Guatemala Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.40 Billion |

| Market Size (2026) | USD 3.7 Billion |

| Market Size (2031) | USD 5.64 Billion |

| Growth Rate (2026 - 2031) | 8.79% CAGR |

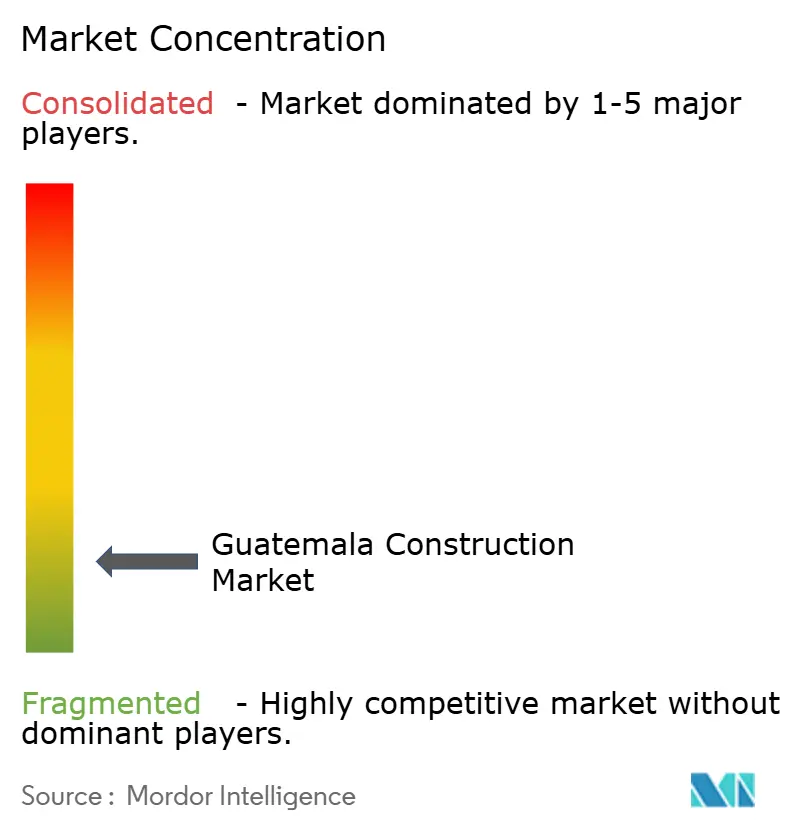

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Guatemala Construction Market Analysis by Mordor Intelligence

The Guatemala Construction market size is expected to grow from USD 3.40 billion in 2025 to USD 3.70 billion in 2026 and is forecast to reach USD 5.64 billion by 2031 at 8.79% CAGR over 2026-2031. Robust public investment in social housing, rejuvenated infrastructure spending, and rising foreign direct investment in nearshoring–oriented facilities are propelling this expansion. Demand is concentrated in urban centers, especially Guatemala City, where vertical residential formats and commercial complexes dominate new project pipelines. Escuintla’s industrial parks and logistics corridors are underpinning momentum outside the capital, while renewable‐energy projects add a steady pipeline of utility work. Despite persistent headwinds from political risk and skilled-labor shortages, the Guatemala construction market is benefiting from private capital’s growing appetite for industrial, energy, and mixed-use developments, signaling a gradual improvement in investor sentiment.

Key Report Takeaways

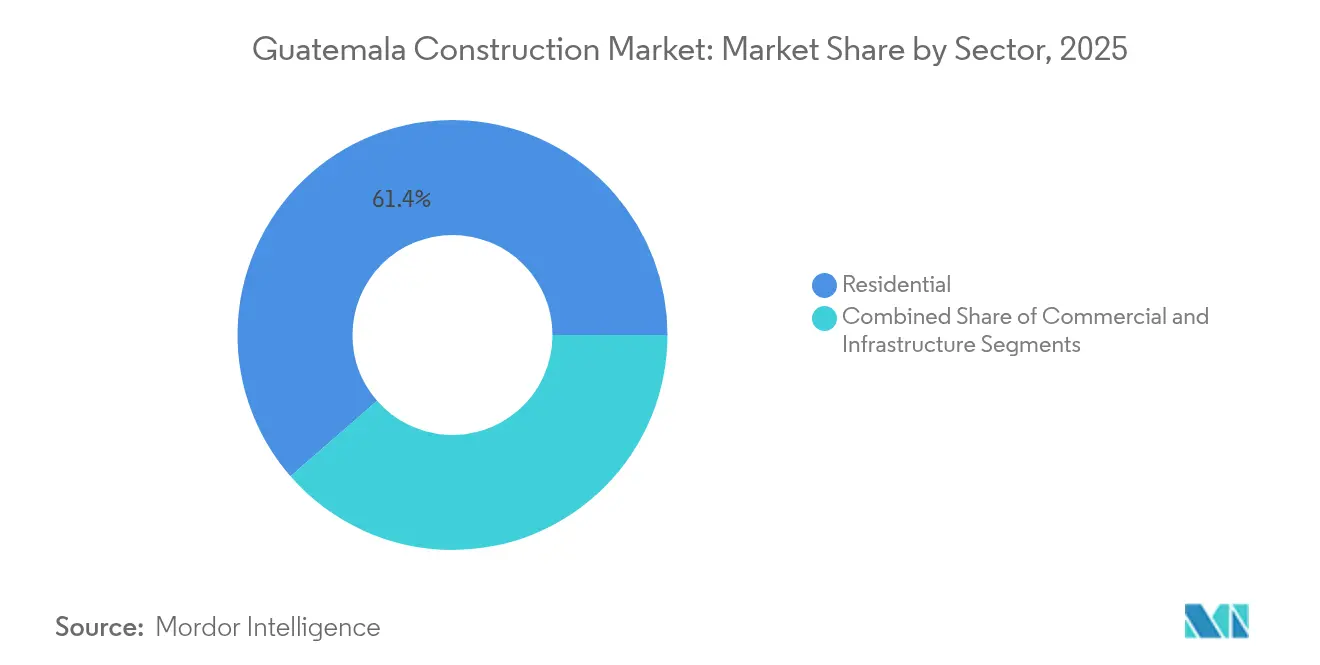

- By sector, Residential segment captured 61.42% of the Guatemala construction market share in 2025. Guatemala construction market size for the infrastructure segment is projected to grow at a 10.26% CAGR between 2026-2031.

- By construction type, New construction captured 57.35% of the Guatemala construction market share in 2025. Guatemala construction market size for new construction is projected to grow at a 9.96% CAGR between 2026-2031.

- By investment source, Public funding captured 64.35% of the Guatemala construction market share in 2025. Guatemala construction market size for private investment is projected to grow at a 10.18% CAGR between 2026-2031.

- By region, Guatemala City captured 45.55% of the Guatemala construction market share in 2025. Guatemala construction market size for the Escuintla Region is projected to grow at a 10.34% CAGR between 2026-2031.

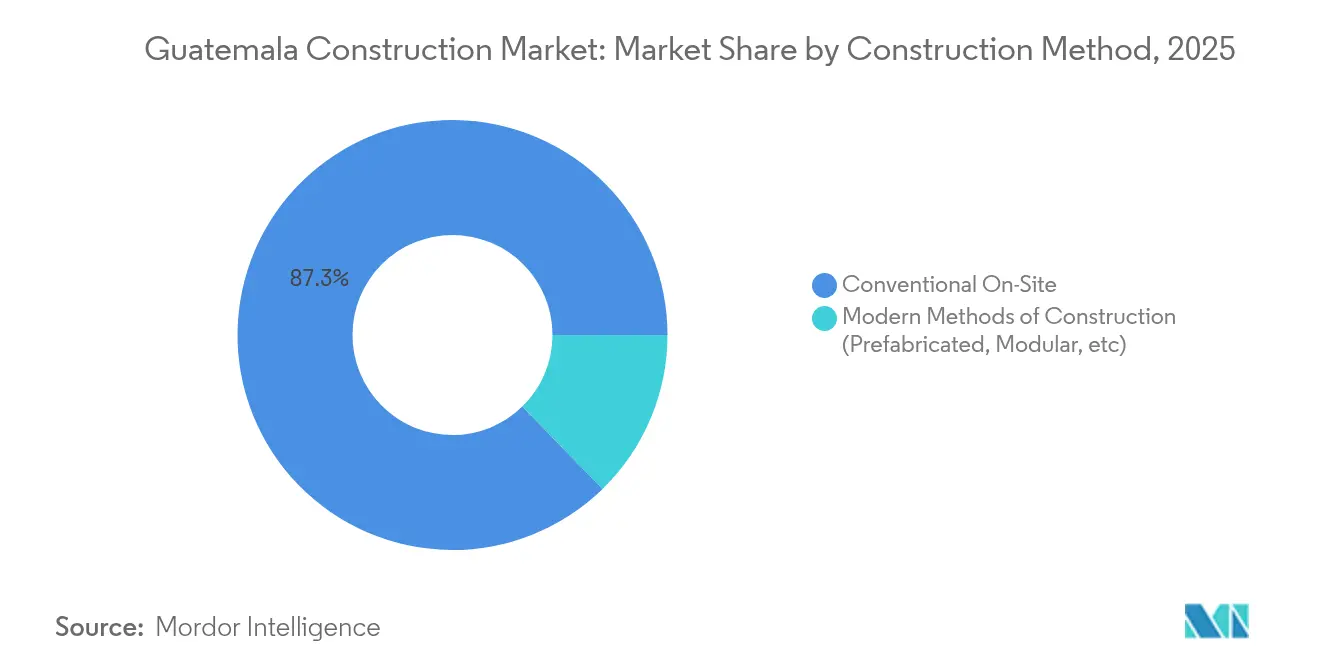

- By construction method, Conventional on-site techniques captured 87.30% of the Guatemala construction market share in 2025. Guatemala construction market size for modern construction methods is projected to grow at an 11.15% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Guatemala Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public sector push for affordable housing | +2.3% | Guatemala City, Mixco, Villa Nueva | Medium term (2-4 years) |

| Expansion of national and regional transport infrastructure | +2.8% | Nationwide; corridors to ports | Long term (≥ 4 years) |

| Renewable-energy investments | +1.9% | Escuintla, Quetzaltenango | Medium term (2-4 years) |

| Industrial logistics zones from trade integration | +1.5% | Escuintla, Guatemala City periphery | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Public Sector Push for Affordable Housing to Address Urban Deficits

Government reforms targeting Guatemala’s 1.9 million-unit housing gap center on low-interest mortgages and streamlined permitting. Micro-finance schemes such as Génesis Empresarial combine credit with technical assistance, improving build quality and compliance. Showcase projects like “Trasciende La Parroquia” in Guatemala City illustrate that sustainable features can coexist with cost-effective design. Rising urban land values are driving a 3-7% increase in property prices in 2025, intensifying demand for vertical housing. These dynamics reinforce the Guatemala construction market’s emphasis on mass-scale residential production and modern prefabricated solutions that cut timelines.[1]U.S. Department of Commerce, “Guatemala – Construction Equipment and Services"

Ongoing Expansion of National and Regional Transport Infrastructure

After a decade of under-spending, transport outlays exceed USD 1.6 billion under the National Agency for Economic Infrastructure Alliances. Taiwan’s USD 100 million commitment to the Atlantico road and planning for a USD 7–9 billion inter-oceanic corridor signal generational upgrades. Public-private partnerships are central to execution, leveraging concession models that de-risk large capital projects. Improved highways and rail links shorten freight times from Guatemala City to Puerto Quetzal, boosting competitiveness for exporters. Consequently, the Guatemala construction market is witnessing an uptick in bids for bridges, viaducts, and tunnel packages that demand higher engineering capabilities.

Renewable Energy Investments Fueling Utility and Infrastructure Projects

MPC Energy Solutions’ 65 MWp solar plant and the Transportation System Expansion Plan (PET 2024-2054) create a rolling backlog of transmission builds. Guatemala’s net-exporter status in regional power trade highlights grid resilience and encourages further solar and wind additions. PEG-4-2022 and PEG-5 tenders are contracting new generation capacity, locking in construction workflows for civil works, piling, and substations. Financing remains strong, evidenced by USD 11 million secured for the San Antonio wind farm expansion. These utility projects diversify the Guatemala construction market beyond housing and roads, pulling in specialist EPC firms.

Emergence of Industrial Logistics Zones through Central American Trade Integration

Nearshoring strategies capitalize on Guatemala’s proximity to Mexico and the United States, attracting textiles, BPO, and light manufacturing investors. Escuintla’s industrial parks offer ready land and port access, underpinning warehouse and factory builds. Commitments such as Protela’s USD 45 million facility and Hansae’s USD 300 million complex validate demand for large-scale manufacturing shells. Wal-Mart’s USD 530 million retail-distribution network expansion signals sustained retail logistics growth. Streamlined construction permits under “Guatemala No Se Detiene” reduce lead times, reinforcing the Guatemala construction market’s pivot to time-critical industrial real estate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Political Instability and Corruption Eroding Investor Confidence and Delaying Public Works | -1.8% | National, with heightened impact in rural regions | Medium term (2-4 years) |

| Underdeveloped Capital Markets Limiting Access to Long-Term Local Financing | -1.2% | National | Long term (≥ 4 years) |

| Chronic Shortage of Skilled Construction Labor and Digital Engineering Talent | -0.9% | National, with acute impact in specialized construction segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Political Instability and Corruption Eroding Investor Confidence

Political turbulence limits project approvals and prolongs procurement cycles, as underscored in the IMF’s 2024 Article IV report. The UK Government’s risk assessment notes that only one PPP has reached financial close since the 2010 law, highlighting administrative frictions. Although transparency reforms are underway, discretionary decision-making still deters long-horizon investors. Budget reallocations in election years disrupt construction cash flows, delaying mobilization. These uncertainties shave growth from the Guatemala construction market by elevating contingency pricing and discouraging multi-year commitments.

Chronic Shortage of Skilled Construction Labor and Digital Engineering Talent

Guatemala certifies fewer than 2,000 construction apprentices annually, well below demand. Swisscontact’s “Nuevas Oportunidades” program trains returning migrants, yet the skills gap persists. Low technical-education funding and emigration of qualified personnel constrain adoption of BIM and modular systems. FHI 360’s labor assessment links high poverty to limited vocational access, amplifying regional disparities. Consequently, conventional methods dominate because contractors cannot readily staff advanced techniques, slowing the Guatemala construction market’s productivity gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Residential Dominance Meets Infrastructure Momentum

The residential segment accounted for 61.42% of the Guatemala construction market in 2025, supported by state-backed mortgage subsidies and a vibrant micro-finance ecosystem. Vertical condominiums and gated suburban communities have surged as developers respond to land scarcity and shifting lifestyle preferences. Urban property prices rising 3-7% in 2025 further incentivize new unit launches. Luxury towers in Guatemala City’s Zona 14 incorporate green roofs and energy-efficient façades, illustrating demand for sustainable amenities. Infrastructure, while smaller today, is forecast to register the fastest 10.26% CAGR, reflecting commitments to the USD 119 million Atlantico road revamp and the envisioned USD 7–9 billion inter-oceanic corridor. These megaprojects will stretch over a decade, anchoring long-term contractor pipelines.

Infrastructure’s impending scale is reshaping contractor strategies, with local builders forming joint ventures to meet pre-qualification thresholds for bridges, tunnels, and rail packages. Taiwanese funding accelerates early works, positioning procurement for 2026 ground-breaks. Simultaneously, residential developers are adopting prefabrication to compress schedules, evidenced by a 25% rise in eco-friendly housing starts last year. As such, the Guatemala construction market balances high-volume social housing with capital-intensive transport and utilities, broadening opportunity sets across value chains.

By Construction Type: New Construction Drives Market Expansion

New-builds represented 57.35% of the Guatemala construction market size in 2025 and are projected to retain dominance with a 9.96% CAGR through 2031. Government roadmaps such as “Guatemala No Se Detiene” prioritize green-field industrial parks, trans-regional highways, and grid extensions, ensuring a robust order book. World Bank program loans earmark USD 2.5 billion for resilient schools and health facilities, creating steady civic demand. Renovation, although smaller, benefits from historic-district upgrades where European investors refurbish colonial assets for boutique hotels, capitalizing on tourism rebounds.

Resilience requirements are raising specifications for new civil works. The Comprehensive School Safety Policy mandates seismic-resistant designs, pushing engineers toward performance-based standards. Insurance providers increasingly condition coverage on adherence to these codes, prompting developers to integrate base isolators and reinforced masonry. Consequently, modern materials suppliers gain traction, and the Guatemala construction market witnesses gradual transitions from unreinforced blockwork to engineered solutions.

By Construction Method: Technological Transition Underway

Conventional on-site techniques still account for 87.30% of 2025 activity, reflecting entrenched craft traditions and fragmented contractor structures. Yet modern construction methods are expanding at 11.15% CAGR as public housing agencies pilot modular steel and CLT systems. The “Construyendo Guatemala” initiative in Antigua showcases cross-laminated timber’s seismic performance, achieving rapid completion while preserving colonial aesthetics. International EPC firms introduce precast bridge girders and automated rebar cages on transport projects, cutting tilt-up times.

Adoption, however, is uneven. High-profile urban towers deploy BIM for clash detection, while small provincial builds rely on manual drafting. Training gaps and limited supply-chain depth impede mass scaling of industrialized methods. Nonetheless, cost pressures and urban land constraints drive developers to explore volumetric modules for student housing and mid-rise apartments, reinforcing an incremental but irreversible shift within the Guatemala construction market.

By Investment Source: Public Leadership with Private Sector Momentum

Public funds provided 64.35% of total 2025 outlays, channelled into social programs and flagship infrastructure. ANADIE’s PPP agenda, worth USD 1.6 billion, blends treasury support with private risk capital to extend fiscal reach. As macro-stability improves, private investment is forecast to grow 10.18% annually, led by multinational manufacturers relocating supply chains closer to North-American clients. Renewable-energy developers, backed by international lenders, are another growth node, with grid-connected solar capacity slated to double by 2027.

Private capital also finances mixed-use urban developments, where retail anchors fund public‐realm enhancements via impact fees. This collaborative model reduces fiscal burdens and accelerates permit cycles. Consequently, the Guatemala construction market is evolving toward balanced funding streams, enabling diversification beyond short-tender public works.

Geography Analysis

Guatemala City anchors the Guatemala construction market, with vertical condominiums reshaping the skyline as developers respond to land scarcity. Demand for tech-enabled apartments equipped with smart metering and high-speed fiber is growing quickly. Luxury projects in Zona 10 and Zona 14 couple energy-efficient façades with 24/7 security, sustaining premium valuations. Gated suburban estates on the city fringe cater to middle-income households migrating from congested urban cores, creating a dual-track residential scene that sustains both high-rise and low-density demand. Municipal infrastructure upgrades, including storm-water tunnels and intersection flyovers, reinforce the capital’s dominance in the Guatemala construction market.

Escuintla’s industrial surge is anchored by its proximity to Puerto Quetzal, Guatemala’s principal Pacific gateway. Logistics corridors linking the port to Guatemala City facilitate time-sensitive exports, prompting developers to erect cross-dock warehouses and temperature-controlled facilities. Solar and wind farms cluster nearby, requiring substations and service buildings that employ skilled steelwork crews. The PET 2024-2054 transmission plan allocates capital for sub-station upgrades, ensuring reliable energy for expanding factories. Transport upgrades, such as the Atlantico-El Rancho highway section, will trim trucking times, reinforcing Escuintla’s allure for regional distribution nodes within the Guatemala construction market.

Secondary cities—Quetzaltenango, Mixco, and Villa Nueva—are capturing residential spill-over as housing prices in the capital climb. Génesis Empresarial’s micro-finance loans support self-build and incremental expansions that improve housing stock quality. EU development funds target water, sanitation, and school builds, adding public-works volume. Road widening projects under “Guatemala No Se Detiene” enhance links between these towns and economic hubs, fostering corridor-based growth. Rural regions benefit from electrification efforts like Project Ohio 2025, which extends low-voltage lines to underserved communities. As connectivity improves, localized construction markets emerge, broadening the Guatemala construction market’s geographic footprint beyond its historic core.

Competitive Landscape

Guatemala’s construction market is fragmented. Holcim’s USD 200 million acquisition of CEMEX’s assets consolidated the cement segment, granting Holcim control over one grinding mill, three ready-mix plants, and five distribution centers. Local contractors such as Corporacion San Francisco S.A. and Corporacion San Francisco S.A. leverage political networks to secure public tenders for highways and social housing. Mid-sized specialists like Precon supply precast components that cater to growing modular demand. International EPCs, including COMSA Corporación, bring rail expertise, partnering with Guatemalan builders to navigate permitting requirements.

Technology is a key differentiator. Firms adopting BIM and cloud-based project-management platforms reduce rework and improve cash-flow forecasting, outperforming rivals stuck with paper-based processes. Sustainable-construction advocates gain market share by integrating low-carbon concrete and energy-efficient façades, responding to potential carbon-pricing schemes outlined by the Ministry of Environment and the UNFCCC. Skilled-labor shortages nevertheless pose execution risks, prompting larger contractors to invest in on-site training centers and collaborate with Swisscontact’s certification programs.

Segment-specific opportunities are emerging. Renewable-energy EPC packages require electrical and civil expertise, creating niches for firms with ISO-certified safety protocols. Industrial build-to-suit contracts linked to nearshoring demand hybrid funding, combining developer equity with tenant capex guarantees. As foreign developers search for local partners, alliances between Guatemalan contractors and multinational materials suppliers become prevalent, redefining competitive boundaries within the Guatemala construction market.

Guatemala Construction Industry Leaders

Corporacion San Francisco S.A.

Constructora AICSA S.A.

Metro Proyectos S.A.

CVG ITSA S.A.

Futuros Constructivos Sobre la Roca S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: MPC Energy Solutions reached financial close on a 65 MWp solar project, expanding Guatemala’s renewable portfolio and generating EPC opportunities

- March 2025: Government launched a transport infrastructure revitalization initiative emphasizing PPPs to accelerate road and rail builds

- February 2025: Taiwan committed USD 100 million for the Atlantico road upgrade, a milestone foreign investment in strategic transport links

- January 2025: Project Ohio 2025 began electrification works in Cerro Grande village, adding 60 connections for 120 families

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Guatemala's construction market as the annual value (USD, current prices) of on-site building and civil works completed within the country across residential, commercial, industrial, infrastructure, energy, and utilities assets; repair and maintenance jobs that materially extend asset life are counted, while routine upkeep is not.

Scope Exclusions: Off-site design, engineering consulting, and sales of standalone construction equipment are outside our scope.

Segmentation Overview

- By Sector

- Residential

- Apartments/Condominiums

- Villas/Landed Houses

- Commercial

- Office

- Retail

- Industrial and Logistics

- Others

- Infrastructure

- Transportation Infrastructure (Roadways, Railways, Airways, others)

- Energy & Utilities

- Others

- Residential

- By Construction Type

- New Construction

- Renovation

- By Construction Method

- Conventional On-Site

- Modern Methods of Construction (Prefabricated, Modular, etc)

- By Investment Source

- Public

- Private

- By Key Region

- Guatemala City

- Mixco & Villa Nueva

- Quetzaltenango City

- Escuintla Region

- Rest of Guatemala

Detailed Research Methodology and Data Validation

Primary Research

We next interview contractors, materials suppliers, urban-planning officials, private-bank credit officers, and housing-coop leaders across Guatemala City, Escuintla, Quetzaltenango, and rural corridors. Those conversations help us validate pipeline volumes, average selling prices, typical lead times, and funding mix assumptions before we finalize the model.

Desk Research

Mordor analysts first gather publicly available macro-sector inputs from tier-one outlets such as the Bank of Guatemala, the Ministry of Communications, Infrastructure and Housing, the National Statistics Institute's construction-cost index, and trade-flow data from UN Comtrade. We enrich that base with thematic white papers from the Inter-American Development Bank and OECD, peer-reviewed journals tracking seismic-resilient design, and project databases issued by Guatemala's public-private partnership unit.

To ground company activity, we draw on annual filings, tender notices, and press releases, then pull financial snapshots from D&B Hoovers and headline trends from Dow Jones Factiva. A wider pool of official gazettes, association newsletters, and reputable press supplements our desk work. The sources listed illustrate our process; many additional records were checked to verify, cross-check, or clarify data points.

Market-Sizing & Forecasting

A top-down build begins with national accounts construction value added, which we reconstruct into subsector pools using housing-starts series, public capital-expenditure budgets, cement shipments, FDI approvals, remittance inflows, and building-permit tallies. Select bottom-up checks, supplier roll-ups, sampled ASP × unit counts, and channel feedback are then used to adjust totals. Multivariate regression, supported by expert consensus on drivers such as mortgage rates and infrastructure allocations, underpins our 2025-2030 projections; scenario analysis captures political-risk swings. Data gaps in micro segments are bridged with ratio proxies from matched markets and are retested once new evidence surfaces.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, senior-analyst peer checks, and a lead-author sign-off. Results are reconciled with external benchmarks, and material anomalies trigger re-contact of sources. Reports refresh annually, while any major policy shift or mega-project award prompts an interim update so clients always receive the latest view.

Why Mordor's Guatemala Construction Baseline Commands Reliability

Published figures often diverge because publishers vary geography, segment mix, price bases, and refresh timing. By locking scope to in-country works, harmonizing inputs, and revisiting drivers each year, Mordor Intelligence delivers a dependable anchor for decision-makers.

Key gap drivers arise when other studies fold Guatemala into wider Latin America totals, rely solely on government budgets, or freeze assumptions over long horizons, which together inflate or compress values relative to our balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.40 B | Mordor Intelligence | - |

| USD 491.83 B | Regional Consultancy A | Aggregates 20-country Latin America region; mixes off-site engineering revenues |

| USD 9.11 B | Trade Journal B | Tracks only eco-friendly high-rise initiatives; excludes infrastructure and informal housing |

In sum, because Mordor's model ties clearly defined activity to transparent variables and is revalidated through both local insight and quantitative checks, our baseline offers a balanced, reproducible foundation for strategy and investment planning.

Key Questions Answered in the Report

What is the current value of the Guatemala construction market?

The Guatemala construction market size is USD 3.70 billion in 2026 and is projected to reach USD 5.64 billion by 2031.

Which segment holds the largest share of the market?

Residential construction leads with 61.42% of the Guatemala construction market share in 2025.

Which region is growing the fastest?

The Escuintla Region is expected to expand at a 10.34% CAGR between 2026 and 2031, the fastest among all regions.

What are the key growth drivers for the sector?

Major drivers include public investment in affordable housing, large-scale transport infrastructure upgrades, renewable-energy projects, and the rise of industrial logistics zones linked to nearshoring.

How significant is private investment in the future market outlook?

Private capital is forecast to grow at a 10.18% CAGR to 2031, supported by manufacturing, logistics, and renewable-energy developments.

What challenges could slow market growth?

Political instability, underdeveloped capital markets, and a shortage of skilled construction labor remain critical constraints on the Guatemala construction market.

Page last updated on: