Acromegaly Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.63 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

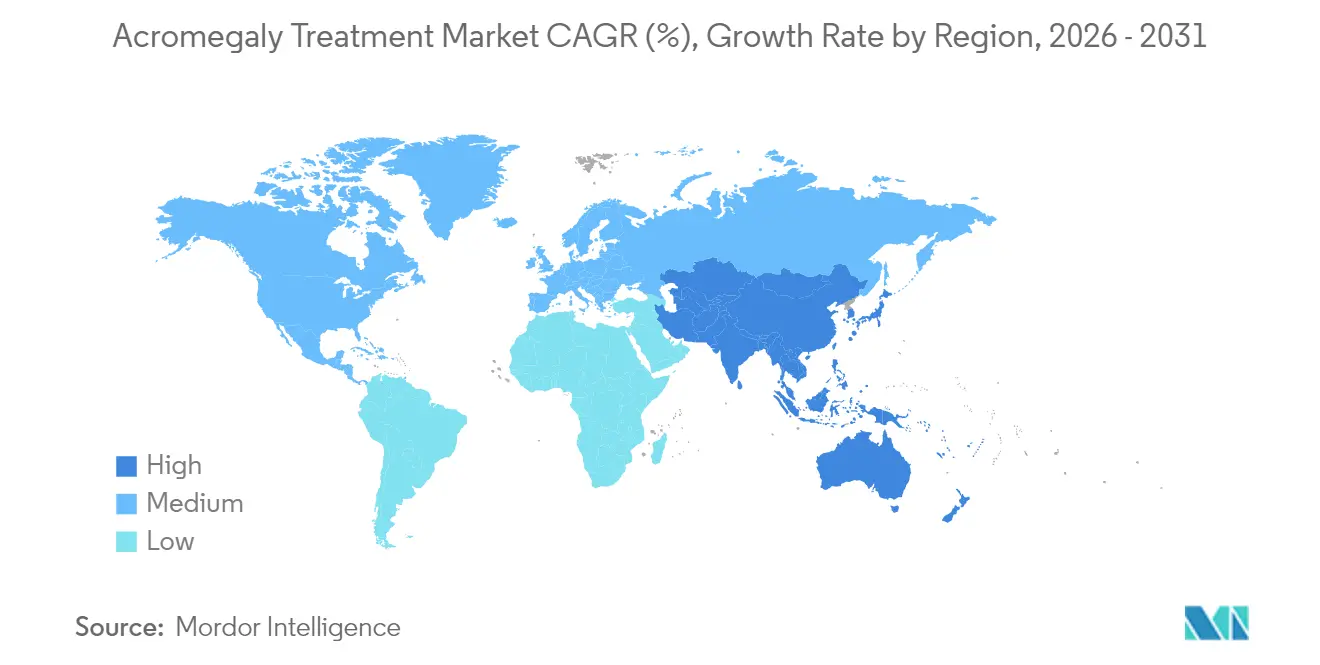

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

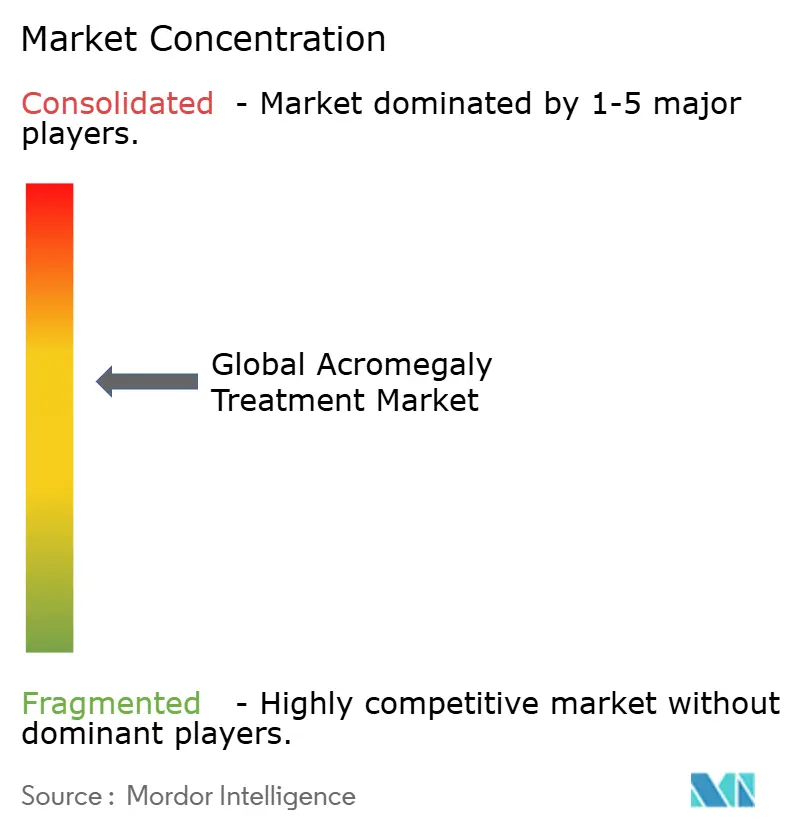

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acromegaly Treatment Market Analysis by Mordor Intelligence

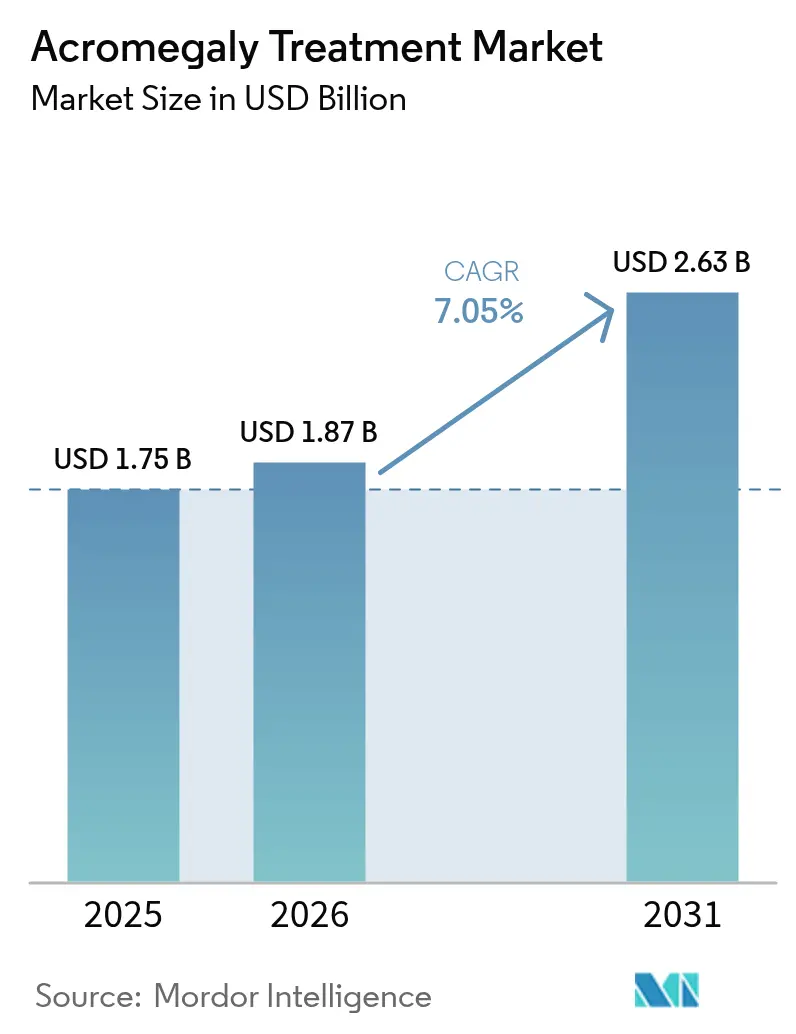

Acromegaly treatment market size in 2026 is estimated at USD 1.87 billion, growing from 2025 value of USD 1.75 billion with 2031 projections showing USD 2.63 billion, growing at 7.05% CAGR over 2026-2031. Growth is fueled by a rising pool of diagnosed patients, earlier detection protocols, and the steady launch of patient-friendly long-acting formulations. Industry participants are allocating larger budgets to clinical programs that improve biochemical control rates and reduce dosing frequency, while payers are experimenting with outcomes-based agreements to offset therapy costs. Digital dispensing channels, especially online pharmacies, are scaling quickly as oral options reach the market, and specialized surgical centers are reinforcing demand for adjuvant pharmacological care. Competitive momentum is intensifying as emerging biotechs challenge established players with differentiated delivery platforms, setting the stage for a pipeline-driven shift in market leadership.

Key Report Takeaways

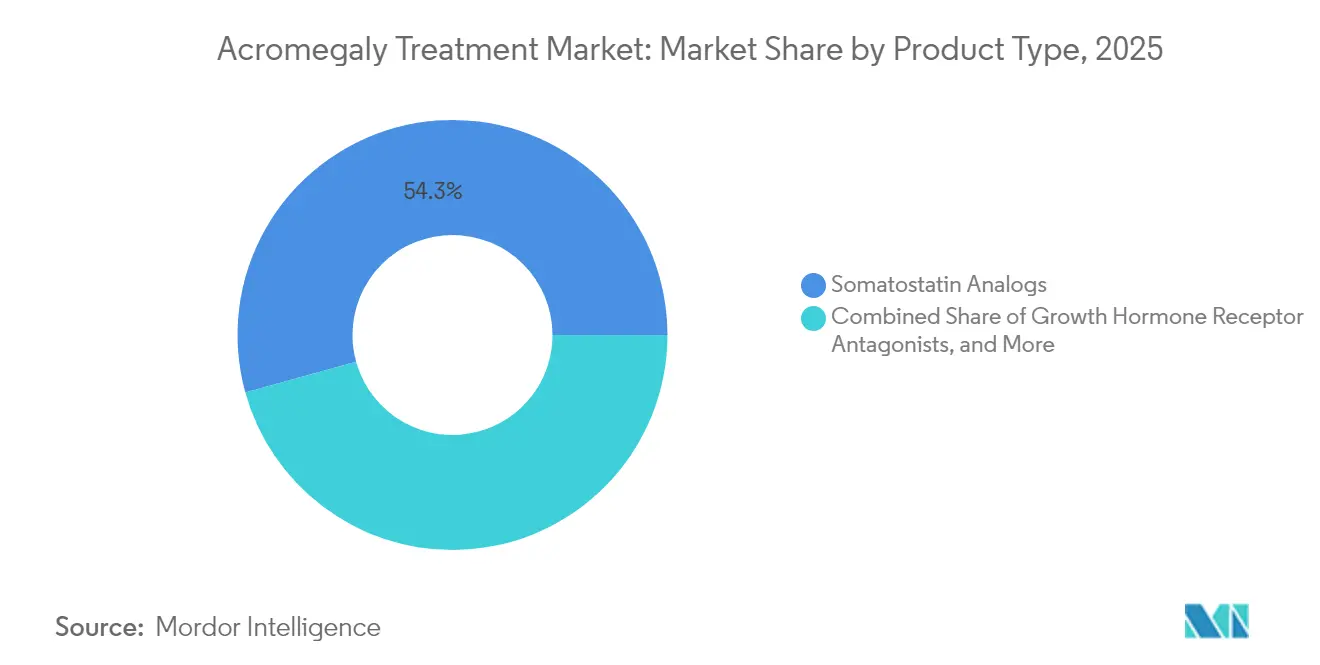

- By product type, somatostatin analogs led with 54.30% of the acromegaly treatment market share in 2025, while growth hormone receptor antagonists are projected to expand at a 9.15% CAGR to 2031.

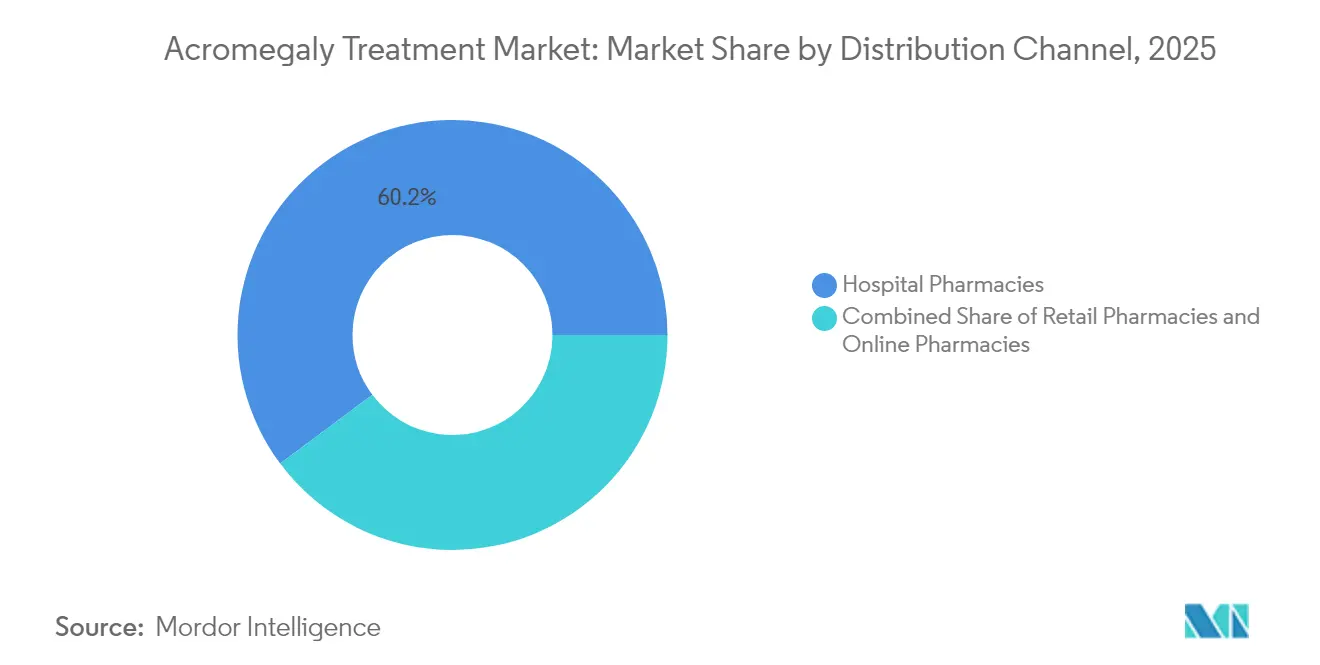

- By distribution channel, hospital pharmacies accounted for 60.20% share of the acromegaly treatment market size in 2025; online pharmacies are advancing at a 13.10% CAGR through 2031.

- By geography, North America held 42.60% of the acromegaly treatment market share in 2025; Asia Pacific is forecast to grow at an 7.95% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acromegaly Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of GH-secreting pituitary adenomas | +2.2% | Global, higher in Europe and North America | Long term (≥ 4 years) |

| Earlier diagnosis under updated Endocrine Society guidelines | +1.9% | North America & Europe, expanding in Asia Pacific | Medium term (2-4 years) |

| Transition toward long-acting depot formulations | +1.5% | Europe with spill-over to North America and Asia Pacific | Medium term (2-4 years) |

| Orphan-drug incentives accelerating R&D funding | +1.1% | Global, strongest in US and EU | Long term (≥ 4 years) |

| Growing adoption of MRI-guided trans-sphenoidal surgery creating adjuvant demand | +0.9% | North America, Europe, advanced systems in Asia | Medium term (2-4 years) |

| Expansion of national rare-disease reimbursement lists | +0.6% | China, Brazil, GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Growth Hormone–Secreting Pituitary Adenomas

The global incidence of acromegaly now approaches 0.38 per 100,000 person-years, and prevalence has reached 5.9 per 100,000 population[1]Mi Kyung Kim, “Insulin-Like Growth Factor 1 as a Pillar in Acromegaly: From Diagnosis to Long-Term Management,” Endocrinology and Metabolism, doi.org. High-resolution MRI and sensitive IGF-1 assays shorten diagnostic delays and uncover latent cases, especially among middle-aged adults. A European registry tracking 3,173 patients reported a median diagnostic age of 43.5 years for men and 46.4 years for women, with noted delays in female cohorts[2]Patrick Petrossians, “Acromegaly at Diagnosis in 3173 Patients from the Liège Acromegaly Survey Database,” Endocrine-Related Cancer, erc.bioscientifica.com. As the recognized patient base expands, manufacturers are scaling production capacity and broadening compassionate-use programs, while insurers model higher long-term spending on endocrine disorders.

Earlier Diagnosis from Endocrine Society Guideline Uptake

The 14th Acromegaly Consensus shifted the confirmatory threshold to IGF-1 levels 1.3 times above the upper normal limit, removing the need for routine GH suppression tests. Specialized centers now report a compressed diagnostic lag of 5-7 years versus the previous 10-12-year average. Earlier intervention expands the acromegaly treatment market by adding patients who previously progressed to advanced disease states. Laboratories offering same-day IGF-1 testing see double-digit revenue gains, and multidisciplinary clinics integrate sleep-apnea and diabetes screenings to flag high-risk individuals sooner.

Transition Toward Long-Acting Depot Formulations in Europe

European endocrinologists increasingly prescribe monthly depot injections that can be self-administered at home. In Phase 3 data, CAM2029 achieved biochemical control in 77.2% of participants compared with 37.5% on placebo. Patient preference surveys show 88.9% favor long-acting options for convenience and fewer injection-site reactions. Regulatory momentum continues; the European Medicines Agency issued a positive opinion for Oczyesa (octreotide) in April 2025. These developments are prompting hospital formularies to reorder stock toward depot versions, boosting recurring revenues for device-integrated delivery systems.

Orphan-Drug Incentives Accelerating R&D Funding

Seven investigational agents now hold orphan designation in either the US or EU, unlocking fee waivers, tax credits, and 10-year exclusivity in Europe. Paltusotine secured EU orphan status in March 2025, positioning Crinetics for an expedited review[3]European Medicines Agency, “CHMP Meeting Highlights April 2025,” ema.europa.eu. The National Institutes of Health earmarked USD 1.0 million in 2024 for a first-in-class antibody program directed at excess growth hormone activity. These incentives lower development risk, attract venture capital, and broaden the competitive field, reinforcing innovation cycles that keep the acromegaly treatment market on a high-growth trajectory.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-injection fibrosis and lipoatrophy limiting depot compliance | −1.5% | Global, higher where follow-up care is limited | Medium term (2-4 years) |

| Pegvisomant-induced liver enzyme elevations necessitating monitoring | −1.1% | Global, pronounced in low-resource diagnostics | Short term (≤ 2 years) |

| Limited specialist centers in low-income Africa & Caribbean nations | −0.8% | Africa, Caribbean, other low-income regions | Long term (≥ 4 years) |

| High annual therapy cost (> USD 250 K) constraining payer budgets | −1.3% | Global, highest impact where universal coverage is absent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Injection Fibrosis & Lipoatrophy Limiting Depot Compliance

Long-term use of injectable somatostatin analogs leads to injection-site reactions in up to 20% of patients, with 5-8% developing significant fibrosis or lipoatrophy that forces regimen changes. Oral octreotide capsules deliver a 65% biochemical response without these complications but introduce challenges such as variable absorption and the need for twice-daily dosing. Clinicians now rotate injection sites more aggressively and consider early oral switchovers for high-risk profiles, yet real-world adherence data indicate continued attrition that erodes potential acromegaly treatment market size gains.

Pegvisomant-Induced Liver Enzyme Elevations Necessitating Monitoring

French ACROSTUDY data covering 312 patients over 6.3 years confirmed that pegvisomant normalizes IGF-1 in 64.4% of recipients but requires regular hepatic monitoring due to elevated transaminases. Annual monitoring adds USD 1,200-1,800 to treatment costs, intensifying payer scrutiny in value-based contracts. Combination regimens with somatostatin analogs raise hepatotoxicity risk to 11-15% of patients, prompting development of next-generation antagonists such as AZP-3813, which aims for lower liver liability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Somatostatin Analogs Maintain Dominance

Somatostatin analogs accounted for 54.30% of acromegaly treatment market share in 2025, anchored by Somatuline (lanreotide) revenue of USD 1,121.3 million. The segment benefits from broad guideline endorsements as first-line medical therapy and from depot innovations that enhance patient convenience. Growth hormone receptor antagonists held a smaller slice of the acromegaly treatment market size but are set to grow at 9.15% CAGR through 2031 as pegvisomant and pipeline entrants demonstrate high biochemical normalization rates. Oral nonpeptide agents such as paltusotine showed 83% IGF-1 control in PATHFNDR-1, signaling future shifts in prescribing patterns toward once-daily oral therapy.

Pipeline activity is reshaping competitive dynamics. CAM2029 offers once-monthly subcutaneous delivery with patient-enabled autoinjectors, improving adherence and reducing clinic visits. Developers are also exploring antisense RNA and GHRH receptor blockade to penetrate refractory disease niches. As these modalities reach late-stage trials, the acromegaly treatment industry may witness a redistribution of revenue streams, with oral and self-administered products capturing share from hospital-administered injectables.

By Distribution Channel: Hospital Pharmacies Lead, Online Segment Surges

Hospital pharmacies controlled 60.20% of the acromegaly treatment market in 2025 because complex injectables are typically initiated under specialist supervision. This channel benefits from integrated care pathways, bundled service billing, and close monitoring capabilities. The acromegaly treatment market size for hospital pharmacies will hold steady as new long-acting depots still require specialist oversight on initiation, dose titration, and MRI follow-up.

Online pharmacies represent the fastest-growing channel at a 13.10% CAGR, propelled by the commercialization of oral agents that bypass cold-chain handling. Wider telemedicine adoption removed geographic barriers for follow-up consultations, allowing accredited e-pharmacies to deliver costly endocrinology drugs directly to patients. Regulations such as the Prescription Drug Price Transparency Act highlight wide price spreads; in Minnesota alone, high drug prices affected 75,000 residents and added USD 53.2 million to state spending in 2022. Transparent pricing paired with direct-to-patient distribution positions the online segment to capture incremental acromegaly treatment market share over the next five years.

Geography Analysis

North America remains the anchor for the acromegaly treatment market, holding 42.60% share in 2025. Approximately 27,000 diagnosed patients reside in the United States, with 11,000 receiving pharmacologic intervention. The Inflation Reduction Act introduced a USD 2,000 cap on Medicare Part D out-of-pocket drug costs, improving adherence prospects for seniors. Academic centers in Boston, Houston, and Los Angeles are early adopters of oral somatostatin receptor agonists, accelerating physician experience curves and influencing guideline updates across the region.

Europe ranks second by revenue, driven by widespread use of long-acting depots and robust specialist networks. Surveyed Pituitary Tumor Centers of Excellence reported that 48.9% of patients are on medical therapy, with first-generation somatostatin receptor ligands as the preferred option for nearly half the cohort. Health technology assessment bodies such as NICE and IQWiG scrutinize incremental clinical value, leading to active price negotiations but also fostering uptake of cost-effective depot innovations. EMA approval cycles remain predictable, supporting steady expansion of the acromegaly treatment market size in large economies such as Germany, France, and Italy.

The Asia Pacific acromegaly treatment market is projected to grow at an 7.95% CAGR through 2031. China, Japan, and South Korea account for the bulk of regional volume, thanks to rising specialist density and expanded private insurance coverage. Thailand’s rare-disease audit showed only 46.8% of recommended medicines registered and just 22.93% listed as essential, underscoring lingering access gaps. India’s USD 574.5 million Production Linked Incentive scheme aims to localize manufacturing for complex injectables, which could cut costs and widen availability. As regional governments roll out universal health programs, demand for affordable depot and oral therapies will lift the overall acromegaly treatment market.

Regulatory Landscape

In the United States, the FDA approved PALSONIFY (paltusotine) in September 2025 as a once-daily oral option for adults with acromegaly, broadening the regulatory benchmark beyond injectable somatostatin analogs and reinforcing the role of post-approval safety monitoring and outcomes tracking for high-cost chronic therapies. In Europe, the European Commission approved PALSONIFY in April 2026 across the EU and EEA markets referenced in the authorization. Japan is also active on the regulatory front, with Sanwa Kagaku Kenkyusho submitting a Japan NDA in April 2026 for paltusotine for acromegaly and pituitary gigantism, signaling continued multi-region filings for pipeline-to-commercial transitions.

Competitive Landscape

Market concentration is moderate. Ipsen maintains leadership with Somatuline, representing roughly one-third of corporate revenue, while Novartis and Pfizer retain sizeable but stable positions through portfolio breadth. Recordati bolstered its presence by acquiring niche endocrine assets that complement its rare-disease focus. New entrants emphasize differentiated delivery; CAM2029 promises at-home monthly dosing, and paltusotine seeks to eliminate injections altogether. AZP-3813 from Amolyt Pharma targets improved hepatic safety to address pegvisomant drawbacks.

Strategic alliances and licensing deals accelerate technology transfer. Ipsen partners with device firms to co-develop pre-filled syringes that cut nurse administration time. Crinetics collaborates with contract manufacturers in Singapore to secure supply ahead of expected 2025 approval. Patent filings for octreotide nano-depot systems and oral receptor agonists surged 18% year-on-year, concentrated in the US and Europe but rising in Korea and China. Digital therapeutics add another competitive dimension; remote IGF-1 monitoring apps paired with smart injectors are in pilot studies at US academic centers.

White-space opportunities revolve around treatment-resistant disease that affects up to 40% of patients on first-generation analogs. Combination regimens integrating pegvisomant with somatostatin analogs report 90% biochemical control but remain cost-intensive and monitor-heavy. Companies that align value-based pricing with real-world evidence could break through payer resistance and expand reach within the acromegaly treatment market.

Acromegaly Treatment Industry Leaders

Novartis AG

Ipsen SA

Pfizer Inc.

Recordati S.p.A.

Amryt Pharma plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The commercialization of once-daily oral SSTR2 therapy has created whitespace to shift treated patients away from long-term injectable burden and to expand persistence in maintenance care. FDA approval of PALSONIFY (paltusotine) in September 2025 for first-line treatment, followed by European Commission approval in April 2026, provides a direct platform for broader payer and provider adoption of oral regimens in a market still dominated by depot somatostatin analogs. A second opportunity sits in patient-convenient depot innovation that reduces administration complexity while preserving somatostatin analog familiarity in clinical practice. EU marketing authorization for Camurus Oczyesa (octreotide subcutaneous depot) for maintenance treatment validates a pathway for ready-to-use, patient-friendly formulations that can lessen clinic resource intensity for stable patients, while keeping specialist oversight for titration and monitoring. Together, these approvals support portfolio strategies that combine oral initiation or switch options with maintenance-focused depots, and they strengthen the business case for services that improve biochemical control and adherence, such as structured IGF-1 monitoring and specialist-led care pathways.

Recent Industry Developments

- June 2026: Crinetics presented long-term data at ENDO 2026 from PATHFNDR-1 and PATHFNDR-2 open-label extensions showing durable and consistent acromegaly control with PALSONIFY (paltusotine). The update reinforces physician confidence in sustained biochemical management and supports lifecycle evidence needs as oral therapy competes against established injectable regimens.

- April 2026: European Commission approved PALSONIFY across the EU and EEA markets, expanding access and aligning payer coverage for once-daily oral therapy in eligible adults with acromegaly.

- April 2026: Sanwa Kagaku Kenkyusho submitted a Japan NDA for paltusotine for acromegaly and pituitary gigantism, signaling continued multi-region filings for pipeline-to-commercial transitions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues from prescription medicines used to treat acromegaly by controlling excess growth hormone effects and helping normalize IGF-1 levels in diagnosed patients. Value is tracked as drug sales across standard dispensing channels, then summed across the covered geographies.

Scope exclusions: We exclude surgical procedures, radiotherapy services, and diagnostic testing or imaging equipment used during diagnosis and follow-up.

Segmentation Overview

- By Product Type

- Somatostatin Analogs

- Growth Hormone Receptor Antagonists

- Dopamine Agonists

- Other Product Types

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research builds the foundation on how many patients exist, how many get treated, and what changes demand over time. We mainly use public health and regulator sources such as NIH and NORD disease information, FDA and EMA approval and label updates, CDC and OECD health statistics, and World Bank macro indicators that help explain access and affordability.

To ground pricing and utilization assumptions, we also review sources such as national health service reimbursement notes where available, published guidelines and peer-reviewed endocrinology journals, and company filings and investor presentations for therapy focus and commercial footprint. A paid subscription for company financials and news is used selectively to confirm timelines and large portfolio shifts, and a patent database is checked when it clarifies launch risk and exclusivity windows. These desk sources are illustrative rather than exhaustive, and we reviewed many other public references for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys are used to test model assumptions that desk research does not answer clearly, especially treated rates, switching behavior, and real-world persistence on therapy. We speak with endocrinologists, hospital pharmacists, payers, and distribution-side experts across APAC, EMEA, and the Americas, so regional access and reimbursement differences are reflected in the final estimates.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 43% |

| Mid tier: 50% | Functional/Unit leaders: 43% | EMEA: 31% |

| Smaller Players: 17% | Managers: 44% | Americas: 26% |

Market-Sizing & Forecasting

Sizing uses a prevalence-to-treated-cohort approach, where the diagnosed population, treatment eligibility, and therapy uptake are translated into an addressable demand pool and then into revenues. The top-down structure is supported with selective bottom-up checks, such as sampled price per unit multiplied by expected patient volume by therapy class, then followed by channel checks to ensure totals stay realistic.

Key model inputs include diagnosed prevalence trends, treatment initiation rates after diagnosis, persistence and adherence patterns for long-acting injectables, share shifts between drug classes, and expected price changes driven by new launches and generic timing. Where data is thin for smaller countries, we bridge gaps using proxy indicators like specialist density and reimbursement accessibility, then adjust using expert feedback so the output remains plausible.

For forecasting, we use scenario analysis to reflect different adoption speeds for newer therapies and different levels of access expansion. Assumptions are kept consistent year to year, and they are updated when expert views and public signals (regulatory events and reimbursement changes) indicate a sustained shift.

Data Validation & Update Cycle

Validation happens in layers so results are not driven by a single assumption. We compare outputs against independent signals such as therapy class mix, country-level access patterns, and directionally expected spending per treated patient, then investigate variances before sign-off.

When unusual changes appear, analysts revisit pricing, treated rates, and mix assumptions and, if needed, re-contact relevant experts for confirmation. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery check is completed so the published view reflects the latest available data.

Mordor Intelligence's Acromegaly Treatment Market Size Compared With Other Published Estimates

Published market values for acromegaly treatment can vary even when they appear to cover the same topic, because the underlying year, currency conversion timing, and how therapy pricing is normalized are often not aligned. Differences also show up when one study counts a broader set of care components, or when treatment coverage assumptions are not rechecked after a major policy or launch event.

In refresh-led work, the spread usually comes from whether list prices are used versus net realized pricing assumptions, how quickly generic or new therapy effects are reflected in ASP progression, and whether treated patient pools are updated for diagnosis and persistence changes. The estimate below is kept stable by revalidating key inputs on a set cadence and locking currency timing for each year, which is a step applied in Mordor Intelligence to reduce drift across update cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.87 B (2026) | |

| Global Consultancy A | USD 1.64 B (2024) | Uses a 2024 base year and a different forecast window, and the pricing basis appears closer to list price reporting, which can understate net price adjustments and delay mix-driven ASP resets. |

| Industry Publisher B | USD 1.50 B (2024) | Reports a lower 2024 value that likely reflects narrower treated-pool assumptions and earlier currency timing, and it may not fully carry forward persistence and adherence updates into the revenue build. |

The comparison mainly shows that year selection and refresh discipline matter as much as the therapy scope itself. When the treated cohort, ASP logic, and currency timing are kept consistent and rechecked after key events, the final number becomes easier to trace, repeat, and explain to decision-makers.

Key Questions Answered in the Report

What is the current size of the acromegaly treatment market?

The acromegaly treatment market is valued at USD 1.87 billion in 2026 and is projected to reach USD 2.63 billion by 2031.

Which therapy class dominates the market today?

Somatostatin analogs account for 54.30% of market share, reflecting their guideline-endorsed first-line status and strong sales of agents like lanreotide.

Why are online pharmacies gaining traction in this market?

Oral products such as octreotide capsules enable direct-to-patient shipping, and broader telehealth adoption supports remote prescription fulfillment, resulting in a 13.10% CAGR for online channels.

How are pricing pressures being addressed?

Payers favor outcomes-based contracts, and legislative actions like the Medicare Part D out-of-pocket cap aim to enhance affordability without stifling innovation.

Which pipeline product could disrupt current treatment patterns?

Paltusotine, an oral selective somatostatin receptor type 2 agonist, reported 83% IGF-1 normalization in late-stage trials and holds EU orphan designation, positioning it for potential market disruption in 2025.

Page last updated on: