Guillain-Barre Syndrome Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.81 Billion |

| Market Size (2031) | USD 1.07 Billion |

| Growth Rate (2026 - 2031) | 5.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Guillain-Barre Syndrome Market Analysis by Mordor Intelligence

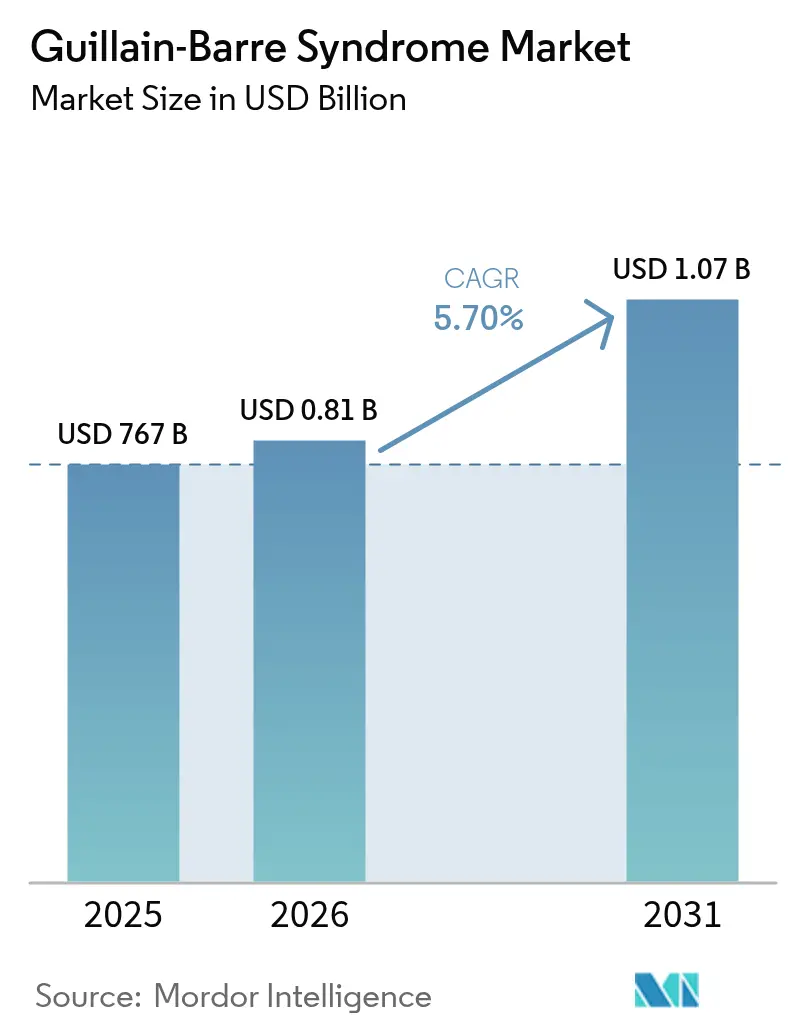

The Guillain-Barré Syndrome market size is expected to grow from USD 767 million in 2025 to USD 810.7 million in 2026 and is forecast to reach USD 1.07 billion by 2031 at 5.7% CAGR over 2026-2031. Demand is pivoting from traditional immunomodulators toward precision-targeted biologics, influenced by complement inhibitor breakthroughs, Medicare-backed home infusion coverage, and post-COVID neurological complications that have widened patient pools. IVIG still leads today, yet rising biologic adoption signals an inflection in clinical practice toward disease-specific inhibition strategies. Capacity expansions at fractionation plants, especially in Asia-Pacific, are easing supply bottlenecks while sharpening regional competition. Even so, Europe’s continued reliance on US plasma donors underscores structural fragility that may temper global growth despite rising clinical need.[1]Wiley Online Library, “Europe Needs 2 Million Extra Donors of Blood and Plasma: How to Find Them?,” Wiley Online Library, onlinelibrary.wiley.com

Key Report Takeaways

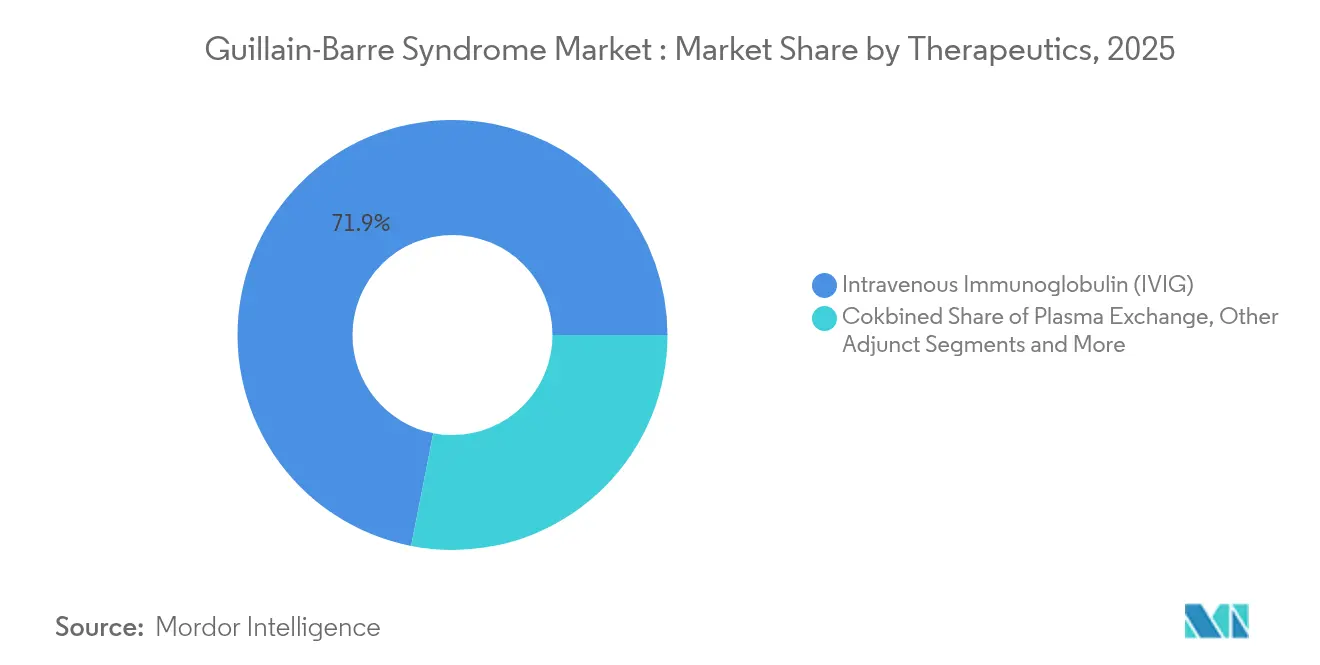

- By therapeutics, intravenous immunoglobulin retained 71.92% of Guillain-Barré Syndrome market share in 2025, whereas complement-inhibitors and novel biologics are tracking a 9.32% CAGR through 2031.

- By route of administration, the intravenous segment commanded 78.85% of the Guillain-Barré Syndrome market size in 2025, while subcutaneous delivery shows a 7.64% CAGR to 2031.

- By distribution channel, hospital pharmacies held 57.55% share of the Guillain-Barré Syndrome market in 2025; home infusion providers are expanding at a 9.18% CAGR.

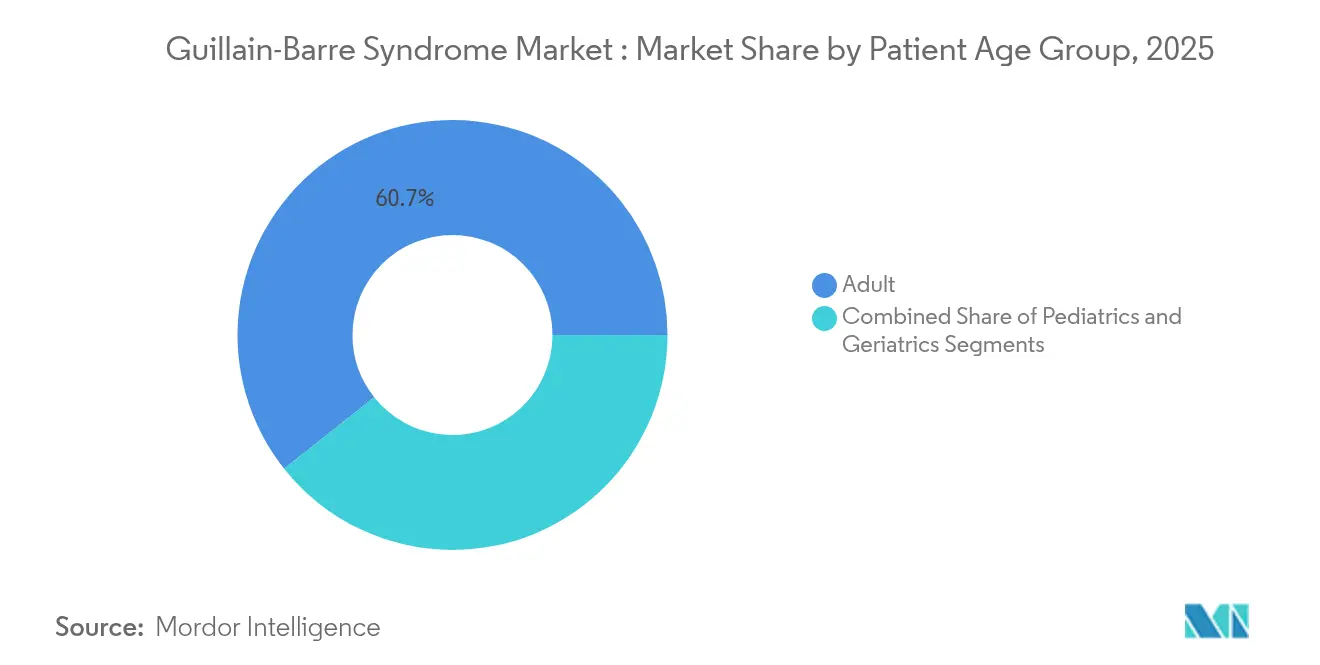

- By patient age, adults (18-64) accounted for 60.68% share of the Guillain-Barré Syndrome market size in 2025; the geriatric cohort (≥65) is rising at an 8.69% CAGR.

- By disease variant, AIDP held 66.05% share of the Guillain-Barré Syndrome market in 2025, whereas AMAN is the fastest-growing variant at an 8.58% CAGR.

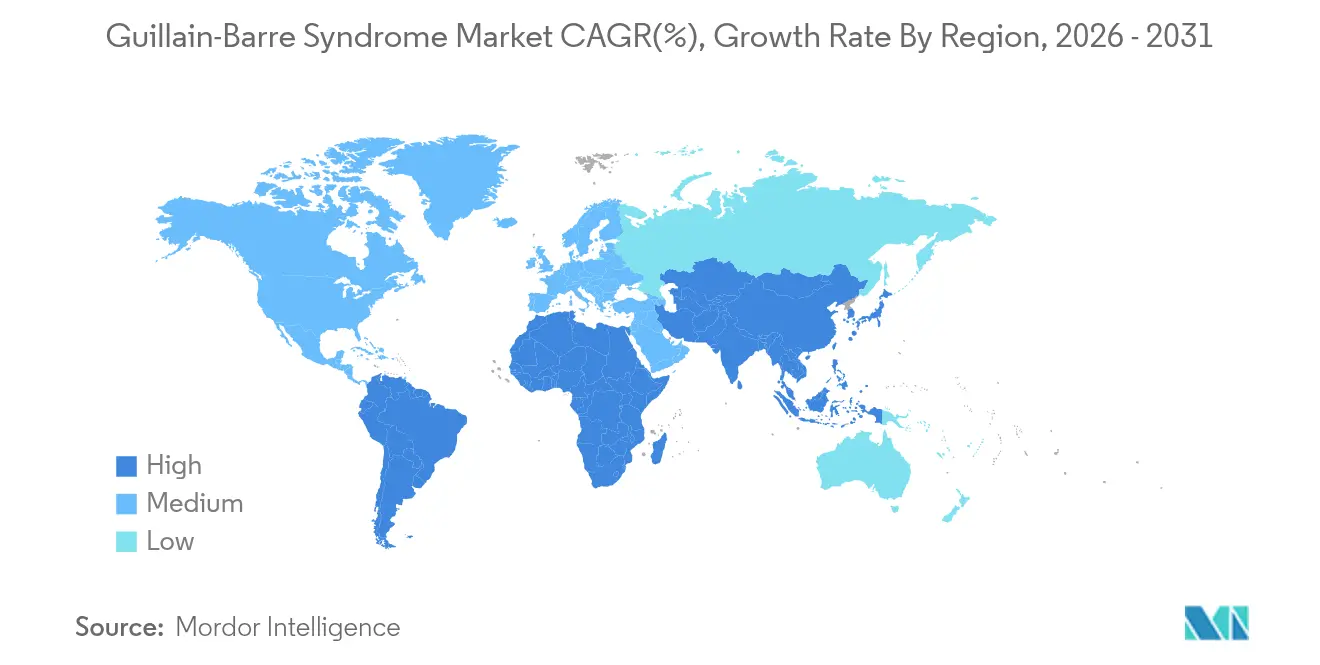

- By geography, North America represented 44.18% share of the Guillain-Barré Syndrome market in 2025, yet Asia-Pacific is projected to grow at an 8.45% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Guillain-Barre Syndrome Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Prevalence Of GBS & Ageing Population | 1.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Sustained Capacity Additions By Plasma-Fractionators Are Boosting IVIG Supply | 0.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Faster Regulatory Pathways Boosting Novel Biologics | 1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Growing IVIG/PLEX Capacity Expansions By Plasma-Fractionators | 0.7% | Global, with Asia-Pacific leading expansion | Medium term (2-4 years) |

| COVID-19–Linked Spike In Post-Infectious GBS Incidence | 0.9% | Global, higher in regions with low vaccination coverage | Short term (≤ 2 years) |

| Precision-Dosing Analytics Reducing Wastage & Enabling Payor Uptake | 0.6% | North America & EU, pilot programs in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence of GBS & Ageing Population

Global demographic shifts are reshaping the Guillain-Barré Syndrome market as geriatric patients (≥65 years) represent the fastest-growing group at 8.83% CAGR through 2030. NIH has earmarked USD 3 million to pinpoint genetic susceptibility markers that may refine personalized protocols.[2]National Institutes of Health, “RFA-NS-25-025: Exploratory/Developmental Research on Guillain-Barré Syndrome (GBS) and Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) (R21),” NIH, grants.nih.gov Years lived with disability for GBS almost doubled from 2020 to 2021, showing the pandemic’s amplifying effect on disease burden. WHO’s surveillance in Pune continues to confirm elevated case counts in low-to-middle-income regions, emphasizing the need for tailored immunotherapy pathways.

Sustained Capacity Additions by Plasma Fractionators Are Boosting IVIG Supply

Plasma fractionators are expanding to alleviate chronic IVIG shortages. CSL posted 15% immunoglobulin sales growth, reflecting robust uptake despite historical supply gaps. Indonesia’s 600,000-liter fractionation plant marks Southeast Asia’s largest build-out and trims regional dependence on imports. Kedrion’s FDA-cleared facility underscores quality gains that help stabilize therapeutic protein yields. Yet Europe’s need for 2 million more plasma donors shows that structural shortages persist.

Faster Regulatory Pathways Boosting Novel Biologics

The US FDA and EMA are streamlining review timelines for ultra-rare neurology drugs. Annexon’s ANX005 received both fast-track and orphan designations, lining it up for a 2025 BLA filing and potentially becoming the first GBS-specific biologic. EMA’s alignment on Vyvgart shows that transatlantic harmonization is shortening the classic 15-year discovery-to-launch cycle to nearer seven years.[3]European Medicines Agency, “Vyvgart, INN: efgartigimod alfa,” EMA, ema.europa.eu

Large-scale capacity investments such as Grifols’ Dublin site and Takeda’s indication broadening for GAMMAGARD LIQUID widen access and diversify revenue streams. Small-volume plasmapheresis protocols are also rising in resource-limited settings, demonstrating clinical equivalence to IVIG at lower cost.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic IVIG Shortages & High Therapy Cost | -1.8% | Global, most severe in Europe & emerging markets | Long term (≥ 4 years) |

| Adverse-Event & Thrombo-Embolism Concerns Limiting Repeat-Dose IVIG | -0.9% | Global, higher impact in elderly populations | Medium term (2-4 years) |

| Tighter Reimbursement Audits On Off-Label IVIG In LMICs | -0.7% | Low-to-middle income countries, Asia-Pacific & Africa | Medium term (2-4 years) |

| Evidence Of Higher Relapse Risk And Cost-Effectiveness Concerns For Plasma Exchange | -0.4% | Global, particularly in resource-limited settings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic IVIG Shortages & High Therapy Cost

A full IVIG course costs USD 5,000–10,000, imposing heavy budget pressure, especially when supply disruptions arise from quality-related lot withdrawals. Qatar’s 10-year audit logged USD 10 million spent on just 669 patients, highlighting economic burdens in emerging systems.

Adverse-Event & Thrombo-Embolism Concerns Limiting Repeat-Dose IVIG

Thromboembolic events and acute kidney injury—seen in up to 30% of high-dose users—require stricter monitoring, dissuading repeat courses in high-risk elders. These safety risks elevate interest in complement-targeting biologics that may deliver equal benefit with fewer systemic effects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutics: Novel Biologics Challenge IVIG Dominance

Intravenous immunoglobulin led the Guillain-Barré Syndrome market with a 71.92% share in 2025, yet complement-inhibitors and other novel biologics are growing at 9.32% CAGR through 2031. The Guillain-Barré Syndrome market size for these targeted biologics is projected to surpass USD 337.6 million by 2031 as positive Phase 3 data from ANX005 show 2.4-fold functional improvements over placebo. Efgartigimod has delivered compelling results in refractory AMAN cases, confirming the shift toward mechanism-specific intervention.

Traditional plasma exchange remains vital in cost-constrained settings, and its share of the Guillain-Barré Syndrome market is steady where donor plasma availability aligns with treatment protocols. Adjunct supportive care—such as physiotherapy and ventilatory support—continues to integrate with precision dosing analytics to ensure optimal biological exposure. Collectively, these trends illustrate how the Guillain-Barré Syndrome market is transitioning from broad immunomodulation to targeted pathway inhibition.

By Route of Administration: Subcutaneous Delivery Gains Momentum

The intravenous route accounted for 78.85% of the Guillain-Barré Syndrome market in 2025, supported by hospital infrastructure and clinician familiarity. Subcutaneous immunoglobulin, however, is the fastest-growing at 7.64% CAGR, propelled by biweekly dosing regimens under the expanded XEMBIFY label. Manual push Ig20Gly simplifies self-administration and reduces pump costs, broadening adoption among stable patients.

Home-based care is reshaping therapeutic logistics and driving payer alignment with value-based models. Precision dosing further supports subcutaneous uptake by minimizing wastage. The Guillain-Barré Syndrome market size for subcutaneous modalities is forecast to grow steadily as new formulations reach regulatory approval.

By Distribution Channel: Home Infusion Providers Accelerate Growth

Hospital pharmacies held 57.55% share of the Guillain-Barré Syndrome market in 2025 due to their central role in acute care. Home infusion services, however, are expanding at 9.18% CAGR, catalyzed by the CMS bundled payment that covers professional services, supplies, and equipment. Specialty and retail pharmacies provide medication management and patient education, acting as linchpins between hospital discharge and home-based treatment.

This distribution shift reflects the broader health-system move toward outpatient modalities that reduce nosocomial infection risk and improve patient convenience. As reimbursement stabilizes, the Guillain-Barré Syndrome market is likely to see an even larger share transitioning to home infusion.

By Patient Age Group: Geriatric Segment Drives Market Expansion

Adults aged 18-64 years captured 60.68% share of the Guillain-Barré Syndrome market in 2025. The geriatric cohort is advancing fastest at 8.69% CAGR, fueled by ageing populations and heightened vaccine-associated surveillance that flags higher susceptibility in older adults. Pediatric cases, though smaller, necessitate specialized protocols, with therapeutic plasma exchange offering viable outcomes in severe presentations.

Thromboembolic risk and slower functional recovery in seniors demand personalized regimens. Adaptive dosing analytics and subcutaneous delivery stand out as solutions to balance efficacy and safety in this demographic.

By Disease Variant: AIDP Dominance Faces AMAN Challenge

AIDP controlled 66.05% share of the Guillain-Barré Syndrome market in 2025, but AMAN is growing at 8.58% CAGR thanks to improved electrodiagnostic tools that refine subtype identification. Variant-specific responses to therapies such as complement inhibitors further support precision medicine direction.

Regional heterogeneity matters: AMAN is more prevalent in certain Asian countries, guiding local clinical pathways. Novel biologics like efgartigimod showcase effectiveness in refractory AMAN cases, potentially narrowing the recovery gap.

Geography Analysis

North America led the Guillain-Barré Syndrome market with a 44.18% share in 2025, supported by Medicare reimbursement for home infusion and ubiquitous access to precision analytics platforms. Granular electronic health records facilitate earlier diagnosis and outcome tracking, reinforcing payer confidence in high-cost biologics. Research consortia, such as those spearheaded by NIH, continue to draw funding into breakout discovery programs that amplify innovation spill-overs across the region.

Europe trails at second but confronts supply fragility, importing roughly 40% of its plasma-derived medicines from the United States. Regulatory agencies are encouraging domestic donor recruitment, yet demographic aging complicates collection targets. Despite advanced healthcare infrastructure, uncertain reimbursement for newer biologics could temper growth.

Asia-Pacific is the fastest-expanding at 8.45% CAGR, powered by large investments in local fractionation capacity such as Indonesia’s new 600,000-liter plant. Rising urbanization and improved surveillance reveal a larger underlying patient pool. China’s heterogeneous incidence profiles emphasize the need for regionally tailored product portfolios.

Latin America, the Middle East, and Africa follow with niche opportunities. Small-volume plasmapheresis protocols and mobile infusion units reduce infrastructure barriers, offering cost-effective alternatives in resource-limited settings. Collectively, these regions underscore the Guillain-Barré Syndrome market’s drive toward localized manufacturing and distribution resilience.

Competitive Landscape

The Guillain-Barré Syndrome market is moderately consolidated. CSL, Takeda, and Grifols anchor the IVIG domain using vertically integrated plasma networks. CSL’s 15% immunoglobulin revenue growth to USD 3.174 billion in H1 2025 evidences scale advantages that consolidate share. Takeda’s label expansion for GAMMAGARD LIQUID into CIDP highlights portfolio leveraging that extracts more value from existing plants.

Emerging players such as Annexon and Argenx are reshaping the competitive mix through targeted complement inhibition. Annexon’s ANX005 posted 2.4-fold disability-score improvements, positioning it to secure early-mover credibility in biologic therapy. These biotech entrants often turn to strategic alliances with fractionation firms to shore up distribution.

Technology differentiation guides competition. While plasma giants invest in donor-management software and fractionation automation, biologics developers channel resources into accelerated clinical programs and companion diagnostic tools. White-space remains in pediatric-friendly formulations and variant-specific protocols, inviting collaboration between established and emerging players.

Guillain-Barre Syndrome Industry Leaders

CSL Behring LLC

Takeda Pharmaceutical Company Limited

Grifols SA

Kedrion Biopharma Inc.

Octapharma AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Annexon presented Phase 3 tanruprubart data at the 2025 PNS Meeting, reinforcing rapid and durable GBS benefits.

- April 2025: Annexon showcased late-stage data for tanruprubart at the AAN Annual Meeting; a session replay is available to registrants.

- January 2025: FDA required a Guillain-Barré Syndrome warning in RSV vaccine prescribing information for Abrysvo and Arexvy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Guillain-Barré syndrome therapeutics market as all prescription medicines and plasma-based interventions employed to reverse or limit acute immune-mediated neuropathies classified under GBS, primarily intravenous immunoglobulin and plasma exchange, delivered through hospital or home-infusion settings worldwide.

Scope Exclusion: Screening diagnostics, physiotherapy services, and over-the-counter analgesics are outside our remit.

Segmentation Overview

- By Therapeutics

- Intravenous Immunoglobulin (IVIG)

- Plasma Exchange (PLEX)

- Complement-inhibitors & Novel Biologics

- Other Adjunct / Supportive Care

- By Route of Administration

- Intravenous

- Sub-cutaneous

- Oral / Enteral

- By Distribution Channel

- Hospital Pharmacies

- Specialty & Retail Pharmacies

- Home-Infusion Providers

- By Patient Age Group

- Pediatric (<18 yrs)

- Adult (18 – 64 yrs)

- Geriatric (≥65 yrs)

- By Disease Variant

- AIDP (Acute Inflammatory Demyelinating)

- AMAN (Acute Motor Axonal)

- AMSAN (Acute Motor-Sensory Axonal)

- Miller-Fisher Syndrome

- Other rare variants (PCB, PNC, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We validated key assumptions through interviews and short surveys with neurologists, transfusion-medicine specialists, hospital pharmacy chiefs, and patient-advocacy leaders across North America, Europe, Asia-Pacific, and the Middle East, obtaining real-world dose patterns, length-of-stay norms, and imminent formulary shifts.

Desk Research

Mordor analysts grounded the model in incidence statistics from the World Health Organization, the US Centers for Disease Control and Prevention, and Eurostat hospital discharge records, which map post-infection case spikes. Treatment cost curves came from national reimbursement catalogs and longitudinal trials in Lancet Neurology and the New England Journal of Medicine. Company revenue splits were reviewed on D&B Hoovers, and regulatory milestones were tracked through FDA and EMA portals, with news flow monitored via Dow Jones Factiva. The sources cited here are illustrative; many additional publications informed data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down incidence-to-therapy uptake model converts country GBS cases into treated patient pools, followed by average selling price per gram of IVIG and typical plasma-exchange cycles, which are then cross-checked with supplier shipment indications and sampled hospital purchasing data. Inputs include annual incidence per 100,000 population, share of severe cases needing pharmacologic intervention, gram-per-patient dosage, ASP progression, pipeline launch timelines for complement inhibitors, and exchange-rate trends. Multivariate regression that blends population aging, infection-outbreak indices, and payer reimbursement elasticity drives our 2025-2030 forecasts, while scenario analysis tests faster biologic adoption. Gaps in bottom-up roll-ups are bridged with midpoint estimates corroborated by primary sources.

Data Validation & Update Cycle

Outputs pass three-layer variance screening, peer review, and senior-analyst sign-off. We refresh the model every year, and we trigger mid-cycle revisions when label expansions or material price shifts occur. A final sweep is completed just before publication so clients receive the most current view.

Why Mordor's Guillain-Barre Syndrome Baseline Earns Trust

Published estimates often diverge because firms select unlike geographies, mingle diagnostics, or freeze price decks for several years. According to Mordor Intelligence, our disciplined scope, variable selection, and annual refresh narrow such gaps.

These contrasts show that our model, built on live incidence data, validated dosage economics, and continual updates, gives decision-makers a balanced, transparent baseline they can rely on.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 767 (USD mn) | Base Year: 2025 | Mordor Intelligence | |

| 773 (USD mn) | Base Year: 2025 | Regional Consultancy A | Focus on five high-income nations only |

| 724 (USD mn) | Base Year: 2024 | Trade Journal B | Combines diagnostics revenue, omits pipeline impact |

| 645 (USD mn) | Base Year: 2023 | Global Consultancy C | Older base year and pre-COVID incidence profile |

These contrasts show that our model, built on live incidence data, validated dosage economics, and continual updates, gives decision-makers a balanced, transparent baseline they can rely on.

Key Questions Answered in the Report

What is driving growth in the Guillain-Barré Syndrome market?

Demand is rising due to ageing populations, post-COVID neurological complications, and faster biologic approvals that introduce new targeted therapies.

How big is the Guillain-Barré Syndrome market today?

The Guillain-Barré Syndrome market is valued at USD 810.7 million in 2026 and is forecast to reach USD 1.07 billion by 2031 at a 5.7% CAGR.

Why are complement inhibitors gaining attention?

Phase 3 data show complement inhibitors like tanruprubart improve disability scores more than IVIG, positioning them as potential first-line options once approved.

Which route of administration is expanding fastest?

Subcutaneous immunoglobulin is growing at 7.64% CAGR as home infusion and patient autonomy gain traction.

How are supply shortages being addressed?

Capacity expansions in Asia-Pacific and strategic donor recruitment in Europe aim to reduce dependence on US plasma and stabilize IVIG availability.

What risk does the market face from safety concerns?

Thromboembolic and renal events linked to high-dose IVIG prompt tighter monitoring, potentially shifting usage toward safer targeted biologics in susceptible groups.

Page last updated on: