Gravure Decorative Laminate Inks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

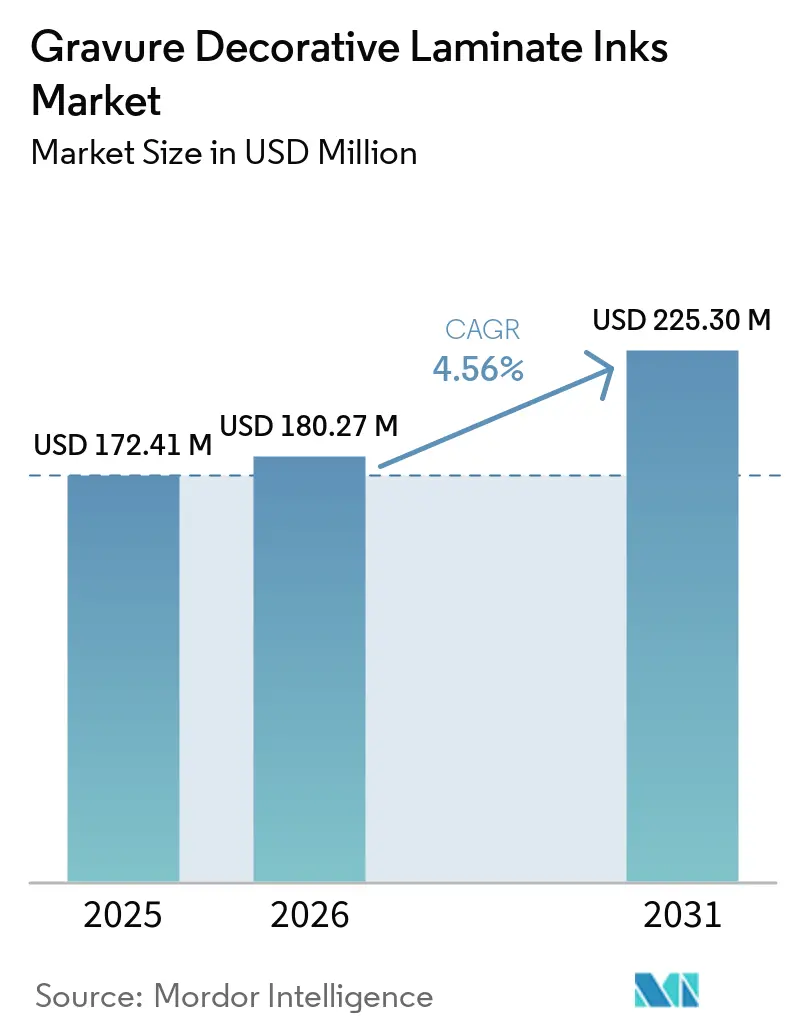

| Market Size (2026) | USD 180.27 Million |

| Market Size (2031) | USD 225.30 Million |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gravure Decorative Laminate Inks Market Analysis by Mordor Intelligence

The Gravure Decorative Laminate Inks Market size was valued at USD 172.41 million in 2025 and is estimated to grow from USD 180.27 million in 2026 to reach USD 225.30 million by 2031, at a CAGR of 4.56% during the forecast period (2026-2031). Demand is supported by large-scale printing of décor papers used in furniture, flooring, and interior panels, while formulation adjustments are accelerating to comply with regulations on volatile organic compounds (VOC) and per- and polyfluoroalkyl substances (PFAS) in Europe and North America. Solvent-based systems continue to dominate high-speed presses; however, water-based chemistries are increasingly adopted as converters prepare for the substance exclusions outlined in the March 2026 European Printing Ink Association (EuPIA) Charter. Simultaneously, gravure printers are leveraging ongoing housing and renovation activities in the Asia-Pacific region, particularly in China and India, where middle-income consumers prefer premium woodgrain and stone-effect laminates. Competitive strategies focus on mergers, regional capacity expansions, and the development of nitrocellulose-free portfolios to align with recyclability targets under the European Union’s Packaging and Packaging Waste Regulation.

Key Report Takeaways

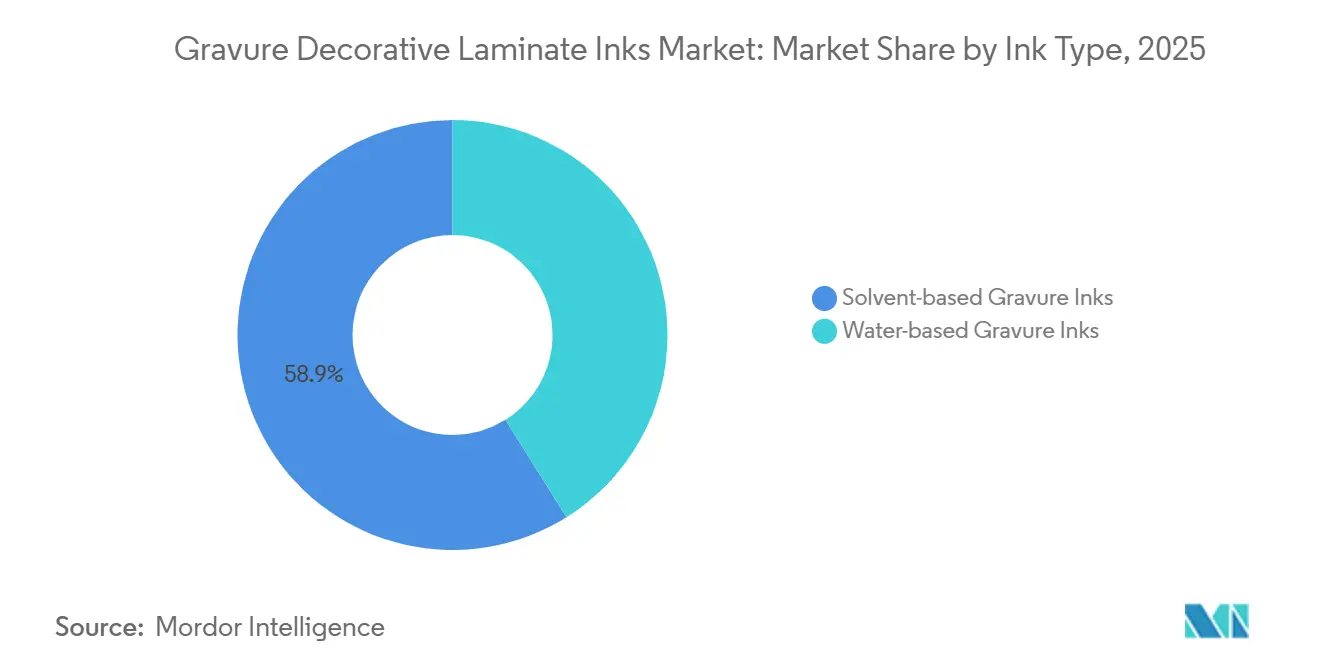

- By ink type, solvent-based formulations held 58.89% of the gravure decorative laminate inks market share in 2025 and remain the revenue leader, and water-based gravure systems are projected to register a 5.23% CAGR through 2031.

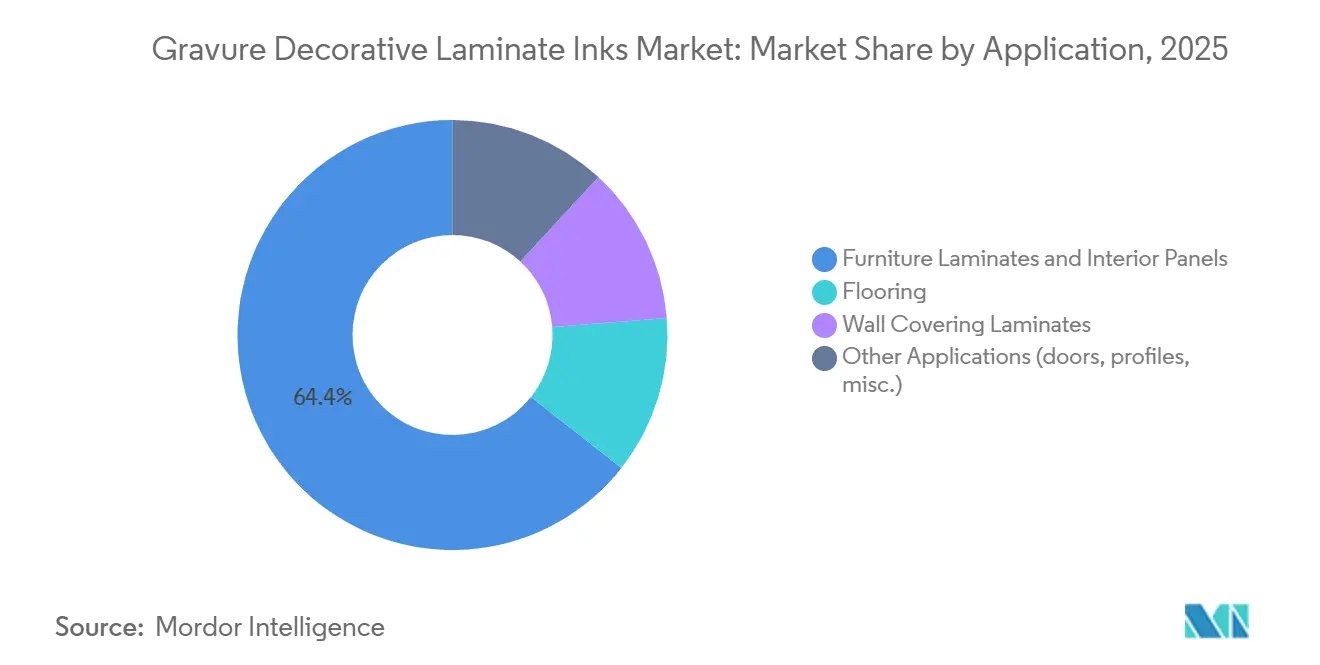

- By application, furniture laminates and interior panels captured 64.38% of 2025 revenue, while flooring applications are forecast to expand at a 5.88% CAGR to 2031.

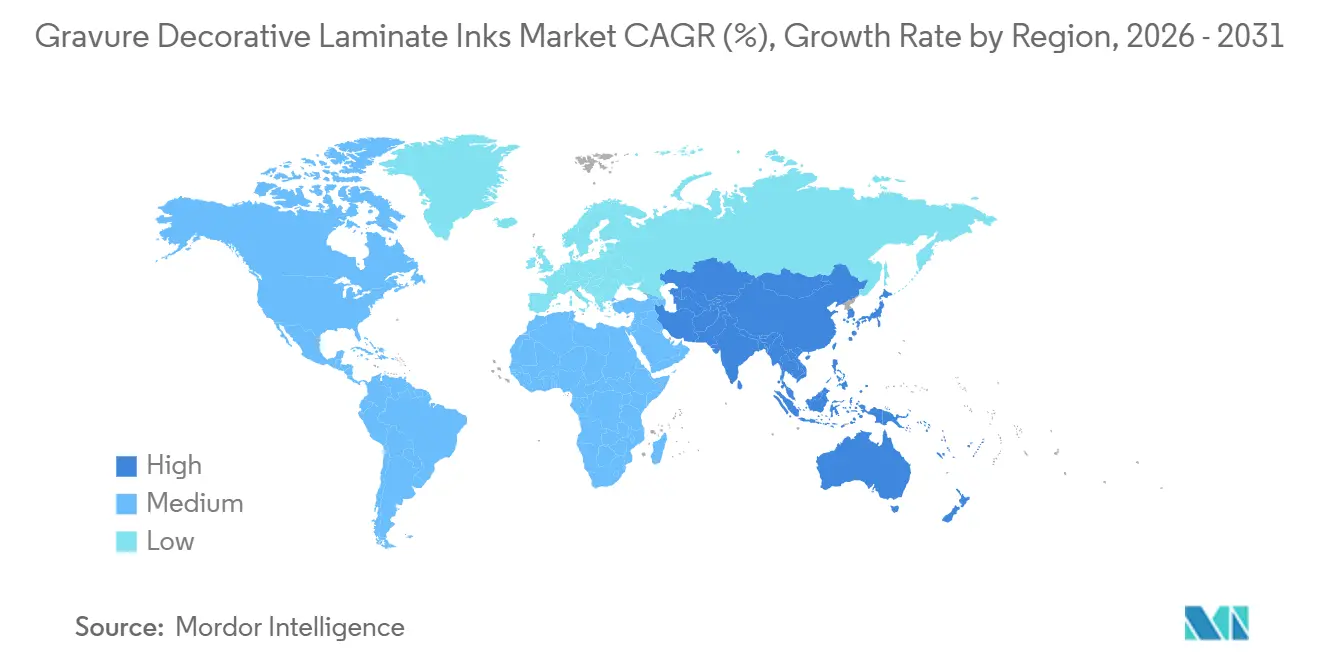

- By geography, Asia-Pacific accounted for 40.12% of 2025 demand and is set to advance at a 5.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gravure Decorative Laminate Inks Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for decorative laminates in furniture and interior applications | +1.2% | Global, with concentration in Asia-Pacific (Vietnam, China, India) and Europe | Medium term (2-4 years) |

| Rapid urbanization boosting premium aesthetic finishes in emerging Asia | +1.0% | Asia-Pacific core (China, India, Vietnam), spill-over to Middle East and Africa | Long term (≥4 years) |

| Mass-customization trend favoring gravure's repeat print accuracy | +0.6% | North America and Europe, selective adoption in Asia-Pacific | Short term (≤2 years) |

| Furniture export incentives in Vietnam and Poland expanding production bases | +0.8% | Vietnam (ASEAN), Poland (EU), with export flows to North America | Medium term (2-4 years) |

| Bio-solvent breakthroughs lowering VOCs and widening regulatory head-room | +0.7% | Europe and North America (regulatory-driven), early adoption in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Decorative Laminates in Furniture and Interior Applications

Furniture and interior panel manufacturers are increasingly adopting high-pressure decorative laminates that replicate natural wood, marble, and textile finishes while adhering to ISO 4586-2:2018 performance standards[1]International Organization for Standardization, “ISO 4586-2:2018,” iso.org. Gravure printing enables micron-level pattern precision, allowing for pearlescent, metallic, and emboss-in-register effects that enhance perceived value. Suppliers such as DIC Corporation offer nitrocellulose-free FINART AP inks, which exclude toluene and methyl ethyl ketone while maintaining press speeds above 200 meters per minute. Additionally, decorative laminates align with retailers' circular-economy initiatives, as décor paper can be recycled alongside particleboard when de-inking systems are utilized at panel mills.

Rapid Urbanization Boosting Premium Aesthetic Finishes in Emerging Asia

Urban households in China and India are increasingly replacing standard laminates with premium synchronized-pore products. These products require gravure inks capable of achieving fine tonal gradients and low metamerism. Laser-engraved cylinders now provide over 10-micron depth resolution, improving pigment dispersion and ensuring consistent gloss uniformity across extended production runs. The growth of residential towers, modular kitchens, and organized retail spaces supports multi-shift gravure operations, where set-up cycles under three hours optimize overall equipment effectiveness.

Mass-Customization Trend Favoring Gravure’s Repeat Print Accuracy

Furniture brands are leveraging artificial intelligence (AI) design tools to create thousands of unique woodgrain patterns, but continue to rely on gravure printing for batch sizes exceeding two tons of décor paper. Digitally engraved cylinders ensure consistent cell geometry and can endure runs exceeding two million linear meters with minimal dot gain, a performance level not yet matched by single-pass inkjet technology. Flint Group’s OmniLam G portfolio eliminates nitrocellulose, enabling converters to meet the European Union’s 2030 recyclability mandate while maintaining high-temperature bond strength for dry lamination processes.

Bio-Solvent Breakthroughs Lowering VOCs

A 2025 patent introduced polyether polyurethane binders containing 50-90% bio-renewable carbon, achieving lap-shear bonds above 2 Newtons per 15 millimeters and ensuring viscosity stability during three-shift production cycles[2]Trea, “High Bio Renewable Content Inks,” trea.com. TOYO INK’s Real NEX BO S3 series, which carries independent biomass certification, operates at 200 meters per minute on standard gravure lines. These advancements provide greater compliance flexibility within California’s 300 grams per liter VOC limit framework without necessitating extensive dryer retrofits.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC and PFAS limits in European Union and California | -0.9% | Europe (EU REACH, EuPIA), North America (California SCAQMD, MDAQMD) | Short term (≤2 years) |

| Rising adoption of single-pass industrial ink-jet for short runs | -0.5% | Europe and North America, with selective adoption in the Asia-Pacific | Medium term (2-4 years) |

| Volatile nitro-cellulose prices squeezing margins | -0.6% | Global, with an acute impact in North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stricter VOC and PFAS Limits in European Union and California

The 2026 European Printing Ink Association (EuPIA) Charter prohibits the use of methanol, chlorinated solvents, and trimethylbenzoyl diphenylphosphine oxide starting April 2027, requiring reformulation of traditional gravure inks. In California, Rule 1117 imposes a 300 grams per liter (g/L) Volatile Organic Compound (VOC) limit, while Rule 1130 reduces cleaning solvent limits to 25 g/L. These regulations necessitate converters to either install regenerative thermal oxidizers or transition to water-based systems. Simultaneously, the European Chemicals Agency's draft Per- and Polyfluoroalkyl Substances (PFAS) restriction sets a threshold of 25 micrograms per kilogram (µg/kg), with a 13.5-year derogation available only if annual audits and site-specific management plans are submitted. Compliance with these regulations increases costs due to testing, documentation, and raw material adjustments, particularly affecting smaller converters.

Rising Adoption of Single-Pass Industrial Inkjet for Short Runs

Unilin Technologies' Digicor platform integrates AGFA water-based pigment inks with proprietary primers, achieving peel strengths of up to 78 Newtons per 5 centimeters (N/5 cm) on Polyvinyl Chloride (PVC) foil décor panels. The single-pass architecture eliminates the need for cylinder engraving and reduces makeready time to minutes, making it suitable for the expanding "drop-ship" furniture market in North America. While gravure printing remains cost-effective for runs exceeding approximately two tons, its market share in niche, design-intensive segments is declining, limiting ink volume growth in these areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ink Type: Solvent-Based Dominance Meets Water-Based Momentum

Solvent-based systems represented 58.89% of the gravure decorative laminate inks market share in 2025, attributed to their strong adhesion and fast drying properties on low-surface-energy films. Facilities equipped with thermal oxidizers maintain total hydrocarbon emissions below 50 parts per million (ppm), ensuring compliance with regional air-quality regulations. Nitrocellulose or polyurethane binders dissolved in alcohol–ester blends achieve DIN-4 viscosities of 25 seconds and operate at speeds exceeding 250 meters per minute (m/min) without dirty-print defects.

Water-based gravure inks are expected to grow at the highest CAGR of 5.23%, driven by their solvent-free composition and regulatory support in Europe. StarColor’s neutral-pH lamination series operates at 180 m/min and withstands press temperatures of up to 150 degrees Celsius (°C), reducing the need for oven retrofits. Alcohol-soluble inks serve as a transitional category, replacing benzene with isopropanol while retaining fast solvent evaporation. Energy-curable gravure inks, leveraging AGFA’s free-radical patent, aim for solvent-free formulations and are projected for double-digit growth once light-emitting diode ultraviolet (LED-UV) modules achieve 25 watts per centimeter (W/cm) output.

By Application: Furniture Laminates Lead, Flooring Accelerates

Furniture and interior panels accounted for 64.38% of the gravure decorative laminate inks market demand in 2025, remaining the primary application segment. International Organization for Standardization (ISO) 4586 testing standards drive ink formulations to incorporate fine-particle aluminum oxide and high-chroma pigments, ensuring durability during melamine impregnation at 160 °C without color degradation. Premium applications such as kitchens, office partitions, and commercial wall cladding favor pearlescent effects, with some gold and copper shades requiring pigment loadings exceeding 20% by weight. The market size for furniture laminates is projected to reach USD 147 million by 2031, supported by increased hotel refurbishments and corporate fit-outs.

Flooring applications, including laminate planks, luxury vinyl tiles, and stone-polymer composites, are expected to grow at the fastest CAGR of 5.88%. European EN 438-8 design laminate standards drive the adoption of synchronized-pore embossing, which requires sub-3 micrometer (µm) pigment dispersion for optimal clarity. Gravure printing remains cost-effective for long-run oak or hickory designs, while digital printing is increasingly used for boutique stock-keeping units (SKUs) with run lengths below 10,000 square meters (m²). Wall-covering laminates and niche products, such as compact laminates, contribute to the remaining market volume, often requiring specialized fire-retardant or antimicrobial properties that limit the use of generic inks.

Geography Analysis

Asia-Pacific accounted for 40.12% of the market share in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 5.33% through 2031. In China, domestic panel mills continue operating double-shift presses despite slower gross domestic product (GDP) growth. India’s housing programs are driving increased interior panel installations, particularly in Tier-2 cities. Vietnam, Malaysia, and Thailand are attracting the relocation of décor-paper printing operations due to their strategic logistics hubs and free-trade agreements. Regional suppliers are investing in alcohol-recovery systems to meet upcoming volatile organic compound (VOC) regulations modeled on Japan’s voluntary limits.

North America, while trailing Asia-Pacific, remains an important market due to the United States' high imports of pre-printed papers for domestic lamination. California’s Rule 1130 is encouraging the adoption of water-based gravure or hybrid alcohol-soluble formulations, leading to incremental increases in installed capacity for aqueous inks in the Southwest. In Mexico, panel producers rely on solvent-based inks sourced from U.S. Gulf Coast plants but are facing rising freight costs, prompting consideration of regional toll-manufacturing options. In Canada, the renovation market is driving demand for niche high-pressure laminate (HPL) grades with metallic accents, sustaining the need for specialty pigment dispersions.

Europe combines design innovation with stringent regulatory requirements. German and Italian pressrooms are implementing closed-loop viscosity controls and reduced-solvent, fast-flash mixes to comply with accident-prevention regulations. The European Printing Ink Association (EuPIA) Charter’s 2027 photoinitiator phase-out is pushing Italian converters to explore light-emitting diode ultraviolet (LED-UV) gravure pilots capable of achieving speeds of 350 meters per minute (m/min) on décor paper. Poland benefits from its proximity to Scandinavian retailers, operating multi-color gravure lines that account for approximately 9% of European consumption. However, growth in Eastern Europe is constrained by wage inflation, though domestic demand for cost-effective medium-density fiberboard (MDF) furniture helps maintain core ink volumes.

Competitive Landscape

The gravure decorative laminate inks market is moderately fragmented. The top five suppliers maintain global pigment integration and regional production facilities. Siegwerk’s planned acquisition of Hi-Tech Inks in March 2026 is expected to enhance its gravure capacity in South Asia, strengthening its position in the Indian packaging and decorative segments. SAKATA INX has allocated JPY 4.7 billion (USD 0.02 billion) to its Vietnamese facility to reduce lead times for Association of Southeast Asian Nations (ASEAN) customers and meet the growing demand for solvent-based products. DIC’s integrated report highlights investments in low-viscosity, high-color gravure systems and closed-loop de-inking solutions, aligning with the European recyclability mandate. Flint Group utilizes its EcoVadis Gold certification and endorsement from the Science Based Targets initiative to secure sustainability-focused sourcing awards. hubergroup’s DYNAMICA series complements its portfolio with Cradle to Cradle material health certification, meeting the requirements of specifiers in healthcare and hospitality interiors. Niche players like Marabu and Wikoff Color Court focus on rapid color-matching services and regional technical support teams, although they lack global resin backward integration.

Innovation in the market is focused on nitrocellulose-free lamination inks, bio-solvent blends, and energy-curable gravure inks that eliminate the need for post-press drying. Suppliers are also exploring digital-gravure hybrid lines, which combine inkjet and engraved cylinder technologies to balance design flexibility with high-volume production efficiency.

Gravure Decorative Laminate Inks Industry Leaders

DIC CORPORATION

Hi-Tech Color Inc.

Lio Chem

SAKATA INX CORPORATION

Siegwerk Druckfarben AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Siegwerk entered into a definitive agreement to acquire India-based Hi-Tech Inks. The acquisition included two manufacturing plants in Rajasthan and Gujarat, consolidated over 20% of India's packaging ink market share, and strengthened Siegwerk's capabilities in gravure decorative laminate inks.

- March 2026: The European Printing Ink Association has introduced its Charter on raw material selection, restricting the use of methanol, chlorinated solvents, and specific photoinitiators. This regulation, which impacts gravure decorative laminate inks, includes a phased compliance schedule extending until April 2027.

Global Gravure Decorative Laminate Inks Market Report Scope

Gravure decorative laminate inks are low-viscosity liquid inks designed for high-speed rotogravure printing on decorative papers. These inks are formulated for durability, resistance to heat, abrasion, and melamine-formaldehyde resin impregnation. They are used to produce surface finishes for applications such as flooring, furniture, and wall panels.

The gravure decorative laminate inks market is segmented by ink type, application, and geography. By ink type, the market is segmented into solvent-based gravure inks and water-based gravure inks. By application, the market is segmented into furniture laminates and interior panels, flooring, wall covering laminates, and other applications (doors, profiles, misc.). The report also covers the market size and forecasts for gravure decorative laminate inks in 16 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Solvent-based Gravure Inks |

| Water-based Gravure Inks |

| Furniture Laminates and Interior Panels |

| Flooring |

| Wall Covering Laminates |

| Other Applications (doors, profiles, misc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Ink Type | Solvent-based Gravure Inks | |

| Water-based Gravure Inks | ||

| By Application | Furniture Laminates and Interior Panels | |

| Flooring | ||

| Wall Covering Laminates | ||

| Other Applications (doors, profiles, misc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Spain | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is current market size of Gravure Decorative Laminate Inks Market?

The Gravure Decorative Laminate Inks Market size was valued at USD 172.41 million in 2025 and is estimated to grow from USD 180.27 million in 2026 to reach USD 225.30 million by 2031, at a CAGR of 4.56% during the forecast period (2026-2031).

Which ink chemistry leads current demand?

Solvent-based formulations hold 58.89% of 2025 revenue due to adhesion and high-speed press compatibility.

Where is regional consumption expanding the quickest

Asia-Pacific posts the fastest 5.33% CAGR through 2031, underpinned by housing and furniture production in China, India, and ASEAN.

What regulation is reshaping formulation strategies in Europe?

The 2026 EuPIA Charter eliminates methanol, chlorinated solvents, and certain photoinitiators by staged deadlines, forcing water-based and bio-solvent adoption.

Page last updated on: