Soluble Beta Glucan Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

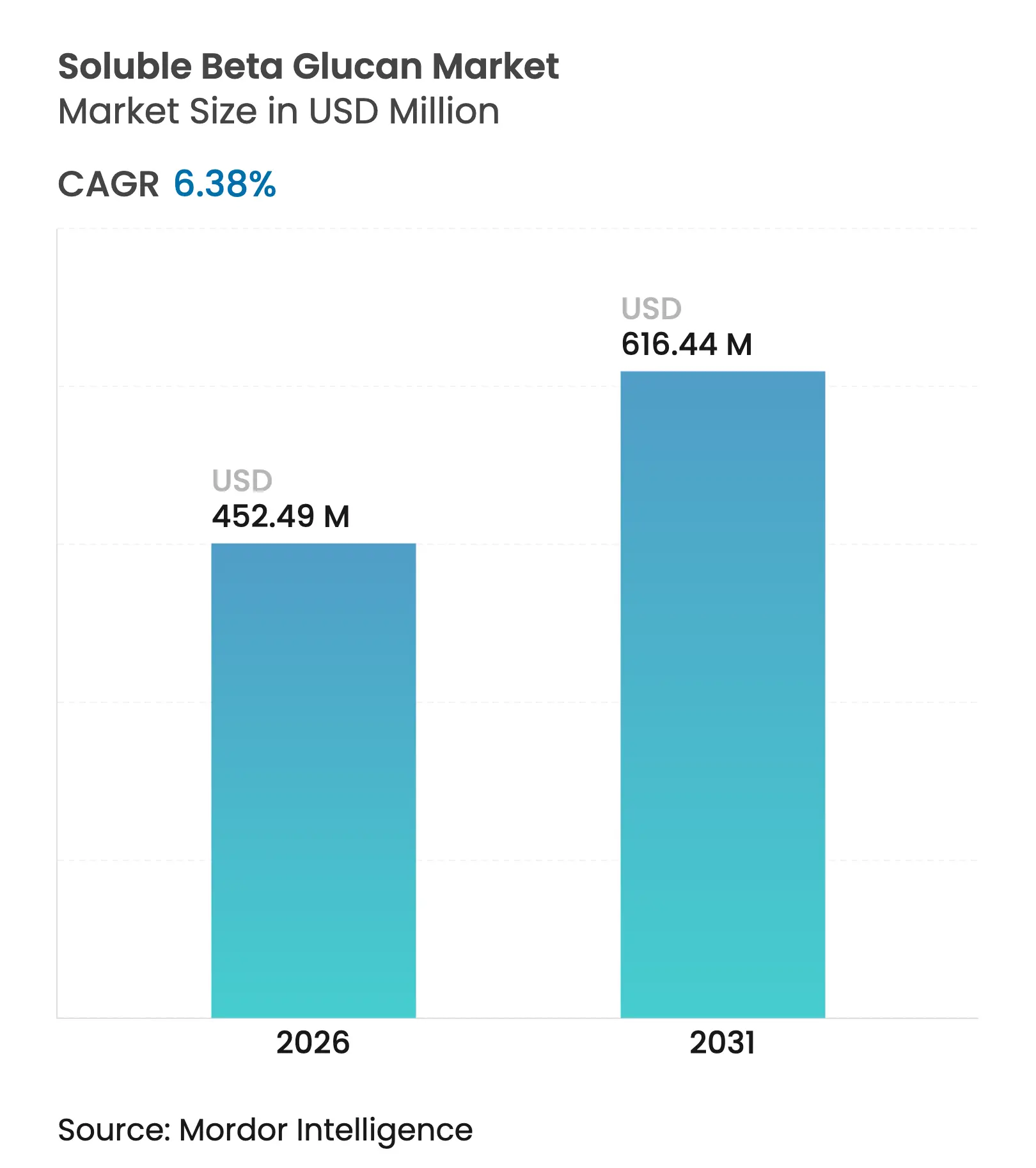

| Market Size (2026) | USD 452.49 Million |

| Market Size (2031) | USD 616.44 Million |

| Growth Rate (2026 - 2031) | 6.38 % CAGR |

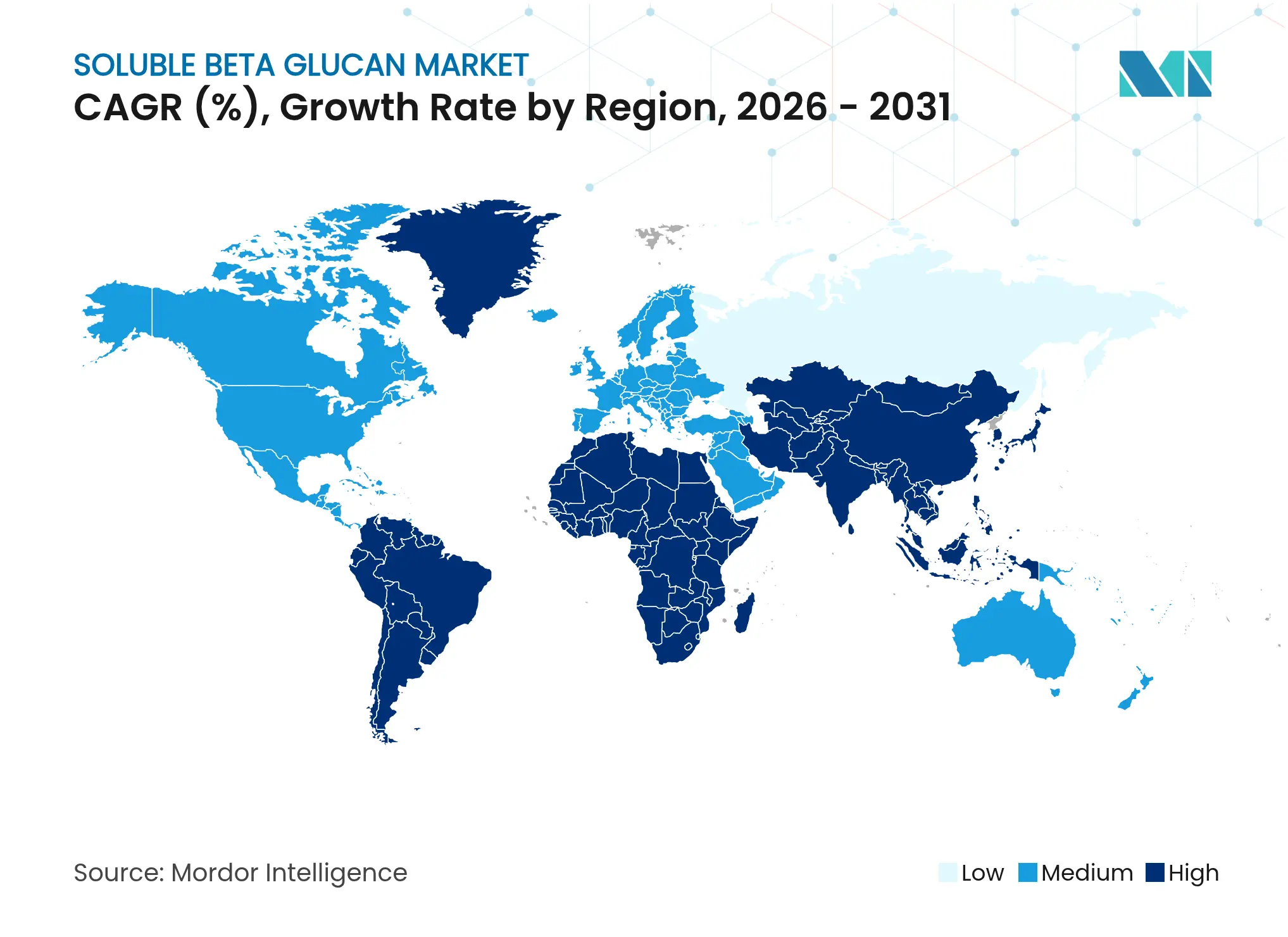

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

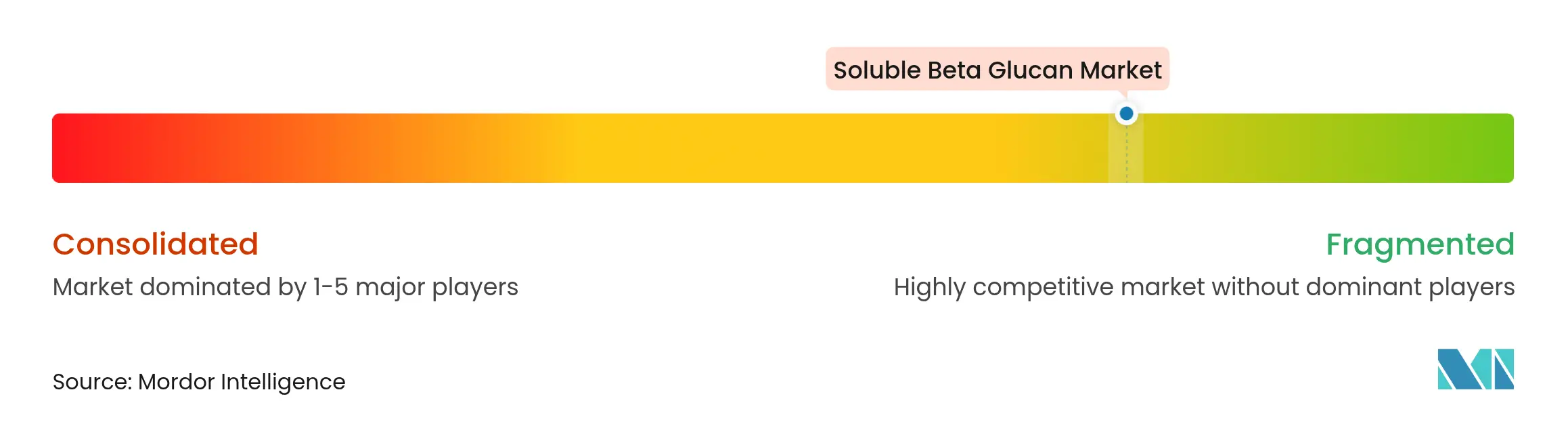

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Soluble Beta Glucan Market Analysis by Mordor Intelligence

The soluble beta-glucan market size is expected to grow from USD 425.36 million in 2025 to USD 452.49 million in 2026 and is forecast to reach USD 616.44 million by 2031 at 6.38% CAGR over 2026-2031. This growth trajectory represents a strategic inflection point where regulatory harmonization across major markets coincides with unprecedented consumer focus on immune health and functional nutrition. The European Food Safety Authority's 2024 approval of paramylon from Euglena gracilis microalgae marks a pivotal regulatory milestone, enabling Kemin Foods to secure five-year market exclusivity for its algae-derived beta-glucan products. Meanwhile, the FDA's[1]Food and Drug Administration, “Food Labeling: Nutrient Content Claims; Definition of ‘Healthy,’” Federal Register, federalregister.govupdated "healthy" food labeling definition, effective February 2025, creates new pathways for beta-glucan-enriched products to capture premium positioning in mainstream food categories. The increasing adoption of beta-glucan in functional beverages and dietary supplements further highlights its expanding application scope. Moreover, rising investments in R&D to enhance product efficacy and diversify applications are expected to drive market competitiveness during the forecast period.

Key Report Takeaways

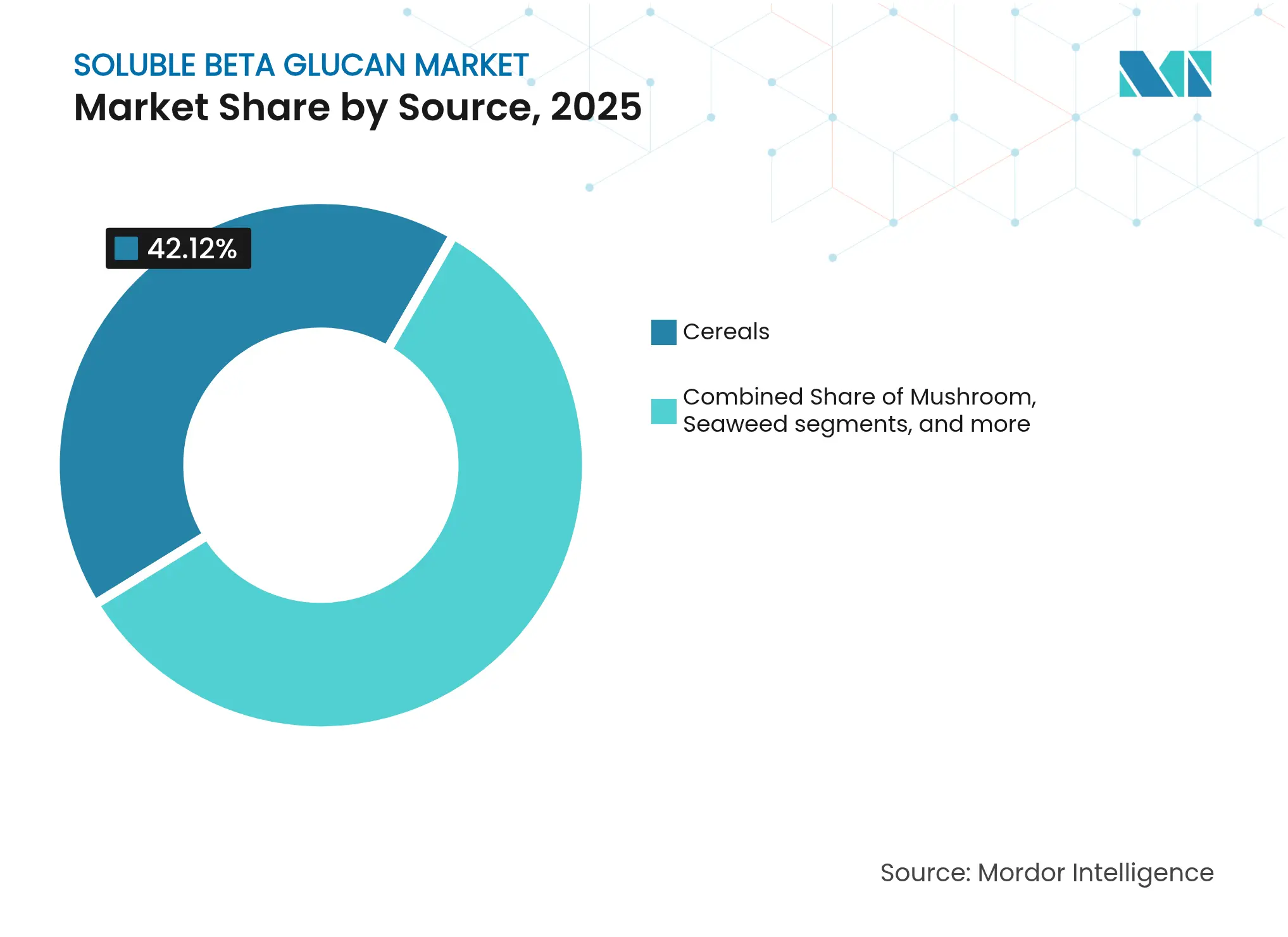

- By source, cereals led with a 42.12% share of the soluble beta-glucan market in 2025, while seaweed sources are projected to grow at a 7.55% CAGR from 2026-2031.

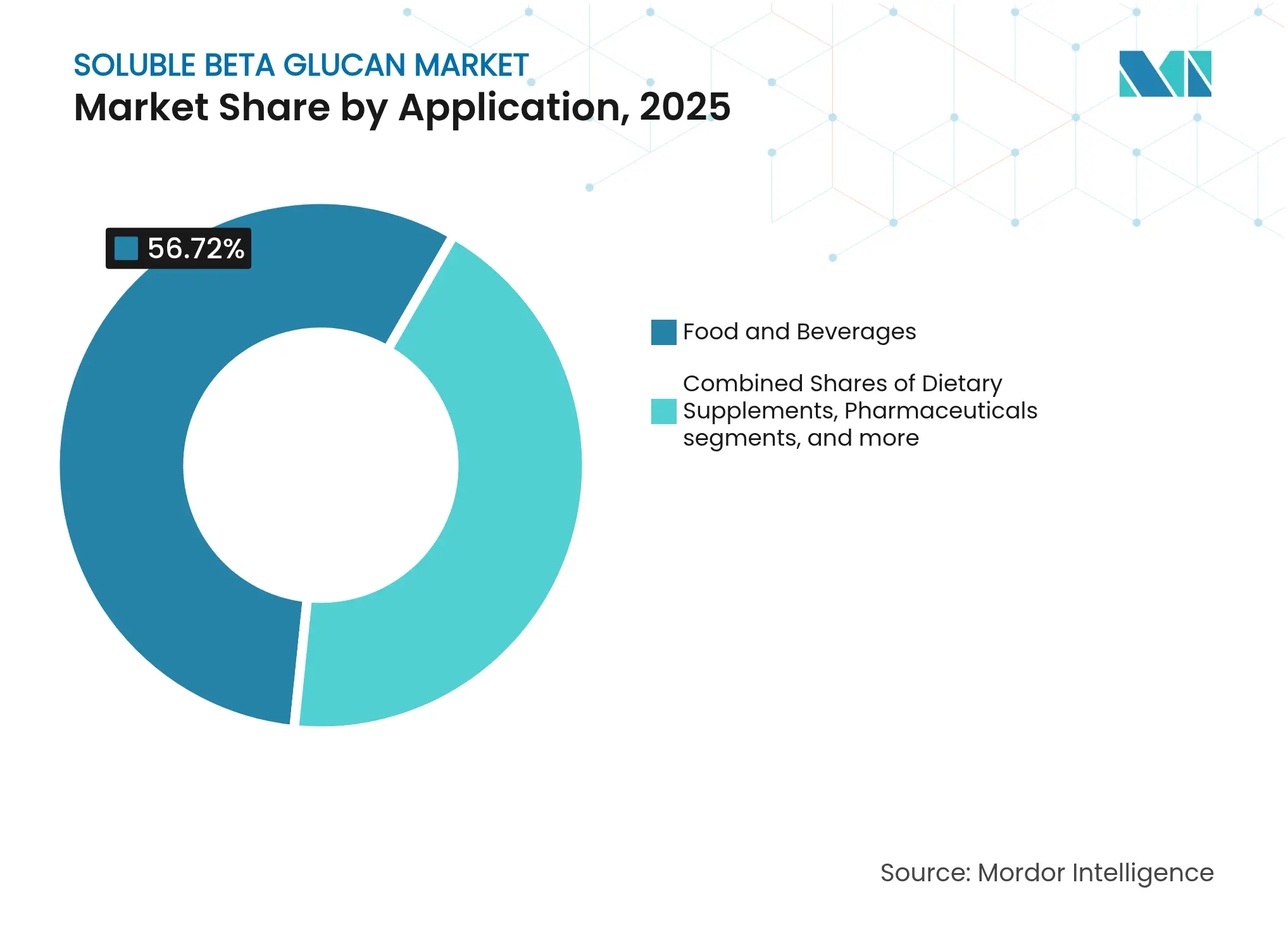

- By application, food and beverages accounted for a 56.72% share of the soluble beta-glucan market in 2025; dietary supplements record the highest CAGR at 7.9% through 2031.

- By geography, North America dominated with a 32.05% revenue share in 2025, whereas Asia-Pacific is forecast to expand at a 7.18% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Soluble Beta Glucan Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surging demand for functional food Surging demand for functional food | +1.8% | Global, with early gains in North America, Europe, Asia-Pacific | Medium term (2-4 years) | (~) % Impact on CAGR Forecasts:+1.8% | Geographic Relevance:Global, with early gains in North America, Europe, Asia-Pacific | Impact Timeline:Medium term (2-4 years) |

Growing popularity of natural and plant-based ingredients Growing popularity of natural and plant-based ingredients | +1.2% | North America and EU, spill-over to APAC | Long term (≥ 4 years) | |||

Proven health benefits and approved claims Proven health benefits and approved claims | +1.5% | Global, strongest in regulated markets | Medium term (2-4 years) | |||

Expanding nutraceutical and dietary supplement markets Expanding nutraceutical and dietary supplement markets | +1.1% | APAC core, spill-over to MEA | Long term (≥ 4 years) | |||

Increasing use in pet food and animal feed for immune health Increasing use in pet food and animal feed for immune health | +0.6% | North America and EU, expanding to APAC | Short term (≤ 2 years) | |||

Heightened consumer awareness of immune health benefits Heightened consumer awareness of immune health benefits | +0.9% | Global, accelerated post-pandemic | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Surging Demand for Functional Food

The functional food revolution drives beta-glucan adoption as manufacturers respond to consumer demands for foods that deliver health benefits beyond basic nutrition. Alberta Agriculture and Forestry reports that 63% of food companies are actively developing or marketing functional foods, with cardiovascular health and weight management emerging as primary consumer concerns, according to Alberta Agriculture data from 2023. This trend accelerates as regulatory bodies streamline health claim approvals, enabling manufacturers to communicate beta-glucan's cholesterol-lowering and glycemic control benefits directly to consumers. The FDA's recognition of beta-glucan's heart health benefits through approved health claims creates competitive advantages for products containing minimum effective doses, typically 3 grams daily from oat or barley sources. Food manufacturers increasingly incorporate beta-glucan into mainstream products like cereals, dairy preparations, and baked goods to capture premium pricing while meeting clean-label requirements that resonate with health-conscious consumers.

Growing Popularity of Natural and Plant-Based Ingredients

Consumer preference for natural, plant-derived ingredients transforms beta-glucan from a specialty additive into a mainstream functional component across food and supplement categories. The shift toward plant-based nutrition creates opportunities for beta-glucan sourced from oats, barley, and emerging algae platforms that align with vegan and vegetarian dietary preferences. This technological convergence enables sustainable beta-glucan production while reducing resource intensity compared to conventional extraction methods. The clean-label movement further amplifies demand as manufacturers seek recognizable ingredients that consumers can easily understand and trust, positioning beta glucan as a natural fiber source that delivers measurable health benefits without synthetic additives or chemical processing concerns.

Proven Health Benefits and Approved Claims

Regulatory validation of beta-glucan's health benefits through official health claims creates substantial market differentiation opportunities for manufacturers seeking premium positioning. The European Food Safety Authority's comprehensive evaluation confirms beta-glucan's efficacy in reducing post-prandial blood glucose response and lowering blood cholesterol levels, enabling manufacturers to make specific health claims on product packaging. Clinical evidence demonstrates that daily consumption of 3 grams of beta-glucan from oats or barley can reduce LDL cholesterol by 5-10%, while 4 grams per 30 grams of available carbohydrates significantly attenuates glycemic response, according to the UK Government[2]Government of UK, "UKNHCC scientific opinion: beta-glucan from oats or barley and reduction of blood glucose rise after a meal", www.gov.uk. These validated claims enable manufacturers to command premium pricing while building consumer trust through science-backed positioning. The breadth of approved health benefits, spanning cardiovascular health, diabetes management, and immune support, creates multiple market entry points for beta-glucan-enhanced products across diverse consumer segments.

Expanding Nutraceutical and Dietary Supplement Markets

Asian markets demonstrate particularly strong growth potential, with China, Japan, and India implementing regulatory frameworks that facilitate nutraceutical market access while maintaining safety standards. Japan's Foods with Function Claims system enables simplified product registration for ingredients with established safety profiles, while India's Food Safety and Standards Authority streamlines health supplement approval processes, according to the Food Compliance International. The supplement industry's shift toward evidence-based formulations favors beta-glucan's extensive clinical validation, with over 15 published studies supporting its immune health and metabolic benefits. Consumer preference for single-ingredient supplements that deliver specific health outcomes drives demand for purified beta-glucan products that can be precisely dosed and easily incorporated into daily wellness routines.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Unfavorable viscosity/taste profile Unfavorable viscosity/taste profile | -0.8% | Global, particularly in food applications | Medium term (2-4 years) | (~) % Impact on CAGR Forecasts:-0.8% | Geographic Relevance:Global, particularly in food applications | Impact Timeline:Medium term (2-4 years) |

Price competition from other functional fibers Price competition from other functional fibers | -0.6% | Global, strongest in cost-sensitive markets | Long term (≥ 4 years) | |||

Complex extraction and bioavailability issues Complex extraction and bioavailability issues | -0.5% | Global, affecting product development | Long term (≥ 4 years) | |||

Low awareness of beta glucan benefits in developing regions Low awareness of beta glucan benefits in developing regions | -0.4% | MEA, Latin America, parts of APAC | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Unfavorable Viscosity/Taste Profile

Beta-glucan's inherent viscosity properties create formulation challenges that limit its application versatility across food and beverage categories. The polysaccharide's gel-forming characteristics, while beneficial for cholesterol reduction and glycemic control, can negatively impact product texture and mouthfeel in liquid applications like beverages and dairy products. Food manufacturers must balance functional efficacy with consumer acceptability, often requiring complex formulation adjustments or taste-masking technologies that increase production costs. Recent technological advances in molecular weight modification and structural alteration show promise for addressing these challenges, with ultrasonic-microwave extraction techniques producing beta-glucan fractions with improved solubility and reduced viscosity. However, these processing innovations require significant investment in specialized equipment and technical expertise, creating barriers for smaller manufacturers seeking to incorporate beta-glucan into their product portfolios. The development of highly soluble, low-viscosity beta-glucan variants represents a critical breakthrough for expanding market applications beyond traditional high-fiber products.

Price Competition from Other Functional Fibers

The functional fiber market's competitive landscape intensifies as alternative ingredients like psyllium, inulin, and resistant starch compete for market share through aggressive pricing strategies and established supply chains. Psyllium husk, in particular, offers similar viscosity-dependent health benefits at potentially lower costs, while inulin provides prebiotic functionality that appeals to gut health-focused consumers. Beta-glucan's premium positioning requires clear differentiation through superior clinical validation and specific health claims that justify higher ingredient costs. The market's price sensitivity varies significantly across applications, with dietary supplement manufacturers more willing to pay premium prices for clinically validated ingredients compared to food manufacturers operating under tight margin constraints. Successful beta-glucan suppliers must demonstrate clear value propositions that extend beyond basic fiber functionality to include specific immune health, cardiovascular, and metabolic benefits that alternative fibers cannot deliver with equivalent clinical support.

Segment Analysis

By Sources: Cereals Lead the Market, while Algae is the Fastest Growing Market

Cereals command 42.12% market share in 2025, establishing oats and barley as foundational sources for soluble beta-glucan extraction due to their established agricultural supply chains and extensive regulatory validation. The segment's dominance reflects decades of clinical research supporting health claims for cereal-derived beta-glucan, particularly the FDA's approval for cholesterol reduction claims requiring a 3-gram daily intake from oat or barley sources. Mushroom-derived beta-glucan maintains steady demand in immune health applications, while yeast sources benefit from established fermentation infrastructure and consistent quality profiles. Microbial and bacterial sources serve niche applications requiring specific molecular weight characteristics or enhanced bioavailability profiles.

Seaweed emerges as the fastest-growing source segment with 7.55% CAGR through 2031, driven by breakthrough extraction technologies and superior concentration levels compared to traditional sources. The European Commission's April 2024 authorization of beta-glucan from Euglena gracilis microalgae creates new market opportunities, with Kemin Foods securing five-year exclusivity for its BetaVia product line. Algae-derived beta-glucan offers over 50% concentration levels compared to 3-6% typical in cereal sources, enabling more efficient processing and reduced shipping costs. The sustainability advantages of algae cultivation, including minimal land and water requirements, align with corporate environmental commitments and consumer preferences for eco-friendly ingredients.

Note: Segment shares of all individual segments available upon report purchase

By Application: Food Integration Accelerates Supplement Growth

Food and beverages dominate with a 56.72% market share in 2025, reflecting the successful integration of beta-glucan into mainstream products like cereals, dairy preparations, and functional beverages. The segment benefits from established consumer acceptance of fiber-enriched foods and regulatory frameworks that support health claim communication directly to consumers. Dairy products increasingly incorporate beta-glucan for cholesterol management positioning, while functional beverages overcome viscosity challenges through specialized processing techniques.

Dietary supplements accelerate at 7.9% CAGR through 2031, driven by consumer preference for targeted health solutions and precise dosing control. The segment's growth reflects increasing consumer sophistication regarding specific health benefits and willingness to pay premium prices for clinically validated ingredients. Animal feed and pet nutrition represent an emerging high-growth segment, with clinical studies demonstrating immune health benefits in dogs, cats, and livestock that justify premium ingredient positioning. Pharmaceutical applications remain specialized but show promise for immune therapy adjuvant uses, particularly in cancer treatment protocols where beta-glucan enhances conventional therapy effectiveness.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America maintains a 32.05% market share in 2025, anchored by mature regulatory frameworks, extensive clinical research infrastructure, and established consumer awareness of beta-glucan health benefits. The region's leadership reflects decades of FDA health claim approvals and widespread incorporation of beta-glucan into mainstream food products, particularly breakfast cereals and functional foods. Canada's health claim recognition for beta-glucan creates additional market opportunities, while Mexico's growing middle class drives demand for premium health-focused ingredients. The region's sophisticated supply chain infrastructure and quality control standards support premium pricing strategies that justify higher production costs associated with specialized extraction and purification processes.

Asia-Pacific emerges as the fastest-growing region with 7.18% CAGR through 2031, driven by regulatory harmonization efforts and expanding consumer health awareness across major markets. Japan's Foods with Function Claims system enables streamlined product registration for ingredients with established safety profiles, while China's evolving nutraceutical regulations create substantial market access opportunities for validated health ingredients. India's Food Safety and Standards Authority implements registration requirements that favor clinically validated ingredients, positioning beta-glucan advantageously against less substantiated alternatives. The region's growing disposable income and increasing health consciousness drive demand for premium functional ingredients, while expanding manufacturing capabilities support local production and reduce import dependencies.

Europe demonstrates steady growth supported by EFSA's comprehensive health claim evaluations and strong consumer preference for natural, plant-derived ingredients. The region's stringent regulatory standards create barriers for new entrants but provide competitive advantages for established beta-glucan suppliers with approved health claims. The Middle East and Africa represent emerging opportunities as regulatory frameworks develop and consumer awareness increases, though market penetration remains limited by distribution challenges and price sensitivity in developing economies.

Competitive Landscape

Market Concentration

The soluble beta-glucan market remains fragmented, with established ingredient suppliers and innovative disruptors competing to secure market share through distinct positioning strategies. Key players such as Tate & Lyle, Kerry Group, and DSM-Firmenich leverage their advanced R&D capabilities and regulatory expertise to sustain premium positioning. Meanwhile, emerging companies are focusing on developing novel extraction technologies and targeting specialized applications.

The competitive landscape highlights the market's progression from a commodity fiber focus to its current status as a precision health ingredient. Clinical validation and regulatory approvals have become critical factors in establishing long-term competitive advantages. Additionally, strategic consolidation is gaining momentum, driven by targeted acquisitions that integrate complementary capabilities and extend geographic reach.

An analysis of the industry's patent landscape reveals significant innovation in areas such as extraction optimization, molecular weight modification, and bioavailability enhancement. Companies like Cargill are actively securing intellectual property for advancements, including fermentation-derived postbiotic ingredients containing beta-glucan metabolites. Furthermore, personalized nutrition presents untapped opportunities, as beta-glucan's measurable health benefits enable precision dosing tailored to individual metabolic profiles and health objectives.

Soluble Beta Glucan Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Tate & Lyle announced a strategic partnership with BioHarvest to develop next-generation plant-based ingredients using botanical synthesis technology, enabling sustainable production of non-GMO plant-derived ingredients without traditional agricultural constraints. The collaboration aims to create more affordable and accessible ingredients for the food and beverage industry

- November 2024: Tate & Lyle completed the USD 1.8 billion acquisition of CP Kelco, creating a leading global specialty food and beverage solutions business with enhanced capabilities in pectin and nature-based ingredients. The merger positions the combined entity to better serve consumer demands for healthier and sustainable food options.

- October 2024: Lesaffre acquired a 70% stake in Biorigin, a Brazilian company specializing in yeast-derived products for human and animal nutrition, enhancing production processes and expanding supply of yeast derivatives including beta glucans. The acquisition strengthens Lesaffre's position in the global yeast extracts market

- October 2023: Baneo, a producer of functional fibre ingredients launched its first barley beta-glucan ingredient, Orafti B-Fit. The product claims to be used in foods like breakfast cereals, bread, baked goods, dairy alternatives, and pasta.

Table of Contents for Soluble Beta Glucan Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Surging demand for the functional food

- 4.2.2Growing Popularity of Natural and Plant-Based Ingredients

- 4.2.3Proven Health Benefits and Approved Claims

- 4.2.4Expanding Nutraceutical and Dietary Supplement Markets

- 4.2.5Increasing use of beta glucans in pet food and animal feed for immune health.

- 4.2.6Heightened Consumer Awareness of Immune Health Benefits

- 4.3Market Restraints

- 4.3.1Unfavourable viscosity/taste profile

- 4.3.2Price Competition from Other Functional Fibers

- 4.3.3Complex extraction and bioavailability issues

- 4.3.4Low awareness of beta glucan benefits in developing regions

- 4.4Supply-Chain Analysis

- 4.5Regulatory Outlook

- 4.6Porter’s Five Forces

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers/Consumers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE IN USD)

- 5.1By Sources

- 5.1.1Cereals

- 5.1.2Mushroom

- 5.1.3Yeast

- 5.1.4Seaweed

- 5.1.5Microbial/Bacterial

- 5.1.6Others

- 5.2By Application

- 5.2.1Food and Beverages

- 5.2.1.1Bakery and Confectionery

- 5.2.1.2Dairy Products

- 5.2.1.3Functional Beverages

- 5.2.1.4Other Food and Beverage Applications

- 5.2.2Dietary Supplements

- 5.2.3Personal Care and Cosmetics

- 5.2.4Animal Feed and Pet Nutrition

- 5.2.5Pharmaceuticals

- 5.2.6Others

- 5.3By Geography

- 5.3.1North America

- 5.3.1.1United States

- 5.3.1.2Canada

- 5.3.1.3Mexico

- 5.3.1.4Rest of North America

- 5.3.2South America

- 5.3.2.1Brazil

- 5.3.2.2Argentina

- 5.3.2.3Rest of South America

- 5.3.3Europe

- 5.3.3.1United Kingdom

- 5.3.3.2Germany

- 5.3.3.3France

- 5.3.3.4Italy

- 5.3.3.5Russia

- 5.3.3.6Rest of Europe

- 5.3.4Asia-Pacific

- 5.3.4.1China

- 5.3.4.2India

- 5.3.4.3Japan

- 5.3.4.4Australia

- 5.3.4.5Rest of Asia-Pacific

- 5.3.5Middle East and Africa

- 5.3.5.1Saudi Arabia

- 5.3.5.2South Africa

- 5.3.5.3Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Ranking Analysis

- 6.4Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1Tate & Lyle PLC

- 6.4.2Kerry Group plc

- 6.4.3DSM-Firmenich

- 6.4.4Cargill Inc.

- 6.4.5Sudzucker Group (Beneo)

- 6.4.6Lesaffre Group

- 6.4.7Givaudan SA

- 6.4.8Super Beta Glucan Inc.

- 6.4.9Garuda International

- 6.4.10Ohly GmbH

- 6.4.11Lallemand Inc.

- 6.4.12Angel Yeast Co. Ltd

- 6.4.13Kemin Industries Inc.

- 6.4.14Immudyne Nutraceuticals

- 6.4.15Grain Millers, Inc.

- 6.4.16Nutragreen Biotechnology Co., Ltd

- 6.4.17Merck KGaA

- 6.4.18ABF Ingredients

- 6.4.19Fuji Chemical Industries Co., Ltd. (AstaReal AB)

- 6.4.20Van Wankum Ingredients BV

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Global Soluble Beta Glucan Market Report Scope

The global soluble beta-glucan market is segmented by source and application. Based on source, the market is segmented into cereals, mushroom, others. Based on application, the market is segmented into food and beverage, health and dietary supplement, personal care industry, others. Based on geography, the study provides an analysis of the soluble beta-glucan market in the emerging and established markets across the globe, including North America, Europe, Asia-Pacific, and Rest of the World