Dominican Republic Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

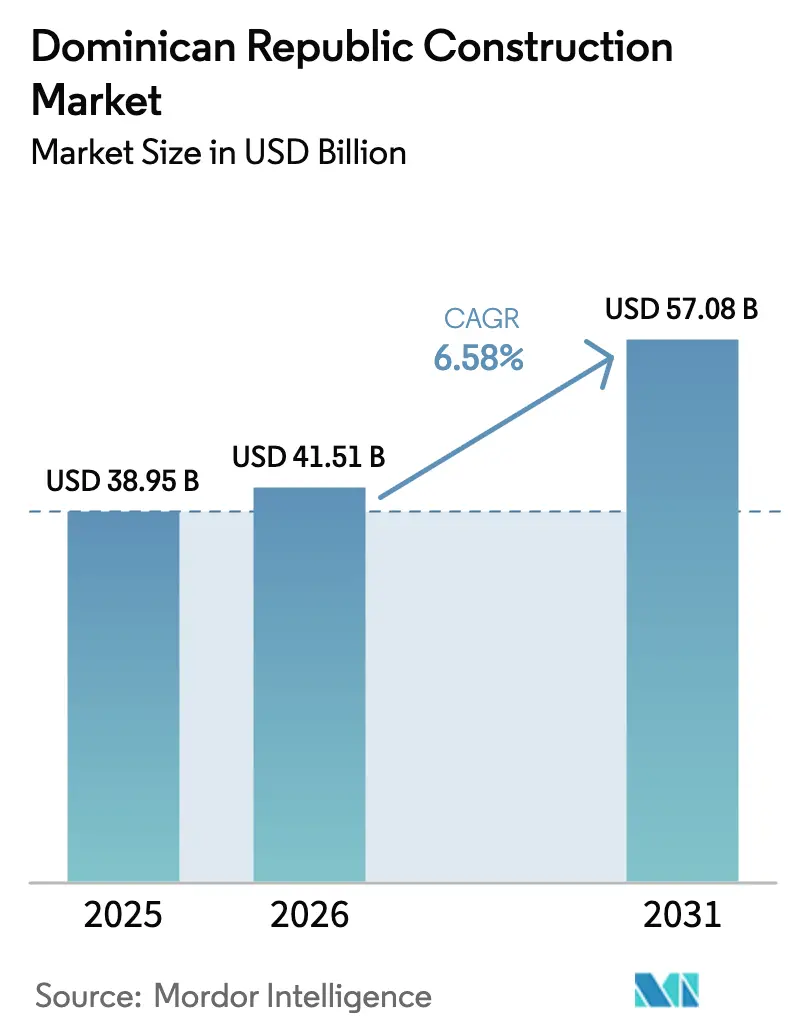

| Base Year Market Size (2025) | USD 38.95 Billion |

| Market Size (2026) | USD 41.51 Billion |

| Market Size (2031) | USD 57.08 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

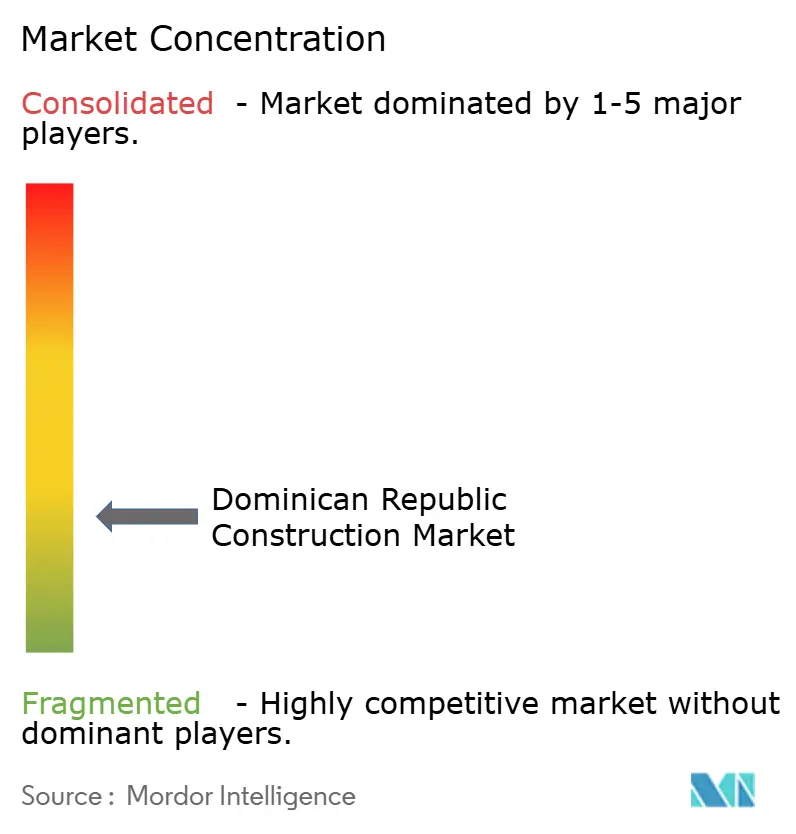

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dominican Republic Construction Market Analysis by Mordor Intelligence

The Dominican Republic Construction Market size is expected to grow from USD 38.95 billion in 2025 to USD 41.51 billion in 2026 and is forecast to reach USD 57.08 billion by 2031 at 6.58% CAGR over 2026-2031. Rising infrastructure allocations under Vision 2030, strong near-shoring inflows, and buoyant tourism demand together keep order backlogs full across civil, commercial, and utility-scale projects. Public-private-partnership (PPP) Law 47-20 has widened access to long-term capital, lowering early-stage risk and bringing global contractors into highway, airport, and renewable-energy tenders. On the private side, a steady stream of remittances, USD 10 billion in 2024, continues to underwrite mid-market housing, while free-trade-zone (FTZ) expansions trigger a new round of industrial work. Despite material-cost volatility and a persistent skills gap, project pipelines remain resilient because multilateral lenders such as CABEI and IDB Invest routinely co-finance priority transport and energy schemes.

Key Report Takeaways

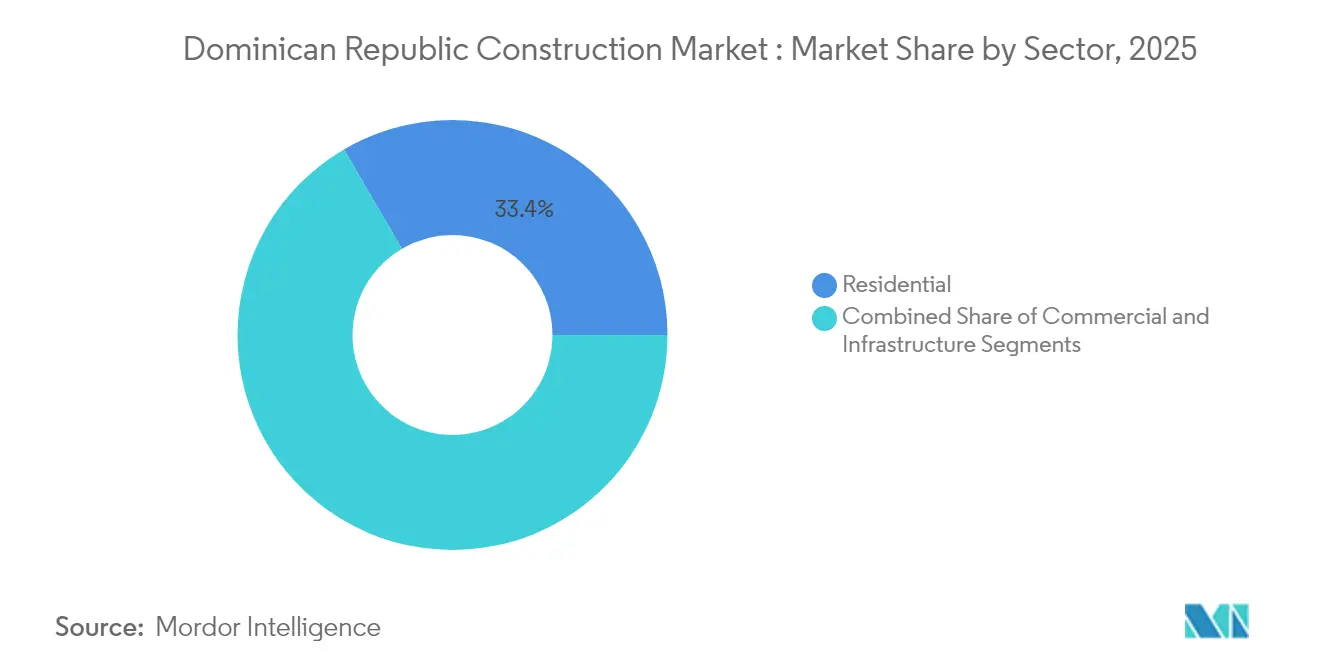

- By sector, residential captured 33.42% of the Dominican Republic construction market share in 2025, while commercial work is projected to post the fastest 7.92% CAGR through 2031.

- By construction type, new construction held 61.69% of the Dominican Republic construction market size in 2025; renovation is advancing at a 6.08% CAGR to 2031.

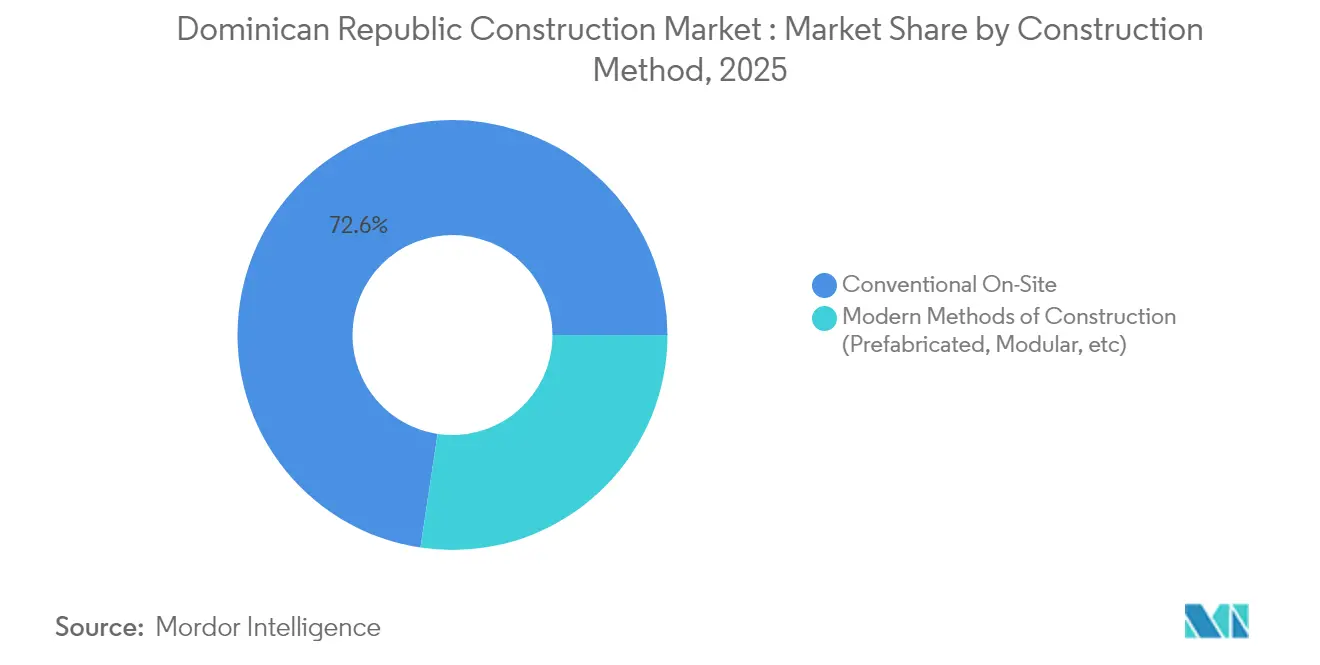

- By construction method, conventional on-site techniques accounted for 72.62% share in 2025, whereas prefabricated and modular solutions led growth at a 9.58% CAGR over the same horizon.

- By investment source, private capital provided 56.11% of the Dominican Republic construction market size in 2025, while public spending logs the fastest 8.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Dominican Republic Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National infrastructure build-out under Vision 2030 | +1.8% | National, with concentration in Santo Domingo, Santiago, Puerto Plata corridors | Long term (≥ 4 years) |

| Tourism-led boom in hospitality & mixed-use projects | +1.5% | Coastal regions, Punta Cana, Puerto Plata, Miches development zones | Medium term (2-4 years) |

| Rising housing demand fuelled by remittances & urban middle-class growth | +1.2% | Greater Santo Domingo, Santiago, secondary urban centers | Medium term (2-4 years) |

| Near-shoring & Free-Trade-Zone expansions spurring industrial facilities | +0.9% | Free trade zones, Santiago, San Pedro de Macorís industrial corridors | Long term (≥ 4 years) |

| Utility-scale renewable-energy pipeline (solar, wind) | +0.8% | National grid integration points, rural solar development areas | Long term (≥ 4 years) |

| Public-Private-Partnership Law 47-20 unlocking long-tenor financing | +0.6% | National infrastructure projects, transportation networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Infrastructure Build-Out Under Vision 2030

The Vision 2030 roadmap has ushered in the country’s largest public works program, covering highways, urban rail, and energy links. Flagship schemes such as the USD 421 million PLANACOVIAL road package and the USD 250 million Santo Domingo Metro Line 2C are already under execution. Faster permit processing, cut from 206 days to as few as 60, removes a chronic bottleneck and lets contractors move quickly from design to ground-breaking. New mobility assets also feed into climate goals because upgraded rail and cable-propelled transit cut urban emissions. Together, these factors make infrastructure the single biggest pull-factor for the Dominican Republic construction market over the decade[1]Banco Centroamericano de Integración Económica, “PLANACOVIAL Loan Document,” bcie.org.

Tourism-led Boom in Hospitality & Mixed-Use Projects

Global chains see the Dominican coast as a safe, high-yield bet, prompting a wave of resort and branded residential builds. Miches alone hosts confirmed developments by Wyndham, Marriott, Hilton, and Hyatt, alongside a Four Seasons slated for 2026. Complementary assets, notably the USD 67.5 million* Cabo Rojo Airport runway, ensure visitor capacity keeps pace with room supply. Public agencies support the boom via RD $300 million (USD 5.3 million) highway upgrades that shorten travel times from airports to beaches. Construction work, therefore, spans hotels, retail promenades, and supporting utilities, multiplying spend across the value chain.

Rising Housing Demand Fueled by Remittances & Urban Middle-Class Growth

Continuous inflows from the Dominican diaspora allow families to self-finance homebuilding, explaining why residential still tops market share. Over 200 active projects were logged in the two largest metros in 2024. Government social-housing programs add a second vector, with the Ministry of Housing completing multiple health and education facilities that anchor new neighborhoods. Private developers chase the upper-mid tier, where buyers seek gated communities, better finishes, and energy-efficient designs. Innovative deals such as Eco Buildings Group’s letter of intent for 10,000 modular units signal that off-site methods could narrow the affordability gap while lifting productivity.

Near-Shoring & Free-Trade-Zone Expansions

Tighter North American supply-chain rules have vaulted the Dominican Republic onto corporate site-selection shortlists. The country now hosts 87 FTZ parks, and medical-device majors lead a pipeline of clean-room factories that require strict HVAC and utilities. Eaton’s USD 150 million fuse-assembly plant in Santiago typifies investor confidence and adds a high-spec industrial reference for local builders. Tax waivers under CAFTA-DR keep operating costs competitive, reinforcing the structural demand for production halls, logistics hubs, and back-office campuses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated interest-rate environment inflating borrowing costs | -1.1% | National, affecting private sector projects disproportionately | Short term (≤ 2 years) |

| Skilled-labour shortages due to emigration & informal sector pull | -0.9% | National, concentrated in technical specializations | Medium term (2-4 years) |

| Volatile import prices for steel, cement & fuels | -0.8% | National, with greater impact on large infrastructure projects | Medium term (2-4 years) |

| Protracted land-titling & cadastral disputes delaying projects | -0.6% | Rural areas, peri-urban development zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Interest-Rate Environment is Inflating Borrowing Costs

High policy rates translate directly into costlier construction loans, especially for small and midsize homebuilders that rely on bank credit. Developers are postponing projects or scaling down floor-area ratios to protect margins. Although PPP structures soften this headwind for public works, commercial malls, and middle-income housing remain exposed until monetary easing resumes. The squeeze also discourages first-time buyers, curbing presales that normally fund early construction stages.

Skilled-Labor Shortages Due to Emigration & Informal-Sector Pull

By 2025, the construction sector will need 378,503 workers, rising to 387,019 in 2026. However, the supply of skilled trades is declining as many craftworkers seek better opportunities abroad. Copymecon notes that despite daily pay for general labor ranging from DOP 800 to DOP 1,200 (USD 14–21), vacancies remain high as experienced masons, carpenters, and electricians leave. Contractors often rely on Haitian crews, but many lack proper immigration status, limiting formal hiring and worsening shortages. The informal economy further complicates the issue by attracting workers with cash wages and flexible hours, making it harder for compliant firms to compete. Business associations are collaborating with immigration authorities to address labor gaps and simplify permits, but progress is slow due to procedural hurdles and public concerns. The shortage is most critical in technical roles like electrical wiring, plumbing, and heavy-equipment operation, where limited training capacity delays projects and affects quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Residential Holds the Largest Share while Commercial Races Ahead

Residential commanded 33.42% of the Dominican Republic construction market share in 2025, anchored by remittance-funded self-builds and government social-housing completions in Santo Domingo and Santiago. Investor appetite stays strong because net migration to cities lifts apartment absorption and keeps vacancy low. Modular pilots are gaining visibility, and once regulatory approvals are streamlined, that channel could reclaim a slice of conventional masonry.

The commercial segment leads growth at an 7.92% CAGR thanks to sustained tourism pipelines and FTZ lease-ups. Hotel majors bundle retail promenades, conference centers, and branded residences inside master plans, enlarging construction scopes and diversifying cash flows. The Dominican Republic construction market size tied to tourism alone is set to pass USD 10.74 billion by 2031, validating capital-expenditure commitments from groups such as Grupo Puntacana, which earmarked USD 70 million for a Puerto Plata project.

By Construction Type: New Builds Dominate but Renovation Gains Traction

New construction made up 61.69% of expenditure in 2025, driven by greenfield highways, airports, and solar farms under Vision 2030. Contractors benefit from clear right-of-way on government land, and multilateral co-lending reduces payment-risk perception. Higher materials inflation, however, pushes owners to lock in lump-sum contracts early, shifting contingency risk downstream.

Renovation activity rises at a 6.08% CAGR as hotel operators refurbish pre-2005 resorts to meet brand standards. Office landlords in Santo Domingo retrofit buildings for flexible-workspace providers, adding digital infrastructure and LEED upgrades that command premium rents. For many local contractors, this niche offers steadier volumes and lower bonding requirements than public megaprojects.

By Construction Method: Conventional Still Rules, Prefab Accelerates

Conventional site-built work retained a 72.62% share in 2025 because skilled labor remains relatively affordable, and supply chains for cement block and rebar are entrenched. Local builders favor incremental construction, funding progress through installment sales common in the housing sector.

Modern methods, led by modular steel frames and panelized walls, notch a 9.58% CAGR as developers chase faster cycle times and predictable quality. Eco Buildings Group’s USD 237 million memorandum for 10,000 units shows that scale is achievable when off-site factories sit near urban demand centers. Policy makers also view prefab as a lever to mitigate the forecast 378,503-worker shortfall by 2025.

By Investment Source: Private Capital Leads, Public Budgets Scale Up

Private investors supplied 56.11% of spending in 2025 on the back of hotel, FTZ, and residential pipelines. These sponsors prize clear exit routes through condo presales or sale-leasebacks, which Dominican legislation facilitates. Exchange-rate stability and CAFTA-DR duty-free access further sharpen deal economics.

Public outlays climb at an 8.34% CAGR through 2031 as the Abinader administration accelerates road, rail, and energy projects. CABEI’s USD 421 million PLANACOVIAL loan and IDB Invest’s clean-energy tranches de-risk procurement and keep tender activity brisk. This blend of funding sources cushions the Dominican Republic construction market against cyclical shocks.

Geography Analysis

Greater Santo Domingo remains the single largest regional market, absorbing 37.45% of nationwide spend in 2025 and projected to advance at a 6.04% CAGR. Transit megaprojects, the USD 250 million Metro Line 2C extension and a USD 250 million urban cable car anchor civil-works demand while unlocking adjacent residential plots. A dense service economy draws corporate developers into mixed-use towers, further amplifying crane counts across the skyline.

Santiago holds the second-largest share, propelled by the monorail slated for 2025 commissioning and the Eaton fuse-assembly plant that sets a new benchmark for industrial fit-outs. Free-trade-zone growth around San Pedro de Macorís and La Romana spreads activity along the country’s main logistics spine, connecting ports with inland distribution hubs. Contractors competent in ISO-cleanroom specifications capture repeat work as medical-device exporters consolidate production under near-shoring strategies.

Coastal provinces, notably Punta Cana, Miches, and Puerto Plata, post the fastest aggregate growth at 8.36% through 2031. The USD 2.25 billion Pedernales master plan and early-work packages at Cabo Rojo Airport unlock a large pipeline of hospitality, water-treatment, and power-distribution contracts. Public highway upgrades RD $300 million (USD 5.3 million) shorten airport-hotel transfer times, making secondary beaches viable for integrated resort clusters. Renewable-energy developers dot rural hinterlands with solar arrays, requiring grid expansions that spread civil-works orders beyond the tourist belt.

Competitive Landscape

Local firms such as Constructora Rizek, Noval, and Cocime hold sway in small-to-midscale housing and commercial builds, leveraging community ties and familiarity with municipal approval processes. Their collective share keeps overall market concentration moderate, encouraging price competition yet making large projects contingent on joint-venture formations.

International majors, including ACCIONA, Dominion, and Sacyr, win transportation and renewable-energy concessions where performance guarantees and specialized equipment are prerequisites. These players usually partner with local subcontractors for earthworks and finishing trades, injecting global project-management standards while preserving domestic labor content.

M&A activity underscores strategic repositioning. Sika’s 2024 purchase of Vinaldom deepens its chemicals portfolio and expands local distribution, enhancing value-engineering options on waterproofing and admixtures. Conversely, CEMEX’s USD 950 million exit signals portfolio rotation toward core U.S. assets, opening market space for new entrants or local producers seeking backward integration. Contractors increasingly deploy BIM and drone-based progress tracking to boost productivity; however, adoption skews toward tier-one firms, leaving an innovation gap among small enterprises.

Dominican Republic Construction Industry Leaders

Constructora Rizek y Asociados SRL

Noval SRL

Contratistas Civiles y Mecanicos SA

Metro Country Club SA

Paredes y Asociados Constructora, C. por A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The government selected Consorcio Consultores Especializados to manage, engineer and supervise the Guayubín hydro-electric build. Scheduled for completion in 2026, the plant will add new renewable capacity to the national grid.

- June 2025: A follow-on award set the Guayubín project’s professional-services budget at RD $434 million (USD 7 million). The contract covers technical studies, on-site QA/QC and timeline control to keep the scheme on cost and compliant.

- February 2025: The U.S. Consulate issued a USD 1–5 million design-build tender for slope stabilization at Los Bambues, Santo Domingo. The works package includes perimeter walls, drainage upgrades and full storm-water controls to protect nearby housing.

- April 2025: TotalEnergies signed a 15-year deal to supply 0.4 million t of LNG each year to Enadom’s 470 MW combined-cycle plant now under construction. Guaranteed fuel flow de-risks the USD 700 million* project and advances the shift from fuel oil to cleaner gas.

Dominican Republic Construction Market Report Scope

Construction includes any on-site physical work that involves erecting a structure, cladding, external finish, formwork, fixtures, installing services, unloading equipment, supplies, or the like. A complete background analysis of the Dominican Republic Construction Market is covered in this report. It includes the assessment of the economy and the contribution of sectors in the economy, market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics and geographical trends, and COVID-19 impact.

The Dominican Republic Construction Market is segmented by sector (residential, commercial, industrial, transportation infrastructure, and energy and utilities). The report offers market sizes and forecasts in value (USD ) for all the above segments.

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

| Public |

| Private |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

Key Questions Answered in the Report

What is the estimated value of construction activity in the Dominican Republic in 2026?

Spending stands at USD 41.51 billion, reflecting robust demand across housing, tourism and infrastructure.

How quickly is overall construction spending projected to expand?

Outlays are forecast to rise at a 6.58% CAGR, reaching about USD 57.08 billion by 2031.

Which segment currently attracts the largest share of building spend?

Residential work leads with 33.42% of 2025 activity, driven by remittances and steady household formation in the main metros.

How does Public-Private-Partnership Law 47-20 influence project finance?

The statute unlocks long-tenor capital, helping the government and private sponsors advance a USD 1.5 billion pipeline of roads, ports and energy assets.

Why are prefab and modular techniques growing in popularity?

Off-site methods deliver faster completion and consistent quality while easing the skilled-labor shortfall; they are expanding at a 9.58% CAGR through 2031.

How big is the skilled-labor gap facing builders?

The sector needs about 378,500 workers in 2025 and nearly 387,000 in 2026, yet emigration and informal hiring leave key technical roles unfilled.

Page last updated on: