Tissue Paper Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.2 Billion |

| Market Size (2031) | USD 30.01 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

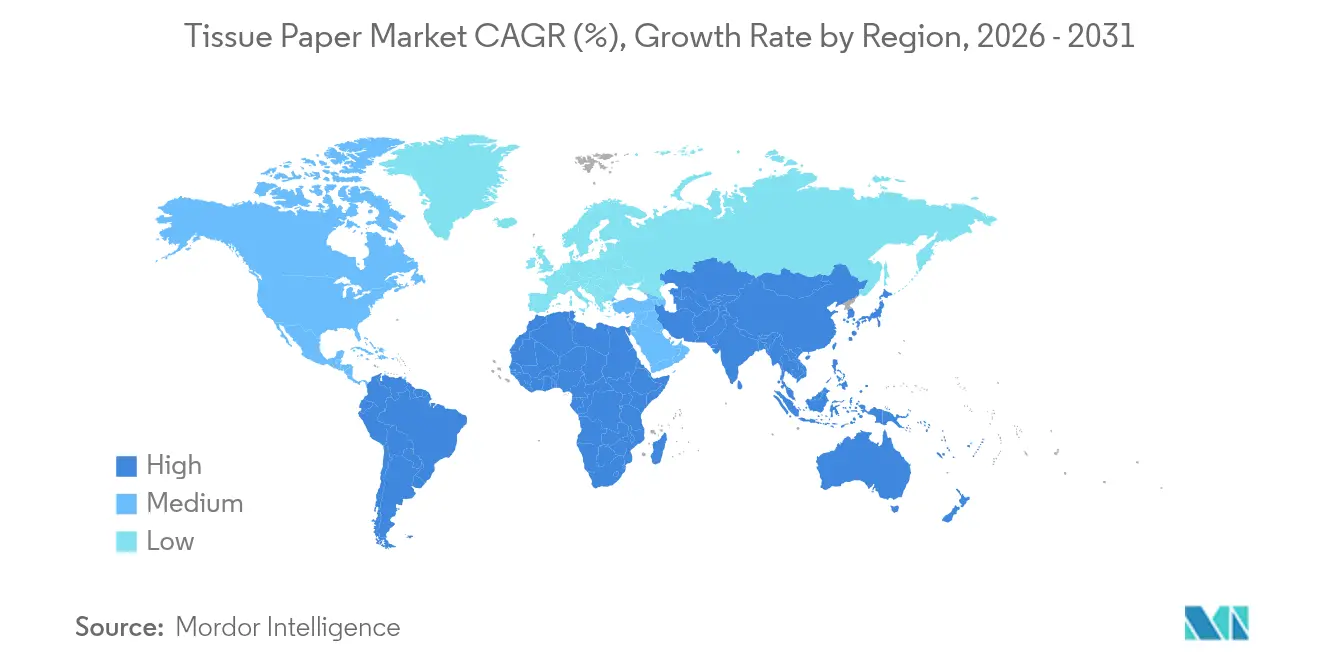

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tissue Paper Market Analysis by Mordor Intelligence

The global tissue paper market size was valued at USD 22.03 billion in 2025 and estimated to grow from USD 23.2 billion in 2026 to reach USD 30.01 billion by 2031, at a CAGR of 5.29% during the forecast period (2026-2031). This expansion shows the tissue paper market’s ability to absorb elevated fiber and energy costs while sustaining consumer demand. Large integrated mills have committed more than USD 3 billion to new capacity and acquisitions since 2024, underscoring confidence in steady long-term consumption. North American producers are modernizing lines with through-air-dried (TAD) technology that cuts manual operations by 85%, whereas Asia-Pacific converters scale recycled-fiber grades to meet urban hygiene needs. Regulatory pressure- from the EU Packaging and Packaging Waste Regulation (PPWR) to the EU Deforestation Regulation (EUDR)- is reshaping sourcing and packaging strategies but simultaneously creating niches for certified, traceable products. On the demand side, the commercial reopening of offices, schools, and HoReCa outlets is lifting the away-from-home channel and shifting the mix toward higher-margin towel and napkin formats.

Key Report Takeaways

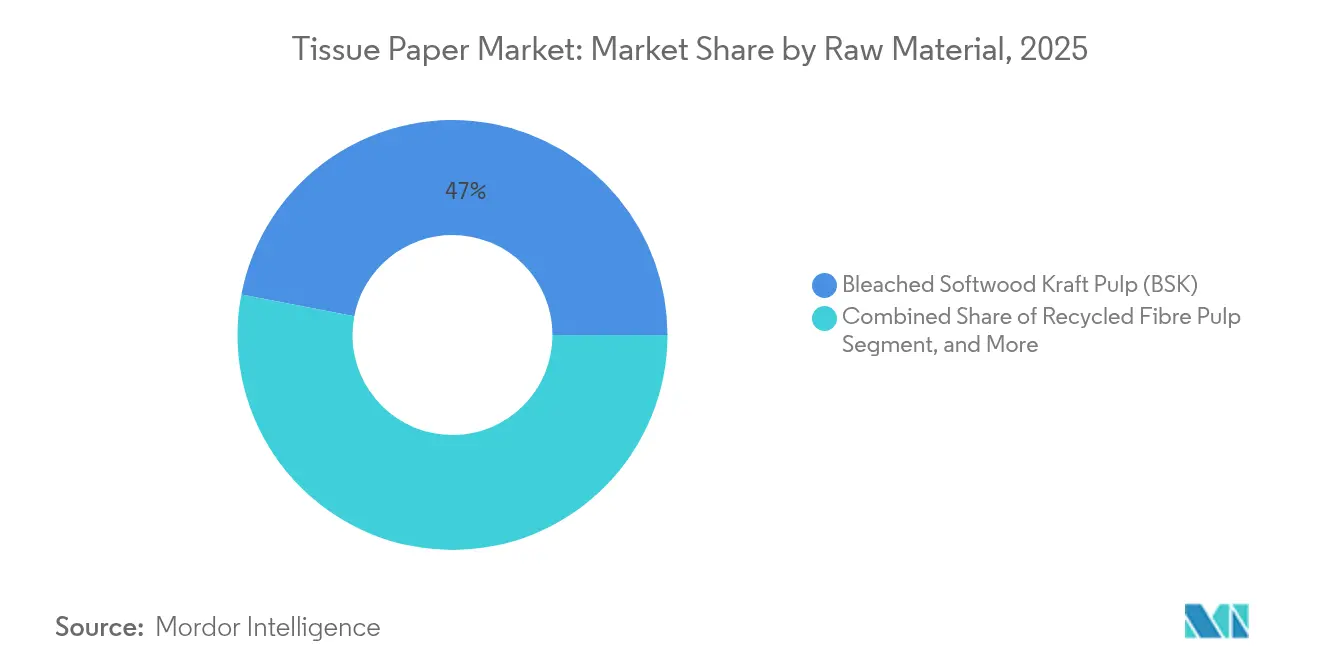

- By raw material, Bleached Softwood Kraft Pulp held 46.98% of the tissue paper market share in 2025, while recycled fiber pulp is projected to expand at a 6.34% CAGR through 2031.

- By product type, bathroom tissue commanded 57.90% of the tissue paper market size in 2025; paper towels are advancing at a 6.73% CAGR to 2031.

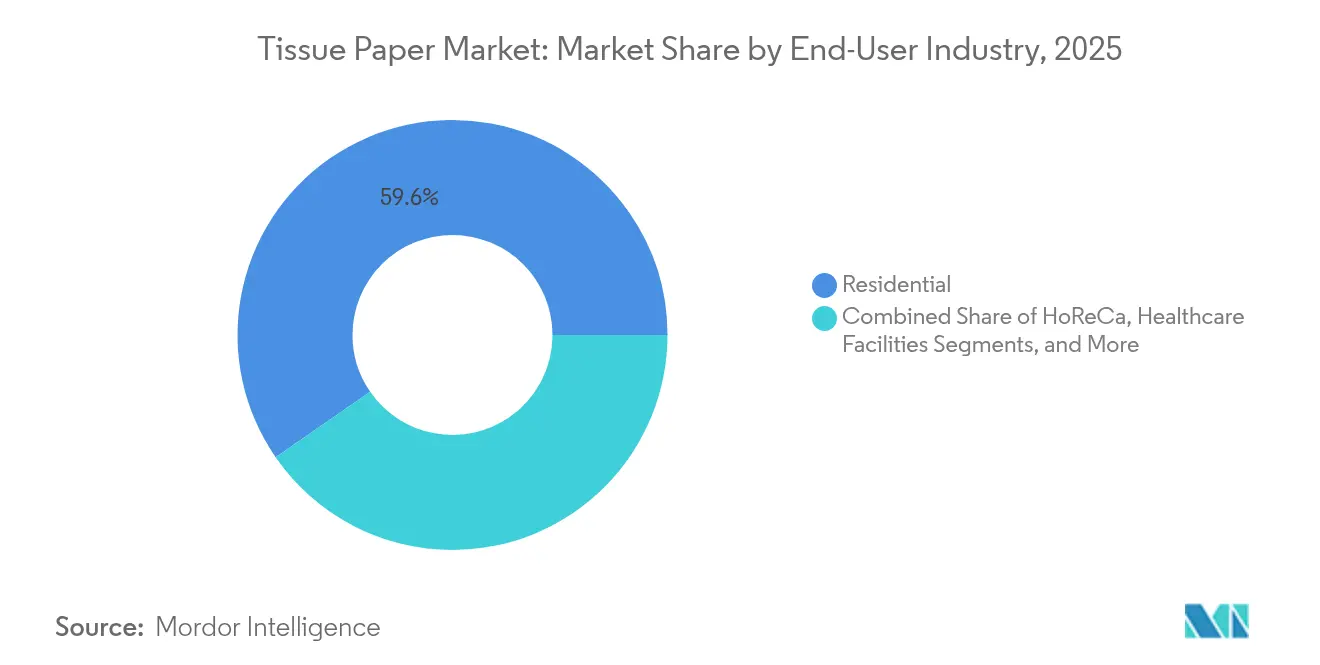

- By end-user, the residential segment accounted for 59.62% of the tissue paper market size in 2025, and offices and educational institutions are progressing at a 6.72% CAGR through 2031.

- By distribution channel, offline retail controlled 50.68% of the tissue paper market share in 2025, whereas online sales are widening at a 6.84% CAGR during the forecast period.

- By geography, North America led with 37.95% revenue share in 2025; Asia-Pacific is forecast to grow at an 7.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tissue Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing hygiene and sanitation expenditure | +1.2% | Global (strongest in Asia-Pacific) | Medium term (2-4 years) |

| Rapid away-from-home reopening post-COVID | +0.9% | North America and Europe; spillover to Asia-Pacific | Short term (≤ 2 years) |

| Capacity additions of large integrated mills | +0.8% | North America and Latin America | Long term (≥ 4 years) |

| E-commerce-led private-label tissue boom | +0.7% | North America and Europe; growing in urban Asia-Pacific | Medium term (2-4 years) |

| Plastic-free packaging mandates | +0.4% | Europe and North America; global regulatory spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Hygiene and Sanitation Expenditure

Escalating public-health awareness is translating into sustained tissue usage. National programs such as India’s Swachh Bharat Mission have delivered toilet access to 100 million rural households, changing hygiene habits and adding new volume to the tissue paper market. [1]M. Dey et al., “Cleaning Bharat (India): A Scoping Review...,” mdpi.com Institutional buyers likewise raise specifications: randomized trials in schools prove disposable wipes reduce contamination more effectively than traditional solutions, reinforcing demand for wet-strength toweling. Healthcare facilities champion antibacterial seat covers, a subcategory projected to reach USD 602.5 million by 2028, while commercial cleaning services valued at USD 117 billion in 2025, embed daily paper-based protocols. As hygiene budgets expand, producers with FSC and Green Seal portfolios capture procurement preference across hospitals, airports, and universities.

Rapid Away-from-Home Reopening Post-COVID

Return-to-office mandates and restored HoReCa footfall are reviving away-from-home consumption. In the United States, federal agencies reported toilet-paper stock-outs during the first quarter of 2025, exposing deferred procurement and triggering expedited contracts. European converters such as Lucart generated EUR 765 million (USD 817 million) in 2024 on the strength of AfH towels and napkins produced from recycled fibers, illustrating the channel’s rebound. Food-service operators, responsible for 27.5% of total food waste, are adopting premium napkins to support cleaner presentation, thereby nudging overall value per kilogram higher. Manufacturers are collaborating with facility managers to install smart dispensers that cut overuse and provide real-time refill alerts, turning hygiene into a data-driven service offering.

Capacity Additions of Large Integrated Paper Mills

Long-cycle investments are reshaping global supply. UPM’s 2.1 million-ton eucalyptus pulp complex in Uruguay, commissioned in 2024, boosts hardwood availability for Chinese tissue producers by more than 50%. In North America, Georgia-Pacific completed a USD 550 million expansion in Green Bay, adding a TAD line dedicated to paper towels and trimming manual labor requirements by 85%. Concurrently, Kimberly-Clark has earmarked over USD 2 billion for new U.S. capacity, including a greenfield site in Warren, Ohio that will employ 900 workers. These projects not only close regional supply gaps but also incorporate biomass cogeneration and water-recycling loops to cut scope-1 emissions.

E-Commerce-Led Private-Label Tissue Boom

Online platforms are redefining how households replenish tissue. Subscription models ship multi-month bundles straight to consumers, smoothing demand and lowering last-mile emissions through optimized parcel density. Retailers leverage the format by launching recyclable paper-based insulated mailers that align with plastic-free initiatives. Sustainability surveys in the United Kingdom show 78% of shoppers rank biodegradability as critical in packaging choices, prompting private-label operators to advertise recycled-fiber composition prominently. Branded manufacturers respond by elevating quality: Georgia-Pacific relaunched its ARIA line as a three-ply product made entirely from recycled fiber, positioning sustainability as a premium cue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile virgin pulp prices | -0.8% | North America and Europe | Short term (≤ 2 years) |

| ESG backlash over deforestation | -0.6% | Europe and North America; spreading to global supply chains | Medium term (2-4 years) |

| Freight container imbalance post-pandemic | -0.4% | Asia-Europe and Trans-Pacific routes | Short term (≤ 2 years) |

| Soft demand in low-income economies | -0.3% | Sub-Saharan Africa and parts of South Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Virgin Pulp Prices

Sharp swings in Northern Bleached Softwood Kraft and eucalyptus pulp have tightened tissue producer margins, forcing some mills to accelerate fiber-substitution trials. The closure of older fluff-pulp lines in the United States adds further supply uncertainty, encouraging converters to hedge inventories or lock multiyear contracts. Hardwood’s shorter fiber length enhances softness, yet the widened price spread versus softwood raises cost-mix questions for premium bath tissue. Producers are experimenting with bamboo and wheat straw to diversify inputs, but large-scale availability remains nascent. Mill downtime planning and procurement analytics thus become critical disciplines in safeguarding profitability.

ESG Backlash Over Deforestation

The EUDR, effective December 30, 2024, requires geolocation tracing of wood inputs and imposes fines equal to at least 4% of EU revenue for non-compliance. [2]Programme for the Endorsement of Forest Certification, “EU Deforestation Regulation Software,” pefc.org Only one-fifth of corporations have robust deforestation programs, indicating sizable readiness gaps. Mills with captive plantations gain an advantage because they can certify origin more easily, whereas converters reliant on multiple third-party suppliers confront additional due diligence layers. Sappi’s release-paper division is already building the IT backbone to issue mandatory Due Diligence Statements, highlighting the operational overhead now embedded in cross-border shipments. [3]Sappi, “Release Paper and the EU Deforestation Regulation,” sappi.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Softwood Strength Meets Recycled Fiber Momentum

Bleached Softwood Kraft Pulp accounts for nearly half of the tissue paper market size in 2025, sustaining premium strength and absorbency levels demanded by luxury bathroom and facial grades. Yet recycled fiber is posting the fastest climb, growing at a 6.34% CAGR as converters respond to EUDR scrutiny and brand owners’ circular-economy pledges. Several European lines now integrate through-air-dried technology that elevates recycled sheets to near-virgin softness, blurring historical quality gaps. The tissue paper market share for alternative fibers such as bamboo remains in single digits but garners interest from niche eco-labels seeking deforestation-free claims. Hardwood kraft pulp supplements softwood in layered ply structures to improve hand-feel without spiking furnish cost, while high-yield chemithermo-mechanical pulp caters to value-tier napkins and away-from-home rolls.

Recycled fiber’s rise also dovetails with brand-owner packaging shifts. As consumer-goods companies pivot toward paper-based wraps to satisfy plastic-free targets, collection rates of post-consumer corrugated and folding boxboard increase, enhancing furnish availability for tissue furnish. Mills that bolt on de-inking units target these streams, capturing cost savings and lowering scope-3 carbon footprints. Over the forecast horizon, recycled furnish penetration is set to temper virgin pulp exposure, giving risk-diversified suppliers a stronger negotiating hand.

By Product Type: Bathroom Tissue Dominance, Towel Upswing

Bathroom rolls held 57.90% of the tissue paper market share in 2025, owing to entrenched household habits and pandemic-era pantry stocking. Even so, paper towels exhibit the highest trajectory at a 6.73% CAGR, buoyed by commercial facilities’ elevated surface-wiping standards and household substitution away from textile dishcloths. The tissue paper market size for towels receives an added lift from TAD capacity that delivers plush, cloth-like textures prized in premium kitchen segments. Facial tissues cling to relevancy through lotion-infused and antiviral variants, while paper napkins benefit from HoReCa refurbishment, where operators upgrade to thicker emboss patterns for upscale presentation. Specialty tissue, wrapping, interleaving, and MG paper remain a boutique but profitable corner, serving confectionery, apparel, and fresh-produce niches.

Within bathroom tissue, brands are layering odor-neutralizing cores and biodegradable wet-wipe companions to differentiate beyond sheet count. Smart dispensers in airports and stadiums optimize roll changeovers and feed digital dashboards, fusing product with service. Towels, meanwhile, are migrating to sustainable packaging: plastic film overwraps are being replaced by molded-fiber belly bands that double as shelf signage, reinforcing the hygiene-and-eco dual value proposition.

By End-User Industry: Residential Stability, Institutional Rebound

Home consumption still accounts for 59.62% of the tissue paper market size, underpinned by enduring hybrid-work patterns that lift per-capita household usage. Consumers trade up to three-ply and scented variants, accepting higher unit prices in exchange for softness and wellness cues. Offices and educational facilities, however, post the fastest growth at 6.72% CAGR as occupancy normalizes. Universities embed higher-frequency cleaning regimens that call for dispenser-friendly roll formats and antimicrobial formulations. Hospitals specify flushable seat covers and high wet-strength wipes, tapping into the broader infection-prevention mandate. Hotels and restaurants, collectively known as HoReCa, are integrating FSC-certified towels and napkins to match brand sustainability narratives, while large transportation hubs push for jumbo-roll systems to curb replenishment labor.

Institutional customers increasingly bundle tissue with soap and sanitizer under integrated hygiene contracts, raising the strategic importance of cross-category capabilities. Vendors able to furnish ESG reporting on carbon, water, and labor score higher in tender evaluations, further professionalizing the channel.

By Distribution Channel: Offline Weight, Online Velocity

Brick-and-mortar outlets still deliver 50.68% of tissue paper market share in 2025 owing to instant-need purchases and private-label shelf dominance. Grocery chains leverage loyalty programs to drive multipack promotions, especially in the run-up to public holidays when pantry stocking peaks. The digital channel, growing at 6.84% CAGR, introduces subscription replenishment and bulk-shipped cartons that smooth warehouse throughput for producers. E-commerce also shortens feedback loops: manufacturers glean real-time reviews that guide emboss pattern tweaks or sheet-count optimization. In markets with advanced last-mile infrastructure, quick-commerce portals promise 30-minute delivery, nudging incremental volumes for premium facial tissue.

Retailers wield growing influence by aligning online and offline assortments around sustainability icons. Carbon-neutral badges and recycled-content disclosures become searchable filters on webstores, channeling traffic toward brands that can document verifiable impact reductions. For mills, flawless OTIF (on-time-in-full) performance and data-rich digital assets (3-D pack renders, QR-linked traceability) are fast becoming table stakes to secure banner placement.

Geography Analysis

North America contributes 37.95% of global revenue, reflecting high per-capita usage and consolidation benefits among integrated players. Recent headline investments, such as Kimberly-Clark’s USD 2 billion expansion and Georgia-Pacific’s fully automated Green Bay line, signal a renewed commitment to domestic capacity that tempers import reliance. The region’s institutional segment should regain pre-pandemic throughput by 2026 as federal and private employers ratchet up office attendance targets. Through-air-dried towel grades continue to outperform, capturing share from two-ply kitchen rolls as consumers equate a cloth-like feel with superior absorbency and hygiene.

Asia-Pacific delivers the steepest growth, clocking an 7.66% CAGR toward 2031. India aims to consume 30 million tons of paper by March 2027 on the back of e-commerce packaging and FMCG expansion. Chinese converters chase efficiency gains through 70% digitalization targets by 2025, with intelligent process controls trimming waste in sheet caliper and basis-weight variation. Investments in hardwood pulp capacity across Latin America disproportionately favor Asian buyers, cementing intercontinental supply linkages. Rising urban disposable incomes propel premium bathroom and facial grades, while rural programs offer vouchers for basic hygiene products, broadening the consumption base.

Europe faces a twin challenge: stringent environmental statutes and stagnant demographic growth. PPWR and EUDR compliance compels mills to overhaul traceability systems and recycle streams. Companies with vertically integrated forestry assets gain structural advantage, whereas mid-size converters must forge closer ties with certified plantation partners. Still, away-from-home recovery across tourism-heavy southern economies should revive towel and napkin demand. Latin America, meanwhile, leverages cost-competitive eucalyptus plantations to solidify its role as the world’s net pulp supplier, exporting surplus to North America and Asia.

In the Middle East and Africa, currency volatility and lower disposable incomes temper uptake, yet national drives, such as Kenya’s circular-economy initiatives that recycle 22 million trees’ worth of waste paper, create localized momentum. Premium hotel construction in Gulf states opens niche demand for luxury bathroom rolls embroidered with gold-leaf branding, illustrating the region’s bifurcated consumption profile.

Competitive Landscape

The tissue paper market is moderately fragmented, with merger activity redefining the top tier. The USD 3.4 billion Suzano-Kimberly-Clark joint venture amalgamates upstream pulp self-sufficiency with downstream brand equity, producing 1 million tons annually across 70 countries. Sofidel’s USD 1.06 billion pickup of Clearwater elevates it to fourth place in North America, illustrating how European players seek geographic diversification. Equipment investments tilt toward TAD and NeXFormer shoe-press technologies that boost bulk and absorbency while curbing energy intensity. Producers also court carbon-savvy customers by converting spent pulping liquor into biomethanol, usable as mill fuel or chemical feedstock.

Private-label partnerships are accelerating. Retail chains negotiate exclusivity on three-ply recycled variants, capturing higher margins and customer stickiness. Branded incumbents counter with differentiated fragrances, post-consumer recycled fiber thresholds above 80%, and subscription bundles bundled with digital water-tracking apps. Patent filings concentrate on micro-emboss geometries that enhance perceived softness at constant basis weight, reducing pulp consumption without compromising touch. Mills that meet SBTi-validated emissions trajectories tout the certification in RFP submissions, converting decarbonization into a pricing premium.

Tissue Paper Industry Leaders

Kimberly-Clark Corporation

Georgia Pacific LLC

Kruger Products L.P.

Procter & Gamble Company

Metsä Tissue Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Suzano and Kimberly-Clark unveiled a USD 3.4 billion joint venture comprising 22 plants and 1 million tons capacity, slated to close mid-2026.

- May 2025: Kimberly-Clark committed over USD 2 billion to U.S. expansions, including a new Warren, Ohio facility creating 900 jobs, with ground-breaking in May 2025.

- April 2025: Kimberly-Clark’s USD 4 billion international tissue unit drew bids from Asia Pulp & Paper, Royal Golden Eagle, and Suzano, with offers due mid-May.

- February 2025: First Quality Tissue selected Defiance, Ohio for two new TAD machines, first to come online by early 2028.

Global Tissue Paper Market Report Scope

Tissue paper is a lightweight paper product typically made from recycled paper pulp. It is commonly used for wrapping, packaging, cleaning, and as a disposable hygienic product. The demand for tissue paper is driven by several factors, such as population growth, urbanization, improved living standards, health and hygiene awareness, and e-commerce growth, among others. These factors collectively contribute to the consistent and growing demand for tissue paper globally.

The study aims to analyze and understand the tissue paper market's current growth, opportunities, and challenges. The scope of market analysis is segmented by raw material (bleached softwood kraft pulp (BSK), birch hardwood kraft pulp (BHK), high yield pulp (HYP) and other raw materials), product type (bathroom tissue, paper napkins, paper towels, facial tissues, specialty and wrapping tissue), type (at home and away from home) and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Bleached Softwood Kraft Pulp (BSK) |

| Birch Hardwood Kraft Pulp (BHK) |

| High-Yield Pulp (HYP) |

| Recycled Fibre Pulp |

| Other Raw Materials |

| Bathroom Tissue |

| Paper Towels |

| Facial Tissues |

| Paper Napkins |

| Specialty and Wrapping Tissue |

| Residential |

| HoReCa (Hotels/Restaurants/Cafés) |

| Healthcare Facilities |

| Offices and Educational Institutions |

| Other End-User Industries |

| Online Sales |

| Offline Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Raw Material | Bleached Softwood Kraft Pulp (BSK) | ||

| Birch Hardwood Kraft Pulp (BHK) | |||

| High-Yield Pulp (HYP) | |||

| Recycled Fibre Pulp | |||

| Other Raw Materials | |||

| By Product Type | Bathroom Tissue | ||

| Paper Towels | |||

| Facial Tissues | |||

| Paper Napkins | |||

| Specialty and Wrapping Tissue | |||

| By End-User Industry | Residential | ||

| HoReCa (Hotels/Restaurants/Cafés) | |||

| Healthcare Facilities | |||

| Offices and Educational Institutions | |||

| Other End-User Industries | |||

| By Distribution Channel | Online Sales | ||

| Offline Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the tissue paper market in 2026?

The tissue paper market is valued at USD 23.2 billion in 2026, with a projected rise to USD 30.01 billion by 2031.

How fast is Asia-Pacific demand for tissue products growing?

Asia-Pacific demand is set to increase at an 7.66% CAGR through 2031, making it the fastest-expanding region.

Which raw material dominates tissue manufacturing today?

Bleached Softwood Kraft Pulp leads with a 46.98% share, though recycled fiber is gaining quickly.

Why are paper towels outpacing other product categories?

Higher hygiene standards in offices, restaurants, and homes are propelling paper towels at a 6.73% CAGR through 2031.

How are new regulations affecting tissue producers?

Rules such as the EU Deforestation Regulation require geolocation tracing of wood inputs and can levy fines of at least 4% of EU revenue for non-compliance, incentivizing supply-chain transparency.

What technologies are mills adopting to stay competitive?

Producers are investing in through-air-dried lines and biomass-based energy systems, which improve product softness while cutting labor and carbon intensity.

Page last updated on: