Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.18 Billion |

| Market Size (2026) | USD 3.31 Billion |

| Market Size (2031) | USD 4.03 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

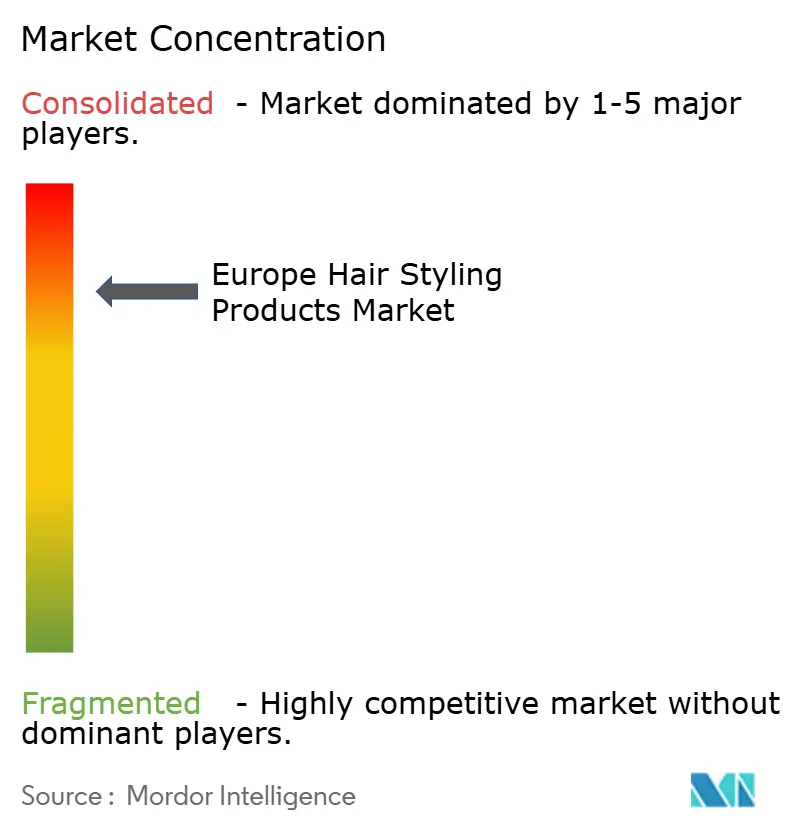

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Hair Styling Products Market Analysis by Mordor Intelligence

The European hair styling products market size was valued at USD 3.18 billion in 2025 and estimated to grow from USD 3.31 billion in 2026 to reach USD 4.03 billion by 2031, at a CAGR of 4.01% during the forecast period (2026-2031). This growth stems from changing consumer preferences, particularly the increased demand for clean, sustainable, and health-focused beauty products. European consumers are showing a stronger preference for sulfate-free and silicone-free hair styling products, driven by concerns about scalp health, hair damage, and chemical exposure. In response, manufacturers are developing new formulations that align with clean beauty requirements. The market expansion is further supported by growing haircare awareness, influenced by social media and online professional haircare content, which drives the consumption of styling products like gels, sprays, waxes, and creams. The market benefits from urbanization, higher disposable incomes, and increased personal grooming focus, particularly among male consumers and younger age groups. The availability of organic and plant-based products, combined with expanded e-commerce distribution, has improved market access for both established and new brands.

Key Report Takeaways

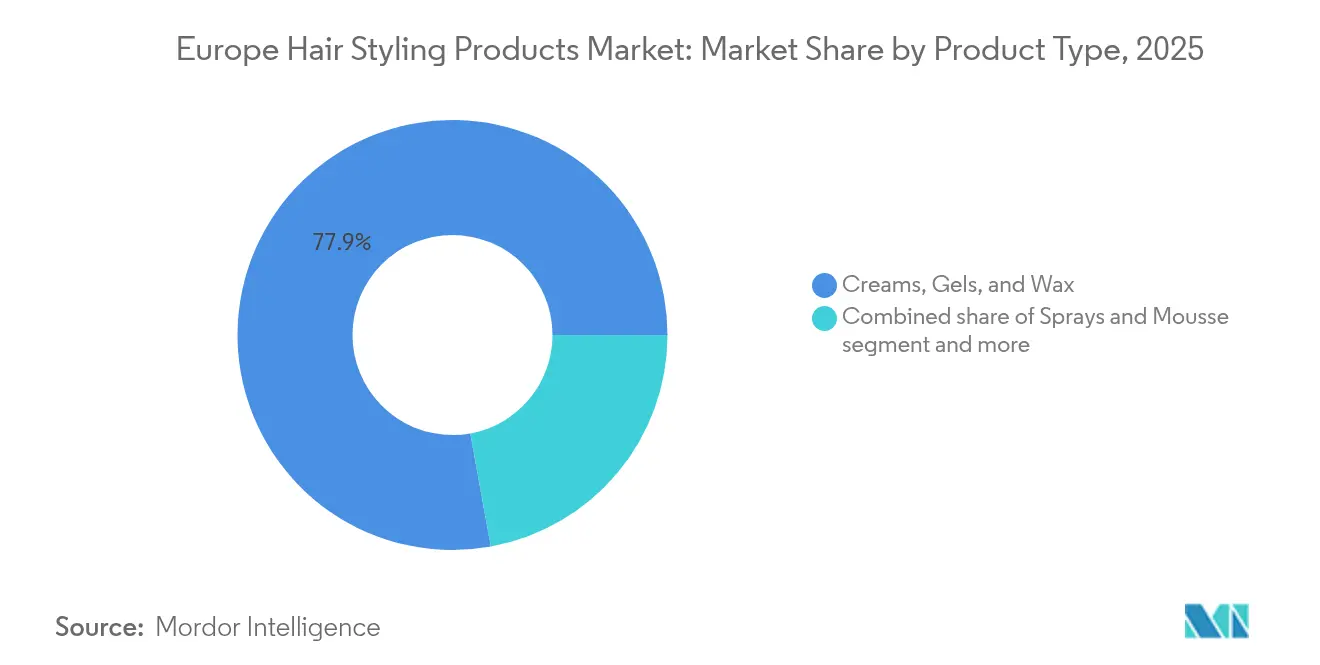

- By product type, creams, gels, and wax collectively captured 77.85% of the European hair styling products market share in 2025, while sprays and mousses are projected to expand at a 4.18% CAGR through 2031.

- By ingredient class, conventional/synthetic formulations commanded 72.95% of the European hair styling products market size in 2025; the natural/organic tier is expected to grow at a 4.39% CAGR to 2031.

- By end user, male consumers contributed 79.55% of the European hair styling products market size in 2025, whereas the female segment is on track for a 4.69% CAGR between 2026 and 2031.

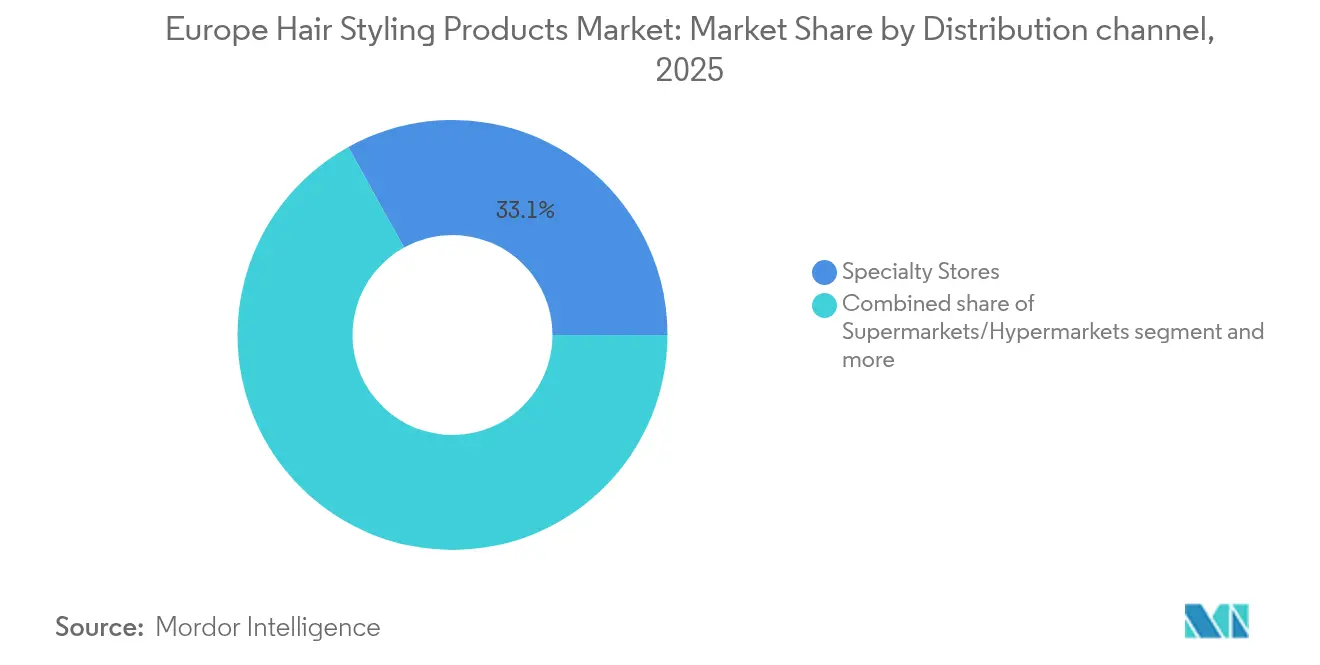

- By distribution channel, specialty stores led with 33.05% revenue share in 2025; online retail is forecast to post the highest 4.88% CAGR.

- By country, Germany led the regional market with a 29.35% revenue share in 2025, while Spain is projected to grow at a 5.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Hair Styling Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge of sulfate-free and silicone-free formulations | +0.2% | Western Europe, spreading to Eastern Europe | Medium term (3-4 years) |

| Influence of social media and celebrity endorsement | +0.4% | Pan-European, strongest in United Kingdom, France, Germany | Short term (≤ 2 years) |

| Shift towards natural and organic products | +0.5% | Nordics, Germany, France, United Kingdom | Long term (≥ 5 years) |

| Technological innovations in product formulations | +0.2% | Germany, France, United Kingdom, Italy | Medium term (3-4 years) |

| Increasing focus on personal grooming | +0.3% | Pan-European, strongest in urban centers | Long term (≥ 5 years) |

| Growing male grooming segment | +0.2% | Western Europe, expanding to Eastern Europe | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Surge of Sulfate-Free and Silicone-Free Formulations

The European hair styling products market demonstrates a significant transition toward sulfate-free and silicone-free formulations, primarily attributed to heightened consumer awareness and increasing demand for healthier, sustainable alternatives. The market evolution reflects a fundamental shift in consumer preferences toward natural ingredients and environmentally conscious products. Contemporary technological advancements in formulation methodologies facilitate superior styling performance while incorporating essential benefits such as thermal protection, enhanced moisturization, and structural repair properties. For instance, in May 2023, Maria Nila introduced the Coils & Curls haircare line, incorporating specialized nourishing ingredients designed to deliver optimal hydration and refined washing and styling processes. The entire Coils & Curls product range maintains strict exclusion of sulfates, parabens, and silicone compounds.

Influence of Social Media and Celebrity Endorsement

The European hair styling products market has experienced a significant transformation through social media platforms' influence on marketing and consumption patterns. Companies strategically implement celebrity endorsements as a primary marketing approach, wherein prominent personalities promote products to drive consumer purchasing decisions. The effectiveness of these endorsements is contingent upon the strategic alignment between the celebrity's profile and the product attributes, coupled with their capacity to effectively convey brand messaging to the target demographic. Companies are demonstrating increased commitment to marketing investments in the European region. For instance, according to L'Oréal's universal registration document, the company's global advertising and promotional expenditure increased from EUR 13.3 billion in 2023 to EUR 14 billion in 2024.

Shift Towards Natural and Organic Products

The European hair styling products market is experiencing a significant shift toward natural and organic formulations. Consumer awareness about the health and environmental impacts of synthetic chemicals has increased the demand for safer and sustainable alternatives. The European Commission's Green Deal initiatives, particularly the Chemicals Strategy for Sustainability, require chemical use in consumer products, including cosmetics, to meet strict safety and sustainability standards. These regulations have led manufacturers to reformulate hair styling products with natural ingredients. Europe maintains its position as the world's largest importer of vegetable and essential oils, key components in natural hair styling products. In 2023, the region represented 48% of global import volume and 42% of value in this category, according to the Ministry of Foreign Affairs. This import strength demonstrates Europe's ability to maintain high natural ingredient usage, supporting the growth of organic hair styling formulations across the region.

Technological Innovations in Product Formulations

Technological advancements in product formulations are driving significant changes in the European hair styling products market. Research and development efforts focus on improving product performance, sustainability, and consumer safety. European manufacturers are developing high-performance hair styling solutions that meet consumer demands for clean-label, environmentally conscious, and multi-functional products. The integration of nanotechnology, encapsulation techniques, and bio-based polymers has improved ingredient delivery systems, providing better texture, hold, and finish while maintaining hair health. Additionally, biotechnology applications have enabled the development of natural active compounds and biodegradable formulations that comply with European regulations. The European Commission's Horizon Europe program, with a budget of EUR 93.5 billion for 2021-2027, supports these developments through funding for scientific research, climate change initiatives, and United Nations Sustainable Development Goals (SDGs) [1]Source: European Commission, "Horizon Europe", commission.europa.eu. This coordination between government initiatives and industry research is increasing the availability of advanced, environmentally responsible hair styling products in the European market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over chemical ingredients | -0.3% | Pan-European, strongest in Nordics and Germany | Long term (≥ 5 years) |

| Proliferation of counterfeit products | -0.3% | Eastern Europe, Southern Europe, Online channels | Medium term (3-4 years) |

| Salon service competition impacts retail market share | -0.2% | Urban centers, professional salon districts | Medium term (3-4 years) |

| Sustainability concerns affect product packaging and manufacturing | -0.2% | Nordics, Germany, Netherlands, France | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over Chemical Ingredients

The increasing consumer awareness about harmful chemical ingredients in European hair styling products presents a significant market restraint. In 2024, the European Chemicals Agency expanded its Candidate List of substances of very high concern, including several ingredients commonly used in traditional hair styling formulations. This development has compelled manufacturers to reevaluate their product formulations and compliance strategies. The European Commission reported 4,137 alerts for dangerous products from European Union Members and EEA countries in 2024, marking the highest number of validated notifications in the "alert" category since the Rapid Alert System for Dangerous Non-food Products began [2]Source: European Commission, "List of dangerous products notified in Commission's Safety Gate 2024 sets the path for increased consumer protection", commission.europa.eu. This increase demonstrates the system's effectiveness in identifying potentially harmful products in the European market, which influences consumer purchasing decisions and manufacturers' product development strategies.

Proliferation of Counterfeit Products

The proliferation of counterfeit luxury hair styling products in the European market presents a substantial impediment to market growth by compromising brand integrity and eroding consumer confidence. These unauthorized replications systematically duplicate the packaging and branding elements of established luxury manufacturers, resulting in consumer deception and the purchase of substandard, potentially hazardous formulations. These counterfeit merchandise, distributed through unauthorized and unregulated distribution channels at substantially reduced price points, create direct market competition with authentic products, particularly affecting consumer segments with price sensitivity. The utilization of these inferior products frequently results in adverse consumer experiences, subsequently diminishing market confidence in legitimate luxury brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Creams, Gels, and Wax Dominate While Sprays Gain Momentum

Creams, gels, and wax products hold a 77.85% share of the European hair styling market in 2025. These products maintain their market leadership through versatility, effectiveness, and consumer preference. Gels and waxes represent the largest segment, a position expected to continue due to their styling capabilities across different hair types. The products deliver hold, shine, and frizz control through ingredients such as silicones and synthetic polymers, which form a protective barrier to enhance manageability and smoothness.

Sprays and mousse products are projected to grow at a CAGR of 4.18% from 2026 to 2031. This growth stems from consumer demand for lightweight, versatile, and easy-to-use styling solutions. These products offer volume, hold, and texture without heaviness, meeting requirements for natural-looking, flexible styles. Heat protectant and UV-shielding sprays have increased in popularity as consumers focus on hair health and multifunctional products. Mousse products appeal to consumers with fine or curly hair seeking professional results at home. Market adoption has increased through fashion trends, social media influence, and advancements in aerosol technology and eco-friendly packaging.

By Ingredient: Conventional Dominates While Natural Grows Fastest

Conventional/synthetic ingredients dominate the European hair styling products market with a 72.95% share in 2025. These products maintain their market leadership due to established consumer habits, widespread availability, and the strong presence of multinational brands. Conventional products remain popular for their proven efficacy, affordability, and broad distribution, especially among consumers prioritizing performance and convenience.

The natural/organic segment is experiencing faster growth with a CAGR of 4.39%. This growth is driven by health-conscious and environmentally aware consumers seeking natural and organic alternatives. Brands are responding by developing plant-based, sulfate-free, and eco-friendly formulations. The shift toward natural products stems from concerns about synthetic chemicals, increasing demand for clean beauty, and regulatory support for safer, non-toxic ingredients. This trend is particularly strong in countries like Germany, where ingredient transparency and sustainability are consumer priorities. While conventional products currently generate the majority of sales, the rapid expansion of the natural segment indicates a transformation in the market's competitive landscape.

By Distribution Channel: Specialty Stores Lead While Online Retail Grows Fastest

The European hair styling products market demonstrates a distinctive distribution pattern, with specialty stores maintaining a commanding market leadership position, holding a 33.05% share in 2025. This market dominance is further substantiated by Eurostat's retail trade statistics, which reveal that the seasonally adjusted retail trade volume in February 2025 exhibited an increase of 0.3% in the euro area and 0.2% in the EU compared to January 2025.

The distribution landscape is experiencing a significant transformation through digital channels, with online retail stores emerging as the fastest-growing segment, projecting a CAGR of 4.88% between 2026 and 2031. This digital evolution is validated by comprehensive Eurostat data, which indicates a remarkable progression in e-commerce adoption across the European Union, with 77% of EU internet users actively participating in online purchases in 2024, representing a substantial increase from 59% in 2014, thus highlighting the shifting consumer preferences in the hair styling products market.

By End User: Male Consumers Lead While Female Segment Grows Faster

Male consumers dominate the European hair styling products market with an 79.55% share in 2025. The market has experienced significant growth due to increased awareness and demand for products addressing men's specific hair requirements. These products contain ingredients formulated for men's grooming needs, such as coarser hair, and feature masculine packaging designs.

The female segment is projected to grow at a CAGR of 4.69% between 2026 and 2031. This growth is driven by cultural, social, and economic factors, emphasizing personal grooming and beauty among women. Fashion trends, celebrity styles, and major events like the Paris and Milan Fashion Weeks influence European women's hairstyling choices. Social media and beauty influencers contribute to increased product adoption as women explore new styles. The rising number of working women and millennials seeking solutions for hair concerns, including damage and hair fall caused by stress and lifestyle changes, has increased demand for specialized, high-quality hair styling products.

Geography Analysis

Germany holds a 29.35% share of the European hair styling products market in 2025, driven by its large market size, robust consumer demand, and focus on personal grooming and innovation. German Gen Z consumers show high engagement with hair styling and frequently try new products and trends. The country's diverse population creates demand for specialized products addressing various hair types, textures, and needs, prompting brands to develop both traditional and natural formulations.

The United Kingdom represents a significant portion of the European hair styling products market, with growth expected across consumer and professional segments. The market benefits from the cultural importance of personal grooming, fashion, and celebrity influence, along with increased digital product accessibility. According to the Office for National Statistics (UK), households in the fifth decile group allocated an average of GBP 3.8 weekly to hair and cosmetic products in 2023 .

The Spain segment demonstrates the strongest growth potential in the European hair styling products market, with a projected compound annual growth rate (CAGR) of 5.32% from 2026 to 2031. The market expansion is attributed to heightened grooming awareness, fashion trend adoption, and increased demand for multifunctional and natural hair styling products. Companies such as Revlon Professional and Salerm Cosmetics are expanding their styling product portfolios in Spain by introducing formulations that combine hold properties with hair nourishment and heat protection capabilities.

Competitive Landscape

The European hair styling products market operates as a consolidated industry, where multinational corporations and regional companies control the competitive landscape. Major companies such as L'Oréal S.A., Henkel AG & Co. KGaA, Procter & Gamble Co., Unilever PLC, and Coty Inc. focus on developing premium products and implementing sustainable practices, including natural formulations and eco-friendly packaging. Independent brands focusing on clean beauty and sustainability have emerged as significant market challengers.

European consumers' growing concerns about traditional hair styling products potential harmful effects have increased demand for natural and organic alternatives. This shift has created opportunities for research and development in natural ingredients that address contemporary hair and scalp issues, particularly those arising from long-term use of chemical-based products. The market has also seen increased competition from local manufacturers who develop products aligned with regional preferences.

The evolving consumer preferences have prompted both established companies and new entrants to adapt their product development strategies. This adaptation includes incorporating natural ingredients, sustainable packaging solutions, and formulations that address specific regional requirements. The market continues to witness a transformation as companies balance innovation with sustainability to meet changing consumer demands.

Europe Hair Styling Products Industry Leaders

-

L’Oréal S.A.

-

Henkel AG & Co. KGaA

-

Unilever PLC

-

Coty Inc.

-

Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: K18 introduced AstroLift, a volumizing spray that increased hair fullness and repaired hair internally. The product utilized K18PEPTIDE technology to provide instant volume and sustained improvements for fine, aging, and damaged hair.

- November 2024: Slick Gorilla introduced its Cream Styler, a men's hair care product. The formulation incorporated castor oil for smoothness, squalene, and hydrolyzed soy protein to enhance moisture and shine.

- August 2024: Dyson introduced its first integrated haircare and styling product range that featured chitosan, a compound derived from oyster mushrooms. The product line incorporated the company's Triodetic technology to maintain flexible hair hold throughout the day.

- May 2024: Volyoume released a hair spray in the United Kingdom that addressed scalp health, hair thinning, and hair loss. The clinically tested product aimed to stimulate natural hair growth.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe hair styling products market as all retail and professional leave-on formulations (creams, gels, waxes, sprays, mousses, pomades, serums) used to shape, hold, or texture hair across Germany, the United Kingdom, France, Italy, Spain, Russia, and the rest of Europe. Values are expressed in USD at manufacturer selling price before taxes.

Scope Exclusions. We exclude electric styling tools, rinse-off shampoos and conditioners, colorants, and salon-only chemical straightening kits.

Segmentation Overview

-

By Product Type

- Creams, Gels, and Wax

- Sprays and Mousse

- Others

-

By Ingredient

- Natural/Organic

- Conventional/Synthetic

-

By End User

- Male

- Female

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Others

-

By Country

- Germany

- United Kingdom

- Italy

- Spain

- France

- Russia

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

We interviewed formulators, salon chain buyers, beauty e-tail managers, and dermatologists in five major economies. Their insights validated shelf-price assumptions, confirmed volume run-rates, and revealed accelerating demand for natural and organic formulations.

Desk Research

We pulled trade flow statistics from Eurostat, ingredient import codes from UN Comtrade, and yearly cosmetic turnover tables issued by Cosmetics Europe. Company 10-Ks, investor decks, and retailer scans helped us map average selling prices, while D&B Hoovers and Dow Jones Factiva supplied revenue splits for key producers. Patent abstracts from Questel highlighted a shift toward sulfate-free polymers, and European Chemicals Agency notices clarified ingredient limits.

Mordor analysts balanced these numeric sources with lifestyle surveys from Statista, salon service counts released by national hairdressing associations, and historical currency tables that keep multi-year values comparable. The list above is not exhaustive. Many additional references guided data collection, validation, and research clarification.

Market-Sizing & Forecasting

A top-down build starts with Eurostat cosmetic output, filters to styling share through trade-code parsing, and then converts volumes to value with weighted ASPs vetted in field calls. Select bottom-up roll-ups of supplier revenues and online SKU trackers provide a reasonableness lens before totals are frozen. Variables such as per-capita disposable income, online beauty penetration, salon visit frequency, male grooming uptake, and natural-ingredient adoption feed a multivariate regression that projects demand to 2030. Data gaps in smaller markets are bridged by regional price-volume proxies discussed with country experts.

Data Validation & Update Cycle

Each model draft passes anomaly checks, peer review, and senior sign-off. Reports refresh annually, and interim updates follow material events like raw-material shocks or regulatory bans. A final analyst sweep ensures clients receive the latest view.

Why Our Europe Hair Styling Products Baseline Earns Trust

Published estimates often diverge because firms mix product families, apply outdated price ladders, or freeze exchange rates at dissimilar points. By keeping scope tight and refreshing numbers every year, Mordor maintains a current, defensible view.

Key gap drivers include competitors stacking rinse-off products with stylers, leaning on consumer-spend surveys without producer audits, or locking ASPs for five-plus years, which inflates totals against Mordor's USD 3.18 billion 2025 baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.18 Bn (2025) | Mordor Intelligence | |

| USD 7.28 Bn (2024) | Regional Consultancy A | Bundles stylers with leave-in treatments, keeps static 2019 ASP |

| USD 6.61 Bn (2023) | Global Consultancy B | Relies on consumer-spend surveys, uses broader geography mix |

| USD 7.70 Bn (2023) | Trade Journal C | Uses import plus salon sales only, lacks mass retail and inflation adjustment |

These comparisons show that once scope creep and dated price assumptions are stripped away, Mordor's disciplined, transparent pathway offers decision-makers a balanced baseline they can replicate and stress-test with ease.

Key Questions Answered in the Report

What is the current value of the Europe hair styling products market?

The market generated USD 3.31 billion in 2026 and is set to reach USD 4.03 billion by 2031.

Which product type holds the largest share?

Creams, gels, and waxes lead with 77.85% share, driven by their versatile hold and finish options.

How fast is the natural and organic segment growing?

Natural and organic styling products are forecast to expand at a 4.39% CAGR between 2026 and 2031, outpacing conventional formulas.

Why is Germany the largest national market?

High purchasing power, a strong salon culture, and early adoption of clean-label innovations give Germany a 29.35% revenue share.

Page last updated on: