Market Overview

| Study Period | 2020 - 2031 |

|---|---|

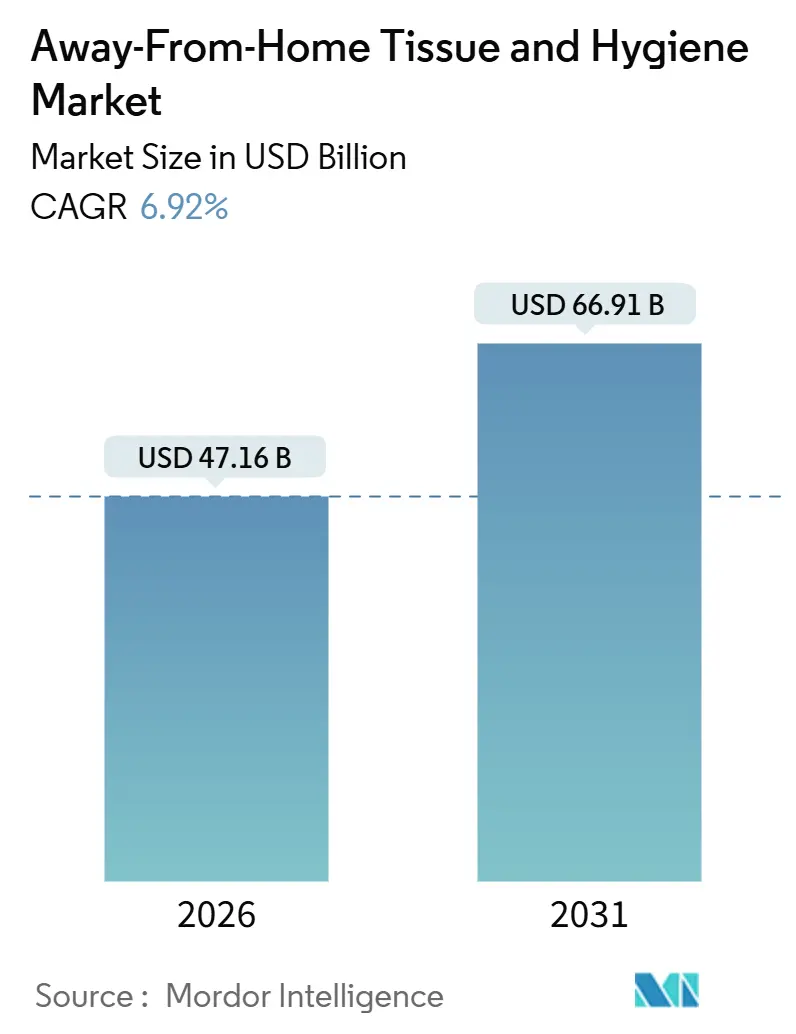

| Market Size (2026) | USD 47.16 Billion |

| Market Size (2031) | USD 65.91 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

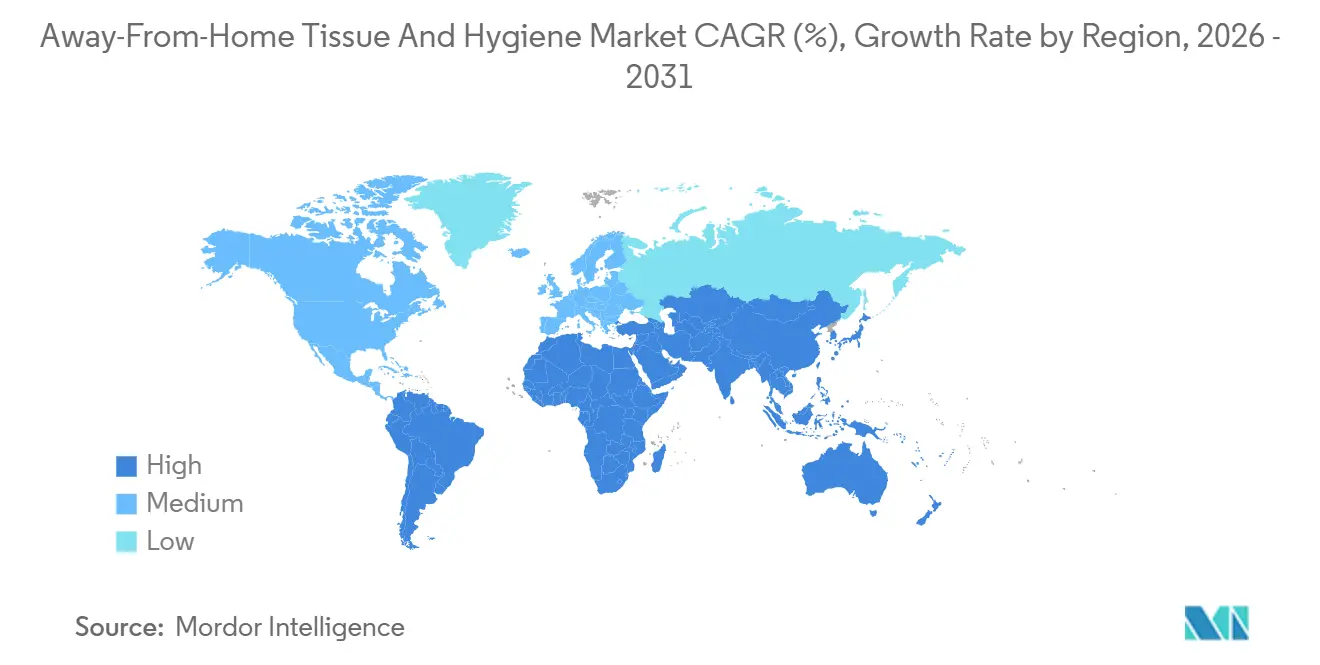

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Away-From-Home Tissue And Hygiene Market Analysis by Mordor Intelligence

The Away-From-Home Tissue and Hygiene market size stands at USD 47.16 billion in 2026 and is forecast to reach USD 65.91 billion by 2031, advancing at a 6.92% CAGR. This growth rests on durable institutional hygiene budgets, expanding hospitality construction, and rising adoption of smart dispensing systems. Regulatory mandates that compel continuous hand-hygiene supplies have converted what was once discretionary spending into a fixed operating line, while vertical integration by pulp producers is reshaping cost curves and bargaining power. In addition, sustainability criteria embedded in public-sector tenders are lifting demand for recycled-content tissue, even as premium-grade virgin products dominate guest-facing applications. Competitive dynamics now hinge on controlling fiber inputs, automating service intervals, and meeting ESG traceability targets, all of which help large integrated suppliers widen their lead over mid-tier converters.

Key Report Takeaways

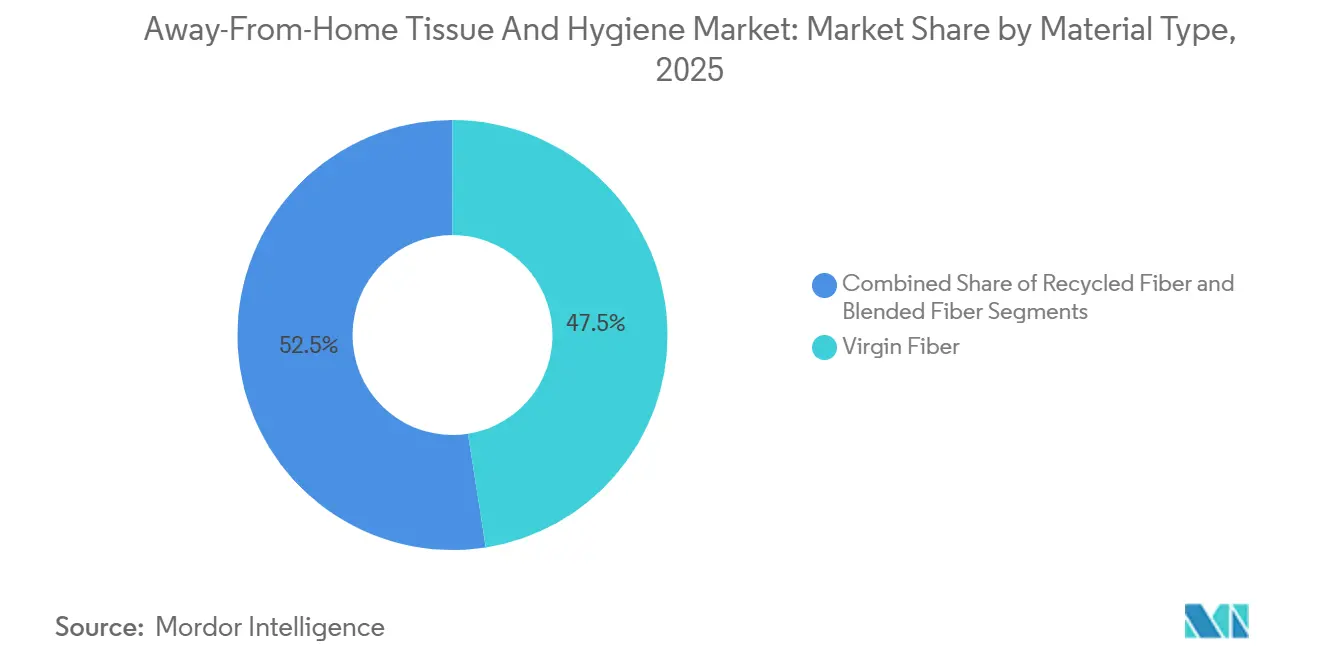

- By material type, virgin fiber led with 47.53% of the Away-From-Home Tissue and Hygiene market share in 2025, while recycled fiber is projected to expand at 7.67% CAGR through 2031.

- By ply and quality, 2-ply products captured 56.31% revenue in 2025, whereas luxury grade tissue is forecast to grow at 7.82% CAGR to 2031.

- By product type, paper towels accounted for 32.10% of the Away-From-Home Tissue and Hygiene market size in 2025, while wipes are advancing at 8.41% CAGR over the same period.

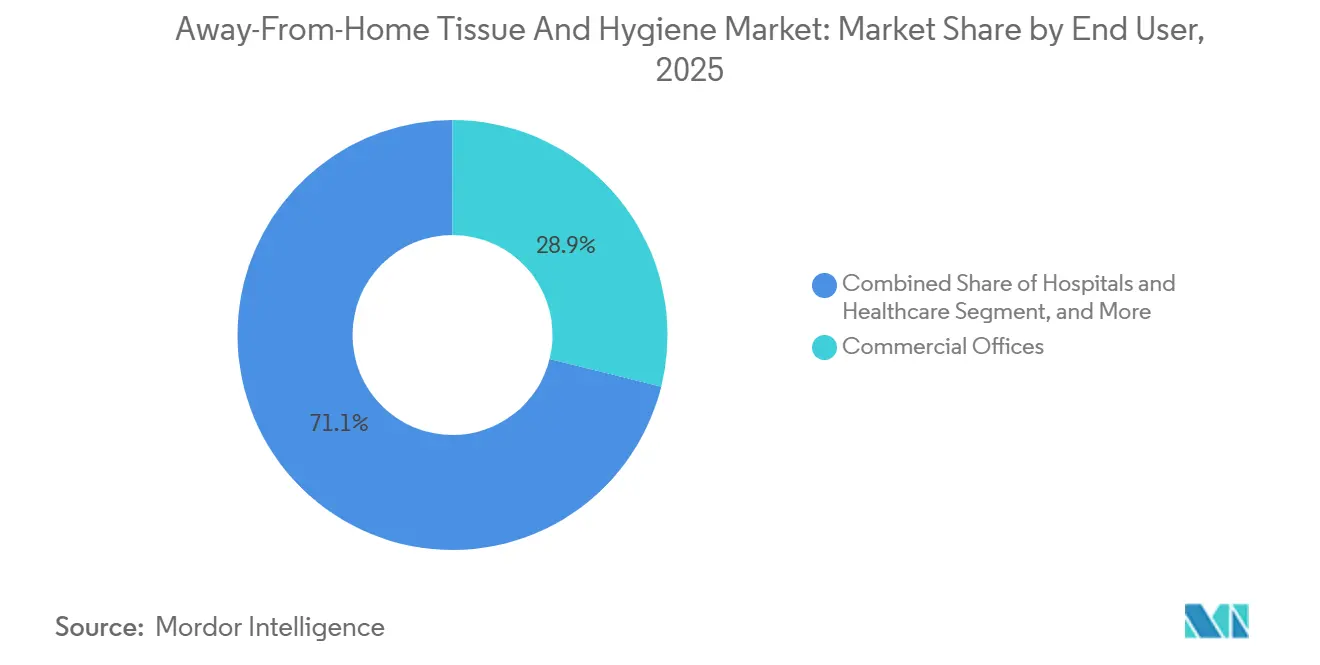

- By end user, commercial offices held 28.87% revenue in 2025, yet hospitals and healthcare facilities are expected to post the fastest 8.52% CAGR to 2031.

- By distribution channel, offline sales dominated with 82.71% in 2025, but online procurement is projected to grow at 7.12% CAGR through 2031.

- By geography, North America commanded 42.09% of the Away-From-Home Tissue and Hygiene market share in 2025, while Asia-Pacific is anticipated to expand at 8.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Away-From-Home Tissue And Hygiene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Recycled Products | +1.2% | Global, strongest in EU and North America public procurement | Medium term (2-4 years) |

| Increased Spending on Hygiene | +1.5% | Global, especially Asia-Pacific urban centers and North America healthcare | Short term (≤ 2 years) |

| Rapid Growth in Hospitality Sector Post-Pandemic | +1.0% | Global, led by Asia-Pacific and Middle East tourism hubs | Short term (≤ 2 years) |

| Government Regulations on Public Sanitation | +0.9% | North America, EU, selected Asia-Pacific markets | Long term (≥ 4 years) |

| Novel Antimicrobial Tissue Coatings Driving Premium AFH Demand | +0.7% | North America and EU healthcare, emerging in Asia-Pacific hospitals | Medium term (2-4 years) |

| Adoption of Smart Dispensers Enabling Consumption Analytics | +0.6% | North America and EU commercial offices, pilot projects in Asia-Pacific | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

Increasing Demand for Recycled Products

Public procurement mandates now specify minimum post-consumer recycled content, lifting baseline demand for recycled-fiber tissue even during budget squeezes.[1]U.S. Environmental Protection Agency, “Comprehensive Procurement Guidelines for Paper and Paper Products,” epa.gov Standardized tender language from the EU Joint Research Centre further cuts transaction costs for buyers and accelerates adoption across municipalities. Performance trade-offs persist, lower tensile strength and absorbency can raise per-use consumption, but advances in blended fibers are steadily narrowing the gap. Suppliers that fuse recycled content with acceptable softness and strength are therefore able to command modest premiums in the expanding green-procurement channel.

Increased Spending on Hygiene

Facility managers have converted pandemic-era sanitation measures into permanent operating procedures, locking in elevated tissue, wipe, and towel consumption.[2]National Restaurant Association, “State of the Industry 2025 Report,” restaurant.org WHO guidelines that frame hand-hygiene supplies as essential infrastructure further reduce demand elasticity, shielding budgets from economic swings. Healthcare operators fuel incremental spend by adopting antimicrobial wipes with validated residual efficacy, while smart dispensers that track usage help justify premium pricing by cutting waste.

Rapid Growth in Hospitality Sector Post-Pandemic

Hotels and resorts are differentiating guest experience through tactile amenities, propelling demand for luxury-grade tissue made with virgin fiber. Restaurant operators continue rolling out touchless fixtures to reassure patrons, which increases demand for compatible dispensers and single-use consumables that fit automated systems. Tiered product portfolios let suppliers match premium tissue to guest areas while using value SKUs in back-of-house locations, maximizing revenue per property without undermining operator cost control.

Government Regulations on Public Sanitation

Legally binding codes, such as the FDA Food Code requirement for single-use towels at every food-service sink, convert hygiene consumables from discretionary to mandatory purchases. WHO sanitation recommendations calling for reliable toilet paper and waste systems in public facilities reinforce this obligation worldwide. At the same time, ISO 20400 guidance embeds environmental criteria into tenders, forcing suppliers to document certified fiber sourcing and lifecycle impacts to remain eligible.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Trend of Electronic Hand Dryers | -0.8% | North America and EU municipal facilities | Medium term (2-4 years) |

| Volatility in Pulp Prices | -1.1% | Global, acute in North America and EU | Short term (≤ 2 years) |

| ESG Pressure Reducing Single-Use Product Procurement | -0.5% | EU and North America corporate buyers | Long term (≥ 4 years) |

| Supply Chain Disruptions of Specialty Fibers | -0.4% | Regions dependent on imported pulp | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Trend of Electronic Hand Dryers

Municipal facilities increasingly install high-speed hand dryers to erase recurring towel purchases and waste-hauling fees, eroding paper-towel volumes in public restrooms.[3]City of Portland, “Hand Dryers Instead of Paper Towels,” portland.gov Yet hygiene studies continue to show higher pathogen dispersion from dryers than from single-use towels, limiting adoption in healthcare and food-service venues where infection-control stakes are highest. Tissue suppliers counter by emphasizing the lower contamination risk of disposable towels and by launching touchless dispensers that slash consumption, shrinking the cost gap with dryers.

Volatility in Pulp Prices

Sharp pulp price swings compress converter margins and destabilize multi-year contracts, making vertical integration a strategic necessity. The Producer Price Index for toilet and facial tissues illustrates the magnitude of upstream cost volatility faced by converters.[4]Federal Reserve Bank of St. Louis, “WPU091207: Producer Price Index by Commodity: Toilet and Facial Tissues,” stlouisfed.org Suzano’s USD 3.4 billion acquisition of Kimberly-Clark’s international tissue unit typifies the pivot toward captive fiber, enabling integrated players to shelter earnings while non-integrated rivals struggle to pass costs through. Independent converters respond with hedging and product-mix adjustments, but prolonged volatility continues to accelerate market consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Fiber Ascends on Policy Tailwinds

Recycled fiber tissue captured only a minority share in 2025, yet it is forecast to deliver a 7.67% CAGR through 2031, the fastest among materials. Public agencies in North America and the EU cannot award contracts unless post-consumer recycled thresholds are met, which anchors demand regardless of economic cycles. Nevertheless, virgin fiber retained 47.53% share in 2025 because hospitality and healthcare buyers value its softness, brightness, and tensile strength. Private operators that prize guest perception continue to specify virgin grades even when recycled options are available at lower cost.

Blended fiber is emerging as the pragmatic bridge between performance and sustainability. Manufacturers now incorporate strategic proportions of recycled pulp to satisfy tender requirements while keeping tactile qualities close to virgin benchmarks. This approach helps suppliers participate in compliance-driven contracts without alienating users who equate softness with cleanliness. As process refinements raise wet-strength and bulk, blended formulations are expected to erode virgin fiber’s lead in non-premium institutional settings. The Away-From-Home Tissue and Hygiene market continues to reward mills that can toggle seamlessly between fiber inputs as policy, pricing, and customer preferences evolve.

By Ply and Quality: Premiumization Drives Luxury-Grade Upswing

Two-ply tissue held 56.31% of sales in 2025 by balancing cost, absorbency, and dispenser compatibility across high-traffic facilities. However, luxury-grade tissue is projected to climb at 7.82% CAGR through 2031 as hotels, lounges, and executive offices use premium softness to signal elevated service standards. Investments in through-air-dried (TAD) machines are lowering unit costs of three-ply and structured sheets, making premium options more accessible to midscale properties.

In contrast, one-ply remains prevalent in transportation hubs and public-sector restrooms where procurement focuses on minimizing spend. Three-ply serves niche prestige applications but benefits from expanding premium hospitality footprints in Asia-Pacific. Suppliers segment portfolios accordingly, steering luxury lines toward guest-facing areas while maintaining two-ply for back-of-house. This stratification lets operators optimize both experience and budget, and it helps brands deepen account penetration across a single property by matching tissue quality to location purpose.

By Product Type: Wipes Accelerate on Infection-Control Needs

Paper towels retained the top product slot with 32.10% of 2025 revenue, yet wipes are forecast for an 8.41% CAGR to 2031, outpacing all other categories. Healthcare facilities increasingly prefer pre-moistened disinfectant wipes that combine cleaning and antimicrobial action, enabling staff to meet strict turnover times while reducing cross-contamination risk. Regulatory guidance requiring scientifically validated efficacy claims further elevates barriers to entry and supports premium pricing for compliant offerings.

Toilet paper and napkins continue to fulfill universal baseline demand, but growth remains tied to venue expansions rather than rising per-capita usage. Incontinence products occupy a specialized space within long-term care, expanding in tandem with aging demographics but contributing modest overall revenue. Specialty items, including seat covers and facial tissues, add incremental value in high-traffic venues. The Away-From-Home Tissue and Hygiene market advantage shifts toward suppliers that document kill-time, residual efficacy, and substrate compatibility, especially as hospitals tighten product formularies to standardize outcomes.

By End User: Healthcare Surges Under Tightened Scrutiny

Commercial offices led spending with 28.87% of 2025 demand, yet hospitals and healthcare institutions are projected to deliver an 8.52% CAGR, the fastest among end users. Stringent infection-control protocols mandate single-use wipes and high-grade toweling, buffering healthcare demand from cyclical downturns. Standardized national procurement frameworks, such as the United Kingdom’s centralized contracts, reward suppliers that provide audited traceability, stable logistics, and product validation data.

Food-service operators form a stable core segment anchored by statutory hand-hygiene codes, but margin sensitivity caps premium uptake outside upscale dining. Transportation hubs purchase in high volume but favor commodity grades to manage cost per passenger. Education facilities struggle with budget constraints, adopting recycled-content tissues when municipal sustainability policies dictate but rarely trading up to luxury products. Suppliers able to demonstrate clinical efficacy credentials remain best positioned to capture healthcare spending momentum, which should offset slower growth in office-tower demand as hybrid work normalizes.

By Distribution Channel: Digital Platforms Capture Incremental Share

Offline distributors accounted for 82.71% of 2025 sales because they bundle stock-management services, dispenser maintenance, and immediate delivery, values that pure-play e-commerce cannot fully replicate. Even so, online procurement is forecast to grow at 7.12% CAGR through 2031 as multi-site corporations and public agencies consolidate orders on e-platforms to negotiate volume discounts and automate replenishment. Integration of consumption analytics into facility-management software further encourages digital adoption by tying reorder points to real-time usage.

A hybrid strategy is emerging wherein large buyers use online portals for routine orders and rely on local distributors for emergency restocks and installations. Tissue’s unfavorable value-to-weight ratio constrains direct-to-door models, but regional distribution hubs combined with digital storefronts can close that gap. The Away-From-Home Tissue and Hygiene market rewards suppliers that support APIs, real-time inventory feeds, and flexible fulfillment, allowing customers to toggle between digital convenience and on-the-ground service.

Geography Analysis

North America accounted for 42.09% of 2025 revenue, driven by stringent food-service sanitation codes, dense commercial real estate, and mature procurement systems that prize reliability over lowest price. Ongoing mill investments indicate confidence in sustained demand despite hybrid work trends that dampen urban office consumption. Energy and labor costs are rising, but vertical integration and local capacity expansions help leading producers defend margins and ensure rapid delivery times.

Europe benefits from robust sustainability frameworks that institutionalize demand for recycled and certified products. Harmonized ecolabel criteria and green-procurement guides lower administrative burdens, allowing public buyers to scale adoption quickly. However, macroeconomic softness and energy-price volatility temper growth in discretionary segments such as entertainment venues, creating a two-speed market where healthcare and government facilities expand steadily while private-sector demand oscillates with GDP.

Asia-Pacific is projected to record the highest 8.07% CAGR, propelled by rapid urbanization, burgeoning hospitality pipelines, and policy upgrades that formalize public-sanitation requirements. Local producers are installing TAD and structured-sheet equipment to compete in premium niches traditionally served by imports. Investments in India, Vietnam, and China reflect a strategic shift to localized supply that mitigates freight costs and tariff exposure. South America and the Middle East and Africa contribute smaller shares but offer selective high-growth pockets tied to tourism corridors and healthcare infrastructure upgrades.

Competitive Landscape

The competitive field is consolidating as pulp producers acquire downstream converting assets to stabilize earnings and exert greater control over the value chain. Mega-deals that integrate fiber, converting, and branded distribution compress margins for stand-alone converters and accelerate exit or merger decisions among mid-tier players. Capital-intensive investments in TAD machines, IoT-enabled dispensers, and advanced coating lines favor companies with strong balance sheets, widening the moat around global leaders.

Digital service layers have become a key differentiator. Platforms that pair tissue sales with sensor-enabled dispensers and analytics deepen customer stickiness by lowering labor costs and enabling predictive refills. ESG compliance is now a sales prerequisite rather than an optional extra, with public buyers demanding FSC certification and lifecycle carbon disclosures. Suppliers able to demonstrate chain-of-custody transparency garner preferred-vendor status and avoid costly tender exclusions.

Regional challengers pursue focused strategies, such as antimicrobial technology or private-label production, to secure niche positions. Yet sustained pulp volatility and rising compliance costs propel many toward partnerships with integrated majors. Over the forecast horizon, competitive intensity will increasingly hinge on the ability to combine scale, fiber control, digital capabilities, and ESG credentials into an integrated customer offering.

Away-From-Home Tissue And Hygiene Industry Leaders

Metsä Tissue Corporation

Sealed Air Corporation

Kimberly-Clark Corporation

Georgia-Pacific LLC

The Procter and Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Sofidel announced a further United States capacity expansion to support away-from-home channels.

- September 2025: Georgia-Pacific invested in its Alabama River Cellulose mill to reinforce upstream pulp security.

- June 2025: Kimberly-Clark divested a majority stake in its international tissue unit to Suzano for USD 3.4 billion.

- March 2025: NHS Supply Chain launched a nationwide contract for standardized paper hygiene products across U.K. healthcare facilities.

Global Away-From-Home Tissue And Hygiene Market Report Scope

The Away-From-Home Tissue and Hygiene Market Report is Segmented by Material Type (Virgin Fiber, Recycled Fiber, Blended Fiber), Ply and Quality (1-Ply, 2-Ply, 3-Ply, Luxury Grade), Product Type (Paper Napkins, Paper Towels, Wipes, Toilet Paper, Incontinence Products, Other Product Types), End User (Commercial Offices, Food and Beverage Establishments, Hospitals and Healthcare, Transportation Hubs, Education Facilities, Other End Users), Distribution Channel (Offline, Online), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Virgin Fiber |

| Recycled Fiber |

| Blended Fiber |

By Ply / Quality

| 1-Ply |

| 2-Ply |

| 3-Ply |

| Luxury Grade |

By Product Type

| Paper Napkins |

| Paper Towels |

| Wipes |

| Toilet Paper |

| Incontinence Products |

| Other Product Types |

By End User

| Commercial Offices |

| Food and Beverage Establishments |

| Hospitals and Healthcare |

| Transportation Hubs |

| Education Facilities |

| Other End Users |

By Distribution Channel

| Offline |

| Online |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Virgin Fiber | ||

| Recycled Fiber | |||

| Blended Fiber | |||

| By Ply / Quality | 1-Ply | ||

| 2-Ply | |||

| 3-Ply | |||

| Luxury Grade | |||

| By Product Type | Paper Napkins | ||

| Paper Towels | |||

| Wipes | |||

| Toilet Paper | |||

| Incontinence Products | |||

| Other Product Types | |||

| By End User | Commercial Offices | ||

| Food and Beverage Establishments | |||

| Hospitals and Healthcare | |||

| Transportation Hubs | |||

| Education Facilities | |||

| Other End Users | |||

| By Distribution Channel | Offline | ||

| Online | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Away-From-Home Tissue and Hygiene market by 2031?

The market is forecast to reach USD 65.91 billion by 2031.

Which product type is expected to grow fastest through 2031?

Wipes are projected to expand at an 8.41% CAGR, the highest among all product types.

Why is recycled-fiber tissue gaining traction in institutional procurement?

Government tenders increasingly mandate minimum recycled content, guaranteeing a demand floor for recycled-fiber grades.

How are smart dispensing systems influencing procurement decisions?

IoT-enabled dispensers provide usage analytics that reduce waste and labor, persuading facility managers to adopt premium tissue programs.

Which region demonstrates the strongest growth outlook?

Asia-Pacific is anticipated to record the fastest 8.07% CAGR, supported by rapid urbanization and hospitality expansion.

How is vertical integration affecting competition?

Pulp producers acquiring converting assets secure fiber supplies and compress margins for non-integrated converters, driving consolidation.

Page last updated on: