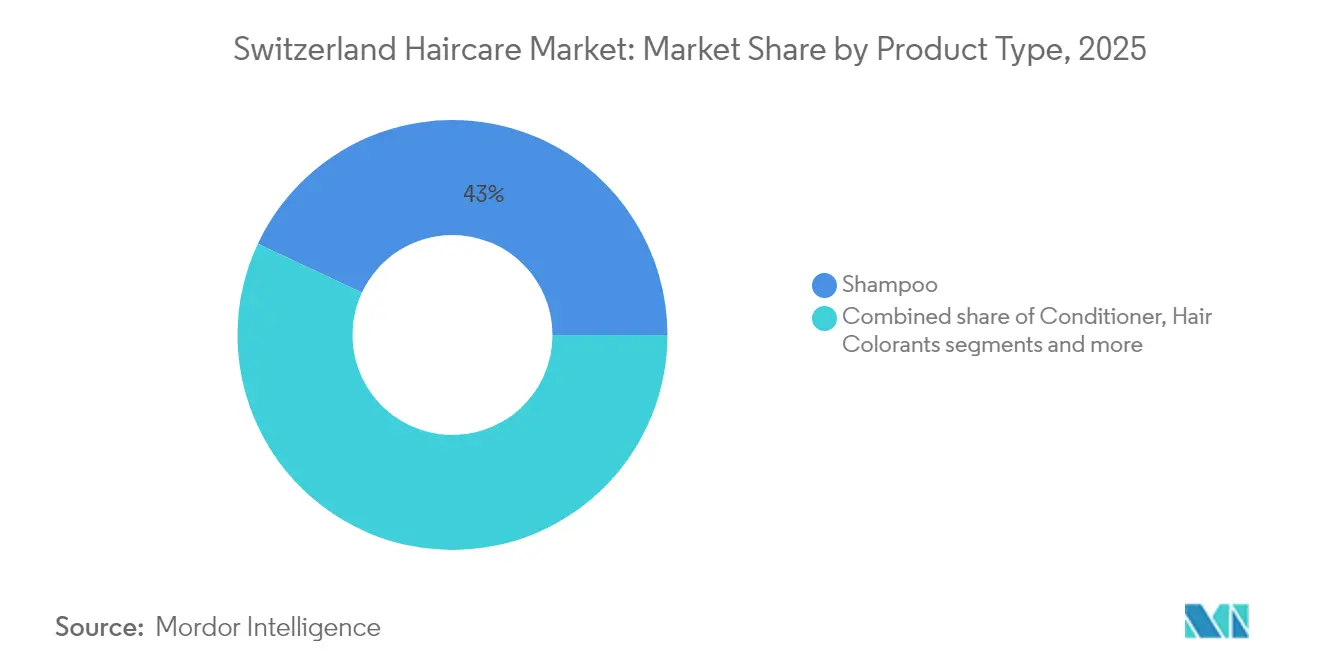

- By product type, shampoo led with 43.02% of the Swiss hair care market share in 2025, whereas hair styling products are advancing at a 5.1% CAGR through 2031.

- By category, mass products accounted for 69.55% of the Swiss hair care market share in 2025, while premium products are forecast to climb at a 6.18% CAGR to 2031.

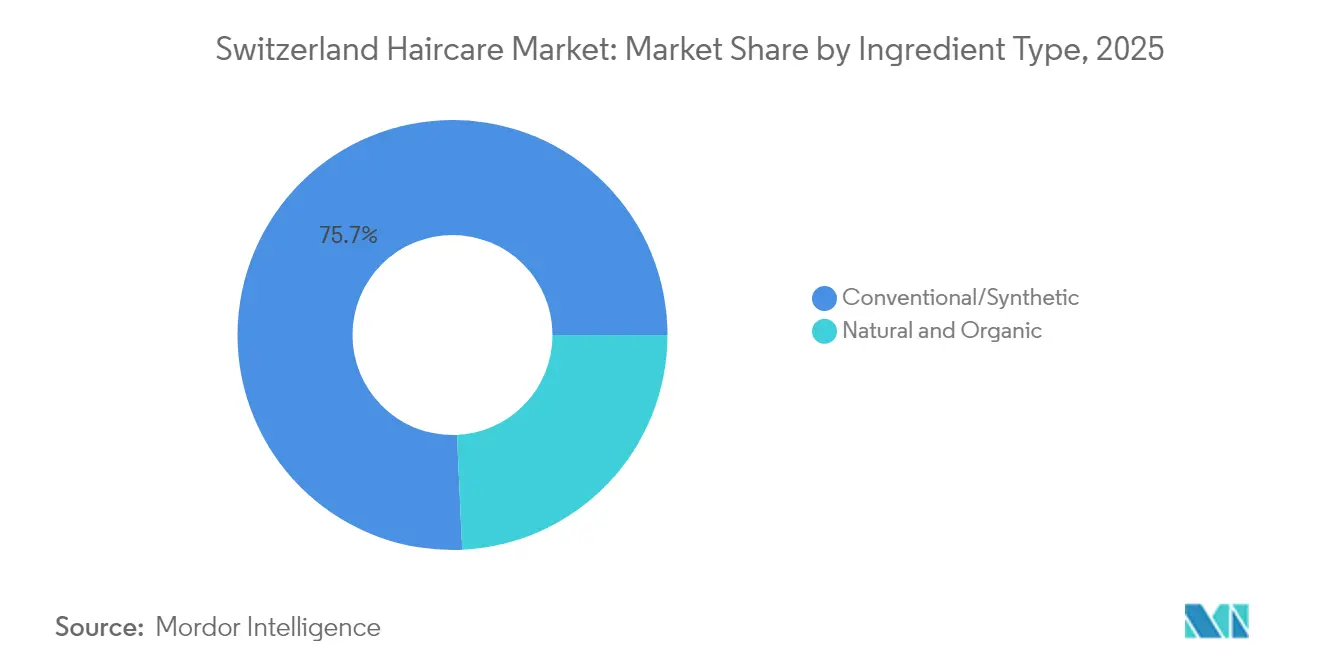

- By ingredient type, conventional formulations captured 75.72% of the Swiss hair care market size in 2025, yet natural and organic alternatives are poised to expand at a 6.44% CAGR between 2026 and 2031.

- By distribution channel, supermarkets and hypermarkets contributed 43.86% to the Swiss hair care market size in 2025, but online retail stores are projected to post the fastest 7.21% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Haircare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for personalized hair care solutions | +0.8% | National, with early gains in Zurich, Geneva, Basel | Medium term (2-4 years) |

| Sustainable packaging appeals to eco-conscious consumers | +0.6% | National, stronger in German-speaking regions | Long term (≥ 4 years) |

| Ageing population driving demand for anti-hair-loss and colour maintenance | +0.9% | National, concentrated in urban cantons | Long term (≥ 4 years) |

| Increasing popularity of scalp health and holistic hair care | +0.7% | National, with premium positioning in affluent areas | Medium term (2-4 years) |

| Influence of social media and beauty influencers | +0.6% | National, youth-concentrated in urban centers | Short term (≤ 2 years) |

| Innovative ingredients and formulations | +0.7% | National, with Research and Development concentration in the Basel region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Personalized Hair Care Solutions

The Swiss Hair Care Market is experiencing increased demand for personalized hair care solutions, driven by evolving consumer preferences and economic factors. Consumers actively seek customized formulations that effectively address specific concerns, including dryness, hair loss, scalp sensitivity, and color preservation. These targeted solutions strongly align with Swiss consumers' established focus on product efficacy and quality. According to the World Population Review, Switzerland's sophisticated high-income consumer base significantly supports the growth of premium hair care products. With an average household net-adjusted disposable income per capita of USD 47,124 in 2023, Swiss consumers demonstrate substantial purchasing power to invest in specialized hair care solutions rather than standard mass-produced products [1]Source: World Population Review. "Disposable Income by Country 2025", https://worldpopulationreview.com. This robust economic strength, combined with the deeply rooted Swiss emphasis on quality and precision, continues to drive substantial growth in the market for personalized hair care products.

Sustainable Packaging Appeals to Eco-Conscious Consumers

Environmental packaging serves as a primary growth catalyst in the Swiss Hair Care Market, as consumers demonstrate an increasing preference for environmentally responsible products. Swiss consumers exhibit a strong inclination toward hair care brands that implement recyclable, biodegradable, or reusable packaging materials. Environmental consciousness and plastic waste concerns significantly influence consumer purchasing patterns, necessitating companies to implement sustainable packaging solutions. Industry participants are advancing their environmental initiatives through packaging innovations. For instance, in April 2024, Wella Company implemented its Welloxon Perfect professional color product, incorporating multi-layer molding technology that facilitates the substitution of up to 70% virgin plastic with post-consumer recycled materials. These advancements correspond to consumer requirements while establishing enhanced sustainability standards in the market.

Ageing Population Driving Demand for Anti-Hair-Loss and Colour Maintenance

The demographic composition in Switzerland demonstrates a significant correlation between the aging population and increased demand for specialized hair care products, particularly anti-hair-loss and color maintenance solutions. The substantial increase in the older adult demographic has generated heightened requirements for addressing hair thinning, loss prevention, and color preservation. This demographic segment requires comprehensive hair care solutions that effectively minimize hair loss, enhance structural integrity, and maintain color retention, thereby addressing both physiological and psychological requirements. According to the Federal Statistical Office of Switzerland, in 2024, there were 37.4 persons aged 65 or older for every 100 economically active persons aged 20 to 64. [2]Source: Federal Statistical Office of Switzerland, "Number of persons aged 65 and older per 100 economically active persons aged 20 to 64", www.bfs.admin.ch. This demographic distribution indicates substantial market opportunities for hair care products specifically formulated for mature consumers. The expansion of the elderly population segment continues to generate consistent demand for specialized formulations addressing aging hair and scalp conditions, with particular emphasis on color retention and hair fortification solutions.

Increasing Popularity of Scalp Health and Holistic Hair Care

The hair care market is driven by the growing focus on scalp health and comprehensive hair care solutions. Consumers recognize that scalp health directly influences hair quality, increasing the demand for products that address scalp cleansing, nourishment, and balance. This approach extends beyond aesthetic improvements to target fundamental scalp conditions, including dryness, irritation, dandruff, and sensitivity. The market growth is supported by new formulations incorporating natural and therapeutic ingredients for scalp care. Product categories such as exfoliating scrubs, serums, oils, and masks designed for scalp improvement and hair growth have gained consumer interest. Technological developments in personalized hair care and diagnostic tools enable consumers to identify and address specific scalp issues. Environmental factors, stress, and frequent use of chemical or heat treatments have increased scalp sensitivity concerns, emphasizing the importance of targeted scalp care products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of counterfeit hair care products affects market revenues | -0.4% | National, with higher impact in border regions | Short term (≤ 2 years) |

| Stringent safety and regulatory compliance | -0.5% | National, affecting all market participants | Long term (≥ 4 years) |

| Health concerns over chemical ingredients | -0.4% | National, stronger in urban educated segments | Medium term (2-4 years) |

| Intense competition between local and international brands | -0.3% | National, concentrated in retail channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Presence of Counterfeit Hair Care Products Affects Market Revenues

The proliferation of counterfeit hair care products presents a substantial impediment to the Swiss Hair Care Market, resulting in diminished market revenues. These unauthorized products, typically sold at lower prices without meeting quality and safety standards, damage consumer trust and market competition. The presence of fake products results in revenue losses for legitimate manufacturers and retailers while damaging brand reputation and consumer confidence. Additionally, counterfeit hair care products may contain harmful ingredients that pose health risks, increasing consumer skepticism toward hair care purchases. The rise of e-commerce platforms has made it more challenging to detect and control counterfeit product distribution. These factors collectively impede market expansion by diminishing sales volumes and compromising initiatives to maintain product quality standards and consumer protection within the Swiss hair care market.

Stringent Safety and Regulatory Compliance

Strict safety and regulatory compliance requirements constrain the Hair Care Market. The industry must adhere to comprehensive regulations, including the revised Swiss Chemicals Ordinance and the upcoming Packaging Ordinance. These regulations establish specific standards for product formulation, ingredient safety, packaging, labeling, and environmental impact. While these measures protect consumers and promote sustainability, they increase product development costs and complicate market entry processes. New and smaller companies face significant challenges in meeting compliance requirements, which involve extensive documentation, testing, and certification. The regulatory requirements can delay product launches, reduce innovation capabilities, and increase operational costs, affecting profit margins. Companies also face risks such as fines, product recalls, and reputation damage for non-compliance. These regulatory demands create market entry barriers and favor established companies with existing compliance systems, limiting growth opportunities for new brands in the Swiss hair care market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoo Dominance Faces Styling Innovation

In 2025, shampoo held the largest share in the Swiss Hair Care Market at 43.02%. This significant share reflects shampoo's essential role in daily hair care routines, primarily for cleansing hair and removing dirt, excess oils, and impurities. The segment's strength stems from ongoing formulation improvements that enhance hair health through the inclusion of vitamins, botanical extracts, and oils for hair growth and scalp health. The availability of diverse variants for different hair types and concerns, including herbal and organic options, maintains consistent consumer demand. The widespread daily use of shampoos across consumer segments reinforces its market position.

Hair Styling Products in the Swiss Hair Care Market are expected to grow at a CAGR of 5.1% through 2031. This growth stems from consumers' increasing focus on hair aesthetics and personal grooming. The market expansion is supported by demand for products offering long-lasting hold, heat protection, and nourishing benefits. Social media, fashion trends, and celebrity influences drive increased product adoption. The segment's growth is further supported by its diverse product range, including gels, sprays, mousses, and serums for various hair types and styling requirements. This growth trajectory indicates a market shift from basic hair care towards styling and personalization.

By Category: Premium Acceleration Amid Mass Market Stability

Mass Products dominated the Switzerland Hair Care Market in 2025 with a market share of 69.55%, meeting the everyday hair care needs of a large consumer base. This dominance stems from their affordability and widespread availability, making these products accessible to consumers across diverse demographics. Mass products are readily available in mainstream retail channels, facilitating convenient purchases and strengthening their market presence. The functional and reliable nature of mass products appeals to price-sensitive consumers who prioritize value for money. Regular innovation within the mass segment, including improvements in formulations that address common hair concerns like dandruff, dryness, and hair fall, helps maintain consumer loyalty while attracting new buyers. Marketing strategies emphasizing everyday practicality and established brand reputations contribute to the strong position of mass products in the Swiss hair care market.

Premium Products in the Switzerland Hair Care Market are projected to grow at a compound annual growth rate (CAGR) of 6.18% through 2031. This growth reflects consumer preferences for high-quality, specialized hair care solutions that offer benefits beyond basic cleansing and conditioning. The increasing demand is driven by greater awareness of advanced formulations with natural, organic, and scientifically backed ingredients that promote hair health and address specific concerns such as damage repair, anti-aging, and scalp care. Consumer interest in personalized beauty routines and premium self-care experiences supports market expansion for these upscale products. The premium segment benefits from innovations in sustainable and eco-friendly packaging that appeal to environmentally conscious consumers.

By Ingredient Type: Natural Surge Challenges Conventional Dominance

In 2025, conventional and synthetic ingredients held a dominant market share of 75.72% within the Market. These ingredients remain prevalent due to their consistent performance and efficacy in hair care products. Conventional and synthetic formulations provide targeted solutions for hair concerns such as dandruff control, hair strengthening, and scalp health, attracting consumers who prioritize proven results at competitive prices. Their widespread use across hair care product categories stems from their versatility and effectiveness. The established manufacturing infrastructure and regulatory compliance of synthetic ingredients further reinforce their market position. Consequently, conventional and synthetic-based products maintain their substantial market presence by offering reliability, affordability, and functionality that address consumer needs.

Natural and organic formulations in the Hair Care Market are growing at a CAGR of 6.44% through 2031, indicating increased consumer preference for clean and environmentally conscious hair care options. This growth stems from heightened awareness of natural ingredient benefits, including reduced chemical exposure, improved scalp health, and sustainable sourcing practices. The trend aligns with Swiss consumers' increasing focus on wellness and environmental responsibility. According to the International Federation of Organic Agriculture Movements (IFOAM), Switzerland recorded one of the highest organic product retail sales shares among European countries in 2023, with organic products accounting for 11.6% of total retail sales . This significant organic market presence demonstrates Swiss consumers' established preference for natural products, directly contributing to the growth of natural and organic hair care formulations.

By Distribution Channel: Digital Acceleration Transforms Traditional Retail

In 2025, supermarkets and hypermarkets held a dominant market share of 43.86% in hair care product distribution. These large-scale retail outlets offer consumers extensive reach and convenience through their one-stop shopping experience for household and personal care items. Their market leadership stems from competitive pricing strategies and regular promotional activities that appeal to price-sensitive consumers. These stores stock a comprehensive range of mass-market and premium hair care brands, addressing diverse consumer needs. Their widespread presence in urban and suburban locations ensures accessibility and consistent customer traffic, maintaining steady sales volumes.

Online retail stores in the Switzerland hair care market are experiencing growth at a CAGR of 7.21% through 2031, indicating a fundamental shift in consumer purchasing patterns. The Federal Statistical Office of Switzerland reports that in 2023, 82% of individuals aged 25 to 34 made online purchases, while 45% of those aged 65 to 74 engaged in e-commerce activities. This growth is driven by the convenience, extensive product selection, and competitive pricing of online platforms. The increasing digital literacy and mobile internet adoption across age groups continue to strengthen the online retail channel for hair care products.

Geography Analysis

Switzerland's hair care market benefits from concentrated population growth in urban cantons surrounding Zurich and Geneva. Demographic projections indicate growth in other urban centers like Lucerne, contributing to a rising consumer base with higher purchasing power and evolving lifestyle preferences. These urban cantons function as centers for mass and premium hair care consumption due to increased awareness of grooming and beauty trends. The high population density in these areas supports a robust market for hair care products.

The regional concentration supports growth in salon density and professional hair care services, particularly in urban corridors connecting major cities. The high number of salons and beauty service providers creates opportunities for specialized treatments and premium product categories through direct consumer interaction and professional recommendations. The expansion of professional channels increases demand for advanced formulations and premium brands, developing a strong value-added segment alongside mass-market sales.

Border cantons face specific competitive challenges due to cross-border shopping, with over half of residents shopping abroad more frequently than the national average. This creates pricing pressure and revenue loss for domestic hair care retailers. In response, the Swiss government implemented a policy in 2025 that reduced the tax-free limit on cross-border purchases. This measure aims to minimize domestic sales loss to foreign markets. The policy change is expected to improve hair care sales within border regions by encouraging local shopping, strengthening domestic market stability, and improving competitive conditions for Swiss retailers in these cantons.

Competitive Landscape

The Swiss hair Care Market shows moderate concentration, with international companies like Beiersdorf AG, The Procter & Gamble Company, Henkel AG & Co. KGaA, Wella Company, and L'Oreal S.A. maintaining dominant positions through established distribution partnerships. These multinational corporations utilize extensive networks to maintain market leadership. Meanwhile, domestic companies focus on Swiss-made products and specialized formulations to capture premium market segments. The market structure balances global brand presence with local players who appeal to quality-focused consumers.

Technology adoption has emerged as a significant competitive differentiator in the market. Major hair care brands implement augmented reality (AR) and virtual reality (VR) technologies for product trials, allowing consumers to test products digitally before purchasing. AI-powered personalization enables brands to provide customized hair care recommendations based on individual consumer needs. These technological integrations improve customer engagement and retention, offering companies strategic advantages in market share growth.

The Swiss Chemicals Ordinance significantly influences competitive dynamics in the hair care market. Established companies with robust regulatory compliance systems are better positioned to meet strict requirements. The regulations require extensive documentation, safety protocols, and sustainability standards, creating substantial barriers for new market entrants who lack the necessary expertise and operational capabilities. These regulatory requirements favor established firms, strengthening their market positions while limiting opportunities for smaller or new companies entering the market.

Switzerland Haircare Industry Leaders

-

Beiersdorf AG

-

The Procter & Gamble Company

-

Henkel AG & Co. KGaA

-

Wella Company

-

L'Oreal S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Wella Company launched its first bonding hair color line under the Clairol brand. The product line features a 3-step hair coloring process that includes Alpha Hydroxy Acid (AHA), a skincare ingredient that strengthens and revitalizes hair from the inside out.

- May 2024: PERL Cosmetics has introduced its Stimulating Hair Oil formulation, which incorporates a proprietary combination of natural ingredients recognized for their restorative and rejuvenating properties.

- October 2023: Marionnaud Switzerland partnered with Revieve to launch an AI-powered hair care advisor in Switzerland. The partnership integrates Revieve's mobile selfie diagnostic technology for hair analysis.

Switzerland Haircare Market Report Scope

Hair care comprises of five types of products which includes Colorants, hair spray, conditioner, styling gel, hair oil, shampoo, mousses, serums, glazes, root touch up products, and accessories. The distribution channels include direct selling, hypermarket and retail chain, specialty store, e-commerce, salon, pharmacy, and other small scale stores, etc. Hair sprays consist of various hair care products in sprays and mist formats, such as dry shampoos, organic detanglers, protective and styling serums, and volumizing products. Furthermore, with men in the country becoming more conscious about their hairstyles, they have been increasingly relying on hairsprays. Moreover, a majority of the male population in the country uses hairspray products, for a lighter and natural look, while delivering a trending hairstyle.

By Product Type

| Shampoo |

| Conditioner |

| Hair Colorants |

| Hair Styling Products |

| Other Product Types |

By Category

| Premium Products |

| Mass Products |

By Ingredient Type

| Natural and Organic |

| Conventional/Synthetic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Shampoo |

| Conditioner | |

| Hair Colorants | |

| Hair Styling Products | |

| Other Product Types | |

| By Category | Premium Products |

| Mass Products | |

| By Ingredient Type | Natural and Organic |

| Conventional/Synthetic | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Health and Beauty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the Switzerland hair care market in 2026?

It is valued at USD 440.36 billion, with growth projected to a USD 557.09 billion ceiling by 2031.

Which product leads category sales?

Shampoo accounts for 43.02% of 2025 value, maintaining category primacy.

What is the fastest-growing segment by ingredient?

Natural and organic formulations are expanding at a 6.44% CAGR through 2031.

Which sales channel is growing the quickest?

Online retail stores are projected to post a 7.21% CAGR, outpacing all physical channels.

Page last updated on: