Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

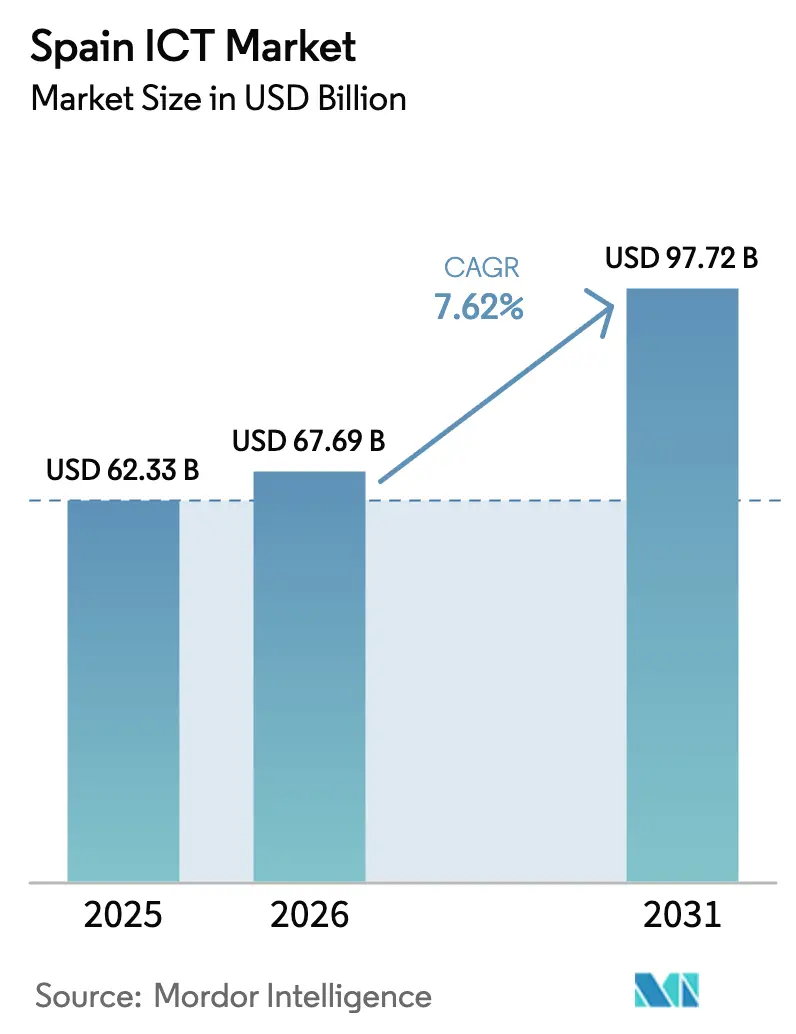

| Base Year Market Size (2025) | USD 62.33 Billion |

| Market Size (2026) | USD 67.69 Billion |

| Market Size (2031) | USD 97.72 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

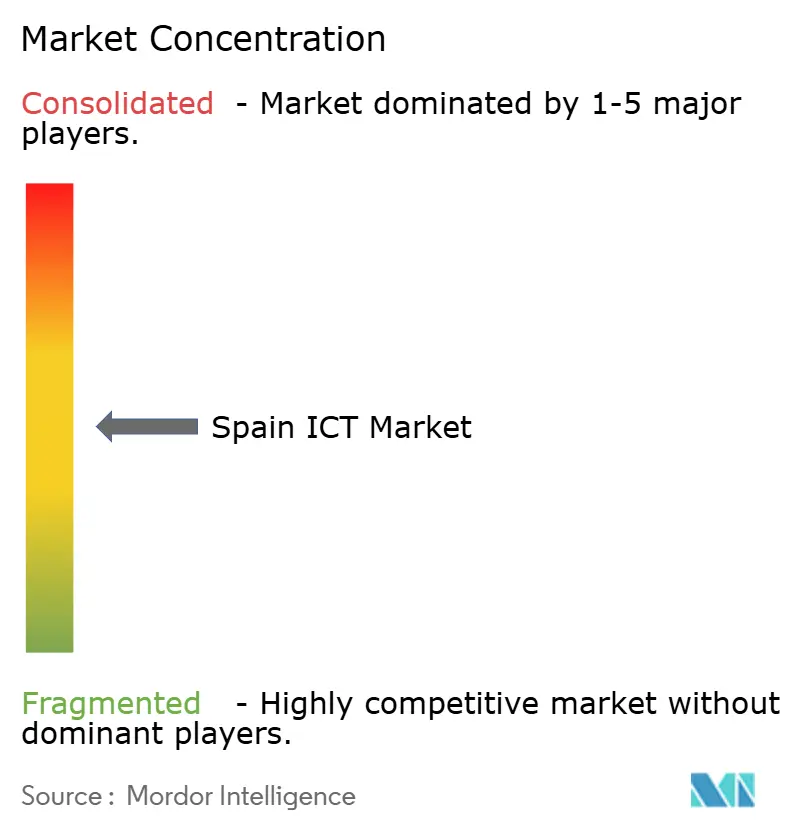

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain ICT Market Analysis by Mordor Intelligence

The Spain ICT Market size is expected to increase from USD 62.33 billion in 2025 to USD 67.69 billion in 2026 and reach USD 97.72 billion by 2031, growing at a CAGR of 7.62% over 2026-2031. Cloud build-outs in Aragon, a nationwide 5G footprint topping 90% population coverage, and EUR 40.4 billion (USD 47.94 billion) in stimulus funding have raised digital-infrastructure density and compressed deployment timelines, lifting technology spending among both public bodies and private firms. Hyperscalers alone earmarked more than EUR 22 billion (USD 26.10 billion) for new capacity through 2026, effectively anchoring the Spain ICT market to Europe’s third-largest cloud node after London and Frankfurt. Security budgets are expanding faster than headline outlays because ransomware strikes climbed 35% year on year in 2025, while the EU’s NIS2 directive imposes new compliance deadlines that push zero-trust architecture to the top of the executive agenda. Small and medium-sized enterprises, armed with Kit Digital vouchers that underwrite up to 80% of software costs, are accelerating cloud adoption even as large enterprises dominate absolute spending. Intensifying vendor consolidation, Telefónica trimmed its IT supplier roster from more than 20 firms to three lead integrators, signaling rising competitive barriers for mid-tier providers.

Key Report Takeaways

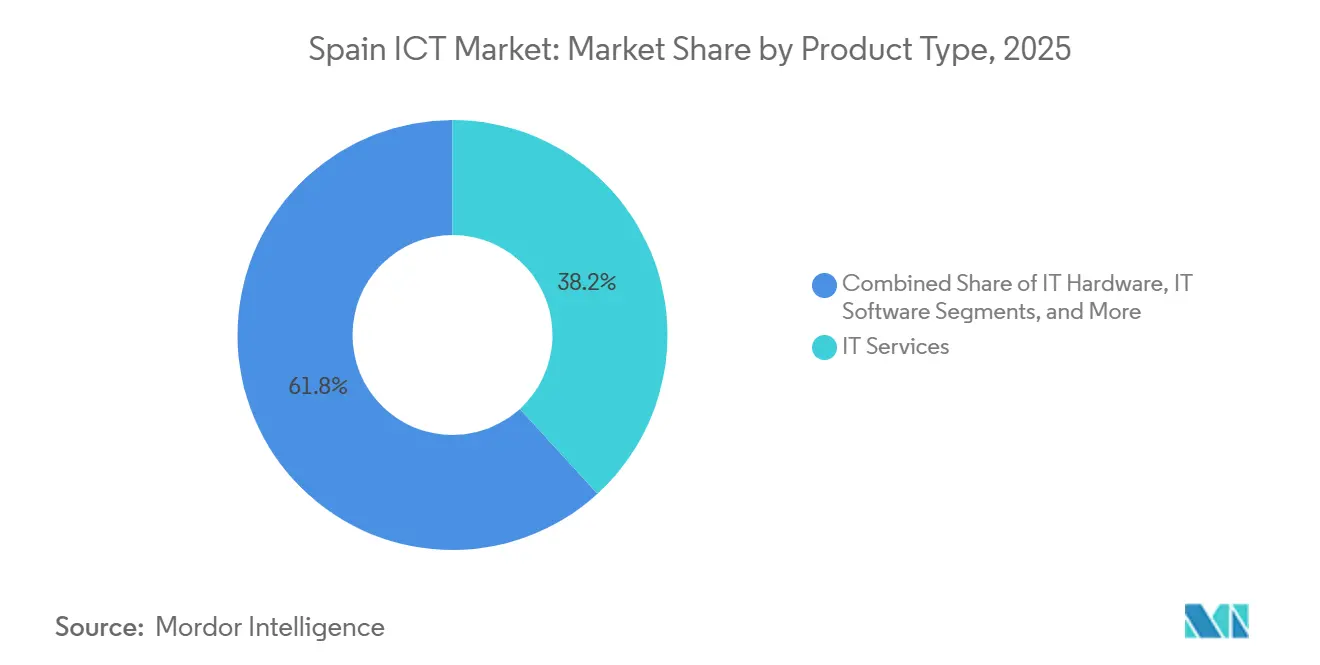

- By product type, IT services led with 38.23% revenue share in 2025, while IT security recorded the highest projected CAGR at 8.18% through 2031.

- By enterprise size, large enterprises accounted for 56.47% of 2025 spend, whereas SMEs are on track for the fastest growth at an 8.43% CAGR to 2031.

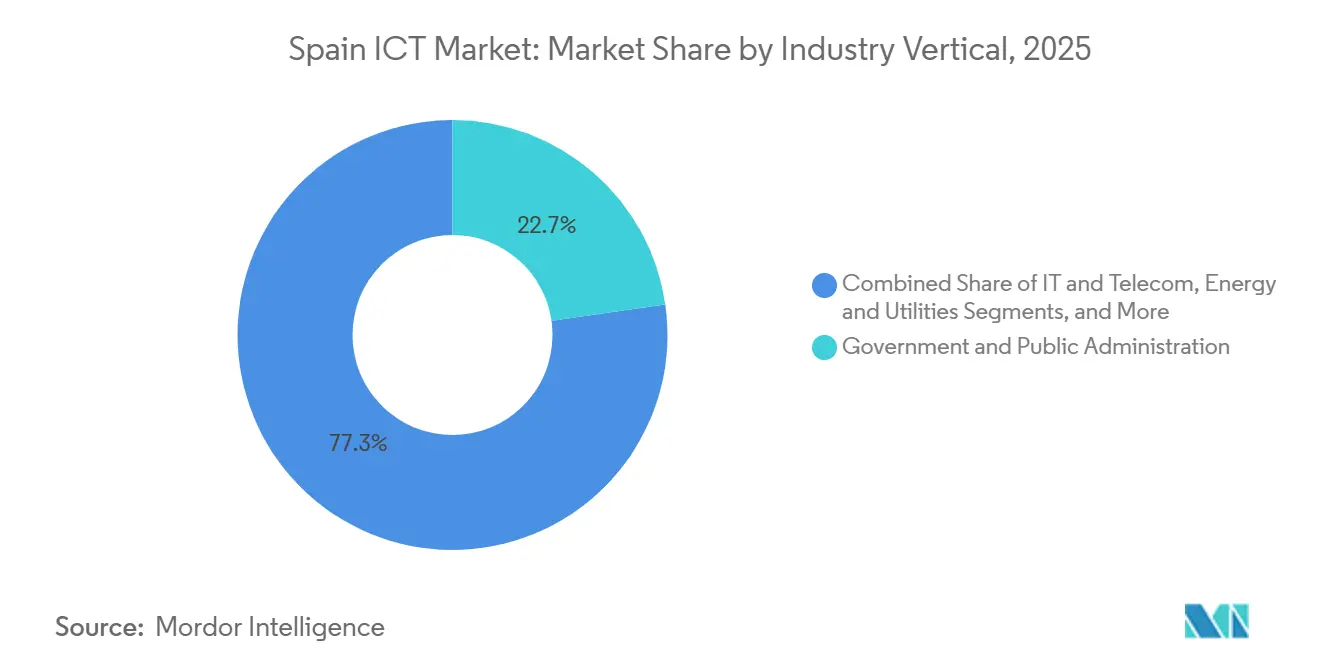

- By industry vertical, government and public administration captured 22.74% of 2025 revenue; manufacturing is set to post the strongest expansion at a 9.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-funded Digital Agenda 2026 programs | +1.8% | National (Madrid, Catalonia) | Medium term (2-4 years) |

| EU-backed SME cloud-voucher scheme uptake | +1.2% | National (industrial regions) | Short term (≤2 years) |

| 5G and FTTH densification accelerates ICT upgrades | +1.5% | National (rural gaps) | Medium term (2-4 years) |

| Near-shoring of LATAM tech support to Spain | +0.8% | Madrid, Barcelona, Valencia | Long term (≥4 years) |

| Spanish-language AI/LLM tool-chain expansion | +1.1% | National, LATAM spill-over | Medium term (2-4 years) |

| Mandatory EU cyber-certification (EUCS) spend | +1.4% | National (critical sectors) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud Adoption Among Spanish SMEs

More than 710,000 vouchers worth EUR 2.9 billion (USD 3.44 billion) lowered the payback period on SaaS investments from three years to under 18 months, lifting the SME cloud-utilization rate to 34% in late 2025. Software vendors now chase monthly recurring revenue, embedding GDPR modules that lock firms into multi-year contracts. Madrid and Catalonia captured nearly half of all vouchers, while rural Extremadura trailed because of limited broadband. As subsidies sunset in late 2026, churn metrics will reveal whether SMEs internalize cloud workflows or retreat to on-premise stacks. For the Spain ICT market, retention, not acquisition, will determine post-subsidy momentum.

EU-Funded Digitalization Surge Post-2026

Spain received the EU’s highest per-capita digital allocation, exceeding EUR 800 (USD 949.24) per inhabitant through 2025. The PERTE Chip initiative injects EUR 12.25 billion (USD 14.54 billion) into semiconductor R&D, while Spain Digital 2026 targets nationwide fiber coverage and online availability of all public services by end-2026. Systems integrators with framework agreements stand to book back-to-back projects as ministries race to hit EU milestones. Municipalities lacking project-management bandwidth risk missing funds, widening the urban-rural digital divide. From 2027 onward, grants morph into blended finance, favoring partners able to absorb balance-sheet risk, a dynamic that reshapes the Spain ICT market’s competitive landscape.

Rapid 5G Roll-Out Catalyzing Edge Demand

Telefónica’s standalone 5G network already touches 94% of Spain’s population, supported by 17 edge nodes co-located with radio sites.[1]Telefónica, “Integrated Annual Report 2024,” telefonica.com Vodafone and MasOrange pledged EUR 4 billion (USD 4.75 billion) to densify their networks, shifting real-time analytics from hyperscale centers to the edge. Automotive plants in the Barcelona-Zaragoza corridor run digital twins that demand sub-10-millisecond latency; edge gateways now process machine-vision feeds locally, slashing production downtime. EU security mandates require every critical-infrastructure edge node to pass ENISA audits, tilting advantage toward carriers with certified facilities. Edge adoption therefore expands the Spain ICT market while narrowing entry routes for independent startups.

Rising Cyber-Attack Sophistication Driving Security Spend

INCIBE now records over 45,000 daily alerts as ransomware and hacktivist campaigns intensify. A EUR 1.157 billion (USD 1.37 billion) national cybersecurity plan funds a centralized security operations center and compulsory penetration testing for essential-service operators. The insurance sector raises the bar by requiring ISO 27001 audits for cyber-liability coverage, embedding compliance as a cost of doing business. Spanish mid-sized providers struggle to deliver zero-trust frameworks, opening doors to global specialists. As regulatory pressure converges with threat escalation, security outlays grow faster than overall ICT budgets, reinforcing the Spain ICT market’s pivot toward managed security services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Shortage of Senior Cloud Architects | -0.9% | National, acute in Madrid and Barcelona tech hubs | Medium term (2-4 years) |

| High Electricity Prices Undermining Local Data-centre Economics | -0.7% | National, grid saturation concentrated in Madrid, Catalonia | Short term (≤ 2 years) |

| Legacy ERP Lock-in Across Public Administration | -0.5% | Central Government ministries, regional administrations | Long term (≥ 4 years) |

| Procurement Bureaucracy Slowing Large-Scale IT Projects | -0.6% | Public sector nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage of Senior Cloud Architects

Spain had up to 200,000 unfilled ICT roles in 2025, with senior cloud architects commanding 20-30% salary premiums. Only 9.2% of graduates emerge with STEM degrees, and women fill just 1.4% of ICT posts, dampening diversity and supply lines.[2]European Commission, “Digital Economy and Society Index (DESI) 2025,” ec.europa.eu Project queues lengthen 6-12 months, inflating migration costs by up to 25%. Although a government-backed Digital Talent program subsidizes bootcamps, the first cohort enters the labor market in late 2026, leaving a critical talent gap that slows the Spain ICT market’s velocity.

High Electricity Prices and Grid Saturation

Wholesale power averaged EUR 0.09 per kWh in 2025, but 83% of grid interconnection points reached capacity, forcing data-center projects into 18-24-month queues. Hyperscalers offset volatility through long-term renewable contracts. AWS lined up 100% green power for Aragon, yet smaller colocation firms lack balance-sheet heft to do the same. Intermittent wind and solar output trigger price spikes that erode Spain’s cost advantage. As grid bottlenecks persist, developers explore on-site solar and batteries, raising capital needs and tempering near-term capacity growth within the Spain ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Lead, Security Surges

IT services contributed 38.23% of 2025 revenue, giving the segment the largest Spain ICT market share across product lines. Managed services, application modernization, and integration workstreams drive this dominance as enterprises transition to hybrid architectures. Meanwhile, IT security revenue is set to grow at an 8.18% CAGR to 2031, the fastest among all categories, driven by ransomware escalation and NIS2 compliance deadlines. Hardware faces margin compression as clients prolong refresh cycles, though network equipment enjoys a bump from 5G rollouts.

Spending patterns demonstrate overlap: cloud vendors now embed automated patching, while managed security providers supply compliance dashboards, blurring classic product boundaries. Hyperscale data-center builds in Aragon illustrate this convergence, pairing infrastructure investment with high-margin professional services. These shifts reinforce the Spain ICT market size at the intersection of services and security, redirecting vendor innovation toward outcome-based pricing.

By Enterprise Size: SMEs Accelerate, Large Enterprises Anchor

Large enterprises captured 56.47% of 2025 revenue, cementing their role as financial anchors for the Spain ICT market. Their spending flows toward multiyear ERP estates, colocation contracts, and sophisticated systems-integration engagements. In contrast, SMEs show the fastest growth, with an 8.43% CAGR projected to 2031, abetted by the Kit Digital program’s subsidy, which cut the payback on SaaS from 3 years to 18 months.

While SMEs embrace cloud velocity, their seat-based spend remains lower, compelling vendors to favor usage-based or freemium models. The compliance load associated with GDPR and the Cyber Resilience Act nudges SMEs toward bundled “compliance-as-a-service” offerings. Consequently, the Spain ICT market size for SME solutions will scale through volume rather than deal value, reshaping partner strategies and customer-success metrics.

By Industry Vertical: Government Anchors, Manufacturing Accelerates

Government and public administration accounted for 22.74% of 2025 spend, marking the largest share of the Spain ICT market by vertical. Activity centers on ERP modernization and electronic health record rollouts under Spain Digital 2026. Manufacturing, particularly automotive, is projected to clock a 9.19% CAGR through 2031, the fastest among all verticals, as plants deploy digital twins and Catena-X protocols for end-to-end supply-chain visibility.[3]seat.com

BFSI modernizes core platforms to meet real-time payment mandates, while energy utilities apply AI to optimize renewable assets. Each use case relies on secure, low-latency connectivity to link vertical demand to the broader Spain ICT market size trajectory. Vendors with deep regulatory fluency and OT-IT integration skills will capture disproportionate growth in these domains.

Geography Analysis

Central Spain, anchored by Madrid, delivered the highest regional contribution in 2025, benefiting from headquarters density, three hyperscaler availability zones, and a EUR 1.2 billion (USD 1.42 billion) regional innovation fund. Economies of scale allow consulting giants to base client teams locally, but this clustering inflates rents and heightens the talent crunch, nudging back-office roles to secondary cities like Valladolid.

Eastern Spain Catalonia and Valencia ranks second in regional spending thanks to Barcelona’s startup magnetism and port-logistics digitalization. Barcelona alone secured EUR 1.8 billion (USD 2.13 billion) in VC inflows during 2024, underpinning mobility and health-tech ventures. SEAT’s Martorell plant showcases how edge gateways perform on-site analytics to orchestrate 16 million daily component moves at sub-10-millisecond latency, a proof point for industrial demand propelling the Spain ICT market.

Northern territories Basque Country, Navarre, Asturias specialize in industrial IoT and renewable analytics, with Iberdrola and Siemens Gamesa co-locating R&D labs in Bilbao. Southern regions lag owing to lower GDP per capita and patchy fiber penetration, yet Málaga Tech Park’s 600-plus companies illustrate the pull of nearshore delivery for Northern European clients. Islands such as the Balearics mandate electronic invoicing for hotels, sparking SaaS uptake that narrows the digital gap. Geography thus shapes go-to-market tactics within the Spain ICT market, tilting resource allocation toward high-density corridors while EU cohesion funds chase inclusion.

Competitive Landscape

The top ten suppliers controlled an estimated major share of 2025 revenue, signaling moderate concentration across the Spain ICT market. Accenture, Capgemini, IBM, and NTT DATA dominate large-scale transformation engagements, leveraging offshore hubs while maintaining Spanish-speaking client teams. Telefónica’s supplier rationalization to Capgemini, Inetum, and Minsait strengthens integration around 5G core and AI-driven automation, raising switching costs for mid-tier rivals.

Indra Sistemas’ EUR 725 million (USD 859.59 million) acquisition of Hispasat consolidates space communications and aims to reach EUR 1 billion (USD 1.19 billion) in defense revenue by 2030. Hyperscalers court local ISVs by extending marketplace revenue-sharing terms, and AWS recruited 120 Spanish partners to build vertical apps in its Aragon region. Niche cybersecurity firms differentiate through bundled ISO 27001 audits and managed SOCs, a proposition resonating with SMEs.

Outcome-based pricing gains traction: providers now peg fees to transaction volumes or uptime SLAs, embedding AI for predictive maintenance and anomaly detection. White-space opportunities persist in edge orchestration for latency-sensitive workloads, but success hinges on carrier partnerships that furnish last-mile connectivity. Competition therefore revolves around platform alliances and regulatory fluency, not merely rate cards.

Spain ICT Industry Leaders

Telefonica S.A.

Indra Sistemas S.A.

Amadeus IT Group S.A.

IBM Corporation

Accenture plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Indra Sistemas secured a USD 342 million contract with the U.S. Federal Aviation Administration to replace legacy radar infrastructure across 11 states.

- December 2025: Indra Sistemas finalized the EUR 725 million (USD 859.59 million) acquisition of satellite operator Hispasat, integrating its geostationary fleet to accelerate space-related revenue.

- September 2025: Amazon Web Services announced a EUR 15.7 billion (USD 18.61 billion) ten-year investment in Aragon data centers, projecting 17,500 jobs and full renewable-energy coverage.

- July 2025: Indra Sistemas won a contract worth EUR 65 million (USD 77.07 million) to deploy air-surveillance radar and control systems for Colombia’s aviation authority.

Spain ICT Market Report Scope

Spain ICT Market Report is Segmented by Product Type (IT Hardware [Computer Hardware, Networking Equipment, and Peripherals]. IT Software (IT Services [IT Consulting and Implementation, IT Outsourcing, Business Process Outsourcing, Managed Security Services, and Cloud and Platform Services] IT Infrastructure, IT Security/Cybersecurity, Communication Services), Enterprise Size (Small and Medium-sized Enterprises, and Large Enterprises), and Industry Vertical (Government and Public Administration, BFSI, IT and Telecom, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, Other Industry Verticals). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Industry Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Industry Verticals | ||

Key Questions Answered in the Report

How fast is ICT spending increasing in Spain?

Overall outlays are projected to climb at a 7.62% CAGR between 2026 and 2031, moving the total from USD 67.69 billion to USD 97.72 billion.

Which product category is growing the quickest?

IT security tops the growth table with an 8.18% CAGR through 2031 as firms respond to sharper cyber threats and stricter EU regulations.

Why are SMEs important for Spanish tech vendors?

SMEs are forecast to expand spend at an 8.43% CAGR thanks to Kit Digital subsidies, making them the fastest-growing customer segment even though individual deal sizes remain small.

What geographic area hosts the most data-center investment?

The Aragon region leads new capacity builds, buoyed by EUR 22 billion in hyperscaler commitments that turn the corridor into Europe’s third-largest cloud hub.

Which vertical will post the strongest ICT growth?

Manufacturing, especially automotive plants deploying digital twins, is projected to advance at a 9.19% CAGR through 2031, outpacing all other industry segments.

Page last updated on: