Veterinary Telehealth Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 335.73 Million |

| Market Size (2030) | USD 802.53 Million |

| Growth Rate (2026 - 2031) | 19.04% CAGR |

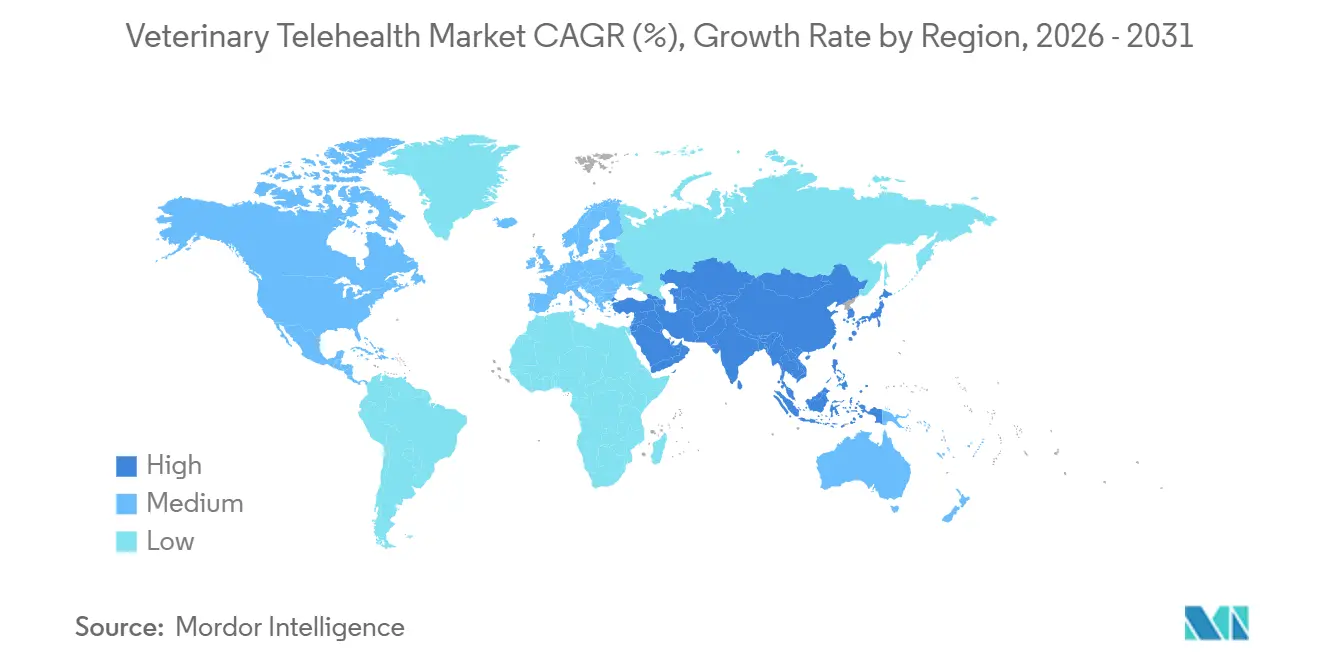

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

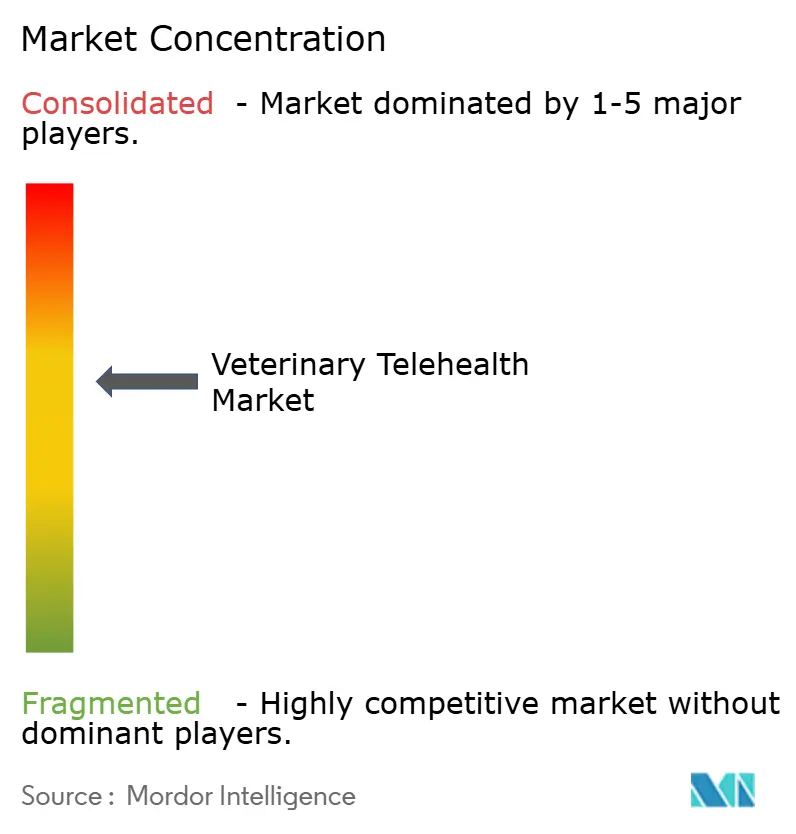

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Telehealth Market Analysis by Mordor Intelligence

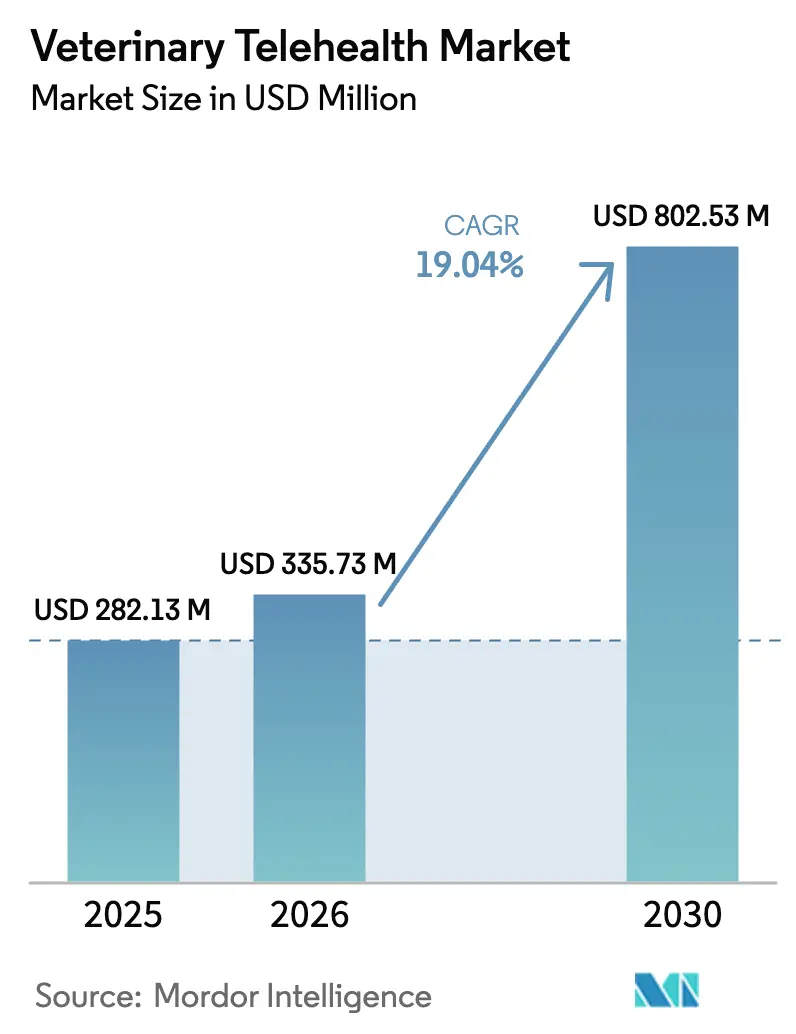

The Veterinary Telehealth Market size is expected to increase from USD 282.13 million in 2025 to USD 335.73 million in 2026 and reach USD 802.53 million by 2030, growing at a CAGR of 19.04% over 2026-2030.

Robust pet-humanization, post-pandemic regulatory flexibility, and AI-enabled wearables are jointly redefining access models and cementing virtual care as a frontline service. North America continues to anchor revenues, yet the Asia-Pacific growth curve is steeper as fast-rising pet ownership collides with a shortage of brick-and-mortar clinics. Continuous remote monitoring is outpacing synchronous video visits because insurers now bundle subscription-based telemetry into mainstream policies. Competitive rivalry intensifies around platform scale, wearable integration, and usage-based pricing, while fragmented licensing laws and uneven reimbursement blunt momentum in certain jurisdictions.

Key Report Takeaways

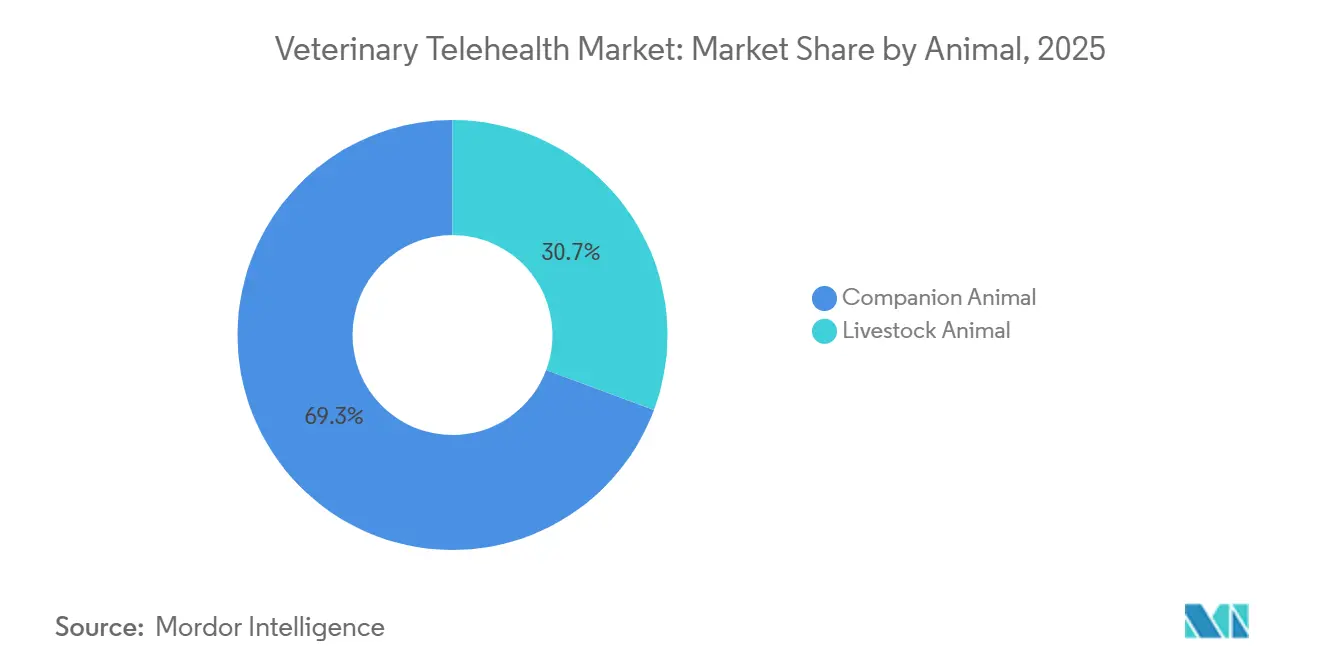

- By animal, companion species led with 69.32% of the veterinary telehealth market share in 2025 and is expected to register the fastest CAGR with 20.22% through 2031.

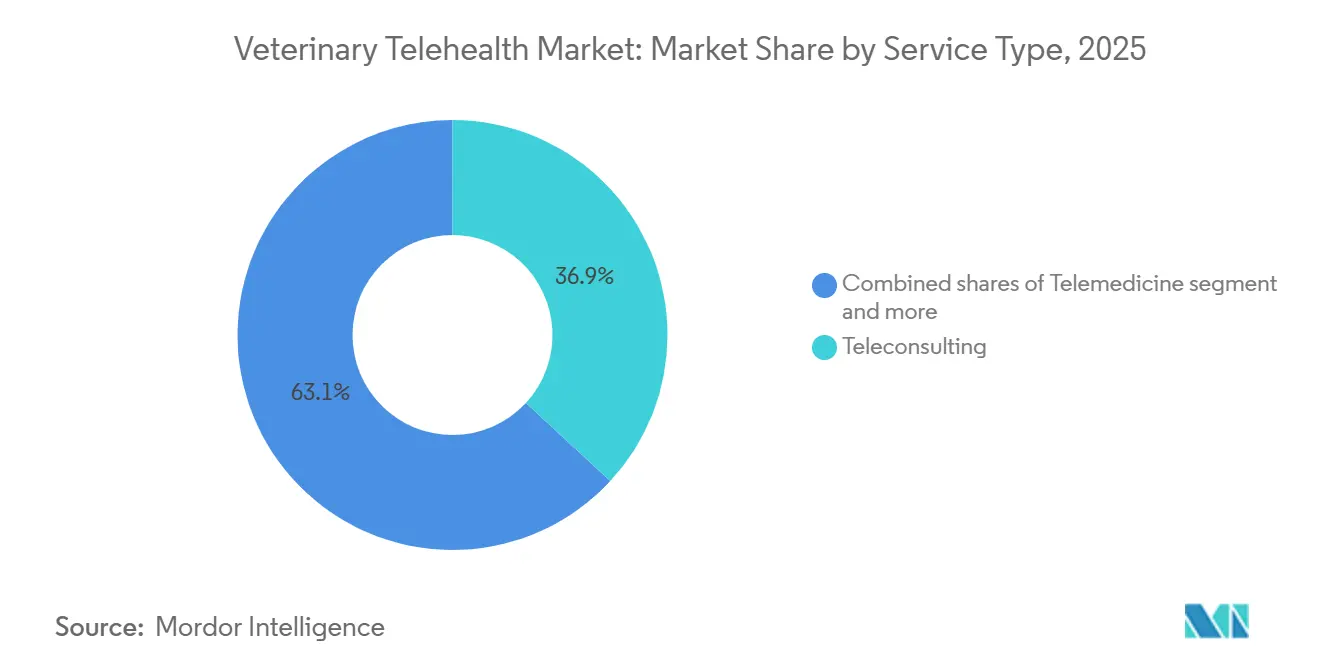

- By consultation modality, synchronous segment led with 45.61% market share in 2025, and remote patient monitoring is projected to expand at a 19.98% CAGR through 2031, the fastest among all modalities.

- By delivery mode, cloud and app-based platforms captured 71.23% revenue in 2025 and are poised for a 21.22% CAGR through 2031.

- By end user, the veterinary clinics & hospitals led with 57.7% share in 2025, yet telehealth platform providers are forecast to register a 20.65% CAGR through 2031, eroding the dominance of traditional clinics.

- By region, Asia-Pacific is expected to rise at a 20.99% CAGR through 2031, while North America retained 45.3% of global revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Telehealth Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing pet ownership & humanization wave | +4.2% | Global, strongest in North America, Western Europe, and urban APAC | Medium term (2-4 years) |

| Rising veterinary healthcare spending and insurance coverage | +3.8% | North America, Europe, and emerging urban APAC | Medium term (2-4 years) |

| Regulatory flexibility post-COVID is accelerating telehealth adoption | +3.5% | United States, United Kingdom, Germany, select APAC | Short term (≤2 years) |

| The growing prevalence of zoonotic diseases is elevating remote triage demand | +2.9% | Global with APAC and Africa hot spots | Long term (≥4 years) |

| AI-enabled wearables & remote diagnostics expanding clinical use-cases | +3.1% | North America, Europe, scaling APAC | Medium term (2-4 years) |

| Usage-based pet-insurance models rewarding virtual-first care | +2.6% | North America, Western Europe, Australia pilots | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Pet Ownership & Humanization Wave

Ninety-four million U.S. households owned a pet in 2025, an all-time peak fueled by millennial and Gen Z adoption patterns [1]American Pet Products Association, “Pet Industry Market Size, Trends & Ownership Statistics,” americanpetproducts.org. Younger cohorts treat pets as family, channel discretionary income into premium veterinary services, and favor virtual care that aligns with digital-first lifestyles. China’s 120 million pet-owning households and India’s expanding middle class multiply the addressable base for localization-ready platforms. Preventive care and chronic-disease management, well-suited to telemonitoring gain momentum as owners increasingly demand continuous oversight rather than episodic clinic visits. This demand spike sustains pricing power for platforms that pair convenience with clinically validated advice.

AI-Enabled Wearables & Remote Diagnostics Expanding Clinical Use-Cases

Smart collars capturing heart rate, respiration, and activity streams let clinicians flag anomalies before symptoms surface. PetPace’s V3.0 sensor suite, launched in 2024, applies machine-learning algorithms to alert both owner and veterinarian in real time [2]PetPace, “PetPace V3.0 Smart Collar Launch,” petpace.com. Precision livestock farming now equips cattle and swine with telemetry tags that detect estrus or early disease, curbing on-farm morbidity and travel costs. As algorithm accuracy improves with larger datasets, veterinarian trust in remote diagnostics rises, closing a feedback loop that accelerates adoption. Subscription revenue tied to continuous monitoring lowers platform churn and deepens lifetime value.

Usage-Based Pet-Insurance Models Rewarding Virtual-First Care

Nationwide embeds unlimited telehealth visits in its flagship Whole Pet with Wellness plan, steering policyholders toward virtual triage over higher-cost in-clinic diagnostics. The National Association of Insurance Commissioners tallied 6.25 million insured U.S. pets in 2024, up from 4.8 million in 2022, and telehealth usage is growing even faster [3]National Association of Insurance Commissioners, “Pet Insurance Market Report 2024,” naic.org. Early pilots in Australia and the United Kingdom show emergency-visit frequency falling 15-20% when insurers incentivize online consultations. Lower claim severity boosts insurer margins, encouraging broader reimbursement for remote monitoring devices and asynchronous follow-ups.

Regulatory Flexibility Post-COVID Accelerating Telehealth Adoption

Colorado HB24-1048, Texas HB3364, Ohio HB96 & SB60, and Florida HB849 abolished the mandatory in-person exam to establish a veterinarian-client-patient relationship for non-controlled substances during 2024-2025. The American Veterinary Medical Association’s December 2025 policy update now allows remote consultations in emergencies, mitigating workforce shortages that are projected to leave the United States short 15,000 veterinarians by 2030. Reduced compliance friction encourages investors to treat veterinary telehealth as infrastructure, not a pandemic stopgap.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Service Costs & Limited Reimbursement Pathways | -2.4% | Global, most acute in uninsured segments and emerging markets (Latin America, MEA, rural APAC) | Medium term (2-4 years) |

| Licensing-Law Variability Restricting Cross-Border Care | -1.8% | North America (state-by-state fragmentation), Europe (country-level barriers), APAC (nascent frameworks) | Long term (≥ 4 years) |

| Fragmented Data Interoperability Hindering AI Triage Accuracy | -1.5% | Global, with highest friction in North America and Europe due to legacy EHR systems | Medium term (2-4 years) |

| Post-Pandemic Owner Preference Swings Back To In-Clinic Exams | -2.1% | North America and Western Europe (mature markets with established clinic infrastructure) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Service Costs & Limited Reimbursement Pathways

Single teleconsultations cost USD 30-75, still steep for uninsured owners in lower-income regions. Although 6.25 million U.S. pets carried coverage in 2024, that equals under 7% of the national pet population, leaving most owners to pay out-of-pocket. Insurer policies vary on co-pays, pre-existing conditions, and device reimbursements, complicating the consumer value proposition. In markets where pet insurance penetration sits below 2%, platforms must underprice in-clinic alternatives, compress margins and slowing expansion.

Licensing-Law Variability Restricting Cross-Border Care

Veterinary licensing stays jurisdiction-specific. A California-licensed veterinarian cannot legally advise a Texas pet owner without an additional license, curbing national platform scalability. Europe mirrors the hurdle: each member state enforces distinct veterinary credentials, and GDPR health-data provisions add compliance overhead. Data silos hamper AI models that depend on diverse clinical inputs, stalling improvements in diagnostic accuracy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal: Companion Dominance Anchors Revenue, Livestock Lags

Companion species captured 69.32% of the veterinary telehealth market share in 2025, and growth is projected at 20.22% CAGR through 2031. The companion segment’s dominance reflects high household affinity for dogs and cats, which together exceed 90% of virtual-care volumes. Over the same horizon, bovine and swine deployments rise as rural broadband and sensor economics improve, but livestock still trails in revenue contribution.

Platform strategies revolve around user experience and insurance tie-ins because price competition escalates once basic connectivity hurdles fall. Equine telehealth remains niche; gait-analysis video assessments gain traction, yet tactile examinations keep many owners reliant on traditional visits. The other category—avian, reptile, exotic grows as specialty veterinarians market their expertise to dispersed clients, though its influence on the overall veterinary telehealth market size remains small.

By Delivery Mode: Cloud Infrastructure Captures Scale Economies

Cloud and app-based systems held 71.23% of revenue in 2025 and are expected to post a 21.22% CAGR to 2031, underscoring the shift away from on-premise servers that burden clinics with IT overhead. SaaS practice-management bundles combine scheduling, EHR, billing, and teleconsultation into one interface, reducing friction for first-time adopters.

Data aggregation across multiple practices fuels algorithm training, creating predictive triage tools that strengthen platform stickiness and defend pricing. On-premise systems maintain relevance within large hospital chains, prioritizing data sovereignty, but this slice of the veterinary telehealth market is set to recede as cloud security certifications multiply and regulatory comfort rises.

By Service Type: Telemonitoring Gains as Insurers Seek Cost Control

Teleconsulting remained the entry gateway with 36.88% share in 2025. Still, telemonitoring is forecast for a 19.6% CAGR to 2031 as insurers fund preventive telemetry that curbs emergency claims. The veterinary telehealth market size attached to remote monitoring is therefore expanding faster than any other service line.

Continuous health streams from glucose meters and smart collars produce longitudinal datasets that flag disease early. Platforms monetize device-linked subscriptions, swapping one-time consult fees for recurring revenue. Broadening VCPR flexibility since 2024 lets providers stitch teleconsulting and monitoring into blended care pathways, pushing utilization higher for chronic-disease cohorts.

By Consultation Modality: Asynchronous Gains Traction, Real-Time Retains Premium

Real-time video and chat commanded 45.61% share in 2025, valued for immediate reassurance in urgent scenarios. Remote patient monitoring, however, is slated for the swiftest 19.98% CAGR, reflecting owner comfort with continuous oversight over episodic check-ins.

Asynchronous “store-and-forward” uploads cut costs for non-urgent needs. AI triage routes cases to specialty veterinarians only when needed, stretching workforce capacity and lowering owner spend. AVMA’s December 2025 emergency-consult rule change legitimizes this hybrid pathway, blending low-cost asynchronous intake with escalated synchronous care as required.

By End User: Platform Providers Disrupt Traditional Clinic Revenue

Veterinary clinics and hospitals held 57.7% share in 2025, yet platform providers are tracking a 20.65% CAGR to 2031, steadily expanding their slice of the veterinary telehealth market size. Marketplace models such as Vetster match surplus veterinary capacity with consumer demand globally, bypassing geographical barriers.

Retail alliances deepen disruption: Walmart bundled Pawp telehealth into Walmart+ subscriptions for unlimited consults, leveraging 230 million weekly shoppers. Insurance carriers, e-commerce sites, and employer wellness programs fall under “Others,” each weaving telehealth into broader ecosystems to increase stickiness and cross-sell opportunities.

Geography Analysis

North America delivered 45.3% of 2025 revenue, buoyed by dense pet ownership, mature insurance, and five key state bills that eased VCPR rules between 2024 and 2025. Canada quickly aligned its provincial frameworks, letting binational platforms operate smoothly. Yet AVMA data show that veterinarian telehealth usage slid from 38% in 2023 to 29.2% in 2024 as some owners reverted to clinics once pandemic restrictions eased.

Asia-Pacific is poised for a 20.99% CAGR through 2031. China’s 120 million pet homes and India’s surging urban pet adoption catalyze mobile-first platforms backed by e-commerce titans. Japan and South Korea focus on geriatric-care telemonitoring, while Australia pilots insurance incentives for virtual-first pathways. Regulatory heterogeneity and low insurance coverage in segments of Southeast Asia temper the speed of scale.

Europe occupies a middle tier. The United Kingdom, Germany, and France lead thanks to established insurance cultures, but cross-border licensing remains a drag. GDPR raises compliance spend, prompting many platforms to limit operations to a single country. Middle East & Africa and South America represent emerging nodes; São Paulo and Dubai show pockets of high-income demand, though currency volatility and patchy broadband slow broader rollout.

Competitive Landscape

No single vendor exceeds a major global share, marking the veterinary telehealth market as structurally fragmented. Competition orbits three axes: veterinary-network breadth, wearable and EHR integration depth, and insurer-aligned pricing. Chewy exploited its 20 million-user e-commerce base to surpass 1 million virtual consults by March 2025, showcasing the reach advantage of incumbent retail ecosystems.

Walmart’s Pawp alliance illustrates retail’s push for ancillary revenue streams, while pure-play marketplaces Vetster and AirVet court independent veterinarians with favorable revenue splits. Technology moats widen as PetPace pairs patented AI analytics with hardware to lock in subscribers and feed continuous data loops, evidenced by a 40% rise in veterinary AI patent filings from 2023-2025.

Regulatory mastery differentiates scale aspirants from regional players: those adept at multistate licensing and EHR interoperability deliver seamless nationwide service, while single-state operators face plateauing addressable markets. Livestock telehealth remains an open frontier; platforms that secure rural connectivity partnerships could command outsized early-mover gains.

Veterinary Telehealth Industry Leaders

Chewy inc.

Vetster

AirVet

Zoetis

VitusVet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Dial A Vet teamed with Pawssum Mobile Vets to link virtual triage to in-home visits, offering a continuous “online-to-doorstep” care pathway.

- December 2025: AVMA amended its telemedicine policy to allow emergency-only remote consultations without prior exams, broadening virtual care eligibility.

- March 2025: Chewy confirmed its Connect With a Vet service crossed 1 million consults since launch.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the veterinary telehealth market as all fee-based real-time or asynchronous remote clinical interactions, video, voice, text, or app, between licensed veterinarians and animal owners or caretakers, delivered through cloud, web, or phone-enabled platforms. The valuation captures gross platform service revenues plus professional service fees for companion and livestock animals worldwide, amounting to USD 282.13 million in 2025.

Scope Exclusions: one-off software license sales, diagnostic hardware, generic practice management systems, and non-clinical pet wellness apps remain outside the scope.

Segmentation Overview

- By Animal

- Companion Animals

- Livestock

- By Delevery Mode

- On Premise

- Cloud/App Based

- By Service Type

- Telemedicine

- Teleconsulting

- Telemonitoring

- Other Service Types

- By Consultation Modality

- Synchronous (Real-time Video/Chat)

- Asynchronous (Store-and-Forward)

- Remote Patient Monitoring

- By End User

- Veterinary Clinics & Hospitals

- Telehealth Platform Providers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and pulse surveys with platform founders, mixed animal clinicians across North America, Europe, and Asia-Pacific, and national regulatory advisors validated utilization rates, average consult pricing, and region-specific Veterinary-Client-Patient-Relationship (VCPR) rules, enabling us to adjust desk-derived assumptions with real-world behavior.

Desk Research

Our analysts first mapped publicly available veterinary service utilization, pet population, and livestock herd data from sources such as the World Organisation for Animal Health, USDA-APHIS, Eurostat livestock statistics, and national veterinary associations. Trade databases (Volza import shipment codes for handheld imaging devices) helped approximate hardware adoption that correlates with teleconsult volume. Annual reports and 10-Ks from listed telehealth platform operators complemented trend signals, while Dow Jones Factiva screened 4,000+ news items for funding and regulatory moves. D&B Hoovers supplied baseline financials for private platforms. The sources cited are illustrative; numerous additional publications were reviewed to cross-verify facts.

Market-Sizing & Forecasting

A top-down reconstruction that starts with companion and production animal counts, typical annual consult rates, and telehealth penetration produced the first set of totals, which are then corroborated through selective bottom-up checks such as sampled average selling price multiplied by platform visit volumes shared confidentially by practitioners. Key fingerprints in the model include urban pet ownership growth, smartphone penetration, regulatory flexibilities post-COVID, average consult price progression, and venture funding inflow to telehealth platforms. Multivariate regression links these variables to historic revenue to forecast through 2030; scenario analysis adjusts for pending VCPR reforms.

Data Validation & Update Cycle

Outputs move through variance and anomaly checks, senior analyst review, and a second pass against independent indicators before sign-off. Reports refresh yearly, with interim re-contacts triggered by material events such as major regulatory changes or large platform funding rounds.

Why Our Veterinary Telehealth Baseline Commands Reliability

Published figures differ because each publisher frames the market in its own way and updates at different cadences. Service scope, animal cohorts, pricing capture, and refresh timing are the usual fault lines.

Key Gap Drivers include inclusion of hardware sales within service revenues, counting consumer wellness apps, or applying straight-line CAGR to dated baselines without VCPR scenario testing, which may inflate or dampen values.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 282.13 M (2025) | Mordor Intelligence | - |

| USD 365.20 M (2025) | Global Consultancy A | Adds telemedicine software licenses and bundled e-pharmacy revenue |

| USD 303.45 M (2024) | Regional Consultancy B | Uses 2024 base and extrapolates 20.8 % CAGR without separate livestock filter |

| USD 400.00 M (2024) | Industry Database C | Blends remote monitoring hardware with platform fees and applies revenue share mark-ups |

The comparison shows that once non-clinical or hardware streams are stripped out and penetration rates are stress tested through primary interviews, Mordor's disciplined approach delivers a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

How fast is the veterinary telehealth market growing between 2026-2031?

The sector is projected to post a 19.04% CAGR, climbing from USD 335.73 million in 2026 to USD 802.53 million by 2031.

Which animal category contributes the most revenue?

Companion animals, primarily dogs and cats, held 69.32% of global revenue in 2025 and remain the principal growth engine.

What delivery mode dominates current deployments?

Cloud and app-based platforms controlled 71.23% of 2025 turnover and are widening their lead because they reduce IT overhead for clinics.

Which consultation modality is expanding the quickest?

Remote patient monitoring is forecast to advance at a 19.98% CAGR through 2031, outpacing both synchronous and asynchronous formats

Why are insurers pushing telehealth adoption?

Usage-based pet insurance models lower claim costs by directing owners to lower-priced virtual triage before authorizing in-clinic diagnostics.

Page last updated on: