Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

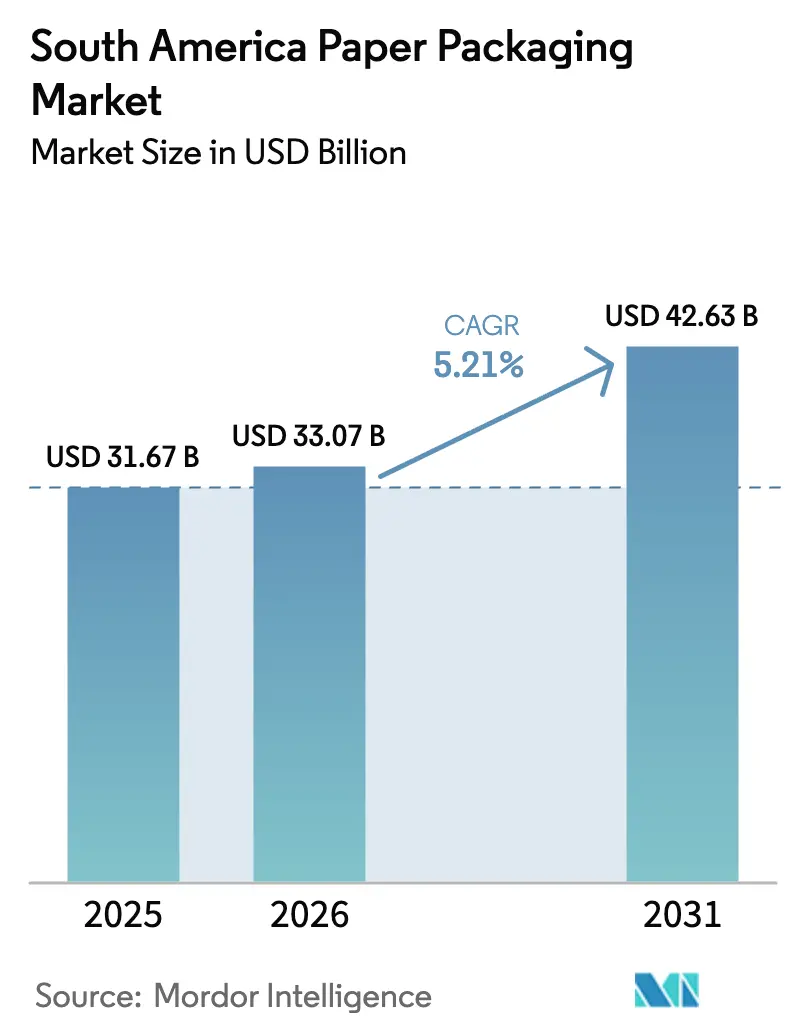

| Base Year Market Size (2025) | USD 31.67 Billion |

| Market Size (2026) | USD 33.07 Billion |

| Market Size (2031) | USD 42.63 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

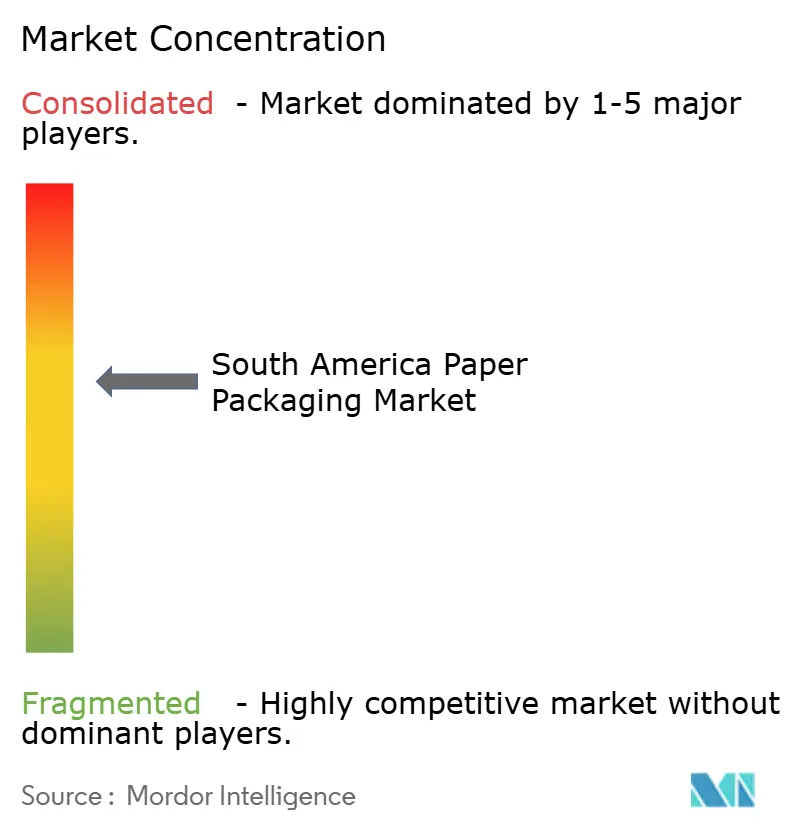

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Paper Packaging Market Analysis by Mordor Intelligence

The South America paper packaging market size is expected to increase from USD 31.67 billion in 2025 to USD 33.07 billion in 2026 and reach USD 42.63 billion by 2031, growing at a CAGR of 5.21% over 2026-2031. The growth outlook rests on regulatory bills that penalize plastics, sizable pulp resources that secure fiber supply, and e-commerce expansion that intensifies demand for corrugated boxes. Brand owners are accelerating lightweighting and high-graphics printing to cut freight emissions and lift shelf impact, while real-time mill automation is containing energy costs and stabilizing margins. Rising cold-chain logistics for pharmaceuticals and perishables is spurring insulated corrugated formats, and consumer readiness to pay a modest premium for sustainable packs is tilting share toward molded pulp and barrier-coated specialty papers.

Key Report Takeaways

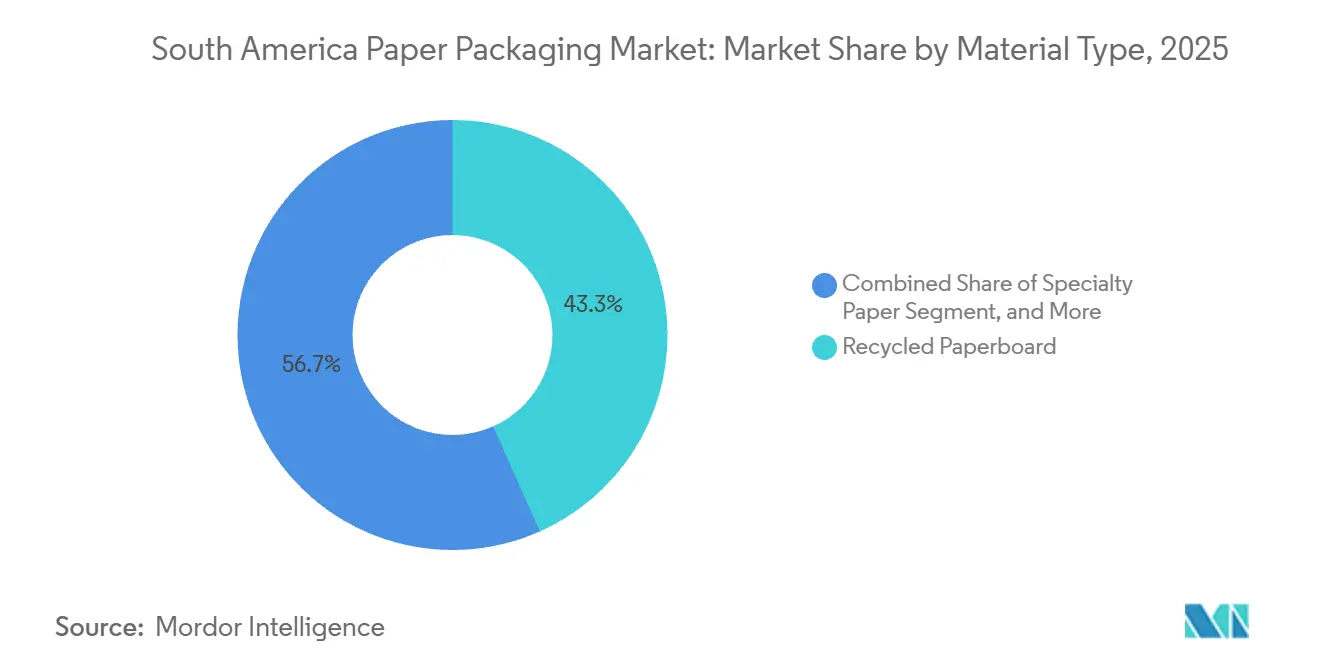

- By material type, recycled paperboard led with 43.34% of the South America paper packaging market share in 2025, whereas specialty paper is projected to advance at a 6.23% CAGR through 2031.

- By product type, rigid paper packaging held 56.32% of the South America paper packaging market share in 2025, while flexible formats are forecast to expand at a 6.35% CAGR to 2031.

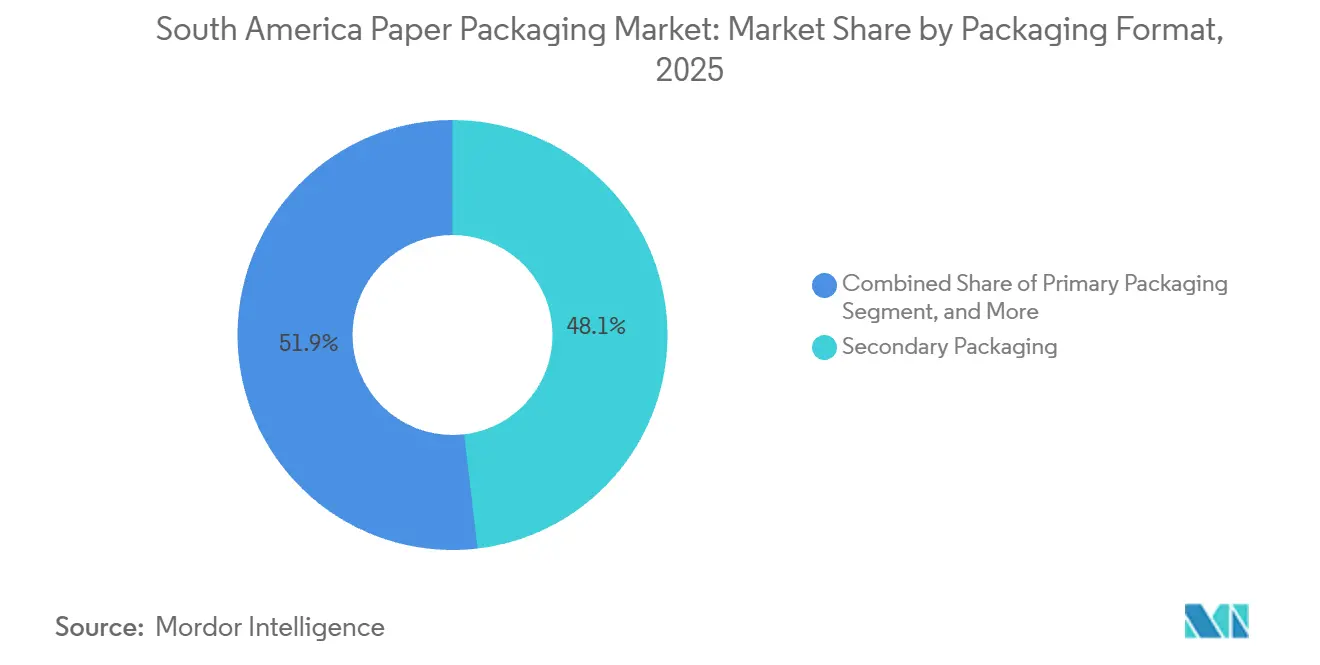

- By packaging format, secondary packaging commanded 48.14% of the South America paper packaging market size in 2025, yet primary packaging is the fastest riser at a 6.61% CAGR across 2026-2031.

- By end-use industry, food applications accounted for 30.32% of market share in 2025; personal care and cosmetics are set to grow the quickest, registering a 7.12% CAGR to 2031.

- By country, Brazil contributed 45.25% of market share in 2025, whereas Argentina is anticipated to post the fastest national rate at a 7.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Led Corrugated Demand | +1.4% | Brazil, Argentina, Colombia; concentrated in São Paulo, Buenos Aires, Bogotá metro areas | Medium term (2-4 years) |

| Mainstream Sustainability-driven Substitution of Plastics | +1.2% | Brazil (Decree 12,688), Colombia (CONPES 4129), Argentina (provincial bans); spillover to Chile, Peru | Long term (≥ 4 years) |

| Food and Beverage Demand Surge | +0.9% | Brazil (agribusiness exports), Argentina (wine, beef), Colombia (coffee, flowers) | Short term (≤ 2 years) |

| Rise in Premium Packaging for Cosmetics | +0.7% | Brazil (4th largest beauty market), Argentina (urban luxury segments), Colombia (emerging middle class) | Medium term (2-4 years) |

| Lightweighting and High-graphics Printing Gains | +0.5% | Brazil (digital press adoption), Argentina (brand differentiation), regional converters | Medium term (2-4 years) |

| Expansion of Cold-chain Logistics | +0.4% | Brazil (USD 2.67 billion cold-chain market), Argentina (pharmaceutical exports), Colombia (flower exports) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Led Corrugated Demand

Online retail penetration in Brazil reached 14.3% of total commerce in 2025, boosting parcel volumes for Mercado Libre and Amazon, which shipped more than 1.2 billion orders and overwhelmingly chose corrugated boxes for secondary protection.[1]Klabin Investor Relations, “Investment Program and Capacity Expansion,” KLABIN.COM.BR Converters are answering with thinner E- and F-flute grades that trim fiber use by up to 20% while maintaining edge-crush strength. Argentina echoes the pattern as subscription coffee and pet-food brands migrate to stand-up paper pouches that nest in outer corrugated shells, shrinking logistics costs and reducing return damage. In Colombia, commerce sales data show online volumes doubling toward 2030, prompting Bogotá and Medellín hubs to specify recyclable cartonboard for fulfillment, an avenue that supports domestic mills running at high utilization. Together, these trends add structural tonnage despite the simultaneous push to lightweight.

Mainstream Sustainability-Driven Substitution of Plastics

Brazil’s Presidential Decree 12,688, enacted in 2025, created a recovery obligation of 32% for plastic packaging but explicitly excluded mixed paper and cardboard, thereby erasing compliance costs for fiber-based boxes and wraps. Colombia’s CONPES 4129 earmarked USD 1.95 billion for circular-economy outlays to subsidize agro-pack converters installing capacity for recycled board. Argentina’s provincial bans on single-use plastics accelerated quick-service chains toward paper clamshells, pushing domestic carton plants to add 18% to their folding capacity in 2025. Consumer sentiment reinforces the pivot, 68% of Brazilian beauty shoppers accept a 10-15% premium for paper jars, motivating Natura and O Boticário to replace 42% of rigid plastics with molded pulp in just two years.[2]ABIHPEC, “Reverse Logistics Consumer Survey 2025,” ABIHPEC.ORG.BR Although high-barrier frozen-food packs still rely on multilayer films, mono-material coated papers are closing the gap quickly as coating chemistries improve.

Food and Beverage Demand Surge

Brazil exported USD 166 billion in agribusiness goods in 2025, spurring the use of corrugated, kraft sacks, and molded-pulp trays across meat, coffee, and soy supply chains. Colombia shipped 11.2 million 60-kg coffee bags, much of it in aroma-retaining barrier paper pouches that earn premiums in Europe.[3]Colombian Coffee Federation, “Export Statistics 2025,” CAFEDCOLOMBIA.COM Argentina’s wine exporters lifted bag-in-box adoption by 22%, bolstering demand for liquid-board cartons fitted with high-barrier films. The cold-chain boom, already a USD 2.67 billion segment in Brazil, extends the same logic to refrigerated corrugated boxes with wax-free coatings that resist condensation. Retail modernization rounds out the driver, as national grocery chains prefer shelf-ready cartons that cut unpacking labor.

Rise in Premium Packaging for Cosmetics

The Brazilian beauty market recorded USD 26.9 billion in 2025, yet remains under-penetrated on a per-capita basis, making premium tiers a high-growth pocket. Brand owners shifted from polypropylene jars to molded-pulp compacts with soft-touch varnishes that meet drop-test norms at lower material cost, supported by new bagasse-pulp lines from Suzano and Klabin. Argentina’s urban luxury cluster mirrors the trajectory, moving to windowed folding cartons that slash plastic by up to 70%. Colombia’s expanding middle class prefers holographic-foil cartons that confer a premium cue without metallized plastics. Price sensitivity, however, caps acceptable retail uplifts at roughly 10%, which accelerates automation investments aimed at lowering unit cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pulp and Starch Price Volatility | -0.8% | Brazil (pulp exports), Argentina (import-dependent), Colombia (regional supply chains) | Short term (≤ 2 years) |

| Competition from Flexible Plastics | -0.6% | Brazil (food packaging), Argentina (industrial films), Colombia (agricultural wraps) | Medium term (2-4 years) |

| Energy Cost Escalation for Production | -0.4% | Brazil (hydroelectric exposure), Argentina (natural gas dependency), Colombia (coal transition) | Medium term (2-4 years) |

| Supply Chain Disruptions, Imported Chemicals | -0.3% | Regional (adhesives, barrier coatings sourced from Asia, Europe) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pulp and Starch Price Volatility

Bleached hardwood kraft pulp averaged USD 544 per ton in Q1 2025 after an 18% slide caused by new Brazilian capacity and weaker Chinese demand. While low prices help independent converters, they dent earnings at integrated giants that sell pulp externally, pressuring capital budgets for coating or AI retrofits. Argentina, which imports 38% of its pulp, missed part of the relief because hedged contracts set in 2024 locked costs at USD 680 per ton, underlining a foreign-exchange risk that distorts competitiveness. Corn-based starch, an adhesive staple, rose 14% in Brazil during 2025 on export pull, lifting corrugating medium cost by USD 0.03 per m². Colombian plants, more reliant on cassava starch, were shielded from corn spikes, yet El Niño cut cassava yield and pushed local starch up 11%. These gyrations are prompting on-site starch projects, such as Smurfit Westrock’s facility that aims to reduce third-party sourcing by 40%.

Competition from Flexible Plastics

Flexible plastics retained 68% share of Brazilian food packaging in 2025 on superior moisture and oxygen barriers. Polyethylene film traded at roughly USD 2.00 per kg, 25-30% below coated paper, challenging payback math for everyday staples. Argentine industrial film suppliers dodged provincial bans by shifting to thicker gauges marketed as reusable, highlighting regulatory loopholes that restrain paper displacement. Colombia’s growers consumed 180,000 tons of mulch film in 2025, and early trials with biodegradable paper mulch cut yields by up to 12% in humid fields, reinforcing a technical hurdle. Still, quick-service restaurants in São Paulo converted 34% of clamshell boxes from plastic to molded pulp after municipal composting rules, illustrating that where barrier needs are modest regulatory pull is decisive. Hybrid laminates, pairing thin PE with kraft, are a transitional option that meets recyclability tests while cutting plastic content 70%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Grades Anchor Volume, Specialty Papers Drive Innovation

Recycled paperboard secured 43.34% of market share in 2025, leveraging robust curbside collection and ABIHPEC’s system that reclaimed 1 million tons of cosmetics packs between 2013 and 2023. Exemption from reverse-logistics targets under Decree 12,688 removes a compliance levy that virgin board must still meet, bolstering recycled economics. Virgin board at 28% remains indispensable for food-contact applications where contaminant migration rules are strict. Kraft paper, with a 16% share, dominates cement, fertilizer, and produce sacks that need tear and wet strength. The South America paper packaging market for specialty paper is set to expand quickly, led by aqueous-coated grades posting a 6.23% CAGR, enabling mono-material coffee and snack pouches. Suzano’s oxygen-barrier innovation falls below 5 cc m²-day, matching metallized-film benchmarks and widening the adoption window. Molded-pulp volumes, at only 4% today, benefit from cost advantages in sugarcane bagasse pulp and a sustainability halo, yet capacity additions require USD 8-12 million per line, tempering the pace of share gains.

Second-generation coating lines lift capex and add USD 0.15 per m² to coated-paper cost, but converters justify the spend on high-run SKUs with 15-20% on-shelf price premiums. As brand owners sign long-term offtake contracts to meet ESG commitments, recycled and specialty mills can lock fiber supply and hedge price swings. The South America paper packaging market share for recycled board is therefore stable, while specialty segments capture incremental tonnage from plastics, maintaining a balanced material mix.

By Product Type: Rigid Formats Lead, Flexible Segments Accelerate

Rigid formats dominated with a 56.32% share in 2025 because corrugated boxes are still the default for e-commerce, industrial, and agricultural logistics. Folding cartons accounted for 38% of rigid tonnage, driven by the adoption of cosmetics and premium food. Corrugated boxes accounted for 52% and are trending toward micro-flute grades that meet automated packing targets while cutting fiber. Tubes and composite cans add niche but growing exposure in premium spirits and confectionery. Flexible products, although smaller, are expanding at a 6.35% CAGR as pouches and wraps replace rigid jars and trays; stand-up pouches alone account for 62% of flexible volume and benefit from zippers and degassing valves that enhance consumer convenience.

Wraps and bakery films help ventilate fresh-produce shipments to delay spoilage, especially in Colombia’s USD 1.6 billion flower trade. Other flexible forms, such as sachets and labels, open pharmaceutical markets where child-resistant paper blisters satisfy regulatory tests. The South America paper packaging market size related to flexible lines therefore outpaces rigid in growth terms, yet absolute tonnage still favors corrugated given South America’s export-heavy agricultural profile. Continuous lightweighting ensures rigid will not lose share precipitously even as flexible rises.

By Packaging Format: Secondary Dominates, Primary Accelerates

Secondary packaging held a 48.14% share in 2025 because palletization and unitization across retail channels rely on corrugated outers that secure transport integrity. E-commerce fulfillment centers in São Paulo and Rio are tapping Klabin’s new micro-flute machines designed for automated pack stations, though the grams per order keep falling. Tertiary loads, at 24%, serve export soy, beef, and coffee flows that accept single-trip boxes to avoid return logistics. Primary packs post a 6.61% CAGR, as paper blisters, trays, and windowed cartons catch on with shoppers who value tactile, recyclable choices. Molded-pulp clamshell uptake in Brazilian quick-service outlets rose sharply once municipal composting bylaws went live, illustrating regulation as a primary-format catalyst.

While coated paper performance is closing in on barrier plastics, frozen foods and dairy still demand multilayer films, limiting paper penetration. Nonetheless, premium chocolate bars and OTC medicines are shifting to tear-strip cartons that enhance tamper-evidence and branding, accelerating primary’s growth. The South America paper packaging market share for secondary is secure but will slowly cede points to brand-facing primary as coating breakthroughs spread.

By End-Use Industry: Food Anchors Volume, Cosmetics Leads Growth

Food remained the workhorse, accounting for 30.32% of the market share in 2025, fueled by Brazil’s USD 166 billion agribusiness export machine, which depends on corrugated shippers and kraft sacks. Coffee, meat, and fresh produce use ventilated or wax-free corrugated to meet phytosanitary rules, tying the segment tightly to global commodity cycles. Beverage packs, 18% of volume, favor aseptic cartons; Tetra Pak alone produced 12 billion units in 2025 in Brazil, serving dairy, juice, and plant-based drinks. Healthcare’s 14% share grows as cold-chain expansion requires insulated boards and molded-pulp cushioning for biologics. Industrial uses account for 12%, aligning with South America’s automotive and electronics assembly clusters.

Personal care and cosmetics are the star growth vertical with a 7.12% CAGR. Molded-pulp compacts, soft-touch cartons, and holographic foils convey luxury cues while meeting recyclability goals, winning consumer acceptance, and achieving final shelf price increases of under 10%. Mass-premium outlets in Bogotá and Lima are echoing the upscale trend. Consequently, the South America paper packaging market size in cosmetics, while smaller, adds high-margin square meters that offset commodity pressure elsewhere.

Geography Analysis

Brazil contributed 45.25% of market share in 2025, thanks to integrated plantations, pulp mills, and converting assets that cut freight and currency risk. Klabin’s BRL 30 billion (USD 6 billion) outlay on corrugated and coated-paper lines came online in October 2025, boosting annual box capacity by 1.2 million tons and directly serving São Paulo’s fulfillment corridor. Suzano’s AI-enabled Ribas do Rio Pardo mill trimmed steam and power use by 8%, buffering profits when average South America pulp prices slipped to USD 544 per ton in Q1 2025. Brazil’s cold-chain logistics spend stood at USD 2.67 billion in 2025, underscoring the need for wax-free insulated corrugated. The plastic-recovery rules of Decree 12,688 give paper packs a regulatory dividend, keeping fiber formats cost-advantaged versus compliant plastics.

Argentina, while smaller, posts the quickest expansion at 7.03% CAGR through 2031. Pouch formats in food and beverage hit USD 910 million in 2025 and remain on a sturdy trajectory as direct-to-consumer channels scale. Provincial single-use bans in Buenos Aires and Córdoba prompted foodservice chains to pivot to carton clamshells, triggering an 18% rise in local folding-carton capacity that same year. Wine exports shifting to bag-in-box lifted liquid-board demand 22%. Currency-linked pulp import costs, however, compress converter margins when hedges mis-time spot moves, underscoring macro sensitivity.

Colombia captured significant market share in 2025, its coffee and flower exports relying on barrier pouches and ventilated wraps that guard shelf life. The CONPES 4129 program, capitalized at USD 1.95 billion, lowers financing for recycled-board expansion, signaling government commitment to circularity. Bogotá freight corridors anticipate e-commerce share doubling by 2030, feeding demand for fine-flute corrugated. Rest-of-region players Chile, Peru, Ecuador account for 8% of tonnage, with Chile’s USD 5.2 billion salmon exports depending on wax-coated corrugated that can tolerate ice slurry during ocean freight.

Competitive Landscape

The market shows moderate concentration. Klabin’s scale push enhanced box output and enabled in-house specialty coating, unlocking mono-material pouch applications, while Suzano’s real-time AI suite elevated mill uptime by 3 percentage points amid volatile pulp prices. Smurfit Westrock’s USD 168 million Brazilian expansion adds two micro-flute lines plus on-site starch hubs, a vertical play that hedges adhesive volatility and speeds delivery to São Paulo DCs.

Outside commodity grades, fragmentation is notable. Specialty and molded-pulp niches host agile entrants leveraging sugarcane bagasse or cassava starch feedstocks. Bio-Pap launched molded-pulp produce trays in 2024, targeting organic grocers seeking compostable alternatives. Packem’s ventilated corrugated for fresh flowers lengthens shelf life by two days, winning trials with Colombian exporters. Equipment vendors such as Valmet and Andritz observe that 40% of converters still run manual set-ups, opening retrofit opportunities that couple vision systems with AI to reduce waste by double digits.

Global majors with advanced barrier know-how, including Mondi, record limited South America revenue, creating white space for local firms to license or replicate high-barrier, heat-sealable paper substrates. Tetra Pak continues to enjoy quasi-monopoly economics in aseptic cartons, insulated by expensive filling lines that discourage switching. The strategic chessboard therefore shows integrated giants scaling and automating, specialty upstarts exploiting feedstock niches, and technology gaps where partnerships or licensing could unlock new value pools.

South America Paper Packaging Industry Leaders

International Paper Company

Klabin SA

Suzano S.A.

Mondi PLC

Smurfit Westrock

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Brazil launched the Inteligência de Embalagem 5.0 platform, with Suzano’s Ribas do Rio Pardo mill reporting an 8% energy saving after implementation.

- October 2025: Klabin completed its BRL 30 billion (USD 6 billion) multiyear investment, adding 1.2 million tons of corrugated capacity and new barrier-coating lines.

- July 2025: Smurfit Westrock committed BRL 840 million (USD 168 million) to two micro-flute corrugators and in-house starch at its Brazilian cluster.

- June 2025: Suzano posted record 14.2 million-ton sales, a 15% jump, as operational efficiencies cut cash cost to BRL 817 (USD 163) per ton.

South America Paper Packaging Market Report Scope

The South America Paper Packaging Industry encompasses the production and utilization of paper-based packaging solutions across various sectors. It includes a wide range of materials, product types, and packaging formats tailored to meet the needs of industries such as food, beverage, healthcare, personal care, and industrial applications.

The South America Paper Packaging Market Report is Segmented by Material Type (Virgin Paperboard, Recycled Paperboard, Kraft Paper, Specialty Paper, and Molded Pulp), Product Type (Flexible Paper Packaging, and Rigid Paper Packaging), Packaging Format (Primary Packaging, Secondary Packaging, and Tertiary or Transit Packaging), End-Use Industry (Food, Beverage, Healthcare and Pharmaceuticals, Personal Care and Cosmetics, Industrial, and Other End-Use Industries), and Country (Brazil, Argentina, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Virgin Paperboard |

| Recycled Paperboard |

| Kraft Paper |

| Specialty Paper |

| Molded Pulp |

By Product Type

| Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | |

| Other Flexible Paper Packaging | |

| Rigid Paper Packaging | Folding Carton |

| Corrugated Boxes | |

| Other Rigid Paper Packaging |

By Packaging Format

| Primary Packaging |

| Secondary Packaging |

| Tertiary / Transit Packaging |

By End-Use Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial |

| Other End-Use Industries |

By Country

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By Material Type | Virgin Paperboard | |

| Recycled Paperboard | ||

| Kraft Paper | ||

| Specialty Paper | ||

| Molded Pulp | ||

| By Product Type | Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | ||

| Other Flexible Paper Packaging | ||

| Rigid Paper Packaging | Folding Carton | |

| Corrugated Boxes | ||

| Other Rigid Paper Packaging | ||

| By Packaging Format | Primary Packaging | |

| Secondary Packaging | ||

| Tertiary / Transit Packaging | ||

| By End-Use Industry | Food | |

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Industrial | ||

| Other End-Use Industries | ||

| By Country | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the South America paper packaging market by 2031?

The market is forecast to reach USD 42.63 billion by 2031, expanding at a 5.21% CAGR from 2026.

Which material segment is expected to grow the fastest through 2031?

Specialty paper, powered by barrier-coated grades for mono-material pouches, is projected to register a 6.23% CAGR.

Why is Argentina the fastest-growing national market in the region?

Provincial plastic bans and a booming pouch segment in food and beverage are propelling Argentina at a 7.03% CAGR to 2031.

How are brand owners in Brazil’s cosmetics sector shifting packaging formats?

Premium brands are replacing rigid plastic jars with molded-pulp compacts and high-graphics folding cartons to meet consumer sustainability preferences.

What role does e-commerce play in corrugated demand?

Rising online retail, especially in Brazil, is driving micro-flute corrugated boxes that lower weight yet maintain protection for last-mile delivery.

Which restraint poses the biggest near-term threat to converters?

Pulp and starch price volatility can squeeze margins, prompting moves toward vertical integration and on-site adhesive production.

Page last updated on: