Large Molecule Contract Development And Manufacturing Organization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

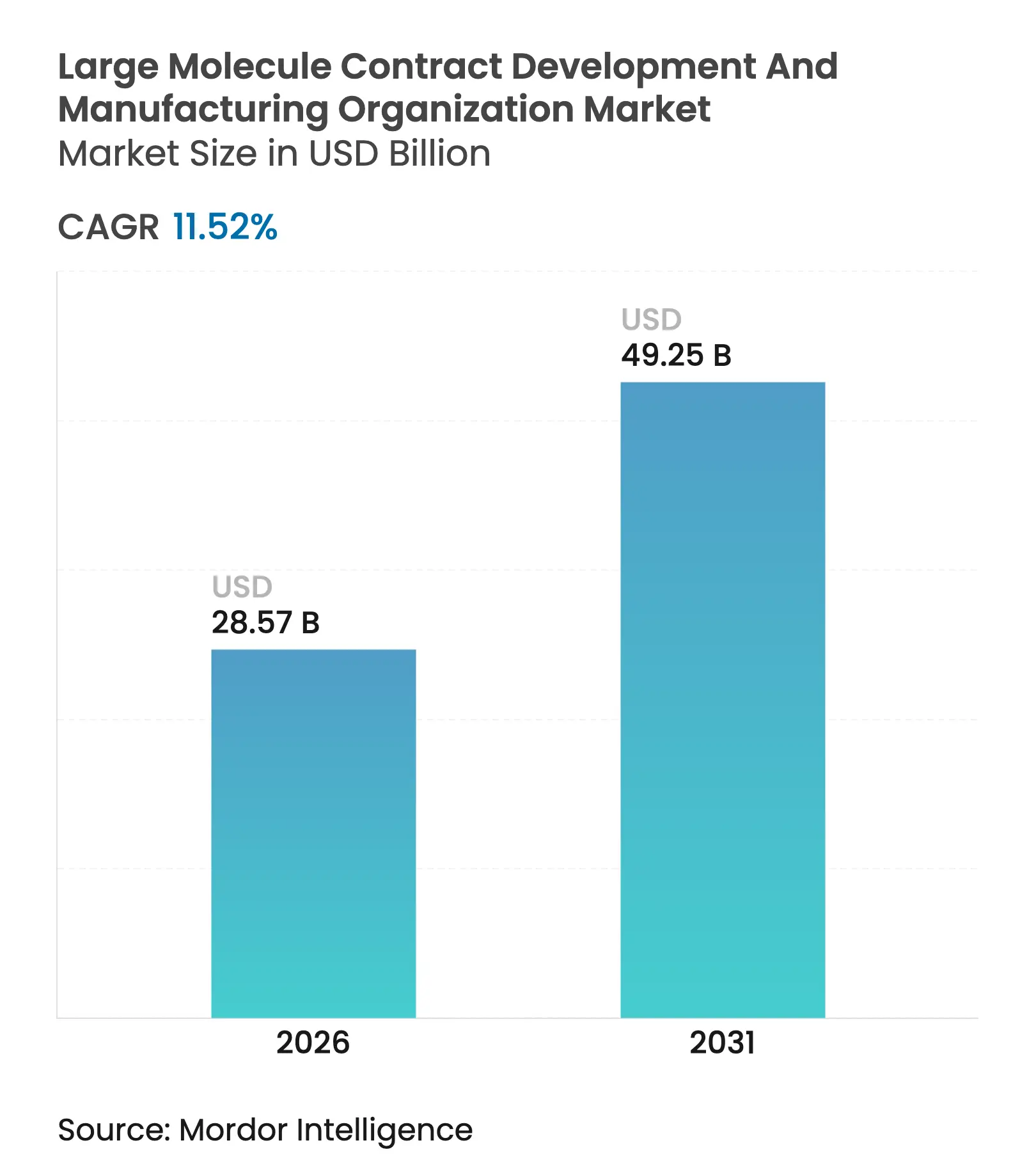

| Market Size (2026) | USD 28.57 Billion |

| Market Size (2031) | USD 49.25 Billion |

| Growth Rate (2026 - 2031) | 11.52 % CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Large Molecule Contract Development And Manufacturing Organization Market Analysis by Mordor Intelligence

The Large molecule contract development and manufacturing organization market size is expected to grow from USD 25.62 billion in 2025 to USD 28.57 billion in 2026 and is forecast to reach USD 49.25 billion by 2031 at 11.52% CAGR over 2026-2031. Rising approvals for complex biologics, wider biosimilar adoption, and a clear preference for asset-light manufacturing strategies keep outsourced demand climbing. Big-pharma divestment of legacy sites, plus record venture funding for emerging biotechs, funnel a steady pipeline of large-molecule programs toward specialist partners. Digitalized single-use capacity coming online in Asia-Pacific removes location barriers and gives sponsors cost-effective scale-up options. Intensifying regulatory scrutiny meanwhile favors providers with proven quality records, further concentrating activity among well-capitalized global players.

Key Report Takeaways

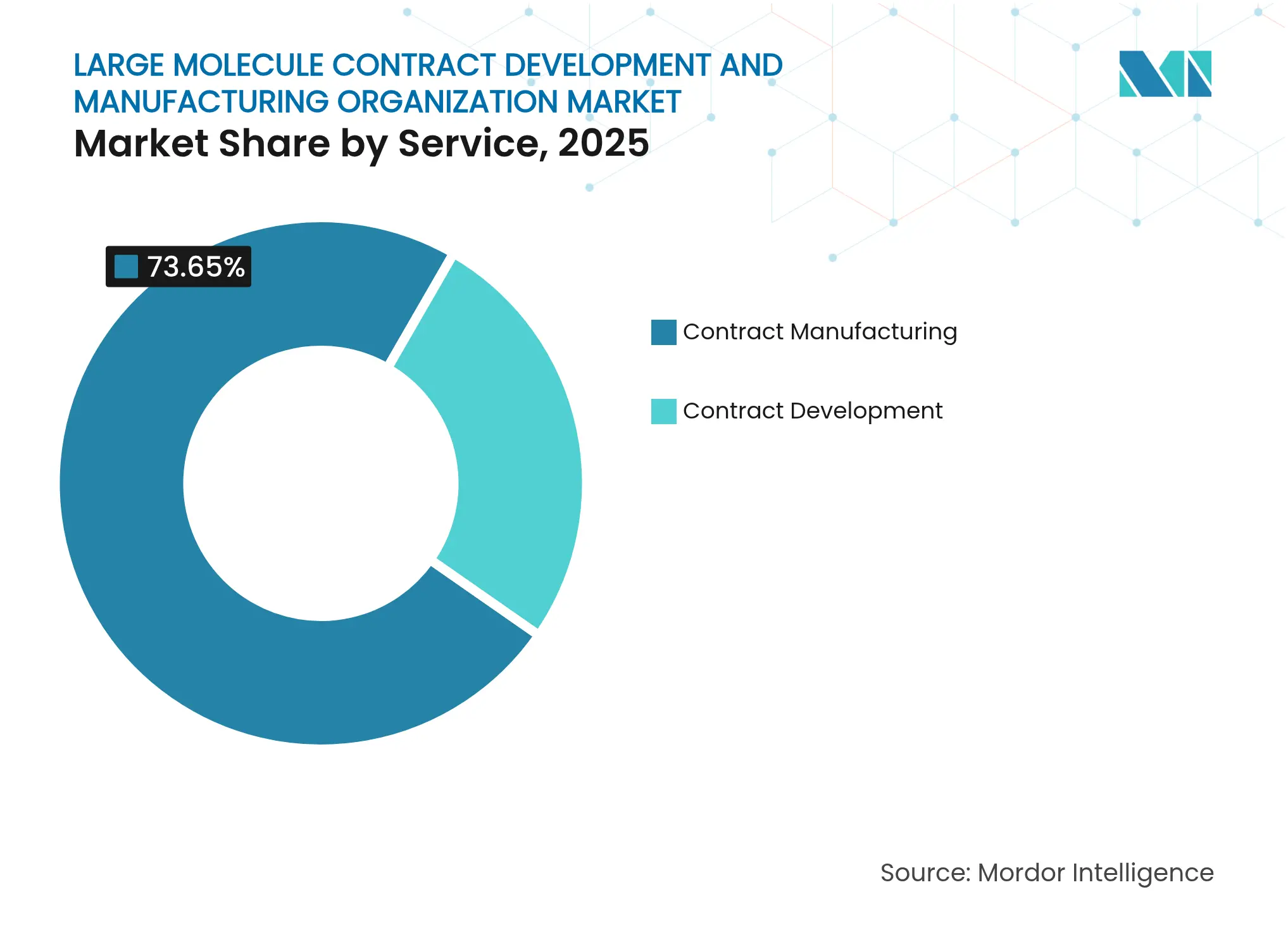

- By service, contract manufacturing led with 73.65% of large molecule contract development and manufacturing organization market share in 2025, while Contract Development is projected to grow at a 13.54% CAGR to 2031.

- By source, mammalian expression platforms accounted for 62.85% of the large molecule contract development and manufacturing organization market size in 2025; microbial systems are set to expand at an 17.48% CAGR through 2031.

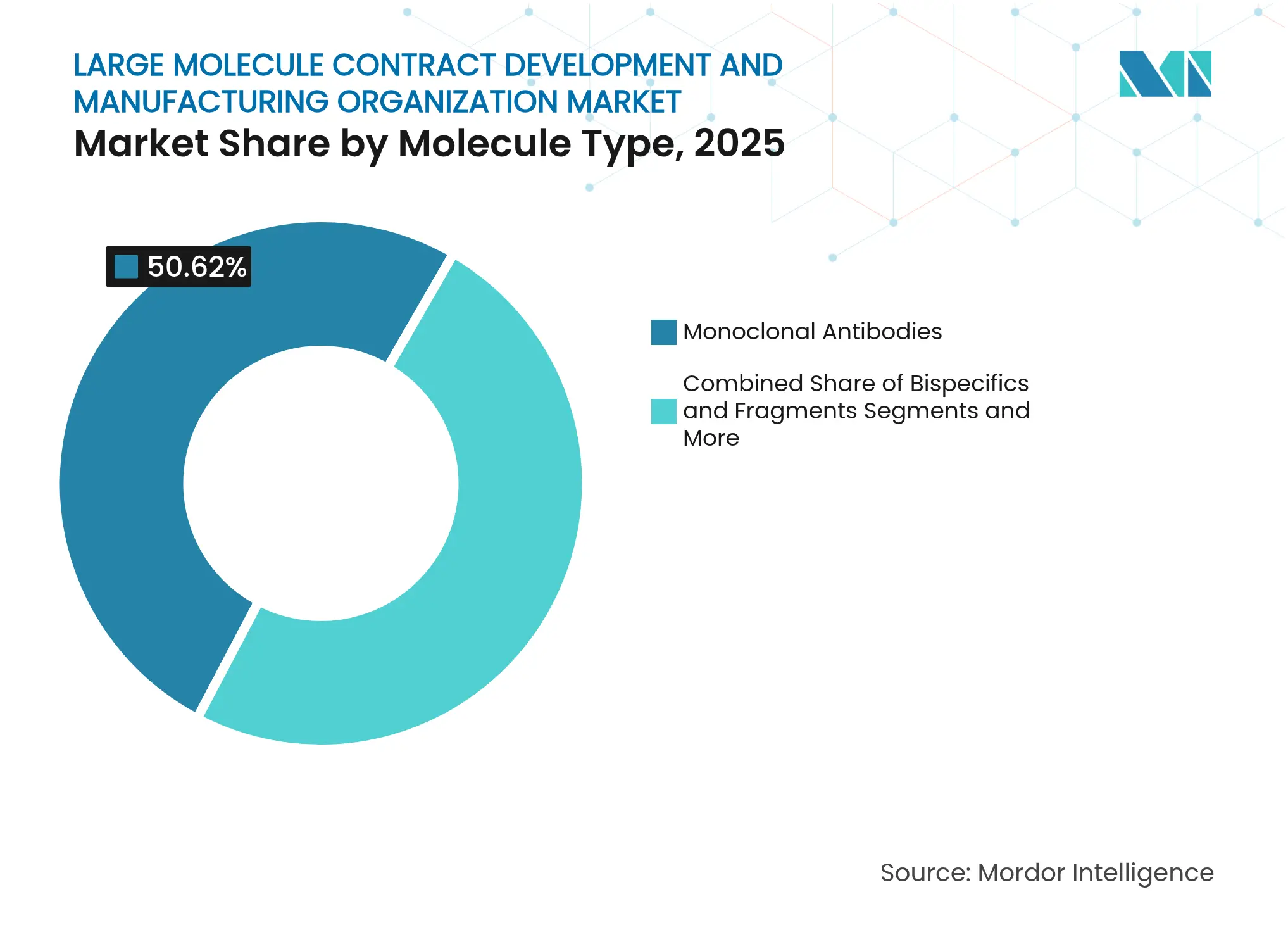

- By molecule type, monoclonal antibodies represented 50.62% revenue share in 2025; RNA therapeutics registered the fastest rise at 15.98% CAGR to 2031.

- By end user, large pharmaceutical companies generated 69.72% of demand in 2025, and research institutes and academics are advancing at a 11.86% CAGR up to 2031.

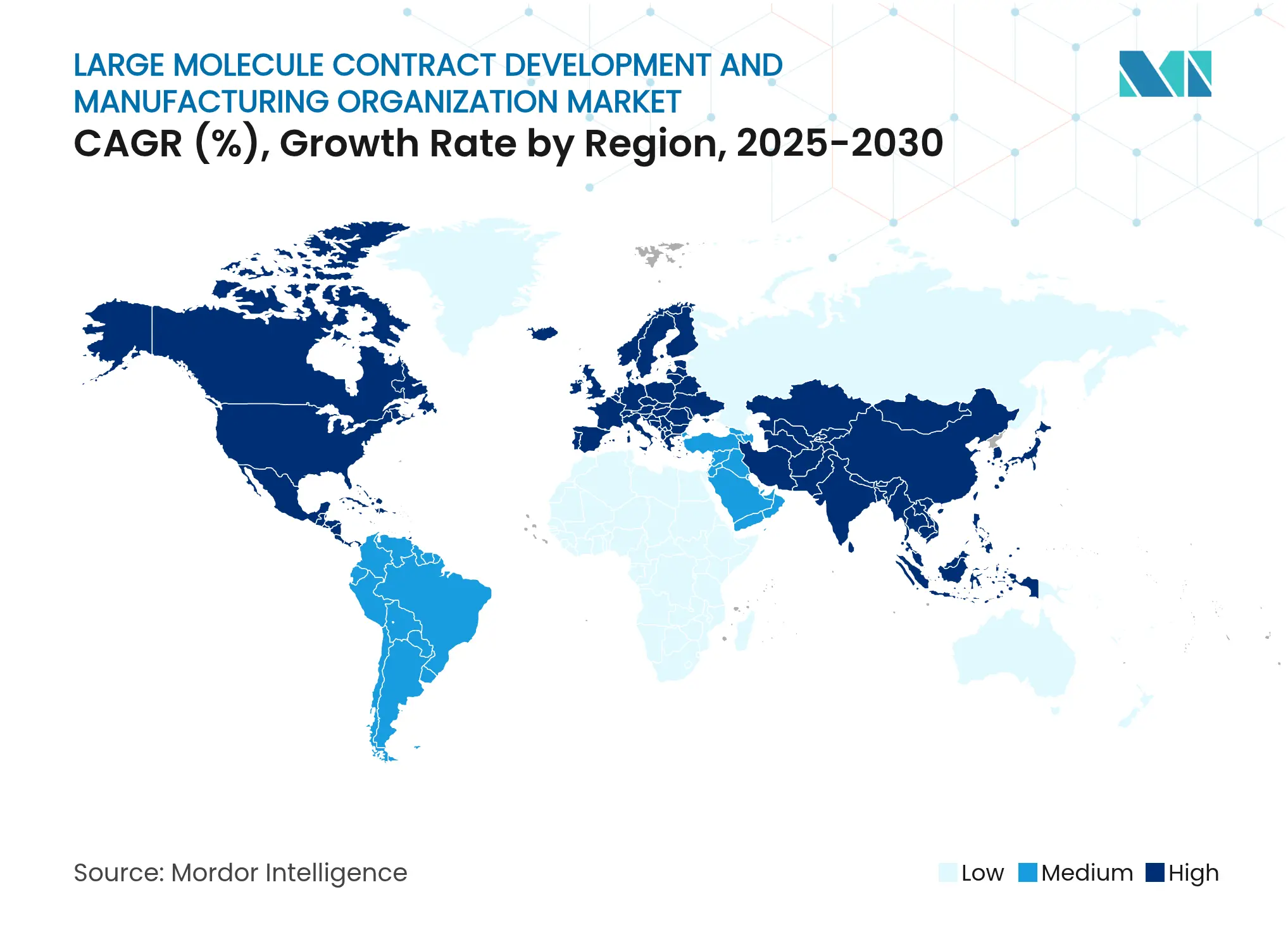

- By geography, North America held 36.21% revenue share of the large molecule contract development and manufacturing organization market in 2025; Asia–Pacific is projected to grow at a 13.24% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Large Molecule Contract Development And Manufacturing Organization Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Regulatory-driven large-molecule approvals Regulatory-driven large-molecule approvals | +2.80% | Global, with accelerated pathways in US and EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.80% | Geographic Relevance:Global, with accelerated pathways in US and EU | Impact Timeline:Medium term (2-4 years) |

Accelerating demand for biologics & biosimilars Accelerating demand for biologics & biosimilars | +3.20% | Global, strongest in North America and Europe | Long term (≥ 4 years) | |||

Big-pharma R&D shift toward complex modalities Big-pharma R&D shift toward complex modalities | +2.10% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

AI-enabled bioprocess optimization unlocking idle capacity AI-enabled bioprocess optimization unlocking idle capacity | +1.40% | Developed markets initially, scaling globally | Long term (≥ 4 years) | |||

Plug-and-play single-use facilities in emerging regions Plug-and-play single-use facilities in emerging regions | +1.80% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) | |||

Increasing outsourcing by cash-constrained biotech start-ups Increasing outsourcing by cash-constrained biotech start-ups | +1.50% | Global, concentrated in biotech hubs | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Regulatory-driven Large-molecule Approvals

Streamlined pathways such as the FDA breakthrough and PRIME in Europe shorten review times for novel biologics, lifting immediate outsourcing needs once products clear Phase III.[1]Nature Biotechnology, “FDA’s 2023 drug approvals reach record high,” nature.com Over half of 2024’s CDER approvals targeted rare diseases, creating sudden scale-up requirements that many sponsors meet through the large-molecule contract development and manufacturing organization market. EMA plans to relax biosimilar comparative efficacy rules in 2025 will further compress development spend and steer extra filings toward trusted CDMOs. Inspection mutual-recognition pacts between the FDA and Swissmedic help multinational providers avoid duplicate audits, saving time that can instead be used for rapid capacity deployment.

Accelerating Demand for Biologics & Biosimilars

Therapeutic monoclonal antibody sales are tracking toward USD 315 billion by 2025, doubling the manufacturing workload for downstream purification suites. Contract manufacturers and hybrid operators are forecast to control 54% of global biologics capacity by 2028, compared with 43% in 2024, underscoring the depth of outsourcing migration. Patent expiries on 117 originator biologics through 2028 unlock multibillion-dollar biosimilar opportunities, encouraging established generic firms to secure quick-turn production slots. Emerging formats such as bispecific antibodies already represent one quarter of fresh approvals and require intricate process platforms that favor mature CDMOs.

Big-pharma R&D Shift Toward Complex Modalities

More than 1,200 active cell- and gene-therapy studies place specialized manufacturing high on big-pharma sourcing agendas. Flagship deals, including Roche’s USD 1.2 billion site sale to Lonza, illustrate the pivot away from owning hard assets toward flexible, vendor-housing models. By handing off routine commercial production, pharma firms unlock capital for discovery pipelines yet still guarantee global supply through master service agreements. CDMOs respond by building universal viral-vector suites and closed-system autologous lines, sealing multi-year volume guarantees linked to new modalities.

AI-enabled Bioprocess Optimization Unlocking Idle Capacity

Regulators now encourage continuous data-driven reviews, publishing guidance on AI models for critical quality-attribute prediction.[2]European Medicines Agency, “Reflection paper on artificial intelligence in medicinal products,” ema.europa.eu Providers adopting digital twins and machine-learning control loops report 15% higher yields and 30% shorter tech-transfer cycles. Improved run-rate efficiency delays expensive greenfield builds while still absorbing extra programs, translating to a +1.4% growth boost. Early adopters in the Large molecule contract development and manufacturing organization market also differentiate on faster batch-release times, attracting sponsors under market-launch pressure.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Heightened cGMP / validation burden Heightened cGMP / validation burden | -1.90% | Global, most acute in EU and US | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.90% | Geographic Relevance:Global, most acute in EU and US | Impact Timeline:Short term (≤ 2 years) |

Volatile resin & raw-material supply chains Volatile resin & raw-material supply chains | -1.30% | Global, concentrated in Asia-Pacific sourcing | Medium term (2-4 years) | |||

Bioprocess-engineer talent crunch Bioprocess-engineer talent crunch | -1.10% | Developed markets primarily, emerging in APAC | Long term (≥ 4 years) | |||

Long lead-times for large-scale bioreactor equipment Long lead-times for large-scale bioreactor equipment | -0.80% | Global, acute in high-growth regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Heightened cGMP / Validation Burden

Revised EU GMP Annex 1 forces wider adoption of isolators and advanced contamination-control strategy mapping, pushing smaller providers toward costly retrofits.[3]Pharmaceutical Online, “FDA Form 483 trends 2023-2024,” pharmaceuticalonline.com Source: PDA, “EU GMP Annex 1 implementation guide,” pda.org FDA inspection data show a rise in Official Action Indicated letters, especially among first-time biologics sites. As regulators expect thorough cleaning validation studies and end-to-end electronic batch records, compliance budgets swell, trimming the market CAGR by -1.9%. Providers with pre-existing barrier isolators and mature quality-management systems secure an advantage while late movers risk warning letters and project losses.

Volatile Resin & Raw-material Supply Chains

Protein A resin throughput tightens as upstream titres climb, while sodium hypochlorite feedstock faces shipping bottlenecks from Asia. Over 75% of global API precursors still reside outside the US, leaving Western CDMOs exposed to geopolitical friction. Many firms double safety-stock levels, tying up working capital and squeezing margins. Dual-sourcing drives fresh supplier audits and comparative validation batches, extending launch schedules.

Segment Analysis

By Service: Manufacturing Dominance Drives Outsourcing Shift

Contract Manufacturing generated 73.65% of revenue in 2025, underscoring its central position within the large-molecule contract development and manufacturing organization market. The segment benefits from high entry barriers linked to stainless-steel installation, aseptic suites, and intensive validation cycles. Sponsors favor external partners to avoid multi-hundred-million-dollar capital outlays and to access immediate regulatory credibility. Contract Development, though smaller, records a 13.54% forecast CAGR as complex modalities require deeper cell-line and process engineering know-how. Pre-clinical clients increasingly sign multi-program master agreements that span tox-grade to commercial launch, reinforcing integrated service pull.

Firms are blending development and production scopes to secure lifetime value, with commercial downstream exclusivity often embedded in Phase I tech-transfer contracts. AI-assisted clone selection cuts timelines by weeks, while perfusion-based upstream strategies drop the cost of goods for low-volume rare-disease biologics. Collectively, these improvements keep the large molecule contract development and manufacturing organization market anchored by manufacturing while fueling rapid growth for development-centric offerings.

Note: Segment shares of all individual segments available upon report purchase

By Source: Mammalian Systems Lead Despite Microbial Surge

Mammalian culture retained a 62.85% share in 2025, thanks to robust glycosylation, but innovations in synthetic biology help microbial hosts score an 17.48% CAGR through 2031. Perfusion intensification in mammalian suites doubles titre without expanding footprint, bolstering capacity use across multinationals. Continuous downstream capture setups harmonize well with perfusion feeds, boosting resin productivity and lowering buffer volumes. Microbial systems gain traction for non-glycosylated proteins and for lower molecular-weight antibody fragments, where rapid fermentation and lower media costs deliver competitive economics.

Coproduction facilities capable of switching between CHO and E. coli runs widen client choice, reinforcing the large-molecule contract development and manufacturing organization's market value proposition. Plant and insect cell lines remain niche yet vital for pandemic-readiness vaccines, drawing strategic governmental contracts that guarantee baseline utilization and de-risk capital projects.

By Molecule Type: Antibodies Dominate While RNA Therapeutics Accelerate

Monoclonal antibodies held a 50.62% share in 2025 and continue to anchor commercial capacity bookings. Biosimilar waves in oncology and immunology extend product life cycles and maintain high clone numbers per facility. Bispecific constructs add complexity but piggyback on established antibody infrastructure, deepening reliance on experienced CDMOs. RNA therapeutics, scaling at 15.98% CAGR, present unique lipid-nanoparticle formulation needs that stretch conventional fill-finish lines. Providers upgrading to microfluidic mixers capture this expanding niche within the Large molecule contract development and manufacturing organization market.

Gene-editing payloads and oncolytic vectors demand vector-specific suites with nanofilter-based viral-clearance steps. Advanced therapy requirements solidify demand for segregated Grade C cleanrooms and drive premium pricing models, offsetting the smaller batch sizes tied to personalized medicine.

Note: Segment shares of all individual segments available upon report purchase

By End User: Large Pharma Leads While Biotech Drives Growth

Large pharmaceutical companies supplied 69.72% of spending in 2025, leveraging multi-year capacity reservations to protect blockbuster launch timelines. Outsourcing complements their strategy of focusing capital on discovery while ensuring robustness in global supply. Small and mid-size biotech firms, expanding at 11.86% CAGR, rely on outsourced platforms from cell-line construction through commercial distribution. Virtual biotech models, staffed primarily by program managers, further widen the client funnel for the large-molecule contract development and manufacturing organization industry.

Academic institutes continue to advance proof-of-concept material, often under tech-transfer arrangements that later flow into full-scale runs. This collaboration pipeline cements long-term utilization for CDMOs that can flex through Phase I micro-batches to 20,000-liter commercial bioreactors without tech-transfer setbacks.

Geography Analysis

North America accounted for the largest regional portion of the large molecule contract development and manufacturing organization market in 2025, propelled by steady biopharma R&D budgets and government incentives favoring domestic capacity. Investments such as FUJIFILM Diosynth’s USD 1.6 billion North Carolina site and Novo Nordisk’s USD 4.1 billion expansion sustain fresh job creation and ensure resilient supply chains. Regulatory proposals like the BIOSECURE Act may limit Chinese CDMO access, potentially rerouting new projects into US-based facilities and fortifying local order books. The region also benefits from a broad venture ecosystem, funding next-generation modalities that require rapid scale-up support.

Europe ranks second yet advances steadily on the back of regulatory harmonization and continued capital inflows. Lonza’s USD 1.2 billion acquisition of Genentech’s Vacaville site and Boehringer Ingelheim’s USD 811 million Austrian unit widens the continent’s high-titre fermenter portfolio. EMA relaxation of biosimilar comparability requirements and draft AI-use guidance increase development efficiency, making Europe a competitive destination for both early-stage and late-stage programs. The Large molecule contract development and manufacturing organization market size in Europe is projected to climb in line with modular capacity additions and supportive bioeconomy policies.

Asia-Pacific posts the fastest growth, stimulated by Samsung Biologics’ sixth-plant announcement and Lotte Biologics’ USD 3.4 billion Bio-Campus build. India’s CRDMO sector may reach USD 25 billion by 2035, championed by tax exemptions and fast-track environmental clearances. Chinese heavyweights like WuXi Biologics add integrated discovery-to-commercial offerings despite geopolitical risks, maintaining project inflow from domestic and emerging-market sponsors. Regional governments prioritize self-sufficiency in vaccine and biologics supply, providing anchor contracts that reinforce the large-molecule contract development and manufacturing organization market.

Middle East & Africa and South America, though smaller, register rising bids for localized advanced therapy manufacturing. Abu Dhabi’s partnership with Resilience and Brazil’s USD 1.09 billion Novo Nordisk injection facility illustrate the shift toward domestic bioproduction. Technology transfer clauses in these deals foster skill development and broaden long-term regional demand.

Competitive Landscape

Market Concentration

Industry consolidation is accelerating as mega-deals redistribute capacity. Novo Holdings' USD 16.5 billion purchase of Catalent and Lonza's uptake of the Vacaville plant together reallocate roughly one-fifth of global volume. Between 2017 and 2021, 244 M&A transactions reshaped service breadth, with buyers prioritizing cell- and gene-therapy competencies. The trend tightens competition, reducing small players' shelf life unless they carve high-value niches, such as messenger RNA or phage display libraries.

Technology investments define the current battleground. Leaders implement digital twins, closed-loop control software, and high-throughput process-development microreactors to cut cost-of-goods and turnaround times. Lonza's MODA-ES® digital platform and Samsung Biologics' 784,000-liter single-use fleet exemplify capacity married to automation. Such differentiation attracts long-term supply contracts, anchoring revenue streams across multiple product lifecycles within the Large molecule contract development and manufacturing organization market.

Smaller CDMOs increasingly specialize. Some adopt microbial-only microbial GMP suites for recombinant vaccines, while others build isolated Grade D plasmid facilities aimed at viral-vector producers. Strategic collaborations, like Agenus linking US biologics assets with Zydus Lifesciences' new BioCDMO arm, mirror a partnership model that blends Western regulatory track record with cost-advantaged geography. Collectively, these moves sustain a moderate-to-high concentration, yet still leave room for innovative entrants to secure footholds by mastering novel formats or underserved regional demand.

Large Molecule Contract Development And Manufacturing Organization Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Agenus and Zydus Lifesciences unveiled a USD 141 million collaboration covering botensilimab and balstilimab production. Agenus’ California plant catalyzed Zydus’ BioCDMO launch.

- April 2025: Thermo Fisher Scientific pledged USD 2 billion to expand US manufacturing and R&D over four years, including USD 1.5 billion for capital projects.

- April 2025: FUJIFILM Diosynth Biotechnologies and Regeneron inked a 10-year, USD 3 billion manufacturing agreement centered on FUJIFILM’s North Carolina mega-facility.

- April 2025: Novo Nordisk confirmed a USD 1.09 billion expansion of its Brazilian injectable-drug site to scale GLP-1 output.

Table of Contents for Large Molecule Contract Development And Manufacturing Organization Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Regulatory-Driven Large-Molecule Approvals

- 4.2.2Accelerating Demand For Biologics & Biosimilars

- 4.2.3Big-Pharma R&D Shift Toward Complex Modalities

- 4.2.4AI-Enabled Bioprocess Optimisation Unlocking Idle Capacity

- 4.2.5Plug-And-Play Single-Use Facilities In Emerging Regions

- 4.2.6Increasing Outsourcing By Cash-Constrained Biotech Start-Ups

- 4.3Market Restraints

- 4.3.1Heightened CGMP / Validation Burden

- 4.3.2Volatile Resin & Raw-Material Supply Chains

- 4.3.3Bioprocess-Engineer Talent Crunch

- 4.3.4Long Lead-Times For Large-Scale Bioreactor Equipment

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Segmentation

- 5.1By Service

- 5.1.1Contract Development

- 5.1.1.1Cell-Line Development

- 5.1.1.2Process Development

- 5.1.2Contract Manufacturing

- 5.1.2.1Pre-clinical

- 5.1.2.2Clinical

- 5.1.2.3Commercial

- 5.2By Source

- 5.2.1Mammalian

- 5.2.2Microbial

- 5.2.3Insect & Plant-based

- 5.3By Molecule Type

- 5.3.1Monoclonal Antibodies

- 5.3.2Bispecifics & Fragments

- 5.3.3Recombinant Proteins

- 5.3.4Vaccines

- 5.3.5Cell & Gene Therapies

- 5.3.6RNA Therapeutics

- 5.4By End User

- 5.4.1Pharmaceutical and Biotechnology Companies

- 5.4.2Research Institutes and Academics

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 6.3.1Lonza Group

- 6.3.2Samsung Biologics

- 6.3.3WuXi Biologics

- 6.3.4Thermo Fisher Scientific

- 6.3.5Catalent

- 6.3.6Rentschler Biopharma

- 6.3.7AGC Biologics

- 6.3.8Fujifilm Diosynth

- 6.3.9Boehringer Ingelheim

- 6.3.10Siegfried

- 6.3.11Recipharm

- 6.3.12Curia

- 6.3.13KBI Biopharma

- 6.3.14Syngene International

- 6.3.15Lotte Biologics

- 6.3.16Abzena

- 6.3.17Just - Evotec Biologics

- 6.3.18MilliporeSigma

- 6.3.19Eurofins Scientific

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Large Molecule Contract Development And Manufacturing Organization Market Report Scope

As per the scope of the report, a contract development and manufacturing organization (CDMO) is a company that provides a comprehensive range of services from drug development to manufacturing. CDMOs provide critical services by incorporating third-party projects and offering their knowledge, development, and manufacturing capabilities. This report focuses only on the outsourcing of development and manufacturing activities related to large molecules.

The large molecule contract development and manufacturing organization market is segmented by service, sources, end user, and geography. By services, the market is segmented into contract development and contract manufacturing. By contract development the market is further segmented as cell line development and process development. By contract manufacturing, the market is further segmented into clinical and commercial. By source, the market is segmented into mammalian, microbial, and other sources. By end user, the market is segmented into pharmaceutical and biotechnology companies and research institutes, and academics. By geography , the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers values in USD for the abovementioned segments. The report also covers the estimated market sizes and trends for 17 countries across major regions globally.