Market Overview

| Study Period | 2021 - 2031 |

|---|---|

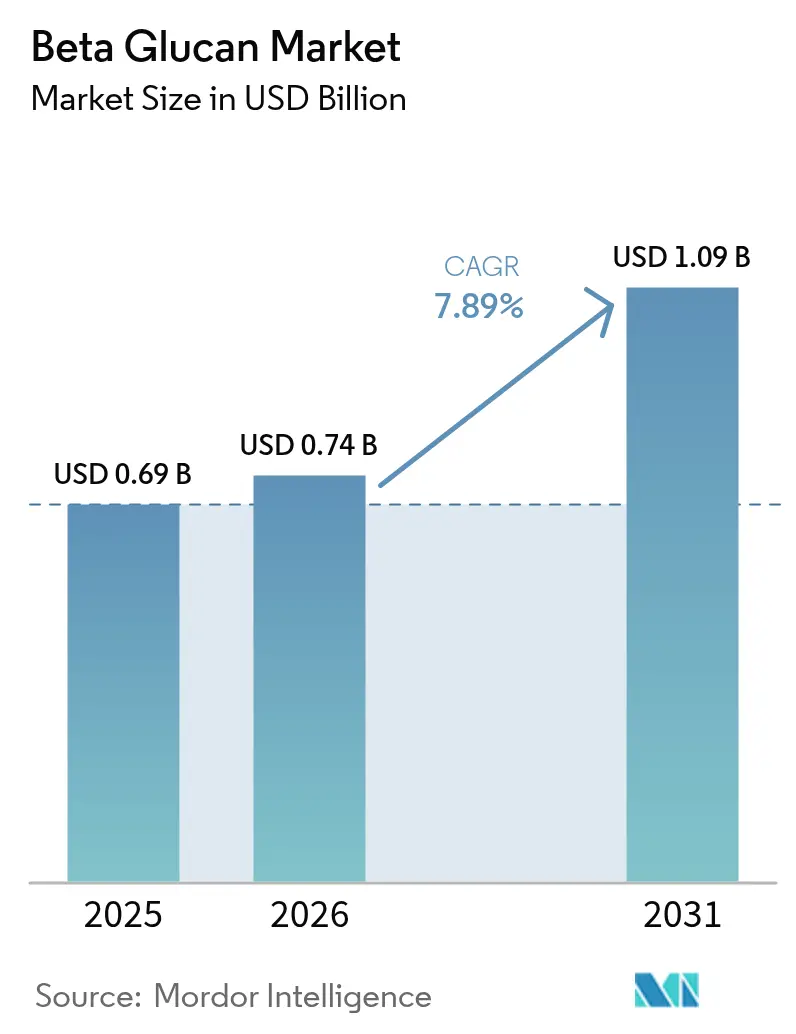

| Market Size (2026) | USD 0.74 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 7.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Beta Glucan Market Analysis by Mordor Intelligence

The beta glucan market size in 2026 is estimated at USD 744.44 million, growing from 2025 value of USD 0.69 billion with 2031 projections showing USD 1.09 billion, growing at 7.89% CAGR over 2026-2031. Rising scientific consensus around cholesterol reduction, immune modulation, and gut-health benefits continues to elevate beta-glucan’s profile in functional food, pharmaceutical, and personal-care lines. The U.S. Food and Drug Administration (FDA) recognizes oat beta-glucan’s cholesterol-lowering efficacy, enabling on-pack health claims that accelerate product launches. Investments in precision fermentation and advanced extraction are expanding supply options while reducing production cost volatilities. Solid regulatory backing from bodies such as the European Food Safety Authority (EFSA) and clear labeling rules are further encouraging brand owners to champion beta-glucan-forward formulations

Key Report Takeaways

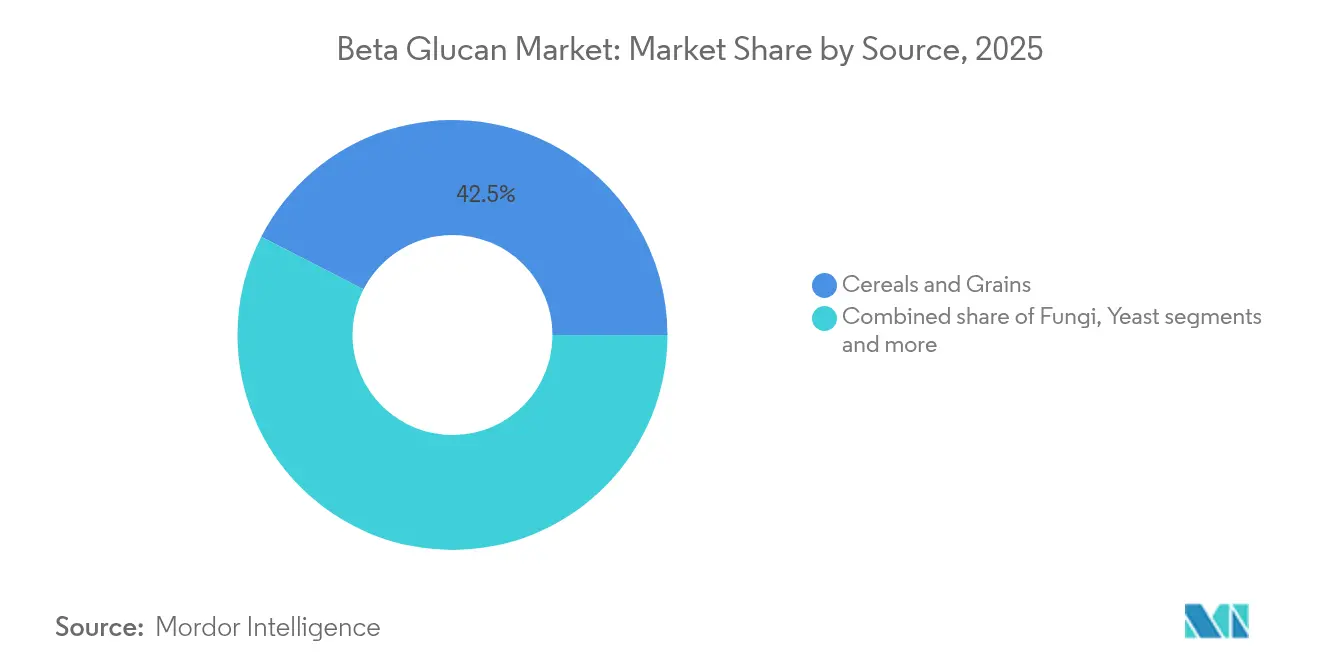

- By source, cereals and grains led with 42.45% revenue share in 2025; fungi-derived formats are projected to expand at 8.49% CAGR through 2031.

- By category, soluble forms commanded 72.05% of the beta-glucan market share in 2025, while insoluble types are poised to grow at 8.81% CAGR to 2031.

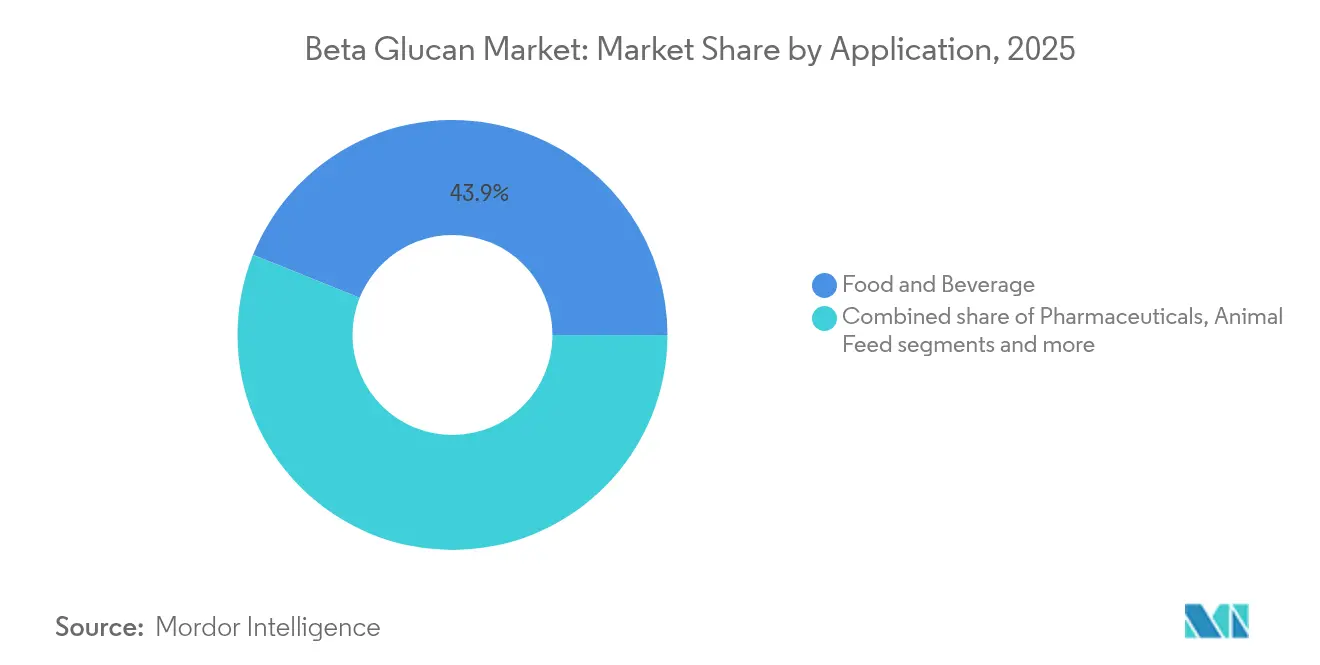

- By application, food and beverage accounted for 43.92% of the beta-glucan market size in 2025; personal care and cosmetics are advancing at 8.68% CAGR between 2026-2031.

- By geography, Europe held a 33.10% share of the beta-glucan market in 2025, whereas Asia-Pacific is on track for a 8.99% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Beta Glucan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for immune-boosting ingredients in functional foods | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing popularity of plant based ingredients | +1.2% | Global, led by Asia-Pacific and Europe | Long term (≥ 4 years) |

| Increasing popularity in gut health and prebiotic products | +1.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growth in vegan and gluten-free product launches | +0.9% | North America and Europe primarily | Short term (≤ 2 years) |

| Expansion of fungi- and yeast-based beta-glucans in pharmaceuticals | +1.1% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Rising research and development investment for enhanced solubility and bioavailability | +0.7% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Immune-Boosting Ingredients in Functional Foods

Post-pandemic health consciousness has fundamentally shifted consumer priorities toward immune-supporting ingredients, with consumers actively seeking products that support immune health, according to the Kerry Group report. Beta-glucan's scientifically validated immunomodulatory effects position it as a preferred ingredient in functional beverages, with 60% of Asia-Pacific, Middle East, and Africa (APMEA) region consumers expressing interest in immune health beverages. The FDA's GRAS approval for beta-glucans from Antrodia cinnamomea at levels up to 150 mg per serving demonstrates regulatory confidence in safety profiles. Clinical studies indicate that beta-glucan consumption enhances immune response in patients with compromised immune systems, as demonstrated in myelodysplastic syndrome trials. This immune-centric positioning drives premium pricing strategies and enables market penetration across previously untapped demographic segments. The convergence of scientific validation and consumer demand creates sustainable competitive advantages for beta-glucan suppliers with robust clinical data portfolios.

Growing Popularity of Plant Based Ingredients

According to the Smart Protein Project, in 2023, 49% of survey respondents in Italy prioritized health benefits, while 26% focused on environmental and climate impact when purchasing plant-based or vegan food products [1]Source: Smart Protein Project, “Evolving Appetites: An In-depth Look At European Attitudes Towards Plant-based Eating”, smartproteinproject.eu. Consumer preferences directly influence purchasing patterns in the plant-based food segment, with demand increasing for clean-label products that deliver health advantages and environmental sustainability. This trend indicates a fundamental shift in the food market, where health and environmental considerations drive product selection. Plant-based positioning enables manufacturers to implement premium pricing strategies and meet sustainability requirements from major food companies. This approach not only satisfies consumer preferences but also aligns with corporate sustainability goals and regulatory requirements. The combination of plant-based trends and functional health benefits creates distinct value propositions that generate higher margins compared to standard beta-glucan products. This convergence of health functionality and sustainability presents significant opportunities for manufacturers to develop innovative products that capture premium market segments.

Increasing Popularity in Gut Health and Prebiotic Products

Gut health awareness drives sophisticated consumer understanding of prebiotic mechanisms, with beta-glucan's ability to modulate beneficial gut bacteria gaining scientific validation. The mechanistic understanding of beta-glucan's interaction with gut microbiota enables targeted product development for specific health outcomes, moving beyond generic fiber positioning. Clinical evidence supporting beta-glucan's role in maintaining healthy cholesterol levels through gut-mediated mechanisms strengthens regulatory health claim substantiation across multiple jurisdictions. This scientific foundation enables premium positioning in the expanding gut health category, where consumers demonstrate a willingness to pay higher prices for proven efficacy. The convergence of microbiome science and beta-glucan functionality creates opportunities for personalized nutrition applications and targeted therapeutic interventions.

Growth in Vegan and Gluten-Free Product Launches

According to The Vegan Society survey, approximately two million people in Great Britain, representing 3% of the population, follow a vegan or plant-based diet [2]Source: The Vegan Society, “Nationwide Trends Highlight Growing Shift Toward Plant-based Diets”, vegansociety.com. This increase indicates a market transition from medical necessity to lifestyle preferences in dietary choices. Beta-glucan, being naturally gluten-free and plant-based, meets the market requirements for vegan and gluten-free products while delivering functional health benefits. Comprehensive research studies demonstrate that beta-glucans derived from Pleurotus ostreatus significantly enhance both the nutritional profile and sensory characteristics of gluten-free bread, effectively addressing a persistent challenge in gluten-free product development. The European Commission's approval of (1-3)(1-6)-β-glucans from mushroom sources as food ingredients has substantially expanded the potential applications across various specialty dietary products. This strategic market positioning enables manufacturers to effectively serve multiple dietary preference segments while maintaining premium price points for their specialized product formulations in both vegan and gluten-free categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low consumer awareness in developing markets | -1.3% | Asia-Pacific developing markets, Latin America, Middle East and Africa | Medium term (2-4 years) |

| Variability in functional efficacy across sources | -0.8% | Global, particularly affecting new entrants | Short term (≤ 2 years) |

| Supply chain disruption in raw material sourcing | -1.1% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Lack of standardization in product quality | -0.6% | Global, with regulatory focus in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Consumer Awareness in Developing Markets

Consumer education gaps in emerging markets constrain beta-glucan adoption despite growing health consciousness and disposable income. Scientific substantiation requirements vary significantly across developing markets, creating compliance complexities that favor established multinational players over local manufacturers. The disconnect between traditional dietary practices and modern functional food concepts requires substantial consumer education investments that many beta-glucan suppliers cannot justify given uncertain return timelines. Regulatory frameworks in developing markets often lack specific guidelines for beta-glucan health claims, creating market entry barriers and limiting promotional messaging effectiveness. This awareness deficit particularly impacts premium-priced beta-glucan products where consumer understanding of functional benefits directly correlates with purchase intent and willingness to pay price premiums.

Variability in Functional Efficacy Across Sources

Source-dependent efficacy variations create quality consistency challenges that undermine consumer confidence and complicate regulatory approval processes. Beta-glucan molecular weight, structural configuration, and extraction methods significantly influence bioactivity, with studies showing that molecular weight variations affect prebiotic efficacy and immune response modulation. The FDA's requirement for comprehensive safety evaluations and toxicological studies for each beta-glucan source, as demonstrated in GRAS notices for Antrodia and white button mushroom extracts, creates regulatory complexity and market entry barriers. Extraction method variations, including enzymatic, alkaline, and subcritical water techniques, produce beta-glucan products with different physicochemical properties and biological activities, complicating standardization efforts. This variability particularly challenges smaller manufacturers lacking resources for comprehensive characterization and clinical validation studies. The resulting market fragmentation limits economies of scale and creates consumer confusion regarding product selection and expected health outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Cereals Anchor Market While Fungi Accelerate

Cereals and grains command 42.45% market share in 2025, reflecting established supply chains and regulatory acceptance for oat and barley-derived beta-glucans. The FDA's recognition of oat beta-glucan's cholesterol-lowering properties at a 3-gram daily intake supports market positioning, while Tate & Lyle's PromOat demonstrates commercial viability in organic food formulations. However, fungi-derived beta-glucans surge ahead with 8.49% CAGR through 2031, driven by superior bioactivity profiles and novel extraction opportunities. Seaweed and microalgae sources face regulatory hurdles, particularly in Europe, where EFSA novel foods approval requirements create market entry barriers despite promising bioactivity profiles.

The competitive landscape reveals strategic positioning differences across source categories, with cereal-based suppliers emphasizing cost efficiency and regulatory compliance while fungi-based producers focus on premium bioactivity and novel applications. Bacterial beta-glucan production through lactic acid bacteria fermentation offers in-situ enrichment opportunities for sourdough applications, addressing clean-label demands while enhancing nutritional profiles. This source diversification strategy enables risk mitigation against supply chain disruptions while capturing premium pricing for specialized applications.

By Category: Soluble Dominance Meets Insoluble Innovation

Soluble beta-glucans maintain a 72.05% market share in 2025, supported by established health claims and proven functionality in food applications. The European Food Safety Authority's approval of health claims for soluble beta-glucans reinforces market positioning, particularly for cholesterol reduction and glycemic response modulation. This category differentiation enables premium pricing strategies for specialized applications while addressing unmet needs in pharmaceutical and cosmetic formulations, where soluble forms prove inadequate.

Insoluble beta-glucans accelerate with a 8.81% CAGR through 2031, driven by emerging applications in personal care and specialized pharmaceutical formulations. The structural properties of insoluble forms enable unique delivery mechanisms, particularly in topical applications where sustained release and barrier function enhancement provide competitive advantages. Additionally, beta-glucans that were insoluble stimulated immune response through macrophage activation and strengthening of the gut barrier. These compounds also improved digestive health by increasing fecal volume and maintaining regular bowel movements, making them essential components in immunity and digestive health supplements.

By Application: Food Dominance Challenged by Personal Care Surge

Food and beverage applications secure 43.92% market share in 2025, anchored by established regulatory pathways and consumer acceptance of functional foods. General Mills' whole grain portfolio, with 86% of cereals providing at least 8 grams of whole grain per serving, demonstrates a major manufacturer's commitment to beta-glucan incorporation, according to the General Mills sustainability report 2024. Bakery and confectionery segments benefit from beta-glucan's functional properties as thickeners and stabilizers, while beverage applications leverage immune health positioning.

Personal care and cosmetics applications surge with 8.68% CAGR through 2031, reflecting beauty-from-within trends and scientific validation of topical benefits. Beta-glucan's wound healing, antioxidant, and anti-inflammatory properties enable premium positioning in skincare formulations, with research demonstrating efficacy in cosmetic applications. According to the Office for National Statistics data from 2024, consumer spending on personal care in the United Kingdom was GBP 41.9 billion . Pharmaceutical applications benefit from beta-glucan's immunomodulatory effects and drug delivery capabilities, with GRAS approvals expanding formulation possibilities. Animal feed applications leverage beta-glucan's immune enhancement properties, reducing antibiotic dependency while improving livestock health outcomes. This application diversification reduces dependence on traditional food markets while capturing higher margins in specialized segments.

Geography Analysis

Europe's market leadership stems from comprehensive regulatory frameworks and established consumer acceptance of functional foods, with the European Food Safety Authority's health claims database providing market clarity for beta-glucan applications. The region's 33.10% market share in 2025 reflects mature supply chains and sophisticated consumer understanding of functional benefits. The KELP -EU project's EUR 6 million investment in sustainable seaweed biorefinery demonstrates European commitment to source diversification while addressing environmental sustainability mandates. Brexit implications continue affecting supply chain logistics and regulatory harmonization, creating opportunities for domestic production expansion.

Asia-Pacific's 8.99% CAGR through 2031 reflects accelerating health consciousness and expanding nutraceutical markets across diverse economies. India's expanding middle class and growing awareness of preventive healthcare drive demand for functional ingredients, while regulatory harmonization across ASEAN markets facilitates regional expansion strategies. The region's diverse dietary traditions create opportunities for culturally adapted beta-glucan formulations.

North America benefits from established oat production infrastructure and regulatory clarity through FDA GRAS approvals, enabling efficient market entry for beta-glucan products. The region's mature functional foods market and sophisticated consumer base support premium positioning strategies, while vertical integration opportunities in agriculture and processing create competitive advantages. Supply chain vulnerabilities in grain sourcing, highlighted by Colorado's local grain supply chain challenges, create opportunities for regional diversification strategies. South America and Middle East and Africa represent emerging opportunities with growing health consciousness and expanding middle-class populations, though regulatory frameworks remain underdeveloped compared to established markets.

Regulatory Landscape

In the United States, beta-glucan commercialization for foods and beverages is governed by FDA labeling and ingredient-safety pathways. The FDA permits authorized health claims for soluble fiber from certain foods, including beta-glucan from oats, in relation to coronary heart disease risk under 21 CFR 101.81, which shapes label language and the minimum-qualifying intake levels used by brand owners.

In the European Union, established beta-glucan sources for foods and supplements coexist with tighter gatekeeping for new sources through the Novel Food framework under Regulation (EU) 2015/2283. A concrete marker is the European Commission Implementing Regulation (EU) 2024/1046, effective from 30 April 2024, which authorized beta-glucan from Euglena gracilis as a novel food with a time-bound exclusivity/data protection period for the applicant. Such authorizations define conditions of use and can accelerate entry for approved suppliers, while also raising the evidence bar for competing novel sources.

Value Chain Analysis

The beta-glucan value chain starts with sourcing from cereals and grains (notably oats and barley) and microbial biomass such as yeast (for example, Saccharomyces cerevisiae), with emerging inputs from fungi and microalgae where permitted. Upstream availability and price volatility of grains and fermentation substrates shape the cost base, while supplier qualification increasingly depends on documentation linked to regulatory status, such as GRAS in the United States or Novel Food authorization in the European Union.

Midstream processing focuses on extraction and purification, typically combining milling or cell-disruption steps with aqueous extraction, filtration, and concentration (including membrane processes such as ultrafiltration) to meet functional specifications like solubility and molecular weight profile. Downstream, ingredient manufacturers sell standardized powders or soluble concentrates to food and beverage formulators and supplement brands, either directly or via distributors, with technical application support such as sensory management, beverage stability, and dose delivery serving as a value-add. Key bottlenecks include consistent quality characterization across sources and batches, and the ability to compile regulatory-ready dossiers to support labeling and permissible use claims.

Competitive Landscape

The beta-glucan market exhibits moderate fragmentation, with major companies including Kerry Group, DSM-Firmenich, and Angel Yeast Co. Ltd. These companies maintain market positions through strategic initiatives. These companies have prioritized product innovation, particularly in developing specialized beta-glucan formulations for diverse applications ranging from food and beverages to pharmaceuticals and personal care products.

The industry has witnessed a significant focus on research and development activities, with companies investing in new extraction technologies and improved production processes to enhance product quality and efficiency. Strategic partnerships, especially with research institutions and distribution networks, have emerged as a key trend to expand market reach and technological capabilities. Companies are also actively pursuing geographical expansion through new manufacturing facilities and distribution centers, particularly in emerging markets, while simultaneously strengthening their presence in established regions through acquisitions and collaborations.

Technology adoption patterns reveal divergent strategies, with established players emphasizing process optimization and cost efficiency while newcomers pursue premium positioning through advanced extraction technologies and novel source materials. White-space opportunities emerge in personalized nutrition applications and targeted therapeutic interventions, where beta-glucan's immunomodulatory properties enable precision health solutions.

Beta Glucan Industry Leaders

Kerry Group

DSM-Firmenich

Tate & Lyle Plc

Lesaffre International

Angel Yeast Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity lies in expanding the addressable supply base beyond traditional oat and barley by scaling fermentation-derived and other novel-source beta-glucans that address formulation constraints such as water solubility, dispersion, and taste neutrality in beverages and dairy matrices. February 2025 activity from Layn Natural Ingredients provides a relevant example: the company opened an expanded biotechnology facility in Guangxi, China and commercialized a precision-fermentation-derived, water-soluble polysaccharide positioned as a functional alternative to conventional beta-glucans, indicating continued investment aimed at improving manufacturability and application performance.

Regulatory milestones are also creating clearer commercial lanes for differentiated sources and proprietary ingredients, supporting premiumization and broader application adoption. In the EU, the 30 April 2024 authorization of beta-glucan from Euglena gracilis as a novel food (Implementing Regulation (EU) 2024/1046) provides a defined route for microalgae-derived formats within approved use conditions, while the United States GRAS pathway continues to be used to broaden permitted ingredient options across food categories such as beverages, bars, and cultured dairy. Across applications, personal care and cosmetics, alongside immune- and gut-health positioned foods, remain key whitespace for suppliers that can combine standardized analytical methods with compliant, claim-supportive positioning.

Recent Industry Developments

- June 2026: YiDa Chemicals announced commercial production and promotion of Salecan, a water-soluble beta-glucan produced via biological fermentation using Rhizobium pusense ZX09. The move broadens fermentation-based supply options beyond traditional cereal and yeast sources and supports formulators seeking highly soluble glucans for beverages and other applications.

- February 2025: Layn Natural Ingredients developed and introduced Galacan at its expanded biotechnology facility, positioning it for gut health, inflammatory response modulation, and personal care applications while pursuing FDA GRAS certification. The combination of facility expansion and a new fermentation-derived ingredient highlights ongoing investment in scalable production routes designed to improve bioavailability and solubility.

- April 2024: The European Commission authorized beta-glucan from Euglena gracilis microalgae as a novel food under Implementing Regulation (EU) 2024/1046, including a defined exclusivity/data protection period for the applicant. This authorization expands the set of approved beta-glucan sources in the EU and raises competitive stakes for suppliers targeting differentiated microalgae-derived ingredients.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of beta-glucan ingredients sold for use in food and beverages, dietary supplements, pharmaceuticals, personal care and cosmetics, and animal feed, across major producing and consuming regions. It includes soluble and insoluble beta-glucans from cereals and grains, yeast, fungi, and microalgae.

Scope exclusions: We do not count finished consumer products or other bioactives and fibers that are not beta-glucan.

Segmentation Overview

- By Source

- Cereals and Grains

- Fungi

- Yeast

- Seaweed and Microalgae

- Others

- By Category

- Soluble

- Insoluble

- By Application

- Food and Beverage

- Bakery and Confectionary

- Beverage

- Snacks

- Dairy and Dairy Products

- Others

- Personal Care and Cosmetics

- Pharmaceuticals

- Animal Feed

- Others

- Food and Beverage

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We started with desk research to set a clear fact base on where beta-glucan is used, and what the realistic source and application mixes look like by region. Public references helped anchor the early model, such as USDA and other national agriculture statistics for oats and barley, FAO and UN Comtrade tables for trade flows, and health-claim guidance published by agencies such as the FDA and EFSA.

To reduce single-source bias, we also reviewed peer-reviewed nutrition and formulation studies, association websites for functional ingredients, plus company filings and investor presentations that describe ingredient portfolios. Paid subscriptions for company financials and news, and for patent databases, were used selectively to cross-check producer presence and product positioning. These desk sources are illustrative only, and many other public references were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

We then spoke with industry participants across the value chain, including ingredient manufacturers, distributors, formulators, and downstream product teams in food, supplements, personal care, and feed. Inputs from these discussions helped confirm what is sold as beta-glucan, typical pricing logic by source and solubility, and how demand varies across the Americas, EMEA, and APAC so desk assumptions could be corrected.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 15% | APAC: 44% |

| Mid tier: 47% | Functional/Unit leaders: 25% | EMEA: 30% |

| Smaller Players: 22% | Managers: 60% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up logic, and the two views were made to meet after repeated checks. On the top-down side, the addressable demand pool was reconstructed by linking end-use output to beta-glucan adoption, and then applying penetration and usage-rate assumptions that were validated through interviews.

The model used market-specific inputs such as production and trade indicators for oats and barley, shifts in mix between cereal, yeast, fungi, and microalgae sources, and the split between soluble and insoluble formats. Application signals, including functional foods, supplements, skin care, and feed inclusion, were used to keep volumes realistic, followed by an ASP range approach by source and grade that was adjusted for region and pack-size economics. For forecasting, scenario analysis was used, where demand growth, application mix, and price progression were varied within ranges that experts considered workable under current regulatory and labeling conditions. Where country coverage was thin in a bottom-up view, the missing portion was filled through ratio-based scaling from comparable markets, and then rechecked using distributor and formulator feedback.

Data Validation & Update Cycle

Outputs were validated in steps, starting with consistency checks between application totals, regional shares, and implied pricing. When an outlier appeared, assumptions were revisited, the model was re-run with tightened ranges, and select experts were re-contacted to confirm what changed.

Before sign-off, the work goes through analyst reviews so that double counting between sources, unit-conversion errors, and currency timing issues are caught early. Reports are refreshed annually, with interim updates when material events occur, such as meaningful capacity additions or major regulatory actions. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Beta Glucan Market Size Compared Against Other Published Estimates

Published market sizes for beta-glucan can differ even when similar applications are described, and the gaps usually come from scope cutoffs, pricing assumptions, and base-year timing. Currency conversion dates and the choice of whether to price at ingredient selling levels or finished product value can also move totals.

Some external estimates start from a 2024 value and may blend adjacent wellness ingredient spend into the beta-glucan total when immune health claims are discussed. For Mordor Intelligence, the count is limited to beta-glucan ingredient revenue across defined sources and soluble and insoluble categories, and it is tied to a 2026 base that is checked against current source mix and application adoption.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.74 B (2026) | |

| Industry Publisher A | USD 0.65 B (2024) | Uses a 2024 base year and can reflect a narrower counted pool when only selected applications are sized, which may understate demand from personal care and animal feed that grows later in the period. |

| Industry Publisher B | USD 0.68 B (2024) | Anchors the market in 2024 and may apply faster ASP progression from supplements-led demand, which can lift implied totals compared with a range-checked pricing model by source and solubility. |

Across the three figures, the spread is mainly explained by base-year choice and whether only beta-glucan ingredients are counted or adjacent items are included. When the scope is kept consistent and then reconciled using signals like source mix, solubility split, and end-use adoption, the final number becomes easier to repeat and update year to year.

Key Questions Answered in the Report

What is the current global value of the beta-glucan market?

The beta glucan market was valued at USD 744.44 million in 2026 and is projected to climb to USD 1.09 billion by 2031.

Which region holds the largest share of beta glucan sales?

Europe leads with 33.10% share, benefiting from harmonized EFSA health-claim rules and consumer familiarity with functional foods.

Which source is growing fastest within the beta glucan market?

Fungi-derived beta glucans are expanding at 8.49% CAGR thanks to superior bioactivity and precision-fermentation capacities.

What is driving beta-glucan adoption in personal care?

Clinical evidence of skin-repair and anti-inflammatory benefits, combined with rising “beauty-from-within” trends, is fueling 8.68% CAGR in cosmetic applications.

Page last updated on: