Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

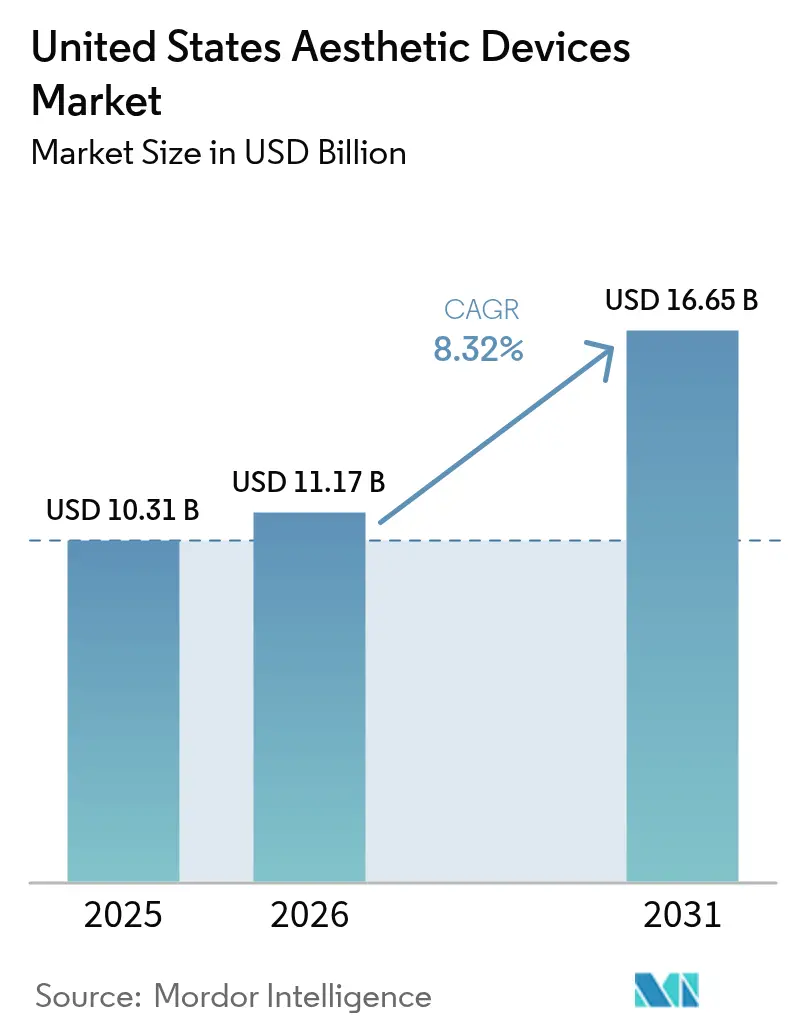

| Base Year Market Size (2025) | USD 10.31 Billion |

| Market Size (2026) | USD 11.17 Billion |

| Market Size (2031) | USD 16.65 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

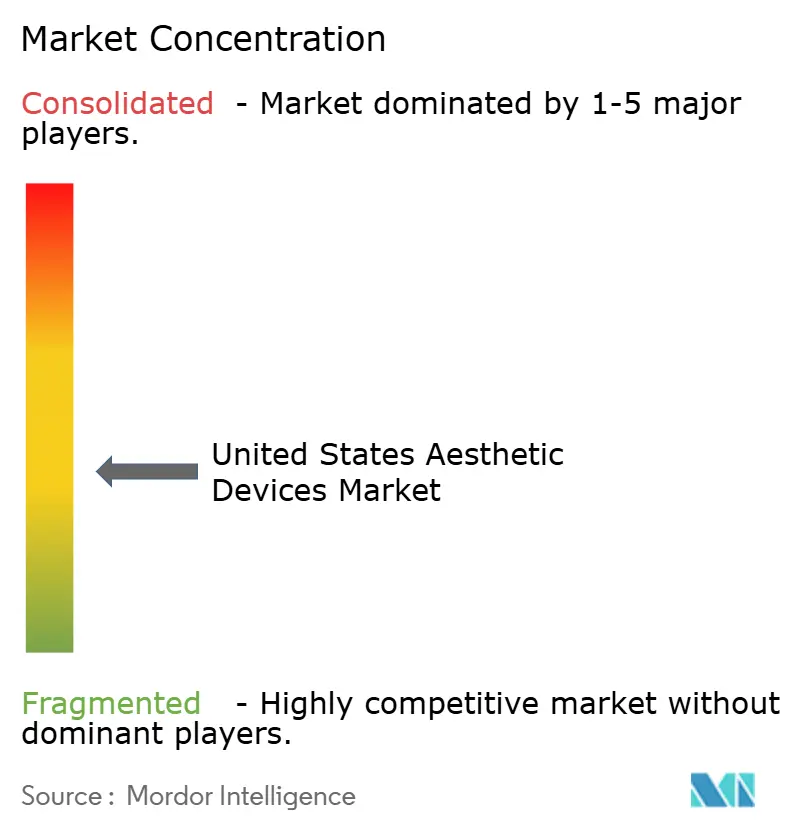

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Aesthetic Devices Market Analysis by Mordor Intelligence

United States Aesthetic Devices market size in 2026 is estimated at USD 11.17 billion, growing from 2025 value of USD 10.31 billion with 2031 projections showing USD 16.65 billion, growing at 8.32% CAGR over 2026-2031.

Accelerated private-equity consolidation, faster FDA clearances for energy-based platforms, and rising demand for minimally-invasive procedures place the United States aesthetic devices market on a strong growth trajectory. Device makers are bundling artificial-intelligence (AI) software with radio-frequency and laser systems, enabling clinics to deliver surgical-level results without incisions. Home-use technologies are moving toward over-the-counter Class II status, widening consumer access and further expanding the United States aesthetic devices market. Meanwhile, semiconductor supply-chain vulnerabilities and new state-level scope-of-practice bills introduce operational complexity that manufacturers must navigate to protect margins and sustain innovation pipelines.

Key Report Takeaways

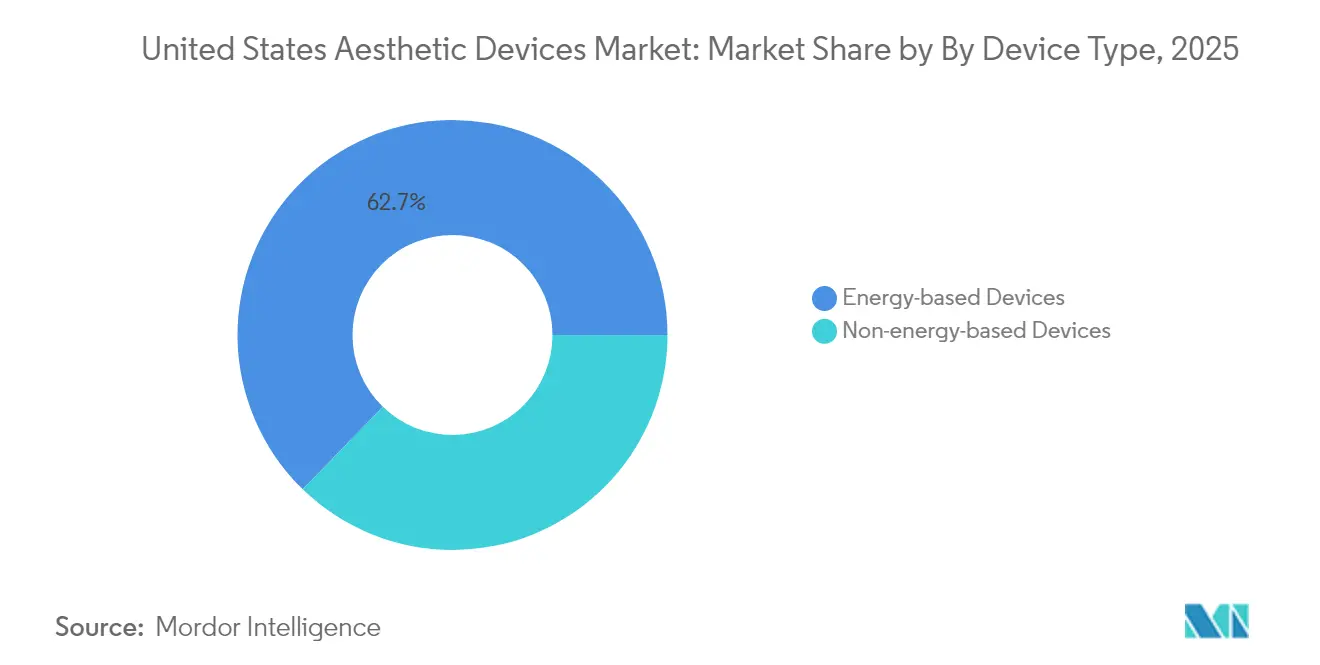

- By device type, energy-based platforms held 62.74% of the United States aesthetic devices market share in 2025, and the radio-frequency-based segment is poised for an 10.78% CAGR to 2031.

- By application, hair removal held 28.55% of the United States aesthetic devices market share in 2025 and body contouring and cellulite reduction are poised for a 9.74% CAGR to 2031, the highest growth across treatment categories.

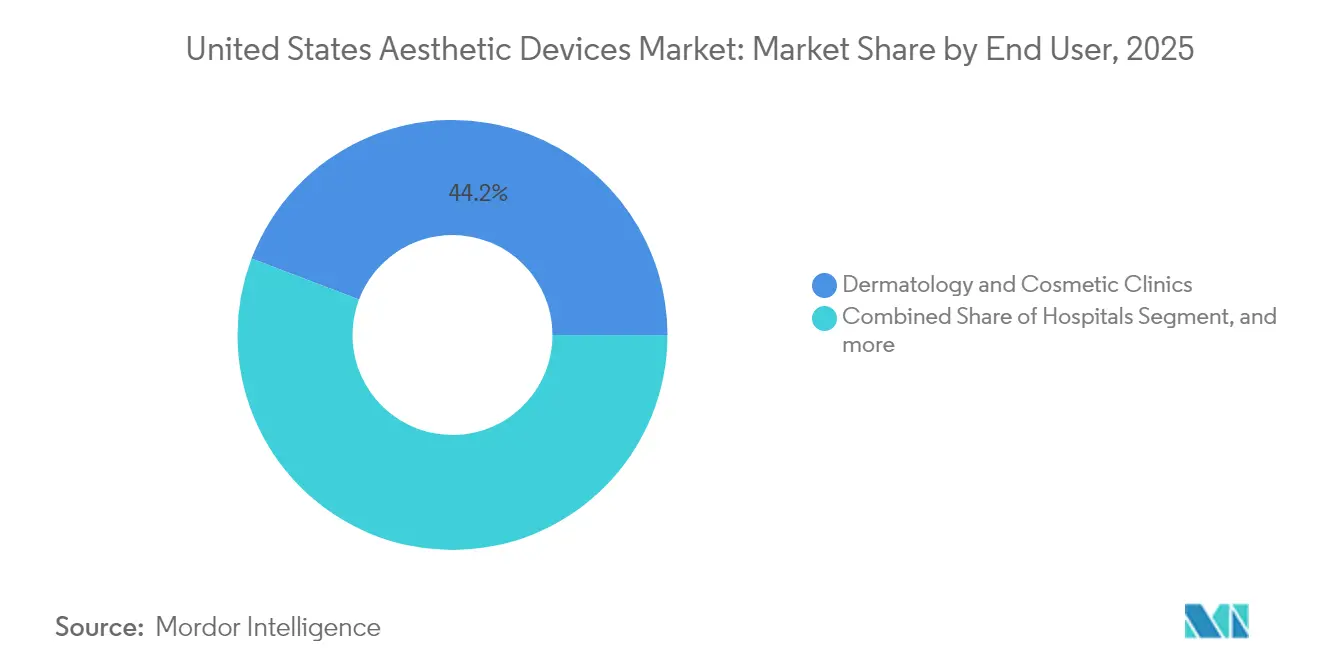

- By end user, dermatology & cosmetic clinics held 44.22% of the United States aesthetic devices market share in 2025 home-use settings are advancing at a 8.95% CAGR through 2031, the fastest among all delivery channels.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Minimally-invasive procedure preference | +2.1% | Nationwide, heightened in West & Northeast | Medium term (2-4 years) |

| Obesity-linked body-contouring demand | +1.8% | National, strongest in South & Midwest | Long term (≥ 4 years) |

| Energy-device technological advances | +1.5% | National, R&D hubs on West Coast | Medium term (2-4 years) |

| Male consumer adoption | +1.2% | Nationwide metro clusters | Long term (≥ 4 years) |

| AI-driven personalization | +0.9% | Tech-forward regions | Short term (≤ 2 years) |

| Private-equity med-spa chains | +0.7% | High-density urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally-Invasive Procedures

American Society of Plastic Surgeons data show non-surgical treatments outpacing surgeries, propelling clinics to favor devices that deliver lift, tightening, or pigment correction without incisions.[1]American Society of Plastic Surgeons, “2024 Procedural Statistics,” plasticsurgery.org FDA clearance of AI-guided radio-frequency platforms, such as Candela’s Matrix, illustrates regulatory encouragement for technologies that minimize downtime while matching surgical outcomes. Manufacturers are shortening redesign cycles to embed thermal sensors and impedance feedback that protect epidermal layers. Patient satisfaction now exceeds 94% for new radio-frequency microneedling protocols, encouraging cross-sell of add-on treatments at medical spas. The United States aesthetic devices market therefore benefits from wider patient pools, including working adults who previously avoided aesthetic enhancement because of recuperation concerns.

Increasing Obese Population Driving Body-Contouring Demand

The pharmaceutical surge in glucagon-like peptide-1 (GLP-1) weight-loss agents has created downstream demand for non-surgical skin-tightening and fat-reduction devices.[2]Modern Aesthetics Editorial, “Hybrid Filler Innovation Trends,” modernaesthetics.com Clinics are forming integrated pathways that begin with semaglutide prescriptions and culminate in cryolipolysis or ultrasound sessions to manage residual adiposity and laxity. FDA approvals for next-generation ultrasound body-shaping systems reposition these treatments from cosmetic to functional wellness, strengthening insurance-preauthorization debates. Practitioners in the South and Midwest report two-digit case-volume gains, aligning with regional obesity prevalence. Consequently, body-contouring revenues are forecast to outstrip hair-removal gains within the United States aesthetic devices market, signaling a structural shift toward comprehensive weight-management ecosystems.

Technological Advancements in Energy-Based Devices

Breakthrough 1,726 nm lasers achieve 70% clearance in inflammatory acne after four sessions, illustrating performance leaps that expand patient indications. InMode’s FDA-cleared Morpheus8 adds fractional radio-frequency microneedling for soft-tissue contraction, pushing platform utility beyond resurfacing into remodeling.[3]Healio Dermatology, “Morpheus8 Receives FDA Clearance for Soft-Tissue Contraction,” healio.com Real-time thermal mapping and closed-loop impedance monitoring now safeguard Fitzpatrick skin types IV–VI, overcoming historic energy-device adoption barriers among diverse populations. Combination platforms integrate Dynamic Muscle Stimulation to treat muscle laxity concurrently with adipose reduction, maximizing device ROI in high-volume clinics. These advances reinforce the premium pricing power that sustains the United States aesthetic devices market even during macroeconomic cooling.

Growing Awareness & Adoption Among Male Consumers

Male clientele now accounts for roughly 22% of U.S. clinic visits, driven by workplace age-bias concerns and social acceptance of aesthetic upkeep. Marketing campaigns underscore minimally invasive treatments and quick return-to-work timelines, resonating with professional males. Devices offering discrete recovery, such as transdermal radio-frequency or focused ultrasound, are preferred. Clinics in New York, Los Angeles, and Miami report double-digit male booking growth, prompting targeted product lines like “bro-tox” bundles. This demographic shift expands the United States aesthetic devices market beyond its historical female base, broadening the payer mix and device utilization rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social stigma & safety concerns | -1.4% | Nationwide cultural variance | Long term (≥ 4 years) |

| Lack of reimbursement | -1.1% | Universal, all socioeconomic tiers | Long term (≥ 4 years) |

| Counterfeit & gray-market devices | -0.8% | Online marketplaces | Short term (≤ 2 years) |

| Semiconductor shortages | -0.6% | All U.S. manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Social Stigma & Safety Concerns

FDA adverse-event files cite burns and pigmentation issues linked to unregulated home-use lasers, fueling negative media narratives. High-profile lawsuits against national surgery chains spotlight practitioner training gaps, undermining public confidence. The absence of a centralized cosmetic-procedure injury registry hinders transparent risk communication. Social media amplifies isolated complications, disproportionately affecting millennial and Gen-Z uptake. Although clinical evidence shows low complication rates in certified settings, stigma lingers, tempering growth potential within segments of the United States aesthetic devices market.

Lack of Reimbursement for Aesthetic Treatments

Because aesthetic services remain predominantly cash-pay, middle-income patients often delay or down-trade procedures during economic slowdowns. Physicians pivot toward aesthetic add-ons to offset declining insurance reimbursements in core medical specialties, but consumer discretionary spending elasticity can limit conversion rates. Financing programs and subscription models ease upfront costs but introduce credit-risk exposure for clinics. Without third-party payer support, the United States aesthetic devices market relies on steady economic conditions to sustain momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Energy Platforms Dominate Innovation

Energy-based platforms held 62.74% of the United States aesthetic devices market in 2025, and the category is projected to expand at a 10.78% CAGR through 2031. This dominance rests on technological elasticity: lasers, radio-frequency, ultrasound, and intense pulsed light (IPL) can each be fine-tuned for multiple indications, generating recurring revenue streams for clinics that invest in stackable handpieces. Radio-frequency leads grow because they penetrate dermal layers with minimal melanin interaction, reducing post-inflammatory hyperpigmentation risks for darker skin types. Laser-based subsegments remain strong, buoyed by 1,726 nm acne-targeting systems that achieve 70% lesion clearance rates. Ultrasound-assisted lipolysis has advanced via cavitation-controlled algorithms that preserve connective tissue, improving downtime metrics. Cryolipolysis technology fights competitive pressure by integrating pre-heating stages that boost adipocyte susceptibility to cold-induced apoptosis. Collectively, these engineering improvements anchor premium pricing and keep capital equipment upgrades flowing throughout the United States aesthetic devices market.

Non-energy devices, including botulinum toxin injectables and dermal fillers, still generate high procedure volumes but exhibit slower equipment replacement cycles. Innovative hybrid fillers, such as calcium-hydroxylapatite blended with hyaluronic acid, now deliver scaffold and hydration benefits in a single syringe, supporting moderate revenue gains. Micro-needling pens, mechanical microdermabrasion units, and chemical-peel applicators fill entry-level niches but confront saturation. Although implantable aesthetics, like silicone chin implants, secure clinical success rates above 90%, regulatory audits on device sterility and long-term biocompatibility restrain their momentum. Overall, non-energy segments add breadth but not breakout velocity to the United States aesthetic devices market.

By Application: Body Contouring Accelerates Growth

Hair-removal systems retained a 28.55% share of the United States aesthetic devices market in 2025, thanks to stable demand for diode lasers and IPL devices targeting both female and male consumers. However, body contouring and cellulite reduction are predicted to log a 9.74% CAGR, the steepest among all indications, propelled by GLP-1 weight-loss therapies that amplify post-diet skin laxity concerns. Cryolipolysis, high-intensity focused electromagnetic (HIFEM) muscle stimulators, and monopolar radio-frequency treatments converge to offer fat apoptosis, muscle toning, and dermal tightening in bundled sessions. Such combination protocols lift ticket sizes by 20%–30% on average, making body-shaping the profit engine of the United States aesthetic devices market.

Skin-resurfacing and tightening devices leverage fractional CO₂ lasers that achieve 45% texture improvement after a single pass, complemented by non-ablative erbium filters that shrink pores without downtime. Tattoo-removal lasers tuned to picosecond pulse widths extend efficacy to stubborn green and blue inks. Acne and scar-management applications ride on energy platforms delivering 70% lesion reduction, while pigment-specific wavelengths like 532 nm tackle melasma. Breast and intimate rejuvenation procedures form emergent niches, aided by temperature-controlled radio-frequency handpieces. Together, these diverse indications maximize device utilization rates, sustaining clinic profitability even as competitive entrants join the United States aesthetic devices market.

By End User: Home Settings Drive Disruption

Dermatology and cosmetic clinics controlled 44.22% of United States aesthetic devices market revenue in 2025, benefiting from specialist skill sets and access to multi-modality platforms. Medical-spa chains leverage private-equity capital to standardize service menus and negotiate volume discounts on equipment, boosting EBITDA margins. Hospitals maintain relevance in complex reconstructive or combination surgical-energy procedures that require anesthesia support.

Home-use systems, however, advance at a 8.95% CAGR through 2031 as FDA guidance on over-the-counter aesthetic devices crystallizes. IPL handsets now feature skin-tone sensors that lock pulses if melanin thresholds are exceeded, reducing burn risks. Consumer preferences for privacy and convenience spur Amazon and pharmacy-chain distribution partnerships. Nevertheless, the spread of unregistered imports has spurred the FDA to authorize port-of-entry destruction, signaling a regulatory balance between accessibility and safety. Professional settings maintain competitive high-intensity energy levels and combination therapy expertise that remain out of reach for consumer gadgets. Thus, while home units enlarge the total addressable population, clinics preserve premium treatment tiers within the United States aesthetic devices market.

Geography Analysis

California, New York, and Florida anchor the West and Northeast corridors, contributing major share of national device sales because of high disposable-income cohorts and dense provider networks. Silicon Valley’s proximity to R&D hubs accelerates prototype-to-market cycles and helps sustain the United States aesthetic devices market with continual software updates and AI-driven imaging add-ons. State boards in California have enacted detailed laser-operator credentialing that has become a de facto standard nationwide. New York’s metro concentration supports flagship training centers where manufacturers host physician-education symposia, augmenting brand loyalty.

Southern states, led by Texas and Florida, log the fastest volume growth, benefiting from population influx and high obesity prevalence, driving body-contouring demand. Texas debates around limiting aesthetic practice to physician-supervised settings could reshape nurse-practitioner-led med-spa models, injecting some policy risk into regional expansion strategies. Florida’s more permissive environment fuels med-spa franchising, with both domestic and Latin American clientele boosting off-season patient flows. The United States aesthetic devices market therefore, gains a diversified geographic revenue base that buffers state-specific regulatory swings.

The Midwest shows growing adoption in Chicago, Minneapolis, and Columbus, supported by hospital-affiliated aesthetic centers seeking ancillary cash-pay income. Equipment vendors deploy tiered pricing to fit lower per-capita income profiles while offering AI-assisted safety features that shorten practitioner learning curves. State governments like Michigan have expanded the esthetician scope to include light-therapy devices, unlocking new buyer segments for entry-level lasers. Simultaneously, North Dakota’s advanced license requirements could restrict device use to highly trained operators, underscoring the regulatory mosaic that characterizes the United States aesthetic devices market.

Competitive Landscape

Cynosure and Lutronic finalized their merger in 2024, creating a top-three revenue player with distribution in 130 countries and a deep energy-platform pipeline. AbbVie’s Allergan Aesthetics unit remains the overall leader, leveraging a diversified portfolio of neurotoxins, fillers, and energy devices, plus newly opened training centers in Orange County, Austin, and Atlanta that sharpen physician loyalty. Venus Concept reduced debt by 47% amid revenue softness, illustrating mid-tier pressures when economic cycles tighten device spending.

Private-equity funds drove 55 U.S. aesthetic deals in 2023, intensifying roll-up activity among med-spa chains and small device manufacturers. Consolidators negotiate favorable equipment leases and require bundled maintenance, fostering predictable revenue streams for suppliers within the United States aesthetic devices market. Emerging disruptors deploy AI-first architectures and subscription-based software analytics to differentiate, challenging incumbents that traditionally led with hardware. In response, established firms embed software-as-a-service dashboards that track treatment outcomes and calibrate settings remotely, complementing capital-equipment sales with recurring revenue.

Strategic pivots include InMode’s software-controlled consumable tips that lock after preset pulse counts, lifting razor-and-blade margins. Lumenis introduced OptiLIFT, which pairs Dynamic Muscle Stimulation with infrared skin contraction, capturing lower-lid laxity treatments that previously lacked non-surgical options. Cutera emerged from Chapter 11 reorganization in March 2025, shedding USD 400 million in debt and retaining its core truSculpt and xeo franchises, signaling that balance-sheet repair can restore competitiveness even after market share erosion. Overall, technology depth, financial agility, and practitioner education form the three pillars that define competitive advantage within the United States aesthetic devices market.

United States Aesthetic Devices Industry Leaders

Lumenis

Bausch Health Companies Inc. (Solta Medical Inc.)

Cynosure

AbbVie (Allergan Aesthetics)

Alma Lasers (Sisram Medical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Allergan Aesthetics opens three new state-of-the-art training centers in Orange County, Austin, and Atlanta, expanding practitioner education capacity and reinforcing market leadership through comprehensive clinical support programs.

- March 2025: Cutera completes Chapter 11 bankruptcy restructuring, reducing debt by USD 400 million while maintaining operations and customer service commitments, positioning the company for long-term growth recovery.

- February 2025: FDA approves Evolysse hyaluronic acid fillers, expanding treatment options for facial volume restoration and marking significant regulatory milestone for new injectable technologies.

United States Aesthetic Devices Market Report Scope

The scope of the United States aesthetic devices market includes all the medical devices that are used for various cosmetic procedures, including plastic surgery, unwanted hair removal, excess fat removal, anti-aging, aesthetic implants, and skin tightening, which are used for beautification, correction, and improvement of the body. Aesthetic procedures include both surgical and non-surgical procedures. The surgical procedures include liposuction, breast implants, facelifts, radiofrequency, and other related procedures. The non-surgical procedures include chemical peel, non-surgical liposuction, and skin-tightening procedures.The United States Aesthetic Devices Market is Segmented by Type of Device (Energy-based Aesthetic Device and Non-energy-based Aesthetic Device), Application (Skin Resurfacing and Tightening, Body Contouring and Cellulite Reduction, Hair Removal, Tattoo Removal, Breast Augmentation and Other Applications) and End User (Hospital, Clinics and Home Settings). The report offers values in (in USD million) for the above segments.

By Device Type

| Energy-based Devices | Laser-based |

| Light-based (IPL) | |

| Radio-frequency-based | |

| Ultrasound-based | |

| Cryolipolysis & Plasma-based | |

| Non-energy-based Devices | Botulinum Toxin |

| Dermal Fillers & Threads | |

| Chemical Peels | |

| Microdermabrasion | |

| Implants | |

| Mesotherapy & Others |

By Application

| Skin Resurfacing & Tightening |

| Body Contouring & Cellulite Reduction |

| Hair Removal |

| Tattoo & Pigmentation Removal |

| Breast Augmentation |

| Acne & Scar Treatment |

| Other Applications |

By End User

| Hospitals |

| Dermatology & Cosmetic Clinics |

| Medical Spas |

| Home-use Settings |

By Region

| Northeast |

| Midwest |

| South |

| West |

| By Device Type | Energy-based Devices | Laser-based |

| Light-based (IPL) | ||

| Radio-frequency-based | ||

| Ultrasound-based | ||

| Cryolipolysis & Plasma-based | ||

| Non-energy-based Devices | Botulinum Toxin | |

| Dermal Fillers & Threads | ||

| Chemical Peels | ||

| Microdermabrasion | ||

| Implants | ||

| Mesotherapy & Others | ||

| By Application | Skin Resurfacing & Tightening | |

| Body Contouring & Cellulite Reduction | ||

| Hair Removal | ||

| Tattoo & Pigmentation Removal | ||

| Breast Augmentation | ||

| Acne & Scar Treatment | ||

| Other Applications | ||

| By End User | Hospitals | |

| Dermatology & Cosmetic Clinics | ||

| Medical Spas | ||

| Home-use Settings | ||

| By Region | Northeast | |

| Midwest | ||

| South | ||

| West | ||

Key Questions Answered in the Report

What is the current value of the United States aesthetic devices market?

The market stands at USD 11.17 billion in 2026 and is forecast to climb to USD 16.65 billion by 2031.

Which application is expanding fastest?

Body contouring and cellulite reduction are projected to grow at a 9.74% CAGR through 2031, driven by rising post-weight-loss skin-tightening demand.

How significant are home-use aesthetic devices?

Home settings hold a small share today but are advancing at 8.95% CAGR as FDA guidance for over-the-counter devices matures.

Which device technology commands the largest share?

Energy-based platforms, spanning lasers and radio-frequency systems, account for 62.74% of national revenue.

How is private equity influencing competitive dynamics?

Fifty-five medical-aesthetic deals closed in 2023, creating capitalized chains that negotiate bulk equipment purchases and drive throughput.

What regulatory trend should manufacturers monitor?

Semiconductor supply-chain shocks and new state scope-of-practice bills will shape manufacturing lead times and provider usage rights over the next four years.

Page last updated on: