Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

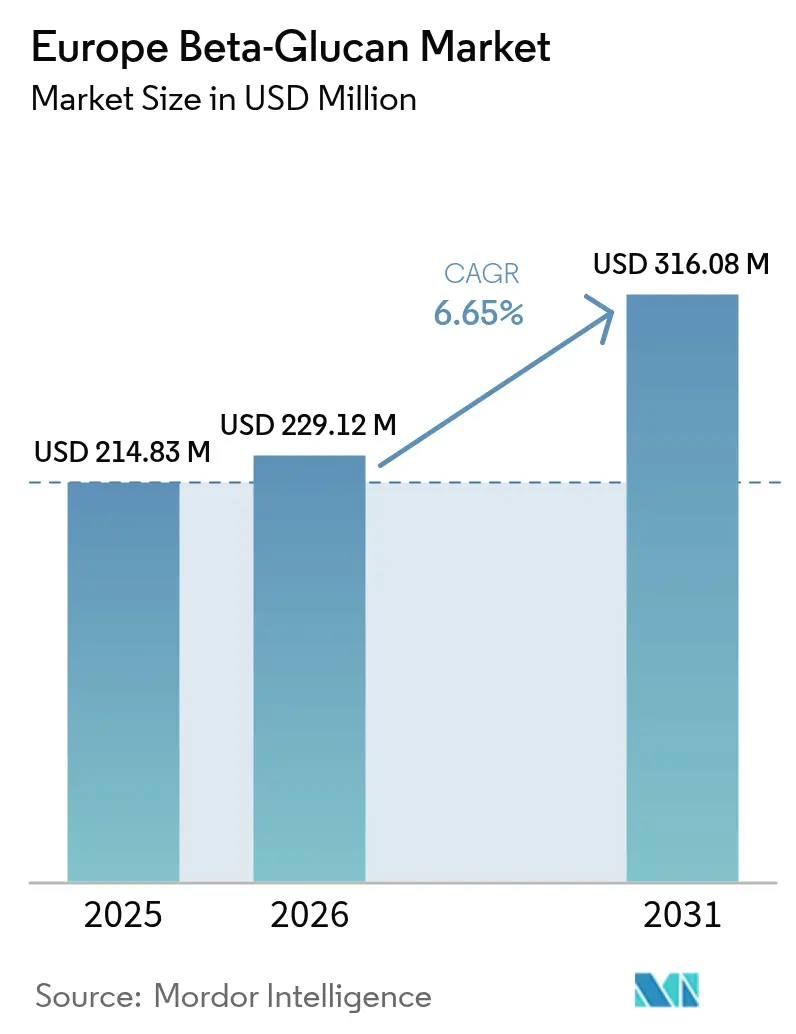

| Base Year Market Size (2025) | USD 214.83 Million |

| Market Size (2026) | USD 229.12 Million |

| Market Size (2031) | USD 316.08 Million |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Beta-Glucan Market Analysis by Mordor Intelligence

The Europe beta-glucan market size was valued at USD 214.83 million in 2025 and estimated to grow from USD 229.12 million in 2026 to reach USD 316.08 million by 2031, at a CAGR of 6.65% during the forecast period (2026-2031). Regulatory clarity from the European Food Safety Authority (EFSA)[1]Source: European Food Safety Authority (EFSA), "Approval of Microalgae Derived Beta-Glucan", www.ec.europea.eu, exemplified by the April 2024 approval of microalgae-derived beta-glucan, is lowering entry barriers for novel sources while widening application scope beyond cereal and yeast origins. Consumer demand for immunity, cardiovascular, and skin-health benefits is deepening penetration in foods, supplements, and personal-care items, allowing formulators to command premium shelf prices in a competitive retail environment. Mid-sized biotechnology firms are using proprietary extraction and purification technologies to create product differentiation, while large multinationals are scaling production lines through advanced automation to drive cost efficiencies and resilient supply chains. Although inconsistent raw-material quality and lengthy novel-food approvals continue to challenge smaller entrants, industry-wide investment in standardized analytical methods is improving batch-to-batch performance, thereby sustaining long-term market momentum.

Key Report Takeaways

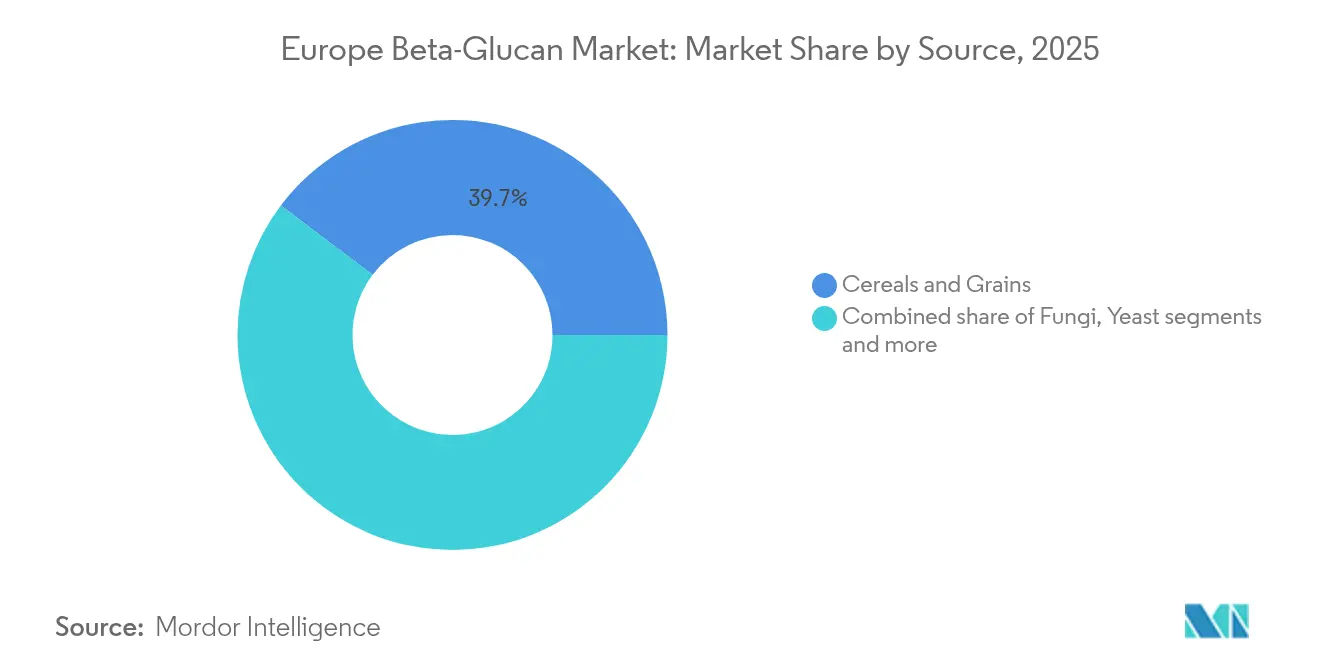

- By source, cereals and grains held 39.72% of the European beta-glucan market share in 2025, and fungi is projected to rise fastest at 8.62% CAGR through 2031.

- By category, soluble beta-glucans led with a 69.62% share in 2025; insoluble beta-glucans will post the strongest 8.92% CAGR through 2031.

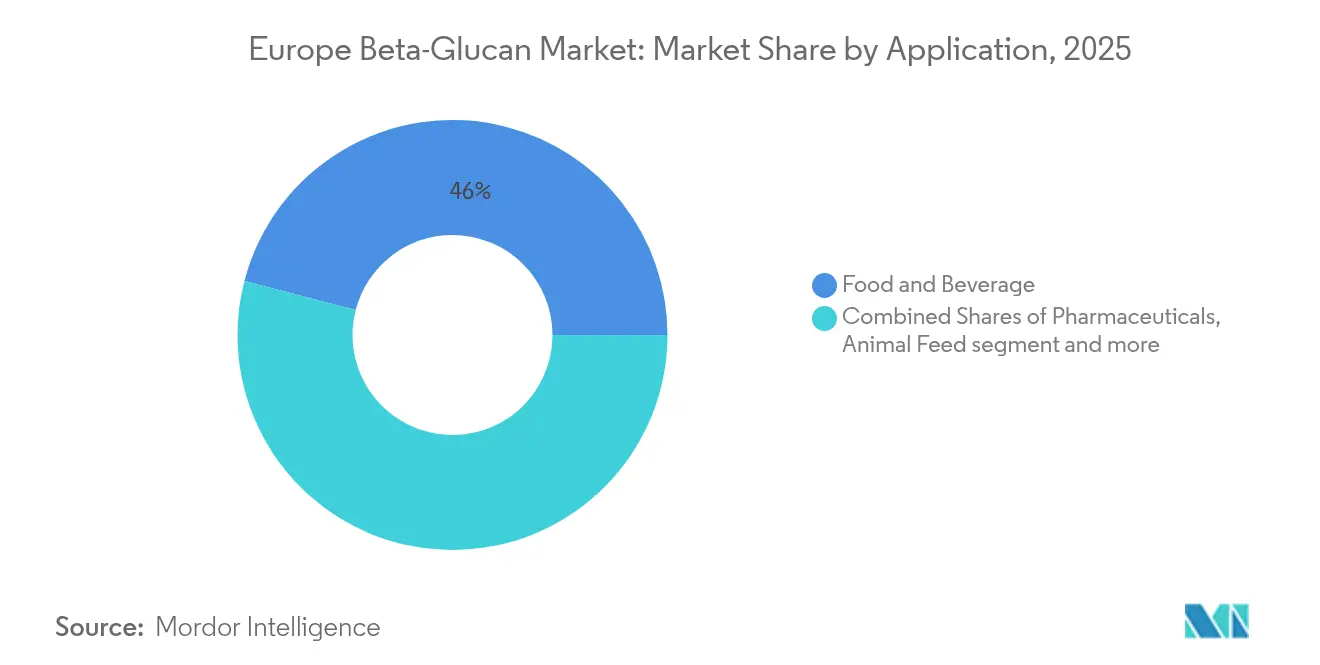

- By application, food and beverage accounted for 45.96% of the European beta-glucan market size in 2025, while personal care and cosmetics will climb at an 8.74% CAGR through 2031.

- By geography, the rest of Europe commanded a 38.21% share in 2025; Italy will register the highest 7.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Beta-Glucan Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer interest in immunity-enhancing functional foods | +1.2% | Global, strongest in Northern Europe | Short term (≤ 2 years) |

| Increasing pharmaceutical applications of fungal and yeast beta-glucans | +0.9% | Germany, France, Switzerland | Medium term (2-4 years) |

| Adoption in dairy alternatives and plant-based beverages | +0.8% | United Kingdom, Netherlands, Scandinavia | Short term (≤ 2 years) |

| Expanding consumer focus on heart health products | +0.7% | Europe-wide, particularly aging populations | Long term (≥ 4 years) |

| Rising demand for plant-based ingredients drives market growth | +0.6% | Western Europe, urban centers | Medium term (2-4 years) |

| Higher research and development investment to improve drug solubility and bioavailability | +0.4% | Germany, Switzerland, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Interest in Immunity-Enhancing Functional Foods

Post-pandemic health priorities have pivoted toward proactive immune support, with 58% of European shoppers buying functional products primarily for immunity benefits. Beta-glucan brands are capitalizing by integrating clinically backed ingredients into snack bars, powders, and ready-to-drink beverages, especially in Northern Europe, where the willingness to pay premium prices is highest. EFSA-approved health claims grant marketing confidence, while specialized yeast and oat fractions enable clean-label positioning across multiple food matrices. Ingredient suppliers have intensified consumer-education campaigns in retail and e-commerce channels, translating academic research into approachable messaging that resonates with health-conscious audiences. The trend is expected to sustain revenue growth in the European beta-glucan market as household penetration widens in both mass and specialty retail formats.

Increasing Pharmaceutical Applications of Fungal and Yeast Beta-Glucans

Drug developers are leveraging beta-glucan’s immunomodulatory and controlled-release properties to improve bioavailability in oncology, antifungal, and vaccine-adjuvant therapies. The European Medicines Agency’s[2]Source: European Medicines Agency, “Public Summary for Ibrexafungerp,” ema.europa.euorphan-drug designation for ibrexafungerp illustrates regulatory support for glucan-based therapeutics. German and Swiss firms are spearheading the scale-up of pharmaceutical-grade production, commanding price premiums that outstrip food-grade equivalents. The segment's key characteristics include standardized dosing, high purity levels, and thorough clinical validation. These attributes ensure consistent product quality and reliable therapeutic outcomes. The rigorous scientific approach and proven efficacy attract substantial venture capital funding and public-sector grants focused on addressing antimicrobial resistance and chronic diseases. The successful commercialization of products increases ingredient demand across pharmaceutical and nutraceutical applications. This market growth strengthens the position of fungi- and yeast-derived molecules in the European beta-glucan market, particularly in therapeutic and preventive healthcare solutions.

Adoption in Dairy Alternatives and Plant-Based Beverages

Europe’s plant-based beverage boom positions beta-glucan as a multifunctional ingredient that delivers creamy mouthfeel, viscosity control, and heart-health benefits. Oat-drink manufacturers in the UK and Scandinavia are incorporating oatwell-branded beta-glucan to substantiate on-pack cholesterol-reduction claims, differentiating their SKUs in a crowded shelf set. Processing advances in enzymatic hydrolysis are producing highly soluble fractions suitable for low-viscosity beverages, thereby overcoming historical formulation hurdles. Regulatory certainty around on-pack claims provides marketing leverage, and consumer preference for plant-based nutrition supports premium pricing. This driver will continue to stimulate demand for specialty beta-glucan fractions and promote cross-category innovation in the European beta-glucan market.

Expanding Consumer Focus on Heart-Health Products

An aging European demographic pushes cardiovascular wellness to the forefront, prompting high interest in pantry staples that reduce LDL cholesterol. EFSA recommends 3 g daily beta-glucan intake for cholesterol management, giving formulators a clear target for efficacy. New research on high-solubility fibers shows improved glucose regulation, broadening health-positioning angles beyond traditional cholesterol reduction.Healthcare providers are incorporating functional foods into preventive care protocols, which maintains consistent demand through supermarket and pharmacy distribution channels. The integration of these products into preventive healthcare strategies reflects a broader shift toward proactive health management. Companies offering beta-glucan products with effective dosage formulations are positioned to benefit from the growing European market's focus on preventive healthcare spending. This alignment with preventive health trends creates opportunities for manufacturers to develop innovative formulations that meet both clinical requirements and consumer preferences.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory hurdles and ingredient approval delays | -0.8% | Europe-wide, particularly novel sources | Medium term (2-4 years) |

| Inconsistent performance among different ingredient sources | -0.6% | Manufacturing-intensive regions | Short term (≤ 2 years) |

| Raw material supply chain challenges impact market growth | -0.5% | Northern Europe, cereal-producing regions | Short term (≤ 2 years) |

| Quality control challenges in product manufacturing | -0.4% | Germany, France, manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Hurdles and Ingredient-Approval Delays

While EFSA approvals provide a safety net, average 38-month review times burden innovators with high dossier-preparation costs, particularly for microalgae and bacterial sources. Post-Brexit divergence adds complexity, as the UK’s Nutrition and Health Claims Committee applies different evidence thresholds, creating fragmented market rules, according to the Government of UK[3]Source: GOV.UK, “UK Nutrition and Health Claims Committee 2024 Opinions,” gov.uk. Small biotechnology companies experience significant financial constraints and operational challenges during the lengthy regulatory approval process, giving larger competitors with substantial compliance budgets and established resources a distinct competitive advantage in the market. Companies that successfully receive regulatory approval gain valuable multi-year market exclusivity rights, as demonstrated by Kemin's five-year protection period for its Euglena-based BetaVia product. This exclusivity period enabled Kemin to establish early market leadership and maintain a strong position in the European beta-glucan segment, highlighting the importance of securing regulatory approvals in the biotechnology industry.

Inconsistent Performance Among Different Ingredient Sources

Weather variations and processing methods significantly affect beta-glucan content in cereal crops, creating substantial challenges for food manufacturers in maintaining consistent specifications. Thermal processes, particularly pressure cooking, decrease functional viscosity, which directly impacts the efficacy of health claims in final products. Suppliers lacking advanced analytical laboratories encounter significant difficulties in ensuring product consistency across batches, leading brand owners to increasingly select vertically integrated or thoroughly audited supply partners. These ongoing challenges drive substantial interest in controlled microalgae and fungal fermentation systems that provide enhanced parameter management and consistent output quality. Additionally, these market dynamics encourage extensive investment in rapid-testing technologies throughout the European beta-glucan market, enabling better quality control and regulatory compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Cereals and Grains Dominance Faces Biotechnology Challenge

Cereal and grains commanded 39.72% of the Europe beta-glucan market share in 2025 due to entrenched oat and barley supply chains and strong consumer familiarity with grain-based nutrition. Fungal beta-glucans, though smaller in scale, are on track for 8.62% CAGR growth as controlled indoor cultivation delivers predictable yields with elevated purity. The Europe beta-glucan market size for fungal sources is projected to expand materially as pharmacopoeia-grade demand gains traction in Germany and Switzerland. Yeast sources benefit from pharmaceutical validation and consistent fermentation outputs, reinforcing interest from pharma ingredient buyers. Meanwhile, microalgae have begun to commercialize following EFSA’s 2024 nod, signaling further diversification and supply-chain resilience. Extraction innovation, like ultrasound-assisted autolysis, achieving 41.34% yield from winery yeast lees, exemplifies circular-economy potential that appeals to ESG-conscious manufacturers.

Competitive intensity within cereal supply is rising as the BARLEYboost consortium refines milling methods that could lift barley consumption by 100,000 t annually in the EU, thereby safeguarding beta-glucan supply amid climate variability. Concurrently, biotechnology startups are exploring Agrobacterium pusense and other bacterial candidates, anticipating novel-food status and opening new revenue streams. The interplay between tradition and innovation therefore defines the source landscape and will continue to shape procurement strategies in the Europe beta-glucan market.

By Category: Soluble Beta-Glucans Lead, While Insoluble Variants Show Strong Growth

Soluble fractions contributed 69.62% of 2025 revenue thanks to over three decades of cholesterol-lowering science and EFSA-approved heart-health claims. They maintain strong institutional acceptance, enabling formulators to hit 3 g daily dosage targets efficiently. Insoluble segment is projected to grow at 8.92% CAGR to 2031 on the back of novel texturizing roles and their incorporation into sustained-release nutraceutical tablets. High-shear dispersion and enzymatic tailoring are blurring traditional solubility lines, allowing developers to fine-tune viscosity without compromising digestibility.

Clinical studies on high-solubility variants demonstrate elevated glucose-regulation efficacy at lower viscosity, making them attractive for ready-to-drink beverages where mouthfeel remains critical. Meanwhile, insoluble derivatives are gaining traction in bakery, meat analogues, and wound-care dressings where water-binding is a key performance metric. These dual growth pathways ensure that both categories will coexist as distinct yet complementary offerings, thereby extending addressable sectors for the Europe beta-glucan market.

By Application: Food and Personal Care Lead Beta-Glucan Market Growth

Food and beverage applications maintained a dominant 45.96% revenue share in 2025, building on established cereal processing capabilities and consumer acceptance of oat-based health benefits. Personal care applications are projected to grow at 8.74% CAGR, driven by clinical evidence supporting beta-glucan's anti-wrinkle and wound-healing properties, aligning with European consumer preferences for dermocosmetic products. The ingredient has gained prominence in premium moisturizers and after-sun formulations, reflecting the broader industry shift toward natural active ingredients.

The pharmaceutical segment commands premium pricing through the incorporation of pharmaceutical-grade beta-glucan in therapeutic applications and drug-delivery systems. The animal feed segment maintains steady demand, as beta-glucan supplementation enhances gut immunity in poultry and swine production, supporting European initiatives to reduce antibiotic use. New applications, including biodegradable packaging, showcase beta-glucan's versatility and position it favorably under emerging sustainability regulations. These diverse applications demonstrate the expanding opportunities within the European beta-glucan market.

Geography Analysis

Rest of Europe held 38.21% of 2025 turnover due to a mosaic of small yet dynamic markets, from Switzerland’s pharma-focused demand to Poland’s rising functional-food manufacturers. The region’s fragmented regulatory regimes allow agile players to pilot new formats and niche positioning strategies without directly confronting the consolidated retail environments of France or Germany. Switzerland leads in pharmaceutical-grade formulations as high-margin hospital channels adopt beta-glucan adjunctive therapies. Austria and the Nordics drive organic and sustainable sourcing, increasing demand for traceable microalgae solutions.

Italy is set to advance at 7.94% CAGR through 2031 as cultural alignment with functional staples and public funding for Mediterranean-diet enhancement spur product innovation. The EU-backed Mush-Med project places Italian mills and bakeries at the forefront of mushroom-based glucan integration, creating regional clusters around Bologna and Parma. This collaborative ecosystem offers SMEs access to shared R&D infrastructure and rapid scale-up pathways, consolidating Italy’s strategic importance within the European beta-glucan market.

Germany, France, and Spain remain volume anchors. Germany’s pharma heavyweights insist on narrow quality specifications, encouraging suppliers to upgrade QC infrastructure. French dermocosmetic brands are infusing beta-glucan into anti-aging lines, reinforcing prestige positioning at pharmacies and beauty retailers. Spain leverages agronomic conditions ideal for high-beta-glucan barley and oat varieties, underscoring potential to become a raw-material hub. The UK contends with dual regulatory tracks after Brexit, yet homegrown brands are crafting UK-specific dosing statements to maintain consumer trust under evolving local guidelines. Collectively, these national dynamics ensure geographic diversification of revenue streams throughout the Europe beta-glucan market.

Competitive Landscape

The market is moderately concentrated, where multinational companies and biotech firms compete based on source materials, product categories, and applications. Companies differentiate themselves through various strategies and capabilities in this competitive environment. Tate & Lyle demonstrates the importance of scale economies through its tenfold capacity expansion using ABB robotics, which helps manage raw material cost fluctuations. Kerry Group markets Wellmune as an immune health ingredient backed by clinical studies, while DSM-Firmenich and Givaudan incorporate beta-glucan into their broader specialty ingredient portfolios to enhance cross-selling opportunities.

Companies gain competitive advantages through proprietary extraction methods and successful novel food registrations. The regulatory landscape plays a crucial role in determining market success, as demonstrated by Kemin's five-year exclusive rights for its algae-derived BetaVia. Smaller companies like COSCIENS Biopharma use advanced technologies such as pressurized gas expansion (PGX) to develop specialized medical-grade powders with anti-fibrotic properties. The development of innovative technologies and processes continues to shape the competitive dynamics of the market.

Biotech companies increasingly form partnerships with contract manufacturers to accelerate product development and maintain quality standards. These collaborations help organizations overcome technical challenges and meet market demands more effectively. In the European beta-glucan market, supply chain stability has become a key differentiator as companies navigate climate-related challenges. The ability to manage geopolitical tensions affecting raw material supply has emerged as a critical success factor for market participants.

Europe Beta-Glucan Industry Leaders

-

Tate & Lyle PLC

-

Kerry Group PLC

-

The Merck Group

-

DSM-Firmenich AG

-

Givaudan S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Tate & Lyle announced a strategic partnership with BioHarvest to develop next-generation plant-based ingredients using botanical synthesis technology, enabling sustainable production of non-GMO plant-derived ingredients without traditional agricultural constraints. The collaboration aims to create more affordable and accessible ingredients for the food and beverage industry

- November 2024: Tate & Lyle completed the USD 1.8 billion acquisition of CP Kelco, creating a leading global specialty food and beverage solutions business with enhanced capabilities in pectin and nature-based ingredients. The merger positions the combined entity to better serve consumer demands for healthier and sustainable food options.

- June 2024: CreaNutrition, a Swiss-based Oat brand specialist, was granted the approval of its beta-glucan claim in its products. The claim was approved by the French Food and Health Safety Agency

Europe Beta-Glucan Market Report Scope

The Europe beta-glucan market is segmented by category that includes soluble and insoluble. The market is divided based on source into cereals, yeast, mushrooms and other sources. Based on application, the market is divided into food and beverages, healthcare and dietary supplements and other applications. The food and beverages section is further divided into baked goods, confectionery, dairy, beverages, snacks, and other products. The healthcare and dietary supplements section is also bifurcated in infant nutrition and others. The study also involves the analysis in regions such as United Kingdom, Germany, France, Italy, Spain, Russia and rest of Europe.

By Source

| Cereals and Grains |

| Fungi |

| Yeast |

| Seaweed and Microalgae |

| Others |

By Category

| Soluble |

| Insoluble |

By Application

| Food and Beverage | Bakery and Confectionary |

| Beverage | |

| Snacks | |

| Dairy and Dairy Products | |

| Others | |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Animal Feed | |

| Others |

By Geography

| United Kingdom |

| Germany |

| Spain |

| France |

| Italy |

| Russia |

| Rest of Europe |

| By Source | Cereals and Grains | |

| Fungi | ||

| Yeast | ||

| Seaweed and Microalgae | ||

| Others | ||

| By Category | Soluble | |

| Insoluble | ||

| By Application | Food and Beverage | Bakery and Confectionary |

| Beverage | ||

| Snacks | ||

| Dairy and Dairy Products | ||

| Others | ||

| Personal Care and Cosmetics | ||

| Pharmaceuticals | ||

| Animal Feed | ||

| Others | ||

| By Geography | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe beta-glucan market?

The market stands at USD 229.12 million in 2026 and is projected to reach USD 316.08 million by 2031 at a 6.65% CAGR (2026-2031).

Which source is expanding fastest?

Fungal beta-glucans are forecast to grow at 8.62% CAGR to 2031, driven by controlled cultivation and pharmaceutical adoption.

How much of the market is held by soluble beta-glucans?

Soluble fractions captured 69.62% share in 2025, maintaining leadership through EFSA-approved cholesterol-reduction claims.

Which new application areas show promise beyond food?

Personal care and cosmetics will see the highest growth at 8.74% CAGR due to validated skin-repair and anti-aging benefits of beta-glucan actives.

Page last updated on: