Glucosamine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

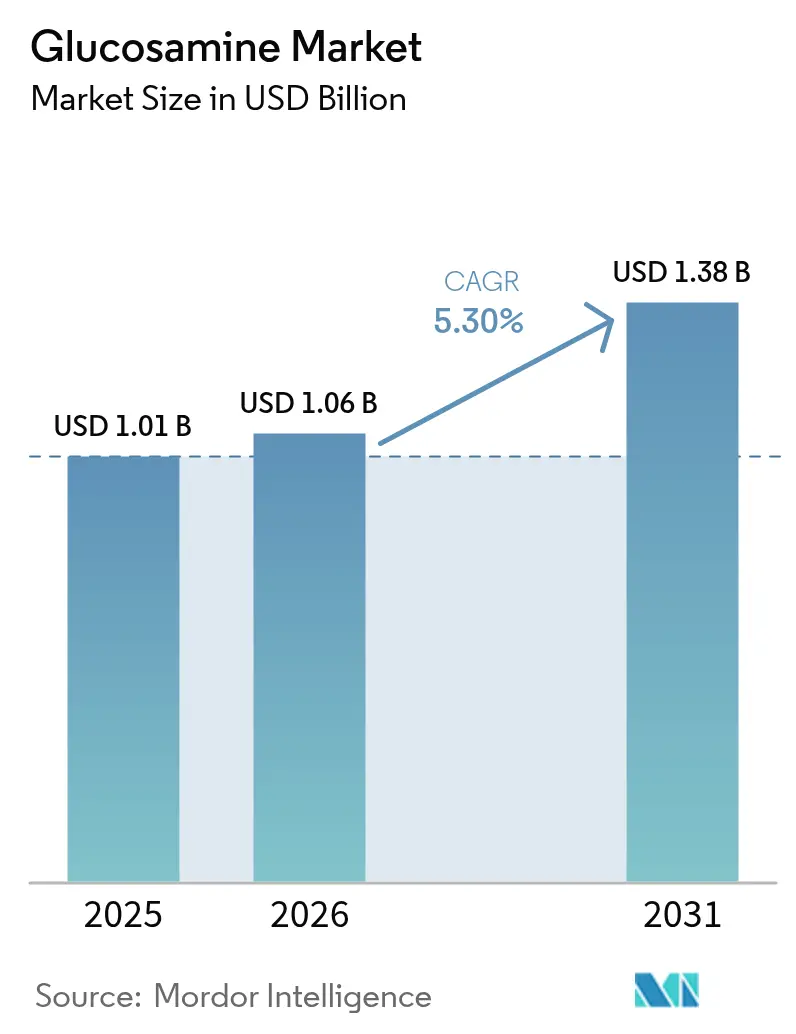

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Glucosamine Market Analysis by Mordor Intelligence

The glucosamine market size was valued at USD 1.01 billion in 2025 and estimated to grow from USD 1.06 billion in 2026 to reach USD 1.38 billion by 2031, at a CAGR of 5.30% during the forecast period (2026-2031). The market growth is driven by increased focus on healthy ageing, improved access to preventive healthcare, and evolving regulatory frameworks across regions. North America leads the market due to its established retail pharmacy network and high consumer awareness, while the Asia-Pacific region demonstrates the highest volume growth, supported by increasing disposable incomes and expanding nutraceutical distribution channels. Advancements in fermentation technology reduce allergen risks and ensure stable raw material supply, enhancing cost efficiency. Additionally, the FDA's revised notification procedures in March 2024 have reduced product launch timelines, enabling increased innovation in dosage forms and functional foods [1]US FDA, “New dietary ingredient notification guidance,” federalregister.gov.

Key Report Takeaways

- By type, glucosamine sulfate held 60.95% share of the glucosamine market in 2025, while glucosamine HCl is set to expand at an 8.79% CAGR to 2031

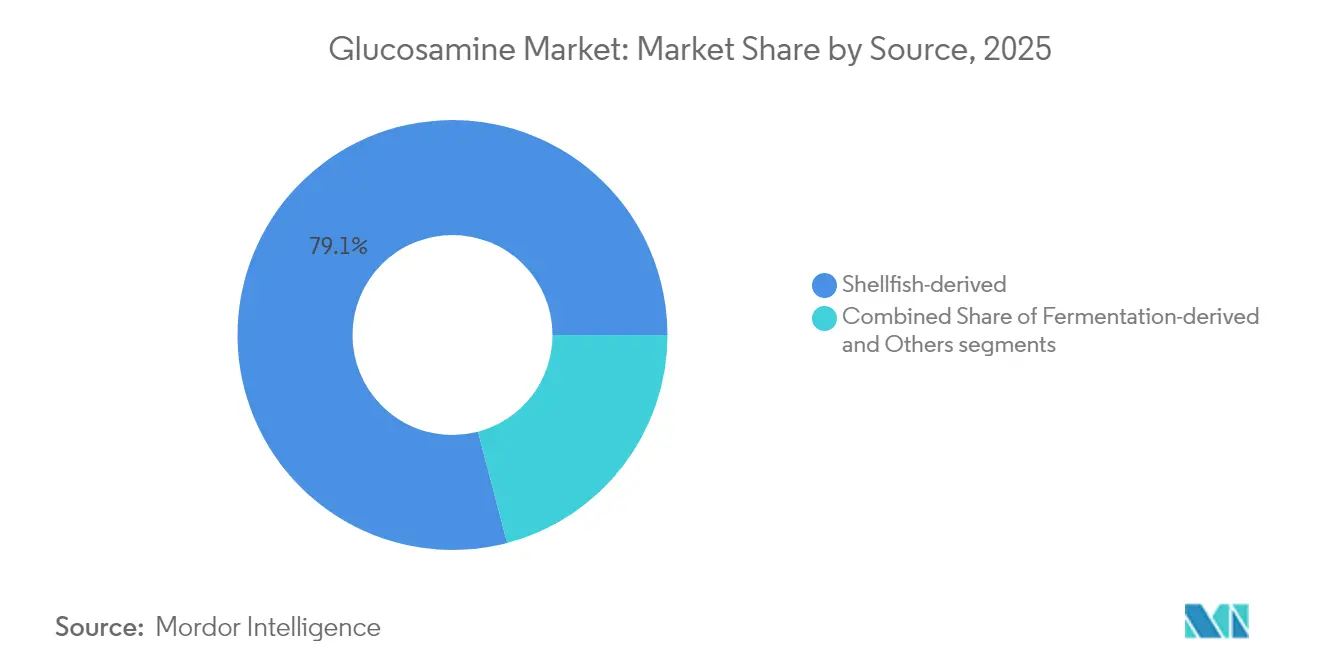

- By source, shellfish-derived glucosamine commanded 79.10% share in 2025; fermentation-derived variants are forecast to grow 7.74% annually through 2031

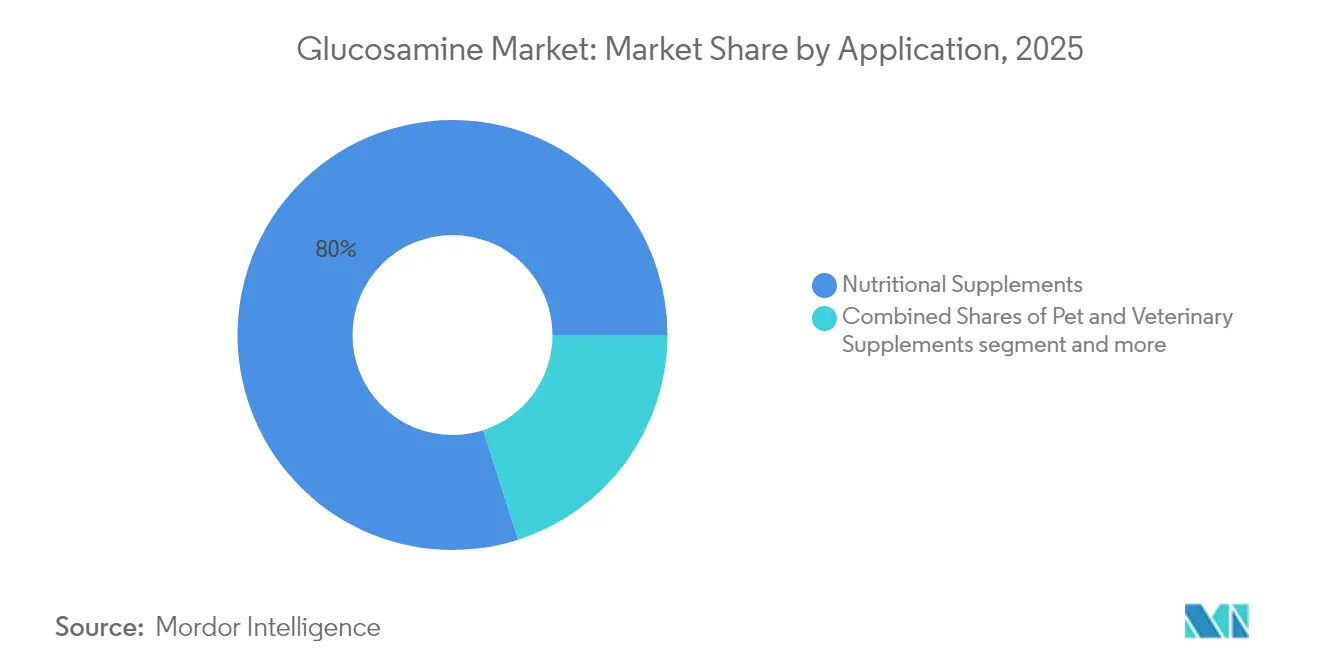

- By application, nutritional supplements captured 79.95% share of the glucosamine market in 2025; functional foods and fortified products record the quickest growth at 7.25% CAGR to 2031

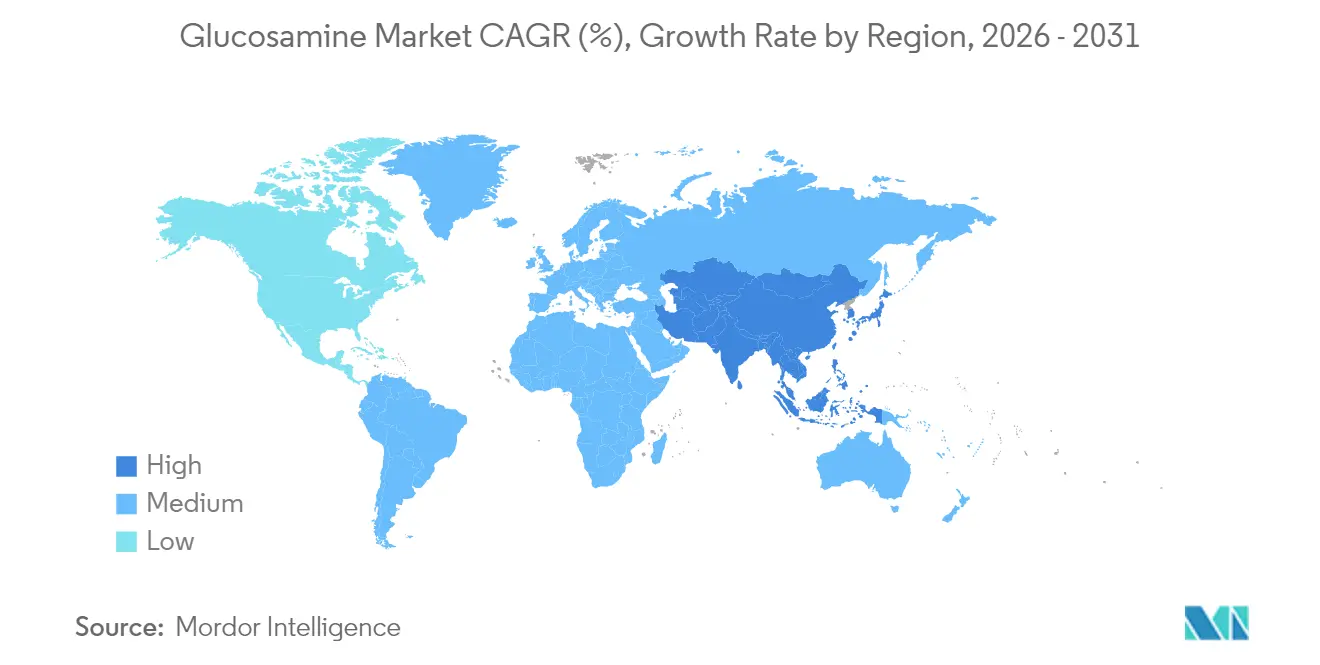

- By geography, North America led with 38.85% revenue share in 2025; Asia-Pacific is projected to post the highest regional CAGR of 7.99% during 2026-2031

- The top players collectively control nearly 60% of sales, confirming a moderate concentration level that allows room for innovative entrants.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glucosamine Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of osteoarthritis and aging population | +1.8% | Global, highest in North America and Europe | Long term (≥ 4 years) |

| Increasing consumption of nutraceuticals | +1.2% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Growing awareness of preventive healthcare and joint health | +0.9% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Expansion of functional foods and fortified products market | +0.7% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Adoption of vegan-fermented glucosamine | +0.5% | Europe and North America, expanding into Asia-Pacific | Long term (≥ 4 years) |

| Growth in pet humanization and veterinary supplements | +0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Osteoarthritis and Aging Population

Osteoarthritis cases worldwide have increased significantly, with higher prevalence rates in developed and developing regions. The condition predominantly affects women and older adults, who require joint-care supplements throughout their lives. As a major cause of global disability, osteoarthritis results in economic losses through reduced workplace productivity, higher healthcare costs, and long-term medical care needs. The persistent health burden, aging global population, and growing awareness of joint health maintain consistent demand for glucosamine products. The chronic nature of osteoarthritis requires continuous management, supporting market stability.

Increasing consumption of nutraceuticals

The United States population regularly incorporates dietary supplements into their health routines. Both young and older adults emphasize preventive healthcare, which increases the sales of combination joint supplements containing glucosamine, chondroitin, and Methylsulfonylmethane (MSM). These supplements support joint health and mobility, particularly among active individuals and aging populations. The rise of personalized nutrition applications, subscription services, and tele-pharmacy platforms drives supplement consumption and expands the glucosamine market through digital channels. These digital platforms enable consumers to access supplements conveniently while receiving personalized recommendations based on their health goals and requirements.

Growing awareness of preventive healthcare and joint health

Healthcare providers and policymakers are shifting their focus toward preventive care solutions that offer cost benefits, aligning with glucosamine's role as a long-term maintenance supplement rather than a treatment for acute conditions. Medical professionals now emphasize mobility maintenance during regular patient visits, which has led to increased consumer trust in scientifically-supported nutritional supplements. The growing adoption of fitness trackers and wearable devices that monitor physical activity levels, movement patterns, and joint impact encourages active individuals to seek preventive joint care products. This trend particularly benefits manufacturers who can effectively communicate clinical evidence through clear product labeling and educational materials. The integration of digital health monitoring with preventive supplementation creates opportunities for brands to develop comprehensive joint health solutions that combine product efficacy with data-driven wellness tracking.

Expansion of functional foods and fortified products market

The food-as-medicine movement is influencing beverage, snack, and dairy companies to incorporate therapeutic doses of glucosamine into their mainstream products. This development aligns with consumers' increasing preference for functional foods and beverages that provide health benefits beyond basic nutrition. Manufacturers are responding to this trend by reformulating existing products and developing new offerings with glucosamine as a key ingredient. The integration spans various product categories, from sports drinks and smoothies to protein bars and yogurt products. According to Treatt, in Europe, 5% of food and drink launches in 2025 will include functional claims related to specific bodily functions, reflecting consumers' focus on maintaining healthy lifestyles [2]Treatt Plc, "UK and EU Functional Beverage Trends in 2025," treatt.com. This trend is particularly evident in markets where aging populations and health-conscious consumers drive demand for products supporting joint health and mobility. The incorporation of glucosamine in mainstream food products also makes these functional ingredients more accessible to consumers who prefer not to take supplements .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile supply of shellfish-based raw materials | -0.8% | Global, highest in shellfish-dependent regions | Short term (≤ 2 years) |

| Availability of effective alternatives | -0.6% | Developed markets with diverse treatment options | Medium term (2-4 years) |

| Stringent regulatory frameworks for novel foods and dietary supplements | -0.4% | Europe and North America | Medium term (2-4 years) |

| High production costs of vegan/fermentation-derived glucosamine | -0.3% | Global, affecting price-sensitive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile supply of shellfish-based raw materials

Glucosamine, primarily sourced from shellfish like shrimp and crabs, faces production disruptions and cost inflation due to fluctuations in shellfish availability. Environmental challenges, including ocean pollution, climate change, and rising sea temperatures, have degraded habitats and diminished shellfish populations in numerous regions. Unsustainable harvesting and overfishing practices further deplete the shellfish shells essential for glucosamine extraction. In Southeast Asia, shrimp farms have grappled with disease outbreaks, leading to marked declines in shellfish production. [3]Aqua Research Pte Ltd., "Marine Shrimp in Asia", www.aquaasiapac.com To safeguard marine ecosystems, regulatory measures such as harvesting quotas and seasonal bans have been implemented, but they also curtail supply. Moreover, geopolitical tensions and trade disruptions in major exporting nations, particularly China and Vietnam, introduce unpredictability to the market. Collectively, these factors contribute to supply instability, escalating costs, and challenges in production planning for glucosamine producers.

Availability of Effective Alternatives

The joint health treatment market encompasses pharmaceutical innovations and alternative therapies alongside glucosamine supplements. Prescription medications, particularly disease-modifying osteoarthritis drugs (DMOADs) in development, aim to improve outcomes for severe cases. These medications target specific pathways involved in joint degeneration and inflammation, offering potential breakthroughs in disease management. The treatment options include physical therapy, regenerative medicine procedures (platelet-rich plasma and stem cell therapies), and surgical interventions. Physical therapy focuses on strengthening muscles around affected joints and improving mobility, while regenerative medicine aims to stimulate natural healing processes. Advanced surgical techniques now include minimally invasive procedures and joint preservation methods. Regulatory requirements influence physician recommendations and insurance coverage policies, impacting the integration of glucosamine supplements into evidence-based medical protocols. These regulations encompass safety standards, clinical trial requirements, and documentation of therapeutic efficacy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Fermentation disrupts shellfish tradition

Shellfish-derived glucosamine maintains 79.10% market share in 2025, benefiting from established supply chains and consumer familiarity. Traditional extraction methods from crab and shrimp shells leverage existing seafood processing waste streams, creating cost efficiencies and environmental benefits through waste utilization. However, fermentation-derived alternatives exhibit 7.74% CAGR growth through 2031, driven by allergy avoidance, sustainability concerns, and supply chain diversification strategies.

The development of advanced production methods, including artificial enzymatic biosystems, enables high conversion efficiency from starch to glucosamine through fermentation. This innovative production method significantly reduces environmental impact while maintaining product quality. The fermentation process utilizes renewable resources and controlled manufacturing conditions, resulting in consistent product quality. This production method offers a sustainable alternative that addresses both supply security concerns and consumer preferences, particularly among those seeking environmentally responsible products.

By Type: Sulfate Dominance Faces HCl Innovation

Glucosamine sulfate holds 60.95% of the market share in 2025, supported by extensive clinical research and its pharmaceutical-grade status. The European Society for Clinical and Economic Aspects of Osteoporosis, Osteoarthritis and Musculoskeletal Diseases (ESCEO) endorses pharmaceutical-grade glucosamine sulfate as a standalone treatment, recommending against its combination with chondroitin. Glucosamine HCl exhibits the highest growth rate at 8.79% CAGR through 2031, due to its stability benefits and lower production costs.

Market competition among glucosamine formulations reflects both consumer needs and production efficiencies. N-acetyl-glucosamine emerges as a distinct segment, marketed for its improved bioavailability as a premium product. Fermentation-based production methods have improved glucosamine HCl yields significantly. These manufacturing advantages support glucosamine HCl's increasing market presence, especially in regions where price sensitivity influences purchasing decisions.

By Application: Functional foods challenge supplement supremacy

Dietary supplements represent 79.95% of the glucosamine market in 2025, primarily distributed through pharmacies and e-commerce platforms. The glucosamine supplements market continues to grow as consumers seek solutions for joint discomfort management. Customer retention mechanisms, including loyalty programs, subscription models, and bundled promotions with collagen supplements, drive consistent repeat purchases.

The functional foods and fortified products segment grows at 7.25% CAGR, offering convenient options through ready-to-drink formulations and protein snacks. Sports nutrition consumers, traditionally focused on protein and branched-chain amino acids (BCAA) supplements, increasingly adopt joint-support chews combining vitamin C and glucosamine. The pet nutrition segment provides additional market growth, with premium pet food manufacturers highlighting joint-care benefits as a key differentiator, despite limited clinical veterinary research.

Geography Analysis

North America maintains market leadership with 38.85% share in 2025, supported by established healthcare infrastructure, high consumer awareness of joint health supplements, and favorable regulatory frameworks under FDA oversight. The region benefits from extensive clinical research conducted at major medical institutions and strong distribution networks through pharmacy chains and specialized retailers. Consumer spending patterns reflect integration of glucosamine into routine healthcare regimens, with insurance coverage occasionally available for pharmaceutical-grade formulations. The aging baby boomer demographic creates sustained demand, while younger consumers increasingly adopt preventive supplementation strategies influenced by fitness and wellness trends.

Asia-Pacific emerges as the fastest-growing region with 7.99% CAGR through 2031, driven by expanding middle-class populations, increasing healthcare expenditure, and growing awareness of Western nutritional approaches. China and India represent particularly dynamic markets, benefiting from domestic manufacturing capabilities and acceptance of traditional medicine natural health products. Japan's sophisticated functional foods market. The region's manufacturing cost advantages, particularly for fermentation-derived production, position Asia-Pacific as both a consumption and export hub for global glucosamine supply chains.

Europe represents a mature market characterized by stringent regulatory oversight and evidence-based healthcare approaches. The European Food Safety Authority's rigorous evaluation processes for health claims create barriers for new entrants while protecting established products with approved claims. Consumer preferences favor pharmaceutical-grade formulations with clinical documentation, reflecting the region's emphasis on evidence-based medicine. The market benefits from strong research institutions conducting osteoarthritis studies and established distribution through pharmacy channels. Brexit implications continue affecting regulatory harmonization, with the UK developing independent evaluation frameworks for dietary supplements and functional foods.

Competitive Landscape

The glucosamine market demonstrates moderate concentration, with established companies implementing vertical integration strategies while new entrants focus on innovation and product differentiation. Market leaders, including Koyo Chemical Co., Ltd., Cargill, Inc., and TSI Group Ltd., among others, gain advantages through economies of scale in raw material procurement and manufacturing operations, while smaller companies compete by offering specialized formulations and targeted distribution channels.

Major consumer brands distinguish themselves through investments in clinical studies and transparent sourcing practices. Mannatech, for example, utilizes proprietary formulations and maintains publicly accessible research archives on its corporate website to build healthcare practitioner loyalty. The industry's quality standards are maintained through cross-licensing agreements between ingredient manufacturers and contract manufacturers, with companies like Catalent operating more than forty facilities to ensure consistent product launches across multiple regions.

Companies are increasingly focusing on higher-margin distribution channels. FitLife Brands expanded its market presence by acquiring MusclePharm, securing direct access to sports nutrition distributors that now include joint-health supplements. Twinlab grows its physical retail presence through strategic acquisitions, while Ingredion enhances its ingredient portfolio by combining clean-label starches with glucosamine for bakery applications. Market success increasingly depends on scientific validation, with GRAS (Generally Recognized as Safe) certifications and stability data influencing retail placement decisions.

Glucosamine Industry Leaders

-

Koyo Chemical Co., Ltd.

-

Cargill, Inc.

-

Zhejiang Aoxing Biotechnology Co., Ltd.

-

TSI Group Ltd.

-

Golden-Shell Pharmaceutical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: DNP International launched vegetarian glucosamine. Clinical trials have demonstrated the joint health benefits of glucosamine.

- May 2024: TSI Group Ltd.'s GlucosaGreen received NSF's Carbon Footprint Statement, ISCC PLUS Certified Sustainability, SGS's Non-GMO Certification, and Vegan Certification (V-Level Criteria).

- May 2023: NutraVita launched a Glucosamine powder supplement designed to help manage osteoarthritis symptoms. The product aims to support joint health and mobility by providing a concentrated form of Glucosamine, a compound known for its potential benefits in reducing joint pain and inflammation associated with osteoarthritis.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the glucosamine market as the total global revenue generated from the sale of glucosamine and its direct salts, glucosamine sulfate, glucosamine hydrochloride, and N-acetyl-glucosamine, used in human and animal health supplements, functional foods, and over-the-counter joint-care formulations.

Scope exclusion: This study deliberately leaves out wider bone and joint ingredients such as chondroitin, collagen peptides, and calcium fortifiers, so our numbers remain focused on stand-alone glucosamine offerings.

Segmentation Overview

-

By Type

- Glucosamine Sulfate

- Glucosamine Hydrochloride (HCl)

- N-Acetyl-glucosamine

- Other Types

-

By Source

- Shellfish-derived

- Fermentation-derived

- Others

-

By Application

- Nutritional Supplements

- Pet and Veterinary Supplements

- Functional Foods and Fortified Products

- Other Applications

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We held structured interviews and short surveys with ingredient manufacturers in China and India, medium-sized supplement brands in North America and Europe, and veterinary formulators in Japan and Brazil. Their inputs let us validate shellfish-based cost curves, adoption hurdles for fermented corn glucosamine, and typical retail price premiums.

Desk Research

Our analysts began with publicly available, high-credibility datasets such as UN Comtrade crustacean shell export flows, the U.S. FDA Dietary Supplement Label Database, EFSA scientific opinions, NHANES supplement intake waves, and Health Canada's Natural and Non-prescription Health Products Directory, which helped us set production, regulatory, and consumption bookends. Trade association briefs from the Council for Responsible Nutrition and the International Marine Ingredients Association, company 10-Ks, and investor decks supplied price points and shipment splits by form factor.

We also tapped D&B Hoovers for supplier financials and Dow Jones Factiva for deal flow that signals capacity shifts. These sources are illustrative, not exhaustive; many additional publications were reviewed to cross-check volumes, prices, and labeling claims.

Market-Sizing & Forecasting

Our model starts with a top-down reconstruction of demand. Global supplement spending is aligned with osteoarthritis prevalence and the 60-plus population, then filtered through product penetration rates by region. Select bottom-up spot checks, supplier revenue roll-ups and average selling price times volume samples, calibrate the totals. Key variables include average cartilage supplement basket spend, raw shellfish price per metric ton, share of plant-based glucosamine launches, and pet care supplement uptake. We forecast through 2030 via multivariate regression that blends those drivers with real GDP and healthcare spend growth, while scenario analysis adjusts for regulatory shifts or raw material shocks.

Data Validation & Update Cycle

Model outputs move through variance checks against import statistics and pharmacy sell-out dashboards before senior review. Reports refresh every twelve months, and we trigger interim updates when raw material prices swing plus or minus 10 percent or when major regulatory approvals occur, ensuring clients receive the latest vetted baseline.

Why Mordor's Glucosamine Baseline Commands Reliability

Published figures often diverge because firms apply dissimilar product scopes, price assumptions, and refresh cadences. We acknowledge these gaps upfront.

Key gap drivers include: some publishers fold glucosamine chondroitin blends into totals, others exclude veterinary demand, and a few convert currencies at spot rather than annual averages, which inflates headline values during dollar weakness.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.01 bn (2025) | Mordor Intelligence | |

| USD 1.10 bn (2024) | Regional Consultancy A | Includes pet treats and synthetic derivatives; broader base year |

| USD 0.65 bn (2024) | Trade Journal B | Narrows scope to prescription strength formats; omits functional foods and e-commerce channels |

These comparisons show that, by clearly defining scope, using mixed methods, and refreshing annually, Mordor Intelligence offers a balanced, transparent market baseline decision makers can rely on.

Key Questions Answered in the Report

What is the current size of the glucosamine market?

The glucosamine market is worth USD 1.06 billion in 2026 and is forecast to hit USD 1.38 billion by 2031.

Which glucosamine type grows the fastest?

Glucosamine HCl registers the highest CAGR at 8.79% through 2031, benefiting from superior processing stability and lower manufacturing costs.

Why is fermentation-derived glucosamine gaining attention?

Fermentation avoids shellfish allergens, delivers steadier supply, and aligns with sustainability mandates, producing a 7.74% CAGR growth path.

Which region shows the quickest demand up-swing?

Asia-Pacific leads with an 7.99% CAGR, driven by rising incomes, expanding e-commerce, and strong functional-food adoption.

Page last updated on: